An Analysis of a Regressive Budget

|

|

|

- Constance Lewis

- 5 years ago

- Views:

Transcription

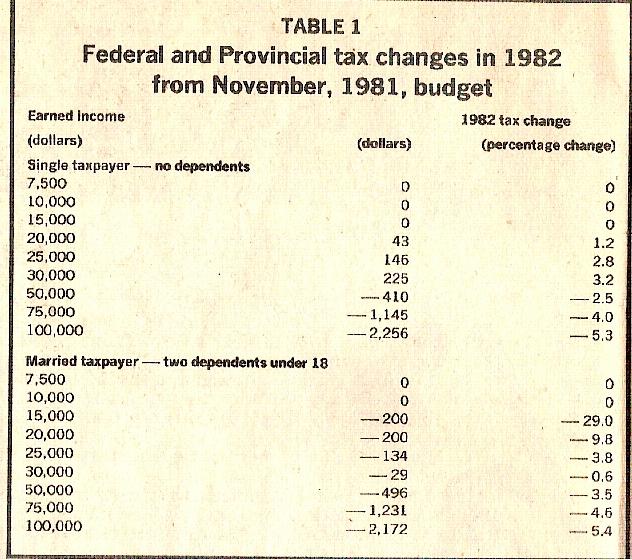

1 Patrick Grady Globe and Mail November 30, 1981 An Analysis of a Regressive Budget THE November 1981, budget was the federal Government's first and last major effort at tax reform since the Benson Iceberg of It marked a serious attempt to make the tax system more equitable. The approach was to reduce the top marginal rates to give a greater incentive to work, save and invest, while at the same time financing the reduction and making the tax system fairer by eliminating many tax preferences. Unfortunately for the success of this bold exercise, the tax measures introduced exhibited a number of technical flaws. This was inevitable given the great difficulty of designing detailed tax changes in secret without taxpayer feedback. The budget's technical flaws contributed to its undoing. But it was more than this. Business groups, trade associations and tax practitioners supported by the financial press used the technical problems as ammunition in mounting a concentrated attack on the fundamental philosophy of the budget. The result was a restoration of many of the tax preferences, which, combined with the reduction in the top marginal rates, served to undermine the progressivity of the tax system. This is demonstrated in Table 1, which shows the impact of the November, 1981, budget measures for typical taxpayers in The lesson of the November, 1981 budget was not lost on the Government. Consultations with the private sector on tax changes became the order of the day. A green paper on the budget process extolling the virtues, of consultations was released in April, Consultations were engaged in before the June, 1982, budget and the October economic and financial statement. A white paper containing proposals for indexed deposits and loans and an Indexed Securities Investment Plan was published and a committee headed by Pierre Lortie was set up to study the proposals. The most ambitious pre-budget process of consultations; was undertaken by. Finance Minister Marc Lalonde before his April 19 budget. These consultations paid off for business groups which participated. Besides calling for expanded business tax incentives, they urged the Government to reduce the deficit. In his budget, the minister responded to these two seemingly contradictory concerns by raising taxes on everybody but business by more than enough to reduce the deficit by the desired amount, thus leaving enough money to finance new corporate tax breaks.

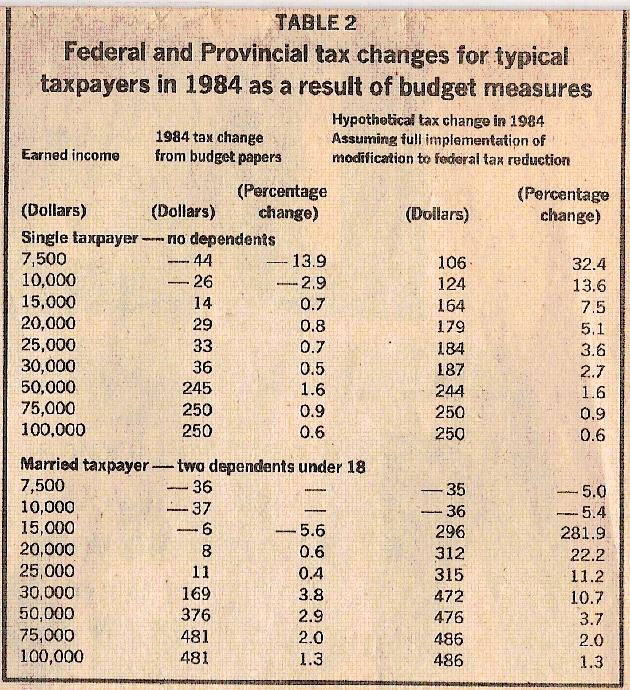

2 By , net tax increases included in the budget amount to $3 billion and corporate tax cuts $815-million. The burden of this tax bill falls on the ordinary taxpayer through increased personal income and sales taxes and the retention of the Canadian Owner ship Charge. In contrast, business groups were rewarded by the implementation of several of their key recommendations. These include, most notably: the Indexed Security Investment Plan, the extended carry-back and carry-forward of business losses, and the proposal for a larger tax credit for research and development The ones hardest hit by the budget are low and middle income working Canadians. The largest proportionate share of the budget's personal income tax increases will be paid by this group. The fact is carefully camouflaged in the budget papers, which contain a table showing the progressive impact of the budget's personal-income tax measures. The table, part of which is shown as the right panel in Table 2, is correct as far as it goes, but is misleading as an indicator of the budget's impact by income class. The largest single personal income tax increase announced in the budget is the modification f to the federal tax reduction of $200. In 1984, this tax reduction will be phased out for higher income individuals with the federal tax reduction diminished by 10 per cent of basic federal tax in excess of $6,000, This is estimated to raise $455 million in In the left panel of Table 2 this measure accounts for $200 of the total tax, increases for single taxpayers in the top two income groups and for $400 of the total tax increases for married taxpayers in the same group. While in 1984 the phasing down of the federal tax reduction affects only upper income taxpayers, as shown in the left panel of Table 2, in 1985 the tax reduction is decreased to $100, and in 1985 and subsequent years the tax reduction is decreased to $50. The decrease in the reduction touches lower and middle income taxpayers. This is not shown in the left panel of Table 2, since it does not occur until However, the budget table on revenue impact indicates that this measure alone will raise $2.1 billion in or almost four times the figure. It more than accounts for the budget's net personal income tax increase in A better indication of the impact of the budget measures at different income levels is provided in the right panel of Table 2. It shows the hypothetical tax change that would occur in 1984 assuming the full phasing down of the federal tax reduction to $50, which is scheduled for As can be seen, the budget raises taxes proportionately much more for low and middle income earners, particularly for single taxpayers with no dependents. The actual budget impact is even more regressive than suggested by the adjusted figures. Another measure which is not fully reflected in the budget table is the maintenance of the

