BEFORE THE MINNESOTA OFFICE OF ADMINISTRATIVE HEARINGS 100 Washington Square, Suite 1700 Minneapolis MN

|

|

|

- Ophelia Cross

- 5 years ago

- Views:

Transcription

1 BEFORE THE MINNESOTA OFFICE OF ADMINISTRATIVE HEARINGS 100 Washington Square, Suite 1700 Minneapolis MN FOR THE MINNESOTA PUBLIC UTILITIES COMMISSION th Place East, Suite 350 St Paul MN In the Matter of the Petition of Northern States Power Company, a Minnesota Corporation and Wholly Owned Subsidiary of Xcel Energy Inc., for Authority to Increase Rates for Natural Gas Service in Minnesota MPUC Docket No. G002/GR OAH Docket No DIRECT TESTIMONY AND EXHIBITS OF MICHELLE A. ST. PIERRE ON BEHALF OF THE MINNESOTA DEPARTMENT OF COMMERCE MARCH 9, 2007

2 DIRECT TESTIMONY AND EXHIBITS OF MICHELLE A. ST. PIERRE NORTHERN STATES POWER COMPANY, A MINNESOTA CORPORATION AND WHOLLY OWNED SUBSIDIARY OF XCEL ENERGY, INC. MPUC DOCKET NO. G002/GR OAH DOCKET NO TABLE OF CONTENTS Section... Page I. INTRODUCTION...1 II. III. PURPOSE...2 COST ALLOCATIONS...3 A. Previous Investigations...3 B. Overview of Allocation Process...5 C. Department Investigation Overall Service Company Allocations Utility Allocations between Gas and Electric Utilities Non-Regulated Business Activity Allocations...15 D. Cost Allocations Conclusions and Recommendations...16 IV. PENSION EXPENSE...17 V. POST RETIREMENT BENEFIT COSTS (FAS 106 EXPENSE)...19 VI. BAD DEBT EXPENSE...21 VII. SUMMARY OF RECOMMENDATIONS...25

3 I. INTRODUCTION Q. Would you state your name, occupation and business address? A. My name is Michelle A. St. Pierre. I am employed as a Public Utilities Financial Analyst by the Energy Planning and Advocacy Division of the Minnesota Department of Commerce (DOC or the Department). My business address is 85 7th Place East, Suite 500, St. Paul, Minnesota Q. What is your educational and professional background? A. I received a Bachelor of Business Administration degree in Accounting from Corpus Christi State University (currently Texas A&M University-Corpus Christi). I also maintain an active Certified Public Accountant license in the state of Minnesota. DOC Exhibit No. (MAS-1) is a summary of my witness qualifications including my current responsibilities, previous testimony in general rate cases, previous employment, and education Q. What is your business experience? A. My business background includes seven years of audit experience of tax returns with the Internal Revenue Service. I also had one year of experience performing governmental audits for an accounting firm in Texas. Currently, I have worked over 19 years as a Financial Analyst for the Department. St. Pierre Direct / 1

4 1 II. PURPOSE Q. What is the purpose of your testimony? A. My responsibility, working in conjunction with Department Witness Mr. Dale V. Lusti, is to review and investigate certain financial components of Northern States Power Company s, a Minnesota Corporation and wholly owned subsidiary of Xcel Energy, Inc. (NSP, Xcel, or the Company) application for a general rate increase. Xcel Energy, Inc (XEI) has numerous subsidiaries, including two NSP subsidiaries. One NSP subsidiary is a Minnesota corporation and one is a Wisconsin corporation. In my testimony, I refer to the Minnesota subsidiary as NSP-MN or the Company. During my review, I issued written information requests and discussed on site with Company personnel various financial information and supporting documentation. The purpose of my testimony is to assist the Minnesota Public Utilities Commission (Commission) in evaluating the reasonableness of NSP s proposed revenue requirement to be used in establishing rates Q. What is the scope of your testimony? A. My testimony focuses only on certain financial areas in which the Department has concerns and for which the Department recommends either adjustments to the numbers proposed by NSP in its rate case filing or where the Department has recommended a condition, with the exception of Pension expense and Post Retirement Benefit Costs. Specifically, the areas on which I focus my testimony and recommended adjustments or conditions are as follows: Cost Allocations, Pension expense, Post Retirement Benefit Costs, and Bad debt expense. St. Pierre Direct / 2

5 III. COST ALLOCATIONS A. PREVIOUS INVESTIGATIONS Q. Has the Department previously investigated NSP s processes and methods of identifying and assigning costs among various activities? A. Yes. The Department performed a fairly extensive review of NSP s regulated/nonregulated cost allocations in the Company s 1992 Minnesota electric and gas rate cases, Docket Nos. E002/GR and G002/GR The Department also reviewed in detail the Company s allocation methods in a number of NSP merger and affiliated interest proceedings, as well as NSP s last two Minnesota gas utility rate cases, Docket Nos. G002/GR and G002/GR ( ) and last electric utility rate case, Docket No. E002/GR ( ) Q. Has the Department previously examined the Service Company allocations? A. Yes. The Department reviewed the initial Service Company affiliated interest Service Agreement filed with the Commission in Docket No. E,G002/AI In Docket No. E,G002/AI , the Department reviewed Xcel s petition for an updated Service Agreement to incorporate new corporate governance allocators resulting from the Securities Exchange Commission audit in Subsequently, in Docket No. E,G002/AI , the Department reviewed Xcel s petition for an updated Service Agreement to incorporate new allocation factors for information technology services. The Department also reviewed the Service Company allocations in the last gas and electric general rate cases. St. Pierre Direct / 3

6 Q. What did the Department conclude about allocations in NSP s most recent gas general rate case? A. In NSP s most recent gas general rate case ( ), Department Witness Sundra Bender concluded that the Service Company s cost allocations to NSP s gas utility appear to generally follow the cost allocation principles adopted by the Commission in the G,E999/CI ( ) docket and/or comply with the Commission approved NSP agreement with the Service Company. Additionally, the Department concluded that although the method for allocating corporate residual costs to NSP s non-regulated activities is different than the Commission approved general allocation method, the nonregulated activities were insignificant based on 2003 data Q. In NSP s last general rate case for the gas utility, did the Commission require some reporting recommendations for the Company s next Minnesota general rate case? A. Yes. Since NSP s subsequent Minnesota general rate case was the Company s electric rate case ( ), NSP provided the required information in that docket. Department Witness Nancy A. Campbell reviewed the information and recommended no adjustment in her Direct testimony Q. Based on its overall review of allocations, what did the Department conclude in NSP s most recent electric general rate case? A. In NSP s most recent electric general rate case ( ), Ms. Campbell concluded that she did not find anything in her review of the rate case information and information requests at the time that raised further concerns or caused her to recommend adjustments regarding allocations. St. Pierre Direct / 4

7 B. OVERVIEW OF ALLOCATION PROCESS Q. What Company Witnesses discuss cost allocations? A. Company Witness Janet S. Schmidt-Petree sponsors Direct testimony on NSP s ( NSP- MN ) and Xcel Energy Service, Inc. s ( XES or the Service Company ) cost allocation methodologies. Company Witness Jeffery C. Robinson also discusses the Company s proposed adjustment to common costs related to Utility Allocations, as well as Jurisdictional Allocations Q. Would you please describe the utility operating company, NSP-MN? A. Yes. As stated on page 3, lines 10-13, of Ms. Schmidt-Petree s testimony: NSP-MN is a wholly owned subsidiary of Xcel Energy Inc. NSP-MN is a multi-utility, multi-jurisdictional company that provides electric service to customers in Minnesota, North Dakota, and South Dakota and natural gas service to customers in Minnesota and North Dakota. Q. Please explain the Service Company s role in providing services to the operating companies. A. On page 4, lines 8-15, Ms. Schmidt-Petree states that: First, pursuant to the PUHCA [Public Utility Holding Company Act] 1935, registered holding companies, such as Xcel Energy Inc., were permitted to form and operate centralized service companies. However, one of the underlying requirements was that services be provided at cost to the utility operating companies and affiliates within the holding company system. To accomplish this, employees who provide services to more than one legal entity are employed by the Service Company, which provides shared or common administrative and management services to Xcel Energy Inc. and its subsidiaries. St. Pierre Direct / 5

8 Q. How are the Service Company allocations determined? A. NSP-MN has a Service Agreement with the Service Company which provides the cost assignment and allocation process. The Service Agreement is included in Ms. Schmidt- Petree s Exhibit (JSSP-1), Schedule Q. Once NSP-MN receives services and billings of directly assigned and allocated costs from the Service Company, how are the costs allocated after that point? A. Ms. Schmidt-Petree states on page 7, lines 10-12, After all billings to NSP-MN have occurred, specific Utility Allocations, Jurisdictional Allocations, and Non-Regulated Business Activity Allocations take place Q. Would you please briefly explain the purpose of the Utility Allocations, Jurisdictional Allocations, and Non-Regulated Business Activity Allocations? A. Yes. Utility Allocations allocates common costs between the gas and electric utilities, Jurisdictional Allocations allocates investment between states (Minnesota, North Dakota, and South Dakota), and Non-Regulated Business Activity Allocations allocates corporate residual costs and calculates the labor overhead rate to be applied to non-regulated entities labor costs. These allocations are further explained in NSP s Cost Assignment and Allocation Manual (CAAM) dated October 2006 and included in Ms. Schmidt- Petree s Exhibit (JSSP-1), Schedule Q. Please explain the need for Jurisdictional Allocations. A. According to Mr. Robinson, page 25-26, the process for assigning investment in gas plant is based on the use of such assets in providing gas service in a particular jurisdiction and St. Pierre Direct / 6

9 the underlying elements of cost causation. The Company s production and storage system is designed, built, and operated to provide an integrated source of natural gas shared by the Company s natural gas customers in Minnesota and North Dakota. Therefore, each jurisdiction s respective design day demand for gas is used for allocation of these facilities. Additionally, the Transmission and Distribution investment is directly assigned based on the jurisdiction(s) served by each of the individual facilities Q. According to Ms. Schmidt-Petree, NSP-MN may provide services to and bill other affiliates, and vice versa. How are billings to NSP-MN from other affiliates handled? A. The Direct testimony for Ms. Schmidt-Petree states on page 5, lines that: For those costs billed to NSP-MN, the costs may also be billed at the utility operations level, the jurisdictional level, or the non-regulated business activity level. Any common costs billed to NSP-MN must then be allocated again through Utility Allocations, Jurisdictional Allocations, or Non-Regulated Business Activity Allocation. Q. Does the Company have an Administrative Services Agreement (ASA) for shared services with affiliates? A. Yes. In Docket No. E002/AI , the Commission approved an ASA allowing NSP and the other regulated operating utility subsidiaries of Xcel Energy, Inc. to share a limited amount of services, leasing arrangements, equipment, and other goods when it is mutually beneficial to the operating utilities involved. St. Pierre Direct / 7

10 C. DEPARTMENT S INVESTIGATION 1. Overall Q. Please briefly explain your review of NSP s allocation methods in the current rate case. A. I reviewed the testimony and exhibits of Ms. Schmidt-Petree and Mr. Robinson that discuss the cost allocation methodologies. The Department also issued information requests to obtain further information on the Company s cost allocations Q. What allocation process does NSP-MN follow? A. Ms. Schmidt-Petree states the following on page 17, lines 15-20: NSP-MN follows the same cost allocation process for all types of costs. The cost allocation approach is a fully distributed costing method, as approved by the Commission in numerous electric and gas rate cases (Docket Nos. E002/GR , G002/GR , G002/GR , G002/GR , and E002/GR ) and the Commission s September 28, 1994, Order in Docket No. G,E999/CI Q. What did the Commission decide in the docket? A. The Commission found that the following four basic hierarchical cost allocation principles, extracted from the comprehensive FCC cost methodology, are the best means of ensuring proper cost separations between regulated and non-regulated activities: 1. Tariffed rates shall be used to value tariffed services provided to the nonregulated activity. 2. Costs shall be directly assigned to either regulated or non-regulated activities whenever possible. 3. Costs which cannot be directly assigned are common costs which shall be grouped into homogeneous cost categories. Each cost category shall be allocated based on direct analysis of the origin of the costs whenever possible. If direct analysis is not possible, common costs shall be allocated based upon St. Pierre Direct / 8

