EPF WITHDRAWALS FOR HOUSING USE

|

|

|

- Wesley McCoy

- 5 years ago

- Views:

Transcription

1 Guidelines

2 EPF WITHDRAWALS FOR HOUSING USE For further information, please refer to

3 a) EPF WITHDRAWALS FOR PURCHASING A HOUSE / BUILD A HOUSE Description This withdrawal is used to partially finance the purchase of a house (eligible for the first and second house). However, withdrawal for purchasing the second house is only allowed after the first house is sold or disposal of ownership of property has taken place (proof of sale of the first house must be produced). After making this withdrawal, you are eligible to withdraw your savings to reduce / redeem the housing loan for the same house once a year. You must also have minimum RM500 savings in your Account II. You are not eligible to withdraw for the purpose of:- Buy a land or a house lot only Renovate, repair or do additional work to the existing house Ownership of property is not via sale and purchase transaction Have taken an overdraft loan Buy a third house Buy a house abroad Amount Eligible to Withdraw You can withdraw your savings (account II) based on the following, whichever is lower but not less than RM500: Withdrawing via Individual Purchase The difference between the price of the house and the housing loan with an additional 10% of the price of the house; OR All balance available in Account II Withdrawing via Joint Purchase with Spouse, Family Members or Other Individuals The difference between the price of the house and the housing loan with an additional 10% of the price of the house; OR All balance available in Account II of all applicants subject to the maximum eligible amount as stated above. If you obtained a full housing loan (100%), you are eligible to withdraw as much as 10% of the price of the house OR All balance available in Account II You are allowed to apply only if you have signed the Sale and Purchase Agreement in not more than 3 years from the application date.

4 b) EPF WITHDRAWALS TO REDUCE / REDEEM HOUSING LOAN Description This withdrawal is used to reduce or redeem the housing balance with the financial institution approved by the EPF for the purchase or construction of a house. Withdrawal application can be made once a year from the date of last housing withdrawal. You must also have minimum RM500 savings in your Account II. You are not eligible to withdraw for the purpose of:- Renovate, repair or carry additional work to the existing house or for personal purposes Have taken an overdraft loan Have take a loan from an individual Wish to reduce / redeem the loan balance of your third house Wish to reduce / redeem the loan balance for a house you bought overseas The original housing loan balance is fully settled Amount Eligible to Withdraw You can withdraw your savings (account II) based on the following, whichever is lower but not less than RM500: Withdrawing via Individual / Assisting Spouse Total balance of housing loan; OR All savings in Account II Withdrawing via Joint Withdrawal with Spouse / Family Members / other Individuals Total balance of housing loan; OR All savings in Account II of all applicants subject to the total balance of housing loan. You can choose to determine the amount you wish to withdraw from your savings in Account II, subject to the maximum amount you are entitled to withdrawal by completing "Surat Akujanji Pilihan Amaun Pengeluaran".

5 c) HOUSING LOAN MONTHLY INSTALMENT WITHDRAWAL Description Withdrawal is used to pay housing loan monthly instalments taken for the purpose of buying or building a house. This withdrawal is an additional to the existing withdrawal, which is withdrawal to reduce / redeem housing loan. The maximum age allowed is 55 years and must also have minimum RM600 savings in your Account II. You can withdraw your savings (account II) based on the following: Amount Eligible to Withdraw Withdrawing via Individual / Assisting Spouse Total balance of housing loan; OR All savings in Account II. (Whichever is lower but subject to the minimum monthly payment of RM for the minimum period of 6 months and the maximum monthly payment does not exceed the total of monthly loan instalments) Withdrawing via Joint Withdrawal with Spouse / Family Members / other Individuals Total balance of housing loan; OR All savings in Account II of all applicants subject to the housing loan balance (Whichever is lower but subject to the minimum monthly payment of RM for the minimum period of 6 months and the maximum monthly payment of the borrowers does not exceed the total of monthly loan instalments) The amount withdrawn from Account II will be set aside in a special account and the monthly payments will be made out from this account. The amount set aside in the special account will be paid dividend and will be credited into Account II when dividend is declared in the following year.

6 d) FLEXIBLE HOUSING WITHDRAWAL Objective The Flexible Housing Withdrawal is a process to ring fence or set aside a part of savings in member s Account II to the Flexible Housing Withdrawal Account to enable the member to obtain a higher housing loan amount to purchase or build a house. This concept is to utilise the current and future EPF s saving or contribution value in consideration of providing loan by the Financial Institution. Based on this concept, the monthly contribution to the EPF is considered as an income. Therefore, the member can obtain a higher loan amount since the credit assessment on the net income also take the EPF contribution into consideration (employee and employer s share). As a result, the member can purchase or build a house with a higher price since this would enable them to obtain a higher loan to finance the purchase or building a house. You are not eligible to withdraw for the purpose of:- Buying a land or house lot only Renovate, repair / additional works to the existing house Purchasing/ building a house overseas Has a loan in the form of overdraft or the purpose of refinancing Ring Fencing and Transfer Amount Application amount must not be more than the Housing Loan Amount. Application to transfer existing savings in account II can be made as follows: Transfer of existing savings from Account II and monthly transfer (according to the fixed amount applied by the member) Monthly transfer (according to the fixed amount applied by the member) only. The monthly fixed transfer amount cannot be changed and will remain according to the amount selected during application.

7 THE ACQUISITION OF PROPERTIES BY FOREIGN INTERESTS This Guideline is to clarify the procedure on the acquisition of properties. Foreign interest means any interest, associated group of interests or parties acting in concert which comprises: Non Malaysian citizen; or Permanent Resident (Non Malaysian citizen and has been granted Permanent Resident status by the Malaysia Government); or Foreign companies or institution; or Companies incorporated in Malaysia with more than 50% owned by the above three definitions The guideline is divided into the following categories: - 1. ACQUISITION OF PROPERTY 2. EXEMPTIONS / RESTRICTION For further information, please refer to

8 a) ACQUISITION OF PROPERTY (effective from 1 March 2014) Acquisition Of Property By Foreign Interest All property acquisition by foreign interest that do not require the approval of the Economic Planning Unit, Prime Minister s Department but falls under the purview of the relevant Ministries and /or Government Departments as follows:- 1. Acquisition of Commercial Unit valued at RM1,000,000 and above; 2. Acquisition of agricultural land valued at RM1,000,000 and above or at least five (5) acres in area for the following purposes: agricultural activities on a commercial scale using modern or high technology; agro-tourism projects; agricultural or agro-based industrial activities for the production of goods for export. 3. Acquisition of residential unit valued at RM1,000,000 and above; 4. Acquisition of industrial land valued at RM1,000,000 and above; and 5. Transfer of property to a foreigner based on family ties is only allowed among immediate family members. b) EXEMPTIONS / RESTRICTION a) Exemption From Obtaining The Approval Of The FIC Acquisition of residential unit under Malaysia My Second Home Programme; Multimedia Super Corridor (MSC) status companies are allowed to acquire any property in the MSC area without obtaining the approval of FIC provided that the property is only used for their operational activities including as residence for their employees; Acquisitions of properties in the approved area in any regional development corridor by companies that have been granted the status by the local authority as determined by Government; Acquisition of properties by a company that has obtained the endorsement from the Secretariat of the Malaysia International Islamic Financial Centre (MIFC); Acquisition of residential units to be occupied as a hostel for company s employees. However, local companies owned by foreign interest are only allowed to acquire residential units valued at RM100,000 and above and this matter is under the jurisdiction of the relevant state authorities; Transfer of property pursuant to a will and court order; Acquisition of industrial property by manufacturing company licensed by the Ministry of International Trade and Industry for own manufacturing; Acquisition of properties by Ministries and Government Departments (Federal and State), Ministry of Finance Incorporated, Menteri Besar Incorporated or Chief Minister Incorporated, State Secretary Incorporated and listed Government Linked Companies; Acquisition of properties under the privatization projects, whether at the Federal or State level, provided that it involves the companies that are the original signatories in the contracts for the privatized projects; and Acquisition of properties by companies that have been granted the status of International Procurement Centres, Operational Headquarters, Representative Offices, Regional Offices, Labuan offshore companies and Bio-Nexus or other special status by the Ministry of Finance, Ministry of International trade and Industry and other ministries. b) Restrictions Foreign interest is not allowed to acquire: - Properties valued less than RM1,000,000/- per unit; All properties under the category of low and medium low cost as determined by the State Authority; All properties built on Malay reserve land; and Properties allocated to Bumiputera interest in any property development project as determined by the State Authority

