ALPHA BANK ROMANIA S.A. FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2017

|

|

|

- Bridget Rice

- 5 years ago

- Views:

Transcription

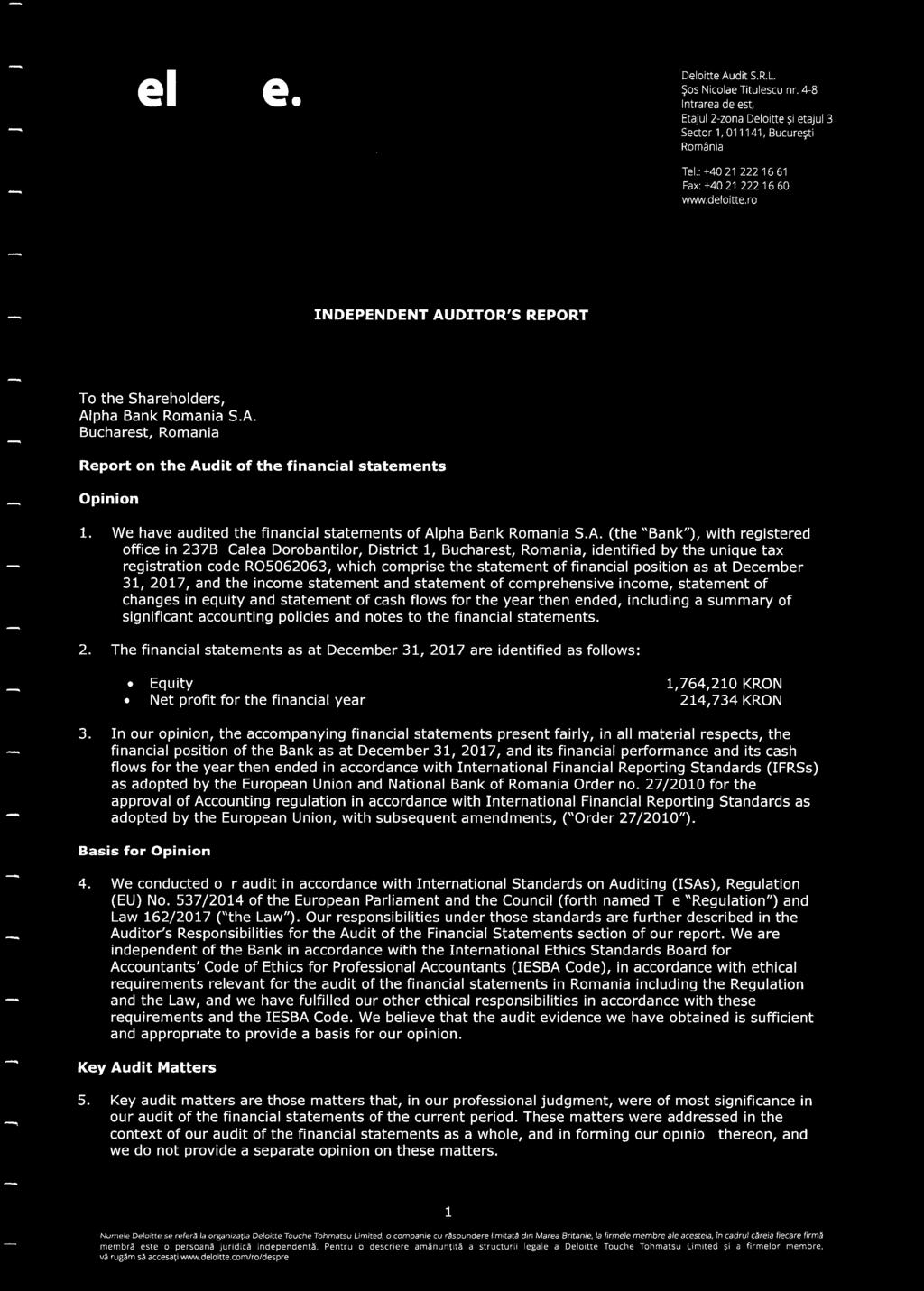

1 ALPHA BANK ROMANIA S.A. FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS AS ENDORSED BY THE EUROPEAN UNION

2 CONTENTS PAGE INDEPENDENT AUDITORS REPORT 1 6 INCOME STATEMENT 7 STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME 8 STATEMENT OF FINANCIAL POSITION 9 STATEMENT OF CHANGES IN EQUITY 10 STATEMENT OF CASH FLOWS

3

4

5

6

7

8

9 INCOME STATEMENT (all amounts are expressed in RON thousand ( RON 000 ) Note Year ended 2017 RON 000 Year ended 2016* RON 000 Interest and similar income 7 493, ,639 Interest expense 7 (87,676) (88,760) Net interest income 406, ,879 Fee and commission income 8 94,775 91,826 Fee and commission expense 8 (17,791) (15,372) Net fee and commission income 76,984 76,454 Dividend income 886 3,035 Gains less losses on financial transactions 9 104,869 94,884 Other operating income 8,315 7,320 Net operating income 597, ,572 Net impairment gain/(loss) on financial assets 10 41,390 (85,829) Staff costs 11 (160,534) (149,732) Depreciation and amortization 17 (17,090) (15,773) Other operating expenses 12 (204,321) (204,350) Operating expenses (340,555) (455,684) Share from loss of associates (150) (216) Profit before tax 256, ,672 Income tax expense 26 (41,675) (7,294) Net profit for period 214, ,378 *See note 2f) The financial statements were authorized for issue by the Board of Directors on 18 April 2018 and were signed on its behalf by: Sergiu Oprescu Executive President Gabriel Mateescu Executive Financial Vice-president The accompanying notes form an integral part of these financial statements. 7

10 STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME (all amounts are expressed in RON thousand ( RON 000 ) Year ended 2017 RON 000 Year ended 2016* RON 000 Net profit for the period 214, ,378 Other comprehensive income: Items that may be reclassified to profit or loss Fair value reserve (available-for-sale financial assets): Net change in fair value 4,402 (6,812) Net amount transferred to profit or loss (6,096) (602) Income tax 271 1,186 Other comprehensive income, net of tax (1,423) (6,228) Total comprehensive income 213, ,150 *See note 2f) The financial statements were authorized for issue by the Board of Directors on 18 April 2018 and were signed on its behalf by: Sergiu Oprescu Executive President Gabriel Mateescu Executive Financial Vice-president The accompanying notes form an integral part of these financial statements. 8

11 STATEMENT OF FINANCIAL POSITION Note 2017 RON * RON 000 ASSETS Cash and balances with National Bank of Romania 13 2,044,314 2,445,616 Derivative financial assets 18 1,566 3,106 Due from other banks , ,495 Available-for-sale securities 15 1,323,342 1,252,556 Investments in associates Loans and advances to customers 16 10,938,335 10,335,770 Property and equipment 17 91,803 96,552 Intangible assets 17 17,800 7,336 Other assets 19 36,992 41,814 Assets held for sale ,291 11,033 TOTAL ASSETS 15,635,918 14,732,244 LIABILITIES AND EQUITY Due to banks 20 3,369,298 4,472,042 Derivative financial liabilities 18 1,714 4,248 Due to customers 21 9,440,296 7,918,486 Other borrowed funds ,791 6,076 Subordinated debt , ,540 Provisions 24 13,627 18,638 Deferred tax liabilities 26 1, Other liabilities 25 88,658 55,597 Total liabilities 13,871,708 13,181,335 Share capital , ,145 Reserve on available for sale financial assets (2,356) (933) Other reserves 154, ,736 Retained earnings 628, ,961 Total equity 1,764,210 1,550,909 TOTAL LIABILITIES AND EQUITY 15,635,918 14,732,244 *See note 2f) The financial statements were authorized for issue by the Board of Directors on 18 April 2018 and were signed on its behalf by: Sergiu Oprescu Executive President Gabriel Mateescu Executive Financial Vice-president The accompanying notes form an integral part of these financial statements. 9