11 an indirect cost-causative linkage to another cost category or group of cost categories for which direct assignment or allocation is available. 4. When neither direct nor indirect measures of cost causation can be found, the cost category shall be allocated based upon a general allocator computed by using the ratio of all expenses directly assigned or attributed to regulated and non-regulated activities, excluding the cost of fuel, gas, purchased power, and the purchased cost of goods sold. Additionally, the Commission required all utilities to be prepared to demonstrate in future rate cases that it follows these four cost allocation principles, or that: 1. its non-regulated activities are insignificant; or 2. its cost allocation principles produce similar results as would allocations following the recommended cost allocation principles; or 3. the public interest is better served by another method. 2. Service Company Allocations Q. How often do the Service Company allocation factors change and what data is used as the basis of the test year allocation factors? A. The Service Company updates the statistics used in the allocation factors annually for June business based on the prior calendar year statistics. The allocations used in the 2007 test year budget are based on December 31, 2005 data Q. Has there been any changes or updates in the Service Company s allocation methods since the last gas general rate case? A. According to Ms. Schmidt-Petree, page 11 of her Direct testimony, lines 18-20, There have been no changes or updates in the allocation methods since the information technology allocation methodologies were approved in Q. Is the Service Company s allocation system based on the allocation principles adopted by the Commission in the docket? St. Pierre Direct / 9

