sources for FY , only a portion of the statedistributed revenue would be available for new capital projects.

|

|

|

- Christina Rodgers

- 5 years ago

- Views:

Transcription

1 6 REVENUE PROJECTIONS, SARASOTA/MANATEE 2040 LRTP The purpose of this analysis is to begin to document the financial resources and revenues available for consideration in developing the Financially Feasible element of the Sarasota/Manatee Metropolitan Planning Organization s (MPO s) 2040 Long Range Transportation Plan (LRTP). This technical memorandum presents a preliminary estimate of potentially available transportation revenues from federal, state, and local sources. The revenue estimates are presented in five-year Fiscal Year increments starting in FY 2016, and are expressed in year of expenditure (YOE) dollars to reflect an assumed rate of inflation. Inflation may fluctuate from year to year, but the assumptions are intended to represent an average across the long-term horizon. The projections for most revenues are adjusted for inflation according to FDOT guidelines, which assume a long term inflation factor of 3.3 percent per year in most years. Future impact fee revenue is not adjusted for inflation, as discussed later in this memo. Estimates are provided for federal and state sources, state-distributed fuel taxes, and local sources. The federal and state revenue estimates were obtained from the Florida Department of Transportation. Estimates of state-distributed fuel tax revenues and most local revenues were based on county-level population estimates prepared by the University of Florida s Bureau of Economic and Business Research (BEBR), adjusted by Renaissance Planning Group to incorporate plans and projections prepared by local governments. The rate of increase for these funding sources was assumed to be tied to population growth, so actual revenue collections from previous fiscal years, adjusted for inflation, provided the basis for future projections. The revenue collections data were obtained from the Local Government Financial Information Handbook prepared by the Legislative Committee on Intergovernmental Relations (LCIR). OVERVIEW OF PROJECTIONS The tables on the following three pages present a summary of the preliminary revenue projections for each of the evaluated revenue sources, which include federal and state programs, state-distributed fuel tax revenues, local option fuel tax revenues, local infrastructure sales surtaxes, local transit revenues, and local transportation impact fees. While the sum of each of these sources indicates a potential revenue total of about $1.8 billion from federal/state sources and $4.4 billion from state-distributed and local sources for FY , only a portion of the state-distributed and local revenue would be available for new capital projects. While the sum of each of these sources indicates a potential revenue total of about $1.8 billion from federal/state sources and $4.4 billion from statedistributed and local sources for FY , only a portion of the statedistributed and local revenue would be available for new capital projects. A6-1

2 FEDERAL/STATE REVENUE SOURCES Table 1 presents revenue projections of federal and state sources available to the MPO as provided in the 2040 Revenue Forecast Handbook (July 2013 supplement) prepared by FDOT. SIS Highways Construction/ROW represents programmed projects in the 2014 edition of the Strategic Intermodal System Funding Strategy. The Other Arterials revenues can be applied to non-sis State Highway System roadways for capacity and non-capacity programs. The Transportation Alternatives funds in the table are used for locally defined projects providing enhancements, typically for bicycle and pedestrian projects. Transit revenues may be used for technical and operating/capital assistance for transit, paratransit, and rideshare programs. TMA Funds may be used for any of the above categories. There are two other pools of revenue the State of Florida may allocate to projects located within the MPO. In addition to funds specifically dedicated to the Sarasota/Manatee MPO, the State also allocates funds from the Transportation Regional Incentive Program (TRIP) and New Starts/Small Starts for transit. TRIP funds apply to improvements on facilities designated as regionally significant, and funds are allocated within each FDOT District based on regional project prioritization processes. The State also receives federal funding for new transit programs. These New Starts/Small Starts are available to transit agencies statewide. Table 5 below summarizes these available discretionary federal and state revenue sources. The TRIP funds and New Starts/Small Starts are not included in the totals in Tables 1 through 4 due to their discretionary nature. Table 1: Sarasota/Manatee MPO Federal/State Revenue Estimates (in millions of dollars, Year of Expenditure) Revenue Source * SIS Highways Construction/ROW Manatee County SIS Highways Construction/ROW Sarasota County 25 Year Total Other Arterial Construction/ROW Transportation Alternatives TMA Funds Transit TOTAL FEDERAL/STATE ,844.0 * Includes only FY 2020 revenues; earlier years are already committed to projects A6-2

3 STATE-DISTRIBUTED FUEL TAXES There are three types of fuel taxes collected at the state level that are distributed to local governments. These taxes are not part of the local option taxes, and are collected for every gallon of fuel sold in the state. For each gallon of motor fuel sold, the Constitutional Fuel Tax yields two cents per gallon, and the County Fuel Tax yields one cent per gallon. The Municipal Fuel Tax is a one-cent per gallon tax, and each municipality may dedicate a percentage of its Municipal Revenue Sharing Program funds for certain types of transportation projects. CONSTITUTIONAL FUEL TAX Each county is eligible for revenues through an allocation formula used by the State that is based on the certified fuel gallons sold and a distribution factor calculated using the county s population, land area, and tax collected in the previous fiscal year. The actual revenue distributions by year and BEBR population estimates for those years were used to calculate per capita revenue values for each county from , and the average of those past values was used for the base year (2015) projection. Future years were projected out to 2040 using this average per capita value and adjusting for inflation. COUNTY FUEL TAX The County Fuel Tax allocation to counties is determined by the State using the same methodology as the Constitutional Fuel Tax. For this analysis, the five-year average per capita distribution and future projections were calculated in the same manner described above. MUNICIPAL FUEL TAX This tax is a one-cent per gallon tax on motor fuel sold within the state s municipalities, and is collected within the Municipal Revenue Sharing Program trust fund. Each municipality s share of the funds is calculated based on an adjusted municipal population, municipal sales tax collections, and a municipality s relative ability to raise revenue. The Municipal Fuel Tax s portion of the trust fund is determined by the Department of Revenue, and varies each year depending on tax collections. As with the Constitutional and County fuel taxes, the five-year average per capita distribution for each municipality was calculated from actual municipal distributions in each county from The expected percentage allocated to each municipality was obtained from each year s Local Government Financial Handbook. The per capita values were adjusted for inflation and multiplied by the municipal population projections prepared by Renaissance to project future tax revenues. For simplicity, the total Municipal Fuel Tax revenues projected for all of the cities in each county and the MPO planning area are shown in Tables 2 through 4. EXISTING LOCAL REVENUE SOURCES One of the means by which local governments are able to raise funds for transportation projects is through the implementation of local option fuel taxes. These taxes must be approved by the county governing body, or by voter approval in a countywide referendum. Sarasota and Manatee Counties currently use the maximum rate of local optional fuel taxes available. A6-3

4 Other existing local revenue sources include sales surtaxes for infrastructure, the locally generated revenues of the two county transit agencies, and local transportation impact fees charged to new development projects. LOCAL OPTION FUEL TAXES All Florida counties have the option to raise additional revenues by augmenting the State's taxes on highway fuels that are discussed above. Local governments are authorized to collect up to an additional 12 cents (ninth-cent fuel tax and maximum local option fuel taxes) per gallon, which may be spent on local or state transportation projects. NINTH CENT FUEL TAX This tax is collected on both regular and diesel fuel, and is used to fund transportation expenditures. Applied at a rate of one cent per gallon, the counties do not share the Ninth Cent Fuel Tax with the municipalities within their jurisdictions. The projection methodology, therefore, is similar to that used for the Constitutional Fuel Tax. SIX-CENT AND FIVE-CENT LOCAL OPTION FUEL TAXES These are two separate local fuel taxing options that are collected and distributed in the same manner. The 6-cent Fuel Tax is levied at a rate of six cents for each gallon of fuel, both regular and diesel, sold within a county. The 5-cent Fuel Tax is not applied to diesel fuel. The 6-cent tax may be used for general transportation expenditures, while the 5-cent tax may only be used for transportation expenditures needed to meet the requirements of the capital improvement element of an adopted local government comprehensive plan and other capacity-adding projects. The 5-cent tax may not be used for operating and maintenance expenditures. In Sarasota County, the collected revenues are distributed to each local government based on interlocal agreements between the County and its municipalities that are updated annually for the coming fiscal year. The distribution formula is based on the annual population estimates prepared by BEBR. According to the Local Government Financial Information Handbook, Manatee County does not distribute local option fuel tax revenues to its municipalities. Revenues were projected for each of these two fuel taxes using similar methodologies as described above. The LCIR provided actual revenue distributions from for the two counties, and BEBR population estimates for those years were used to derive annual per capita distributions. Using the population projections for the counties prepared by Renaissance, and adjusting the average per capita values for inflation, future revenue projections for each county were calculated by multiplying the two figures. Municipal distributions were calculated using the same per capita methodology and the municipal allocation percentages provided in the Local Government Financial Handbook. DISCRETIONARY SALES SURTAX Sarasota County currently imposes an additional 1.0 percent sales tax on goods and services, above the six percent standard sales tax, as a revenue stream for local government infrastructure. Fees collected may be used to finance, plan, and construct infrastructure, which includes transportation infrastructure (and now also land purchases for affordable housing). It may also be used to purchase land for public recreation, conservation, or protection of natural resources. The tax is effective until December 31, Sarasota A6-4