12 STATEMENT OF CHANGES IN EQUITY Share Capital Reserves on available for sale financial assets Other reserves Retained Earnings Total Balance as at 01 January ,145 5, , ,677 1,442,759 Changes for the period * Net profit for the period , ,378 Other comprehensive income, net of income tax Net change in available-for-sale financial assets, net of tax - (6,228) - - (6,228) Appropriation of legal reserves - - 6,094 (6,094) - Total other comprehensive income - (6,228) 6,094 (6,094) (6,228) Total comprehensive income for the period - (6,228) 6, , ,150 Balance as at ,145 (933) 141, ,961 1,550,909 Balance as at 01 January ,145 (933) 141, ,961 1,550,909 Changes for the period Net profit for the period , ,734 Other comprehensive income, net of income tax Net change in available-for-sale financial assets, net of tax - (1,423) - - (1,423) Appropriation of legal reserves ,828 (12,828) - Total other comprehensive income - (1,423) 12,828 (12,828) (1,423) Total comprehensive income for the period - (1,423) 12, , ,311 Other (10) (10) Balance as at ,145 (2,356) 154, ,857 1,764,210 *See note 2f) As at 2017 statutory non-distributable reserves set-up in accordance with Romanian law amount to RON 154,564 thousand ( 2016: RON 141,736 thousand). The financial statements were authorized for issue by the Board of Directors on 18 April 2018 and were signed on its behalf by: Sergiu Oprescu Executive President Gabriel Mateescu Executive Financial Vice-president The accompanying notes form an integral part of these financial statements. 10

13 STATEMENT OF CASH FLOWS Note Year ended 2017 Year ended 2016* Cash flow from operating activities Profit before taxation 256, ,672 Adjustments: Net impairment loss/gain on financial assets 10 (32,116) 91,504 Dividend and similar income (886) (3,035) Depreciation and amortization 17 17,090 15,773 Fixed assets written-off and impairment ,964 (Gain) from transactions of equity investments 15 - (5,327) (Gain) from sales of tangible assets - (127) (Gain) from sales of assets recovered from customers (172) (23) Share of loss in associates Other adjustments 49,014 6,110 Operating profit before changes in operating assets and liabilities 290, ,727 Changes in operating assets: Decrease/(increase) in amounts due from other banks (237,393) 1,078 Decrease/(increase) in loans and advances to customers** (858,293) (22,546) Decrease/(increase) in other assets 6,689 (1,664) Total changes in operating assets (1,088,997) (23,132) Changes in operating liabilities (Decrease)/increase in amounts due to banks (1,102,708) (2,026,500) (Decrease)/increase in amounts due to customers 1,518,159 1,621,318 (Decrease)/increase in other liabilities (12,715) 13,782 Total changes in operating liabilities 402,736 (391,400) Net cash from operations (395,820) (185,805) Income tax paid - (8,565) Net cash flows from operating activities (395,820) (194,370) Cash flow from investing activities Purchase of property and equipment and intangibles 17 (23,757) (11,393) Proceeds from sale of property and equipment Proceeds from sale/maturities of AFS securities 1,887,302 2,011,635 Purchase of AFS securities (1,959,296) (2,012,686) Proceeds from sale of equity investments - 52,707 Purchase of equity investments - (1,125) Dividends received 886 3,035 Net cash flows from investing activities (94,865) 42,300 The accompanying notes form an integral part of these financial statements. 11

14 STATEMENT OF CASH FLOWS Note Year ended 2017 Year ended 2016* Cash flow from financing activities Finance lease repayments (150) (151) Other borrowed funds ,378 (1,353) Subordinated loan Net cash flows from financing activities 228,228 (1,489) Net increase / (decrease) in cash and cash equivalents (262,457) (153,559) Cash and cash equivalents at 1 January 32 2,966,971 3,120,530 Cash and cash equivalents at 32 2,704,514 2,966,971 Interest received 523, ,579 Interest paid 85,718 87,486 *See note 2f) ** Including the loan portfolio reclassified as Assets Held for Sale (see note 4.b.iii) The financial statements were authorized for issue by the Board of Directors on 18 April 2018 and were signed on its behalf by: Sergiu Oprescu Executive President Gabriel Mateescu Executive Financial Vice-president The accompanying notes form an integral part of these financial statements. 12

15 1. REPORTING ENTITY Alpha Bank Romania SA (the "Bank") was incorporated in Romania in 1994 and is licensed by the National Bank of Romania to conduct banking activities. The Bank is principally engaged in wholesale and retail banking operations in Romania. Currently, the Bank operates through its head office located in Bucharest and 130 branches ( 2016: 130). As of 2017, 36 were located in Bucharest ( 2016: 36) and 94 in other cities in Romania (31 December 2016: 94). The registered office of the Bank is: Alpha Bank Romania SA Calea Dorobantilor no. 237B, District 1 Bucharest Romania As of 2017, the members of Board of Directors were as follows: Mr. Christos Giampanas, Chairman Mr. Sergiu Bogdan Oprescu, Member and Executive President Mr. Evangelos Kalamakis, Member Mr. Nikolaos Zagorisios, Member Mr. Lazaros Papagaryfallou, Member Mr. Georgios Michalopoulos, Member Mr. Stelios Louisides, Member Mrs. Irene Rouvitha Panou, Independent Member Mr. Radu Gheorghe Deac, Independent Member The Bank serves a broad client base that includes corporations and individuals and offers banking services to local and international entities which include but are not limited to wholesale and retail banking operation, issuing of cards under the VISA and MasterCard network, mortgage and consumer loans, money transfers, trade finance. The number of employees as at 2017 was 1,973 ( 2016: 1,895). Alpha Bank AE, the parent company of the Bank, based in Greece, 40 Stadiou Street Athens, prepares a set of consolidated financial statements in accordance with International Financial Reporting Standards as endorsed by the European Union for the year ended 31 December 2017, available on the following web site: As at 2017 and 2016, the Bank had no subsidiaries. 13

16 2. BASIS OF PRESENTATION a) Statement of compliance These financial statements relate to the financial year ended 2017 and they have been prepared in accordance with International Financial Reporting Standards (IFRS) as endorsed by the European Union and sanctioned by the Order no. 27/2010 issued by National Bank of Romania. The accounts of the Bank are maintained in RON. b) Basis of measurement The financial statements of the Bank have been prepared on the historical cost basis except for the available for sale debt instruments and derivative financial instruments which were measured at fair value. Available for sale equity instruments are measured at cost where fair value cannot be reliably measured. The Bank applied the going concern principle for the preparation of the financial statements as at c) Functional and presentation currency The Bank s management considers that the functional currency, as defined by IAS 21 The Effects of Changes in Foreign Exchange Rates is RON. The financial statements are presented in Romanian Lei ( RON ), rounded to the nearest thousand, unless otherwise indicated. d) Use of estimates and judgments The preparation of financial statements in conformity with IFRS requires management to make judgments, estimates and assumptions that affect the application of policies and reported amounts of assets and liabilities, income and expenses. Actual results may differ from these estimates. Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimates are revised. In particular, information about significant areas of estimation uncertainty and critical judgments in applying accounting policies that have the most significant effect on the amount recognized in the financial statements are described in Notes 4 and 6. e) Changes in accounting policies All changes in accounting policies represent the effect of changes in relevant International Financial Reporting Standards as endorsed by the European Union. f) Consolidated entities: Associates In 2016 the Bank increased its participation in Alpha Finance Romania S.A up to the level of 26.68% share from capital, as can be seen in note 15. Giving the exemption criteria prescribed in IAS 28 Investments in Associates and Joint Ventures and the provisions of IAS 27 Separate financial statements, the Bank prepared separate financial statements for year ending 2016, in which investments in associates were carried at cost. 14

17 2. BASIS OF PRESENTATION (CONTINUED) As of 2017, the Bank accounted the investment using the equity method. The Bank decided to begin applying the equity method since it has the intention to issue publicly traded instruments and, following that issuance, the IAS 28 exemption no longer apply. Under the equity method the investment is initially recognised at cost and adjusted thereafter for the post acquisition change in the Bank s share of net assets of the associate. In case the losses according to the equity method exceed the investment in ordinary shares, they are recognized as a reduction of other elements that are essentially an extension of the investment in the associate. The Bank s share of the associate s profit or loss and other comprehensive income is separately recognized in the income statement and in the statement of comprehensive income, accordingly. In respect of comparative information for the period ended 2016, the following items from statement of financial position and income statement as of 2016 have been reclassified and adjusted: Amount previously reported - Separate Financial Statements Year ended Restated amount Financial Statements Year ended 31-Dec-16 Reclassification Adjustment 31-Dec-16 Available-for-sale securities 1,253,738 (1,182) - 1,252,556 Investments in associates - 1,182 (216) 966 Deferred tax liabilities (35) 708 Retained earnings 427,142 - (181) 426,961 Share from loss of associates - - (216) (216) Income tax expense (7,329) - 35 (7,294) 3. SIGNIFICANT ACCOUNTING POLICIES The accounting policies set out below have been applied consistently to all periods presented in these financial statements, and have been applied consistently by the Bank. a) Transactions in foreign currency Transactions in foreign currencies are translated into the functional currency of the Bank at exchange rates at the dates of the transaction. Monetary assets and liabilities denominated in foreign currencies at the balance sheet date are retranslated into the functional currency at the exchange rate at that date. Foreign exchange differences arising on translation are recognized in the income statement, except when deferred in equity as qualifying cash flow hedges and qualifying net investments hedges. Non-monetary assets and liabilities that are measured in terms of historical cost in a foreign currency are translated using the exchange rate at the date of the transaction. Non-monetary assets and liabilities denominated in foreign currencies that are measured at fair value are translated to the functional currency at exchange rates at the dates the fair value was determined. Foreign currency differences arising on retranslation are recognized in profit or loss, except for differences arising on the retranslation of non-monetary available-for-sale financial assets which are included in the fair value reserve in equity. 15