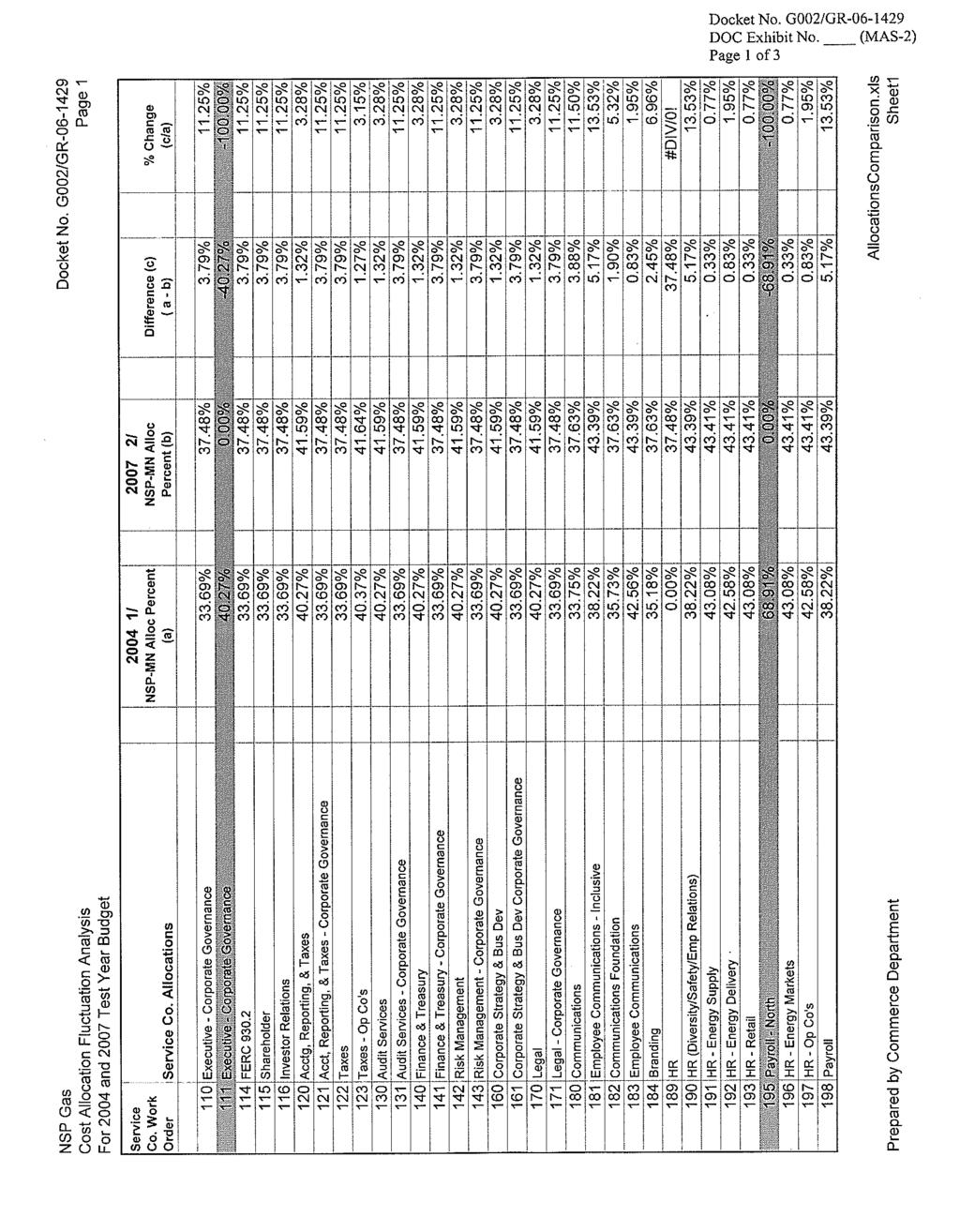

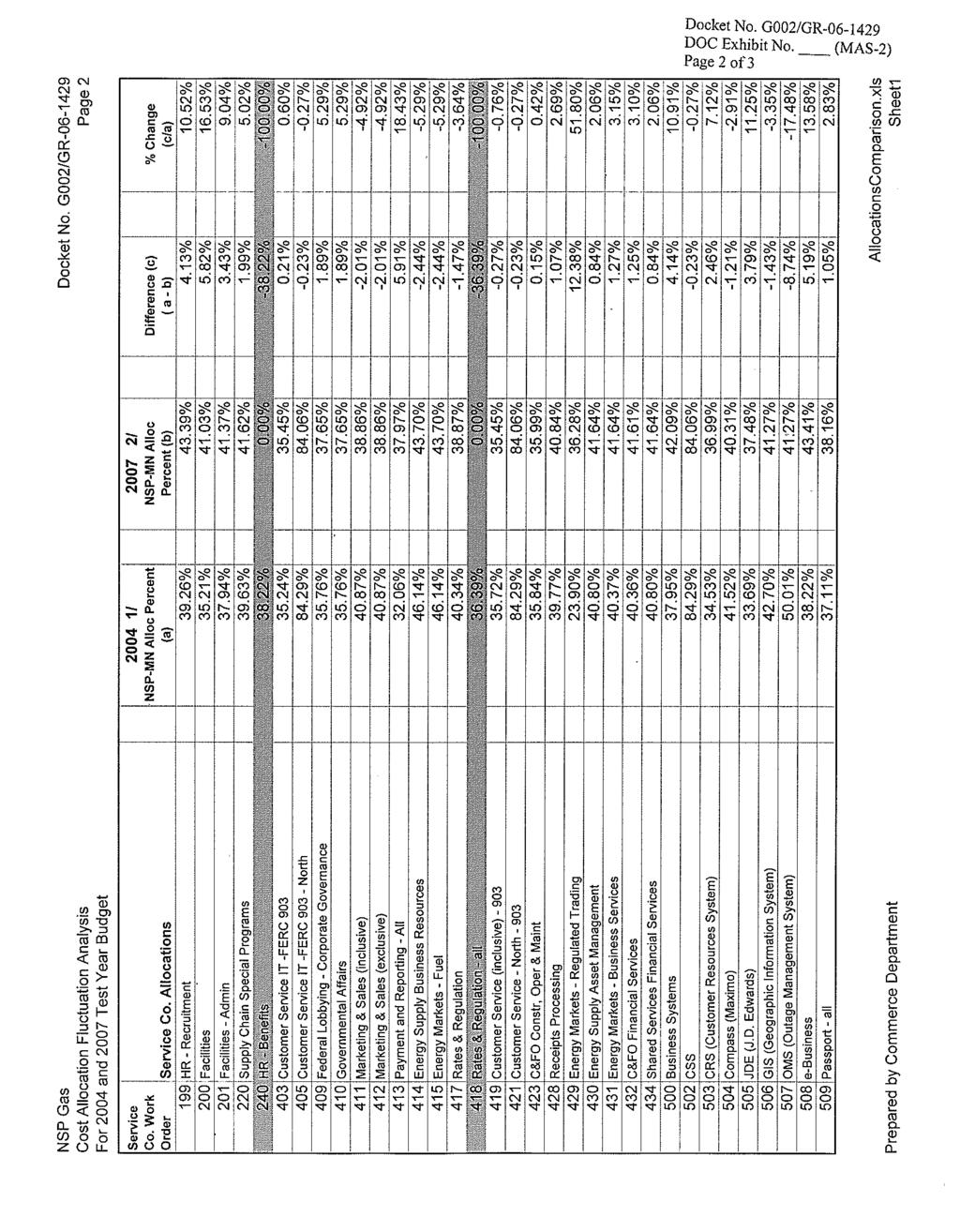

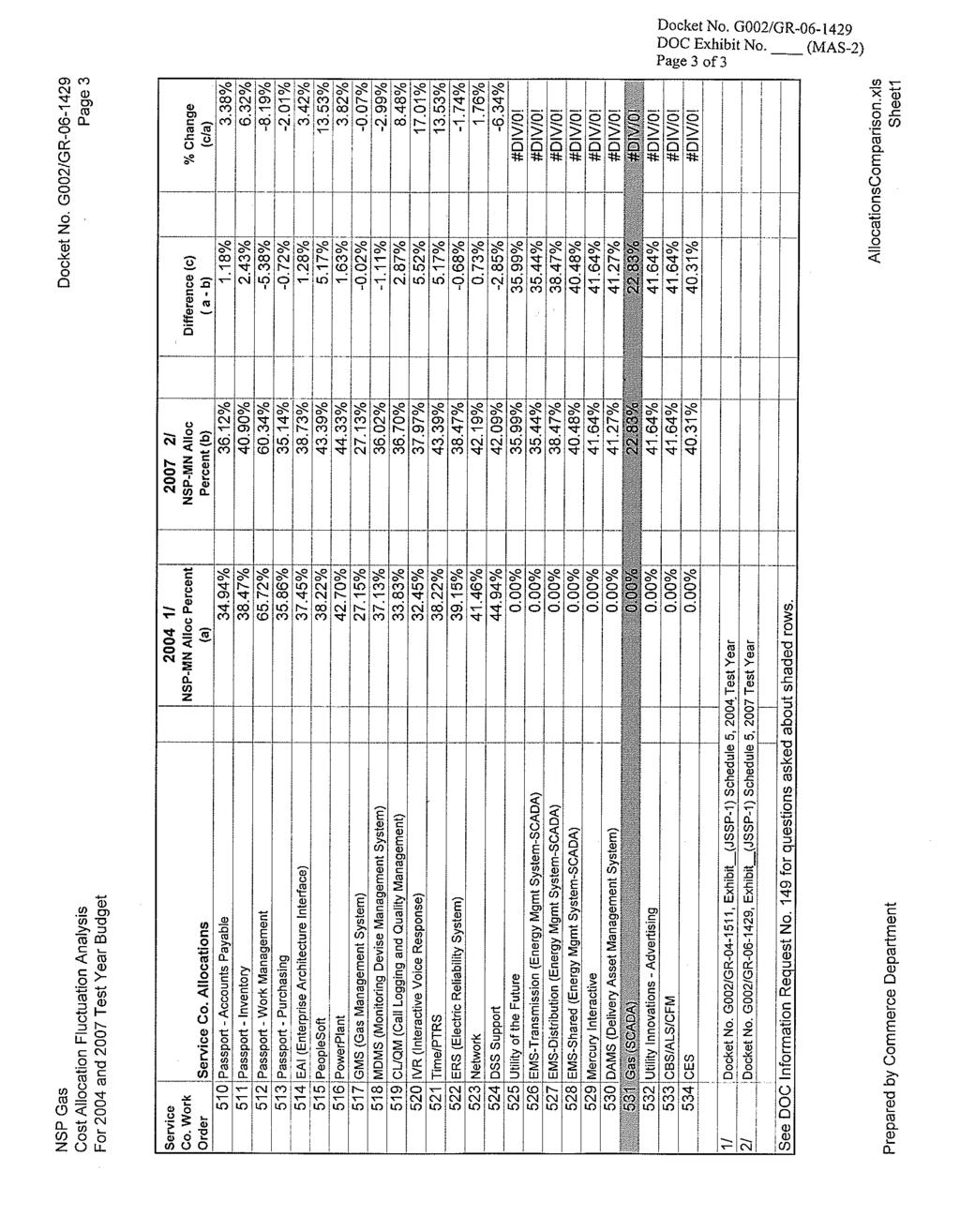

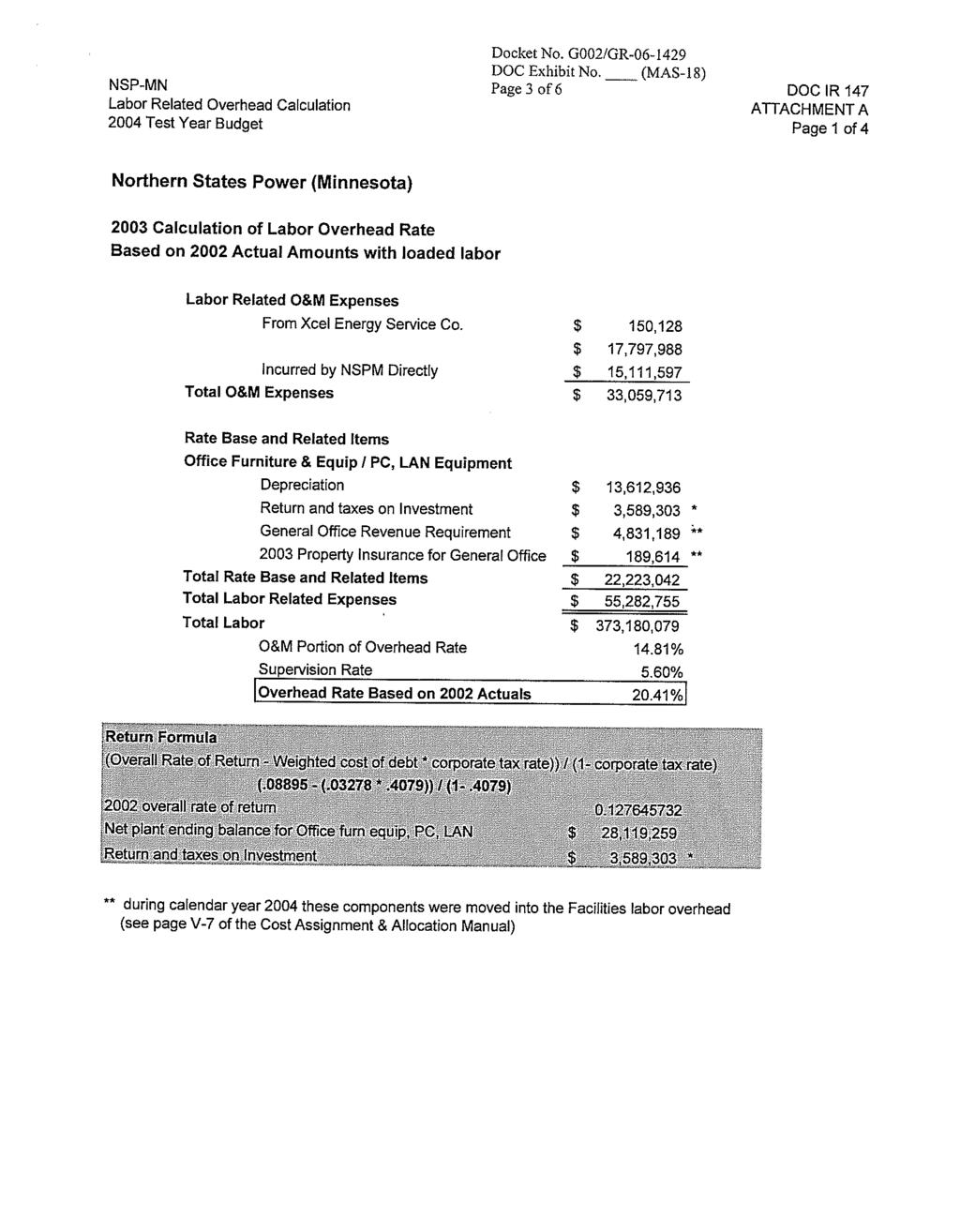

12 A. For the most part. The Service Company allocates costs for which neither direct nor indirect measures of cost causation can be found based upon a different computation than the one prescribed in the docket. A Three-Factor Formula (composed of a revenue ratio, an asset ratio, and a number-of-employees ratio) is used to allocate such costs. The Commission approved the Service Company s use of this formula, as modified in Docket No. E,G002/AI , as a general allocator to allocate costs to NSP Q. Please describe your analysis of the Service Company allocations. A. I compared the Service Company s allocation percentages used in the last gas rate case to the proposed test year percentages to determine the increase or decrease and the resulting percentage changes since the last gas general rate case. (See DOC Exhibit No. (MAS-2) for the Department s Service Company cost allocation fluctuation analysis.) Based on the Department s fluctuation analysis, the Department issued DOC Information Request (IR) Nos. 126, 127, 128, 149, 150, and 151. (See DOC Exhibit No. (MAS- 3) through (MAS-8) for the Company s responses regarding Service Company allocations.) Q. Did your review find any changes or updates to the Service Company s allocation methods since the information technology allocation methodologies were approved in 2004? A. Based on the Department s review, there did not appear to be any methodology changes. The Department s fluctuation analysis identified that since the last gas general rate case, Service Company Work Orders (allocators) 111, 195, 240, and 418 have been eliminated St. Pierre Direct / 10

13 1 2 3 and Work Orders 531 has been added. The Company s responses to DOC IR 150 DOC Exhibit No. (MAS-7) explain the reasons why these Work Orders were eliminated or added Q. Do you have any concerns regarding the Service Company s allocation factors? A. I have one concern. As stated above, the Three-Factor Formula includes an employee ratio that is based on the number of employees at a certain point in time. The Department questions the use of this component because the Company s response to DOC IR 147 (D) (DOC Exhibit No. (MAS-18)) shows that the non-regulated business, Customer Owned Street Lighting, has zero employees based on the employee totals taken from the back up used to develop the service company indirect allocators. Because of this business showing zero employees, a ratio based on labor dollars for each applicable company to the total applicable labor dollars may be a better ratio to use rather than the employee ratio. Additionally, in its March 1, 2007 Order Accepting Compliance Filing As Modified and Requiring Further Filings, the Commission permitted Otter Tail Power Company to use an equal weighting of labor dollars, revenues, and assets in its general allocator in Docket No. E017-M Q. What is your recommendation? A. I recommend that the Company meet with the Department before its next Minnesota general rate case and be prepared to demonstrate the effect of using a labor dollar ratio compared to the employee ratio included in the Service Company s Three-Factor Formula used for allocating common costs. St. Pierre Direct / 11

14 Q. What is your overall conclusion on Service Company s allocations? A. I have not found anything in my review of the Service Company s allocations and related information request responses that cause me to recommend adjustments at this time. However, I recommend that the Company meet with the Department before its next Minnesota general rate case and be prepared to demonstrate the effect of using a labor dollar ratio compared to the employee ratio included in the Service Company s Three- Factor Formula used for allocating common costs Utility Allocations Between Gas and Electric Utilities Q. How often do the Utility Allocation factors change and what data is used as the basis of the test year allocation factors? A. Ms. Schmidt-Petree states on page 26, lines that NSP-MN O&M utility allocation factors are updated on an annual basis using the prior calendar year actual statistics and entered into the system for April business. Further, on lines she states The allocation factors used in the 2007 test year budget are the allocation factors calculated using the 2005 calendar year actual statistics because those are the factors that were being used in mid-2006 when the 2007 test year budget was developed Q. Please explain any changes in the Utility Allocation methods since the last gas general rate case. A. According to Ms. Schmidt-Petree, Direct testimony, pages 27-29, the Utility Allocation of common customer related costs (FERC accounts ) is allocated based on the customer bill counts. As Ms. Schmidt-Petree explains it, the underlying statistical data used to calculate the customer bill counts has changed and that this is the only change. St. Pierre Direct / 12

15 Mr. Robinson also discusses this change on pages 8, 26, and 27 of his testimony. Mr. Robinson states that the new Customer Resource System ( CRS ) (implemented in February 2005) calculates customer bill counts differently than the previous CSS system which has the effect of allocating a larger portion of common customer related costs to the gas utility operations with a corresponding reduction in the amount allocated to electric utility operations. Instead of counting a customer that is both an electric and gas customer as ½ electric customer bill, and ½ gas customer bill, the CRS system counts one electric customer bill and one gas customer bill. The Company argues that By making this change in methodology for the Minnesota jurisdiction, Xcel Energy is now counting customer bills consistently across all of its jurisdictions. However, the Department notes that, for ratemaking purposes, making a change from bill counts to customer counts in the gas rate case would be inconsistent with the allocation used in the 2005 electric rate case where the electric utility s allocation was based on the previous CSS bill count methodology Q. Is the Company proposing to use the new CRS customer bill count in the test year which results in a percent gas allocation factor for common customer related gas and electric costs? A. No. The Company is proposing to use a factor of percent for gas common customer related costs (FERC accounts ) in the test year. Mr. Robinson states the following on page 27, lines15-19: The Company has made the decision to adjust the 2007 O&M budget data to reflect the prior customer bill utility allocation split for common customer related O&M costs to be consistent with the utility allocation of similar costs used St. Pierre Direct / 13

16 in the 2006 electric rate case. We anticipate using the new allocation factor in future rate cases. Q. What is your response? A. The change in the count is significant. Additionally, as I understand it, the allocation method changes from using number of bills to using number of customers. Further, the 5.37 percent change equates to $3,154,000 in the test year. (See Mr. Robinson s Direct testimony, page 28, lines 7-8 for the adjustment amount.) At first glance, the Department has some questions and potential concerns about this new method. Therefore, the Department recommends that the Company meet with the Department to discuss the allocation of common customer related gas and electric costs (FERC accounts ) before implementing the new methodology in any future rate case Q. Please describe your analysis of the Utility Allocations. A. I compared the Utility Allocation percentages used in the last gas rate case to the proposed test year percentages to determine the increase or decrease and the resulting percentage changes since the last gas general rate case. (See DOC Exhibit No. (MAS-9) for the Utility Allocations fluctuation analysis.) Based on the Department s fluctuation analysis, the Department issued DOC IR Nos. 107, 125, 145, and 146. (See DOC Exhibit No. (MAS-10) through (MAS-13) for the Company s responses regarding Utility Allocations.) Q. What is your conclusion on Utility Allocations? A. I have not found anything in my review of the Utility Allocations and related information request responses that cause me to recommend adjustments at this time. However, as St. Pierre Direct / 14