5 County issued revenue bonds in 2008 supported by the infrastructure surtax in the amount of $ million. Manatee County currently does not impose a discretionary surtax for infrastructure, although it has in the past. Revenue projections for the existing Sarasota County surtax were calculated based on the average of actual surtax revenues that were collected from based on figures obtained from the LCIR, plus information from County finance staff. Like the methodology for the local option fuel taxes, the collected tax receipts are normally distributed to each unit of local government in the county according to the standard allocation formula used by the Department of Revenue. However, each county has the option to set a different allocation formula with its municipalities through an interlocal agreement, which Sarasota County currently has in place that distributes part of the revenue from the existing surtax to the Sarasota County School Board. FUEL TAX AND SALES SURTAX REVENUE BONDS Sarasota County issued fuel tax revenue bonds in 2005 to raise money for transportation projects. These bonds will be paid off in 2025, and until they mature a portion of the County s 5-Cent Local Option Fuel Tax revenue will be used to pay the debt service. Sarasota County also issued revenue bonds in 2008 supported by the infrastructure sales surtax whose debt service will be paid by surtax revenues. The annual principal and interest payments starting in 2016 for all of these bonds were obtained from the County s 2013 Debt Report and County finance staff and included in the revenue estimates, which reduces the amount of revenue that will be available for other transportation uses. TRANSIT REVENUES Sarasota County Area Transit (SCAT) and Manatee County Area Transit (MCAT) are the primary public transportation providers within the MPO planning area. The two transit agencies receive both operating and capital revenues from federal, state, and local sources (Table 2 and Table 3). Local operating and capital revenue estimates were collected from the most recent Transit Development Plan (TDP) of each agency. SCAT provided estimates of operating and capital revenues through FY 2024, while MCAT provided projections through FY Projections for subsequent years were prepared using FDOT s inflation guidelines. All federal and state revenue assumptions in the TDPs, for both the capital and operating categories, were not included in the analysis, in order to reduce the likelihood of double-counting potential federal and state revenues. State and federal transit funding figures from the 2040 Revenue Forecast Handbook were used instead (see Table 5). Projections to 2040 were estimated by dividing the TDP-estimated local operating and capital revenues for each transit provider by the population of the respective counties to obtain per capita revenue values for the fiscal years addressed in the TDP. For subsequent years, the annual increase in revenue was tied to the increase in population and the inflation factor recommended by FDOT. To project revenues for future years, the average for per capita revenues for the last five fiscal years in the TDP was set as the base per capita value from which to calculate annual inflation-adjusted values. These per capita values were in turn applied to the population projections of the two counties to yield annual local transit revenues. A6-5

6 Table 2: Manatee County State-Distributed and Local Revenue Estimates millions of dollars, Year of Expenditure) (in Revenue Source State-Distributed Fuel Tax Revenues 25 Year Total Constitutional Fuel Tax County Fuel Tax Municipal Fuel Tax TOTAL STATE FUEL TAXES Local Fuel Tax Revenues Ninth Cent cent Local Option (County) cent Local Option (County) TOTAL LOCAL FUEL TAXES Local Transit Revenues Local Operating Revenues Local Capital Revenues TOTAL TRANSIT REVENUES Local Transportation Impact Fees County Municipalities TOTAL IMPACT FEES STATE-DISTRIBUTED/LOCAL TOTAL Total State-Distributed and Local Revenues Note: future impact fee revenue is not adjusted for inflation ,664.2 A6-6

7 Table 3: Sarasota County State-Distributed and Local Revenue Estimates millions of dollars, Year of Expenditure) (in Revenue Source State-Distributed Fuel Tax Revenues 25 Year Total Constitutional Fuel Tax County Fuel Tax Municipal Fuel Tax TOTAL STATE FUEL TAXES Local Fuel Tax Revenues Ninth Cent cent Local Option (County) cent Local Option (Municipalities) cent Local Option (County) cent Local Option (Municipalities) TOTAL LOCAL FUEL TAXES Discretionary Sales Surtax TOTAL SALES SURTAX Fuel Tax and Sales Surtax Revenue Bonds TOTAL DEBT SERVICE (100.8) (83.7) (184.5) Local Transit Revenues Local Operating Revenues ,091.6 Local Capital Revenues TOTAL TRANSIT REVENUES ,091.6 Local Transportation Impact Fees Unincorporated County Municipalities TOTAL IMPACT FEES A6-7

8 STATE-DISTRIBUTED/LOCAL TOTAL Total State-Distributed and Local Revenues Note: future impact fee revenue is not adjusted for inflation ,686.9 A6-8

9 Table 4: Total MPO State-Distributed and Local Revenue Estimates (in millions of dollars, Year of Expenditure) Revenue Source State-Distributed Fuel Tax Revenues 25 Year Total Constitutional Fuel Tax County Fuel Tax Municipal Fuel Tax TOTAL STATE FUEL TAXES Local Fuel Tax Revenues Ninth Cent cent Local Option (Counties) cent Local Option (Municipalities) cent Local Option (Counties) cent Local Option (Municipalities) TOTAL LOCAL FUEL TAXES ,616.3 Discretionary Sales Surtax TOTAL SALES SURTAX Fuel Tax and Sales Surtax Revenue Bonds TOTAL DEBT SERVICE (100.8) (83.7) (184.5) Local Transit Revenues Local Operating Revenues ,444.1 Local Capital Revenues TOTAL TRANSIT REVENUES ,447.0 Local Transportation Impact Fees Counties Municipalities TOTAL IMPACT FEES Total State-Distributed and Local Revenues STATE-DISTRIBUTED/LOCAL TOTAL , ,351.1 Note: future impact fee revenue is not adjusted for inflation A6-9

10 Table 5: Discretionary Federal/State Revenue Sources (in millions of dollars, Year of Expenditure) Revenue Source Year Total Districtwide TRIP Funds Statewide New Starts Funds IMPACT FEES/MOBILITY FEES Within Manatee County the County government, the City of Bradenton, and the City of Palmetto charge impact fees or mobility fees on new development to fund transportation facilities. Within Sarasota County the County government, the City of Sarasota, and the City of North Port charge such fees. The City of Venice and Town of Longboat Key have interlocal agreements in place with the County to charge the County s impact fees within their jurisdictions. Because these fees are dedicated to funding capital improvements related to transportation, Renaissance prepared projections of this revenue source based on the 2040 forecasts of population and employment that are used in the regional travel demand model. Given the inherent uncertainty of forecasting future development, these projections are intended to be conservative and a starting point for discussion. Current fee rates were used to project future revenue even if a jurisdiction has enacted a moratorium or discount on transportation impact/mobility fees at the present time. We also assumed the new mobility fee currently under consideration by Sarasota County is implemented and that Venice and Longboat Key opt into it. Renaissance examined the currently available impact fee schedules for the relevant jurisdictions and calculated average fees per dwelling unit (for residential land uses) or per 1,000 square feet (for nonresidential land uses) using selected property type categories that were determined to be generally representative of that land use. Residential land uses were classified as single-family or multifamily. The non-residential land uses analyzed were classified as industrial, commercial, or service to conform to the employment categories used in the regional travel demand model. The property types selected to calculate the average impact fee rates are generally described as follows: Single-Family Residential: single-family homes, small to moderately sized if broken out by square footage Multifamily Residential: townhouses, duplexes, and condominiums, small to moderately sized if broken out by square footage Industrial: warehouse and light industrial Commercial: general shopping center, retail of 100,000 square feet or less Service: general office of 100,000 square feet or less, office/business park, medical office The average impact fee assumptions per land use for each jurisdiction are shown in Table 6 below. A6-10

11 Table 6: Impact/Mobility Fee Rate Assumptions Jurisdiction Single Family Residential Multifamily Residential Industrial Commercial Service Impact Fees Manatee County $3,600 $1,585 $590 $7,152 $1,823 Bradenton $1,875 $1,264 $581 $4,247 $2,422 Palmetto $1,211 $848 $606 $3,634 $2,423 North Port $6,487 $4,551 $3,360 $14,275 $16,211 Mobility Fees Sarasota $5,014 $2,828 $1,613 $7,699 $10,230 Sarasota County: Standard $3,963 $2,801 $1,890 $6,604 $4,028 Mixed Use $2,972 $2,101 $1,417 $4,953 $3,021 Infill $2,081 $1,471 $992 $3,467 $2,115 Venice: Standard $3,963 $2,801 $1,890 $6,604 $4,028 Mixed Use $2,972 $2,101 $1,417 $4,953 $3,021 Longboat Key n/a n/a n/a n/a n/a Note: Residential uses are per dwelling unit, non-residential uses are per 1,000 square feet. Longboat Key would charge the Sarasota County mobility fee but is assumed to not generate significant fee revenue. In order to convert the non-residential impact fee rates from per-1,000-square-feet to per-worker, Renaissance assumed building space usage of one employee per 1,000 square feet for industrial, two employees per 1,000 square feet for commercial, and three employees per 1,000 square feet for service. A6-11