18 3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) The exchange rates of major foreign currencies were: Currencies % Increase/(Decrease) Euro (EUR) 1: RON : RON % US Dollar (USD) 1: RON : RON % b) Segment reporting An operating segment is a component of the Bank that engages in business activities from which it may earn revenues and incur expenses, including revenues and expenses that relate to transactions with any of the Bank s other components. Operating segments are determined and measured based on the information provided to the Executive Committee of the Bank, which is the body responsible for the allocation of resources between the Bank s operating segments and the assessment of their performance. Based on the above, as well as the Bank s administrative structure and activities, the following operating segments have been determined: Retail Banking Wholesale Banking Treasury Other It is noted that the methods used to measure operating segments for the purpose of reporting to the Executive Committee are not different from those required by the International Financial Reporting Standards. c) Interest income and expense Interest income and expense are recognized in the income statement for all interest bearing instruments on an accrual basis using the effective interest method. The effective interest method is a method of calculating the amortized cost of a financial asset or a financial liability and of allocating the interest income or interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments or receipts through the expected life of the financial instrument or, when appropriate, a shorter period to the net carrying amount of the financial asset or financial liability. When calculating the effective interest rate, the Bank estimates cash flows considering all contractual terms of the financial instrument but does not consider future credit losses. The calculation includes all fees and points paid or received between parties to the contract that are an integral part of the effective interest rate, transaction costs, and all other premiums or discounts. Interest income on impaired loans is recognized based on the carrying value of the loan net of impairment, at the original effective interest rate. Loan origination fees, such as evaluating the borrowers financial condition, collateral and other security arrangements, and related direct incremental expenses are deferred and subsequently recognized in income as an adjustment to the effective yield. 16

19 3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) d) Fees and commission Fees and commissions income and expenses that are integral to the effective interest rate as a financial asset or liability are included in the measurement of the effective interest rate. Other fee and commission income arising on the financial services provided by the Bank including cash management services, brokerage services, investment advice, financial planning, are recognized in the separate income statement as the related service is provided. Other fees and commission expenses relate mainly to transaction and service fees, which are expensed as the services are received. e) Gain less losses on financial transactions Net income from other financial instruments comprises gains and losses related to financial assets and liabilities and it includes all realized and unrealized fair value changes, gain and losses from the sale of loans, disposal of securities and foreign exchange differences. Differences that may arise between the carrying amount of financial liabilities settled or transferred and the consideration paid are also recognised in gains less losses on financial transactions. f) Dividends Dividend income is recognized in the income statement when the right to receive income is established. g) Lease payments The Bank as a lessee Assets held by the Bank under leases that transfer to the Bank substantially all of the risks and rewards of ownership are classified as finance leases. The leased asset is recognised as property, plant and equipment and the related liability is recognised in Other Liabilities. The leased asset and the liability are initially measured at an amount equal to the lower of its fair value and the present value of the minimum lease payments. Subsequent to initial recognition, the leased assets are depreciated over their useful lives unless the duration of the lease is less than the useful life of the leased asset and the Bank is not expected to obtain ownership at the end of the lease, in which case the asset is depreciated over the term of the lease. The lease payments are apportioned between the finance charge and the reduction of the outstanding liability. Assets held under other leases are classified as operating leases and are not recognized in the Bank s statement of financial position. Payments made under operating leases are recognized in profit or loss on a straight-line basis over the term of the lease. Lease incentives received are recognized as an integral part of the total lease expense, over the term of the lease. Minimum lease payments made under finance leases are apportioned between the interest expense and the reduction of the outstanding liability. The interest expense is allocated to each period during the lease term so as to produce a constant periodic rate of interest on the remaining balance of the liability. Contingent lease payments are accounted for by revising the minimum lease payments over the remaining term of the lease when the lease adjustment is confirmed. 17

20 3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) g) Lease payments (continued) The Bank as a lessor The bank acts as a lessor only for assets under operating leases. The leased asset is recognized and depreciation is charged over its estimated useful life. Income arising from the leased asset is recognized as other income on an accrual basis. h) Income tax expense Income tax for the period comprises current and deferred tax. Income tax is recognized in the income statement except to the extent that it relates to items recognized directly to equity, in which case it is recognized in equity. Current tax is the expected tax payable or receivable on the taxable income for the year, using tax rates enacted or substantially enacted at the balance sheet date, and any adjustment to tax payable in respect of prior periods. Deferred tax is recognized using the balance sheet method, providing for all temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes. Temporary deductible differences are the difference between the carrying amount of an asset or liability in the balance sheet and its tax base, which will results in amounts that are deductible in the determination of taxable profit for future periods in which the carrying amount of the asset or liability is recovered or settled. The existence of a deductible temporary difference depends only on a comparison of the carrying amount of an asset and its tax base at the end of the reporting period and is not affected by any future changes in the carrying amount. The amount of deferred tax recognized is based on the expected manner of realization or settlement of the carrying amount of assets and liabilities, using tax rates enacted or substantially enacted at the balance sheet date. A deferred tax asset is recognized only to the extent that it is probable that future taxable profits will be available against which the unused tax losses and credits can be utilized. Deferred tax assets are reduced to the extent that it is no longer probable that the related tax benefit will be realized. Additional income taxes that arise from the distribution of dividends are recognized at the same time as the liability to pay the related dividend. The tax rate used to calculate the current and deferred tax position at 2017 is 16% (2016: 16%). 18

21 3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) i) Financial assets and liabilities i) Recognition The Bank initially recognizes loans and advances, deposits, debt securities issued and subordinated liabilities on the date that they are originated. All other financial assets and liabilities (including assets and liabilities designated at fair value through profit or loss) are initially recognized on the trade date at which the Bank becomes a party to the contractual provisions of the instrument. A financial asset or financial liability is measured initially at fair value plus, for an item not at fair value through profit or loss, transaction costs that are directly attributable to its acquisition or issue. ii) Classification, initial recognition and subsequent measurement The Bank classifies its financial assets in the following categories: A. Financial assets at fair value through profit or loss. This category has two sub-categories: financial assets held for trading and those designated at fair value through profit or loss at inception. A financial instrument is classified in this category if acquired principally for the purpose of short term profit-taking or if so designated by management. Financial assets at fair value through profit or loss include derivatives held by the Bank for risk management and trading assets. Derivatives held for risk management Derivative financial instruments held for risk management include currency swaps and interest rate swaps. The Bank uses derivative financial instruments to hedge risks associated with exchange rate fluctuations. These derivatives are recognized in the balance sheet at fair value. Derivatives are carried as assets when their fair value is positive. Any gains or losses arising from changes in fair values are recognized in the income statement. Trading assets Trading assets are those assets that the Bank acquires or incurs principally for the purpose of selling or repurchasing in the near term, or holds as part of a portfolio that is managed together for short-term profit or position taking. Trading assets are initially recognized and subsequently measured at fair value in the balance sheet with transaction costs taken directly to profit or loss. All changes in fair value are recognized as part of net trading income in profit or loss. Reclassification out of the held-for-trading category to the loans and receivables category, held-to-maturity investments category or available-for-sale category is permitted only when there are rare circumstances and the financial assets are no longer held for sale in the foreseeable future. In addition, reclassification out of the held-for-trading category to either loans and receivables or available-for-sale is permitted, even when there are no rare circumstances, only if the financial assets meet the definition of loans and receivables and there is the intention to hold them for the foreseeable future or until maturity. On reclassification of a financial asset out of the fair value through profit or loss category, all embedded derivative will be (re)assessed and, if necessary, separately accounted for in financial statements. 19