3 family income threshold for the child tax credit. This weighs disproportionately on the middle income married taxpayer with children. Eventually, assuming the continuation of inflation, it will result in the elimination of the child tax credit for all those with the lowest real incomes. The budget table is also deceptive because it treats the repeal of the $100 standard deduction the same way it would treat an exemption. This creates, the impression that the, budget changes bear more heavily on upper income taxpayers than is actually the case. In fact, only lower and middle income earners use the standard deduction. Upper income individuals almost always itemize their charitable donations and medical expenses. The only conclusion that can be drawn from an analysis of the budget's personal income tax measures is that they are regressive. This reinforces other regressive elements, such as the sales tax increase and business tax incentives, and comes on top of large increases in unemployment insurance contributions announced in October. It represents a further movement in the direction of.a less progressive tax structure. Almost a year and a half afterward, the reaction to the November, 1981 budget continues. There is a fundamental issue at stake here which cuts to the heart of politics in a democratic state. It is who has influence over the budget. The Government tried tax reform prepared under the cloak of budgetary secrecy and was forced to retreat in the face of powerful opposition mobilized by business groups. Opening up the budget process. and engaging in more extensive consultations was seen as a way of. maximizing input before the event and thus avoiding the repetition of another November budget. This in itself is a good thing. The problem is to ensure that all points of view are given equal consideration. This was not the case in the budget. The most numerous and best prepared pre-budget submissions came from the business community. In contrast, except for the Canadian Labor Congress's brief, which was good and recommended tax cuts for low and middle income earners to stimulate the economy, the quality of the briefs from labor was low and devoid of constructive suggestions. Public interest groups, with the exception of the Canadian Council on Social Development, did not submit detailed briefs. Against this backdrop, it is understandable why the budget is pro-business and decreases the progressivity of the tax system. A way must be found to get a broader degree of public participation in the budget process. Public interest groups, economic research organizations and other concerned citizens must take a more active role. Otherwise, budgets will continue to reflect business input.

4

5

U.S. House of Representatives COMMITTEE ON WAYS AND MEANS

U.S. House of Representatives COMMITTEE ON WAYS AND MEANS The TAX CUTS & JOBS ACT CHARGE & RESPONSE Americans have been waiting for years for Washington to fix this broken tax code because they know it

U.S. House of Representatives COMMITTEE ON WAYS AND MEANS The TAX CUTS & JOBS ACT CHARGE & RESPONSE Americans have been waiting for years for Washington to fix this broken tax code because they know it

Would the Senate Democrats proposed excise tax on highcost employer-paid health insurance benefits be progressive?

Citizens for Tax Justice December 11, 2009 Would the Senate Democrats proposed excise tax on highcost employer-paid health insurance benefits be progressive? Summary Senate Democrats have proposed a new,

Citizens for Tax Justice December 11, 2009 Would the Senate Democrats proposed excise tax on highcost employer-paid health insurance benefits be progressive? Summary Senate Democrats have proposed a new,

POLICY REPORT The Iowa Policy Project

POLICY REPORT The Iowa Policy Project Child & Family Policy Center April 2003 The Merits of a Cigarette Tax, With Alternative Tax Offsets By Charles Bruner and Peter S. Fisher Driven partly by state budget

POLICY REPORT The Iowa Policy Project Child & Family Policy Center April 2003 The Merits of a Cigarette Tax, With Alternative Tax Offsets By Charles Bruner and Peter S. Fisher Driven partly by state budget

The Debate over Expiring Tax Cuts: What about the Deficit? Adam Looney*

The Debate over Expiring Tax Cuts: What about the Deficit? Adam Looney* As the economy begins to recover from the Great Recession, policymakers must confront the next fiscal challenge: the long-run federal

The Debate over Expiring Tax Cuts: What about the Deficit? Adam Looney* As the economy begins to recover from the Great Recession, policymakers must confront the next fiscal challenge: the long-run federal

Res HJ13. iget. Bud1. '9c In-brief. Complime ts. of. June CAPITAL BRIEFIlla. Canada.

Res HJ13 '9c 1982 Bud1 iget In-brief June 1982 Complime ts. of CAPITAL BRIEFIlla Canada. "Solidarity and sharing built Canada. That sharing is what the unemployed, the many firms in trouble, and the thousands

Res HJ13 '9c 1982 Bud1 iget In-brief June 1982 Complime ts. of CAPITAL BRIEFIlla Canada. "Solidarity and sharing built Canada. That sharing is what the unemployed, the many firms in trouble, and the thousands

Federal Income Taxes: Who Pays and How Much. By Peter Ferrara August 14, 2008

Federal Income Taxes: Who Pays and How Much By Peter Ferrara August 14, 2008 The Internal Revenue Service recently released official data on the payment of income taxes by different income groups, compiled

Federal Income Taxes: Who Pays and How Much By Peter Ferrara August 14, 2008 The Internal Revenue Service recently released official data on the payment of income taxes by different income groups, compiled

The Canada Pension Plan Where Next?

The Canada Pension Plan Where Next? Saskatchewan Federation of Labour Pensions Conference Regina, Saskatchewan May 2, 2018 Chris Roberts Canadian Labour Congress Outline Summary of 2016 CPP enhancement

The Canada Pension Plan Where Next? Saskatchewan Federation of Labour Pensions Conference Regina, Saskatchewan May 2, 2018 Chris Roberts Canadian Labour Congress Outline Summary of 2016 CPP enhancement

Canadian Budget Delivers Outbound Tax Relief

Volume 53, Number 5 February 2, 2009 Canadian Budget Delivers Outbound Tax Relief by Steve Suarez Canadian Budget Delivers Outbound Tax Relief by Steve Suarez Canadian Finance Minister Jim Flaherty on

Volume 53, Number 5 February 2, 2009 Canadian Budget Delivers Outbound Tax Relief by Steve Suarez Canadian Budget Delivers Outbound Tax Relief by Steve Suarez Canadian Finance Minister Jim Flaherty on

I S S U E B R I E F PUBLIC POLICY INSTITUTE PPI PRESIDENT BUSH S TAX PLAN: IMPACTS ON AGE AND INCOME GROUPS

PPI PUBLIC POLICY INSTITUTE PRESIDENT BUSH S TAX PLAN: IMPACTS ON AGE AND INCOME GROUPS I S S U E B R I E F Introduction President George W. Bush fulfilled a 2000 campaign promise by signing the $1.35

PPI PUBLIC POLICY INSTITUTE PRESIDENT BUSH S TAX PLAN: IMPACTS ON AGE AND INCOME GROUPS I S S U E B R I E F Introduction President George W. Bush fulfilled a 2000 campaign promise by signing the $1.35

HOW THE TAX REFORM OF 1986 SUPERCHARGED THE AMERICAN ECONOMY

HOW THE TAX REFORM OF 1986 SUPERCHARGED THE AMERICAN ECONOMY By Marc Kilmer 12/20/14 In 1986, something remarkable happened: President Ronald Reagan and members of Congress from both parties came together

HOW THE TAX REFORM OF 1986 SUPERCHARGED THE AMERICAN ECONOMY By Marc Kilmer 12/20/14 In 1986, something remarkable happened: President Ronald Reagan and members of Congress from both parties came together

The U.S. Tax Cut and Jobs Act

The U.S. Tax Cut and Jobs Act A Brief Economic Analysis Joshua Greene Visiting Professor SMU Research Seminar, Feb. 9, 2018 Presentation Outline Main provisions of the Act Estimated distributional impact

The U.S. Tax Cut and Jobs Act A Brief Economic Analysis Joshua Greene Visiting Professor SMU Research Seminar, Feb. 9, 2018 Presentation Outline Main provisions of the Act Estimated distributional impact

The Debate over Expiring Tax Cuts: What about the Deficit? Adam Looney

The Debate over Expiring Tax Cuts: What about the Deficit? Adam Looney As the economy begins to recover from the Great Recession, policymakers must confront the next fiscal challenge: the long-run federal