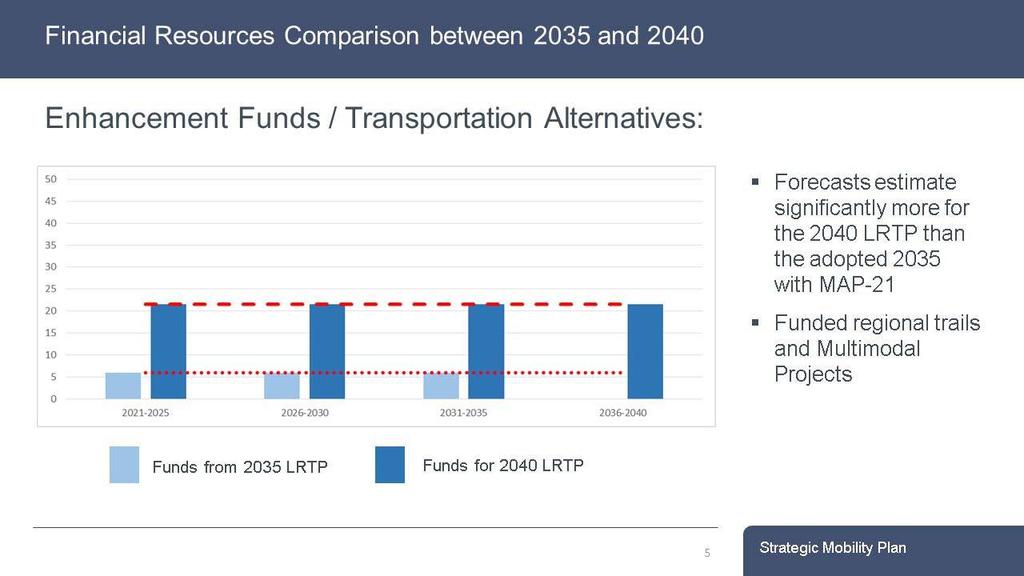

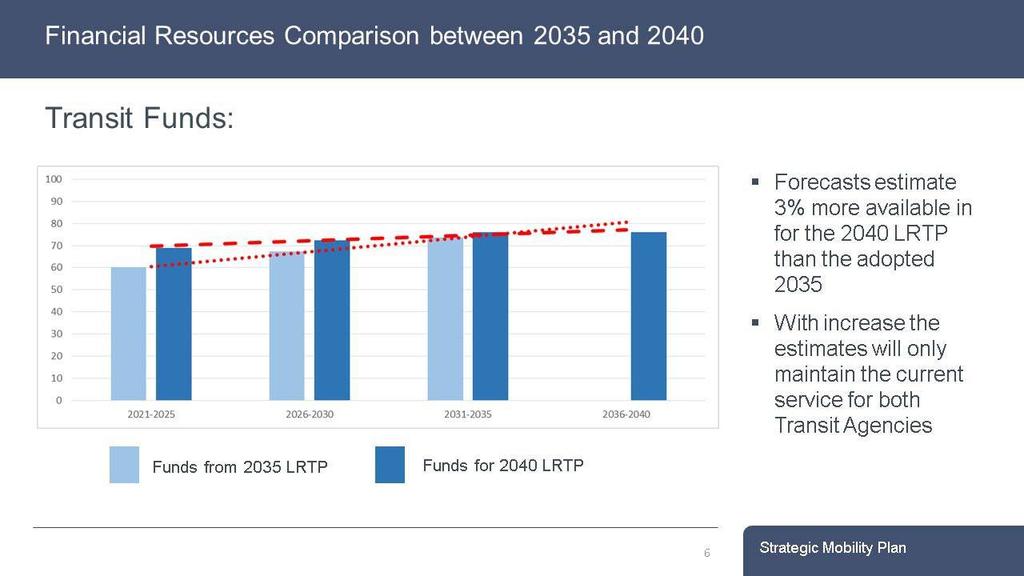

12 As shown in Table 6, the proposed Sarasota County mobility fee has three tiers of fee rates depending on the type of development being assessed: standard, mixed-use, and urban infill. The mixed-use and urban infill fee rates are lower than the standard rate due to adjustments for internal capture and reduced trip lengths, and they would be applied to specific projects with mixed-use characteristics and/or development located within designated infill areas. For the purposes of our projections, we assumed that future development within unincorporated Sarasota County would be 25 percent standard development, 50 percent mixed-use, and 25 percent urban infill. Because Venice would be charging the County mobility fee, we assumed that 75 percent of the City s future development would be standard and 25 percent would be mixed-use. Longboat Key would also charge the County mobility fee, but because of the small size and minimal level of development activity expected in the Town we assumed that it would not generate any significant mobility fee revenue. The average annual number of new dwelling units and workers forecast for each jurisdiction from was multiplied by the relevant fee rate assumption for that jurisdiction to estimate the annual revenue from transportation impact/mobility fees. Furthermore, the non-residential fee estimates were reduced by 25 percent to account for new jobs that backfill into existing building space rather than locate within newly developed building space. Unlike the other revenue sources discussed in this memo, future impact/mobility fee revenues were not adjusted for inflation because the fee rates are not changed on an annual basis and also to produce a more conservative estimate. The following graphs show the differences in each of the major funding sources between the 2035 LRTP and the 2040 LRTP, the direction given by the MPO Board on how to expend the funds, and how much is going towards each transportation program. A6-12

13 A6-13

14 A6-14

15 A6-15

Technical Report No. 4. Revenue and Costs

Technical Report No. 4 Revenue and Costs Technical Report No. 4 REVENUE AND COSTS PASCO COUNTY METROPOLITAN PLANNING ORGANIZATION 8731 Citizens Drive New Port Richey, FL 34654 Ph (727) 847-8140, fax (727)

Technical Report No. 4 Revenue and Costs Technical Report No. 4 REVENUE AND COSTS PASCO COUNTY METROPOLITAN PLANNING ORGANIZATION 8731 Citizens Drive New Port Richey, FL 34654 Ph (727) 847-8140, fax (727)

YEAR 2035 LONG RANGE TRANSPORTATION PLAN FINAL TECHNICAL REPORT NO. 2: DATA COLLECTION, MAPPING AND DATA DEVELOPMENT

YEAR 2035 LONG RANGE TRANSPORTATION PLAN FINAL TECHNICAL REPORT NO. 2: DATA COLLECTION, MAPPING AND DATA DEVELOPMENT Prepared for: METROPOLITAN TRANSPORTATION PLANNING ORGANIZATION FOR THE GAINESVILLE

YEAR 2035 LONG RANGE TRANSPORTATION PLAN FINAL TECHNICAL REPORT NO. 2: DATA COLLECTION, MAPPING AND DATA DEVELOPMENT Prepared for: METROPOLITAN TRANSPORTATION PLANNING ORGANIZATION FOR THE GAINESVILLE

Chapter 5: Cost and Revenues Assumptions

Chapter 5: Cost and Revenues Assumptions Chapter 5: Cost and Revenues Assumptions INTRODUCTION This chapter documents the assumptions that were used to develop unit costs and revenue estimates for the

Chapter 5: Cost and Revenues Assumptions Chapter 5: Cost and Revenues Assumptions INTRODUCTION This chapter documents the assumptions that were used to develop unit costs and revenue estimates for the

Chapter 4: Available Funds and Financial Scenarios

Funding the Plan Federal and State requirements say that a Long Range Transportation Plan (LRTP) must include a financial plan. The financial plan must indicate resources from public and private sources

Funding the Plan Federal and State requirements say that a Long Range Transportation Plan (LRTP) must include a financial plan. The financial plan must indicate resources from public and private sources

Technical Appendix. FDOT 2040 Revenue Forecast

Technical Appendix FDOT 040 Revenue Forecast This page was left blank intentionally. APPENDIX FOR THE METROPOLITAN LONG RANGE PLAN 040 Forecast of State and Federal Revenues for Statewide and Metropolitan

Technical Appendix FDOT 040 Revenue Forecast This page was left blank intentionally. APPENDIX FOR THE METROPOLITAN LONG RANGE PLAN 040 Forecast of State and Federal Revenues for Statewide and Metropolitan

APPENDIX FOR THE METROPOLITAN LONG RANGE TRANSPORTATION PLAN Forecast of State and Federal Revenues for Statewide and Metropolitan Plans

APPENDIX FOR THE METROPOLITAN LONG RANGE TRANSPORTATION PLAN 2035 Forecast of State and Federal Revenues for Statewide and Metropolitan Plans Overview This appendix documents the current Florida Department

APPENDIX FOR THE METROPOLITAN LONG RANGE TRANSPORTATION PLAN 2035 Forecast of State and Federal Revenues for Statewide and Metropolitan Plans Overview This appendix documents the current Florida Department

HILLSBOROUGH COUNTY MPO 2035 LONG RANGE TRANSPORTATION PLAN

HILLSBOROUGH COUNTY MPO 2035 LONG RANGE TRANSPORTATION PLAN REASONABLY AVAILABLE AND NEW AND ADDITIONAL PROJECTED REVENUE SOURCES IN HILLSBOROUGH COUNTY TECHNICAL MEMORANDUM Hillsborough County Metropolitan

HILLSBOROUGH COUNTY MPO 2035 LONG RANGE TRANSPORTATION PLAN REASONABLY AVAILABLE AND NEW AND ADDITIONAL PROJECTED REVENUE SOURCES IN HILLSBOROUGH COUNTY TECHNICAL MEMORANDUM Hillsborough County Metropolitan

Financial Resources Report BAY COUNTY DIRECTION 2035 SHAPING OUR FUTURE LONG RANGE TRANSPORTATION PLAN. Prepared for

Financial Resources Report BAY COUNTY DIRECTION 2035 SHAPING OUR FUTURE LONG RANGE TRANSPORTATION PLAN Prepared for Bay County Transportation Planning Organization and The Florida Department of Transportation,

Financial Resources Report BAY COUNTY DIRECTION 2035 SHAPING OUR FUTURE LONG RANGE TRANSPORTATION PLAN Prepared for Bay County Transportation Planning Organization and The Florida Department of Transportation,

Technical Report #2: Financial Resources Final Adopted Plan January 2016

2040 Long Range Transportation Plan Technical Report #2: Financial Resources Final Adopted Plan January 2016 250 South Orange Avenue, Suite 200, Orlando, FL 32801 407-481-5672 www.metroplanorlando.com

