The Top 10 Loan Documentation Mistakes

|

|

|

- Lambert Bruce

- 5 years ago

- Views:

Transcription

1 Your State Association Presents Lenders Learn TM The Top 10 Loan Documentation Mistakes Program Materials Use this document to follow along with the webinar. Please test your system before the broadcast. Be sure to print enough copies for all listeners. September 7, 2016 Presenter: Robin Russell Technical Support (for faster service please submit inquiries via or online): (Registration & Tech Support): - Phone- (877) FOR ADDITIONAL ASSISTANCE PLEASE REFER TO OUR FAQs

2 About Lenders Learn TM Lenders Learn TM provides lenders and compliance officers with a deep understanding of secured lending. For each of the 15 core courses (30 hours total), attendees receive a copy of the slides and at least one chapter from Robin s new 2016 Multistate Secured Lending Guide. Once you have completed the core curriculum, you will have a 17 chapter reference. Whether your bank registers for one or all 15 webinars, you will find the information practical and valuable. See below for 2016 broadcast dates. 1: Basic Business Entities (1/21) 2: The UCC for Lenders (2/3) 3: Loan Doc 101: The Basics (2/10) 4: Loan Doc 101: Business Collateral (2/23) 5 & 6: Loan Doc 101: Perfection by Possession & Control (2/18) 7 & 8: Basic RE Loan Documentation (3/2 & 3/3) 9: Oil & Gas Lending (4/6) 10: Agricultural Lending (4/18) 11: Commercial Loan Documentation (5/3 & 5/4) 12: Letters of Credit (5/17) 13: Lending to Municipalities (8/24) 14, 15, 16: Basic Bankruptcy for Bankers (11/2) 17: Loan Participations (11/15) Also Recommended: Advanced Commercial Loan Documentation (6/1) Top Loan Documentation Mistakes (9/7) Understanding Commercial Loan Documents (9/20) Understanding Real Estate Loan Documents (9/22) Commercial Real Estate Loan Documentation (12/7) All programs will be recorded and available for viewing after the broadcast date. If you would like to complete the Lenders Learn TM curriculum and missed the webinar, please visit the on-demand catalog to register.

3 The Top 10 Loan Documentation Mistakes Robin Russell Andrews Kurth LLP 1

4 Robin Russell ROBIN RUSSELL Robin is a fellow in the American College of Bankruptcy. She combines a depth of experience in bankruptcy restructuring and litigation with financial transactions. She has represented corporate debtors, liquidating trustees, bondholders, unsecured creditors' committees, bank groups, private equity funds, landlords, trade creditors and bidders for estate assets in Chapter 11 and Chapter 7 bankruptcy proceedings and has litigated fraudulent conveyance and preference claims in bankruptcy and district court. She has also represented banks, institutional lenders and corporate borrowers in commercial loan transactions and debt restructurings. Robin is the principal author of Thomson Reuters Texas Practice Guides for both Creditors Rights and Financial Transactions and the Texas Bankers Association s Texas Secured Lending Guide, Texas Real Estate Lending Guide, Texas Problem Loan Guide and Texas Account Documentation Guide. She is a frequent speaker on banking, bankruptcy and financial restructuring related topics, an elected member of the American Law Institute and has served as a Chapter 7 Trustee. Robin received her LL.M. in Banking Law from Boston University and her J.D. from Baylor University where she was Editor in Chief of the Baylor Law Review and the highest ranking graduate in her class. Prior to joining the firm she clerked for the Texas Supreme Court. 2 2

5 Notice This presentation is designed to provide accurate and authoritative information in regard to the subject matter covered. It is provided with the understanding that neither the presenter nor your State Bankers Association is engaged in rendering legal, accounting or other professional advice or service. If legal advice or other expert assistance is required, the services of a competent professional person should be sought from a Declaration of Principles Adopted by the American Bar Association and a committee of Publishers and Associations. 3 3

6 How Do I Become A Secured Creditor? Lien a/k/a Attachment + Perfection = Secured Status Security Agreement + UCC-1 Deed of Trust + Recording in County Ship Mortgage + Coast Guard Filing Aircraft Security Agreement + FAA Filing Investment Property + Account Control Agreement Security Agreement 4 4

7 Attachment Bank gives value Debtor has rights in collateral Debtor has signed written agreement granting lien 5 5

8 So Why Do I Want To Be A Secured Creditor? 6 6

9 The Covered Dish Supper Rules of Priority Possessory Lienholder PMSI Secured Unsecured Equity 7 7

10 Bankruptcy 101 Assets fmv 500,000 Liabilities 2,000,000 Bank Debt 500,000 Trade Debt 750,000 Judgment 750,000 If Bank is secured and perfected - 100% recovery If Bank unsecured or unperfected - 25% recovery 8 8

11 Top 10 Mistakes 1. Misclassification of collateral 2. Filing the perfection document in the wrong location 3. Using the wrong borrower/debtor name 4. Not obtaining the proper authorization documentation 5. Having a bad collateral description 6. Improper assessment of lien position 7. Failing to amend your UCC-1 8. Failing to continue or terminate your UCC-1 9. Leaving items to post closing or making exceptions 10. Inadvertently waiving rights 9 9

12 Avoiding Mistake #1: Proper Classification of Collateral 10 10

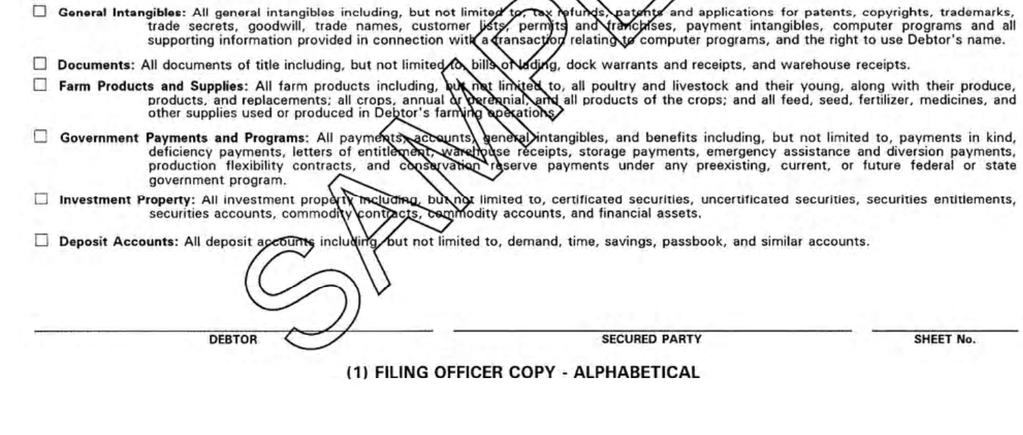

13 Business Collateral Inventory Warehouse Receipts and Bills of Lading Farm Products Warehouse Receipts and Bills of Lading Deposit Accounts Accounts Government Contracts Instruments Investment Property Cash Chattel Paper Letter of Credit Rights General Intangibles Tort Claims Equipment Fixtures Motor Vehicles Boats Vessels Aircraft Rolling Stock 11 11

14 Types of Collateral Inventory Accounts U.S. Government Contracts Chattel Paper Equipment Fixtures Leasehold Improvements General Intangibles Instruments Deposit Accounts Investment Property Documents: Warehouse Receipts and Bills of Lading Agricultural Collateral/Farm Products Consumer Goods Life Insurance Motor Vehicles Manufactured Homes Boats and Vessels Aircraft Rolling Stock Oil and Gas Tort Claims Letter of Credit Rights Guaranties and Third Party Pledges of Collateral 12 12

15 What Types of Collateral Are Covered by the UCC-1? The UCC covers five types of tangible personal property: Inventory Equipment Fixtures Farm Products Consumer Goods Intangible personal property is divided into the following classifications under the UCC: Accounts (If accounts represent amounts due from the U.S. government, they may be subject to special rules for Government Contracts) Chattel Paper General Intangibles Instruments Investment Property Deposit Accounts (Commercial) Letter of Credit Rights Commercial Tort Claims 13 13

16 What Types of Collateral are Not Covered by the UCC-1? Tangible personal property includes the following types of collateral not exclusively covered by the UCC: Motor Vehicles Manufactured Homes Boats and Vessels Aircraft Rolling Stock (i.e., railroad cars) Intangible personal property also includes the following types of collateral not subject to the UCC: Life Insurance Deposit Accounts (Consumer) Non Commercial Tort Claims 14 14

17 Avoiding Mistake #2: Filing in the Right Location 15 15

18 16 16

19 Methods Of Perfection File UCC-1 Possession Control Notation on Title Non-UCC Filings 17 17

20 Basic UCC-1 Filing Location Rules A debtor who is an individual is located in the state of the individual s principal residence. A registered organization that is organized under the law of a state is located in that state. A debtor that is a nonregistered organization (i.e., a general partnership) and has only one place of business is located in the state of its place of business. A debtor that is a nonregistered organization and has more than one place of business is located in the state of its chief executive office

21 Additional UCC-1 Filing Locations A registered organization that is organized under the law of the United States and a branch or agency of a bank that is not organized under the law of the United States or a state are located: in the state that the law of the United States designates, if the law designates a state of location; in the state that the registered organization, branch, or agency designates, if the law of the United States authorizes the registered organization, branch, or agency to designate its state of location; or in the District of Columbia, if neither of the above applies (ex. Citizen of foreign country). A branch or agency of a bank that is not organized under the law of the United States or a state is located in the state in which the branch or agency is licensed, if all branches and agencies of the bank are licensed in only one state. The United States is located in the District of Columbia. A foreign air carrier is located at the designated office of the agent upon which service of process may be made on behalf of the carrier

22 Special UCC-1 Filing Location Issues A registered organization continues to be located in the jurisdiction notwithstanding: the suspension, revocation, forfeiture, or lapse of the registered organization s status as such in its jurisdiction of organization; or the dissolution, winding up, or cancellation of the existence of the registered organization. A debtor who ceases to exist, have a residence or have a place of business continues to be located in the jurisdiction where it last existed, resided or did business