The Debate over Expiring Tax Cuts: What about the Deficit? Adam Looney As the economy begins to recover from the Great Recession, policymakers must confront the next fiscal challenge: the long-run federal

A Fair Way to Limit Tax Deductions

REPORT NOVEMBER 2018 A Fair Way to Limit Tax Deductions STEVE WAMHOFF and CARL DAVIS Download state-by-state data on each option presented in this report The cap on federal tax deductions for state and

REPORT NOVEMBER 2018 A Fair Way to Limit Tax Deductions STEVE WAMHOFF and CARL DAVIS Download state-by-state data on each option presented in this report The cap on federal tax deductions for state and

FASB Looks to. Leslie F. Seidman, FASB Chair. Annual Tax Update Marriage and Taxes Estate Tax Portability Tax Preferences for Education

www.cpaj.com December 2011 FASB Looks to the Future Leslie F. Seidman, FASB Chair Annual Tax Update Marriage and Taxes Estate Tax Portability Tax Preferences for Education T A X A T I O N federal taxation

www.cpaj.com December 2011 FASB Looks to the Future Leslie F. Seidman, FASB Chair Annual Tax Update Marriage and Taxes Estate Tax Portability Tax Preferences for Education T A X A T I O N federal taxation

Who Pays? The Unfairness of Connecticut s State and Local Tax System

Who Pays? The Unfairness of Connecticut s State and Local Tax System Douglas Hall, Ph.D. April 2009 This report is produced with the support of the Stoneman Family Foundation and the Melville Charitable

Who Pays? The Unfairness of Connecticut s State and Local Tax System Douglas Hall, Ph.D. April 2009 This report is produced with the support of the Stoneman Family Foundation and the Melville Charitable

Regressing Towards Proportionality: Personal Income Tax Reform in New Brunswick

Regressing Towards Proportionality: Personal Income Tax Reform in New Brunswick by Joe Ruggeri and Jean-Philippe Bourgeois March 21 Regressing Towards Proportionality: Personal Income Tax Reform in New

Regressing Towards Proportionality: Personal Income Tax Reform in New Brunswick by Joe Ruggeri and Jean-Philippe Bourgeois March 21 Regressing Towards Proportionality: Personal Income Tax Reform in New

Tax Cut by Income Group, Fully Phased-In

Testimony of Michael P. Ettlinger, Tax Policy Director, The Institute on Taxation and Economic Policy, before the Rhode Island Senate Select Committee. October 7, 1999 Analysis of Proposed Tax Cut Good

Testimony of Michael P. Ettlinger, Tax Policy Director, The Institute on Taxation and Economic Policy, before the Rhode Island Senate Select Committee. October 7, 1999 Analysis of Proposed Tax Cut Good

EVIDENCE ON INEQUALITY AND THE NEED FOR A MORE PROGRESSIVE TAX SYSTEM

EVIDENCE ON INEQUALITY AND THE NEED FOR A MORE PROGRESSIVE TAX SYSTEM Revenue Summit 17 October 2018 The Australia Institute Patricia Apps The University of Sydney Law School, ANU, UTS and IZA ABSTRACT

EVIDENCE ON INEQUALITY AND THE NEED FOR A MORE PROGRESSIVE TAX SYSTEM Revenue Summit 17 October 2018 The Australia Institute Patricia Apps The University of Sydney Law School, ANU, UTS and IZA ABSTRACT

Progressive Community and Interested Parties. John Podesta, Cassandra Butts and John Halpin. Date: February 14, 2005

To: From: Progressive Community and Interested Parties John Podesta, Cassandra Butts and John Halpin Date: February 14, 2005 Subject: Progressive Message on the President s Budget The president s budget

To: From: Progressive Community and Interested Parties John Podesta, Cassandra Butts and John Halpin Date: February 14, 2005 Subject: Progressive Message on the President s Budget The president s budget

Poverty Alliance Briefing 23

Poverty Alliance Briefing 23 Devolved Taxation in Scotland Introduction The Scottish Government has increasing powers to vary tax rates in Scotland. In addition to having full control over local property

Poverty Alliance Briefing 23 Devolved Taxation in Scotland Introduction The Scottish Government has increasing powers to vary tax rates in Scotland. In addition to having full control over local property

THE CHANCELLOR S CHOICES

BUDGET 212 BRIEFING AN ECONOMIC STIMULUS FOR THE UK THE CHANCELLOR S CHOICES Kayte Lawton March 212 IPPR 212 Institute for Public Policy Research ABOUT THE AUTHOR Kayte Lawton is a senior research fellow

BUDGET 212 BRIEFING AN ECONOMIC STIMULUS FOR THE UK THE CHANCELLOR S CHOICES Kayte Lawton March 212 IPPR 212 Institute for Public Policy Research ABOUT THE AUTHOR Kayte Lawton is a senior research fellow

Taxation-Overview (Chapter 18)

") (Chapter 18) So far, we have talked about different government expenditure items: Education Social Security Health insurance Welfare programs How does local and federal governments finance such programs?

(Chapter 18) So far, we have talked about different government expenditure items: Education Social Security Health insurance Welfare programs How does local and federal governments finance such programs?

PRELIMINARY ANALYSIS OF THE FAMILY FAIRNESS AND OPPORTUNITY TAX REFORM ACT

PRELIMINARY ANALYSIS OF THE FAMILY FAIRNESS AND OPPORTUNITY TAX REFORM ACT Len Burman, Elaine Maag, Georgia Ivsin, and Jeff Rohaly 1 Urban-Brookings Tax Policy Center March 4, 2014 On October 30, 2013,

PRELIMINARY ANALYSIS OF THE FAMILY FAIRNESS AND OPPORTUNITY TAX REFORM ACT Len Burman, Elaine Maag, Georgia Ivsin, and Jeff Rohaly 1 Urban-Brookings Tax Policy Center March 4, 2014 On October 30, 2013,

The Child and Dependent Care Credit: Impact of Selected Policy Options

The Child and Dependent Care Credit: Impact of Selected Policy Options Margot L. Crandall-Hollick Specialist in Public Finance Gene Falk Specialist in Social Policy December 5, 2017 Congressional Research

The Child and Dependent Care Credit: Impact of Selected Policy Options Margot L. Crandall-Hollick Specialist in Public Finance Gene Falk Specialist in Social Policy December 5, 2017 Congressional Research

New Analysis Finds GOP Tax Plan would Give Richest One Percent of CT Residents $125,380 More Per Year on Average than Obama s Approach

NEWS RELEASE FOR IMMEDIATE RELEASE Wednesday, June 20, 2012 33 Whitney Avenue New Haven, CT 06510 Voice: 203-498-4240 Fax: 203-498-4242 www.ctvoices.org Contact: Wade Gibson, Senior Policy Fellow, CT Voices

NEWS RELEASE FOR IMMEDIATE RELEASE Wednesday, June 20, 2012 33 Whitney Avenue New Haven, CT 06510 Voice: 203-498-4240 Fax: 203-498-4242 www.ctvoices.org Contact: Wade Gibson, Senior Policy Fellow, CT Voices

Conservative manifesto tax policy and Universal Credit

Conservative manifesto tax policy and Universal Credit Introduction At the Conservative party conference in October 2014, the Prime Minister David Cameron committed his party to two important income tax

Conservative manifesto tax policy and Universal Credit Introduction At the Conservative party conference in October 2014, the Prime Minister David Cameron committed his party to two important income tax

The Coalition s Policy to Lower Company Tax

1 Our Plan Real Solutions for all Australians The direction, values and policy priorities of the next Coalition Government. The Coalition s Policy to Lower Company Tax August 2013 Our Plan s Real Solution

1 Our Plan Real Solutions for all Australians The direction, values and policy priorities of the next Coalition Government. The Coalition s Policy to Lower Company Tax August 2013 Our Plan s Real Solution

North Carolina Justice Center Opportunity and Prosperity for All THE FUTURE IS NOW: A Plan to Modernize North Carolina s Revenue System.