17 stated above, I recommend that the Company meet with the Department to discuss the Utility Allocation of common customer related gas and electric costs (FERC accounts ) before implementing its new customer count methodology in any future rate case Non-Regulated Business Activity Allocations Q. Please describe how NSP allocates costs among its regulated utilities and nonregulated activities. A. According to the Company, NSP follows allocation principles almost identical to the principles recommended in the docket except for the allocation to non-regulated operations of corporate residual costs. In that instance, NSP allocates corporate residual costs using a two-factor allocation ratio based on the number of employees and revenues Q. Please describe your analysis of the Non-Regulated Business Activity Allocations. A. I compared the Non-Regulated Business Activity Allocation percentages used in the last gas rate case to the proposed test year percentages to determine the increase or decrease and the resulting percentage changes since the last gas general rate case. (See DOC Exhibit No. (MAS-14) for the allocation factor comparison.) Based on the Department s fluctuation analysis, the Department issued DOC IR Nos. 108, 123, 124, and 147. (See DOC Exhibit No. (MAS-15) through (MAS-18) for the Company s responses regarding Non-Regulated Business Activity Allocations.) St. Pierre Direct / 15

18 Q. Since the Company s two-factor allocation ratio is different than the Commission approved general allocation method, does NSP demonstrate that: 1. its non-regulated activities are insignificant; or 2. its cost allocation principles produce similar results as would allocations following the recommended cost allocation principles; or 3. the public interest is better served by another method? A. Yes. Ms. Schmidt-Petree s Exhibit (JSSP-1), Schedule 10, shows that its NSP s nonregulated operations account for approximately 0.5 percent of NSP-MN s total 2005 actual revenues and 1.3 percent of NSP-MN s 2005 actual operating expenses (excluding purchased fuel, power and gas expenses). Further, she states (page 33, lines 9-11) that The test year 2007 levels are not materially different. Additionally, in response to DOC IR 108 (B) (DOC Exhibit No. (MAS-15), the Company revised Schedule 10 to remove the purchased cost of goods sold from the non-regulated operating expense. The result is that NSP-MN s non-regulated operations account for approximately 0.77 percent of NSP-MN s 2005 actual operating expenses. Department Witness Dale V. Lusti uses this 0.77 percent in his allocation of rate case expense to the non-regulated operations Q. What is your conclusion on Non-Regulated Business Activity Allocations? A. I conclude that NSP s non-regulated activities are insignificant D. COST ALLOCATIONS CONCLUSIONS AND RECOMMENDATIONS Q. Please summarize your cost allocations conclusions and recommendations. A. I have not found anything in my review of the Service Company s allocations or Utility Allocations and related information request responses that cause me to recommend adjustments at this time. I also conclude that NSP s non-regulated activities are St. Pierre Direct / 16

19 insignificant. However, I recommend that the Company meet with the Department to discuss the Utility Allocation of common customer related gas and electric costs (FERC accounts ) before implementing its new customer count methodology in a future rate case. I also recommend that at that meeting, the Company be prepared to demonstrate the effect of using a labor dollar ratio compared to the employee ratio included in the Service Company s Three-Factor Formula used for allocating common costs IV. PENSION EXPENSE Q. What is the level of NSP s Pension expense in the test year? A. Mr. Robinson testifies on page 50, lines that The pension fund remains fully funded and, therefore, there are no pension related expenses included in the 2007 test year Q. Please describe your analysis of Pension expense. A. The Department issued DOC IR Nos. 132 and 154 (see DOC Exhibit Nos. (MAS-19) and (MAS-20), respectively, for the Company s responses regarding pension expense.) Q. What does the response to DOC IR 132 (A) say about the level of Pension expense in the test year? A. There is a total of $135,996 of pension expense included in the 2007 test year. These costs are for nonqualified pension expense of $140,818 and a qualified pension expense of negative $4,822. St. Pierre Direct / 17

20 Q. What did the Department ask in DOC IR 154? A. The Department requested that the Company explain why the test year amount in the current proceeding includes $135,996 of pension expense, when Company Witness Linda K. Erickson s Direct testimony, page 3, in the most recent electric general rate case, indicated that the increased pension benefits are expected to be funded for at least 20 years by excess funds in the pension fund at no cost to ratepayers or shareholders Q. What was the Company s response? A. The Company responded that The primary purpose of Ms. Erickson s testimony in the electric rate case was to explain that qualified pension plan benefits were enhanced at the same time retiree medical benefits were discontinued in order to continue to offer a competitive total compensation package for employees. Further, Ms. Erickson disclosed in her Direct testimony, page 9, as follows: Furthermore, Cost allocations related to NMC [Nuclear Management Company] and Xcel Energy Services Inc. (XES) employees, and the corresponding future cash requirements to fund such allocations, were not significantly affected by the benefit plan changes. The 2006 test year budget includes $359,000 in Service Company pension accrual and $947,000 for NMC. There is no pension expense included in 2006 test-year costs for the Company s employees. Schedule 4-1 of Ms. Erickson s testimony shows the qualified pension cost for NSP-Minnesota employees as $0 for the test year 2006, and also contains a note that the pension costs in the schedule excluded other retirement plan items often grouped with pension costs, such as 401 (k) plan contributions, actuarial and other pension administration costs, etc. Nonqualified pension costs were considered to be part of these other retirement plan items since the testimony was focused on the qualified pension plan changes. St. Pierre Direct / 18

21 Q. What does qualified and nonqualified mean? A. The terms derive their meaning from the Internal Revenue Service (IRS) Code. According to the IRS code, the term qualified means that the expense qualifies for funding and current tax deduction. The term nonqualified means just the opposite. Thus, the nonqualified amount in the test year is not ever fully funded since the amount is not funded Q. What is your conclusion? A. I conclude that including the nonqualified pension plan expense in the 2007 test year is reasonable V. POST RETIREMENT BENEFITS COSTS (FAS 106 Expense) Q. What is NSP s FAS 106 expense in the test year? A. Mr. Robinson testifies on page 50, lines that The 2007 test year level of accrual for Post-retirement Medical Benefits is $909, Q. How did the Company determine the level of test year expense? A. On page 50, lines 15-18, Mr. Robinson states This level of expenses was determined in the same manner used in the most recent electric rate case and relies on the estimated expense level provided by our outside actuaries in accordance with FAS Q. What does Mr. Robinson say about the test year level of FAS 106 expense compared to the last general rate case? St. Pierre Direct / 19

22 1 2 3 A. There has been a decline since the time of our last natural gas rate case, while overall costs have increased since the time of our last natural gas rate case, the amount ultimately allocated to the MN gas utility has declined slightly. (Page 50, lines 18-21) Q. Please describe your analysis of the FAS 106 expense. A. The Department issued DOC IR 133 (see DOC Exhibit No. (MAS-18) for the Company s response regarding FAS 106 expense.) Q. When was the actuarial s report completed that was used to determine the test year FAS 106 costs? A. The Company s response to DOC IR 133 (B) and (C) states that the report was completed June 14, 2006 and that Xcel Energy has not received any updated actuarial reports since that time. Q. What did the Company say in response to DOC IR 133 (E) about the test year level of FAS 106 expense? A. The number presented in testimony should be corrected to reflect a test year indicated amount of $1,222,000 for included FAS 106 costs. The amount included in Mr. Robinson s testimony of $909,000 was based on a calculation that represents only a portion of the total amount included in the test year. Q. With this correction, what are the Minnesota jurisdictional amounts since 2003? A. The Company provided the following jurisdictional computed FAS 106 amounts in its response to DOC IR 133 (E): 2004 test year $1,221, $1,258, $1,216, test year $1,222,000 St. Pierre Direct / 20

23 1 2 Q. What is your response to the level of FAS 106 expense in the 2007 test year? A. The level of FAS 106 expense in the 2007 test year appears reasonable Q. What is your conclusion on the test year level of FAS 106 expense? A. I have not found anything in my review of the FAS 106 expenses and related information request responses that cause me to recommend adjustments at this time. 7 8 VI. BAD DEBT EXPENSE Q A Was bad debt expense an issue or a major concern in the Company s last gas general rate case? No Q. Why is bad debt expense an issue it this general rate case? A. The Department reviewed the bad debt expense since the Company proposes to increase bad debt expense by approximately 100 percent Q. What level of bad debt expense does the Company propose for the 2007 Test Year? A. Company Witness David M. Sparby states on page 10, lines 13-14, that Our 2004 test year bad debt expense for our gas business was $1.6 million, rising to $3.25 million in our 2007 test year. However, the amount included in the Company s response to DOC IR 130 (A) shows that $3,193,887 is included in the test year which reflects the change in the budgeted versus the test year Utility Allocation ratio related to customer counts discussed above in Section III Cost Allocations. St. Pierre Direct / 21

24 Q. Does the Company propose to reduce the test year level of bad debt expense in its Supplemental response to DOC IR 130 (A)? A. Yes. The Company stated that it discovered that the test year data included Energy Markets related bad debt that was incorrectly coded as common utility and should have been coded as electric utility. Further, The corresponding 2007 total Minnesota Jurisdiction gas utility budget should be reduced by $43,546 resulting in a revised total of $3,150,341. Furthermore, Based on this information the Company recommends that the test year bad debt expense be reduced by $44, Q. Do you agree with the Company s recommendation to reduce bad debt expense for this error? A. Yes. Therefore, I recommend that the Commission reduce bad debt expense in the income statement by $43,546 for the electric Energy Markets amount Q. How did the Company determine bad debt expense for the 2007 Test Year? A. Mr. Robinson states on page 44, lines 16-18, that Our bad debt forecast is based on actual results from 2003 to April, 2006, which includes periods of higher and lower priced natural gas.... Also, the Company states in response to OAG IR 15 (a): Xcel Energy currently uses a percentage of accounts receivable by age model to create a provision reserve estimate (bad debt expense) for the allowance for doubtful accounts. The percentage estimates are reviewed periodically and updated if needed Q. What is the test year bad debt expense ratio when compared to sales revenue? A. The ratio is 0.42 percent ($3,150,341 as reduced for electric Energy Markets amount/$749,020,440 Retail revenues). St. Pierre Direct / 22

25 Q. What customer classes pay for bad debt expense in base rates? A. In response to DOC IR 139 (D), the Company states that bad debt expense was allocated to all customer classes in the current rate case, as well as in the previous two gas rate cases (test years 1998 and 2004). Thus, I used Retail revenues in the denominator of the bad debt ratio. Q. Please describe your analysis of bad debt expense. A. Using the Company s responses to DOC IR Nos. 130, , and 142 (DOC Exhibit Nos. (MAS-22) through (MAS-25)), I calculated and reviewed the Company s estimated bad debt expense ratios and actual account write off ratios to examine the annual ratios since (See DOC Exhibit No. (MAS-26) for the Department s bad debt ratio analysis.) Q. Were there any outliers in the data? A. Yes. The year 2004 includes the bankruptcy of one large customer. Response to DOC IR 139 (C) states, The sales revenue amount written-off for the one large bankruptcy in 2004 for Minnesota Gas is $4,350,000. This amount was significant enough to remove the amount as outlier data from 2004 Retail revenue, write-offs, and bad debt expense in order to normalize the data Q. What is the relationship of bad debt expense to Retail revenues? A. The relationship of bad debt expense to Retail revenues from 2002 to 2006 has historically been in the range of 0.29 percent to 0.69 percent. Yr. % St. Pierre Direct / 23