2040 Long Range Transportation Plan Technical Report #2: Financial Resources Final Adopted Plan January 2016 250 South Orange Avenue, Suite 200, Orlando, FL 32801 407-481-5672 www.metroplanorlando.com

Chapter 6: Financial Resources

Chapter 6: Financial Resources Introduction This chapter presents the project cost estimates, revenue assumptions and projected revenues for the Lake~Sumter MPO. The analysis reflects a multi-modal transportation

Chapter 6: Financial Resources Introduction This chapter presents the project cost estimates, revenue assumptions and projected revenues for the Lake~Sumter MPO. The analysis reflects a multi-modal transportation

2035 Long Range Transportation Plan Update

Broward MPO 2035 Long Range Transportation Plan Update Technical Report # 6 Prepared by: In association with: December 2009 TABLE OF CONTENTS 1.0 Introduction... 1 1.1 Purpose... 1 1.2 Methodology and

Broward MPO 2035 Long Range Transportation Plan Update Technical Report # 6 Prepared by: In association with: December 2009 TABLE OF CONTENTS 1.0 Introduction... 1 1.1 Purpose... 1 1.2 Methodology and

Fiscal Analysis November 14, Fiscal Analysis Fiscal Conditions Project Background

3.11 Fiscal Analysis Fiscal Analysis 3.11.1 Fiscal Conditions 3.11.1.1 Project Background The proposed action is a 149 unit residential development, including a private road and appurtenances, on a 29.3

3.11 Fiscal Analysis Fiscal Analysis 3.11.1 Fiscal Conditions 3.11.1.1 Project Background The proposed action is a 149 unit residential development, including a private road and appurtenances, on a 29.3

Indian River County 2030 Comprehensive Plan

2030 Comprehensive Plan Chapter 6 Supplement #15; Adopted December 5, 2017, Ordinance 2017-015 TABLE OF CONTENTS List of Figures... ii List of Tables... iii Introduction... 1 Existing Conditions... 2 Financial

2030 Comprehensive Plan Chapter 6 Supplement #15; Adopted December 5, 2017, Ordinance 2017-015 TABLE OF CONTENTS List of Figures... ii List of Tables... iii Introduction... 1 Existing Conditions... 2 Financial

Indian River County 2030 Comprehensive Plan

2030 Comprehensive Plan Chapter 6 Adopted:, 2010 DRAFT January 14, 2010 TABLE OF CONTENTS List of Figures... ii List of Tables... ii Introduction... 1 Existing Conditions... 2 Financial Resources... 2

2030 Comprehensive Plan Chapter 6 Adopted:, 2010 DRAFT January 14, 2010 TABLE OF CONTENTS List of Figures... ii List of Tables... ii Introduction... 1 Existing Conditions... 2 Financial Resources... 2

Fully Utilized Transportation Funding Sources

Ad valorem Taxes Fully Utilized Transportation ing Sources Statutory Ad Valorem Taxes Section 9, Article VII, Florida Constitution has the current authority to levy up to 0.5 mills and is currently levying

Ad valorem Taxes Fully Utilized Transportation ing Sources Statutory Ad Valorem Taxes Section 9, Article VII, Florida Constitution has the current authority to levy up to 0.5 mills and is currently levying

INVESTING STRATEGICALLY

11 INVESTING STRATEGICALLY Federal transportation legislation (Fixing America s Surface Transportation Act FAST Act) requires that the 2040 RTP be based on a financial plan that demonstrates how the program

11 INVESTING STRATEGICALLY Federal transportation legislation (Fixing America s Surface Transportation Act FAST Act) requires that the 2040 RTP be based on a financial plan that demonstrates how the program

MISSION STATEMENT. To Meet the Needs and Exceed the Expectations of Those We Serve, in Fulfilling Our Constitutional Obligations.

MISSION STATEMENT To Meet the Needs and Exceed the Expectations of Those We Serve, in Fulfilling Our Constitutional Obligations. A Message from Karen E. Rushing Clerk of the Circuit Court and County Comptroller

MISSION STATEMENT To Meet the Needs and Exceed the Expectations of Those We Serve, in Fulfilling Our Constitutional Obligations. A Message from Karen E. Rushing Clerk of the Circuit Court and County Comptroller

DRAFT 04/08/ Plan Post Referendum Analysis. Technical Memorandum Two: FUNDING ALTERNATIVE STRATEGIES. Prepared For: Prepared By:

DRAFT 04/08/2011 2035 Plan Post Referendum Analysis Prepared For: 601 East Kennedy Boulevard Tampa, FL 33602 Prepared By: Table of Contents Introduction 1.0 Federal Funding Sources... i 1.1 Federal Transit

DRAFT 04/08/2011 2035 Plan Post Referendum Analysis Prepared For: 601 East Kennedy Boulevard Tampa, FL 33602 Prepared By: Table of Contents Introduction 1.0 Federal Funding Sources... i 1.1 Federal Transit

FY15 REVENUES. FY 14 Adopted Taxes. General Fund $ $ $753.50

BROWARD COUNTY BUDGET-IN-BRIEF FY15 REVENUES Overview County services are funded with a variety of revenue sources. These sources include the following: property taxes, miscellaneous taxes and assessments,

BROWARD COUNTY BUDGET-IN-BRIEF FY15 REVENUES Overview County services are funded with a variety of revenue sources. These sources include the following: property taxes, miscellaneous taxes and assessments,

Mobility Plans and Fees in Florida

Mobility Plans and Fees in Florida Mobility Plans and Fees in Florida GIC Conference November 13, 2014 Bradenton, Florida Bob Wallace, P.E., AICP Tindale-Oliver Alex DavisShaw, P.E., PTOE, City Engineer,

Mobility Plans and Fees in Florida Mobility Plans and Fees in Florida GIC Conference November 13, 2014 Bradenton, Florida Bob Wallace, P.E., AICP Tindale-Oliver Alex DavisShaw, P.E., PTOE, City Engineer,

COLLECTION AND DISTRIBUTION OF TRANSPORTATION FUNDS

COLLECTION AND DISTRIBUTION OF TRANSPORTATION FUNDS FY1995-FY2018 Jennifer Stults, AICP CTP, CPM & Ben Walker, PE March 23, 2015 Sarasota Manatee MPO Board Meeting OUTLINE Statutory Fund Allocation Process

COLLECTION AND DISTRIBUTION OF TRANSPORTATION FUNDS FY1995-FY2018 Jennifer Stults, AICP CTP, CPM & Ben Walker, PE March 23, 2015 Sarasota Manatee MPO Board Meeting OUTLINE Statutory Fund Allocation Process

FY16 REVENUES. FY 15 Adopted Taxes. General Fund $ $ $ Voter Approved Debt Service $37.30 $36.90 $37.50

FY16 REVENUES Overview County services are funded with a variety of revenue sources. These sources include the following: property taxes, miscellaneous taxes and assessments, federal and state grants,

FY16 REVENUES Overview County services are funded with a variety of revenue sources. These sources include the following: property taxes, miscellaneous taxes and assessments, federal and state grants,

Capital Improvements

Capital Improvements CAPITAL IMPROVEMENT ELEMENT GOAL 7-1: PROVIDE & MAINTAIN PUBLIC FACILITIES AND SERVICES Provide and maintain public facilities and services which protect and promote the public health,

Capital Improvements CAPITAL IMPROVEMENT ELEMENT GOAL 7-1: PROVIDE & MAINTAIN PUBLIC FACILITIES AND SERVICES Provide and maintain public facilities and services which protect and promote the public health,

Big Chino Water Ranch Project Impact Analysis Prescott & Prescott Valley, Arizona

Big Chino Water Ranch Project Impact Analysis Prescott & Prescott Valley, Arizona Prepared for: Central Arizona Partnership August 2008 Prepared by: 7505 East 6 th Avenue, Suite 100 Scottsdale, Arizona

Big Chino Water Ranch Project Impact Analysis Prescott & Prescott Valley, Arizona Prepared for: Central Arizona Partnership August 2008 Prepared by: 7505 East 6 th Avenue, Suite 100 Scottsdale, Arizona

FY19 Adopted Budget Overview

FY19 Budget Overview FY19 Financial Plan Overview The Sarasota County total FY2019 Financial Plan is $1,242,441,007 for all funds. When excluding transfers and reserves equaling $212,401,925, the FY19

FY19 Budget Overview FY19 Financial Plan Overview The Sarasota County total FY2019 Financial Plan is $1,242,441,007 for all funds. When excluding transfers and reserves equaling $212,401,925, the FY19

Pinellas County Bonded Debt. Last ten years (dollars in thousands)

") DEBT SERVICE Debt Service Costs include the annual payments of interest, principal and other fees on long term bond indebtedness. This section includes the budgeted debt service for obligations which provide

DEBT SERVICE Debt Service Costs include the annual payments of interest, principal and other fees on long term bond indebtedness. This section includes the budgeted debt service for obligations which provide

1. identifies the required capacity of capital improvements to serve existing and future development based on level-of-service (LOS) standards;

standards;") DIVISION 4.200 CAPITAL IMPROVEMENTS ELEMENT SECTION 4.201 INTRODUCTION The purpose of the Capital Improvements Element (CIE) is to tie the capital improvement needs identified in the other elements to

DIVISION 4.200 CAPITAL IMPROVEMENTS ELEMENT SECTION 4.201 INTRODUCTION The purpose of the Capital Improvements Element (CIE) is to tie the capital improvement needs identified in the other elements to