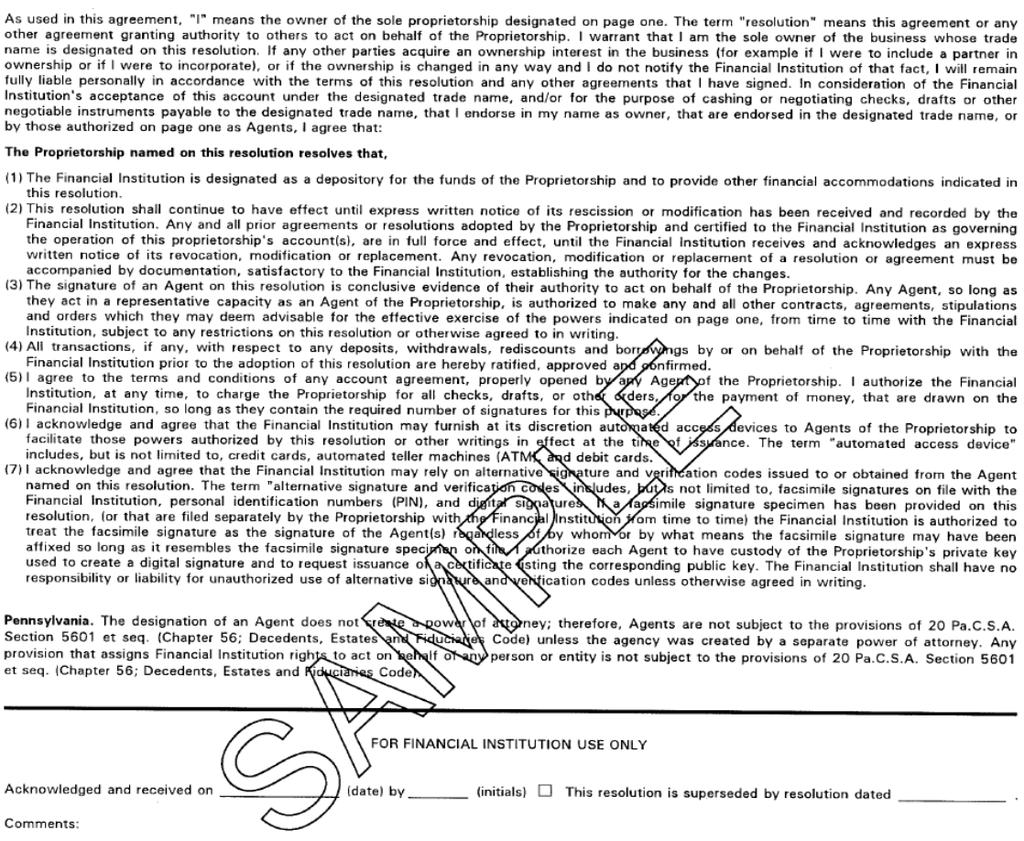

23 At What Point in Time Do I File a UCC-1? May file before security agreement signed Should file before funds advanced 21 21

24 Avoiding Mistakes #3 and #4: Using the Debtor s Name Right and Obtaining Proper Authorization Documentation 22 22

25 Who is your Debtor? The person who owns the property being pledged to you. This is not always the borrower. It may be a guarantor or a third party only pledging collateral

26 Debtor Name The most important element when preparing a UCC-1 financing statement is the debtor name. The debtor name should be nothing more and nothing less than the legal name of the debtor. Do not abbreviate words in the debtor name unless the legal debtor name contains abbreviations

27 Individual Exact full legal name Goes By Nickname = John Lee Doe = J.L. Doe = Bubba Doe Debtor for UCC-1 = John Lee Doe 25 25

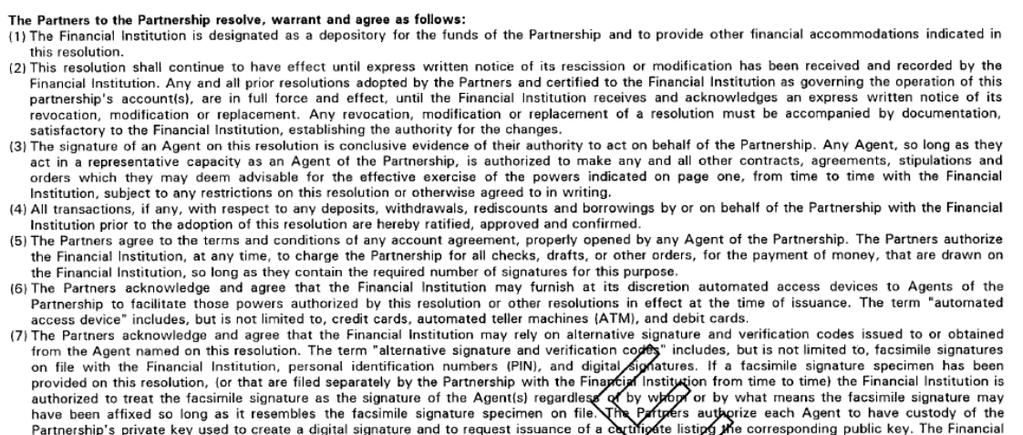

28 26 26

29 Sole Proprietorship d/b/a An individual doing business under an assumed name John Lee Doe d/b/a John s Auto d/b/a Autoworld d/b/a John s Flowers 27 27

30 Authorization Documents Required for Sole Proprietorship Assumed Name Certificate Sole Proprietorship Resolution of Authority 28 28

31 29 29

32 30 30

33 What if my loan officer wants to put the d/b/a in the loan documents? Correct > John Lee Doe* * individually and doing business under any assumed name including, without limitation, John s Auto Wrong > John Lee Doe d/b/a John s Auto 31 31

34 UCC-1? General partner personally liable for partnership debts UCC-1? general partner John Doe Robert Brown John s Auto UCC-1 If all partner s surnames are not in partnership name (i.e., Doe & Brown Auto) then in most states the partnership name (i.e., John s Auto) is considered an assumed name

35 Authorization Documents Required for General Partnership/Joint Venture Partnership Agreement Partnership Resolution of Authority Assumed Name Certificate 33 33

36 34 34

37 35 35

38 John s Corporate Shell, Inc. General Partner John Doe Jane Doe Limited Partners Bob Smith Liable for debts of limited partnership Not liable for debts of limited partnership John s Auto, LP John s Auto, L.P. by its general partner John s Corporate Shell, Inc. Signature By: Title: John Doe, President 36 36

39 Authorization Documents Required for Limited Partnership Limited Partnership Agreement Certificate of Limited Partnership or Certificate of Formation Certificate of Fact: Status Partnership Resolution of Authority Certificate of Authority to Transact Business in all states in which entity does business Certificate of Fact: Assumed Name 37 37

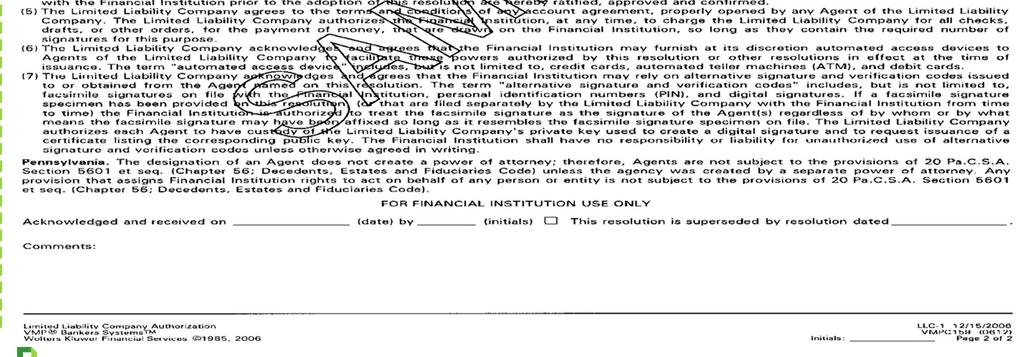

40 Shareholder Shareholder Shareholder John s Auto, Inc. John s Auto, Inc. Signature By: Title: 38 38

41 Authorization Documents Required for Corporation Certificate of Formation or Articles or Certificate of Incorporation Bylaws Certificate of Fact: Status Certificate of Franchise Tax Account Status Resolutions of the Board of Directors Certificate of Authority to Transaction Business Certificate of Fact: Assumed Name 39 39

42 Corporate Resolutions A meeting was held on a certain date The corporation made a decision to request a loan from the lender The loan will benefit the corporation Certain officers designated by name and title are authorized to execute loan documents on behalf of the corporation Pledging of corporate assets as collateral is authorized *Funding of any loan should not occur prior to receipt of a properly executed corporate borrowing resolution. Otherwise, the borrowing could be challenged as unauthorized

43 Best Practices Checklist Has the Bank satisfied itself prior to funding that: The borrowing under consideration is permitted Officers who are signing have been properly authorized Corporation does not have a maximum indebtedness clause which will be violated (from another credit arrangement or board action) All conditions precedent to borrowing have been met Exact corporate name on loan documents matches with documents on file related to the corporation, Liens and security interests in collateral are proper and within the powers of the corporation as granted by its Board

44 42 42

45 43 43

46 Member Member Member John s Auto, L.L.C. John s Auto, L.L.C. Signature By: Title: Manager 44 44

47 Authorization Documents Required for Limited Liability Company Articles of Organization or Certificate of Formation Regulations or Company Agreement Certificate of Fact: Status Certificate of Franchise Tax Account Status Resolutions of the Members Certificate of Authority to Transact Business in all states in which entity does business Certificate of Fact: Assumed Name 45 45

48 46 46

49 47 47

50 Agent Acting under Power of Attorney durable v. nondurable powers of attorney broad powers v. limited powers effective now v. effective later and later even if the principal becomes incompetent or incapacitated when the principal becomes incompetent or incapacitated a P of A cannot survive the death of the principal 48 48

51 Trust/Custodial Relationships Trustee legal title Custodian Trust Property UTMA Property Beneficiary income stream (general intangible) beneficial owner Minor John Doe, Trustee The Doe Family Trust Name Diana Doe as Custodian under UTMA for Sterling Doe 49 49

52 Authorization Documents Required for Trust Trust Agreement Confirmation that loan proceeds are for benefit of beneficiary 50 50

53 Beneficiary of a Trust A trust interest is a general intangible A spendthrift trust prohibits the beneficiary from pledging the trust interest as collateral for a loan The Bank may take a lien on the property purchased with loan proceeds as collateral but not the trust interest The Bank may consider the trust distributions in determining creditworthiness 51 51

54 Avoiding Mistake #5: Correct Collateral Description 52 52

55 Requirements Of A Lien Document Mandatory Identify parties Identify what obligation is being secured Identify collateral Contain words of grant granting lien on collateral In writing Signed by owner of collateral Optional Representations/Warranties Covenants Events of Default Remedies 53 53

56 COVENANTS Duties Toward Property possession good repair payment of taxes access to inspect collateral notification of loss access to books and records nondisposition (unless ordinary course) recordation of security interest on chattel paper proper collection and settlement of accounts no commingling of proceeds direct payment of accounts receivable list of buyers for Farm Security Act notices insurance Other Duties authorization of secured party to file financing statement authorization of secured party to protect collateral 54 54

57 Representations and Warranties valid existence as entity authorization to execute and perform past, present and future name ownership of collateral use of property (personal, business, agricultural) 55 55

58 UCC-1 Financing Statement Requirements To be effective, a Financing Statement must: give the name of the debtor(s), give the name of the secured party, give a description of the collateral, provide a mailing address for the debtor and the Secured Party of record, indicate whether the debtor is an individual or an organization, or, if the debtor is an organization, provide the type of organization and the jurisdiction of organization of the debtor, signature of debtor not required