9 MY FIRST HOME SCHEME The scheme was announced in 2011 Malaysia Budget in order to assist young adults to own their first home with up to 100% financing from Financial Institutions Who is THE BORROWER? Malaysian citizen First time home-buyer Individuals up to age 35 years Single borrowers with gross income RM3,000 per month Confirmed employee with minimum employment of 6 months with same employer. Repayment of total commitment amount must not be more than 55% of the gross monthly income. What are the criteria of PROPERTY? Residential properties located in Malaysia only Property value between RM100,000 and RM220,000 Owner occupied only (Buyers are required to reside in the property) How to APPLY? Eligible buyer will need to apply directly with participating banks. What are the FINANCING REQUIREMENTS? Financing tenure not exceeding 40 years, subject to borrower s age not exceeding 65 years at the end of financing tenure Amortizing facilities only (no redrawable features) Installments payable via monthly salary deductions or standing instruction Savings record (3 months installment liquidity reserve) Compulsory fire insurance/takaful Below are the PARTICIPATING BANKS: For more info please refer to:

")

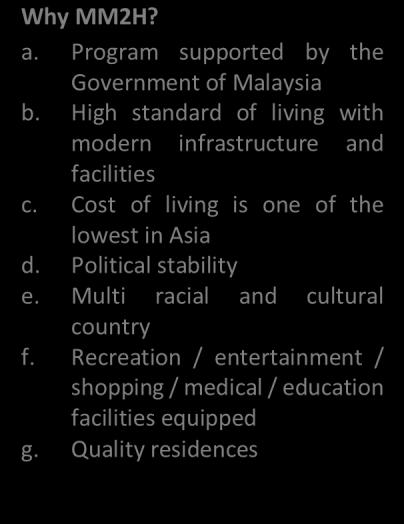

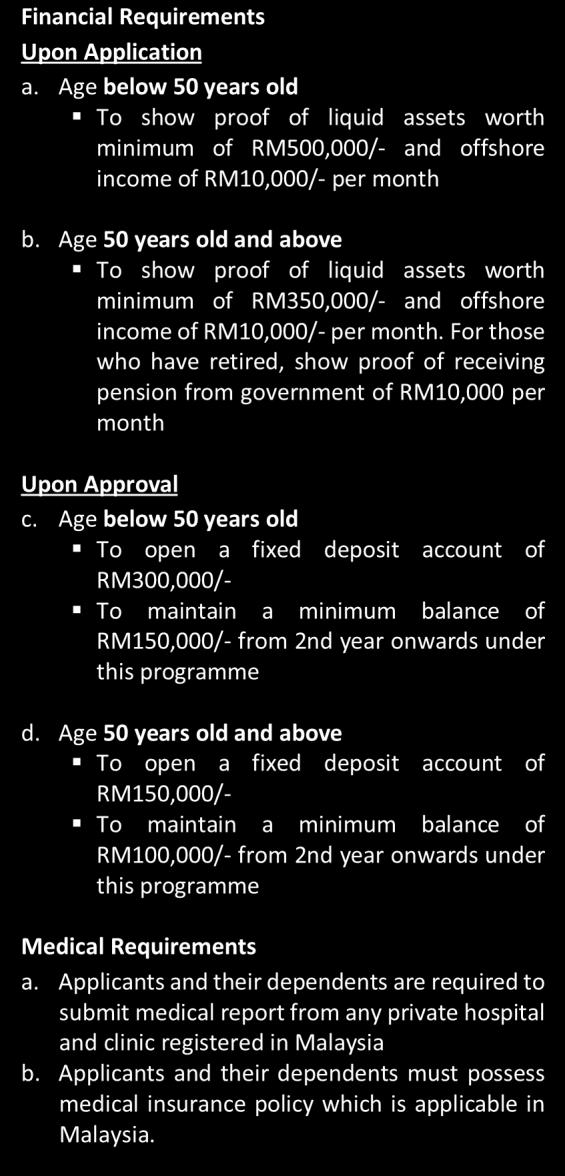

10 MALAYSIA MY SECOND HOME (MM2H) For further information, please refer to

11

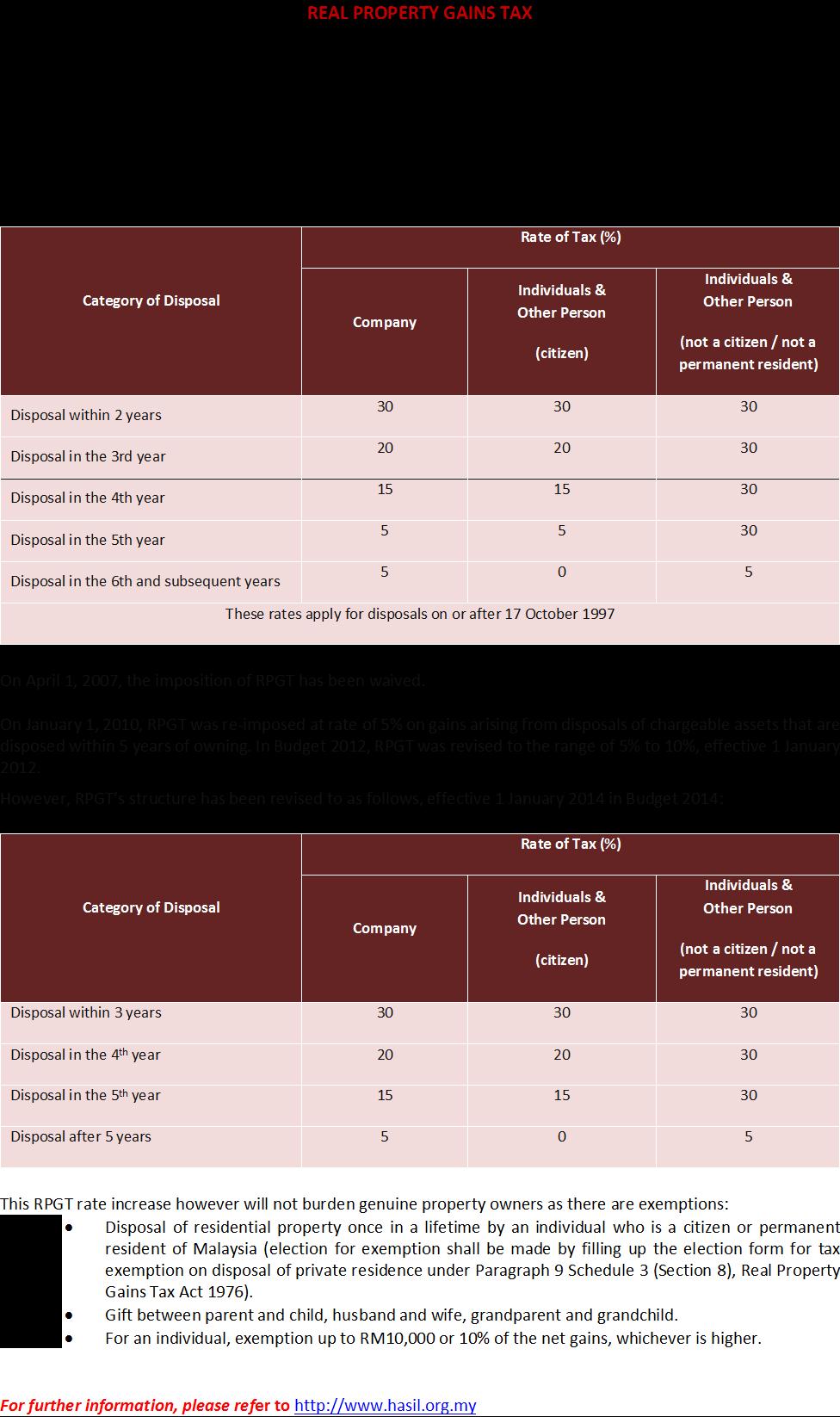

12 The Ad Valorem Duties (that is, according to the value) is levied on: i. Instruments of transfer of property including marketable securities, shares of other companies and of non tangible property, for example, book debts, benefits to legal rights and goodwill; ii. Instruments creating interests in property, for example tenancies and leases; iii. Instrument of security for monies including instruments creating contracts for payment of monies or obligation for payment of monies (generally described as "Bond"); iv. Certain capital market instrument, for example, Contract Notes and The Imposition of Fixed Duties on v. A number of other legal, commercial, mercantile or capital market instruments, for example, Power of Attorney, Articles of Association, Promissory Notes, Policy of Insurance etc; and vi. A duplicate or a subsidiary or a collateral instrument when it can be shown that the original or principal or primary instrument has been duly stamped Example Of Instruments Liable To Stamp Duty PURCHASE OF PROPERTY In the case of purchase of Immovable Property, the contract of sale and purchase is chargeable to ad valorem duty on the price. The duty at this rate is also payable where the instrument of transfer constitutes a DEED OF ASSIGNMENT executed on sale or gift of the contractual interest on the property. i. On the first RM100,000 RM1.00 for every RM100 or fractional part of RM100. (i.e. 1% on the 1 st RM100,000) ii. On any amount in excess of RM100,000 but not exceeding RM500,000 RM2.00 for every RM100 or fractional part of RM100. (i.e. 2% on the residue up to RM500,000) iii. On any amount in excess of RM500,000 RM3.00 for every RM100 or fractional part of RM100. (i.e. 3% on the residue over RM500,000) Lease & Tenancy Lease & Tenancy The lease or tenancy agreement which secures rental not exceeding RM2,400 per annum is EXEMPTED from duty. The prescribed rate of annual rent exceeding RM2,400 is as follows: When the lease is for a period Duty Rate Not exceeding one year RM1.00 Exceeding one but not exceeding three years RM2.00 Exceeding three years or for any indefinite period RM4.00 (For every RM250 or part thereof in excess of RM2,400) The undertaking for discharge of a debt is: Person Receiving Financing i) By way of promissory note, the duty on the note is RM10.00 irrespective of whether it is executed in favour of a commercial bank, merchant bank or borrowing company or otherwise. The stamping must be completed BEFORE the instrument is executed. ii) Secured by way of mortgage, charge, debenture and others, the duty on the principal security is calculated at the rate of RM 5.00 for every RM or part thereof.

GUIDELINE ON THE ACQUISITION OF PROPERTIES

GUIDELINE ON THE ACQUISITION OF PROPERTIES Economic Planning Unit, Prime Minister s Department CONTENTS I. INTRODUCTION... 1 II. APPLICATIONS... 1 III. CONDITIONS FOR ACQUISITION... 2 Equity Condition