North Carolina Justice Center Opportunity and Prosperity for All THE FUTURE IS NOW: A Plan to Modernize North Carolina s Revenue System February 2011 Revenue Plan Goals Protect effective public investments

North Carolina Justice Center Opportunity and Prosperity for All THE FUTURE IS NOW: A Plan to Modernize North Carolina s Revenue System February 2011 Revenue Plan Goals Protect effective public investments

Five Easy Pieces Scorecard

Five Easy Pieces Scorecard John S. Irons, Ph.D. October 19, 2005 As journalists like Nicholas Confessore and Jonathan Chait have recounted, conservatives seeking to shift America away from progressive

Five Easy Pieces Scorecard John S. Irons, Ph.D. October 19, 2005 As journalists like Nicholas Confessore and Jonathan Chait have recounted, conservatives seeking to shift America away from progressive

Women s Budget Group Pre-Budget Briefing, March 2012

Women s Budget Group Pre-Budget Briefing, March 2012 Plan A has failed. It is time for Plan F: a feminist economic strategy to stimulate social and economic recovery. Austerity measures are damaging women,

Women s Budget Group Pre-Budget Briefing, March 2012 Plan A has failed. It is time for Plan F: a feminist economic strategy to stimulate social and economic recovery. Austerity measures are damaging women,

SOCIAL WELFARE STRATEGY

SOCIAL WELFARE STRATEGY ACTU Congress September 1989 1. INTRODUCTION 1.1 The post 1983 Accord Process has enabled the union movement, through participation in government, to play a significant role in

SOCIAL WELFARE STRATEGY ACTU Congress September 1989 1. INTRODUCTION 1.1 The post 1983 Accord Process has enabled the union movement, through participation in government, to play a significant role in

xiii Executive Summary

Executive Summary President George W. Bush created the President s Advisory Panel on Federal Tax Reform in January 2005. The President instructed the Panel to recommend options that would make the tax

Executive Summary President George W. Bush created the President s Advisory Panel on Federal Tax Reform in January 2005. The President instructed the Panel to recommend options that would make the tax

V. MAKING WORK PAY. The economic situation of persons with low skills

V. MAKING WORK PAY There has recently been increased interest in policies that subsidise work at low pay in order to make work pay. 1 Such policies operate either by reducing employers cost of employing

V. MAKING WORK PAY There has recently been increased interest in policies that subsidise work at low pay in order to make work pay. 1 Such policies operate either by reducing employers cost of employing

Social Security Its Problems and How to Solve Them

Social Security Its Problems and How to Solve Them Currently social security is running a cash surplus. The surplus will grow smaller when the baby boomers begin to retire, and it will turn into a cash

Social Security Its Problems and How to Solve Them Currently social security is running a cash surplus. The surplus will grow smaller when the baby boomers begin to retire, and it will turn into a cash

The Child Tax Credit: Current Law and Legislative History

The Child Tax Credit: Current Law and Legislative History Margot L. Crandall-Hollick Analyst in Public Finance January 19, 2016 Congressional Research Service 7-5700 www.crs.gov R41873 Summary This report

The Child Tax Credit: Current Law and Legislative History Margot L. Crandall-Hollick Analyst in Public Finance January 19, 2016 Congressional Research Service 7-5700 www.crs.gov R41873 Summary This report

FEDERAL TAX REFORM AND THE STATES

FEDERAL TAX REFORM AND THE STATES Harley Duncan Sally Wallace August 12, 2013 Got conformity? Corporate and individual income taxes come in all shapes and sizes conformity does as well VERY simple look

FEDERAL TAX REFORM AND THE STATES Harley Duncan Sally Wallace August 12, 2013 Got conformity? Corporate and individual income taxes come in all shapes and sizes conformity does as well VERY simple look

Budget. Reducing Income Tax

2004-2005 Budget Reducing Income Tax 2004-2005 Budget Reducing Income Tax ISBN 2-550-42379-8 Legal deposit Bibliothèque nationale du Québec, 2004 Publication date: March 2004 Gouvernement du Québec, 2004

2004-2005 Budget Reducing Income Tax 2004-2005 Budget Reducing Income Tax ISBN 2-550-42379-8 Legal deposit Bibliothèque nationale du Québec, 2004 Publication date: March 2004 Gouvernement du Québec, 2004

14-1: How Taxes Work NOTES

14-1: How Taxes Work NOTES Learning Target 1. I will demonstrate my understanding of the different types of taxes and what tax revenue is used for. Government Revenue Tax: a mandatory payment to a local,

14-1: How Taxes Work NOTES Learning Target 1. I will demonstrate my understanding of the different types of taxes and what tax revenue is used for. Government Revenue Tax: a mandatory payment to a local,

The Danish labour market System 1. European Commissions report 2002 on Denmark

Arbejdsmarkedsudvalget AMU alm. del - Bilag 95 Offentligt 1 The Danish labour market System 1. European Commissions report 2002 on Denmark In 2002 the EU Commission made a joint report on adequate and

Arbejdsmarkedsudvalget AMU alm. del - Bilag 95 Offentligt 1 The Danish labour market System 1. European Commissions report 2002 on Denmark In 2002 the EU Commission made a joint report on adequate and

IFA Submission to Government on Reform of PRSI, Levies and Income Tax System

IFA Submission to Government on Reform of, Levies and System April 2010 1 Table of Contents 1 INTRODUCTION BUDGET 2010 STATEMENT ON REFORM OF INCOME TAX...3 1.1 IFA S STRATEGY ON REFORM OF THE METHOD OF

IFA Submission to Government on Reform of, Levies and System April 2010 1 Table of Contents 1 INTRODUCTION BUDGET 2010 STATEMENT ON REFORM OF INCOME TAX...3 1.1 IFA S STRATEGY ON REFORM OF THE METHOD OF

Preliminary Details and Analysis of the Senate s 2017 Tax Cuts and Jobs Act

SPECIAL REPORT No. 240 Nov. 2017 Preliminary Details and Analysis of the Senate s 2017 Tax Cuts and Jobs Act Tax Foundation Staff Key Findings The Senate s version of the Tax Cuts and Jobs Act would reform

SPECIAL REPORT No. 240 Nov. 2017 Preliminary Details and Analysis of the Senate s 2017 Tax Cuts and Jobs Act Tax Foundation Staff Key Findings The Senate s version of the Tax Cuts and Jobs Act would reform

What Works, Why and at What Cost? Tax Credits and Capital Gains Strategies

MODERNISING CHARITY LAW CONFERENCE Australia April 26 to April 18, 2009 What Works, Why and at What Cost? Tax Credits and Capital Gains Strategies By Terrance S. Carter, B.A., LL.B., Trade-mark Agent 2009