59 Collateral Description A collateral description in the UCC-1 (but not the security agreement) on commercial collateral may simply state all assets or all property. A UCC-1 on consumer goods requires a description of the specific consumer good. A security interest in a consumer s investment property requires specific identification of the account. A commercial tort claim must be specifically described

60 Name of Record Owner If the name of the record owner is required in the UCC-1, it should be obtained through an abstract or title company or from a recent real estate tax bill or some similar document. A mailing or street address is not sufficient as a description. The following is an example of a legal description of real property: Lot Fifty-Six (56), in Block Five (5), Plat of Bayou Woods, Section (8), in Harris County, Texas, according to the map thereof recorded in Volume 224, Page 15, of the Map Records of Harris County, Texas

61 59 59

62 60 60

63 61 61

64 Avoiding Mistake #6: Proper Assessment of Lien Position 62 62

65 Types of Lien Searches UCC Secretary of State or other Central Filing Office County Real Estate Records Review of Certificate of Title Special Filing Office 63 63

66 Where Do I Conduct a Lien Search? Lien searches are done in the locations for UCC-1 Financing Statements in the state where the debtor is located. A lien search is done on the legal name of the Debtor

67 What Names Do I Search? An incomplete debtor name may result in a failure to disclose all the desired information. Example #1: Example #2: Real Name: Autoworld, Inc. Name Searched: Autoworld, Corp Result: Filings against Autoworld Inc. will be shown because Inc. and Corp. are currently considered ancillary information by the Texas Secretary of State. Real Name: Autoworld of Texas, Inc. Name Searched: Autoworld of California; Result: Filings against Autoworld of Texas not shown

68 66 66

69 67 67

70 68 68

71 Liens Not Disclosed By UCC Lien Search Liens filed at the county level such as state tax liens and liens on fixtures. Liens perfected by possession, such as liens on chattel paper and certificated securities. Liens on special classes of collateral such as ships, aircraft, rolling stock, motor vehicles and manufactured homes. UCC-1 filings on the debtor in states not searched. Nonownership of the collateral by the debtor. A lien against the prior owner of the collateral

72 General Rules of Priority secured v. unsecured > secured wins perfected v. unperfected > perfected wins possession v. filing > possession wins first to file > wins pre-existing security interest > wins purchase money security > wins as to interest (PMSI) specific collateral 70 70

73 First-to-File (Subordination) John s Auto, Inc. 9/8/03 UCC-1 filed by John Doe, Sr. John s Auto, Inc. 8/10/07 UCC-1 filed by Bank #1 Subordination 71 71

74 Purchase Money Security Interest Equipment and Fixtures file UCC-1 within 20 days of possession Inventory file UCC-1 before debtor takes possession (i.e., pre-filing) notification to other lien holders within last five years Farm Products pre-filing notification to other lien holders within last six months Consumer Goods 72 72

75 Purchase Money Security Interest John s Auto, Inc. 9/8/03 UCC-1 John Doe, Sr. John s Auto, Inc. 8/10/07 UCC-1 filed by Bank #1 on all assets John s Auto, Inc. 12/8/09 UCC-1 filed by Bank #2 PMSI on specific office equipment 73 73

76 Possessory Liens John s Auto, Inc. 9/8/03 UCC-1 John Doe, Sr. John s Auto, Inc. 8/10/07 UCC-1 filed by Bank #1 on all assets John s Auto, Inc. 12/8/09 UCC-1 filed by Bank #2 PMSI on specific office equipment John s Auto, Inc. 4/15/12 Equipment taken to repair shop John s Auto, Inc. 1/10/14 Rent is unpaid 74 74

77 What are Proceeds? Proceeds include whatever is received upon the sale, exchange, collection or other disposition of collateral or proceeds of collateral. Insurance payable due to loss or damage to collateral is proceeds if the debtor is the beneficiary. Money, checks, deposit accounts and the like are cash proceeds. All other proceeds of collateral are noncash proceeds

78 Requirements for Continued Perfection of a Security Interest in Proceeds The Bank s security interest continues in collateral, notwithstanding the sale, exchange or other disposition thereof by the borrower unless the disposition was authorized by the Bank in the security agreement or otherwise. Bank s security interest continues described below, in any identifiable proceeds of the collateral, including collections received by the borrower. The Bank s security interest in proceeds becomes unperfected on the 21 st day after the borrower receives the proceeds unless: A UCC-1 covers the original collateral and the proceeds are collateral in which a security interest may be perfected by filing a UCC-1 in the same office in which the original UCC-1 was filed. The proceeds are identifiable cash proceeds; or A security interest in the proceeds is perfected before the expiration of the 20- day period

79 Illustration of Perfection Requirements For Proceeds If the Bank has a security interest in medical equipment which it has perfected by the filing of a financing statement describing medical equipment and the borrower exchanges some of the medical equipment for office equipment, the Bank will have a continuously perfected security interest in the office equipment. On the other hand, if the borrower sells the medical equipment and uses the cash to buy a car, the Bank s perfected security interest in the car will lapse at the end of the 20 days, because there will be no notation on the certificate of title to indicate that the Bank has a security interest in the office equipment. If the borrower sells an x-ray machine for cash and then uses the cash to buy the vaccine, the Bank will have a continuously perfected security interest in the vaccine because it is inventory as described in the financing statement

80 Personal Property Lien Subordination 78 78

81 79 79

82 80 80

83 Examples of Title Verification Documentation Bill of Sale Invoice Title Deed of Trust 81 81

84 Avoiding Mistake #7: Knowing When to Amend Your UCC

85 UCC-3 Form UCC-3 is used to make changes in the original UCC-1 Financing Statement. A UCC-3 is a multipurpose form used to renew, transfer, amend or terminate a UCC

86 84 84

87 When Do I Need to Amend a UCC-1? Add collateral Delete collateral (i.e., a partial release) Reflect an address change Anytime the UCC-1 becomes seriously misleading 85 85

88 Addition of Collateral An Amendment filed on Form UCC-3 may be used to add other collateral. A clear description of any collateral to be added must be included. An Amendment adding collateral is effective as to the added collateral only from the date of filing the Amendment

89 What is Seriously Misleading? John s Auto Inc. UCC-1 5/8/08 Jane Anne Doe Autoworld, Inc. 1/1/10 4 months Jane Anne Smith 5/1/10 no longer perfected on after acquired 8/21/10 Bank #2 files UCC-1 on Autoworld, Inc

90 Change Corporate Structure of Debtor If the debtor changes its location to another jurisdiction the Bank must refile in the new location within four months. EXAMPLE: Debtor is a general partnership whose chief executive office is in Texas. Bank perfects a security interest by filing in Texas. Debtor moves its chief executive office to New Mexico. Bank has four months to refile in New Mexico. If the original debtor merges with another entity resulting in a new debtor located in a different state (example, Delaware corporation merges into Texas corporation), the following rules will apply: The Secured Party has one year to file a UCC-1 in the new state (in the above example, Texas) unless the name of the new debtor is seriously misleading when compared to the name of the original debtor. In this event the Secured Party has only four months to file in the new state to file or risk the loss of a perfection with respect to after-acquired property

91 Refiling of Expired Financing Statements A new Financing Statement may be filed where the original filing has lapsed. Priority established with the original filing would not be maintained as the new filing would not relate back to the file date of the original filing. An intervening lien would take priority over the lapsed financing statement 89 89

92 Transfer of Collateral by Borrower The UCC does not require a refiling in the name of a transferee in the case of a transfer of the collateral by the borrower to a transferee located in the same state as the borrower. It is advisable for the Bank to file Form UCC-3 when the transfer is made subject to the Bank s security interest or to file Form UCC-1 when a transfer is made by the borrower to a transferee who executes an assumption agreement. If the original debtor transfers the collateral to a transferee located in a different state, the Secured Party has one year to file in the new state to maintain perfection and priority. Example: Delaware corporation transfers to California limited partnership Bank has one year to refile in California

93 Avoiding Mistake #8: Knowing When to Continue or Terminate Your UCC

94 How Long Does My UCC-1 Last? A Form UCC-1 Financing Statement is effective for five (5) years and may be extended for additional five year periods during the six-month window prior to expiration of the previous five-year period. A UCC-1 filed in connection with a public-finance transaction is effective for 30 years. A UCC-1 on fixtures filed in the County Real Property Records is effective for five years. A fixture financing statement contained within a mortgage or deed of trust it is effective for the term of the mortgage or deed of trust

95 Termination/Total Release A Termination Statement may be filed where all secured parties wish to terminate a financing statement, or where one or more, but not all, secured parties wish to totally release their lien against the debtor. The termination is only effective as to the secured parties who are named in item 9 of form UCC

96 Termination Consumer Bank (i.e., secured party) must file termination within 20 days after authenticated demand but no later than one month after no outstanding obligation and no commitment to advance Business Bank must send debtor termination statements or file them within 20 days after authenticated demand if no commitment to advance no outstanding obligation 94 94

97 Continuation Central Filing: UCC-1 good for five (5) years County Real Estate Records (on fixtures) in most states good for longer of UCC-1 or length of deed of trust Bankruptcy filing continuation does not violate automatic stay 95 95

98 Total or Partial Assignment An assignment may be made by One or more secured parties A secured party may assign all (Total Assignment) or part (Partial Assignment) of their interest under a Financing Statement. The Form UCC-3 must set forth the name and address of the assignee and identify the secured party making the assignment (Item 9). For a Partial Assignment, a description of the specific collateral assigned must be included

99 Avoiding Mistake #9: Don t Make Exceptions or Leave Items Until Post Closing 97 97

100 Guarantees Must be in writing Must be supported by consideration Guarantees signed after funding are not supported by consideration 98 98

101 Review Checklists Make certain promissory note, lien document and guaranty contain no errors, all blanks have been filled in, all blocks checked and all signatures obtained and witnessed or notarized, if required. Loan officers or their counsel must review the lien searches so the bank will be in first lien position. Check collateral specific documents required

102 Review Checklists (continued) Obtain Borrower s affidavit regarding no bankruptcies, judgments or other legal actions pending. Existing insurance policies should be reviewed for adequacy of coverage. Bank to be named as mortgagee and loss payee on casualty policy. Prepare regulatory disclosures and notices (if consumer). Determine valuation of collateral is acceptable to bank prior to closing. Take assignment of any building leases

103 Review Checklists (continued) Get up-to-date financial statements from all makers, co-makers and guarantors. Obtain authorizing documents for non-natural person borrowers (corporation, partnership, LLC) Confirm UCC-1s and/or mortgage/deed of trust are properly filed

104 Avoiding Mistake #10: Documenting Default Waivers

105 Documenting Default Waivers Defaults monetary = payments nonmonetary = covenants, representations, etc. Cure Periods None (principal payment, voluntary bankruptcy) 3 to 90 days for others Under some agreements Default becomes Event of Default after expiration of cure period

106 The Alternatives Bank waives default for specified period to allow borrower to come back into compliance Bank begins to negotiate workout, renewal, extension, etc. Bank begins collection process (i.e., sue, foreclose, etc.)