Hillsborough County Population and Employment Projections and Allocations DECEMBER 2017

Hillsborough County Population and Employment Projections and Allocations DECEMBER 2017 Presentation Overview Overview of the Allocation Process Population and Employment Projections Trend Analysis 2045

Hillsborough County Population and Employment Projections and Allocations DECEMBER 2017 Presentation Overview Overview of the Allocation Process Population and Employment Projections Trend Analysis 2045

2017 Educational Series FUNDING

2017 Educational Series FUNDING TXDOT FUNDING INTRODUCTION Transportation projects take many years to develop and construct. In addition to the design, engineering, public involvement, right-of-way acquisition,

2017 Educational Series FUNDING TXDOT FUNDING INTRODUCTION Transportation projects take many years to develop and construct. In addition to the design, engineering, public involvement, right-of-way acquisition,

Section 19 Revenues. Overview

Section 19 Revenues Overview Local governments generate revenues from a wide range of sources. The authority for generating revenues is derived from the State Constitution, home rule authority, or Florida

Section 19 Revenues Overview Local governments generate revenues from a wide range of sources. The authority for generating revenues is derived from the State Constitution, home rule authority, or Florida

D R A F T APPENDIX A. Future Employment Forecast Methodology

Transit Development Plan Memo #3: Planning Framework Appendix A APPENDIX A Future Employment Forecast Methodology Transit Development Plan Memo #3: Planning Framework Appendix A APPENDIX A FUTURE EMPLOYMENT

Transit Development Plan Memo #3: Planning Framework Appendix A APPENDIX A Future Employment Forecast Methodology Transit Development Plan Memo #3: Planning Framework Appendix A APPENDIX A FUTURE EMPLOYMENT

REVENUE MANUAL PALM BEACH COUNTY Edition February 2018

REVENUE MANUAL PALM BEACH COUNTY 218 Edition February 218 TABLE OF CONTENTS About this. 2 Index of Revenues Index of Revenues by Revenue Source Code Index of Revenues by Name. 3 4 1 About this The Palm

REVENUE MANUAL PALM BEACH COUNTY 218 Edition February 218 TABLE OF CONTENTS About this. 2 Index of Revenues Index of Revenues by Revenue Source Code Index of Revenues by Name. 3 4 1 About this The Palm

CAPITAL IMPROVEMENTS ELEMENT:

CAPITAL IMPROVEMENTS ELEMENT: Goals, Objectives and Policies Goal 1. The provision of needed public facilities in a timely manner, which protects investments in existing facilities, maximizes the use of

CAPITAL IMPROVEMENTS ELEMENT: Goals, Objectives and Policies Goal 1. The provision of needed public facilities in a timely manner, which protects investments in existing facilities, maximizes the use of

MPOAC REVENUE STUDY. Study Update Northwest Florida Regional TPO January 18, 2012

Study Update Northwest Florida Regional TPO January 18, 2012 Study History 2008 Florida Senate Bill 1688 Recommend funding mechanism 13 members- 3 governor s, 3 Senate, 3 House, FDOT, MPOAC, FL Association

Study Update Northwest Florida Regional TPO January 18, 2012 Study History 2008 Florida Senate Bill 1688 Recommend funding mechanism 13 members- 3 governor s, 3 Senate, 3 House, FDOT, MPOAC, FL Association

Arizona Low Income Housing Tax Credit and Housing Trust Fund Economic and Fiscal Impact Report

Arizona Low Income Housing Tax Credit and Housing Trust Fund Economic and Fiscal Impact Report Prepared for: Arizona Department of Housing January 2014 Prepared by: Elliott D. Pollack & Company 7505 East

Arizona Low Income Housing Tax Credit and Housing Trust Fund Economic and Fiscal Impact Report Prepared for: Arizona Department of Housing January 2014 Prepared by: Elliott D. Pollack & Company 7505 East

System Development Charge Methodology

City of Springfield System Development Charge Methodology Stormwater Local Wastewater Transportation Prepared By City of Springfield Public Works Department 225 Fifth Street Springfield, OR 97477 November

City of Springfield System Development Charge Methodology Stormwater Local Wastewater Transportation Prepared By City of Springfield Public Works Department 225 Fifth Street Springfield, OR 97477 November

MOBILITY FEES IN PASCO COUNTY

MOBILITY FEES IN PASCO COUNTY History Objectives Today Overview of Pasco County Mobility Fees Overcoming Objections to Mobility Fees 2 Motivating Factors 48% of Pasco County workers employed outside of

MOBILITY FEES IN PASCO COUNTY History Objectives Today Overview of Pasco County Mobility Fees Overcoming Objections to Mobility Fees 2 Motivating Factors 48% of Pasco County workers employed outside of

Fiscal Impact Analysis

May 12, 2017 Fiscal Impact Analysis Westport Cupertino Development Prepared for: KT Urban, LLC Prepared by: Applied Development Economics, Inc. 1756 Lacassie Avenue, #100, Walnut Creek, CA 94596 925.934.8712

May 12, 2017 Fiscal Impact Analysis Westport Cupertino Development Prepared for: KT Urban, LLC Prepared by: Applied Development Economics, Inc. 1756 Lacassie Avenue, #100, Walnut Creek, CA 94596 925.934.8712

5/3/2016. May 4, Item #1 CITIZENS PARTICIPATION

May 4, 2016 Item #1 CITIZENS PARTICIPATION 1 Item #2 ELECT AN ACTING CHAIR Item #3 APPROVAL OF MINUTES 2 Item #4 OVERVIEW OF TRAC AGENDA Committee Goals Learn about the RTC including its roadway and transit

May 4, 2016 Item #1 CITIZENS PARTICIPATION 1 Item #2 ELECT AN ACTING CHAIR Item #3 APPROVAL OF MINUTES 2 Item #4 OVERVIEW OF TRAC AGENDA Committee Goals Learn about the RTC including its roadway and transit

Mobility Plans and Fees: The Future of Transportation Funding

Mobility Plans and Fees: The Future of Transportation Funding Mobility Plans and Fees: The Future of Transportation Funding Growth & Infrastructure Consortium November 4, 2010 Tampa, Florida Bob Wallace,

Mobility Plans and Fees: The Future of Transportation Funding Mobility Plans and Fees: The Future of Transportation Funding Growth & Infrastructure Consortium November 4, 2010 Tampa, Florida Bob Wallace,

Transit Alternate Funding Options Study Technical Memo Task 1 November 23, 2010

Transit Alternate Funding Options Study Technical Memo Task 1 November 23, 2010 Prepared for: Volusia Transportation Planning Organization Votran Prepared by: The PFM Group 300 South Orange Avenue Suite

Transit Alternate Funding Options Study Technical Memo Task 1 November 23, 2010 Prepared for: Volusia Transportation Planning Organization Votran Prepared by: The PFM Group 300 South Orange Avenue Suite

GRASS VALLEY TRANSPORTATION IMPACT FEE PROGRAM NEXUS STUDY

HEARING REPORT GRASS VALLEY TRANSPORTATION IMPACT FEE PROGRAM NEXUS STUDY Prepared for: City of Grass Valley Prepared by: Economic & Planning Systems, Inc. March 2008 EPS #17525 S A C R A M E N T O 2150

HEARING REPORT GRASS VALLEY TRANSPORTATION IMPACT FEE PROGRAM NEXUS STUDY Prepared for: City of Grass Valley Prepared by: Economic & Planning Systems, Inc. March 2008 EPS #17525 S A C R A M E N T O 2150

TABLE OF CONTENTS INTRODUCTION... 1 CAPITAL IMPROVEMENTS INVENTORY AND ANALYSIS... 1 DEFINITIONS... 2 DATA INVENTORY... 23

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 Chapter 8 TABLE OF CONTENTS INTRODUCTION... 1 CAPITAL IMPROVEMENTS INVENTORY AND

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 Chapter 8 TABLE OF CONTENTS INTRODUCTION... 1 CAPITAL IMPROVEMENTS INVENTORY AND

CHAPTER 4 FINANCIAL STRATEGIES: PAYING OUR WAY

The financial analysis of the recommended transportation improvements in the 2030 San Diego Regional Transportation Plan: Pathways for the Future (RTP or the Plan ) focuses on four components: Systems

The financial analysis of the recommended transportation improvements in the 2030 San Diego Regional Transportation Plan: Pathways for the Future (RTP or the Plan ) focuses on four components: Systems

City of Redding, California Development Impact Mitigation Fee Nexus Study

, California Development Impact Mitigation Fee Nexus Study December 5, 2017 Prepared by helping communities fund to morrow This page intentionally left blank. TABLE OF CONTENTS Executive Summary...1 Background

, California Development Impact Mitigation Fee Nexus Study December 5, 2017 Prepared by helping communities fund to morrow This page intentionally left blank. TABLE OF CONTENTS Executive Summary...1 Background

Revenue Options for Baltimore City s Affordable Housing Trust Fund

Revenue Options for Baltimore City s Affordable Housing Trust Fund A P R I L 2 0 1 8 Baltimore City voters approved a ballot question in 2016 to create an affordable housing trust fund. The purpose of

Revenue Options for Baltimore City s Affordable Housing Trust Fund A P R I L 2 0 1 8 Baltimore City voters approved a ballot question in 2016 to create an affordable housing trust fund. The purpose of

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF BLOOMINGTON MUNICIPAL PROFILE

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF BLOOMINGTON MUNICIPAL PROFILE by John Stafford March 2016 1 CITY OF BLOOMINGTON MUNICIPAL PROFILE MARCH 2016 Introduction This document is