22 3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) i) Financial assets and liabilities (continued) ii) Classification, initial recognition and subsequent measurement (continued) B. Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market, other than those that the Bank intends to sell immediately or in the near term, those that the Bank, upon initial recognition, designates as at fair value through profit and loss, those that the Bank, upon initial recognition, designates as available for sale or those for which the holder may not recover substantially all of its initial investment, other than because of credit deterioration. Loans and receivables comprise loans and advances to banks and customers. Loans and advances are initially measured at fair value plus incremental direct transaction costs, and subsequently measured at their amortized cost using the effective interest method. C. Held-to-maturity investments are non-derivative financial assets with fixed or determinable payments and fixed maturities that the Bank s management has the positive intention and ability to hold to maturity, and which are not designated as at fair value through profit or loss or as available-for-sale and the asset shall not meet the definition of a loan and receivable. Held-to-maturity investments are carried at amortized cost using the effective interest method. Any sale or reclassification of a significant amount of held-to-maturity investments not close to their maturity would result in the reclassification of all held-to-maturity investments as available-for-sale, and prevent the Bank from classifying investment securities as held-to-maturity for the current and the following two financial years. However, sales and reclassifications in any of the following circumstances would not trigger a reclassification: sales or reclassifications that are so close to maturity that changes in the market rate of interest would not have a significant effect on the financial asset s fair value sales or reclassifications after the Bank has collected substantially all of the asset s original principal sales or reclassifications attributable to non-recurring isolated events beyond the Bank s control that could not have been reasonably anticipated. D. Available-for-sale financial assets are those financial assets that are designated as available for sale or are not classified as loans and advances, held-to-maturity investments or financial assets at fair value through profit or loss. Available-for-sale instruments include treasury bonds and other bonds eligible for discounting with central banks, corporate bonds investments in unit funds and other investment securities that are not at fair value through profit and loss or held-to-maturity. Debt securities such as bonds and treasury bills issued by the Ministry of Public Finance of Romania and corporate bonds are classified as available-for-sale assets and measured at fair value using bid market quotations from active markets. Securities such as investments in mutual funds are classified as available-for-sale assets and are carried at their market prices. Equity investments are classified as available-for-sale assets and are carried at the fair value. Where no reliable estimate of fair value is available, equity investments are stated at cost less impairment. 20

23 3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) i) Financial assets and liabilities (continued) ii) Classification, initial recognition and subsequent measurement (continued) Interest income is recognized in profit or loss using the effective interest method. Dividend income is recognized in profit or loss when the Bank becomes entitled to the dividend. Foreign exchange gains or losses on available-for-sale debt security investments are recognized in profit or loss. Other fair value changes are recognized directly in other comprehensive income until the investment is sold or impaired and the cumulative gains and losses previously recognized in other comprehensive income are reclassified to profit or loss as a reclassification adjustment. The Bank classifies its financial liabilities in the following categories: A. Financial liabilities at fair value through profit or loss. This category has two subcategories: financial liabilities designated by the entity as a liability at fair value through profit or loss upon initial recognition and financial liabilities held for trading. A financial instrument is classified in this category if acquired principally for the purpose of short term profit-taking or if so designated by management. Financial assets or liabilities (other than those held for trading) may be classified upon initial recognition at fair value through profit or loss, if they either: eliminate or significantly reduce a measurement or recognition inconsistency ( accounting mismatch ) that would otherwise arise from measuring assets and liabilities or recognizing the gains or losses on them on different bases; the assets or liabilities are managed, evaluated and reported internally on a fair value basis; or the asset or liability contains an embedded derivative that significantly modifies the cash flows that could otherwise be required under the contract. Derivatives held for risk management Derivative financial instruments held for risk management include currency swaps and interest rate swaps. The Bank uses derivative financial instruments to mitigate risks associated with exchange rate fluctuations and interest rate fluctuations. These derivatives are recognized in the balance sheet at fair value. Trading liabilities Trading liabilities are those liabilities that the Bank acquires or incurs principally for the purpose of selling or repurchasing in the near term, or holds as part of a portfolio that is managed together for short-term profit or position taking. Trading liabilities are initially recognized and subsequently measured at fair value in the balance sheet with transaction costs taken directly to profit or loss. All changes in fair value are recognized as part of net trading income in profit or loss. 21

24 3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) B. Other financial liabilities are measured at amortized cost using the effective interest rate method. All financial instruments that don t qualify to be classified as financial liabilities at fair value through profit or loss are classified in this category. Deposits from customers and from banks, loans from banks and other financial institutions, subordinated liabilities. Deposits from customers and from banks, loans from banks and subordinated liabilities are initially measured at fair value plus incremental direct transaction costs, and subsequently measured at amortized cost using the effective interest method. When the Bank sells a financial asset and simultaneously enters into an agreement to repurchase the asset (or a similar asset) at a fixed price on a future date ( repo ), the arrangement is accounted for as Due to banks, and the underlying asset continues to be recognized in the Bank s financial statements. Financial guarantees Financial guarantees are contracts that require the Bank to make specified payments to reimburse the holder for a loss it incurs because a specified debtor fails to make payment when due in accordance with the terms of a debt instrument. Financial guarantee liabilities are initially recognized at their fair value, and the initial fair value is amortized over the life of the financial guarantee. The guarantee liability is subsequently carried at the higher of this amortized amount and the present value of any expected payment (when a payment under the guarantee has become probable). Financial guarantees are included within other liabilities. iii) Derecognition The Bank derecognizes a financial asset when the contractual rights to the cash flows from the asset expire, or it transfers the rights to receive the contractual cash flows on the financial asset in a transaction in which substantially all the risks and rewards of ownership of the financial asset are transferred. Any interest in transferred financial assets that is created or retained by the Bank is recognized as a asset or liability. On derecognition of a financial asset, the difference between the carrying amount of the asset (or the carrying amount allocated to the portion of the asset transferred), and the sum of (i) the consideration received (including any new asset obtained less any new liability assumed) and (ii) any cumulative gain or loss that had been recognized in other comprehensive income is recognized in profit or loss. The Bank derecognizes a financial liability when the obligation specified in the contract is either discharged or cancelled or expires. Where there is an exchange between an existing borrower and lender of debt instruments with substantially different terms, or there is a substantial modification of the terms of an existing financial liability, this transaction is accounted for as derecognition of the original financial liability and recognition of a new financial liability. Any gain or loss from extinguishment of the original financial liability is recognized in profit or loss. The terms are considered substantially different if the discounted present value of the cash flows under the new terms (including any fees paid net of any fees received), discounted using the original effective interest rate, is at least 10% different from the present value of the remaining cash flows of the original financial liability. When the Bank enters into transactions whereby it transfers assets recognized on its balance sheet, but retains either all risks or rewards of the transferred assets or a portion of them, if all or substantially all risks and rewards are retained, then the transferred assets are not derecognized from the balance sheet. Transfers of assets with retention of all or substantially all risks and rewards include, for example, securities lending and repurchase transactions. 22

25 3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) i) Financial assets and liabilities (continued) iii) Derecognition (continued) When assets are sold to a third party with a concurrent total rate of return swap on the transferred assets, the transaction is accounted for as a secured financing transaction similar to repurchase transactions. In transactions where the Bank neither retains nor transfers substantially all the risks and rewards of ownership of a financial asset, it derecognizes the asset if control over the asset is lost. The rights and obligations retained in the transfer are recognized separately as assets and liabilities as appropriate. In transfers where control over the asset is retained, the Bank continues to recognize the asset to the extent of its continuing involvement, determined by the extent to which it is exposed to changes in the value of the transferred asset. iv) Offsetting Financial assets and liabilities are offset and the net amount reported in the statement of financial position when and only when there is a legally enforceable right to set off the recognized amounts and there is an intention to settle on a net basis, or realize the asset and settle the liability simultaneously. Income and expenses are presented on a net basis only when permitted by the accounting standards, or for gains and losses arising from a bank of similar transactions such as in the Bank s trading activity. v) Amortized cost measurement The amortized cost of a financial asset or liability is the amount at which the financial asset or liability is measured at initial recognition, minus principal repayments, plus or minus the cumulative amortization using the effective interest method of any difference between the initial amount recognized and the maturity amount, minus any reduction for impairment. j) Cash and cash equivalents For the purposes of the cash flow statement, cash and cash equivalents comprise balances with less than 90 days maturity including: cash, current accounts with banks, short term due from banks and Reverse Repo agreements. Short-term balances due from banks are amounts that mature within three months. Cash is carried at nominal value and cash equivalents are carried at amortized cost in the statement of financial position. k) Fair value measurement Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date in the principal or, in its absence, the most advantageous market to which the Bank has access at the date. The fair value of a liability reflects its nonperformance risk. When available, the Bank measures the fair value of an instrument using the quoted price in an active market for that instrument. A market is regarded as active if transactions for the asset or liability take place with sufficient frequency and volume to provide pricing information on an ongoing basis. 23