107 Legal Action upon Default Notice of Default Demand for Payment Notice of Intent to Accelerate Notice of Acceleration Abandonment of Acceleration Reinstatement

108 Elements of Waiver A right of the bank (i.e., to call default and accelerate) Knowledge of its existence - Right set forth in loan document - Bank aware of breach Bank engages in conduct inconsistent with claiming the right

109 Course of Dealing Effect of Failure to Take Action could constitute a waiver Waivers should be limited and documented Effect of Acceptance of Post-Default Payments

110

111

112

113 HOU:

Lenders Learn TM Chapter 3

Your State Association Presents Lenders Learn TM Chapter 3 Loan Documentation 101 - Part 1 The Basics Program Materials Use this document to follow along with the webinar. Please test your system before

Your State Association Presents Lenders Learn TM Chapter 3 Loan Documentation 101 - Part 1 The Basics Program Materials Use this document to follow along with the webinar. Please test your system before

Understanding Loan Documents

Your State Association Presents Lenders Learn TM Understanding Loan Documents Program Materials Use this document to follow along with the webinar. Please test your system before the broadcast. Be sure

Your State Association Presents Lenders Learn TM Understanding Loan Documents Program Materials Use this document to follow along with the webinar. Please test your system before the broadcast. Be sure

Basics of UCC Article 9 -- Your Guide to Security Interests

Basics of UCC Article 9 -- Your Guide to Security Interests June 28, 2018 Panelists: James C. Schulwolf (moderator), Shipman & Goodwin LLP, Hartford, CT R. Marshall Grodner, McGlinchey Stafford, Baton

Basics of UCC Article 9 -- Your Guide to Security Interests June 28, 2018 Panelists: James C. Schulwolf (moderator), Shipman & Goodwin LLP, Hartford, CT R. Marshall Grodner, McGlinchey Stafford, Baton

Personal Property Security Agreement

Personal Property Security Agreement (This form is intended for use in Washington State consumer transactions and for related personal property specified in Exhibit A; it is not intended for general use

Personal Property Security Agreement (This form is intended for use in Washington State consumer transactions and for related personal property specified in Exhibit A; it is not intended for general use

Secured Transactions Professor Keith A. Rowley William S. Boyd School of Law University of Nevada Las Vegas Fall Article 9 Priorities (Revised)

") Secured Transactions Professor Keith A. Rowley William S. Boyd School of Law University of Nevada Las Vegas Article 9 Priorities (Revised) I. The Concept: If the value of collateral is insufficient to

Secured Transactions Professor Keith A. Rowley William S. Boyd School of Law University of Nevada Las Vegas Article 9 Priorities (Revised) I. The Concept: If the value of collateral is insufficient to

FORMULARY INTERCREDITOR SUBORDINATION AGREEMENTS

FORMULARY INTERCREDITOR SUBORDINATION AGREEMENTS Materials Prepared By: R. Marshall Grodner 14 th Floor, One American Place Baton Rouge LA 70825 Telephone: (225) 383-9000 Facsimile: (225) 343-3076 E-mail:

FORMULARY INTERCREDITOR SUBORDINATION AGREEMENTS Materials Prepared By: R. Marshall Grodner 14 th Floor, One American Place Baton Rouge LA 70825 Telephone: (225) 383-9000 Facsimile: (225) 343-3076 E-mail:

Principles of Business Credit

Principles of Business Credit National Education Department 8840 Columbia 100 Parkway, Columbia, MD 21045-2158 Fax: 410-740-5574 Email: education_info@nacm.org Eighth Edition UCC ARTICLE 2 SALES OFFER

Principles of Business Credit National Education Department 8840 Columbia 100 Parkway, Columbia, MD 21045-2158 Fax: 410-740-5574 Email: education_info@nacm.org Eighth Edition UCC ARTICLE 2 SALES OFFER

Credit Enhancements: Beyond the Personal Guaranty. Thomas R. Fawkes and Brian J. Jackiw Goldstein & McClintock LLLP

Credit Enhancements: Beyond the Personal Guaranty Thomas R. Fawkes and Brian J. Jackiw Goldstein & McClintock LLLP Warning Signs of Impending Default Deviations in the manner or timing of counterparty

Credit Enhancements: Beyond the Personal Guaranty Thomas R. Fawkes and Brian J. Jackiw Goldstein & McClintock LLLP Warning Signs of Impending Default Deviations in the manner or timing of counterparty

Today s Presenter. The SBA Authorization Wisconsin SBA Lenders Conference May 19, SBA Loan Closing: Proper Documentation & Pitfalls

2016 Wisconsin SBA Lenders Conference May 19, 2016 SBA Loan Closing: Proper Documentation & Pitfalls Today s Presenter Nick Jellum, Anastasi Jellum P.A. 14985 60 th Street North, Stillwater, MN 55082 Phone:

2016 Wisconsin SBA Lenders Conference May 19, 2016 SBA Loan Closing: Proper Documentation & Pitfalls Today s Presenter Nick Jellum, Anastasi Jellum P.A. 14985 60 th Street North, Stillwater, MN 55082 Phone:

TITLE LOAN AGREEMENT

Borrower(s): Name: Address: Motor Vehicle: Year Color Make TITLE LOAN AGREEMENT Lender: Drivers License Number VIN Title Certificate Number Model Date of Loan ANNUAL PERCENTAGE RATE The cost of your credit

Borrower(s): Name: Address: Motor Vehicle: Year Color Make TITLE LOAN AGREEMENT Lender: Drivers License Number VIN Title Certificate Number Model Date of Loan ANNUAL PERCENTAGE RATE The cost of your credit

INTERCOMPANY SUBORDINATION AGREEMENT

10 The indebtedness evidenced by this instrument is subordinated to the prior payment in full of the Senior Indebtedness (as defined in the Intercreditor and Subordination Agreement hereinafter referred

10 The indebtedness evidenced by this instrument is subordinated to the prior payment in full of the Senior Indebtedness (as defined in the Intercreditor and Subordination Agreement hereinafter referred

Secured Transactions Professor Keith A. Rowley William S. Boyd School of Law University of Nevada Las Vegas Fall 2010

Secured Transactions Professor Keith A. Rowley William S. Boyd School of Law University of Nevada Las Vegas Perfecting the Security Interest (Final Cut) I. The Concept: Perfection determines the relative

Secured Transactions Professor Keith A. Rowley William S. Boyd School of Law University of Nevada Las Vegas Perfecting the Security Interest (Final Cut) I. The Concept: Perfection determines the relative

FIRST LIEN/SECOND LIEN INTERCREDITOR AGREEMENTS AND RELATED ISSUES

FIRST LIEN/SECOND LIEN INTERCREDITOR AGREEMENTS AND RELATED ISSUES An Introduction to the ABA Model Intercreditor Agreement Presented by: Michael S. Himmel, Chapman and Cutler LLP ABA Business Law Section

FIRST LIEN/SECOND LIEN INTERCREDITOR AGREEMENTS AND RELATED ISSUES An Introduction to the ABA Model Intercreditor Agreement Presented by: Michael S. Himmel, Chapman and Cutler LLP ABA Business Law Section

Secured Transactions Professor Keith A. Rowley William S. Boyd School of Law University of Nevada Las Vegas Fall 2011

Secured Transactions Professor Keith A. Rowley William S. Boyd School of Law University of Nevada Las Vegas Perfecting the Security Interest (Final Cut) I. The Concept: Perfection determines the relative

Secured Transactions Professor Keith A. Rowley William S. Boyd School of Law University of Nevada Las Vegas Perfecting the Security Interest (Final Cut) I. The Concept: Perfection determines the relative

PRACTICE CHECKLISTS MANUAL

LAW SOCIETY OF BRITISH COLUMBIA SECURITY AGREEMENT INTRODUCTION Purpose and currency of checklist. This checklist is designed to be used with the CLIENT IDENTIFICATION AND VERIFICATION PROCEDURE (A-1)

LAW SOCIETY OF BRITISH COLUMBIA SECURITY AGREEMENT INTRODUCTION Purpose and currency of checklist. This checklist is designed to be used with the CLIENT IDENTIFICATION AND VERIFICATION PROCEDURE (A-1)

ILLINOIS FINANCE AUTHORITY GUARANTEED LOAN PROGRAMS LENDER S AGREEMENT

ILLINOIS FINANCE AUTHORITY GUARANTEED LOAN PROGRAMS LENDER S AGREEMENT The purpose of this Lender s Agreement (the Agreement ) is to establish Lender as an approved participant in the guaranteed loan programs

ILLINOIS FINANCE AUTHORITY GUARANTEED LOAN PROGRAMS LENDER S AGREEMENT The purpose of this Lender s Agreement (the Agreement ) is to establish Lender as an approved participant in the guaranteed loan programs

Loan Enforcement Improving the Odds of Recovery. By Michael A. Campbell Polsinelli Shughart PC

Loan Enforcement Improving the Odds of Recovery By Michael A. Campbell Polsinelli Shughart PC Copyright 2009 Contents 1. Good Underwriting 2. Speed and its Effect on Recoveries 3. Pre-Enforcement Asset

Loan Enforcement Improving the Odds of Recovery By Michael A. Campbell Polsinelli Shughart PC Copyright 2009 Contents 1. Good Underwriting 2. Speed and its Effect on Recoveries 3. Pre-Enforcement Asset

Chapter VII SECURED TRANSACTIONS IN PERSONAL PROPERTY CONDENSED OUTLINE

Chapter VII SECURED TRANSACTIONS IN PERSONAL PROPERTY CONDENSED OUTLINE I. METHODS USED BEFORE UNIFORM COMMERCIAL CODE A. In General. B. Pledge. C. Trust Receipt. D. Chattel Mortgage. E. Conditional Sale.

Chapter VII SECURED TRANSACTIONS IN PERSONAL PROPERTY CONDENSED OUTLINE I. METHODS USED BEFORE UNIFORM COMMERCIAL CODE A. In General. B. Pledge. C. Trust Receipt. D. Chattel Mortgage. E. Conditional Sale.

How to Structure and Manage Secured Transactions Under New Article 9 By Richard R. Gleissner Finkel & Altman, L.L.C.

Page 1 of 18 1.D. How to Structure and Manage Secured Transactions under New Article 9. Structuring and managing secured transactions is complicated and cannot be adequately addressed in this brief introduction

Page 1 of 18 1.D. How to Structure and Manage Secured Transactions under New Article 9. Structuring and managing secured transactions is complicated and cannot be adequately addressed in this brief introduction

A good working knowledge of the UCC is critical to your auction business.