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF BLOOMINGTON MUNICIPAL PROFILE by John Stafford March 2016 1 CITY OF BLOOMINGTON MUNICIPAL PROFILE MARCH 2016 Introduction This document is

DOTD s Response to House Resolution 178 (2016)

") DOTD s Response to House Resolution 178 (2016) Part II: Feasibility of Implementing Local Option Motor Fuel Taxes 2016 HDR, Inc., all rights reserved. National Context Current Events Federal motor fuel

DOTD s Response to House Resolution 178 (2016) Part II: Feasibility of Implementing Local Option Motor Fuel Taxes 2016 HDR, Inc., all rights reserved. National Context Current Events Federal motor fuel

Minimum Elements of a Local Comprehensive Plan

Minimum Elements of a Local Comprehensive Plan Background OKI is an association of local governments, business organizations and community groups serving more than 180 cities, villages, and townships in

Minimum Elements of a Local Comprehensive Plan Background OKI is an association of local governments, business organizations and community groups serving more than 180 cities, villages, and townships in

Analysis of Regional Transportation Spending

Analysis of Regional Transportation Spending An overview of transportation revenues and expenses of Greater Des Moines June 2016 Contents Executive Summary Purpose Key Findings Regional Goals Federal Funding

Analysis of Regional Transportation Spending An overview of transportation revenues and expenses of Greater Des Moines June 2016 Contents Executive Summary Purpose Key Findings Regional Goals Federal Funding

CAPITAL IMPROVEMENTS ELEMENT GOALS, OBJECTIVES AND POLICIES. Goal 1: [CI] (EFF. 7/16/90)

![CAPITAL IMPROVEMENTS ELEMENT GOALS, OBJECTIVES AND POLICIES. Goal 1: [CI] (EFF. 7/16/90)](/thumbs/93/114312533.jpg "CAPITAL IMPROVEMENTS ELEMENT GOALS, OBJECTIVES AND POLICIES. Goal 1: [CI] (EFF. 7/16/90)") CAPITAL IMPROVEMENTS ELEMENT GOALS, OBJECTIVES AND POLICIES Goal 1: [CI] (EFF. 7/16/90) To use sound fiscal policies to provide adequate public facilities concurrent with, or prior to development in order

CAPITAL IMPROVEMENTS ELEMENT GOALS, OBJECTIVES AND POLICIES Goal 1: [CI] (EFF. 7/16/90) To use sound fiscal policies to provide adequate public facilities concurrent with, or prior to development in order

CAPITAL IMPROVEMENTS ELEMENT

Goals, Objectives and Policies CAPITAL IMPROVEMENTS ELEMENT GOAL 9.1.: USE SOUND FISCAL POLICIES TO PROVIDE ADEQUATE PUBLIC FACILITIES TO ALL RESIDENTS WITHIN THE CITY. FISCAL POLICIES MUST PROTECT INVESTMENTS

Goals, Objectives and Policies CAPITAL IMPROVEMENTS ELEMENT GOAL 9.1.: USE SOUND FISCAL POLICIES TO PROVIDE ADEQUATE PUBLIC FACILITIES TO ALL RESIDENTS WITHIN THE CITY. FISCAL POLICIES MUST PROTECT INVESTMENTS

CAPITAL IMPROVEMENTS ELEMENT

CAPITAL IMPROVEMENTS ELEMENT INTRODUCTION The purpose of the Capital Improvements Element is to consider the need for and the location of public facilities in order to encourage the efficient use of such

CAPITAL IMPROVEMENTS ELEMENT INTRODUCTION The purpose of the Capital Improvements Element is to consider the need for and the location of public facilities in order to encourage the efficient use of such

Monroe County, FL Fiscal Year Capital Improvement Program

Monroe County, FL Fiscal Year 2018 2022 Capital Improvement Program Capital Improvement Plan Overview Capital Improvement Plan The Capital Improvement Plan is a resource that assists Monroe County in ensuring

Monroe County, FL Fiscal Year 2018 2022 Capital Improvement Program Capital Improvement Plan Overview Capital Improvement Plan The Capital Improvement Plan is a resource that assists Monroe County in ensuring

8. FINANCIAL ANALYSIS

8. FINANCIAL ANALYSIS This chapter presents the financial analysis conducted for the Locally Preferred Alternative (LPA) selected by the Metropolitan Transit Authority of Harris County (METRO) for the.

8. FINANCIAL ANALYSIS This chapter presents the financial analysis conducted for the Locally Preferred Alternative (LPA) selected by the Metropolitan Transit Authority of Harris County (METRO) for the.

CHAPTER 9 FINANCIAL CONSIDERATIONS

CHAPTER 9 FINANCIAL CONSIDERATIONS 9.1 INTRODUCTION This chapter presents anticipated costs, revenues, and funding for the Berryessa Extension Project (BEP) Alternative and the Silicon Valley Rapid Transit

CHAPTER 9 FINANCIAL CONSIDERATIONS 9.1 INTRODUCTION This chapter presents anticipated costs, revenues, and funding for the Berryessa Extension Project (BEP) Alternative and the Silicon Valley Rapid Transit

CHAPTER 11: Economic Development and Sustainability

AGLE AREA COMMUNITY Plan CHAPTER 11 CHAPTER 11: Economic Development and Sustainability Economic Development and Sustainability The overall economy of the Town and the Town government s finances are inextricably

AGLE AREA COMMUNITY Plan CHAPTER 11 CHAPTER 11: Economic Development and Sustainability Economic Development and Sustainability The overall economy of the Town and the Town government s finances are inextricably

Chapter 3: Regional Transportation Finance

Chapter 3: Regional Transportation Finance This chapter examines the sources of funding for transportation investments in the coming years. It describes recent legislative actions that have changed the

Chapter 3: Regional Transportation Finance This chapter examines the sources of funding for transportation investments in the coming years. It describes recent legislative actions that have changed the

FY 2018 Revenue Manual CITY OF ST. AUGUSTINE

FY 2018 Revenue Manual CITY OF ST. AUGUSTINE This Revenue Manual was developed to provide a comprehensive reference source for all revenue collected by the City of St. Augustine. The manual is an in depth

FY 2018 Revenue Manual CITY OF ST. AUGUSTINE This Revenue Manual was developed to provide a comprehensive reference source for all revenue collected by the City of St. Augustine. The manual is an in depth

WASATCH FRONT REGIONAL TRANSPORTATION PLAN FINANCIAL PLAN. Technical Report 47 May 2007 DAVIS MORGAN SALT LAKE TOOELE WEBER

WASATCH FRONT REGIONAL TRANSPORTATION PLAN 2007-2030 FINANCIAL PLAN Technical Report 47 May 2007 DAVIS MORGAN SALT LAKE TOOELE WEBER 2030 RTP Financial Plan WASATCH FRONT REGIONAL TRANSPORTATION PLAN

WASATCH FRONT REGIONAL TRANSPORTATION PLAN 2007-2030 FINANCIAL PLAN Technical Report 47 May 2007 DAVIS MORGAN SALT LAKE TOOELE WEBER 2030 RTP Financial Plan WASATCH FRONT REGIONAL TRANSPORTATION PLAN

bae urban economics Memorandum Fee Analysis for General Plan Update Cost Recovery and for General Plan Implementation

bae urban economics Memorandum To: Vacaville City Council From: Matt Kowta, Principal, MCP Date: July 10, 2016 Re: Fee Analysis for General Plan Update Cost Recovery and for General Plan Implementation

bae urban economics Memorandum To: Vacaville City Council From: Matt Kowta, Principal, MCP Date: July 10, 2016 Re: Fee Analysis for General Plan Update Cost Recovery and for General Plan Implementation

Presented By: L. Carson Bise II, AICP President

Impact Fee Basics: Methodology and Fee Design Presented By: L. Carson Bise II, AICP President Basic Options for One-Time Infrastructure Charges Funding from broad-based revenues (general taxes) Growth

Impact Fee Basics: Methodology and Fee Design Presented By: L. Carson Bise II, AICP President Basic Options for One-Time Infrastructure Charges Funding from broad-based revenues (general taxes) Growth

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF GREENWOOD MUNICIPAL PROFILE

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF GREENWOOD MUNICIPAL PROFILE by John Stafford March 2016 1 CITY OF GREENWOOD MUNICIPAL PROFILE MARCH 2016 Introduction This document is a summary

THE FISCAL HEALTH OF INDIANA S LARGER MUNICIPALITIES: CITY OF GREENWOOD MUNICIPAL PROFILE by John Stafford March 2016 1 CITY OF GREENWOOD MUNICIPAL PROFILE MARCH 2016 Introduction This document is a summary

TECHNICAL PLANNING COMMITTEE AGENDA 3/18/2015; ITEM II.B. Amendment Number Four to the FY Transportation Improvement Program

TECHNICAL PLANNING COMMITTEE AGENDA 3/18/2015; ITEM II.B. Amendment Number Four to the FY 2015-2018 Transportation Improvement Program AGENDA DESCRIPTION: Ozarks Transportation Organization (Springfield,

TECHNICAL PLANNING COMMITTEE AGENDA 3/18/2015; ITEM II.B. Amendment Number Four to the FY 2015-2018 Transportation Improvement Program AGENDA DESCRIPTION: Ozarks Transportation Organization (Springfield,

Pasco County, Florida. Multi-Modal Mobility Fee 2018 Update Study

Pasco County, Florida Multi-Modal Mobility 2018 Update Study PCPT December 3, 2018 PASCO COUNTY 2018 MULTI MODAL MOBILITY FEE UPDATE STUDY Prepared for: Pasco County, Florida Prepared by: W.E. Oliver,

Pasco County, Florida Multi-Modal Mobility 2018 Update Study PCPT December 3, 2018 PASCO COUNTY 2018 MULTI MODAL MOBILITY FEE UPDATE STUDY Prepared for: Pasco County, Florida Prepared by: W.E. Oliver,

TRANSPORTATION-SPECIFIC SALES TAX REVENUE 23% Visitors Generate Roughly 23 Percent of Taxable Retail Sales

EXECUTIVE SUMMARY Applied Analysis was retained by the Las Vegas Convention and Visitors Authority ( LVCVA ) to review and analyze the economic impacts associated with its various operations and the overall

EXECUTIVE SUMMARY Applied Analysis was retained by the Las Vegas Convention and Visitors Authority ( LVCVA ) to review and analyze the economic impacts associated with its various operations and the overall

River Edge Fiscal Impact Analysis

Final Report Prepared for: Carbondale Investments Prepared by: Economic & Planning Systems, Inc. EPS #20813 App. N-2 Table of Contents 1. INTRODUCTION AND SUMMARY OF FINDINGS... 1 Summary of Findings...