GUIDELINE ON THE ACQUISITION OF PROPERTIES Economic Planning Unit, Prime Minister s Department CONTENTS I. INTRODUCTION... 1 II. APPLICATIONS... 1 III. CONDITIONS FOR ACQUISITION... 2 Equity Condition

Malaysian Budget Member Firm of CAS International

Malaysian Budget 2010 Member Firm of CAS International Contents Introduction Pages A. Personal Tax 1. Reduction in individual tax rate 2. Increase in Personal Relief 3. Individual tax relief on broadband

Malaysian Budget 2010 Member Firm of CAS International Contents Introduction Pages A. Personal Tax 1. Reduction in individual tax rate 2. Increase in Personal Relief 3. Individual tax relief on broadband

LIST OF APPENDICES. Tax Incentives for Small and Medium Enterprises to Register Patents and Trademarks Enhancing Tax Incentive for Health Tourism

LIST OF APPENDICES Appendix 1 : Appendix 2 : Tax Incentives for Small and Medium Enterprises to Register Patents and Trademarks Enhancing Tax Incentive for Health Tourism Appendix 3 : Individual Tax Relief

LIST OF APPENDICES Appendix 1 : Appendix 2 : Tax Incentives for Small and Medium Enterprises to Register Patents and Trademarks Enhancing Tax Incentive for Health Tourism Appendix 3 : Individual Tax Relief

Paper P6 (MYS) Advanced Taxation (Malaysia) Monday 3 December Professional Level Options Module

Advanced Taxation (Malaysia) Monday 3 December Professional Level Options Module") Professional Level Options Module Advanced Taxation (Malaysia) Monday 3 December 2007 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Professional Level Options Module Advanced Taxation (Malaysia) Monday 3 December 2007 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

It is proposed that the adjudication fee be abolished with effect from 1 January 2009.

C2 STAMP DUTY STAMP DUTY RATES Stamp duty is chargeable on certain instruments and documents. The rate of duty varies according to the nature of the instruments/documents and transacted values. Exemption

C2 STAMP DUTY STAMP DUTY RATES Stamp duty is chargeable on certain instruments and documents. The rate of duty varies according to the nature of the instruments/documents and transacted values. Exemption

Paper P6 (MYS) Advanced Taxation (Malaysia) Friday 7 December Professional Level Options Module

Advanced Taxation (Malaysia) Friday 7 December Professional Level Options Module") Professional Level Options Module Advanced Taxation (Malaysia) Friday 7 December 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Professional Level Options Module Advanced Taxation (Malaysia) Friday 7 December 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

SKIM RUMAH PERTAMAKU (SRP) MY FIRST HOME SCHEME

MY FIRST HOME SCHEME") SKIM RUMAH PERTAMAKU (SRP) MY FIRST HOME SCHEME PRODUCT DISCLOSURE SHEET Bank : Affin Bank Berhad Product : Skim Rumah Pertamaku (SRP) My First Home Scheme Date : 20 February 2018 1. What is this product

SKIM RUMAH PERTAMAKU (SRP) MY FIRST HOME SCHEME PRODUCT DISCLOSURE SHEET Bank : Affin Bank Berhad Product : Skim Rumah Pertamaku (SRP) My First Home Scheme Date : 20 February 2018 1. What is this product

LATEST INVESTMENT REGULATIONS IN MALAYSIA:

I. RELEVANT LEGISLATION LATEST INVESTMENT REGULATIONS IN : To enhance Malaysia s investment climate, effective from 17 June 2003, equity holdings in manufacturing projects were liberalised. Foreign investors

I. RELEVANT LEGISLATION LATEST INVESTMENT REGULATIONS IN : To enhance Malaysia s investment climate, effective from 17 June 2003, equity holdings in manufacturing projects were liberalised. Foreign investors

PUBLIC FINANCE MANAGEMENT ACT (No. 18 of 2012) COUNTY GOVERNMENT OF KIRINYAGA

COUNTY GOVERNMENT OF KIRINYAGA") LEGAL NOTICE NO. PUBLIC FINANCE MANAGEMENT ACT (No. 18 of 2012) COUNTY GOVERNMENT OF KIRINYAGA IN EXERCISE of the powers conferred by Section 116 of the Public Finance Management Act, 2012, the County

LEGAL NOTICE NO. PUBLIC FINANCE MANAGEMENT ACT (No. 18 of 2012) COUNTY GOVERNMENT OF KIRINYAGA IN EXERCISE of the powers conferred by Section 116 of the Public Finance Management Act, 2012, the County

ARREIT MTN 1 SDN BHD PROPOSED ISSUANCE OF UNRATED MEDIUM TERM NOTES PROGRAMME OF UP TO RM950.0 MILLION IN NOMINAL VALUE ( MTN PROGRAMME )

") Other Terms and Conditions (i) Interest/ coupon rate Tranche 1 MTNs 0.5% per annum ( p.a. ) plus the Investor s Cost Funds ( COF ) quoted by the Investor prior to issuance the Tranche 1 MTNs or prior to