A good working knowledge of the UCC is critical to your auction business. The Uniform Commercial Code ( UCC ), in conjunction with state specific laws, and your contracts, govern the rights and obligations

A good working knowledge of the UCC is critical to your auction business. The Uniform Commercial Code ( UCC ), in conjunction with state specific laws, and your contracts, govern the rights and obligations

Security over Collateral. USA PENNSYLVANIA Eckert Seamans Cherin & Mellott, LLC

Security over Collateral USA PENNSYLVANIA Eckert Seamans Cherin & Mellott, LLC CONTACT INFORMATION Jay T. Blount Louis J. Moraytis Eckert Seamans Cherin & Mellott, LLC U.S. Steel Tower 600 Grant Street,

Security over Collateral USA PENNSYLVANIA Eckert Seamans Cherin & Mellott, LLC CONTACT INFORMATION Jay T. Blount Louis J. Moraytis Eckert Seamans Cherin & Mellott, LLC U.S. Steel Tower 600 Grant Street,

DEED OF TRUST AND ASSIGNMENT OF RENTS SAN FRANCISCO POLICE IN THE COMMUNITY LOAN PROGRAM (PIC)

") Free Recording Requested Pursuant to Government Code Section 27383 When recorded, mail to: Mayor's Office of Housing AND Community Development of the City and County of San Francisco One South Van Ness

Free Recording Requested Pursuant to Government Code Section 27383 When recorded, mail to: Mayor's Office of Housing AND Community Development of the City and County of San Francisco One South Van Ness

, Note (the Note ) made by Borrower in the amount of the Loan payable to the order of Lender.

made by Borrower in the amount of the Loan payable to the order of Lender.") , 201 Re:, Illinois (the Project ) Ladies and Gentlemen: We have served as [general] [special] [local] counsel to (A), a partnership ( Beneficiary ), the sole beneficiary of ( Trustee ), as Trustee under

, 201 Re:, Illinois (the Project ) Ladies and Gentlemen: We have served as [general] [special] [local] counsel to (A), a partnership ( Beneficiary ), the sole beneficiary of ( Trustee ), as Trustee under

TD DEED OF TRUST

58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 101 102 103 104 105 106 107 108 109 110 111 112 113 114 115 forfeiture

58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 101 102 103 104 105 106 107 108 109 110 111 112 113 114 115 forfeiture

Crash Course in Covenants and Collateral

Crash Course in Covenants and Collateral Robert J. Heinrich Emily L.M. Clubb May 19, 2016 Structuring Considerations Borrowers and guarantors Consider who ultimately gets the funds Cross-defaulting/guarantying/collateralization

Crash Course in Covenants and Collateral Robert J. Heinrich Emily L.M. Clubb May 19, 2016 Structuring Considerations Borrowers and guarantors Consider who ultimately gets the funds Cross-defaulting/guarantying/collateralization

Information & Instructions: Demand letter opportunity to cure and intent to accelerate the note

Information & Instructions: Demand letter opportunity to cure and intent to accelerate the note 1. The demand letter in the form that follows is used to advise the debtor that he or she is delinquent in

Information & Instructions: Demand letter opportunity to cure and intent to accelerate the note 1. The demand letter in the form that follows is used to advise the debtor that he or she is delinquent in

UCC Financing Statements

Rich Maxwell Woods Rogers PLC Greg Feldmann Skyline Capital Strategies, LLC UCC Financing Statements Perfection of Liens Filing in the Right Location Getting the Name of the Debtor Correct Standard search

Rich Maxwell Woods Rogers PLC Greg Feldmann Skyline Capital Strategies, LLC UCC Financing Statements Perfection of Liens Filing in the Right Location Getting the Name of the Debtor Correct Standard search

UCC Secured Transactions: Documenting and Perfecting Security Interests, Navigating Competing and Hidden Liens

Presenting a live 90-minute webinar with interactive Q&A UCC Secured Transactions: Documenting and Perfecting Security Interests, Navigating Competing and Hidden Liens WEDNESDAY, MARCH 9, 2016 1pm Eastern

Presenting a live 90-minute webinar with interactive Q&A UCC Secured Transactions: Documenting and Perfecting Security Interests, Navigating Competing and Hidden Liens WEDNESDAY, MARCH 9, 2016 1pm Eastern

United Auto Credit Securitization Trust Automobile receivables-backed notes series

Standard & Poor s Ratings Services 17g-7(N) Representations & Warranties Disclosure Report JAN. 14, 2016 SEC Rule 17g-7(N) SEC Rule 17g-7(N) requires an NRSRO, for any report accompanying a credit rating

Standard & Poor s Ratings Services 17g-7(N) Representations & Warranties Disclosure Report JAN. 14, 2016 SEC Rule 17g-7(N) SEC Rule 17g-7(N) requires an NRSRO, for any report accompanying a credit rating

SECURED TRANSACTIONS Spring Wednesday 8:10-10:00 am Hofstra Law School Koppelman Hall 0038N Adjunct Professor Marc L.

Spring 2015- ednesday 8:10-10:00 am Contact info: Moritt Hock & Hamroff LLP 400 Garden City Plaza Garden City, NY 11530 ebsite: www.moritthock.com mhamroff @moritthock.com Tel: (516) 873-2000 Fax: (516)

Spring 2015- ednesday 8:10-10:00 am Contact info: Moritt Hock & Hamroff LLP 400 Garden City Plaza Garden City, NY 11530 ebsite: www.moritthock.com mhamroff @moritthock.com Tel: (516) 873-2000 Fax: (516)

RENOVATION LOAN AGREEMENT

THIS IS A MODEL DOCUMENT FOR USE IN FANNIE MAE RENOVATION LOAN TRANSACTIONS. THIS FORM IS PROVIDED AS AN EXAMPLE AND HAS NOT BEEN EVALUATED FOR VALIDITY AND ENFORCEABILITY IN ANY JURISDICTION. LENDERS

THIS IS A MODEL DOCUMENT FOR USE IN FANNIE MAE RENOVATION LOAN TRANSACTIONS. THIS FORM IS PROVIDED AS AN EXAMPLE AND HAS NOT BEEN EVALUATED FOR VALIDITY AND ENFORCEABILITY IN ANY JURISDICTION. LENDERS

Loan Documentation Michael Gibson, Sheppard Mullin Richter & Hampton LLP Steve Park, Ballard Spahr LLP

EB-5 Attorney Workshop Loan Documentation Michael Gibson, Sheppard Mullin Richter & Hampton LLP Steve Park, Ballard Spahr LLP Moderated by: Jennifer Hermansky, Greenberg Traurig LLP Jennifer Hermansky

EB-5 Attorney Workshop Loan Documentation Michael Gibson, Sheppard Mullin Richter & Hampton LLP Steve Park, Ballard Spahr LLP Moderated by: Jennifer Hermansky, Greenberg Traurig LLP Jennifer Hermansky

Article 9 - Secured Transactions

Article 9 - Secured Transactions OBJECTIVES What and Why of the UCC Some history of the UCC Article 9 The nuts and bolts Purchase Money Security Interest (PMSI) Default, Enforcement & Bankruptcy WHY TEACH

Article 9 - Secured Transactions OBJECTIVES What and Why of the UCC Some history of the UCC Article 9 The nuts and bolts Purchase Money Security Interest (PMSI) Default, Enforcement & Bankruptcy WHY TEACH

American Land Title Association Revised 10/17/92 Section II-1 POLICY OF TITLE INSURANCE. Issued by BLANK TITLE INSURANCE COMPANY

POLICY OF TITLE INSURANCE Issued by BLANK TITLE INSURANCE COMPANY SUBJECT TO THE EXCLUSIONS FROM COVERAGE, THE EXCEPTIONS FROM COVERAGE CONTAINED IN SCHEDULE B AND THE CONDITIONS AND STIPULATIONS, BLANK

POLICY OF TITLE INSURANCE Issued by BLANK TITLE INSURANCE COMPANY SUBJECT TO THE EXCLUSIONS FROM COVERAGE, THE EXCEPTIONS FROM COVERAGE CONTAINED IN SCHEDULE B AND THE CONDITIONS AND STIPULATIONS, BLANK

BASIC SECURED LOAN DOCUMENTATION By Robin Russell CHAPTER 3

BASIC SECURED LOAN DOCUMENTATION By Robin Russell CHAPTER 3 I. INTRODUCTION... 1 Overview... 1 Purpose... 1 Use of Forms... 1 Checklist... 2 II. LOAN APPLICATIONS... 2 Overview... 2 Consumer Issues...

BASIC SECURED LOAN DOCUMENTATION By Robin Russell CHAPTER 3 I. INTRODUCTION... 1 Overview... 1 Purpose... 1 Use of Forms... 1 Checklist... 2 II. LOAN APPLICATIONS... 2 Overview... 2 Consumer Issues...

ASSET BASED LENDING IN CANADA CANADIAN PRIMER ON ASSET BASED FINANCING. based on ASSET BASED FINANCING: A TRANSACTIONAL GUIDE

ASSET BASED LENDING IN CANADA CANADIAN PRIMER ON ASSET BASED FINANCING based on ASSET BASED FINANCING: A TRANSACTIONAL GUIDE Alison M anzer Howard Ruda LexisNexis* TABLE OF CONTENTS Preface About thè Authors

ASSET BASED LENDING IN CANADA CANADIAN PRIMER ON ASSET BASED FINANCING based on ASSET BASED FINANCING: A TRANSACTIONAL GUIDE Alison M anzer Howard Ruda LexisNexis* TABLE OF CONTENTS Preface About thè Authors

NEGOTIABLE INSTRUMENTS. Common Law of Contracts: reasonable expectations

NEGOTIABLE INSTRUMENTS LESE Spring 2002 O'Hara 1 Common Law of Contracts: reasonable expectations Old Common Law all assignments and delegations violate the parties reasonable expectations. New Common

NEGOTIABLE INSTRUMENTS LESE Spring 2002 O'Hara 1 Common Law of Contracts: reasonable expectations Old Common Law all assignments and delegations violate the parties reasonable expectations. New Common

MINNESOTA REAL ESTATE FORECLOSURES: 21 COMMON QUESTIONS & ANSWERS

MINNESOTA REAL ESTATE FORECLOSURES: 21 COMMON QUESTIONS & ANSWERS Our Creditors Remedies attorneys answer the most asked questions from their clients. Practice Area: CREDITORS REMEDIES, BANKRUPTCY & WORK-OUT

MINNESOTA REAL ESTATE FORECLOSURES: 21 COMMON QUESTIONS & ANSWERS Our Creditors Remedies attorneys answer the most asked questions from their clients. Practice Area: CREDITORS REMEDIES, BANKRUPTCY & WORK-OUT

[FORM OF] INTERCREDITOR AGREEMENT. Dated as of [ ], Among. CITIBANK, N.A., as Representative with respect to the ABL Credit Agreement,