26 3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) k) Fair value measurement (continued) The fair value of financial instruments that are not traded in an active market is determined by the use of valuation techniques, appropriate in the circumstances, and for which sufficient data to measure fair value are available, maximizing the use of relevant observable inputs and minimizing the use of unobservable inputs. If observable inputs are not available, other model inputs are used which are based on estimations and assumptions such as the determination of expected future cash flows, discount rates, probability of counterparty default and prepayments. In all cases, the Bank uses the assumptions that market participants would use when pricing the asset or liability, assuming that market participants act in their economic best interest. Assets and liabilities which are measured at fair value or for which fair value is disclosed, are categorized according to the inputs used to measure their fair value as follows: Level 1 inputs: quoted market prices (unadjusted) in active markets, Level 2 inputs: directly or indirectly observable inputs, Level 3 inputs: unobservable inputs used by the Bank, to the extent that relevant observable inputs are not available. The best evidence of a fair value of a financial instrument at initial recognition is normally the transaction price the fair value of a consideration given or received. If the Bank determines that the fair value at initial recognition differs from the transaction price and the fair value is evidenced neither by a quoted price in an active market for an identical asset or liability nor based on a valuation technique that uses only data from observable markets, then the financial instrument is initially measured at the fair value, adjusted to defer the difference between the fair value at initial recognition and the transaction price. Subsequently, that difference is recognized in profit or loss on an appropriate basis over the life of an instrument but not later than when the valuation is wholly supported by observable market data or the transaction is closed out. The principal inputs to the valuation techniques used by the Bank are: Bond prices - quoted prices available for government bonds and certain corporate securities. Credit spreads - these are derived from active market prices, prices of credit default swaps or other credit based instruments, such as debt. Values between and beyond available data points are obtained by interpolation and extrapolation. Interest rates - these are principally benchmark interest rates such as the LIBOR (London Interbank Offered Rate), OIS (Overnight Index Swaps) and other quoted interest rates in the swap, bond and futures markets. Values between and beyond available data points are obtained by interpolation and extrapolation. Foreign currency exchange rates - observable markets both for spot and forward contracts and futures. Equity and equity index prices - quoted prices are generally readily available for equity shares listed on stock exchanges and for major indices on such shares. 24

27 3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) k) Fair value measurement (continued) Price volatilities and correlations - Volatility and correlation values are obtained from pricing services or derived from option prices. Unlisted equities - financial information specific to the company or industry sector comparables. Loans and Deposits - market data and Bank/customer specific parameters. The Bank recognizes transfers between levels of the fair value hierarchy as of the end of the reporting period during which the change has occurred. Where the Bank has positions with offsetting risks, mid-market prices are used to measure the offsetting risk positions and a bid or asking price adjustment is applied only to the net open position as appropriate. Fair values reflect the credit risk of the instrument and include adjustments to take account of the credit risk of the Bank entity and the counterparty where appropriate. Fair value estimates obtained from models are adjusted for any other factors, such as liquidity risk or model uncertainties to the extent that the Bank believes a third-party market participant would take them into account in pricing a transaction. The most important category of non-financial assets for which fair value is estimated is real estate property. The process, mainly, followed for the determination of the fair value is summarized below: Assignment to the engineer - valuer Case study- Setting of additional data Autopsy - Inspection Data processing - Calculations Preparation of the valuation report To derive the fair value of the real estate property, the valuer chooses among the three following valuation techniques: Market approach (or sales comparison approach), which measures the fair value by comparing the property to other identical ones for which information on transactions is available. Income approach, which capitalizes future cash flows arising from the property using an appropriate discount rate. Cost approach, which reflects the amount that would be required currently to replace the asset with another asset with similar specifications, after taking into account the required adjustment for impairment. 25

28 3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) k) Fair value measurement (continued) Examples of inputs used to determine the fair value of properties and which are analysed to the individual valuations, are the following: Commercial property: price per square meter, rent growth per annum, long-term vacancy rate, discount rate, expense rate of return, lease term, rate of non-leased properties/units for rent. Residential property: Net return, reversionary yield, net rental per square meter, rate of continually non leased properties/units, expected rent value per square meter, discount rate, expense rate of return, lease term etc. General assumptions such as the age of the building, residual useful life, square meter per building etc. are also included in the analysis of the individual valuation assessments. It is noted that the fair value measurement of a property takes into account a market s participant ability to generate economic benefits by using the asset in its highest and best use or by selling it to another market participant that would use the asset in its highest and best use. l) Property and equipment (i) Recognition and measurement Items of property and equipment are measured at their cost less accumulated depreciation value and impairment losses. Capital expenditure on property and equipment in the course of construction is capitalized and depreciated once the assets enter into use. Cost includes expenditures that are directly attributable to the acquisition of the asset. (ii) Subsequent costs The Bank recognizes in the carrying amount of an item of property, plant and equipment the cost of replacing part of such an item when that cost is incurred, if it is probable that the future economic benefits embodied with the item will flow to the Bank and the cost of the item can be measured reliably. All other costs are recognized in the income statement as an expense as incurred. Expenditure incurred to replace a component of an item of property and equipment that is accounted for separately, including major inspection and overhaul expenditure, is capitalized. Other subsequent expenditure is capitalized only when it increases the future economic benefits embodied in the item of property and equipment. All other expenditure is recognized in the income statement as an expense as incurred. (iii) Depreciation Depreciation is charged to the income statement on a straight-line basis over the estimated useful lives of each part of an item of property, plant and equipment. The estimated useful lives for the current and comparative periods are as follows: Buildings Equipment Motor vehicles Other tangible fixed assets 33 years 3 18 years 5-9 years 3 24 years 26

29 3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) l) Property and equipment (continued) Land is not depreciated but it is tested for impairment. Depreciation methods, useful lives and residual values are reassessed periodically and adjusted if appropriate. m) Intangible assets Intangible assets consist of purchased and in-house developed software. Costs associated with developing or maintaining software programs are recognized as an expense when incurred. Costs that are directly associated with the production of identifiable and unique software products controlled by the Bank, and that will probably generate economic benefits exceeding costs beyond one year, are recognized as intangible assets. Subsequent expenditure on software assets is capitalized only when it increases the future economic benefits embodied in the specific asset to which it relates. All other expenditure is expensed as incurred. Amortization is recognized in profit or loss on a straight-line basis over the estimated useful life of the software, from the date that it is available for use. The estimated useful life of the software is three to five years. n) Assets held for sale Non-current assets or disposal groups that are expected to be recovered principally through a sale transaction, along with the related liabilities, are classified as held-for-sale. The above classification is used if the asset is available for immediate sale in its present condition and its sale is highly probable. Assets held for sale are initially recognized and subsequently remeasured at the lower of their carrying amount and fair value less cost to sell. Any loss arising from the above measurement is recorded in profit or loss and can be reversed in the future. Assets in this category are not depreciated. Gains or losses from the sale of these assets are recognized in the income statement. Non - current assets that are acquired through enforcement procedures but are not available for immediate sale or are not expected to be sold within a year are included in Other Assets and are measured at the lower of cost (or carrying amount) and fair value. Non-current assets held for sale, that the Bank subsequently decides either to use or to lease, are reclassified to the categories of property, plant and equipment or investment property respectively. During their reclassification, they are measured at the lower of their recoverable amount and their carrying amount before they were classified as held for sale, adjusted for any depreciation, amortization or revaluation that would have been recognized had the assets not been classified as held for sale. o) Identification and measurement of impairment i) Impairment losses for financial assets At each balance sheet date the Bank assesses whether there is objective evidence that financial assets not carried at fair value through profit or loss are impaired. Financial assets are impaired when objective evidence demonstrates that a loss event has occurred after the initial recognition of the asset, and that the loss event has an impact on the future cash flows on the asset that can be estimated reliably. 27

ALPHA BANK ROMANIA S.A.