Other Terms and Conditions (i) Interest/ coupon rate Tranche 1 MTNs 0.5% per annum ( p.a. ) plus the Investor s Cost Funds ( COF ) quoted by the Investor prior to issuance the Tranche 1 MTNs or prior to

BELIZE DEVELOPMENT FINANCE CORPORATION ACT CHAPTER 279 REVISED EDITION 2000 SHOWING THE LAW AS AT 31ST DECEMBER, 2000

BELIZE DEVELOPMENT FINANCE CORPORATION ACT CHAPTER 279 REVISED EDITION 2000 SHOWING THE LAW AS AT 31ST DECEMBER, 2000 This is a revised edition of the law, prepared by the Law Revision Commissioner under

BELIZE DEVELOPMENT FINANCE CORPORATION ACT CHAPTER 279 REVISED EDITION 2000 SHOWING THE LAW AS AT 31ST DECEMBER, 2000 This is a revised edition of the law, prepared by the Law Revision Commissioner under

Putrajaya Holdings Sdn Bhd RM850.0 Million in Nominal Value of Al-Bai Bithaman Ajil Serial Bonds PRINCIPAL TERMS AND CONDITIONS

1. Issuer: Putrajaya Holdings Sdn Bhd 2. Adviser: RHB Sakura Merchant Bankers Berhad 3. Joint Arrangers: RHB Sakura Merchant Bankers Berhad Alliance Merchant Bank Berhad 4. Facility Agent: RHB Sakura Merchant

1. Issuer: Putrajaya Holdings Sdn Bhd 2. Adviser: RHB Sakura Merchant Bankers Berhad 3. Joint Arrangers: RHB Sakura Merchant Bankers Berhad Alliance Merchant Bank Berhad 4. Facility Agent: RHB Sakura Merchant

CHAPTER 1 INTRODUCTION

CHAPTER 1 INTRODUCTION 1 Chapter 1 1.1 Introduction The social changes in the diminishing role of the extended family and the ageing of the population in both developed and emerging market economies have

CHAPTER 1 INTRODUCTION 1 Chapter 1 1.1 Introduction The social changes in the diminishing role of the extended family and the ageing of the population in both developed and emerging market economies have

Country Tax Guide.

Country Tax Guide www.bakertillyinternational.com Facts and figures as presented are correct as at 15 August 2014. Corporate Income Taxes Singapore has a territorial tax system. Resident companies, defined

Country Tax Guide www.bakertillyinternational.com Facts and figures as presented are correct as at 15 August 2014. Corporate Income Taxes Singapore has a territorial tax system. Resident companies, defined

PRINCIPAL TERMS AND CONDITIONS

PRINCIPAL TERMS AND CONDITIONS Issuer : Sejingkat Power Corporation Sdn Bhd ( Sejingkat Power ) Facility : Al-Bai Bithaman Ajil ( deferred payment sale ) with Islamic Debt Securities Issuance Facility

PRINCIPAL TERMS AND CONDITIONS Issuer : Sejingkat Power Corporation Sdn Bhd ( Sejingkat Power ) Facility : Al-Bai Bithaman Ajil ( deferred payment sale ) with Islamic Debt Securities Issuance Facility

STAMP DUTIES (MISCELLANEOUS AMENDMENTS) ACT

ACT") STAMP DUTIES (MISCELLANEOUS AMENDMENTS) ACT 1990 No. 95 NEW SOUTH WALES Act No. 95, 1990 An Act to amend the Stamp Duties Act 1920 to make further provision with respect to the imposition of stamp duties

STAMP DUTIES (MISCELLANEOUS AMENDMENTS) ACT 1990 No. 95 NEW SOUTH WALES Act No. 95, 1990 An Act to amend the Stamp Duties Act 1920 to make further provision with respect to the imposition of stamp duties

AFFIN HOME ASSIST PLUS

AFFIN HOME ASSIST PLUS PRODUCT DISCLOSURE SHEET Bank : Affin Bank Berhad Product : Affin Home Assist Plus Date : 20 February, 2018 1. What is this product about? AFFIN HOME ASSIST PLUS is a housing loan

AFFIN HOME ASSIST PLUS PRODUCT DISCLOSURE SHEET Bank : Affin Bank Berhad Product : Affin Home Assist Plus Date : 20 February, 2018 1. What is this product about? AFFIN HOME ASSIST PLUS is a housing loan

MM2H participants are allowed to employ one domestic helper.

INCENTIVES MM2H (Malaysia My Second Home) Car Purchase Successful applicants are allowed to purchase one new motorcar made or assembled in Malaysia without the need to pay excise duty and sales tax, within

INCENTIVES MM2H (Malaysia My Second Home) Car Purchase Successful applicants are allowed to purchase one new motorcar made or assembled in Malaysia without the need to pay excise duty and sales tax, within

Paper P6 (MYS) Advanced Taxation (Malaysia) Thursday 10 December Professional Level Options Module

Advanced Taxation (Malaysia) Thursday 10 December Professional Level Options Module") Professional Level Options Module Advanced Taxation (Malaysia) Thursday 10 December 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours This question paper is divided into two sections:

Professional Level Options Module Advanced Taxation (Malaysia) Thursday 10 December 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours This question paper is divided into two sections:

PRINCIPAL TERMS AND CONDITIONS

PRINCIPAL TERMS AND CONDITIONS Issuer : Sarawak Power Generation Sdn Bhd Facility : Al-Bai Bithaman Ajil ( deferred payment sale ) with Islamic Debt Securities Issuance Facility (hereinafter referred to

PRINCIPAL TERMS AND CONDITIONS Issuer : Sarawak Power Generation Sdn Bhd Facility : Al-Bai Bithaman Ajil ( deferred payment sale ) with Islamic Debt Securities Issuance Facility (hereinafter referred to

NATIONAL HOUSING FUND ACT

NATIONAL HOUSING FUND ACT ARRANGEMENT OF SECTIONS 1. Establishment of the National Housing Fund. 2. Aims and objectives of the Fund. 3. Resources of the Fund. 4. Contribution by Nigerian workers. 5. Contribution

NATIONAL HOUSING FUND ACT ARRANGEMENT OF SECTIONS 1. Establishment of the National Housing Fund. 2. Aims and objectives of the Fund. 3. Resources of the Fund. 4. Contribution by Nigerian workers. 5. Contribution

Paper P6 (MYS) Advanced Taxation (Malaysia) September/December 2017 Sample Questions. Professional Level Options Module

Advanced Taxation (Malaysia) September/December 2017 Sample Questions. Professional Level Options Module") Professional Level Options Module Advanced Taxation (Malaysia) September/December 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH

Professional Level Options Module Advanced Taxation (Malaysia) September/December 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH

Staff Connections - World Bank Intranet

Page 1 of 7 Staff Connections - World Bank Intranet 06 Compensation 06.18 Financial Assistance to Staff Members 01. Subject, Applicability and Definitions 02. General Provisions 03. Loans for Settling-In

Page 1 of 7 Staff Connections - World Bank Intranet 06 Compensation 06.18 Financial Assistance to Staff Members 01. Subject, Applicability and Definitions 02. General Provisions 03. Loans for Settling-In

Paper P6 (MYS) Advanced Taxation (Malaysia) Monday 7 June Professional Level Options Module. The Association of Chartered Certified Accountants

Advanced Taxation (Malaysia) Monday 7 June Professional Level Options Module. The Association of Chartered Certified Accountants") Professional Level Options Module Advanced Taxation (Malaysia) Monday 7 June 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Professional Level Options Module Advanced Taxation (Malaysia) Monday 7 June 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Professional Level Options Module, Paper P6 (MYS)

") Answers Professional Level Options Module, Paper P6 (MYS) Advanced Taxation (Malaysia) December 2007 Answers and Marking Scheme Marks 1 (a) Report to The directors of Salmon Berhad From Tip Top Tax Services

Answers Professional Level Options Module, Paper P6 (MYS) Advanced Taxation (Malaysia) December 2007 Answers and Marking Scheme Marks 1 (a) Report to The directors of Salmon Berhad From Tip Top Tax Services

Q&A. Fixed Deposit. Education. House Purchase

01 Q&A Fixed Deposit Can I withdraw my fixed deposit any time during my stay in Malaysia? Participants must maintain a minimum balance of RM150,000 and RM100,000 in their fixed deposit accounts for applicants

01 Q&A Fixed Deposit Can I withdraw my fixed deposit any time during my stay in Malaysia? Participants must maintain a minimum balance of RM150,000 and RM100,000 in their fixed deposit accounts for applicants

MALAYSIA. Country M&A Team Country Leader ~ Frances Po Peter Wee Chang Huey Yueh. 149 PricewaterhouseCoopers

149 PricewaterhouseCoopers MALAYSIA Country M&A Team Country Leader ~ Frances Po Peter Wee Chang Huey Yueh 150 PricewaterhouseCoopers Name Designation Office Tel Email Frances Po Partner +603 2693 1077

149 PricewaterhouseCoopers MALAYSIA Country M&A Team Country Leader ~ Frances Po Peter Wee Chang Huey Yueh 150 PricewaterhouseCoopers Name Designation Office Tel Email Frances Po Partner +603 2693 1077

Hyperlinks. April Advent Consulting Group Inland Revenue Board. References. PR No. 2/2013 Perquisites from Employment. PR No.