MODERNISING CHARITY LAW CONFERENCE Australia April 26 to April 18, 2009 What Works, Why and at What Cost? Tax Credits and Capital Gains Strategies By Terrance S. Carter, B.A., LL.B., Trade-mark Agent 2009

AP Microeconomics Chapter 16 Outline

I. Learning objectives In this chapter students should learn: A. The main categories of government spending and the main sources of government revenue. B. The different philosophies regarding the distribution

I. Learning objectives In this chapter students should learn: A. The main categories of government spending and the main sources of government revenue. B. The different philosophies regarding the distribution

Capping Pensions Tax Relief

Capping Pensions Tax Relief An Overview of Proposals Considered by the Taxation Policy (Pensions) Group Patrick Burke Background Establishment and Composition of the Taxation Policy (Pensions) Group Requirement

Capping Pensions Tax Relief An Overview of Proposals Considered by the Taxation Policy (Pensions) Group Patrick Burke Background Establishment and Composition of the Taxation Policy (Pensions) Group Requirement

Trend Analysis of Changes to Population and Income in Philadelphia, using American Community Survey (ACS) Data

Data") OFFICE OF THE PRESIDENT FINANCE AND BUDGET TEAM City Council of Philadelphia 9.22.17 Trend Analysis of Changes to Population and Income in Philadelphia, using 2010-2016 American Community Survey (ACS)

OFFICE OF THE PRESIDENT FINANCE AND BUDGET TEAM City Council of Philadelphia 9.22.17 Trend Analysis of Changes to Population and Income in Philadelphia, using 2010-2016 American Community Survey (ACS)

12. Canadians who are also U.S. citizens and considering renouncing such citizenship - Some U.S. tax implications By Simon Sturm

12. Canadians who are also U.S. citizens and considering renouncing such citizenship - Some U.S. tax implications By Simon Sturm Under U.S. tax laws an individual who is either a U.S. citizen or a U.S.

12. Canadians who are also U.S. citizens and considering renouncing such citizenship - Some U.S. tax implications By Simon Sturm Under U.S. tax laws an individual who is either a U.S. citizen or a U.S.

Budget Analysis from the NERI. NERI (Nevin Economic Research Institute) Dublin & Belfast

Dublin & Belfast") Budget Analysis from the NERI NERI (Nevin Economic Research Institute) Dublin & Belfast Tom.mcdonnell@nerinstitute.net Macro Context Improving growth and employment prospects (along with methodological

Budget Analysis from the NERI NERI (Nevin Economic Research Institute) Dublin & Belfast Tom.mcdonnell@nerinstitute.net Macro Context Improving growth and employment prospects (along with methodological

Notes and Definitions Numbers in the text, tables, and figures may not add up to totals because of rounding. Dollar amounts are generally rounded to t

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Distribution of Household Income and Federal Taxes, 2013 Percent 70 60 50 Shares of Before-Tax Income and Federal Taxes, by Before-Tax Income

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Distribution of Household Income and Federal Taxes, 2013 Percent 70 60 50 Shares of Before-Tax Income and Federal Taxes, by Before-Tax Income

1102 Longworth House Office Building 1106 Longworth House Office Building Washington, DC Washington, DC 20515

February 23, 2017 The Honorable Kevin Brady The Honorable Richard Neal Chairman Ranking Member Committee on Ways and Means Committee on Ways and Means U.S. House of Representatives U.S. House of Representatives

February 23, 2017 The Honorable Kevin Brady The Honorable Richard Neal Chairman Ranking Member Committee on Ways and Means Committee on Ways and Means U.S. House of Representatives U.S. House of Representatives

The Massachusetts Joint Committee on Revenue Using a State Employer-Side Payroll Tax to Offset the Limit on the SALT Deduction

The Massachusetts Joint Committee on Revenue Using a State Employer-Side Payroll Tax to Offset the Limit on the SALT Deduction Testimony of Dean Baker Senior Economist at the Center for Economic and Policy

The Massachusetts Joint Committee on Revenue Using a State Employer-Side Payroll Tax to Offset the Limit on the SALT Deduction Testimony of Dean Baker Senior Economist at the Center for Economic and Policy

The Melbourne Institute Report on the 2004 Federal Budget Hielke Buddelmeyer, Peter Dawkins, and Guyonne Kalb

The Melbourne Institute Report on the 2004 Federal Budget Hielke Buddelmeyer, Peter Dawkins, and Guyonne Kalb The Melbourne Institute of Applied Economic and Social Research University of Melbourne May

The Melbourne Institute Report on the 2004 Federal Budget Hielke Buddelmeyer, Peter Dawkins, and Guyonne Kalb The Melbourne Institute of Applied Economic and Social Research University of Melbourne May

The Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010: A Win for Our Economy, Jobs, and Working Families

The Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010: A Win for Our Economy, Jobs, and Working Families Framework on Tax Cuts, Unemployment Insurance and Jobs The Tax Relief,

The Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010: A Win for Our Economy, Jobs, and Working Families Framework on Tax Cuts, Unemployment Insurance and Jobs The Tax Relief,

FACT SHEET MAKING SUPERANNUATION FAIRER

FACT SHEET MAKING SUPERANNUATION FAIRER MAKING SUPERANNUATION FAIRER Labor built Australia s superannuation system. We will always work to ensure that it is fair, sustainable and sets Australians up for

FACT SHEET MAKING SUPERANNUATION FAIRER MAKING SUPERANNUATION FAIRER Labor built Australia s superannuation system. We will always work to ensure that it is fair, sustainable and sets Australians up for

CHILD POVERTY (SCOTLAND) BILL

BILL") CHILD POVERTY (SCOTLAND) BILL POLICY MEMORANDUM INTRODUCTION 1. As required under Rule 9.3.3 of the Parliament s Standing Orders, this Policy Memorandum is published to accompany the Child Poverty (Scotland)

CHILD POVERTY (SCOTLAND) BILL POLICY MEMORANDUM INTRODUCTION 1. As required under Rule 9.3.3 of the Parliament s Standing Orders, this Policy Memorandum is published to accompany the Child Poverty (Scotland)

At the end of Class 20, you will be able to answer the following:

1 Objectives for Class 20: The Tax System At the end of Class 20, you will be able to answer the following: 1. What are the main taxes collected at each level of government? 2. How do American taxes as

1 Objectives for Class 20: The Tax System At the end of Class 20, you will be able to answer the following: 1. What are the main taxes collected at each level of government? 2. How do American taxes as

Securing Canada s Retirement Income System

Securing Canada s Retirement Income System April 1997 FOREWORD Ensuring that Canada s seniors have an adequate retirement income is one of the most important social policy initiatives ever undertaken in

Securing Canada s Retirement Income System April 1997 FOREWORD Ensuring that Canada s seniors have an adequate retirement income is one of the most important social policy initiatives ever undertaken in

MORE THAN HALF OF BLACK AND HISPANIC FAMILIES WOULD NOT BENEFIT FROM BUSH TAX PLAN. by Isaac Shapiro, Allen Dupree and James Sly

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org http://www.cbpp.org February 15, 2001 MORE THAN HALF OF BLACK AND HISPANIC FAMILIES WOULD NOT BENEFIT

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org http://www.cbpp.org February 15, 2001 MORE THAN HALF OF BLACK AND HISPANIC FAMILIES WOULD NOT BENEFIT

How Do the Presidential Candidates Tax Plans Affect Taxpayers Marginal Tax Rates?