ALPHA BANK ROMANIA S.A. FINANCIAL STATEMENTS 31 December 2012 Prepared in accordance with International Financial Reporting Standards as endorsed by the European Union Financial Statements prepared in

ALPHA BANK ROMANIA S.A. FINANCIAL STATEMENTS 31 December 2012 Prepared in accordance with International Financial Reporting Standards as endorsed by the European Union Financial Statements prepared in

Ameriabank cjsc. Financial Statements For the second quarter of 2016

Financial Statements For the second quarter of Contents Statement of profit or loss and other comprehensive income... 3 Statement of financial position... 4 Statement of cash flows... 5 Statement of changes

Financial Statements For the second quarter of Contents Statement of profit or loss and other comprehensive income... 3 Statement of financial position... 4 Statement of cash flows... 5 Statement of changes

Ardshinbank CJSC. Interim Financial Statements for the period ended 30 September 2016

Interim Financial Statements for the period ended 30 September 2016 Contents Interim statement of profit or loss and other comprehensive income... 3 Interim statement of financial position... 4 Interim

Interim Financial Statements for the period ended 30 September 2016 Contents Interim statement of profit or loss and other comprehensive income... 3 Interim statement of financial position... 4 Interim

Consolidated Financial Statements 31 December 2010

Banca Transilvania s.a. Consolidated Financial Statements 31 December 2010 Prepared in accordance with the International Financial Reporting Standards as endorsed by the European Union TRANSLATOR S EXPLANATORY

Banca Transilvania s.a. Consolidated Financial Statements 31 December 2010 Prepared in accordance with the International Financial Reporting Standards as endorsed by the European Union TRANSLATOR S EXPLANATORY

ZAO Bank Credit Suisse (Moscow) Financial Statements for the year ended 31 December 2010

Financial Statements for the year ended 31 December 2010") Financial Statements for the year ended 31 December 2010 Contents Independent Auditors Report... 3 Statement of Comprehensive Income... 4 Statement of Financial Position... 5 Statement of Cash Flows...

Financial Statements for the year ended 31 December 2010 Contents Independent Auditors Report... 3 Statement of Comprehensive Income... 4 Statement of Financial Position... 5 Statement of Cash Flows...

Renesa cjsc. Financial Statements for the year ended 31 December 2013

Financial Statements for the year ended 31 December 2013 Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive income... 5 Statement of financial position... 6 Statement

Financial Statements for the year ended 31 December 2013 Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive income... 5 Statement of financial position... 6 Statement

Artsakhbank cjsc. Financial Statements for the year ended 31 December 2013

Financial Statements for the year ended 31 December Artslllcllbllllk cjsc Stateml!nt ofprofit or Loss Clnd Other Comprehensive income for the year ended 31 December 20 13 Notes AMD'OOO AMD'OOO Interest

Financial Statements for the year ended 31 December Artslllcllbllllk cjsc Stateml!nt ofprofit or Loss Clnd Other Comprehensive income for the year ended 31 December 20 13 Notes AMD'OOO AMD'OOO Interest

BANCA TRANSILVANIA S.A. Consolidated Financial Statements 31 December 2009

BANCA TRANSILVANIA S.A. Consolidated Financial Statements 31 December 2009 Prepared in accordance with the International Financial Reporting Standards as endorsed by the European Union TRANSLATOR S EXPLANATORY

BANCA TRANSILVANIA S.A. Consolidated Financial Statements 31 December 2009 Prepared in accordance with the International Financial Reporting Standards as endorsed by the European Union TRANSLATOR S EXPLANATORY

Closed Joint Stock Company ISBANK. Financial Statements for the year ended 31 December 2013

Financial Statements for the year ended 31 December Contents Auditors Report... 3 Statement of profit or loss and other comprehensive income... 5 Statement of financial position... 6 Statement of cash

Financial Statements for the year ended 31 December Contents Auditors Report... 3 Statement of profit or loss and other comprehensive income... 5 Statement of financial position... 6 Statement of cash

Global Credit Universal Credit Organization cjsc

Global Credit Universal Credit Organization cjsc Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive income...

Global Credit Universal Credit Organization cjsc Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive income...

SMP Bank (OJSC) Consolidated Financial Statements for the year ended 31 December 2011

Consolidated Financial Statements for the year ended 31 December 2011") Consolidated Financial Statements for the year ended 31 December 2011 Contents Independent Auditors Report... 3 Consolidated statement of comprehensive income... 4 Consolidated statement of financial position...

Consolidated Financial Statements for the year ended 31 December 2011 Contents Independent Auditors Report... 3 Consolidated statement of comprehensive income... 4 Consolidated statement of financial position...

Chapter 2 Separate statement of comprehensive income 1 2. Separate statement of financial position 3 4

Chapter 1 Independent auditor s report Chapter 2 Separate statement of comprehensive income 1 2 Separate statement of financial position 3 4 Separate statement of changes in shareholders equity 5 6 Separate

Chapter 1 Independent auditor s report Chapter 2 Separate statement of comprehensive income 1 2 Separate statement of financial position 3 4 Separate statement of changes in shareholders equity 5 6 Separate

Tekstil Bankası Anonim Şirketi and Its Subsidiaries

TABLE OF CONTENTS Page ------ Independent Auditors Report Consolidated Statement of Financial Position 1 Consolidated Statement of Comprehensive Income 2-3 Consolidated Statement of Changes in Equity 4

TABLE OF CONTENTS Page ------ Independent Auditors Report Consolidated Statement of Financial Position 1 Consolidated Statement of Comprehensive Income 2-3 Consolidated Statement of Changes in Equity 4

FINANCIAL STATEMENTS 31 DECEMBER 2016

FINANCIAL STATEMENTS 31 DECEMBER 2016 Prepared in accordance with International Financial Reporting Standards as endorsed by the European Union This version of the accompanying financial statements is

FINANCIAL STATEMENTS 31 DECEMBER 2016 Prepared in accordance with International Financial Reporting Standards as endorsed by the European Union This version of the accompanying financial statements is

BANCA INTESA (CLOSED JOINT-STOCK COMPANY) Consolidated financial statements. Year ended 31 December 2013 Together with Auditors report

Consolidated financial statements. Year ended 31 December 2013 Together with Auditors report") BANCA INTESA (CLOSED JOINT-STOCK COMPANY) Consolidated financial statements Year ended 31 December 2013 Together with Auditors report BANCA INTESA (CLOSED JOINT-STOCK COMPANY) 2013 Consolidated financial

BANCA INTESA (CLOSED JOINT-STOCK COMPANY) Consolidated financial statements Year ended 31 December 2013 Together with Auditors report BANCA INTESA (CLOSED JOINT-STOCK COMPANY) 2013 Consolidated financial

Credit loss expense - - (1,232,568) Net operating income 369,680, ,052, ,599,645. Other Comprehensive Income - - -

Net operating income 369,680, ,052, ,599,645. Other Comprehensive Income - - -") STATEMENT TO THE NIGERIAN STOCK EXCHANGE AND THE SHAREHOLDERS ON THE EXTRACT OF THE UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 30 JUNE, 2017. The Board of Directors of Infinity Trust Mortgage Bank Plc

STATEMENT TO THE NIGERIAN STOCK EXCHANGE AND THE SHAREHOLDERS ON THE EXTRACT OF THE UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 30 JUNE, 2017. The Board of Directors of Infinity Trust Mortgage Bank Plc

JSC ASIAСREDIT BANK (АЗИЯКРЕДИТ БАНК) Financial Statements for the year ended 31 December 2012

Financial Statements for the year ended 31 December 2012") JSC ASIAСREDIT BANK (АЗИЯКРЕДИТ БАНК) Financial Statements for the year ended 31 December CONTENTS STATEMENT OF MANAGEMENT S RESPONSIBILITIES FOR THE PREPARATION AND APPROVAL OF THE FINANCIAL STATEMENTS

JSC ASIAСREDIT BANK (АЗИЯКРЕДИТ БАНК) Financial Statements for the year ended 31 December CONTENTS STATEMENT OF MANAGEMENT S RESPONSIBILITIES FOR THE PREPARATION AND APPROVAL OF THE FINANCIAL STATEMENTS

Ameriabank cjsc. Financial Statements for the year ended 31 December 2012

Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of comprehensive income... 4 Statement of financial position... 5 Statement of cash flows... 6 Statement

Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of comprehensive income... 4 Statement of financial position... 5 Statement of cash flows... 6 Statement

Consolidated Financial Statements of ALTERNA SAVINGS

Consolidated Financial Statements of ALTERNA SAVINGS INDEPENDENT AUDITORS' REPORT To the Members of Alterna Savings and Credit Union Limited: We have audited the accompanying consolidated financial statements

Consolidated Financial Statements of ALTERNA SAVINGS INDEPENDENT AUDITORS' REPORT To the Members of Alterna Savings and Credit Union Limited: We have audited the accompanying consolidated financial statements

MUGANBANK OPEN JOINT STOCK COMPANY

MUGANBANK OPEN JOINT STOCK COMPANY The International Financial Reporting Standards Financial Statements and Independent Auditors Report For the Year Ended 2015 TABLE OF CONTENTS Page STATEMENT OF MANAGEMENT

MUGANBANK OPEN JOINT STOCK COMPANY The International Financial Reporting Standards Financial Statements and Independent Auditors Report For the Year Ended 2015 TABLE OF CONTENTS Page STATEMENT OF MANAGEMENT

Yapi Kredi Bank Azerbaijan CJSC Consolidated financial statements

Yapi Kredi Bank Azerbaijan CJSC Consolidated financial statements Year ended 31 December 2014 together with independent auditors report 2014 Consolidated financial statements Contents Independent auditors

Yapi Kredi Bank Azerbaijan CJSC Consolidated financial statements Year ended 31 December 2014 together with independent auditors report 2014 Consolidated financial statements Contents Independent auditors

Banca Transilvania S.A.