April 2013 Hyperlinks Advent Consulting Group Inland Revenue Board PR No. 2/2013 Perquisites from Employment The Inland Revenue Board [ IRB ] has recently issued the Public Ruling [ PR ] No. 2/2013 Perquisites

April 2013 Hyperlinks Advent Consulting Group Inland Revenue Board PR No. 2/2013 Perquisites from Employment The Inland Revenue Board [ IRB ] has recently issued the Public Ruling [ PR ] No. 2/2013 Perquisites

General Banking and Wing Lung Sunflower Service Charges

Member CMB Group General Banking and Wing Lung Sunflower Service Charges With effect from 18 th December 2017 Enquiry Hotline: 230 95555 www.winglungbank.com - Table of Content - Part 1 - Deposit Service

Member CMB Group General Banking and Wing Lung Sunflower Service Charges With effect from 18 th December 2017 Enquiry Hotline: 230 95555 www.winglungbank.com - Table of Content - Part 1 - Deposit Service

Subject BR (From 1 Apr 2015)

") C. Overdraft PRODUCT DISCLOSURE SHEET (Read this Product Disclosure Sheet before you decide to take out the Overdraft Facility for Property financing. Be sure to also read the terms in the letter of offer.

C. Overdraft PRODUCT DISCLOSURE SHEET (Read this Product Disclosure Sheet before you decide to take out the Overdraft Facility for Property financing. Be sure to also read the terms in the letter of offer.

JSE Guarantee Fund Rules

Scope of Rules 1 Name 2 Separate Identity and Ownership 3-4 Trustees 5 Definitions 6-9 Administration and Investments 10-11 Fund Assets 12-15 Contributions 16 Liability of the Fund for Losses 17-18 Claims

Scope of Rules 1 Name 2 Separate Identity and Ownership 3-4 Trustees 5 Definitions 6-9 Administration and Investments 10-11 Fund Assets 12-15 Contributions 16 Liability of the Fund for Losses 17-18 Claims

BELIZE STAMP DUTIES ACT CHAPTER 64 REVISED EDITION 2003 SHOWING THE SUBSIDIARY LAWS AS AT 31ST OCTOBER, 2003

BELIZE STAMP DUTIES ACT REVISED EDITION 2003 SHOWING THE SUBSIDIARY LAWS AS AT 31ST OCTOBER, 2003 This is a revised edition of the Subsidiary Laws, prepared by the Law Revision Commissioner under the authority

BELIZE STAMP DUTIES ACT REVISED EDITION 2003 SHOWING THE SUBSIDIARY LAWS AS AT 31ST OCTOBER, 2003 This is a revised edition of the Subsidiary Laws, prepared by the Law Revision Commissioner under the authority

PROMISSORY NOTE. Bellingham Resale Restricted Downpayment

PROMISSORY NOTE Bellingham Resale Restricted Downpayment Today s Date: At, Washington Property Address:, 1. Borrower s Promise to Pay In return for a loan received, I promise to pay to the order of the

PROMISSORY NOTE Bellingham Resale Restricted Downpayment Today s Date: At, Washington Property Address:, 1. Borrower s Promise to Pay In return for a loan received, I promise to pay to the order of the

FOREWORD. Tunisia. Services provided by member firms include:

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

Malaysia company registration

Malaysia company registration Table of contents For over a decade, Healy Consultants has efficiently and effectively assisted our Clients with registering their business in Malaysia. We help our Clients

Malaysia company registration Table of contents For over a decade, Healy Consultants has efficiently and effectively assisted our Clients with registering their business in Malaysia. We help our Clients

DISCLOSURE OF FEES AND CHARGES

DISCLOSURE OF FEES AND CHARGES LENDING AND CREDIT CARDS UNSECURED PERSONAL LOAN Loan Approval Fee: - up to $499; $75.00 - $500 to $4,999; $125.00 - $5,000 to $19,999; $250.00 - $20,000 to $49,999; $500.00

DISCLOSURE OF FEES AND CHARGES LENDING AND CREDIT CARDS UNSECURED PERSONAL LOAN Loan Approval Fee: - up to $499; $75.00 - $500 to $4,999; $125.00 - $5,000 to $19,999; $250.00 - $20,000 to $49,999; $500.00

MH CHEONG & ASSOCIATES CERTIFIED PUBLIC ACCOUNTANTS

Vol. 1 ISSUE 10 November 99 YEAR 2000 MALAYSIAN BUDGET COMMENTARY The Finance Minister, Daim Zainuddin delivered the year 2000 Budget Statement to Parliament on 29 October 1999. Income tax rates were lowered

Vol. 1 ISSUE 10 November 99 YEAR 2000 MALAYSIAN BUDGET COMMENTARY The Finance Minister, Daim Zainuddin delivered the year 2000 Budget Statement to Parliament on 29 October 1999. Income tax rates were lowered

Your Report on Title must be given to the Bank in the Bank s standard form Report on Title - HDB Property.

OVERSEA-CHINESE BANKING CORPORATION LIMITED POLICIES FOR HOUSING & DEVELOPMENT BOARD PROPERTY MORTGAGE 10 January 2019 (CREDIT FACILITIES ADMINISTERED BY CONSUMER LOAN OPERATIONS) General Unless otherwise

OVERSEA-CHINESE BANKING CORPORATION LIMITED POLICIES FOR HOUSING & DEVELOPMENT BOARD PROPERTY MORTGAGE 10 January 2019 (CREDIT FACILITIES ADMINISTERED BY CONSUMER LOAN OPERATIONS) General Unless otherwise

Goods and Services Tax (GST) Frequently Asked Questions (FAQ) For Retail Customers

Frequently Asked Questions (FAQ) For Retail Customers") Goods and Services Tax (GST) Frequently Asked Questions (FAQ) For Retail Customers GENERAL/UNRESTRICTED 2015, Maybank. All Rights Reserved. Page 1 of 9 No. Title Table of Contents Page Number 1.0 Regulatory

Goods and Services Tax (GST) Frequently Asked Questions (FAQ) For Retail Customers GENERAL/UNRESTRICTED 2015, Maybank. All Rights Reserved. Page 1 of 9 No. Title Table of Contents Page Number 1.0 Regulatory

REVERSE MORTGAGE PROGRAMME IMPORTANT NOTICE

REVERSE MORTGAGE PROGRAMME IMPORTANT NOTICE Please read this notice carefully before you proceed with your application for a reverse mortgage loan. This notice only provides additional information about

REVERSE MORTGAGE PROGRAMME IMPORTANT NOTICE Please read this notice carefully before you proceed with your application for a reverse mortgage loan. This notice only provides additional information about

LEGAL PROFESSION ACT 1976 SOLICITORS REMUNERATION ORDER IN exercise of the powers conferred by subsection 113(3) of the Legal Profession

of the Legal Profession") LEGAL PROFESSION ACT 1976 SOLICITORS REMUNERATION ORDER 2006 IN exercise of the powers conferred by subsection 113(3) of the Legal Profession Act 1976 [Act 166], the Solicitors Cost Committee makes the