26 This equates to a five-year average of 0.41 percent. For information purposes, if the one large bankruptcy is included in the 2004 data, the bad debt expense ratio for 2004 is 1.01 percent and the five-year average is 0.55 percent Q. What is the relationship of bad debt write offs to Retail revenues? A. The relationship of bad debt write offs to Retail revenues from 2002 to 2006 has historically been in the range of 0.37 percent to 0.65 percent (after normalizing 2004 for one large bankruptcy). Yr. % This equates to a five year average of 0.47 percent. Again, for information purposes, if the one large bankruptcy is included in the 2004 data, the bad debt write off ratio for 2004 is 1.13 percent and the five-year average is 0.62 percent Q. What is your conclusion? A. Excluding the data from the one large bankruptcy in 2004, the Company s 0.42 percent test year bad debt ratio falls within a range of 0.05 percent when compared to the fiveyear average (2002 to 2006) for both the bad debt expense ratio (0.41 percent) and bad debt write-offs ratio (0.47 percent). Based on my analysis, the Company s proposed bad debt expense (reduced for the electric Energy Markets amount of $43,546) is reasonable. St. Pierre Direct / 24

27 VII. SUMMARY OF RECOMMENDATIONS Q. Please summarize your specific recommended adjustments. A. My specific recommended adjustments are as follows: Bad Debt Expense: I recommend that the Commission reduce bad debt expense in the income statement by $43,546 for the electric Energy Markets amount. Q. Please summarize any other specific recommendations that do not contain adjustments at this time. A. My other specific recommendations that do not contain adjustments are as follows: Cost Allocations: I recommend that the Company meet with the Department to discuss the allocation of common customer related gas and electric costs (FERC accounts ) before implementing the new methodology in any future rate case. I also recommend that at that meeting, the Company be prepared to demonstrate the effect of using a labor dollar ratio verses the employee ratio included in the Service Company s Three-Factor Formula used for allocating common costs Q. Does this conclude your testimony? A. Yes. St. Pierre Direct / 25

28 SUMMARY OF EXHIBITS TO THE DIRECT TESTIMONY OF MICHELLE A. ST. PIERRE MPUC Docket No. G002/GR OAH Docket No Description Reference Resume of Michelle St. Pierre...MAS-1 DOC s Service Company Cost Allocation Fluctuation Analysis...MAS-2 Company Response to DOC IR 126 (Service Company Allocations)...MAS-3 Company Response to DOC IR 127 (Service Company Allocations)...MAS-4 Company Response to DOC IR 128 (Service Company Allocations)...MAS-5 Company Response to DOC IR 149 (Service Company Allocations)...MAS-6 Company Response to DOC IR 150 (Service Company Allocations)...MAS-7 Company Response to DOC IR 151 (Service Company Allocations)...MAS-8 DOC s Utility Allocations Fluctuation Analysis...MAS-9 Company Response to DOC IR 107 (Utility Allocations)...MAS-10 Company Response to DOC IR 125 (Utility Allocations)...MAS-11 Company Response to DOC IR 145 (Utility Allocations)...MAS-12 Company Response to DOC IR 146 (Utility Allocations)...MAS-13 DOC s Non-Regulated Business Activity Allocations Fluctuation Analysis...MAS-14 Company Response to DOC IR 108 (Non-Regulated Allocations)...MAS-15 Company Response to DOC IR 123 (Non-Regulated Allocations)...MAS-16 Company Response to DOC IR 124 (Non-Regulated Allocations)...MAS-17

29 SUMMARY OF EXHIBITS TO THE DIRECT TESTIMONY OF MICHELLE A. ST. PIERRE MPUC Docket No. G002/GR OAH Docket No (continued) Description Reference Company Response to DOC IR 147 (Non-Regulated Allocations)...MAS-18 Company Response to DOC IR 132 (Pension Expense)...MAS-19 Company Response to DOC IR 154 (Pension Expense)...MAS-20 Company Response to DOC IR 133 (FAS 106 Expense)...MAS-21 Company Supplemental Response to DOC IR 130 (Bad Debt Expense)...MAS-22 Company Response to DOC IR 136 (Bad Debt Expense)...MAS-23 Company Response to DOC IR 139 (Bad Debt Expense)...MAS-24 Company Response to DOC IR 142 (Bad Debt Expense)...MAS-25 DOC s Bad Debt Ratio Analysis...MAS-26

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

122

123

124

125

126

127

128

129

130

131

132

133

134

135

136

137

138

139

140

141

142

143

144

145

146

147

148

149

150

151

RR1 - Page 181 of 518

DOCKET NO. APPLICATION OF SOUTHWESTERN PUBLIC SERVICE COMPANY FOR AUTHORITY TO CHANGE RATES PUBLIC UTILITY COMMISSION OF TEXAS DIRECT TESTIMONY of JENNIFER S. PYTLIK on behalf of SOUTHWESTERN PUBLIC SERVICE

DOCKET NO. APPLICATION OF SOUTHWESTERN PUBLIC SERVICE COMPANY FOR AUTHORITY TO CHANGE RATES PUBLIC UTILITY COMMISSION OF TEXAS DIRECT TESTIMONY of JENNIFER S. PYTLIK on behalf of SOUTHWESTERN PUBLIC SERVICE

UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION. Public Service Company of Colorado ) Docket No.

Docket No.") Page of UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION Public Service Company of Colorado ) Docket No. ER- -000 PREPARED TESTIMONY OF Deborah A. Blair XCEL ENERGY SERVICES INC.

Page of UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION Public Service Company of Colorado ) Docket No. ER- -000 PREPARED TESTIMONY OF Deborah A. Blair XCEL ENERGY SERVICES INC.

Before the Minnesota Public Utilities Commission State of Minnesota. Docket No. E002/GR Exhibit (CRB-3) Multi-Year Rate Plan

Multi-Year Rate Plan") Surrebuttal Testimony and Schedules Charles R. Burdick Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority

Surrebuttal Testimony and Schedules Charles R. Burdick Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority

RR9 - Page 229 of 510

DOCKET NO. APPLICATION OF SOUTHWESTERN PUBLIC SERVICE COMPANY FOR AUTHORITY TO CHANGE RATES PUBLIC UTILITY COMMISSION OF TEXAS DIRECT TESTIMONY of RICHARD R. SCHRUBBE on behalf of SOUTHWESTERN PUBLIC SERVICE

DOCKET NO. APPLICATION OF SOUTHWESTERN PUBLIC SERVICE COMPANY FOR AUTHORITY TO CHANGE RATES PUBLIC UTILITY COMMISSION OF TEXAS DIRECT TESTIMONY of RICHARD R. SCHRUBBE on behalf of SOUTHWESTERN PUBLIC SERVICE

Before the Minnesota Public Utilities Commission State of Minnesota. Docket No. E002/GR Exhibit (LRP-2) Decoupling and Sales True-Up

Decoupling and Sales True-Up") Rebuttal Testimony and Schedule Lisa R. Peterson Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to Increase

Rebuttal Testimony and Schedule Lisa R. Peterson Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to Increase

Before the Minnesota Public Utilities Commission State of Minnesota. Docket No. E002/GR Exhibit (LRP-1) Decoupling

Decoupling") Direct Testimony and Schedule Lisa R. Peterson Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to Increase

Direct Testimony and Schedule Lisa R. Peterson Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to Increase

BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * * DIRECT TESTIMONY AND ATTACHMENTS OF RICHARD R. SCHRUBBE BEHALF OF

Page of BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * * RE: IN THE MATTER OF ADVICE LETTER NO. -GAS FILED BY PUBLIC SERVICE COMPANY OF COLORADO TO REVISE ITS COLORADO PUC NO.

Page of BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * * RE: IN THE MATTER OF ADVICE LETTER NO. -GAS FILED BY PUBLIC SERVICE COMPANY OF COLORADO TO REVISE ITS COLORADO PUC NO.

Before the Minnesota Public Utilities Commission. State of Minnesota

Direct Testimony and Schedules Jamie L. Jago Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Minnesota Power for Authority to Increase Rates for

Direct Testimony and Schedules Jamie L. Jago Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Minnesota Power for Authority to Increase Rates for

BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) DIRECT TESTIMONY MELISSA L. OSTROM.

) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) DIRECT TESTIMONY MELISSA L. OSTROM.") BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION IN THE MATTER OF SOUTHWESTERN PUBLIC SERVICE COMPANY S APPLICATION REQUESTING APPROVAL TO RETIRE AND ABANDON ITS PLANT X GENERATING STATION UNIT, PLANT

BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION IN THE MATTER OF SOUTHWESTERN PUBLIC SERVICE COMPANY S APPLICATION REQUESTING APPROVAL TO RETIRE AND ABANDON ITS PLANT X GENERATING STATION UNIT, PLANT

Before the Minnesota Public Utilities Commission State of Minnesota. Docket No. E002/GR Exhibit (GET-1)

") Direct Testimony and Schedules George E. Tyson, II Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to

Direct Testimony and Schedules George E. Tyson, II Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to

BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION ) ) ) ) ) ) ) ) ) ) ) DIRECT TESTIMONY RICHARD R. SCHRUBBE. on behalf of

) ) ) ) ) ) ) ) ) ) DIRECT TESTIMONY RICHARD R. SCHRUBBE. on behalf of") BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION IN THE MATTER OF SOUTHWESTERN PUBLIC SERVICE COMPANY S APPLICATION FOR REVISION OF ITS RETAIL RATES UNDER ADVICE NOTICE NO., SOUTHWESTERN PUBLIC SERVICE

BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION IN THE MATTER OF SOUTHWESTERN PUBLIC SERVICE COMPANY S APPLICATION FOR REVISION OF ITS RETAIL RATES UNDER ADVICE NOTICE NO., SOUTHWESTERN PUBLIC SERVICE

Before the Minnesota Public Utilities Commission State of Minnesota. Docket No. E002/GR Exhibit (RRS-1) Pension and Benefits Expense

Pension and Benefits Expense") Direct Testimony and Schedules Richard R. Schrubbe Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to

Direct Testimony and Schedules Richard R. Schrubbe Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to

Before the South Dakota Public Utilities Commission of the State of South Dakota

Direct Testimony and Exhibits Jeff Berzina Before the South Dakota Public Utilities Commission of the State of South Dakota In the Matter of the Application of Black Hills Power, Inc., a South Dakota Corporation

Direct Testimony and Exhibits Jeff Berzina Before the South Dakota Public Utilities Commission of the State of South Dakota In the Matter of the Application of Black Hills Power, Inc., a South Dakota Corporation

RR16 - Page 57 of

DOCKET NO. 43695 APPLICATION OF SOUTHWESTERN PUBLIC SERVICE COMPANY FOR AUTHORITY TO CHANGE RATES PUBLIC UTILITY COMMISSION OF TEXAS DIRECT TESTIMONY of DEBORAH A. BLAIR on behalf of SOUTHWESTERN PUBLIC

DOCKET NO. 43695 APPLICATION OF SOUTHWESTERN PUBLIC SERVICE COMPANY FOR AUTHORITY TO CHANGE RATES PUBLIC UTILITY COMMISSION OF TEXAS DIRECT TESTIMONY of DEBORAH A. BLAIR on behalf of SOUTHWESTERN PUBLIC

Before the Minnesota Public Utilities Commission State of Minnesota. Docket No. E002/GR Exhibit (MCG-1) Customer Care and Bad Debt Expense

Customer Care and Bad Debt Expense") Direct Testimony and Schedules Michael C. Gersack Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to

Direct Testimony and Schedules Michael C. Gersack Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company for Authority to

BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA PUBLIC UTILITY COMMISSION PECO ENERGY COMPANY ELECTRIC DIVISION

PECO ENERGY COMPANY STATEMENT NO. BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA PUBLIC UTILITY COMMISSION v. PECO ENERGY COMPANY ELECTRIC DIVISION DOCKET NO. R-01-0001 DIRECT TESTIMONY

PECO ENERGY COMPANY STATEMENT NO. BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA PUBLIC UTILITY COMMISSION v. PECO ENERGY COMPANY ELECTRIC DIVISION DOCKET NO. R-01-0001 DIRECT TESTIMONY

Trailblazer Pipeline Company LLC Docket No. RP Exhibit No. TPC-0079

Trailblazer Pipeline Company LLC Docket No. RP- -000 UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION Trailblazer Pipeline Company LLC ) ) ) Docket No. RP- -000 SUMMARY OF PREPARED

Trailblazer Pipeline Company LLC Docket No. RP- -000 UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION Trailblazer Pipeline Company LLC ) ) ) Docket No. RP- -000 SUMMARY OF PREPARED

THE STATE OF NEW HAMPSHIRE BEFORE THE PUBLIC UTILITIES COMMISSION NORTHERN UTILITIES, INC. DIRECT TESTIMONY OF LAURENCE M. BROCK

THE STATE OF NEW HAMPSHIRE BEFORE THE PUBLIC UTILITIES COMMISSION DG -0 NORTHERN UTILITIES, INC. DIRECT TESTIMONY OF LAURENCE M. BROCK EXHIBIT LMB- 000 TABLE OF CONTENTS II. III. IV. V. A. B. C. D. A.