Consolidated Financial Statements 31 December 2014 Prepared in accordance with the International Financial Reporting Standards as endorsed by the European Union Free translation Contents Independent auditors

Consolidated Financial Statements 31 December 2014 Prepared in accordance with the International Financial Reporting Standards as endorsed by the European Union Free translation Contents Independent auditors

Intesa Sanpaolo Banka d.d. Bosna i Hercegovina

Intesa Sanpaolo Banka d.d. Bosna i Hercegovina Financial Statements as at 2016 Intesa Sanpaolo Banka, d.d. Financial statements as at 2016 Contents Management Board s Report 2 Responsibilities of the Management

Intesa Sanpaolo Banka d.d. Bosna i Hercegovina Financial Statements as at 2016 Intesa Sanpaolo Banka, d.d. Financial statements as at 2016 Contents Management Board s Report 2 Responsibilities of the Management

Ameriabank CJSC Financial statements

Ameriabank CJSC Financial statements for the year ended 31 December together with independent auditor s report Ameriabank CJSC Financial statements Contents Independent auditor s report Statement of comprehensive

Ameriabank CJSC Financial statements for the year ended 31 December together with independent auditor s report Ameriabank CJSC Financial statements Contents Independent auditor s report Statement of comprehensive

National Investment Corporation of the National Bank of Kazakhstan JSC. Financial Statements for the year ended 31 December 2016

National Investment Corporation of the National Bank of Kazakhstan JSC Financial Statements for the year ended 31 December 2016 Contents Independent Auditors Report Statement of Profit or Loss and Other

National Investment Corporation of the National Bank of Kazakhstan JSC Financial Statements for the year ended 31 December 2016 Contents Independent Auditors Report Statement of Profit or Loss and Other

Ameriabank CJSC Financial statements

Ameriabank CJSC Financial statements for the year ended 31 December together with independent auditors report Ameriabank CJSC Financial statements Contents Independent auditors report Statement of comprehensive

Ameriabank CJSC Financial statements for the year ended 31 December together with independent auditors report Ameriabank CJSC Financial statements Contents Independent auditors report Statement of comprehensive

Orange Rules GUARANTY TRUST BANK PLC

Orange Rules GUARANTY TRUST BANK PLC Contents Page Consolidated financial statements Consolidated statement of financial position 1 Consolidated statement of comprehensive income 2 Consolidated statement

Orange Rules GUARANTY TRUST BANK PLC Contents Page Consolidated financial statements Consolidated statement of financial position 1 Consolidated statement of comprehensive income 2 Consolidated statement

FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2010 PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS

EMPORIKI BANK ROMANIA SA FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2010 PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER

EMPORIKI BANK ROMANIA SA FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2010 PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER

PUBLIC JOINT STOCK COMPANY JOINT STOCK BANK UKRGASBANK Financial Statements. Year ended 31 December 2011 Together with Independent Auditors Report

PUBLIC JOINT STOCK COMPANY JOINT STOCK BANK UKRGASBANK Financial Statements Year ended 31 December 2011 Together with Independent Auditors Report Contents Independent Auditors Report Statement of financial

PUBLIC JOINT STOCK COMPANY JOINT STOCK BANK UKRGASBANK Financial Statements Year ended 31 December 2011 Together with Independent Auditors Report Contents Independent Auditors Report Statement of financial

Consolidated Financial Statements

Consolidated Financial Statements Table of Contents Consolidated Statement of Financial Position 34 Consolidated Statement of Income 35 Consolidated Statement of Comprehensive Income 36 Consolidated Statement

Consolidated Financial Statements Table of Contents Consolidated Statement of Financial Position 34 Consolidated Statement of Income 35 Consolidated Statement of Comprehensive Income 36 Consolidated Statement

AGBANK OPEN JOINT-STOCK COMPANY

AGBANK OPEN JOINT-STOCK COMPANY Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive income... 5 Statement of

AGBANK OPEN JOINT-STOCK COMPANY Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive income... 5 Statement of

Accounting policy

Accounting policy 30.06.18 1. Principal activities ACBA-Credit Agricole Bank CJSC (the Bank ) is the parent company in the Group, which is comprised of the Bank and its subsidiary ACBA Leasing Credit Organization

Accounting policy 30.06.18 1. Principal activities ACBA-Credit Agricole Bank CJSC (the Bank ) is the parent company in the Group, which is comprised of the Bank and its subsidiary ACBA Leasing Credit Organization

JSC «AsiaСredit Bank (АзияКредит Банк)» Financial Statements for the year ended 31 December 2010

» Financial Statements for the year ended 31 December 2010") JSC «AsiaСredit Bank (АзияКредит Банк)» Financial Statements for the year ended 31 December Contents Independent Auditors Report Statement of Comprehensive Income 5 Statement of Financial Position 6 Statement

JSC «AsiaСredit Bank (АзияКредит Банк)» Financial Statements for the year ended 31 December Contents Independent Auditors Report Statement of Comprehensive Income 5 Statement of Financial Position 6 Statement

Ardshinbank CJSC. Financial Statements for the year ended 31 December 2014

Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive income... 4 Statement of financial position... 5 Statement

Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive income... 4 Statement of financial position... 5 Statement

ALPHA BANK ALBANIA SH.A

Financial Statements for the year ended 31 December 2015 (with independent auditors report thereon) Contents Independent Auditors Report Page Financial statements for the year ended 31 December 2015: Statement

Financial Statements for the year ended 31 December 2015 (with independent auditors report thereon) Contents Independent Auditors Report Page Financial statements for the year ended 31 December 2015: Statement

INDUSTRIAL AND COMMERCIAL BANK OF CHINA (CANADA)

") Financial Statements of INDUSTRIAL AND COMMERCIAL BANK OF CHINA (CANADA) KPMG LLP Telephone (416) 777-8500 Chartered Accountants Fax (416) 777-8818 Bay Adelaide Centre Internet www.kpmg.ca 333 Bay Street

Financial Statements of INDUSTRIAL AND COMMERCIAL BANK OF CHINA (CANADA) KPMG LLP Telephone (416) 777-8500 Chartered Accountants Fax (416) 777-8818 Bay Adelaide Centre Internet www.kpmg.ca 333 Bay Street

Anelik Bank CJSC. Financial Statements for the year ended 31 December 2017

Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive income... 8 Statement of financial position... 9 Statement

Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other comprehensive income... 8 Statement of financial position... 9 Statement

Ameriabank cjsc. Financial Statements for the Year Ended 31 December 2009

Financial Statements for the Year Ended 31 December Contents Independent Auditors Report... 3 Statement of comprehensive income... 4 Statement of financial position... 5 Statement of cash flows... 6 Statement

Financial Statements for the Year Ended 31 December Contents Independent Auditors Report... 3 Statement of comprehensive income... 4 Statement of financial position... 5 Statement of cash flows... 6 Statement

Prospera Credit Union. Consolidated Financial Statements December 31, 2012 (expressed in thousands of dollars)

") Consolidated Financial Statements February 19, 2013 Independent Auditor s Report To the Members of Prospera Credit Union We have audited the accompanying consolidated financial statements of Prospera Credit

Consolidated Financial Statements February 19, 2013 Independent Auditor s Report To the Members of Prospera Credit Union We have audited the accompanying consolidated financial statements of Prospera Credit