LEGAL PROFESSION ACT 1976 SOLICITORS REMUNERATION ORDER 2006 IN exercise of the powers conferred by subsection 113(3) of the Legal Profession Act 1976 [Act 166], the Solicitors Cost Committee makes the

SELF-EMPLOYMENT PROGRAM MONTHLY REPORTING WORKSHEET

CLIENT NAME BUSINESS NAME MONTH ENDED INSTRUCTIONS This worksheet is for use by clients participating in an approved ministry Self-Employment Program. This worksheet is not a required form but is intended

CLIENT NAME BUSINESS NAME MONTH ENDED INSTRUCTIONS This worksheet is for use by clients participating in an approved ministry Self-Employment Program. This worksheet is not a required form but is intended

First floor 400,000 Second floor 200, ,000 Total for three floors 1,200,000 Portion exempt (600,000/1,200,000) 50%

50%") Answers Fundamentals Level Skills Module, Paper F6 (MYS) Taxation (Malaysia) Section B March/June 07 Sample Answers and Marking Scheme (a) Adora and Zizan Real property gains tax (RPGT) (i) Adora will

Answers Fundamentals Level Skills Module, Paper F6 (MYS) Taxation (Malaysia) Section B March/June 07 Sample Answers and Marking Scheme (a) Adora and Zizan Real property gains tax (RPGT) (i) Adora will

FOREWORD. Grenada. Services provided by member firms include:

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

Income Tax Act 1967 Orders

Income Tax Act 1967 Orders Subsidiary legislation Orders Income Tax (Exemption) (No 24) Order 1993 (Income of an approved research institute or approved research company) Income Tax (Exemption) (No 25)

Income Tax Act 1967 Orders Subsidiary legislation Orders Income Tax (Exemption) (No 24) Order 1993 (Income of an approved research institute or approved research company) Income Tax (Exemption) (No 25)

Guide to Residential Property Letting

Guide to Residential Property Letting How is tax calculated and when is it due? The amount on which tax is charged is the net rental income for each tax year (i.e. for each tax year ending on 5 April).

Guide to Residential Property Letting How is tax calculated and when is it due? The amount on which tax is charged is the net rental income for each tax year (i.e. for each tax year ending on 5 April).

The Chartered Tax Adviser Examination

The Chartered Tax Adviser Examination Sample Paper Application and Professional Skills Owner Managed Businesses Suggested solutions REPORT TO HORATIO STILES ON 1) THE USE OF SURPLUS FUNDS STILES CONSTRUCTION

The Chartered Tax Adviser Examination Sample Paper Application and Professional Skills Owner Managed Businesses Suggested solutions REPORT TO HORATIO STILES ON 1) THE USE OF SURPLUS FUNDS STILES CONSTRUCTION

REGISTRATION DUTY ACT Arrêté du 16 Frimaire An XII 17 December 1804 Act 1 of 1955 Act 31 of 1962

Revised Laws of Mauritius REGISTRATION DUTY ACT Arrêté du 16 Frimaire An XII 17 December 1804 Act 1 of 1955 Act 31 of 1962 ARRANGEMENT OF SECTIONS SECTION PART I PRELIMINARY 1. Short title 2. Interpretation

Revised Laws of Mauritius REGISTRATION DUTY ACT Arrêté du 16 Frimaire An XII 17 December 1804 Act 1 of 1955 Act 31 of 1962 ARRANGEMENT OF SECTIONS SECTION PART I PRELIMINARY 1. Short title 2. Interpretation

INTRODUCTION. Situations should be viewed separately based on specific facts of each scenario.

TAX FACTS 2018 CONTENTS INTRODUCTION... 3 PERSONAL INCOME TAX... 4 CORPORATION TAX... 8 SOCIAL INSURANCE... 12 SPECIAL CONTRIBUTION FOR DEFENCE... 13 INTELLECTUAL PROPERTY... 16 VALUE ADDED TAX... 18 CAPITAL

TAX FACTS 2018 CONTENTS INTRODUCTION... 3 PERSONAL INCOME TAX... 4 CORPORATION TAX... 8 SOCIAL INSURANCE... 12 SPECIAL CONTRIBUTION FOR DEFENCE... 13 INTELLECTUAL PROPERTY... 16 VALUE ADDED TAX... 18 CAPITAL

FINANCE BILL 2016 LIST OF ITEMS PART 1 MEASURES ANNOUNCED IN THE BUDGET PART 2 FURTHER MEASURES INCLUDED IN THE FINANCE BILL

FINANCE BILL 2016 LIST OF ITEMS PART 1 MEASURES ANNOUNCED IN THE BUDGET PART 2 FURTHER MEASURES INCLUDED IN THE FINANCE BILL 1 PART 1 - MEASURES ANNOUNCED IN THE BUDGET INCOME TAX... 4 SECTIONS 2 TO 4

FINANCE BILL 2016 LIST OF ITEMS PART 1 MEASURES ANNOUNCED IN THE BUDGET PART 2 FURTHER MEASURES INCLUDED IN THE FINANCE BILL 1 PART 1 - MEASURES ANNOUNCED IN THE BUDGET INCOME TAX... 4 SECTIONS 2 TO 4

FREQUENTLY ASKED QUESTIONS (FAQ) TRANSITIONAL 6% - 0%

TRANSITIONAL 6% - 0%") Without prejudice. FREQUENTLY ASKED QUESTIONS (FAQ) TRANSITIONAL 6% - 0% Note: The FAQ dated 17 May 2018 is cancelled. 1. STATUS OF GST 1.1. S : What does the MOF statement mean / What happens to GST?

Without prejudice. FREQUENTLY ASKED QUESTIONS (FAQ) TRANSITIONAL 6% - 0% Note: The FAQ dated 17 May 2018 is cancelled. 1. STATUS OF GST 1.1. S : What does the MOF statement mean / What happens to GST?

CIMB CashLite Terms and Conditions

CIMB CashLite Terms and Conditions CashLite Terms and Conditions (Updated 21 st August 2013)Page 1 CashLite Terms and Conditions CashLite Programme 1. The CashLite Programme (the Programme ) is offered

CIMB CashLite Terms and Conditions CashLite Terms and Conditions (Updated 21 st August 2013)Page 1 CashLite Terms and Conditions CashLite Programme 1. The CashLite Programme (the Programme ) is offered

General Banking and Sunflower Service Charges

Member CMB Group General Banking and Sunflower Service Charges Effective on 1 November 2016 Enquiry Hotline: 230 95555 www.winglungbank.com - Table of Content - Part 1 - Deposit Service Charges 1 Part

Member CMB Group General Banking and Sunflower Service Charges Effective on 1 November 2016 Enquiry Hotline: 230 95555 www.winglungbank.com - Table of Content - Part 1 - Deposit Service Charges 1 Part

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON FUND MANAGEMENT

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON FUND MANAGEMENT Publication Date Published: 11 April 2016. The Guide on Fund Management revised as at 27 October 2013 is withdrawn and replaced by

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON FUND MANAGEMENT Publication Date Published: 11 April 2016. The Guide on Fund Management revised as at 27 October 2013 is withdrawn and replaced by

IKATAN PERKASA SDN BHD ( IPSB ) RM185 MILLION NOMINAN VALUE REDEEMABLE SECURED SERIALBONDS PRINCIPAL TERMS AND CONDITIONS OF THE PROPOSED BONDS ISSUE

RM185 MILLION NOMINAN VALUE REDEEMABLE SECURED SERIALBONDS PRINCIPAL TERMS AND CONDITIONS OF THE PROPOSED BONDS ISSUE") IKATAN PERKASA SDN BHD ( IPSB ) RM185 MILLION NOMINAN VALUE REDEEMABLE SECURED SERIALBONDS PRINCIPAL TERMS AND CONDITIONS OF THE PROPOSED BONDS ISSUE Issuer : Ikatan Perkasa Sdn Bhd ( IPSB ) Issue : Proposed