FISCAL October 2008 No. 150 FACT How Do the Presidential Candidates Tax Plans Affect Taxpayers Marginal Tax Rates? By Robert Carroll Summary The Presidential candidates have proposed comprehensive tax

FISCAL October 2008 No. 150 FACT How Do the Presidential Candidates Tax Plans Affect Taxpayers Marginal Tax Rates? By Robert Carroll Summary The Presidential candidates have proposed comprehensive tax

Summary of 1971 Tax Reform Legislation

Res HJ2449 C38 1971 st= Summary of 1971 Tax Reform Legislation Honourable E. J. Benson, Minister of Finance 301450007 5920 Re5, I-1J `-1 11 1 19171 Summary of 1971 Tax Reform Legislation TREASURY BOARD

Res HJ2449 C38 1971 st= Summary of 1971 Tax Reform Legislation Honourable E. J. Benson, Minister of Finance 301450007 5920 Re5, I-1J `-1 11 1 19171 Summary of 1971 Tax Reform Legislation TREASURY BOARD

17 November Committee Secretary Senate Economics Legislation Committee PO Box 6100 Parliament House Canberra ACT 2600.

17 November 2016 Committee Secretary Senate Economics Legislation Committee PO Box 6100 Parliament House Canberra ACT 2600 Dear Secretary, Re: Inquiry into Superannuation (Excess Transfer Balance Tax)

17 November 2016 Committee Secretary Senate Economics Legislation Committee PO Box 6100 Parliament House Canberra ACT 2600 Dear Secretary, Re: Inquiry into Superannuation (Excess Transfer Balance Tax)

Personal Income. Tax Reduction

Personal Income Tax Reduction B E N E F I T S F O R A L L T A X P A Y E R S Personal Income Tax Reduction Benefits for all taxpayers FOREWORD FOREWORD By the Deputy Prime Minister and Minister of State

Personal Income Tax Reduction B E N E F I T S F O R A L L T A X P A Y E R S Personal Income Tax Reduction Benefits for all taxpayers FOREWORD FOREWORD By the Deputy Prime Minister and Minister of State

Department of Finance Canada Consultation: Tax Planning Using Private Corporations

Department of Finance Canada Consultation: Tax Planning Using Private Corporations Date of Submission: September 29, 2017 Executive Summary CFA believes the proposed tax changes related to the Department

Department of Finance Canada Consultation: Tax Planning Using Private Corporations Date of Submission: September 29, 2017 Executive Summary CFA believes the proposed tax changes related to the Department

CRS Report for Congress

Order Code RL33285 CRS Report for Congress Received through the CRS Web Tax Reform and Distributional Issues February 27, 2006 Jane G. Gravelle Senior Specialist in Economic Policy Government and Finance

Order Code RL33285 CRS Report for Congress Received through the CRS Web Tax Reform and Distributional Issues February 27, 2006 Jane G. Gravelle Senior Specialist in Economic Policy Government and Finance

TAXES ARE A CHILDREN S ISSUE

TAXES ARE A CHILDREN S ISSUE PART II: REVENUE Webinar for the Children s Leadership Council Joan Entmacher Vice President for Family Economic Security National Women s Law Center October 2, 2014 WHY TAXES

TAXES ARE A CHILDREN S ISSUE PART II: REVENUE Webinar for the Children s Leadership Council Joan Entmacher Vice President for Family Economic Security National Women s Law Center October 2, 2014 WHY TAXES

Preliminary Details and Analysis of the Tax Cuts and Jobs Act

SPECIAL REPORT No. 241 Dec. 2017 Preliminary Details and Analysis of the Tax Cuts and Jobs Act Tax Foundation Staff Key Findings The Tax Cuts and Jobs Act would reform both individual income and corporate

SPECIAL REPORT No. 241 Dec. 2017 Preliminary Details and Analysis of the Tax Cuts and Jobs Act Tax Foundation Staff Key Findings The Tax Cuts and Jobs Act would reform both individual income and corporate

Federal, State, and Local Taxes in NYS. Counties TAXES IN NYS. April Fire districts 1% Villages 2% Library 1% Towns 7% Cities (w/nyc) 18%

18%") TAXES IN NYS Library 1% Fire districts 1% Villages 2% Towns 7% Cities (w/nyc) 18% School Districts 62% Counties 9% Chart Includes NYC Federal, State, and Local Taxes in NYS April 2018 HON. MARYELLEN ODELL

TAXES IN NYS Library 1% Fire districts 1% Villages 2% Towns 7% Cities (w/nyc) 18% School Districts 62% Counties 9% Chart Includes NYC Federal, State, and Local Taxes in NYS April 2018 HON. MARYELLEN ODELL

continue to average 0.2 percent of GDP from 2018 through 2028, CBO projects.

74 The Budget and Economic Outlook: 2018 to 2028 April 2018 continue to average 0.2 percent of GDP from 2018 through 2028, CBO projects. Tax Many exclusions, deductions, preferential rates, and credits

74 The Budget and Economic Outlook: 2018 to 2028 April 2018 continue to average 0.2 percent of GDP from 2018 through 2028, CBO projects. Tax Many exclusions, deductions, preferential rates, and credits

NBER WORKING PAPER SERIES CAPPING INDIVIDUAL TAX EXPENDITURE BENEFITS. Martin Feldstein Daniel Feenberg Maya MacGuineas

NBER WORKING PAPER SERIES CAPPING INDIVIDUAL TAX EXPENDITURE BENEFITS Martin Feldstein Daniel Feenberg Maya MacGuineas Working Paper 16921 http://www.nber.org/papers/w16921 NATIONAL BUREAU OF ECONOMIC

NBER WORKING PAPER SERIES CAPPING INDIVIDUAL TAX EXPENDITURE BENEFITS Martin Feldstein Daniel Feenberg Maya MacGuineas Working Paper 16921 http://www.nber.org/papers/w16921 NATIONAL BUREAU OF ECONOMIC

FISCAL FACT No. 516 July, 2016 Director of Federal Projects Key Findings Embargoed

FISCAL FACT No. 516 July, 2016 Details and Analysis of the 2016 House Republican Tax Reform Plan By Kyle Pomerleau Director of Federal Projects Key Findings The House Republican tax reform plan would reform

FISCAL FACT No. 516 July, 2016 Details and Analysis of the 2016 House Republican Tax Reform Plan By Kyle Pomerleau Director of Federal Projects Key Findings The House Republican tax reform plan would reform

Midyear Tax Planning Letter

Midyear Tax Planning Letter 2015 Introduction Tax planning for 2015 is a venture in uncertainty. Last December, Congress passed legislation extending a number of expired tax provisions. Unfortunately,

Midyear Tax Planning Letter 2015 Introduction Tax planning for 2015 is a venture in uncertainty. Last December, Congress passed legislation extending a number of expired tax provisions. Unfortunately,

Speech: Priorities for EU tax policy

EUROPEAN COMMISSION Algirdas Šemeta Commissioner responsible for Taxation and Customs Union, Audit and Anti-fraud Speech: Priorities for EU tax policy Irish Parliament Committee on Finance / Dublin 10