Consolidated Financial Statements of ALTERNA SAVINGS

Consolidated Financial Statements of March 9, 2018 Independent Auditor s Report To the Members of Alterna Savings and Credit Union Limited We have audited the accompanying consolidated financial statements

Consolidated Financial Statements of March 9, 2018 Independent Auditor s Report To the Members of Alterna Savings and Credit Union Limited We have audited the accompanying consolidated financial statements

Individual Financial Statements 30 June 2012

Individual Financial Statements 30 June 2012 Prepared in accordance with the International Financial Reporting Standards as endorsed by the European Union Contents Individual income statement 1 Individual

Individual Financial Statements 30 June 2012 Prepared in accordance with the International Financial Reporting Standards as endorsed by the European Union Contents Individual income statement 1 Individual

STATEMENT OF PROFIT OR LOSS For the year ended 31 December 2014 Financial statements Note 2014 2013 Interest income Cash and cash equivalents 893,744 506,424 Loans to customers 1,020,693 440,642 Amounts

STATEMENT OF PROFIT OR LOSS For the year ended 31 December 2014 Financial statements Note 2014 2013 Interest income Cash and cash equivalents 893,744 506,424 Loans to customers 1,020,693 440,642 Amounts

- CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME Note 2015 2014 US$ 000s US$ 000s (Restated) Continuing operations Lease revenue 56,932 48,691 Other income 9 3,202 3,435 60,134

- CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME Note 2015 2014 US$ 000s US$ 000s (Restated) Continuing operations Lease revenue 56,932 48,691 Other income 9 3,202 3,435 60,134

Prospera Credit Union. Consolidated Financial Statements December 31, 2015 (expressed in thousands of dollars)

") Consolidated Financial Statements February 19, 2016 Independent Auditor s Report To the Members of Prospera Credit Union We have audited the accompanying consolidated financial statements of Prospera Credit

Consolidated Financial Statements February 19, 2016 Independent Auditor s Report To the Members of Prospera Credit Union We have audited the accompanying consolidated financial statements of Prospera Credit

Union Bank of Nigeria Plc

Consolidated Interim Financial Statements For the period ended 31 March 2013 Table of Contents Consolidated financial statements Page Consolidated financial statements: Consolidated statement of financial

Consolidated Interim Financial Statements For the period ended 31 March 2013 Table of Contents Consolidated financial statements Page Consolidated financial statements: Consolidated statement of financial

Universal Investment Bank AD Skopje. Financial Statements for the year ended 31 December 2010

for the year ended 31 December 2010 Contents Independent Auditors' report Statement of financial position 1 Statement of comprehensive income 2 Statement of changes in equity 3 Statement of cash flows

for the year ended 31 December 2010 Contents Independent Auditors' report Statement of financial position 1 Statement of comprehensive income 2 Statement of changes in equity 3 Statement of cash flows

Tirana Bank sh.a. Financial Statements as of and for the year ended 31 December 2016

Financial Statements as of and for the year ended 31 December 2016 TABLE OF CONTENT AUDITOR S REPORT STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME 8 STATEMENT OF FINANCIAL POSITION 9 STATEMENT

Financial Statements as of and for the year ended 31 December 2016 TABLE OF CONTENT AUDITOR S REPORT STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME 8 STATEMENT OF FINANCIAL POSITION 9 STATEMENT

Farm Credit Armenia Universal Credit Organization Commercial Cooperative

Farm Credit Armenia Universal Credit Organization Commercial Cooperative Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other

Farm Credit Armenia Universal Credit Organization Commercial Cooperative Financial Statements for the year ended 31 December Contents Independent Auditors Report... 3 Statement of profit or loss and other

Notes to the Consolidated Financial Statements

251 Deutsche Bank Consolidated Statement of Income 245 Annual Report 2015 Consolidated Statement of Consolidated Financial Statements 251 Consolidated Statement of Consolidated Balance Sheet 289 Consolidated

251 Deutsche Bank Consolidated Statement of Income 245 Annual Report 2015 Consolidated Statement of Consolidated Financial Statements 251 Consolidated Statement of Consolidated Balance Sheet 289 Consolidated

PASHA YATIRIM BANKASI A.Ş. FINANCIAL STATEMENTS AS AT 31 DECEMBER 2017 TOGETHER WITH INDEPENDENT AUDITOR S REPORT

FINANCIAL STATEMENTS AS AT 31 DECEMBER 2017 TOGETHER WITH INDEPENDENT AUDITOR S REPORT CONTENTS Independent auditors review report Statement of financial position... 1 Statement of income... 2 Statement

FINANCIAL STATEMENTS AS AT 31 DECEMBER 2017 TOGETHER WITH INDEPENDENT AUDITOR S REPORT CONTENTS Independent auditors review report Statement of financial position... 1 Statement of income... 2 Statement

Azer-Turk Bank Open Joint Stock Company Financial statements. Year ended 31 December 2016 together with independent auditor s report

Financial statements Year ended 31 December together with independent auditor s report financial statements Contents Independent auditor s report Financial statements Statement of financial position...

Financial statements Year ended 31 December together with independent auditor s report financial statements Contents Independent auditor s report Financial statements Statement of financial position...

NALCOR ENERGY MARKETING CORPORATION FINANCIAL STATEMENTS December 31, 2016

FINANCIAL STATEMENTS December 31, 2016 Deloitte LLP 5 Springdale Street, Suite 1000 St. John's NL A1E 0E4 Canada Tel: (709) 576-8480 Fax: (709) 576-8460 www.deloitte.ca Independent Auditor s Report To

FINANCIAL STATEMENTS December 31, 2016 Deloitte LLP 5 Springdale Street, Suite 1000 St. John's NL A1E 0E4 Canada Tel: (709) 576-8480 Fax: (709) 576-8460 www.deloitte.ca Independent Auditor s Report To

Annual Financial Statements 2017

Annual Financial Statements 2017 For the year ended March 31, 2017 Contents 02 Consolidated Statement of Income 02 Consolidated Statement of Comprehensive Income 03 Consolidated Statement of Financial

Annual Financial Statements 2017 For the year ended March 31, 2017 Contents 02 Consolidated Statement of Income 02 Consolidated Statement of Comprehensive Income 03 Consolidated Statement of Financial

BPS-Sberbank and subsidiaries Consolidated financial statements

and subsidiaries Consolidated financial statements For the year ended together with independent auditors report Consolidated financial statements Contents Audit report of independent audit firm Consolidated

and subsidiaries Consolidated financial statements For the year ended together with independent auditors report Consolidated financial statements Contents Audit report of independent audit firm Consolidated

NALCOR ENERGY MARKETING CORPORATION FINANCIAL STATEMENTS December 31, 2017

FINANCIAL STATEMENTS December 31, 2017 Deloitte LLP 5 Springdale Street, Suite 1000 St. John's NL A1E 0E4 Canada Tel: (709) 576-8480 Fax: (709) 576-8460 www.deloitte.ca Independent Auditor s Report To

FINANCIAL STATEMENTS December 31, 2017 Deloitte LLP 5 Springdale Street, Suite 1000 St. John's NL A1E 0E4 Canada Tel: (709) 576-8480 Fax: (709) 576-8460 www.deloitte.ca Independent Auditor s Report To

LLC Deutsche Bank. Financial Statements for the year ended 31 December 2014 and Auditors Report

Financial Statements for the year ended 31 December 2014 and Auditors Report Contents Auditors Report... 3 Statement of profit or loss and other comprehensive income... 6 Statement of financial position...

Financial Statements for the year ended 31 December 2014 and Auditors Report Contents Auditors Report... 3 Statement of profit or loss and other comprehensive income... 6 Statement of financial position...

JOINT-STOCK COMPANY BANK CREDIT SUISSE (MOSCOW) Financial Statements for the year ended 31 December 2015 and Auditors Report

Financial Statements for the year ended 31 December 2015 and Auditors Report") JOINT-STOCK COMPANY BANK CREDIT SUISSE (MOSCOW) Financial Statements for the year ended 31 December 2015 and Auditors Report 1 Contents Auditors Report... 3 Statement of Profit or Loss anf Other Comprehensive

JOINT-STOCK COMPANY BANK CREDIT SUISSE (MOSCOW) Financial Statements for the year ended 31 December 2015 and Auditors Report 1 Contents Auditors Report... 3 Statement of Profit or Loss anf Other Comprehensive

PUBLIC JOINT-STOCK COMPANY JOINT STOCK BANK UKRGASBANK