![[FORM OF] INTERCREDITOR AGREEMENT. Dated as of [ ], Among. CITIBANK, N.A., as Representative with respect to the ABL Credit Agreement,](/thumbs/80/80492541.jpg "[FORM OF] INTERCREDITOR AGREEMENT. Dated as of [ ], Among. CITIBANK, N.A., as Representative with respect to the ABL Credit Agreement,") DPW DRAFT 3/7/13 [FORM OF] INTERCREDITOR AGREEMENT Dated as of [ ], 2013 Among CITIBANK, N.A., as Representative with respect to the ABL Credit Agreement, WILMINGTON TRUST, NATIONAL ASSOCIATION, as Representative

DPW DRAFT 3/7/13 [FORM OF] INTERCREDITOR AGREEMENT Dated as of [ ], 2013 Among CITIBANK, N.A., as Representative with respect to the ABL Credit Agreement, WILMINGTON TRUST, NATIONAL ASSOCIATION, as Representative

DEED OF TRUST AND ASSIGNMENT OF RENTS FIRST RESPONDERS DOWNPAYMENT ASSISTANCE LOAN PROGRAM (FRDALP)

") Free Recording Requested Pursuant to Government Code Section 27383 When recorded, mail to: Mayor's Office of Housing and Community Development of the City and County of San Francisco 1 South Van Ness Avenue,

Free Recording Requested Pursuant to Government Code Section 27383 When recorded, mail to: Mayor's Office of Housing and Community Development of the City and County of San Francisco 1 South Van Ness Avenue,

INTERCREDITOR/ SUBORDINATION AGREEMENTS. R. Marshall Grodner McGlinchey Stafford

INTERCREDITOR/ SUBORDINATION AGREEMENTS R. Marshall Grodner McGlinchey Stafford mgrodner@mcglinchey.com INTRODUCTION Types of Subordination Types of Lien Subordination Players General Definition Issues

INTERCREDITOR/ SUBORDINATION AGREEMENTS R. Marshall Grodner McGlinchey Stafford mgrodner@mcglinchey.com INTRODUCTION Types of Subordination Types of Lien Subordination Players General Definition Issues

LIMITED LIABILITY COMPANY CODE (As adopted January 13, 2010) SUMMARY OF CONTENTS. 1. TABLE OF REVISIONS ii. 2. TABLE OF CONTENTS iii

SUMMARY OF CONTENTS. 1. TABLE OF REVISIONS ii. 2. TABLE OF CONTENTS iii") TITLE 11B TITLE 11B LIMITED LIABILITY COMPANY CODE (As adopted January 13, 2010) SUMMARY OF CONTENTS SECTION ARTICLE-PAGE 1. TABLE OF REVISIONS ii 2. TABLE OF CONTENTS iii 3. ARTICLE 1: GENERAL PROVISIONS

TITLE 11B TITLE 11B LIMITED LIABILITY COMPANY CODE (As adopted January 13, 2010) SUMMARY OF CONTENTS SECTION ARTICLE-PAGE 1. TABLE OF REVISIONS ii 2. TABLE OF CONTENTS iii 3. ARTICLE 1: GENERAL PROVISIONS

Lesson 12: Real Estate Financing 311

Real Estate Principles of Georgia 1 of 97 Lesson 12: Real Estate Financing 311 Economics of Real Estate Finance For a lender, a loan is an investment. Interest paid on loan is lender s return. Riskier

Real Estate Principles of Georgia 1 of 97 Lesson 12: Real Estate Financing 311 Economics of Real Estate Finance For a lender, a loan is an investment. Interest paid on loan is lender s return. Riskier

Mango Bay Properties & Investments dba Mango Bay Mortgage

WHOLESALE BROKER AGREEMENT This Wholesale Broker Agreement (the Agreement ) is entered into on this day of between Mango Bay Property and Investments Inc. dba Mango Bay Mortgage (MBM) and ( Broker ). RECITALS

WHOLESALE BROKER AGREEMENT This Wholesale Broker Agreement (the Agreement ) is entered into on this day of between Mango Bay Property and Investments Inc. dba Mango Bay Mortgage (MBM) and ( Broker ). RECITALS

Secured Transactions Law School Legends Professor Michael I. Spak

Secured Transactions Law School Legends Professor Michael I. Spak Introduction What Article 9 is NOT: 99.99% of all sales. E.g., I sell you my tie for $1 down and $1 a month for 9 months. You stop making

Secured Transactions Law School Legends Professor Michael I. Spak Introduction What Article 9 is NOT: 99.99% of all sales. E.g., I sell you my tie for $1 down and $1 a month for 9 months. You stop making

DOCUMENTING AND COLLECTING AGRICULTURAL LOANS By Tom Flynn Brick Gentry, P.C Westown Parkway, Suite 100 West Des Moines, IA Phone:

DOCUMENTING AND COLLECTING AGRICULTURAL LOANS By Tom Flynn Brick Gentry, P.C. 6701 Westown Parkway, Suite 100 West Des Moines, IA 50266 Phone: 515-271-5915 tom.flynn@brickgentrylaw.com Prepared for Iowa

DOCUMENTING AND COLLECTING AGRICULTURAL LOANS By Tom Flynn Brick Gentry, P.C. 6701 Westown Parkway, Suite 100 West Des Moines, IA 50266 Phone: 515-271-5915 tom.flynn@brickgentrylaw.com Prepared for Iowa

LIENS OUTSIDE ARTICLES 9 AND 8 OF THE UNIFORM COMMERCIAL CODE

Conflicting security interests in property has been a major source of litigation in the lending industry since common law times. With respect to real estate, early recording statutes went a long way towards

Conflicting security interests in property has been a major source of litigation in the lending industry since common law times. With respect to real estate, early recording statutes went a long way towards

Crash Course in Covenants and Collateral

Crash Course in Covenants and Collateral Robert J. Heinrich Emily L.M. Clubb May 19, 2016 Structuring Considerations Borrowers and guarantors Consider who ultimately gets the funds Cross-defaulting/guarantying/collateralization

Crash Course in Covenants and Collateral Robert J. Heinrich Emily L.M. Clubb May 19, 2016 Structuring Considerations Borrowers and guarantors Consider who ultimately gets the funds Cross-defaulting/guarantying/collateralization

The Right of Setoff- What Does a Banker Need to Know?

The Right of Setoff- What Does a Banker Need to Know? By Terri D. Thomas, JD tthomas@ksbankers.com Presented on February 10, 2016 10:00 a.m.-12:00 p.m. CST The information contained in this material and

The Right of Setoff- What Does a Banker Need to Know? By Terri D. Thomas, JD tthomas@ksbankers.com Presented on February 10, 2016 10:00 a.m.-12:00 p.m. CST The information contained in this material and

DEED OF TRUST (Assumable Not Due on Transfer)

") 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 The printed portions of this form, except

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 The printed portions of this form, except

Chapter 15: Creditor - Debtor Relations and Bankruptcy

Chapter 15: Creditor - Debtor Relations and Bankruptcy Copyright 2009 South-Western Legal Studies in Business, a Copyright part of South-Western 2009 South-Western Cengage Legal Learning. Studies Business,

Chapter 15: Creditor - Debtor Relations and Bankruptcy Copyright 2009 South-Western Legal Studies in Business, a Copyright part of South-Western 2009 South-Western Cengage Legal Learning. Studies Business,

Commercial Lender Policy

Commercial Lender Policy Commercial Lender Policy Stewart Title Limited s Commercial Lender Policy will insure you subject to the terms and conditions of the Policy against your actual loss resulting from

Commercial Lender Policy Commercial Lender Policy Stewart Title Limited s Commercial Lender Policy will insure you subject to the terms and conditions of the Policy against your actual loss resulting from

Presented by: Terri D. Thomas, JD February 10, 2016

Presented by: Terri D. Thomas, JD February 10, 2016 Setoff is the act of deducting an amount owed by one party to another from an amount that is due to be paid from the other party to the first party;

Presented by: Terri D. Thomas, JD February 10, 2016 Setoff is the act of deducting an amount owed by one party to another from an amount that is due to be paid from the other party to the first party;

UNDERWRITING REQUIREMENTS

Texas Business Organizations Entities and Sole Proprietorships Presented by: Eric McNeese Underwriting Counsel National Investors Title Insurance Company 1 SOLE PROPRIETORSHIP Individual person, not an

Texas Business Organizations Entities and Sole Proprietorships Presented by: Eric McNeese Underwriting Counsel National Investors Title Insurance Company 1 SOLE PROPRIETORSHIP Individual person, not an

Your State Association Presents. Program Materials

Your State Association Presents Lenders Learn TM Chapter 10 Agricultural Lending Program Materials Use this document to follow along with the webinar. Please test your system before the broadcast. Be sure

Your State Association Presents Lenders Learn TM Chapter 10 Agricultural Lending Program Materials Use this document to follow along with the webinar. Please test your system before the broadcast. Be sure

6 Things Every Accounts Receivable Buyer Should Know

Portfolio Media. Inc. 111 West 19 th Street, 5th Floor New York, NY 10011 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com 6 Things Every Accounts Receivable Buyer

Portfolio Media. Inc. 111 West 19 th Street, 5th Floor New York, NY 10011 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com 6 Things Every Accounts Receivable Buyer

American Land Title Association Adopted OWNER S POLICY OF TITLE INSURANCE Issued by [TITLE INSURANCE COMPANY]

![American Land Title Association Adopted OWNER S POLICY OF TITLE INSURANCE Issued by [TITLE INSURANCE COMPANY]](/thumbs/77/76699165.jpg "American Land Title Association Adopted OWNER S POLICY OF TITLE INSURANCE Issued by [TITLE INSURANCE COMPANY]") OWNER S POLICY OF TITLE INSURANCE Issued by [TITLE INSURANCE COMPANY] Any notice of claim and any other notice or statement in writing required to be given to the Company under this Policy must be given

OWNER S POLICY OF TITLE INSURANCE Issued by [TITLE INSURANCE COMPANY] Any notice of claim and any other notice or statement in writing required to be given to the Company under this Policy must be given

RECEIVABLES SALE AND CONTRIBUTION AGREEMENT. between DISCOVER BANK. and DISCOVER FUNDING LLC

EXECUTION VERSION RECEIVABLES SALE AND CONTRIBUTION AGREEMENT between DISCOVER BANK and DISCOVER FUNDING LLC Dated as of December 22, 2015 TABLE OF CONTENTS Page ARTICLE 1. DEFINITIONS... 1 Section 1.1

EXECUTION VERSION RECEIVABLES SALE AND CONTRIBUTION AGREEMENT between DISCOVER BANK and DISCOVER FUNDING LLC Dated as of December 22, 2015 TABLE OF CONTENTS Page ARTICLE 1. DEFINITIONS... 1 Section 1.1

Appendix D Opinion of CDC Counsel

Appendix D Opinion of CDC Counsel Read this first! This appendix contains the standardized text for the Opinion of CDC Counsel required by the Authorization. All paragraphs are mandatory except when noted

Appendix D Opinion of CDC Counsel Read this first! This appendix contains the standardized text for the Opinion of CDC Counsel required by the Authorization. All paragraphs are mandatory except when noted

I. Examinations. Re: Loan from X Bank (the "Lender" ) to Y Corp. (the "Borrower" ) pursuant to a Credit Agreement (the "Credit Agreement" ) dated [0]

![I. Examinations. Re: Loan from X Bank (the Lender ) to Y Corp. (the Borrower ) pursuant to a Credit Agreement (the Credit Agreement ) dated [0]](/thumbs/76/73463614.jpg "I. Examinations. Re: Loan from X Bank (the Lender ) to Y Corp. (the Borrower ) pursuant to a Credit Agreement (the Credit Agreement ) dated [0]") LAW SOCIETY OF UPPER CANADA Continuing Professional Development 3" Annual Business Law Summit May 15, 2013 Prepared for educational uses only. This is a very basic financing opinion under the Ontario PPSA.