EUROPEAN COMMISSION Algirdas Šemeta Commissioner responsible for Taxation and Customs Union, Audit and Anti-fraud Speech: Priorities for EU tax policy Irish Parliament Committee on Finance / Dublin 10

UNIFIED FRAMEWORK FOR FIXING OUR BROKEN TAX CODE

UNIFIED FRAMEWORK FOR FIXING OUR BROKEN TAX CODE SEPTEMBER 27, 2017 1 OVERVIEW It is now time for all members of Congress Democrat, Republican and Independent to support pro-american tax reform. It s time

UNIFIED FRAMEWORK FOR FIXING OUR BROKEN TAX CODE SEPTEMBER 27, 2017 1 OVERVIEW It is now time for all members of Congress Democrat, Republican and Independent to support pro-american tax reform. It s time

The Distribution of Federal Taxes, Jeffrey Rohaly

www.taxpolicycenter.org The Distribution of Federal Taxes, 2008 11 Jeffrey Rohaly Overall, the federal tax system is highly progressive. On average, households with higher incomes pay taxes that are a

www.taxpolicycenter.org The Distribution of Federal Taxes, 2008 11 Jeffrey Rohaly Overall, the federal tax system is highly progressive. On average, households with higher incomes pay taxes that are a

17. Social Security. Congress should allow workers to privately invest at least half their Social Security payroll taxes through individual accounts.

17. Social Security Congress should allow workers to privately invest at least half their Social Security payroll taxes through individual accounts. Although President Bush failed in his efforts to reform

17. Social Security Congress should allow workers to privately invest at least half their Social Security payroll taxes through individual accounts. Although President Bush failed in his efforts to reform

Econ Ch. 9 Practice Test II

Econ Ch. 9 Practice Test II Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The incidence of a tax can more effectively be shifted from the supplier to

Econ Ch. 9 Practice Test II Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The incidence of a tax can more effectively be shifted from the supplier to

Pension Issues for Women

Pension Issues for Women This bulletin aims to highlight the key areas in Britain s pensions system where women have historically lost out and continue to do so. It will also offer guidance to actions

Pension Issues for Women This bulletin aims to highlight the key areas in Britain s pensions system where women have historically lost out and continue to do so. It will also offer guidance to actions

TAX BULLETIN DECEMBER 6, 2017

TAX BULLETIN 2017-7 DECEMBER 6, 2017 0BSENATE AND HOUSE PASS SEPARATE TAX BILLS: 1BTAX REFORM ON THE HORIZON OVERVIEW Following on the heels of the House s passage of a tax reform bill, the Senate passed

TAX BULLETIN 2017-7 DECEMBER 6, 2017 0BSENATE AND HOUSE PASS SEPARATE TAX BILLS: 1BTAX REFORM ON THE HORIZON OVERVIEW Following on the heels of the House s passage of a tax reform bill, the Senate passed

e White Paper Tax Reform 1987

Res. 11,12449 C16 1987 e White Paper Tax Reform 1987 June 18, 1987 The Honourable Michael H. Wilson Minister of Finance The White Paper Tax Reform 1987 1-/-bW9 C)-. /9g7 June 18, 1987 1000101 I I MIDI

Res. 11,12449 C16 1987 e White Paper Tax Reform 1987 June 18, 1987 The Honourable Michael H. Wilson Minister of Finance The White Paper Tax Reform 1987 1-/-bW9 C)-. /9g7 June 18, 1987 1000101 I I MIDI

NATIONAL BUDGET 2017/2018

NATIONAL BUDGET 2017/2018 Summary On 22 February 2017 Finance Minister Pravin Gordhan delivered in parliament the eighth budget speech of the Zuma administration. The minister gave advance warning in his

NATIONAL BUDGET 2017/2018 Summary On 22 February 2017 Finance Minister Pravin Gordhan delivered in parliament the eighth budget speech of the Zuma administration. The minister gave advance warning in his

The Tax Reform Act of 1986: Comment on the 25th Anniversary

The Tax Reform Act of 1986: Comment on the 25th Anniversary The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters Citation Feldstein,

The Tax Reform Act of 1986: Comment on the 25th Anniversary The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters Citation Feldstein,

Both bills will revitalize our stagnant economy, resulting in higher wages and new or better jobs for American workers.

December 6, 2017 Dear Conferee: ATR Submission to the Conference Committee for the Tax Cuts and Jobs Act I write in support of H.R. 1, the Tax Cuts and Jobs Act. Both the Senate and House bills are progrowth

December 6, 2017 Dear Conferee: ATR Submission to the Conference Committee for the Tax Cuts and Jobs Act I write in support of H.R. 1, the Tax Cuts and Jobs Act. Both the Senate and House bills are progrowth

Obamacare Tax Subsidies: Bigger Deficit, Fewer Taxpayers, Damaged Economy

No. 2554 May 19, 2011 Obamacare Tax Subsidies: Bigger Deficit, Fewer Taxpayers, Damaged Economy Paul L. Winfree Abstract: The number of Americans who pay federal income taxes has been shrinking every year,

No. 2554 May 19, 2011 Obamacare Tax Subsidies: Bigger Deficit, Fewer Taxpayers, Damaged Economy Paul L. Winfree Abstract: The number of Americans who pay federal income taxes has been shrinking every year,

Submission on April 29, to the. President's Advisory Panel on Federal Tax Reform. E. Martin Davidoff, CPA, Esq. Individually

Submission on to the President's Advisory Panel on Federal Tax Reform by E. Martin Davidoff, CPA, Esq. Individually Contact Information E. Martin Davidoff, CPA, Esq. E. Martin Davidoff & Associates Certified

Submission on to the President's Advisory Panel on Federal Tax Reform by E. Martin Davidoff, CPA, Esq. Individually Contact Information E. Martin Davidoff, CPA, Esq. E. Martin Davidoff & Associates Certified

IPART. More efficient, more integrated Opal Fares Transport Draft Report December February 2016

IPART More efficient, more integrated Opal Fares Transport Draft Report December 2015 February 2016 Phone: 02 9211 2599 Email: info@ncoss.org.au Suite 301, Level 3, 52-58 William St, Woolloomooloo NSW

IPART More efficient, more integrated Opal Fares Transport Draft Report December 2015 February 2016 Phone: 02 9211 2599 Email: info@ncoss.org.au Suite 301, Level 3, 52-58 William St, Woolloomooloo NSW

Calling Time on the Alcohol Duty Escalator. Budget Submission 2014 The Scotch Whisky Association

Calling Time on the Alcohol Duty Escalator Budget Submission 2014 The Scotch Whisky Association Executive Summary Scotch Whisky in the UK is under sustained pressure from annual above inflation excise

Calling Time on the Alcohol Duty Escalator Budget Submission 2014 The Scotch Whisky Association Executive Summary Scotch Whisky in the UK is under sustained pressure from annual above inflation excise

THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA HOUSE OF REPRESENTATIVES TREASURY LAWS AMENDMENT (PERSONAL INCOME TAX PLAN) BILL 2018

BILL 2018") 2016-2017-2018 THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA HOUSE OF REPRESENTATIVES TREASURY LAWS AMENDMENT (PERSONAL INCOME TAX PLAN) BILL 2018 EXPLANATORY MEMORANDUM (Circulated by authority of the