Final Report Prepared for: Carbondale Investments Prepared by: Economic & Planning Systems, Inc. EPS #20813 App. N-2 Table of Contents 1. INTRODUCTION AND SUMMARY OF FINDINGS... 1 Summary of Findings...

City of Antioch Development Impact Fee Study

Report City of Antioch Development Impact Fee Study Prepared for: City of Antioch Prepared by: Economic & Planning Systems, Inc. February 2014 EPS #20001 Table of Contents 1. INTRODUCTION AND RESULTS...

Report City of Antioch Development Impact Fee Study Prepared for: City of Antioch Prepared by: Economic & Planning Systems, Inc. February 2014 EPS #20001 Table of Contents 1. INTRODUCTION AND RESULTS...

TABLE OF CONTENTS LIST OF TABLES

TABLE OF CONTENTS A. GOALS, OBJECTIVES, AND POLICIES... 3 B. SUMMARY... 17 LIST OF TABLES Table IX 1: City of Winter Springs Five-Year Schedule of Capital Improvements (SCI) FY 2013/14-2017/18... 11 Table

TABLE OF CONTENTS A. GOALS, OBJECTIVES, AND POLICIES... 3 B. SUMMARY... 17 LIST OF TABLES Table IX 1: City of Winter Springs Five-Year Schedule of Capital Improvements (SCI) FY 2013/14-2017/18... 11 Table

FY 2009 FISCAL RESPONSIBILITY REPORT CARD

FY 2009 FISCAL RESPONSIBILITY REPORT CARD Local Government Division 100 West Randolph Street Chicago, IL 60601 Toll Free Hotline: (877) 304-3899 E-mail: locgov@mail.ioc.state.il.us 2 December 21, 2010

FY 2009 FISCAL RESPONSIBILITY REPORT CARD Local Government Division 100 West Randolph Street Chicago, IL 60601 Toll Free Hotline: (877) 304-3899 E-mail: locgov@mail.ioc.state.il.us 2 December 21, 2010

Schedule of Ad Valorem Taxes and Required Millage. Summary of Total Budget

Citrus County, Florida Schedule of Ad Valorem Taxes and Required Millage BOCC County-Wide 2010/2011 2011/2012 Revenue Millage Revenue Millage General Fund $ 47,539,858 4.9447 $ 46,165,753 4.9447 Road &

Citrus County, Florida Schedule of Ad Valorem Taxes and Required Millage BOCC County-Wide 2010/2011 2011/2012 Revenue Millage Revenue Millage General Fund $ 47,539,858 4.9447 $ 46,165,753 4.9447 Road &

How did we get here?

MOBILITY FEES How did we get here? ULI Report (2008): The County should conduct long-range concurrency studies for each of the five market areas linked to a defined concurrency fee schedule specific to

MOBILITY FEES How did we get here? ULI Report (2008): The County should conduct long-range concurrency studies for each of the five market areas linked to a defined concurrency fee schedule specific to

Economic and Fiscal Impact of the Arizona Public University Enterprise

Economic and Fiscal Impact of the Arizona Public Enterprise Prepared for: January 2019 Prepared by: and Elliott D. Pollack & Company 7505 East 6 th Avenue, Suite 100 Scottsdale, Arizona 85251 1300 E Missouri

Economic and Fiscal Impact of the Arizona Public Enterprise Prepared for: January 2019 Prepared by: and Elliott D. Pollack & Company 7505 East 6 th Avenue, Suite 100 Scottsdale, Arizona 85251 1300 E Missouri

8. CAPITAL IMPROVEMENT ELEMENT Goals, Objectives, and Policies

8. Goals, Objectives, and Policies GOAL 8-1: TO USE SOUND FISCAL POLICIES TO PROVIDE PUBLIC FACILITIES AND SERVICES CONCURRENT WITH DEVELOPMENT/REDEVELOPMENT IN ORDER TO ACHIEVE AND MAINTAIN ADOPTED STANDARDS

8. Goals, Objectives, and Policies GOAL 8-1: TO USE SOUND FISCAL POLICIES TO PROVIDE PUBLIC FACILITIES AND SERVICES CONCURRENT WITH DEVELOPMENT/REDEVELOPMENT IN ORDER TO ACHIEVE AND MAINTAIN ADOPTED STANDARDS

Cost Feasible Plan Technical Report TRANSPORTATION OUTLOOK 2035 OKALOOSA-WALTON 2035 LONG RANGE TRANSPORTATION PLAN UPDATE.

Cost Feasible Plan Technical Report TRANSPORTATION OUTLOOK 2035 OKALOOSA-WALTON 2035 LONG RANGE TRANSPORTATION PLAN UPDATE Prepared for the Okaloosa-Walton Transportation Planning Organization and The

Cost Feasible Plan Technical Report TRANSPORTATION OUTLOOK 2035 OKALOOSA-WALTON 2035 LONG RANGE TRANSPORTATION PLAN UPDATE Prepared for the Okaloosa-Walton Transportation Planning Organization and The

CAPITAL IMPROVEMENTS ELEMENT

GOALS, OBJECTIVES AND POLICIES Goal 1.0.0. To annually adopt and utilize a 5-Year Capital Improvements Program and Annual Capital Budget to coordinate the timing and to prioritize the construction and

GOALS, OBJECTIVES AND POLICIES Goal 1.0.0. To annually adopt and utilize a 5-Year Capital Improvements Program and Annual Capital Budget to coordinate the timing and to prioritize the construction and

LEVEL OF SERVICE / COST & REVENUE ASSUMPTIONS

LEVEL OF SERVICE / COST & REVENUE ASSUMPTIONS APPENDIX TO THE FISCAL IMPACT ANALYSIS OF PHASE I OF CAROLINA NORTH University of North Carolina-Chapel Hill Town of Chapel Hill, North Carolina Town of Carrboro,

LEVEL OF SERVICE / COST & REVENUE ASSUMPTIONS APPENDIX TO THE FISCAL IMPACT ANALYSIS OF PHASE I OF CAROLINA NORTH University of North Carolina-Chapel Hill Town of Chapel Hill, North Carolina Town of Carrboro,

This page intentionally blank. Capital Facilities Chapter Relationship to Vision. Capital Facilities Chapter Concepts

This page intentionally blank. Capital Facilities Chapter Relationship to Vision Vision County Government. County government that is accountable and accessible; encourages citizen participation; seeks

This page intentionally blank. Capital Facilities Chapter Relationship to Vision Vision County Government. County government that is accountable and accessible; encourages citizen participation; seeks

Chapter 9 Financial Considerations. 9.1 Introduction

9.1 Introduction Chapter 9 This chapter presents anticipated costs, revenues, and funding for the NEPA BART Extension Alternative. A summary of VTA s financial plan for the BART Extension Alternative is

9.1 Introduction Chapter 9 This chapter presents anticipated costs, revenues, and funding for the NEPA BART Extension Alternative. A summary of VTA s financial plan for the BART Extension Alternative is

FY 2010 FY 2019 Capital Funding

Capital Improvement Plan Overview Capital Improvement Plan The Capital Improvement Plan is a resource that assists Monroe County in ensuring that decisions on projects and funding are made wisely and in

Capital Improvement Plan Overview Capital Improvement Plan The Capital Improvement Plan is a resource that assists Monroe County in ensuring that decisions on projects and funding are made wisely and in

LEGEND Bridges Parks Fire Stations Project Locations Libraries Schools A

LEGEND Bridges Parks Fire Stations Project Locations Libraries Schools A Aid to Construction Fund The Aid to Construction Fund (Water) are funds received from customers for requested water service and

LEGEND Bridges Parks Fire Stations Project Locations Libraries Schools A Aid to Construction Fund The Aid to Construction Fund (Water) are funds received from customers for requested water service and

Hillsborough County Population and Employment Projections and Allocations DECEMBER 2017

Hillsborough County Population and Employment Projections and Allocations DECEMBER 2017 Presentation Overview Overview of the Allocation Process Population and Employment Projections Trend Analysis 2045

Hillsborough County Population and Employment Projections and Allocations DECEMBER 2017 Presentation Overview Overview of the Allocation Process Population and Employment Projections Trend Analysis 2045

Transportation Funding

Transportation Funding TABLE OF CONTENTS Introduction... 3 Background... 3 Current Transportation Funding... 4 Funding Sources... 4 Expenditures... 5 Case Studies... 6 Washington, D.C... 6 Chicago... 8

Transportation Funding TABLE OF CONTENTS Introduction... 3 Background... 3 Current Transportation Funding... 4 Funding Sources... 4 Expenditures... 5 Case Studies... 6 Washington, D.C... 6 Chicago... 8

Contents. Alamo Area Metropolitan Planning Organization. Introduction S. St. Mary s Street San Antonio, Texas 78205

Contents Introduction 1 Alamo Area Metropolitan Planning Organization Tel 210.227.8651 Fax 210.227.9321 825 S. St. Mary s Street San Antonio, Texas 78205 www.alamoareampo.org aampo@alamoareampo.org Pg.