LAW SOCIETY OF UPPER CANADA Continuing Professional Development 3" Annual Business Law Summit May 15, 2013 Prepared for educational uses only. This is a very basic financing opinion under the Ontario PPSA.

BA MASTER CREDIT CARD TRUST II SECOND AMENDED AND RESTATED RECEIVABLES PURCHASE AGREEMENT. among BANK OF AMERICA, NATIONAL ASSOCIATION,

EXECUTION COPY BA MASTER CREDIT CARD TRUST II SECOND AMENDED AND RESTATED RECEIVABLES PURCHASE AGREEMENT among BANK OF AMERICA, NATIONAL ASSOCIATION, BANC OF AMERICA CONSUMER CARD SERVICES, LLC and BA

EXECUTION COPY BA MASTER CREDIT CARD TRUST II SECOND AMENDED AND RESTATED RECEIVABLES PURCHASE AGREEMENT among BANK OF AMERICA, NATIONAL ASSOCIATION, BANC OF AMERICA CONSUMER CARD SERVICES, LLC and BA

WEFUNDER, INC. Convertible Promissory Note [DATE], 2012

![WEFUNDER, INC. Convertible Promissory Note [DATE], 2012](/thumbs/74/70714656.jpg "WEFUNDER, INC. Convertible Promissory Note [DATE], 2012") THIS CONVERTIBLE PROMISSORY NOTE AND THE SECURITIES ISSUABLE UPON CONVERSION HEREOF HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, OR ANY STATE SECURITIES LAWS. THESE SECURITIES

THIS CONVERTIBLE PROMISSORY NOTE AND THE SECURITIES ISSUABLE UPON CONVERSION HEREOF HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, OR ANY STATE SECURITIES LAWS. THESE SECURITIES

BUSINESS ENTITIES: Schedule C Requirements

BUSINESS ENTITIES: Schedule C Requirements 2015 Texas Land Title Institute Stephen R. Streiff Texas State Counsel Old Republic National Title Insurance Company Houston, TX Stephen R. Streiff is the Texas

BUSINESS ENTITIES: Schedule C Requirements 2015 Texas Land Title Institute Stephen R. Streiff Texas State Counsel Old Republic National Title Insurance Company Houston, TX Stephen R. Streiff is the Texas

Monday, June 19, 2017 Ag Law Rooms: Ag Lien Update: Loan Workout Concerns and Lender Liability Issues in Today s Ag Economy 3:15 p.m.

Monday, June 19, 2017 Ag Law Rooms: 312-313 Ag Lien Update: Loan Workout Concerns and Lender Liability Issues in Today s Ag Economy 3:15 p.m. 4:15 p.m. Presented by Robert Hartwig Legal Counsel Iowa Bankers

Monday, June 19, 2017 Ag Law Rooms: 312-313 Ag Lien Update: Loan Workout Concerns and Lender Liability Issues in Today s Ag Economy 3:15 p.m. 4:15 p.m. Presented by Robert Hartwig Legal Counsel Iowa Bankers

Case JAD Doc 22 Filed 09/30/16 Entered 09/30/16 16:50:46 Desc Main Document Page 1 of 11

Case 16-23458-JAD Doc 22 Filed 09/30/16 Entered 09/30/16 16:50:46 Desc Main Document Page 1 of 11 IN THE UNITED STATES BANKRUPTCY COURT FOR THE WESTERN DISTRICT OF PENNSYLVANIA IN RE: ) Case No. 16-23458-JAD

Case 16-23458-JAD Doc 22 Filed 09/30/16 Entered 09/30/16 16:50:46 Desc Main Document Page 1 of 11 IN THE UNITED STATES BANKRUPTCY COURT FOR THE WESTERN DISTRICT OF PENNSYLVANIA IN RE: ) Case No. 16-23458-JAD

DEED OF TRUST. a resident of the Commonwealth of Virginia, whose full residence or business address is. , and

"THIS DEED OF TRUST SHALL NOT WITHOUT THE CONSENT OF THE SECURED PARTY HEREUNDER BE SUBORDINATED UPON THE REFINANCING OF ANY PRIOR MORTGAGE." Return To: Tax Map Reference #: Prepared by: RPC/Parcel ID

"THIS DEED OF TRUST SHALL NOT WITHOUT THE CONSENT OF THE SECURED PARTY HEREUNDER BE SUBORDINATED UPON THE REFINANCING OF ANY PRIOR MORTGAGE." Return To: Tax Map Reference #: Prepared by: RPC/Parcel ID

CO-OPERATIVE APARTMENT LOAN SECURITY AGREEMENT

CO-OPERATIVE APARTMENT LOAN SECURITY AGREEMENT THIS SECURITY AGREEMENT made the day of, 20, between and, residing at (referred to in this Security Agreement as the Borrower ) and (referred to in this Security

CO-OPERATIVE APARTMENT LOAN SECURITY AGREEMENT THIS SECURITY AGREEMENT made the day of, 20, between and, residing at (referred to in this Security Agreement as the Borrower ) and (referred to in this Security

Walter Energy, Inc. $50,000,000 Debtor-in-Possession Term Loan Facility Summary of Terms and Conditions

Walter Energy, Inc. $50,000,000 Debtor-in-Possession Term Loan Facility Summary of Terms and Conditions Borrower: Guarantors: Backstop Parties: DIP Agent: DIP Lenders: Walter Energy, Inc. (the Borrower

Walter Energy, Inc. $50,000,000 Debtor-in-Possession Term Loan Facility Summary of Terms and Conditions Borrower: Guarantors: Backstop Parties: DIP Agent: DIP Lenders: Walter Energy, Inc. (the Borrower

4. equipment: catch all ; goods other than inventory, farm products, and consumer goods; used or bought for use primarily in business

Secured Transactions Prof. Payne Chapter 1. Goods: all things that are movable when a security interest attaches 1. consumer goods: goods that are used or bought for use primarily for personal, family

Secured Transactions Prof. Payne Chapter 1. Goods: all things that are movable when a security interest attaches 1. consumer goods: goods that are used or bought for use primarily for personal, family

NC General Statutes - Chapter 53C Article 6 1

Article 6. Bank Operations. 53C-6-1. Loans and extensions of credit. (a) A bank may make a loan or extension of credit secured by the pledge of its own shares or the shares of its holding company, provided:

Article 6. Bank Operations. 53C-6-1. Loans and extensions of credit. (a) A bank may make a loan or extension of credit secured by the pledge of its own shares or the shares of its holding company, provided:

FORBEARANCE AGREEMENTS. By Gordon L. Gerson, Esq. May 2009

GLF BEST PRACTICE RECOMMENDATIONS FORBEARANCE AGREEMENTS By Gordon L. Gerson, Esq. May 2009 Forbearance agreements in commercial real estate lending are utilized by lenders and borrowers who mutually agree

GLF BEST PRACTICE RECOMMENDATIONS FORBEARANCE AGREEMENTS By Gordon L. Gerson, Esq. May 2009 Forbearance agreements in commercial real estate lending are utilized by lenders and borrowers who mutually agree

RETAIL INSTALLMENT CONTRACT AND SECURITY AGREEMENT MOTOR VEHICLE. Amount Financed The amount of credit provided to you or on your behalf.

RETAIL INSTALLMENT CONTRACT AND SECURITY AGREEMENT MOTOR VEHICLE Contract Number: Date: Buyer Name and Address (Street Address) (City, State and Zip Code) Co-Buyer Name and Address (Street Address) (City,

RETAIL INSTALLMENT CONTRACT AND SECURITY AGREEMENT MOTOR VEHICLE Contract Number: Date: Buyer Name and Address (Street Address) (City, State and Zip Code) Co-Buyer Name and Address (Street Address) (City,

Problem 1. Assignment 11 Priority: Secured Party v. Buyer. Article 9 s Baseline Priority Rule. Problem 1

Assignment 11 Priority: Secured Party v. Buyer Reference: Understanding Secured Transactions Ch. 11 Problem 1 Burnside buys a used tractor from Henson for $6,000 (assume Henson acquired and used it in

Assignment 11 Priority: Secured Party v. Buyer Reference: Understanding Secured Transactions Ch. 11 Problem 1 Burnside buys a used tractor from Henson for $6,000 (assume Henson acquired and used it in

Consumer General Collateral Mortgage Standard Charge Terms Land Registration Reform Act

Page 1 of 20 Consumer General Collateral Mortgage Standard Charge Terms Land Registration Reform Act Filed By: Canadian Imperial Bank of Commerce Filing Number: 200816 Filing Date: August 8, 2008 The following

Page 1 of 20 Consumer General Collateral Mortgage Standard Charge Terms Land Registration Reform Act Filed By: Canadian Imperial Bank of Commerce Filing Number: 200816 Filing Date: August 8, 2008 The following

Mezzanine Financing Endorsements to Title and UCC Insurance Policies

Mezzanine Financing Endorsements to Title and UCC Insurance Policies By John C. Murray 2003 As a result of the increased securitization of real estate and the packaging of pools of loans for sale into

Mezzanine Financing Endorsements to Title and UCC Insurance Policies By John C. Murray 2003 As a result of the increased securitization of real estate and the packaging of pools of loans for sale into

MICHIGAN REVOCABLE LIVING TRUST OF

MICHIGAN REVOCABLE LIVING TRUST OF This Revocable Living Trust dated day of, 20, by and between: GRANTOR with a mailing address of (referred to as the Grantor, ) and TRUSTEE with a mailing address of (referred

MICHIGAN REVOCABLE LIVING TRUST OF This Revocable Living Trust dated day of, 20, by and between: GRANTOR with a mailing address of (referred to as the Grantor, ) and TRUSTEE with a mailing address of (referred

Chapter 14 Real Estate Financing: Principles

Chapter 14 Real Estate Financing: Principles OUTLINE: I. Mortgage Law A. A mortgage is a voluntary lien on real estate, given by the mortgagor to secure the payment of a debt or the performance of an obligation