THE STATE OF NEW HAMPSHIRE BEFORE THE PUBLIC UTILITIES COMMISSION DG -0 NORTHERN UTILITIES, INC. DIRECT TESTIMONY OF LAURENCE M. BROCK EXHIBIT LMB- 000 TABLE OF CONTENTS II. III. IV. V. A. B. C. D. A.

BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA PUBLIC UTILITY COMMISSION PECO ENERGY COMPANY ELECTRIC DIVISION

PECO ENERGY COMPANY STATEMENT NO. BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA PUBLIC UTILITY COMMISSION v. PECO ENERGY COMPANY ELECTRIC DIVISION DOCKET NO. R-01-1 DIRECT TESTIMONY WITNESS:

PECO ENERGY COMPANY STATEMENT NO. BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA PUBLIC UTILITY COMMISSION v. PECO ENERGY COMPANY ELECTRIC DIVISION DOCKET NO. R-01-1 DIRECT TESTIMONY WITNESS:

RR9 - Page 356 of 510

DOCKET NO. APPLICATION OF SOUTHWESTERN PUBLIC SERVICE COMPANY FOR AUTHORITY TO CHANGE RATES PUBLIC UTILITY COMMISSION OF TEXAS DIRECT TESTIMONY of JEFFREY C. KLEIN on behalf of SOUTHWESTERN PUBLIC SERVICE

DOCKET NO. APPLICATION OF SOUTHWESTERN PUBLIC SERVICE COMPANY FOR AUTHORITY TO CHANGE RATES PUBLIC UTILITY COMMISSION OF TEXAS DIRECT TESTIMONY of JEFFREY C. KLEIN on behalf of SOUTHWESTERN PUBLIC SERVICE

DOCKET NO. 13A-0773EG DIRECT TESTIMONY AND EXHIBITS OF LEE E. GABLER

IN THE MATTER OF THE APPLICATION OF PUBLIC SERVICE COMPANY OF COLORADO FOR APPROVAL OF ITS ELECTRIC AND NATURAL GAS DEMAND-SIDE MANAGEMENT (DSM PLAN FOR THE CALENDAR YEAR 0 AND TO CHANGE ITS ELECTRIC AND

IN THE MATTER OF THE APPLICATION OF PUBLIC SERVICE COMPANY OF COLORADO FOR APPROVAL OF ITS ELECTRIC AND NATURAL GAS DEMAND-SIDE MANAGEMENT (DSM PLAN FOR THE CALENDAR YEAR 0 AND TO CHANGE ITS ELECTRIC AND

BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * *

BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * * RE: IN THE MATTER OF ADVICE LETTER NO. 1-ELECTRIC FILED BY PUBLIC SERVICE COMPANY OF COLORADO TO REVISE ITS COLORADO PUC NO. -ELECTRIC

BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * * RE: IN THE MATTER OF ADVICE LETTER NO. 1-ELECTRIC FILED BY PUBLIC SERVICE COMPANY OF COLORADO TO REVISE ITS COLORADO PUC NO. -ELECTRIC

RR16 - Page 1 of

DOCKET NO. APPLICATION OF SOUTHWESTERN PUBLIC SERVICE COMPANY FOR AUTHORITY TO CHANGE RATES PUBLIC UTILITY COMMISSION OF TEXAS DIRECT TESTIMONY of ARTHUR P. FREITAS on behalf of SOUTHWESTERN PUBLIC SERVICE

DOCKET NO. APPLICATION OF SOUTHWESTERN PUBLIC SERVICE COMPANY FOR AUTHORITY TO CHANGE RATES PUBLIC UTILITY COMMISSION OF TEXAS DIRECT TESTIMONY of ARTHUR P. FREITAS on behalf of SOUTHWESTERN PUBLIC SERVICE

BEFORE THE MINNESOTA OFFICE OF ADMINISTRATIVE HEARINGS 600 North Robert Street St. Paul, MN 55101

BEFORE THE MINNESOTA OFFICE OF ADMINISTRATIVE HEARINGS 00 North Robert Street St. Paul, MN 1 FOR THE MINNESOTA PUBLIC UTILITIES COMMISSION th Place East, Suite 0 St Paul MN 1-1 IN THE MATTER OF THE APPLICATION

BEFORE THE MINNESOTA OFFICE OF ADMINISTRATIVE HEARINGS 00 North Robert Street St. Paul, MN 1 FOR THE MINNESOTA PUBLIC UTILITIES COMMISSION th Place East, Suite 0 St Paul MN 1-1 IN THE MATTER OF THE APPLICATION

PUC DOCKET NO. BEFORE THE PUBLIC UTILITY COMMISSION OF TEXAS APPLICATION OF TEXAS-NEW MEXICO POWER COMPANY FOR AUTHORITY TO CHANGE RATES

BEFORE THE PUBLIC UTILITY COMMISSION OF TEXAS APPLICATION OF TEXAS-NEW MEXICO POWER COMPANY FOR AUTHORITY TO CHANGE RATES PREPARED DIRECT TESTIMONY AND EXHIBITS OF YANNICK GAGNE MAY 0, 0 0v. TABLE OF CONTENTS

BEFORE THE PUBLIC UTILITY COMMISSION OF TEXAS APPLICATION OF TEXAS-NEW MEXICO POWER COMPANY FOR AUTHORITY TO CHANGE RATES PREPARED DIRECT TESTIMONY AND EXHIBITS OF YANNICK GAGNE MAY 0, 0 0v. TABLE OF CONTENTS

BEFORE THE MINNESOTA OFFICE OF ADMINISTRATIVE HEARINGS 600 North Robert Street St. Paul, MN 55101

BEFORE THE MINNESOTA OFFICE OF ADMINISTRATIVE HEARINGS 00 North Robert Street St. Paul, MN 1 FOR THE MINNESOTA PUBLIC UTILITIES COMMISSION th Place East, Suite 0 St Paul MN 1-1 IN THE MATTER OF THE APPLICATION

BEFORE THE MINNESOTA OFFICE OF ADMINISTRATIVE HEARINGS 00 North Robert Street St. Paul, MN 1 FOR THE MINNESOTA PUBLIC UTILITIES COMMISSION th Place East, Suite 0 St Paul MN 1-1 IN THE MATTER OF THE APPLICATION

BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * * DIRECT TESTIMONY AND ATTACHMENTS OF LISA H.

Page of BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * * RE: IN THE MATTER OF ADVICE LETTER NO. -ELECTRIC FILED BY PUBLIC SERVICE COMPANY OF COLORADO TO REVISE ITS PUC NO. -ELECTRIC

Page of BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * * RE: IN THE MATTER OF ADVICE LETTER NO. -ELECTRIC FILED BY PUBLIC SERVICE COMPANY OF COLORADO TO REVISE ITS PUC NO. -ELECTRIC

Minnesota Public Utilities Commission Staff Briefing Papers

Minnesota Public Utilities Commission Staff Briefing Papers Meeting Date: March 6, 2014... Agenda Item # *6 Company: Docket No. Northern States Power Company d/b/a Xcel Energy E-002/GR-10-971 In the Matter

Minnesota Public Utilities Commission Staff Briefing Papers Meeting Date: March 6, 2014... Agenda Item # *6 Company: Docket No. Northern States Power Company d/b/a Xcel Energy E-002/GR-10-971 In the Matter

BEFORE THE MINNESOTA OFFICE OF THE ADMINISTRATIVE HEARINGS 600 North Robert Street St. Paul, Minnesota 55101

BEFORE THE MINNESOTA OFFICE OF THE ADMINISTRATIVE HEARINGS 00 North Robert Street St. Paul, Minnesota FOR THE MINNESOTA PUBLIC UTILITIES COMMISSION th Place East Suite 0 St. Paul, Minnesota - MPUC Docket

BEFORE THE MINNESOTA OFFICE OF THE ADMINISTRATIVE HEARINGS 00 North Robert Street St. Paul, Minnesota FOR THE MINNESOTA PUBLIC UTILITIES COMMISSION th Place East Suite 0 St. Paul, Minnesota - MPUC Docket

XceI Energy. Mnneota. Northern States Power Company. Betore the. Mllnnesota corporaton. FVhnnesota Pubhc UUhhes Commsson

XceI Energy Northern States Power Company Mllnnesota corporaton Betore the ti FVhnnesota Pubhc UUhhes Commsson Apphcaton for Authonty to ncrease Eoctrc Rates Mnneota Docket No EOO2/GR 826 Budget Summary

XceI Energy Northern States Power Company Mllnnesota corporaton Betore the ti FVhnnesota Pubhc UUhhes Commsson Apphcaton for Authonty to ncrease Eoctrc Rates Mnneota Docket No EOO2/GR 826 Budget Summary

INVESTOR RELATIONS EARNINGS RELEASE XCEL ENERGY ANNOUNCES FIRST QUARTER 2006 EARNINGS

U.S. Bancorp Center 800 Nicollet Mall Minneapolis, MN 55402-2023 April 27, 2006 INVESTOR RELATIONS EARNINGS RELEASE XCEL ENERGY ANNOUNCES FIRST QUARTER 2006 EARNINGS MINNEAPOLIS Xcel Energy Inc. (NYSE:

U.S. Bancorp Center 800 Nicollet Mall Minneapolis, MN 55402-2023 April 27, 2006 INVESTOR RELATIONS EARNINGS RELEASE XCEL ENERGY ANNOUNCES FIRST QUARTER 2006 EARNINGS MINNEAPOLIS Xcel Energy Inc. (NYSE:

March 25, 2016 VIA ELECTRONIC FILING

James P. Johnson Assistant General Counsel 414 Nicollet Mall, 5 th Floor Minneapolis, Minnesota 55401 Phone: 612-215-4592 Fax: 612-215-4544 James.P.Johnson@xcelenergy.com VIA ELECTRONIC FILING Honorable

James P. Johnson Assistant General Counsel 414 Nicollet Mall, 5 th Floor Minneapolis, Minnesota 55401 Phone: 612-215-4592 Fax: 612-215-4544 James.P.Johnson@xcelenergy.com VIA ELECTRONIC FILING Honorable

BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION

BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION IN THE MATTER OF SOUTHWESTERN PUBLIC SERVICE COMPANY S APPLICATION FOR APPROVAL OF ITS 2009 ENERGY EFFICIENCY AND LOAD MANAGEMENT PLAN AND ASSOCIATED

BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION IN THE MATTER OF SOUTHWESTERN PUBLIC SERVICE COMPANY S APPLICATION FOR APPROVAL OF ITS 2009 ENERGY EFFICIENCY AND LOAD MANAGEMENT PLAN AND ASSOCIATED

Q. PLEASE STATE YOUR NAME AND BUSINESS ADDRESS. A. My name is Suzanne E. Sieferman, and my business address is 1000 East Main

TESTIMONY OF, MANAGER RATES AND REGULATORY STRATEGY ON BEHALF OF DUKE ENERGY INDIANA, LLC CAUSE NO. BEFORE THE INDIANA UTILITY REGULATORY COMMISSION 0 I. INTRODUCTION Q. PLEASE STATE YOUR NAME AND BUSINESS

TESTIMONY OF, MANAGER RATES AND REGULATORY STRATEGY ON BEHALF OF DUKE ENERGY INDIANA, LLC CAUSE NO. BEFORE THE INDIANA UTILITY REGULATORY COMMISSION 0 I. INTRODUCTION Q. PLEASE STATE YOUR NAME AND BUSINESS

BEFORE THE PUBLIC SERVICE COMMISSION OF WISCONSIN

BEFORE THE PUBLIC SERVICE COMMISSION OF WISCONSIN Application of Wisconsin Public Service Corporation for ) Authority to Adjust Electric and Natural Gas Rates ) 0-UR- Rebuttal Testimony of Rick J. Moras

BEFORE THE PUBLIC SERVICE COMMISSION OF WISCONSIN Application of Wisconsin Public Service Corporation for ) Authority to Adjust Electric and Natural Gas Rates ) 0-UR- Rebuttal Testimony of Rick J. Moras

BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) DIRECT TESTIMONY RUTH M. SAKYA.

) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) DIRECT TESTIMONY RUTH M. SAKYA.") BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION IN THE MATTER OF SOUTHWESTERN PUBLIC SERVICE COMPANY S APPLICATION REQUESTING: (1) ACKNOWLEDGEMENT OF ITS FILING OF THE 2016 ANNUAL RENEWABLE ENERGY PORTFOLIO

BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION IN THE MATTER OF SOUTHWESTERN PUBLIC SERVICE COMPANY S APPLICATION REQUESTING: (1) ACKNOWLEDGEMENT OF ITS FILING OF THE 2016 ANNUAL RENEWABLE ENERGY PORTFOLIO

New York Investor Meetings

New York Investor Meetings May 10, 2016 Safe Harbor Except for the historical statements contained in this release, the matters discussed herein, are forwardlooking statements that are subject to certain

New York Investor Meetings May 10, 2016 Safe Harbor Except for the historical statements contained in this release, the matters discussed herein, are forwardlooking statements that are subject to certain

Otter Tail Power Company Minnesota General Rate Case Documents Docket No. E017/GR

Volume 3 Index 1/3 Otter Tail Power Company Minnesota General Rate Case Documents Docket No. E17/GR-15-133 Volume 1 Notice of Change in Rates Interim Rate Petition Index Filing Letter Notice of Change

Volume 3 Index 1/3 Otter Tail Power Company Minnesota General Rate Case Documents Docket No. E17/GR-15-133 Volume 1 Notice of Change in Rates Interim Rate Petition Index Filing Letter Notice of Change

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * *

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * * In the matter of the application of ) MICHIGAN GAS UTILITIES CORPORATION ) for authority to increase retail natural gas rates )

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * * In the matter of the application of ) MICHIGAN GAS UTILITIES CORPORATION ) for authority to increase retail natural gas rates )

Miller, Canfield, Paddock and Stone, P.L.C. One Michigan Avenue, Suite 900 Lansing, Michigan TEL (517) FAX (517)

FAX (517)") Founded in 185 by Sidney Davy Miller SHERRI A. WELLMAN TEL (517) 8-95 FAX (517) 7-60 E-MAIL wellmans@millercanfield.com Miller, Canfield, Paddock and Stone, P.L.C. One Michigan Avenue, Suite 900 Lansing,

Founded in 185 by Sidney Davy Miller SHERRI A. WELLMAN TEL (517) 8-95 FAX (517) 7-60 E-MAIL wellmans@millercanfield.com Miller, Canfield, Paddock and Stone, P.L.C. One Michigan Avenue, Suite 900 Lansing,

The following table provides a reconciliation of ongoing earnings per share to GAAP earnings per share:

Xcel Energy Second Quarter 2011 Earnings Report Ongoing 2011 second quarter earnings per share were $0.33 compared with $0.29 in 2010. GAAP (generally accepted accounting principles) 2011 second quarter

Xcel Energy Second Quarter 2011 Earnings Report Ongoing 2011 second quarter earnings per share were $0.33 compared with $0.29 in 2010. GAAP (generally accepted accounting principles) 2011 second quarter

STATE OF NEW JERSEY BOARD OF PUBLIC UTILITIES

STATE OF NEW JERSEY BOARD OF PUBLIC UTILITIES In The Matter of the Petition of Public Service Electric and Gas Company for Approval of an Increase in Electric and Gas Rates and For Changes In the Tariffs

STATE OF NEW JERSEY BOARD OF PUBLIC UTILITIES In The Matter of the Petition of Public Service Electric and Gas Company for Approval of an Increase in Electric and Gas Rates and For Changes In the Tariffs

BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * *

BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * * RE: IN THE MATTER OF ADVICE ) LETTER NO. 1672-ELECTRIC FILED BY ) PUBLIC SERVICE COMPANY OF ) PROCEEDING NO. 14AL-0660E COLORADO

BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * * RE: IN THE MATTER OF ADVICE ) LETTER NO. 1672-ELECTRIC FILED BY ) PUBLIC SERVICE COMPANY OF ) PROCEEDING NO. 14AL-0660E COLORADO

BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION ) ) ) ) ) ) ) ) ) ) ) DIRECT TESTIMONY RUTH M. SAKYA. on behalf of.

) ) ) ) ) ) ) ) ) ) DIRECT TESTIMONY RUTH M. SAKYA. on behalf of.") BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION IN THE MATTER OF SOUTHWESTERN PUBLIC SERVICE COMPANY S INTERIM REPORT ON ITS PARTICIPATION IN THE SOUTHWEST POWER POOL REGIONAL TRANSMISSION ORGANIZATION,

BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION IN THE MATTER OF SOUTHWESTERN PUBLIC SERVICE COMPANY S INTERIM REPORT ON ITS PARTICIPATION IN THE SOUTHWEST POWER POOL REGIONAL TRANSMISSION ORGANIZATION,

Minnesota Public Utilities Commission

Minnesota Public Utilities Commission Staff Briefing Papers Meeting Date: January 6, 2011........................ Agenda Item #. Company: Docket No. Issue: Xcel Energy E,G-002/S-10-1158 In the Matter of

Minnesota Public Utilities Commission Staff Briefing Papers Meeting Date: January 6, 2011........................ Agenda Item #. Company: Docket No. Issue: Xcel Energy E,G-002/S-10-1158 In the Matter of

1 Q. What are the ratemaking consequences of the sale of the distribution assets?

Exhibit SPS-AXM 2-14(b)(1) Page 86 of 91 1 Q. What are the ratemaking consequences of the sale of the distribution assets? 2 A. There are two consequences. First, SPS expects to experience a gain on the

Exhibit SPS-AXM 2-14(b)(1) Page 86 of 91 1 Q. What are the ratemaking consequences of the sale of the distribution assets? 2 A. There are two consequences. First, SPS expects to experience a gain on the

BEFORE THE PUBLIC SERVICE COMMISSION OF THE STATE OF UTAH ROCKY MOUNTAIN POWER. Direct Testimony of Michael G. Wilding

Rocky Mountain Power Docket No. 18-035-01 Witness: Michael G. Wilding BEFORE THE PUBLIC SERVICE COMMISSION OF THE STATE OF UTAH ROCKY MOUNTAIN POWER Direct Testimony of Michael G. Wilding March 2018 1

Rocky Mountain Power Docket No. 18-035-01 Witness: Michael G. Wilding BEFORE THE PUBLIC SERVICE COMMISSION OF THE STATE OF UTAH ROCKY MOUNTAIN POWER Direct Testimony of Michael G. Wilding March 2018 1

2015 General Rate Case

Application No.: Exhibit No.: Witnesses: A.--00 SCE-0, Vol. 0, Pt. 1 M. Bennett G. Henry J. Trapp R. Worden (U -E) 01 General Rate Case ERRATA Human Resources (HR) Volume, Part 1 Benefits and Other Compensation

Application No.: Exhibit No.: Witnesses: A.--00 SCE-0, Vol. 0, Pt. 1 M. Bennett G. Henry J. Trapp R. Worden (U -E) 01 General Rate Case ERRATA Human Resources (HR) Volume, Part 1 Benefits and Other Compensation

UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION

UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION Exhibit No. PNM- Page of Public Service Company of New Mexico ) Docket No. ER - -000 PREPARED INITIAL TESTIMONY OF TERRY R. HORN

UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION Exhibit No. PNM- Page of Public Service Company of New Mexico ) Docket No. ER - -000 PREPARED INITIAL TESTIMONY OF TERRY R. HORN

RR4-132 of 571. Attachment TSM-RR-B Page87of SPS Rate Case

RR4-132 of 571 Attachment TSM-RR-B Page87of 97 2008 SPS Rate Case Attachment TSM-RR-B Page 88 of 97 2008 SPS Rate Case I J Attachment TSM-RR-B Page 91 of 97 2008 SPS Rate Case Attachment TSM-RR-B Page92

RR4-132 of 571 Attachment TSM-RR-B Page87of 97 2008 SPS Rate Case Attachment TSM-RR-B Page 88 of 97 2008 SPS Rate Case I J Attachment TSM-RR-B Page 91 of 97 2008 SPS Rate Case Attachment TSM-RR-B Page92

Before the Minnesota Public Utilities Commission State of Minnesota

U-l Direct Testimony and Schedules Janet S. Schmidt-Petree Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company d/h/a Xcel

U-l Direct Testimony and Schedules Janet S. Schmidt-Petree Before the Minnesota Public Utilities Commission State of Minnesota In the Matter of the Application of Northern States Power Company d/h/a Xcel

Attachment 3 - PECO Statement No. 2 Direct Testimony and Exhibits of Alan B. Cohn

Attachment 3 - PECO Statement No. 2 Direct Testimony and Exhibits of Alan B. Cohn PECO ENERGY COMPANY STATEMENT NO. 2 BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PETITION OF PECO ENERGY COMPANY FOR

Attachment 3 - PECO Statement No. 2 Direct Testimony and Exhibits of Alan B. Cohn PECO ENERGY COMPANY STATEMENT NO. 2 BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PETITION OF PECO ENERGY COMPANY FOR

Niagara Mohawk Power Corporation d/b/a National Grid

Niagara Mohawk Power Corporation d/b/a National Grid PROCEEDING ON MOTION OF THE COMMISSION AS TO THE RATES, CHARGES, RULES AND REGULATIONS OF NIAGARA MOHAWK POWER CORPORATION FOR ELECTRIC AND GAS SERVICE

Niagara Mohawk Power Corporation d/b/a National Grid PROCEEDING ON MOTION OF THE COMMISSION AS TO THE RATES, CHARGES, RULES AND REGULATIONS OF NIAGARA MOHAWK POWER CORPORATION FOR ELECTRIC AND GAS SERVICE

BEFORE THE ARKANSAS PUBLIC SERVICE COMMISSION

BEFORE THE ARKANSAS PUBLIC SERVICE COMMISSION IN THE MATTER OF THE APPLICATION OF ) FOR APPROVAL ) OF CHANGES IN RATES FOR RETAIL ) ELECTRIC SERVICE ) DIRECT TESTIMONY OF RONALD G. GARNER, CDP SENIOR CAPITAL

BEFORE THE ARKANSAS PUBLIC SERVICE COMMISSION IN THE MATTER OF THE APPLICATION OF ) FOR APPROVAL ) OF CHANGES IN RATES FOR RETAIL ) ELECTRIC SERVICE ) DIRECT TESTIMONY OF RONALD G. GARNER, CDP SENIOR CAPITAL

THE STATE OF NEW HAMPSHIRE BEFORE THE PUBLIC UTILITIES COMMISSION NORTHERN UTILITIES, INC. DIRECT TESTIMONY OF DAVID L. CHONG

THE STATE OF NEW HAMPSHIRE BEFORE THE PUBLIC UTILITIES COMMISSION DG -0 NORTHERN UTILITIES, INC. DIRECT TESTIMONY OF DAVID L. CHONG EXHIBIT DLC- 0000 Table of Contents INTRODUCTION... SUMMARY OF TESTIMONY...