Contents Introduction 1 Alamo Area Metropolitan Planning Organization Tel 210.227.8651 Fax 210.227.9321 825 S. St. Mary s Street San Antonio, Texas 78205 www.alamoareampo.org aampo@alamoareampo.org Pg.

Local Government Division

2014 Local Government Division ILLINOIS STATE COMPTROLLER LESLIE GEISSLER MUNGER WELCOME LETTERfrom THE COMPTROLLER Illinois State Comptroller Leslie Geissler Munger To the Honorable Members of the General

2014 Local Government Division ILLINOIS STATE COMPTROLLER LESLIE GEISSLER MUNGER WELCOME LETTERfrom THE COMPTROLLER Illinois State Comptroller Leslie Geissler Munger To the Honorable Members of the General

Financial Forecasting Assumptions for Plan 2040 (DRAFT)

") Financial Forecasting Assumptions for Plan 2040 (DRAFT) Inflation and Long Range Cost Escalation For the FY 2012 2017 TIP period, ARC will use the GDOT recommended 4 percent inflation rate. This conservative

Financial Forecasting Assumptions for Plan 2040 (DRAFT) Inflation and Long Range Cost Escalation For the FY 2012 2017 TIP period, ARC will use the GDOT recommended 4 percent inflation rate. This conservative

Okaloosa-Walton 2035 Long Range Transportation Plan Amendment

Okaloosa-Walton 2035 Long Range Transportation Plan Amendment Adopted August 22, 2013 This report was financed in part by the U.S. Department of Transportation, Federal Highway Administration, the Florida

Okaloosa-Walton 2035 Long Range Transportation Plan Amendment Adopted August 22, 2013 This report was financed in part by the U.S. Department of Transportation, Federal Highway Administration, the Florida

FY 2005 FISCAL RESPONSIBILITY REPORT CARD EXECUTIVE SUMMARY

FY 2005 FISCAL RESPONSIBILITY REPORT CARD EXECUTIVE SUMMARY 2 December 15, 2006 Honorable Members of the General Assembly and County Clerks: Pursuant to the Fiscal Responsibility Report Card Act [35 ILCS

FY 2005 FISCAL RESPONSIBILITY REPORT CARD EXECUTIVE SUMMARY 2 December 15, 2006 Honorable Members of the General Assembly and County Clerks: Pursuant to the Fiscal Responsibility Report Card Act [35 ILCS

2040 Long Range Transportation Plan - Needs Assessment: System Preservation Pavement, Bridges, and Transit Costs and Benefits

2040 Long Range Transportation Plan - Needs Assessment: System Preservation Pavement, Bridges, and Transit Costs and Benefits Prepared For: 601 East Kennedy Boulevard Tampa, FL 33602 Prepared by: Jacobs

2040 Long Range Transportation Plan - Needs Assessment: System Preservation Pavement, Bridges, and Transit Costs and Benefits Prepared For: 601 East Kennedy Boulevard Tampa, FL 33602 Prepared by: Jacobs

OHIO MPO AND LARGE CITY CAPITAL PROGRAM SFY 2015 SUMMARY

OHIO MPO AND LARGE CITY CAPITAL PROGRAM SFY 2015 SUMMARY TABLE OF CONTENTS MPO AND LARGE CITY PROGRAM OVERVIEW.. 3 MPO AND LARGE CITY SFY 2015 STP BUDGET SUMMARY......... 4 MPO AND LARGE CITY SFY 2015

OHIO MPO AND LARGE CITY CAPITAL PROGRAM SFY 2015 SUMMARY TABLE OF CONTENTS MPO AND LARGE CITY PROGRAM OVERVIEW.. 3 MPO AND LARGE CITY SFY 2015 STP BUDGET SUMMARY......... 4 MPO AND LARGE CITY SFY 2015

CAPITAL IMPROVEMENTS ELEMENT

[COMPREHENSIVE PLAN] 2025 INTRODUCTION EXHIBIT F CAPITAL IMPROVEMENTS ELEMENT A primary purpose of the Capital Improvements Element (CIE) is to assess and demonstrate the financial feasibility of the Clay

[COMPREHENSIVE PLAN] 2025 INTRODUCTION EXHIBIT F CAPITAL IMPROVEMENTS ELEMENT A primary purpose of the Capital Improvements Element (CIE) is to assess and demonstrate the financial feasibility of the Clay

GENERAL FUND Revenues

GENERAL FUND Revenues The General Fund is used to account for general purpose revenues, which are used to fund general governmental services, excluding utilities. Following are descriptions of the City's

GENERAL FUND Revenues The General Fund is used to account for general purpose revenues, which are used to fund general governmental services, excluding utilities. Following are descriptions of the City's

Transportation Funding and Improving Roadway Services Delivery

Transportation Funding and Improving Roadway Services Delivery Transportation Advisory Commission October 5, 2010 1 STUDY PROGRESS Finalize project scope, perform initial data collection, and gather input

Transportation Funding and Improving Roadway Services Delivery Transportation Advisory Commission October 5, 2010 1 STUDY PROGRESS Finalize project scope, perform initial data collection, and gather input

TAUSSIG DEVELOPMENT IMPACT FEE JUSTIFICATION STUDY CITY OF ESCALON. Public Finance Public Private Partnerships Urban Economics Clean Energy Bonds

DAVID TAUSSIG & ASSOCIATES, INC. DEVELOPMENT IMPACT FEE JUSTIFICATION STUDY CITY OF ESCALON B. C. SEPTEMBER 12, 2016 Public Finance Public Private Partnerships Urban Economics Clean Energy Bonds Prepared

DAVID TAUSSIG & ASSOCIATES, INC. DEVELOPMENT IMPACT FEE JUSTIFICATION STUDY CITY OF ESCALON B. C. SEPTEMBER 12, 2016 Public Finance Public Private Partnerships Urban Economics Clean Energy Bonds Prepared

Florida Legislative Committee on Intergovernmental Relations

Jeff Atwater President Florida Legislative Committee on Intergovernmental Relations Issue Brief Utilization of Local Option Sales Taxes by Florida Counties in Fiscal Year 2009-10 November 2009 Larry Cretul

Jeff Atwater President Florida Legislative Committee on Intergovernmental Relations Issue Brief Utilization of Local Option Sales Taxes by Florida Counties in Fiscal Year 2009-10 November 2009 Larry Cretul

Mobility Fee Legislation

Mobility Fee Legislation The Joint Report contains three recommended legislative options for mobility fees: 1. Require mobility fees statewide by a date certain 2. Require mobility fees in DULA counties

Mobility Fee Legislation The Joint Report contains three recommended legislative options for mobility fees: 1. Require mobility fees statewide by a date certain 2. Require mobility fees in DULA counties

City Services Appendix

Technical vices 1.0 Introduction... 1 1.1 The Capital Facilities Plan... 1 1.2 Utilities Plan... 2 1.3 Key Principles Guiding Bremerton s Capital Investments... 3 1.4 Capital Facilities and Utilities Addressed

Technical vices 1.0 Introduction... 1 1.1 The Capital Facilities Plan... 1 1.2 Utilities Plan... 2 1.3 Key Principles Guiding Bremerton s Capital Investments... 3 1.4 Capital Facilities and Utilities Addressed

CITY OF BREVARD

ANNUAL BUDGET ESTIMATE - REVENUE Amended - 2018-2019 CITY OF BREVARD FY 2017-2018 2016-2017 2017-2018 4/30/2018 2017-2018 2018-2019 Account Actual ($) Budget ($) Actual ($) Estimate %Remaining Requested

ANNUAL BUDGET ESTIMATE - REVENUE Amended - 2018-2019 CITY OF BREVARD FY 2017-2018 2016-2017 2017-2018 4/30/2018 2017-2018 2018-2019 Account Actual ($) Budget ($) Actual ($) Estimate %Remaining Requested

Chapter 4: Regional Transportation Finance

4.1 Chapter 4: Regional Transportation Finance 2040 4.2 CONTENTS Chapter 4: Transportation Finance Overview 4.3 Two Funding Scenarios 4.4 Current Revenue Scenario Assumptions 4.5 State Highway Revenues

4.1 Chapter 4: Regional Transportation Finance 2040 4.2 CONTENTS Chapter 4: Transportation Finance Overview 4.3 Two Funding Scenarios 4.4 Current Revenue Scenario Assumptions 4.5 State Highway Revenues

Strengthening Vermont s Economy by Integrating Transportation and Smart Growth Policy

Strengthening Vermont s Economy by Integrating Transportation and Smart Growth Policy Technical Memorandum #4: Short List of Recommended Alternatives May 21, 2013 Tech Memo #4: Short List of Recommended

Strengthening Vermont s Economy by Integrating Transportation and Smart Growth Policy Technical Memorandum #4: Short List of Recommended Alternatives May 21, 2013 Tech Memo #4: Short List of Recommended