Chapter 14 Real Estate Financing: Principles OUTLINE: I. Mortgage Law A. A mortgage is a voluntary lien on real estate, given by the mortgagor to secure the payment of a debt or the performance of an obligation

Residential Mortgage. Mortgage Memorandum Memorandum number 2007/4241

Residential Mortgage These are the terms and conditions which form part of your mortgage. As this is an important document, please store it in a safe place. Mortgage Memorandum 0100 Memorandum number 2007/4241

Residential Mortgage These are the terms and conditions which form part of your mortgage. As this is an important document, please store it in a safe place. Mortgage Memorandum 0100 Memorandum number 2007/4241

SAMPLE LYING AND BEING LOCATED IN THE CITY OF WINTER PARK, COUNTY OF ORANGE, STATE OF FLORIDA; ALL THAT CERTAIN PARCEL OR TRACT OF LAND KNOWN AS:

1111111111111111111111111111111111111111 Recording reql,lested by and when recl>rded return to: 21 50 Cabot Blvd. West Langhorne, PA 19047 0 Attn: Group 9, Inc. This Mortgage was prepared by: Mary Picard

1111111111111111111111111111111111111111 Recording reql,lested by and when recl>rded return to: 21 50 Cabot Blvd. West Langhorne, PA 19047 0 Attn: Group 9, Inc. This Mortgage was prepared by: Mary Picard

Problem 1. Assignment 11 Priority: Secured Party v. Buyer. Article 9 s Baseline Priority Rule. Problem 1

Assignment 11 Priority: Secured Party v. Buyer Reference: Understanding Secured Transactions Ch. 11 Problem 1 Burnside buys a used tractor from Henson for $6,000 (assume Henson acquired and used it in

Assignment 11 Priority: Secured Party v. Buyer Reference: Understanding Secured Transactions Ch. 11 Problem 1 Burnside buys a used tractor from Henson for $6,000 (assume Henson acquired and used it in

Name of Individual or Legal Entity Responsible for Payment. City State Zip City State Zip. Phone Number Fax Number Phone Number Fax Number

2801 Horace Shepard Drive Dothan, AL 36303 1. Account Information APPLICATION FOR NEW ACCOUNT The following is an application for credit with ONCOLOGY SUPPLY, also known as creditor within the general

2801 Horace Shepard Drive Dothan, AL 36303 1. Account Information APPLICATION FOR NEW ACCOUNT The following is an application for credit with ONCOLOGY SUPPLY, also known as creditor within the general

DEED OF TRUST WITH REQUEST FOR NOTICE

RECORDING REQUESTED BY: When Recorded Mail Document To: APN: SPACE ABOVE THIS LINE IS FOR RECORDER S USE DEED OF TRUST WITH REQUEST FOR NOTICE HIS DEED OF TRUST is made this day of among the Trustor, (herein

RECORDING REQUESTED BY: When Recorded Mail Document To: APN: SPACE ABOVE THIS LINE IS FOR RECORDER S USE DEED OF TRUST WITH REQUEST FOR NOTICE HIS DEED OF TRUST is made this day of among the Trustor, (herein

SECURITY AGREEMENT AND CHATTEL MORTGAGE

LW Draft 7/13/18 SECURITY AGREEMENT AND CHATTEL MORTGAGE This SECURITY AGREEMENT AND CHATTEL MORTGAGE, dated as of July [ ], 2018 (as amended, supplemented or otherwise modified from time to time in accordance

LW Draft 7/13/18 SECURITY AGREEMENT AND CHATTEL MORTGAGE This SECURITY AGREEMENT AND CHATTEL MORTGAGE, dated as of July [ ], 2018 (as amended, supplemented or otherwise modified from time to time in accordance

Consumer General Collateral Mortgage Standard Mortgage Terms

Consumer General Collateral Mortgage Standard Mortgage Terms Filed By: Canadian Imperial Bank of Commerce Filing Number: MT080113 Filing Date: August 1, 2008 The following set of standard mortgage terms

Consumer General Collateral Mortgage Standard Mortgage Terms Filed By: Canadian Imperial Bank of Commerce Filing Number: MT080113 Filing Date: August 1, 2008 The following set of standard mortgage terms

Case 4:11-cv Document 99 Filed in TXSD on 09/10/12 Page 1 of 17

Case 4:11-cv-02830 Document 99 Filed in TXSD on 09/10/12 Page 1 of 17 IN THE UNITED STATES DISTRICT COURT FOR THE SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION SECURITIES AND EXCHANGE COMMISSION, PLAINTIFF,

Case 4:11-cv-02830 Document 99 Filed in TXSD on 09/10/12 Page 1 of 17 IN THE UNITED STATES DISTRICT COURT FOR THE SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION SECURITIES AND EXCHANGE COMMISSION, PLAINTIFF,

Page 1 of 26 EXHIBIT 10.1 EXECUTION COPY ASSET PURCHASE AND FORWARD FLOW AGREEMENT AMONG JEFFERSON CAPITAL SYSTEMS, LLC, SELLER, MIDLAND FUNDING LLC, BUYER AND ENCORE CAPITAL GROUP, INC. ASSET PURCHASE

Page 1 of 26 EXHIBIT 10.1 EXECUTION COPY ASSET PURCHASE AND FORWARD FLOW AGREEMENT AMONG JEFFERSON CAPITAL SYSTEMS, LLC, SELLER, MIDLAND FUNDING LLC, BUYER AND ENCORE CAPITAL GROUP, INC. ASSET PURCHASE

SUBORDINATED NOTE PURCHASE AGREEMENT 1. DESCRIPTION OF SUBORDINATED NOTE AND COMMITMENT

SUBORDINATED NOTE PURCHASE AGREEMENT This SUBORDINATED NOTE PURCHASE AGREEMENT (this Agreement ), dated as of the date it is electronically signed, is by and between Matchbox Food Group, LLC, a District

SUBORDINATED NOTE PURCHASE AGREEMENT This SUBORDINATED NOTE PURCHASE AGREEMENT (this Agreement ), dated as of the date it is electronically signed, is by and between Matchbox Food Group, LLC, a District

Registration Number: Date: February 4, 2016

Filed By: Canadian Imperial Bank of Commerce 6213-2016/03 Page 1 of 17 Consumer General Collateral Mortgage Standard Mortgage Terms Registration Number: 161036262 Date: February 4, 2016 The following set

Filed By: Canadian Imperial Bank of Commerce 6213-2016/03 Page 1 of 17 Consumer General Collateral Mortgage Standard Mortgage Terms Registration Number: 161036262 Date: February 4, 2016 The following set

CUSTOMER CREDIT APPLICATION

CREDIT LIMIT REQUEST: $ CUSTOMER CREDIT APPLICATION Date: Customer warrants that the following information is accurate and complete: (Attach additional sheets as needed) Name of Customer (Legal Name) Trade

CREDIT LIMIT REQUEST: $ CUSTOMER CREDIT APPLICATION Date: Customer warrants that the following information is accurate and complete: (Attach additional sheets as needed) Name of Customer (Legal Name) Trade

The following set of additional terms and conditions form part of Canadian Imperial Bank of Commerce. Contents

Page 1 of 23 Consumer General Collateral Mortgage Additional Terms and Conditions The following set of additional terms and conditions form part of Canadian Imperial Bank of Commerce. Contents 1. Definitions...

Page 1 of 23 Consumer General Collateral Mortgage Additional Terms and Conditions The following set of additional terms and conditions form part of Canadian Imperial Bank of Commerce. Contents 1. Definitions...

and Waivers After Default Crafting Forbearance Agreements That Minimize Lender Liability and Bankruptcy Risks

Presenting a live 60 minute webinar with interactive Q&A Loan Forbearance Options and Waivers After Default Crafting Forbearance Agreements That Minimize Lender Liability and Bankruptcy Risks THURSDAY,

Presenting a live 60 minute webinar with interactive Q&A Loan Forbearance Options and Waivers After Default Crafting Forbearance Agreements That Minimize Lender Liability and Bankruptcy Risks THURSDAY,

Deed of Trust. a resident of the Commonwealth of Virginia, whose full residence or business address is

"THIS DEED OF TRUST SHALL NOT, WITHOUT THE CONSENT OF THE SECURED PARTY HEREUNDER, BE SUBORDINATED UPON THE REFINANCING OF ANY PRIOR MORTGAGE." Return To: Tax Map Reference #: RPC/Parcel ID #: Prepared

"THIS DEED OF TRUST SHALL NOT, WITHOUT THE CONSENT OF THE SECURED PARTY HEREUNDER, BE SUBORDINATED UPON THE REFINANCING OF ANY PRIOR MORTGAGE." Return To: Tax Map Reference #: RPC/Parcel ID #: Prepared

FILED: NEW YORK COUNTY CLERK 09/10/2013 INDEX NO /2012 NYSCEF DOC. NO. 42 RECEIVED NYSCEF: 09/10/2013. Exhibit 10

FILED: NEW YORK COUNTY CLERK 0 INDEX NO. 654314/2012 NYSCEF DOC. NO. 42 RECEIVED NYSCEF: 0 Exhibit 10 Page 1 of 107 EX-10.12 5 dex1012.htm 2ND AMENDED & RESTATED OPERATING AGREEMENT Exhibit 10.12 OPERATING

FILED: NEW YORK COUNTY CLERK 0 INDEX NO. 654314/2012 NYSCEF DOC. NO. 42 RECEIVED NYSCEF: 0 Exhibit 10 Page 1 of 107 EX-10.12 5 dex1012.htm 2ND AMENDED & RESTATED OPERATING AGREEMENT Exhibit 10.12 OPERATING

REVOLVING CREDIT MORTGAGE

REVOLVING CREDIT MORTGAGE WHEN RECORDED, MAIL TO: 1 2 3 PARCEL ID NUMBER: 4 SPACE ABOVE THIS LINE FOR RECORDER'S USE THIS MORTGAGE CONTAINS A DUE-ON-SALE PROVISION AND SECURES INDEBTEDNESS UNDER A CREDIT

REVOLVING CREDIT MORTGAGE WHEN RECORDED, MAIL TO: 1 2 3 PARCEL ID NUMBER: 4 SPACE ABOVE THIS LINE FOR RECORDER'S USE THIS MORTGAGE CONTAINS A DUE-ON-SALE PROVISION AND SECURES INDEBTEDNESS UNDER A CREDIT

CE & CLE FAQs are available under the Texas TIPS tab at

CE & CLE FAQs are available under the Texas TIPS tab at www.stewart.com/texas ATTORNEY INFORMATION Because of opinions expressed by the Texas Department of Insurance (TDI) concerning rebates, legal credit

CE & CLE FAQs are available under the Texas TIPS tab at www.stewart.com/texas ATTORNEY INFORMATION Because of opinions expressed by the Texas Department of Insurance (TDI) concerning rebates, legal credit

Assignment 32 Secured Creditors Against Secured Creditors: The Basics. Problem Problem 32.1: Bank 1 vs. Bank 2