IKATAN PERKASA SDN BHD ( IPSB ) RM185 MILLION NOMINAN VALUE REDEEMABLE SECURED SERIALBONDS PRINCIPAL TERMS AND CONDITIONS OF THE PROPOSED BONDS ISSUE Issuer : Ikatan Perkasa Sdn Bhd ( IPSB ) Issue : Proposed

United Kingdom. I. Taxes on Corporate Income

OECD Model Tax Convention on Income and on Capital (Condensed version 2010) and Key Tax Features of Member countries 2011 United Kingdom 1. Corporate income tax I. Taxes on Corporate Income Corporate profits

OECD Model Tax Convention on Income and on Capital (Condensed version 2010) and Key Tax Features of Member countries 2011 United Kingdom 1. Corporate income tax I. Taxes on Corporate Income Corporate profits

Early Closure means closure of Bursa Securities or such relevant Securities Exchange prior to its scheduled closing time; or

the Market Day immediately preceding the Expiry Date on which there is no Market Disruption Event or on which there is trading of the Underlying Shares ( Last Valuation Date ) shall be deemed to be the

the Market Day immediately preceding the Expiry Date on which there is no Market Disruption Event or on which there is trading of the Underlying Shares ( Last Valuation Date ) shall be deemed to be the

Wing Lung Private Banking Service Charges. With effect from 18 th December Enquiry Hotline:

Wing Lung Private Banking Service Charges With effect from 18 th December 2017 Enquiry Hotline: 268 95555 www.winglungbank.com/privatebanking Member CMB Group - Table of Content - Part 1 - Wing Lung Private

Wing Lung Private Banking Service Charges With effect from 18 th December 2017 Enquiry Hotline: 268 95555 www.winglungbank.com/privatebanking Member CMB Group - Table of Content - Part 1 - Wing Lung Private

RETIRED PERSONS (INCENTIVES) ACT CHAPTER 62 REVISED EDITION 2000 SHOWING THE LAW AS AT 31ST DECEMBER, 2000.

ACT CHAPTER 62 REVISED EDITION 2000 SHOWING THE LAW AS AT 31ST DECEMBER, 2000.") BELIZE RETIRED PERSONS (INCENTIVES) ACT CHAPTER 62 REVISED EDITION 2000 SHOWING THE LAW AS AT 31ST DECEMBER, 2000. This is a revised edition of the law, prepared by the Law Revision Commissioner under

BELIZE RETIRED PERSONS (INCENTIVES) ACT CHAPTER 62 REVISED EDITION 2000 SHOWING THE LAW AS AT 31ST DECEMBER, 2000. This is a revised edition of the law, prepared by the Law Revision Commissioner under

B6 CAPITAL ALLOWANCES

B6 CAPITAL ALLOWANCES A1. CURRENT CAPITAL ALLOWANCES RATES FOR PLANT A1. Standard rates With effect from Y/A 2000 (cyb), capital allowances are re-categorised into three classes and the rates of capital

B6 CAPITAL ALLOWANCES A1. CURRENT CAPITAL ALLOWANCES RATES FOR PLANT A1. Standard rates With effect from Y/A 2000 (cyb), capital allowances are re-categorised into three classes and the rates of capital

[ Published in the Official Gazette Vol. XXVI No. 74 dated 14th December, ]

![[ Published in the Official Gazette Vol. XXVI No. 74 dated 14th December, ]](/thumbs/78/78712671.jpg "[ Published in the Official Gazette Vol. XXVI No. 74 dated 14th December, ]") No. 15 of 2006. The Investment Authority Act, 2006. 1 ANTIGUA [ L.S. ] I Assent, James B. Carlisle, Governor-General. 17th November, 2006. ANTIGUA No. 15 of 2006 FOR AN ACT to establish an investment authority,

No. 15 of 2006. The Investment Authority Act, 2006. 1 ANTIGUA [ L.S. ] I Assent, James B. Carlisle, Governor-General. 17th November, 2006. ANTIGUA No. 15 of 2006 FOR AN ACT to establish an investment authority,

Pre-contractual General Information Sheet (Home Loans)

") Classic Home Loans, Bridge Loans, APluS Accounts, Buy-to-Let Loans and Personal Loans secured by residential immovable property to residents of Malta 1. Lender identity, geographical address and contact

Classic Home Loans, Bridge Loans, APluS Accounts, Buy-to-Let Loans and Personal Loans secured by residential immovable property to residents of Malta 1. Lender identity, geographical address and contact

Help to Buy Buyers Guide

Help to Buy Buyers Guide Homes England http://www.homesengland.gov.uk/helptobuy Page 1 of 29 Contents Key information... 3 What is Help to Buy?... 4 Help to Buy overview... 5 How does it work?... 6 Who

Help to Buy Buyers Guide Homes England http://www.homesengland.gov.uk/helptobuy Page 1 of 29 Contents Key information... 3 What is Help to Buy?... 4 Help to Buy overview... 5 How does it work?... 6 Who

The Shariah concept applicable is Musharakah Mutanaqisah (MM) or Diminishing Musharakah and Tawarruq

or Diminishing Musharakah and Tawarruq") PRODUCT DISCLOSURE SHEET (Read this Product Disclosure Sheet before you decide to take the Affin Tawarruq Home Refinancing-i / Affin Tawarruq BP Refinancing-i. Be sure to also read the terms in the letter

PRODUCT DISCLOSURE SHEET (Read this Product Disclosure Sheet before you decide to take the Affin Tawarruq Home Refinancing-i / Affin Tawarruq BP Refinancing-i. Be sure to also read the terms in the letter

0 Sierra Leone Fiscal Guide 2015/2016. Tax. kpmg.com

0 Sierra Leone Fiscal Guide 2015/2016 Tax kpmg.com 1 Sierra Nigeria Leone Fiscal Fiscal Guide Guide 2013/2014 2015/2016 INTRODUCTION Sierra Leone Fiscal Guide 2015/2016 2 Business income Residents are

0 Sierra Leone Fiscal Guide 2015/2016 Tax kpmg.com 1 Sierra Nigeria Leone Fiscal Fiscal Guide Guide 2013/2014 2015/2016 INTRODUCTION Sierra Leone Fiscal Guide 2015/2016 2 Business income Residents are

Standard Charge/ Mortgage Terms ALBERTA. MCAP Service Corporation. Filing Details: Filing #:_ _. Filing Date: April 26, 2010

Filed By: MCAP Service Corporation Standard Charge/ Mortgage Terms ALBERTA Filing Details: Filing #: 101118288 Filing Date: April 26, 2010 These Standard Charge/ Mortgage Terms form part of every Charge/

Filed By: MCAP Service Corporation Standard Charge/ Mortgage Terms ALBERTA Filing Details: Filing #: 101118288 Filing Date: April 26, 2010 These Standard Charge/ Mortgage Terms form part of every Charge/

Income Tax. Income Tax allowances Personal Allowance (1) 7,475 8,105 N/A

7,475 8,105 N/A") Income Tax Income Tax allowances table Income Tax allowances 2011-12 2012-13 2013-14 Personal Allowance (1) 7,475 8,105 N/A Personal Allowance for people born after 5 April 1948 (1) N/A N/A 9,440 Income

Income Tax Income Tax allowances table Income Tax allowances 2011-12 2012-13 2013-14 Personal Allowance (1) 7,475 8,105 N/A Personal Allowance for people born after 5 April 1948 (1) N/A N/A 9,440 Income

Ghana Tax Guide 2012

Ghana Tax Guide 2012 I IMPORTANT DISCLAIMER: No person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice

Ghana Tax Guide 2012 I IMPORTANT DISCLAIMER: No person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice

PRODUCT DISCLOSURE SHEET

PRODUCT DISCLOSURE SHEET Kindly read this Product Disclosure Sheet together with the terms in the Letter of Offer before you decide to take up the product below: Please tick whichever is applicable in

PRODUCT DISCLOSURE SHEET Kindly read this Product Disclosure Sheet together with the terms in the Letter of Offer before you decide to take up the product below: Please tick whichever is applicable in