THE STATE OF NEW HAMPSHIRE BEFORE THE PUBLIC UTILITIES COMMISSION DG -0 NORTHERN UTILITIES, INC. DIRECT TESTIMONY OF DAVID L. CHONG EXHIBIT DLC- 0000 Table of Contents INTRODUCTION... SUMMARY OF TESTIMONY...

UGI UTILITIES, INC. GAS DIVISION

UGI UTILITIES, INC. GAS DIVISION BOOK IV BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION Information Submitted Pursuant to Section 53.51 et seq of the Commission s Regulations UGI GAS STATEMENT NO. 8

UGI UTILITIES, INC. GAS DIVISION BOOK IV BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION Information Submitted Pursuant to Section 53.51 et seq of the Commission s Regulations UGI GAS STATEMENT NO. 8

STATE OF MINNESOTA BEFORE THE MINNESOTA PUBLIC UTILITIES COMMISSION. LeRoy Koppendrayer

STATE OF MINNESOTA BEFORE THE MINNESOTA PUBLIC UTILITIES COMMISSION LeRoy Koppendrayer Ellen Gavin Marshall Johnson Phyllis Reha Gregory Scott Chair Commissioner Commissioner Commissioner Commissioner

STATE OF MINNESOTA BEFORE THE MINNESOTA PUBLIC UTILITIES COMMISSION LeRoy Koppendrayer Ellen Gavin Marshall Johnson Phyllis Reha Gregory Scott Chair Commissioner Commissioner Commissioner Commissioner

STATE OF VERMONT PUBLIC UTILITY COMMISSION ) ) ) ) PREFILED TESTIMONY OF LAUREN HAMMER ON BEHALF OF VERMONT GAS SYSTEMS, INC.

) ) ) PREFILED TESTIMONY OF LAUREN HAMMER ON BEHALF OF VERMONT GAS SYSTEMS, INC.") STATE OF VERMONT PUBLIC UTILITY COMMISSION Petition of Vermont Gas Systems, Inc. for change in rates, and for use of the System Reliability and Expansion Fund in connection therewith ) ) ) ) PREFILED TESTIMONY

STATE OF VERMONT PUBLIC UTILITY COMMISSION Petition of Vermont Gas Systems, Inc. for change in rates, and for use of the System Reliability and Expansion Fund in connection therewith ) ) ) ) PREFILED TESTIMONY

BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * *

Page of BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * * RE: IN THE MATTER OF ADVICE LETTER NO. -GAS FILED BY PUBLIC SERVICE COMPANY OF COLORADO TO REVISE ITS COLORADO PUC NO.

Page of BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * * RE: IN THE MATTER OF ADVICE LETTER NO. -GAS FILED BY PUBLIC SERVICE COMPANY OF COLORADO TO REVISE ITS COLORADO PUC NO.

BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION ) ) ) ) ) ) ) ) ) ) DIRECT TESTIMONY JANNELL E. MARKS. on behalf of

) ) ) ) ) ) ) ) ) DIRECT TESTIMONY JANNELL E. MARKS. on behalf of") BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION IN THE MATTER OF SOUTHWESTERN PUBLIC SERVICE COMPANY S APPLICATION FOR REVISION OF ITS RETAIL RATES UNDER ADVICE NOTICE NO., SOUTHWESTERN PUBLIC SERVICE

BEFORE THE NEW MEXICO PUBLIC REGULATION COMMISSION IN THE MATTER OF SOUTHWESTERN PUBLIC SERVICE COMPANY S APPLICATION FOR REVISION OF ITS RETAIL RATES UNDER ADVICE NOTICE NO., SOUTHWESTERN PUBLIC SERVICE

PUC DOCKET NO. BEFORE THE PUBLIC UTILITY COMMISSION OF TEXAS APPLICATION OF TEXAS-NEW MEXICO POWER COMPANY FOR AUTHORITY TO CHANGE RATES

PUC DOCKET NO. BEFORE THE PUBLIC UTILITY COMMISSION OF TEXAS APPLICATION OF TEXAS-NEW MEXICO POWER COMPANY FOR AUTHORITY TO CHANGE RATES PREPARED DIRECT TESTIMONY AND EXHIBITS OF EMMANUEL J. LOPEZ ON BEHALF

PUC DOCKET NO. BEFORE THE PUBLIC UTILITY COMMISSION OF TEXAS APPLICATION OF TEXAS-NEW MEXICO POWER COMPANY FOR AUTHORITY TO CHANGE RATES PREPARED DIRECT TESTIMONY AND EXHIBITS OF EMMANUEL J. LOPEZ ON BEHALF

SOCALGAS DIRECT TESTIMONY OF GARRY G. YEE RATE BASE. November 2014

Company: Southern California Gas Company (U 0 G) Proceeding: 01 General Rate Case Application: A.1-- Exhibit: SCG- SOCALGAS DIRECT TESTIMONY OF GARRY G. YEE RATE BASE November 01 BEFORE THE PUBLIC UTILITIES

Company: Southern California Gas Company (U 0 G) Proceeding: 01 General Rate Case Application: A.1-- Exhibit: SCG- SOCALGAS DIRECT TESTIMONY OF GARRY G. YEE RATE BASE November 01 BEFORE THE PUBLIC UTILITIES

STATE OF NEW JERSEY OFFICE OF ADMINISTRATIVE LAW BEFORE THE HONORABLE WALTER J. BRASWELL ) ) ) ) ) ) ) ) ) ) ) ) ) )

) ) ) ) ) ) ) ) ) ) ) ) )") STATE OF NEW JERSEY OFFICE OF ADMINISTRATIVE LAW BEFORE THE HONORABLE WALTER J. BRASWELL I/M/O THE PETITION OF PUBLIC SERVICE ELECTRIC AND GAS COMPANY FOR APPROVAL OF AN INCREASE IN ELECTRIC AND GAS RATES

STATE OF NEW JERSEY OFFICE OF ADMINISTRATIVE LAW BEFORE THE HONORABLE WALTER J. BRASWELL I/M/O THE PETITION OF PUBLIC SERVICE ELECTRIC AND GAS COMPANY FOR APPROVAL OF AN INCREASE IN ELECTRIC AND GAS RATES

BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION. PENNSYLVANIA POWER COMPANY Docket No. R Direct Testimony of Richard A.

Penn Power Statement No. 2 BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA POWER COMPANY Docket No. R-2016-2537355 Direct Testimony of Richard A. D'Angelo List of Topics Addressed Accounting

Penn Power Statement No. 2 BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA POWER COMPANY Docket No. R-2016-2537355 Direct Testimony of Richard A. D'Angelo List of Topics Addressed Accounting

BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION. PENNSYLVANIA ELECTRIC COMPANY Docket No. R Direct Testimony of Richard A.

Penelec Statement No. 2 BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA ELECTRIC COMPANY Docket No. R-2016-2537352 Direct Testimony of Richard A. D'Angelo List of Topics Addressed Accounting

Penelec Statement No. 2 BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA ELECTRIC COMPANY Docket No. R-2016-2537352 Direct Testimony of Richard A. D'Angelo List of Topics Addressed Accounting

EXETER ASSOCIATES, INC Little Patuxent Parkway Suite 300 Columbia, Maryland 21044

OCA STATEMENT BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION Pennsylvania Public Utility Commission v. United Water Pennsylvania, Inc. ) ) ) Docket No. R-01-67 DIRECT TESTIMONY OF JENNIFER L. ROGERS

OCA STATEMENT BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION Pennsylvania Public Utility Commission v. United Water Pennsylvania, Inc. ) ) ) Docket No. R-01-67 DIRECT TESTIMONY OF JENNIFER L. ROGERS

BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION METROPOLITAN EDISON COMPANY DOCKET NO. R Direct Testimony of Jeffrey L.

Met-Ed Statement No. 5 BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION METROPOLITAN EDISON COMPANY DOCKET NO. R-2016-2537349 Direct Testimony of Jeffrey L. Adams List of Topics Addressed Cash Working

Met-Ed Statement No. 5 BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION METROPOLITAN EDISON COMPANY DOCKET NO. R-2016-2537349 Direct Testimony of Jeffrey L. Adams List of Topics Addressed Cash Working

BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO * * * * * ) ) ) ) ) DIRECT TESTIMONY OF JEFFREY C.

) ) ) ) DIRECT TESTIMONY OF JEFFREY C.") Page of BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO IN THE MATTER OF THE APPLICATION OF PUBLIC SERVICE COMPANY OF COLORADO FOR APPROVAL OF ITS 0 0 RENEWABLE ENERGY COMPLIANCE PLAN *

Page of BEFORE THE PUBLIC UTILITIES COMMISSION OF THE STATE OF COLORADO IN THE MATTER OF THE APPLICATION OF PUBLIC SERVICE COMPANY OF COLORADO FOR APPROVAL OF ITS 0 0 RENEWABLE ENERGY COMPLIANCE PLAN *

Xcel Energy Fixed Income Meetings

Xcel Energy Fixed Income Meetings February 1-2, 2016 Safe Harbor Except for the historical statements contained in this release, the matters discussed herein, are forwardlooking statements that are subject

Xcel Energy Fixed Income Meetings February 1-2, 2016 Safe Harbor Except for the historical statements contained in this release, the matters discussed herein, are forwardlooking statements that are subject

RRl of

Commission/Docket Type of Proceeding Testimony FERC ER08-313E SPS Wholesale Transmission Rebuttal Testimony Formula ER10-192 PSCO Wholesale Production Direct Testimony Formula ER11-2853 PSCO Wholesale

Commission/Docket Type of Proceeding Testimony FERC ER08-313E SPS Wholesale Transmission Rebuttal Testimony Formula ER10-192 PSCO Wholesale Production Direct Testimony Formula ER11-2853 PSCO Wholesale

CASE NO.: ER Surrebuttal Testimony of Bruce E. Biewald. On Behalf of Sierra Club

Exhibit No.: Issue: Planning Prudence and Rates Witness: Bruce Biewald Type of Exhibit: Surrebuttal Testimony Sponsoring Party: Sierra Club Case No.: ER-0-0 Date Testimony Prepared: October, 0 MISSOURI

Exhibit No.: Issue: Planning Prudence and Rates Witness: Bruce Biewald Type of Exhibit: Surrebuttal Testimony Sponsoring Party: Sierra Club Case No.: ER-0-0 Date Testimony Prepared: October, 0 MISSOURI

Rocky Mountain Power Docket No Witness: Douglas K. Stuver BEFORE THE PUBLIC SERVICE COMMISSION OF THE STATE OF UTAH ROCKY MOUNTAIN POWER