2016-2017-2018 THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA HOUSE OF REPRESENTATIVES TREASURY LAWS AMENDMENT (PERSONAL INCOME TAX PLAN) BILL 2018 EXPLANATORY MEMORANDUM (Circulated by authority of the

Here is a quick summary of most-important tax changes starting with those that affect individuals. Payroll Tax Holiday Is Over

January 11, 2013 To Our Clients and Friends: The American Taxpayer Relief Act of 2012 (better known as the fiscal cliff legislation) became law on 1/2/13. Due to the expiration of the so-called payroll

January 11, 2013 To Our Clients and Friends: The American Taxpayer Relief Act of 2012 (better known as the fiscal cliff legislation) became law on 1/2/13. Due to the expiration of the so-called payroll

Impact of the Fiscal Cliff on New York State

Impact of the Fiscal Cliff on New York State Sharp Tax Increases, Reductions in Federal Aid Would Hit the Empire State Starting in 2013 Thomas P. DiNapoli New York State Comptroller December 2012 Summary

Impact of the Fiscal Cliff on New York State Sharp Tax Increases, Reductions in Federal Aid Would Hit the Empire State Starting in 2013 Thomas P. DiNapoli New York State Comptroller December 2012 Summary

The tax reform of 2017 explained

I nnealta C A P I T A L SPECIALISTS IN ACTIVE MANAGEMENT OF ETF PORTFOLIOS The tax reform of 2017 explained Key takeaways: Recently introduced tax reform covers three main areas: taxes on individuals,

I nnealta C A P I T A L SPECIALISTS IN ACTIVE MANAGEMENT OF ETF PORTFOLIOS The tax reform of 2017 explained Key takeaways: Recently introduced tax reform covers three main areas: taxes on individuals,

Details and Analysis of the 2017 Tax Cuts and Jobs Act

SPECIAL REPORT No. 239 Nov. 2017 Details and Analysis of the 2017 Tax Cuts and Jobs Act Tax Foundation Staff Key Findings The Tax Cuts and Jobs Act would reform both individual income tax and corporate

SPECIAL REPORT No. 239 Nov. 2017 Details and Analysis of the 2017 Tax Cuts and Jobs Act Tax Foundation Staff Key Findings The Tax Cuts and Jobs Act would reform both individual income tax and corporate

Income Taxes and Tax Rates for Sample Families, 2006 Greg Leiserson. December 2006

Income Taxes and Tax Rates for Sample Families, 2006 Greg Leiserson December 2006 This article examines how much income tax families pay in different situations, as well as the effective marginal tax rates

Income Taxes and Tax Rates for Sample Families, 2006 Greg Leiserson December 2006 This article examines how much income tax families pay in different situations, as well as the effective marginal tax rates

The European Social Model and the Greek Economy

SPEECH/05/577 Joaquín Almunia European Commissioner for Economic and Monetary Affairs The European Social Model and the Greek Economy Dinner-Debate Athens, 5 October 2005 Minister, ladies and gentlemen,

SPEECH/05/577 Joaquín Almunia European Commissioner for Economic and Monetary Affairs The European Social Model and the Greek Economy Dinner-Debate Athens, 5 October 2005 Minister, ladies and gentlemen,

BUDGET Quebecers and Their Disposable Income. Greater Wealth

BUDGET 2012-2013 Quebecers and Their Disposable Income Greater Wealth for All Paper inside pages 100% This document is printed on completely recycled paper, made in Québec, contaning 100% post-consumer

BUDGET 2012-2013 Quebecers and Their Disposable Income Greater Wealth for All Paper inside pages 100% This document is printed on completely recycled paper, made in Québec, contaning 100% post-consumer

Re: Federal Consultation: Tax Planning Using Private Corporations

Chartered Professional Accountants of Canada 277 Wellington Street West Toronto ON CANADA M5V 3H2 T. 416 977.3222 F. 416 977.8585 www.cpacanada.ca Comptables professionnels agréés du Canada 277, rue Wellington

Chartered Professional Accountants of Canada 277 Wellington Street West Toronto ON CANADA M5V 3H2 T. 416 977.3222 F. 416 977.8585 www.cpacanada.ca Comptables professionnels agréés du Canada 277, rue Wellington

WebMemo22. The End of Pro-Growth Tax Policy: How the Rangel Tax Bill Could Affect the U.S. Economy. Published by The Heritage Foundation

WebMemo22 Published by The Heritage Foundation The End of Pro-Growth Tax Policy: How the Rangel Tax Bill Could Affect the U.S. Economy William W. Beach and Guinevere Nell This week, the House of Representatives

WebMemo22 Published by The Heritage Foundation The End of Pro-Growth Tax Policy: How the Rangel Tax Bill Could Affect the U.S. Economy William W. Beach and Guinevere Nell This week, the House of Representatives

2018 New Year s Tax Changes

2018 New Year s s Page 1 About the Canadian Taxpayers Federation The Canadian Taxpayers Federation (CTF) is a federally incorporated, not-for-profit citizen s group dedicated to lower taxes, less waste

2018 New Year s s Page 1 About the Canadian Taxpayers Federation The Canadian Taxpayers Federation (CTF) is a federally incorporated, not-for-profit citizen s group dedicated to lower taxes, less waste

CHAPTER 4. EXPANDING EMPLOYMENT THE LABOR MARKET REFORM AGENDA

CHAPTER 4. EXPANDING EMPLOYMENT THE LABOR MARKET REFORM AGENDA 4.1. TURKEY S EMPLOYMENT PERFORMANCE IN A EUROPEAN AND INTERNATIONAL CONTEXT 4.1 Employment generation has been weak. As analyzed in chapter

CHAPTER 4. EXPANDING EMPLOYMENT THE LABOR MARKET REFORM AGENDA 4.1. TURKEY S EMPLOYMENT PERFORMANCE IN A EUROPEAN AND INTERNATIONAL CONTEXT 4.1 Employment generation has been weak. As analyzed in chapter

IRS and Treasury Issue Proposed Regulations Easing Some of the Burden of the Fractions Rule

Tax Practice Group December 1, 2016 IRS and Treasury Issue Proposed Regulations Easing Some of the Burden of the Fractions Rule For more information, contact: Jonathan Talansky +1 212 790 5321 jtalansky@kslaw.com

Tax Practice Group December 1, 2016 IRS and Treasury Issue Proposed Regulations Easing Some of the Burden of the Fractions Rule For more information, contact: Jonathan Talansky +1 212 790 5321 jtalansky@kslaw.com

2017 YEAR-END. tax planning INDIVIDUALS. guide for

2017 YEAR-END tax planning INDIVIDUALS guide for year in review 2017 is unlike any previous tax year. Major congressional tax reform proposals that generally would go into effect in 2018 if signed into

2017 YEAR-END tax planning INDIVIDUALS guide for year in review 2017 is unlike any previous tax year. Major congressional tax reform proposals that generally would go into effect in 2018 if signed into

Alberta Federation of Labour Submission to Financial Management Commission

Alberta Federation of Labour Submission to Financial Management Commission May 2002 INTRODUCTION The Alberta Federation of Labour (AFL) would like to thank the Commission for the opportunity to make a

Alberta Federation of Labour Submission to Financial Management Commission May 2002 INTRODUCTION The Alberta Federation of Labour (AFL) would like to thank the Commission for the opportunity to make a