Key Features of The Budget 2011 MALAYSIA A Business Perspective Prepared By Chew Por Yan, Angeline Managing Partner ACT Partners Date 18 October 2010

Title Key Features of The Budget 2011 MALAYSIA A Business Perspective Prepared By Chew Por Yan, Angeline Managing Partner ACT Partners Date 18 October 2010 The Prime Minister cum Finance Minister of Malaysia,

Title Key Features of The Budget 2011 MALAYSIA A Business Perspective Prepared By Chew Por Yan, Angeline Managing Partner ACT Partners Date 18 October 2010 The Prime Minister cum Finance Minister of Malaysia,

means payment of or receipt arising from trading of goods or services,

4. Definition of FEA Rules Activities in the Real Sector 11Anticipatory Appointed overseas office Borrowing Activities relating to - (a) The production or consumption of goods or services, other than -

4. Definition of FEA Rules Activities in the Real Sector 11Anticipatory Appointed overseas office Borrowing Activities relating to - (a) The production or consumption of goods or services, other than -

BELIZE RETIRED PERSONS (INCENTIVES) ACT CHAPTER 62 REVISED EDITION 2011 SHOWING THE SUBSTANTIVE LAWS AS AT 31 ST DECEMBER, 2011

ACT CHAPTER 62 REVISED EDITION 2011 SHOWING THE SUBSTANTIVE LAWS AS AT 31 ST DECEMBER, 2011") BELIZE RETIRED PERSONS (INCENTIVES) ACT CHAPTER 62 SHOWING THE SUBSTANTIVE LAWS AS AT 31 ST DECEMBER, 2011 This is a revised edition of the Substantive Laws, prepared by the Law Revision Commissioner under

BELIZE RETIRED PERSONS (INCENTIVES) ACT CHAPTER 62 SHOWING THE SUBSTANTIVE LAWS AS AT 31 ST DECEMBER, 2011 This is a revised edition of the Substantive Laws, prepared by the Law Revision Commissioner under

For translation purpose only Official language is Thai language

For translation purpose only Official language is Thai language Ministerial Regulation No. 126, (B.E. 2509) Issued under the Revenue Code Regarding Revenue Tax Exemption By virtue of Section 4 and Section

For translation purpose only Official language is Thai language Ministerial Regulation No. 126, (B.E. 2509) Issued under the Revenue Code Regarding Revenue Tax Exemption By virtue of Section 4 and Section

MH CHEONG & ASSOCIATES CERTIFIED PUBLIC ACCOUNTANTS

Vol. 1 ISSUE 1 October 98 1999 MALAYSIAN BUDGET COMMENTARY The Malaysian Prime Minister and First Finance Minister, Dato Seri Dr Mahathir Bin Mohamad delivered his 1999 budget Statement to Parliament on

Vol. 1 ISSUE 1 October 98 1999 MALAYSIAN BUDGET COMMENTARY The Malaysian Prime Minister and First Finance Minister, Dato Seri Dr Mahathir Bin Mohamad delivered his 1999 budget Statement to Parliament on

ARAB REPUBLIC OF EGYPT

Public Disclosure Authorized CONFORMED COPY LOAN NUMBER 7396-EGT Public Disclosure Authorized Loan Agreement (Mortgage Finance Project) Public Disclosure Authorized between ARAB REPUBLIC OF EGYPT and INTERNATIONAL

Public Disclosure Authorized CONFORMED COPY LOAN NUMBER 7396-EGT Public Disclosure Authorized Loan Agreement (Mortgage Finance Project) Public Disclosure Authorized between ARAB REPUBLIC OF EGYPT and INTERNATIONAL

21:08 PREVIOUS CHAPTER

TITLE 21 Chapter 21:08 TITLE 21 PREVIOUS CHAPTER ZIMBABWE MINING DEVELOPMENT CORPORATION ACT Acts 31/1982, 29/1990 (s. 22), 3/1991, 22/2001. ARRANGEMENT OF SECTIONS PART I PRELIMINARY Section 1. Short

TITLE 21 Chapter 21:08 TITLE 21 PREVIOUS CHAPTER ZIMBABWE MINING DEVELOPMENT CORPORATION ACT Acts 31/1982, 29/1990 (s. 22), 3/1991, 22/2001. ARRANGEMENT OF SECTIONS PART I PRELIMINARY Section 1. Short

A requester submits a request to a financial. Approval and Reporting System (ECARS)

") PUBLIC HANDBOOK Service Consideration of Requests under the Exchange Control Act Responsible Unit Approval Team, Foreign Exchange Administration and Policy Department, Bank of Thailand (BOT) Scope of Service

PUBLIC HANDBOOK Service Consideration of Requests under the Exchange Control Act Responsible Unit Approval Team, Foreign Exchange Administration and Policy Department, Bank of Thailand (BOT) Scope of Service

Effective date : 01 January 2015 for all new and existing customers of HSBC. Please contact your nearest HSBC branch if you require any clarification.

Edition : January 2015 Effective date : 01 January 2015 for all new and existing customers of HSBC Please take the time to read these Terms & Conditions as they are binding on you. By using the Business

Edition : January 2015 Effective date : 01 January 2015 for all new and existing customers of HSBC Please take the time to read these Terms & Conditions as they are binding on you. By using the Business

(COLLECTIVELY REFERRED TO AS THE PROPOSED REGULARISATION PLAN )

") PERISAI PETROLEUM TEKNOLOGI BHD ( PPTB OR THE COMPANY ) (I) PROPOSED SHARE CAPITAL REDUCTION AND CONSOLIDATION; (II) PROPOSED FUND RAISING EXERCISE; (III) PROPOSED DEBT SETTLEMENT; (IV) PROPOSED SHARE

PERISAI PETROLEUM TEKNOLOGI BHD ( PPTB OR THE COMPANY ) (I) PROPOSED SHARE CAPITAL REDUCTION AND CONSOLIDATION; (II) PROPOSED FUND RAISING EXERCISE; (III) PROPOSED DEBT SETTLEMENT; (IV) PROPOSED SHARE

Module Content Guide. Taxation (TAX)

") Module Content Guide (TAX) All our rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted, in any form or by any means, electronic, mechanical, photocopying,

Module Content Guide (TAX) All our rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted, in any form or by any means, electronic, mechanical, photocopying,

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION DECEMBER 2011 Suggested Answer

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION DECEMBER 2011 Suggested Answer

Paper P6 (MYS) Advanced Taxation (Malaysia) Monday 6 June Professional Level Options Module. The Association of Chartered Certified Accountants

Advanced Taxation (Malaysia) Monday 6 June Professional Level Options Module. The Association of Chartered Certified Accountants") Professional Level Options Module Advanced Taxation (Malaysia) Monday 6 June 2011 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Professional Level Options Module Advanced Taxation (Malaysia) Monday 6 June 2011 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

THE EXPORT-IMPORT BANK OF KOREA Principal Terms and Conditions of the Medium Term Note Programme of up to RM1.0 Billion

THE EXPORT-IMPORT BANK OF KOREA Principal Terms and Conditions of the Medium Term Note Programme of up to RM1.0 Billion Background Information Issuer Name : The Export-Import Bank of Korea ( KEXIM ) Address

THE EXPORT-IMPORT BANK OF KOREA Principal Terms and Conditions of the Medium Term Note Programme of up to RM1.0 Billion Background Information Issuer Name : The Export-Import Bank of Korea ( KEXIM ) Address

SONOMA COUNTY COMMUNITY DEVELOPMENT COMMISSION

SONOMA COUNTY COMMUNITY DEVELOPMENT COMMISSION LOAN POLICIES Affordable Housing Development Affordable Housing Acquisition & Preservation Multi-family Housing Rehabilitation Community Facilities Table

SONOMA COUNTY COMMUNITY DEVELOPMENT COMMISSION LOAN POLICIES Affordable Housing Development Affordable Housing Acquisition & Preservation Multi-family Housing Rehabilitation Community Facilities Table

Structuring Investments into Malaysia Tax Issues

Structuring Investments into Malaysia Tax Issues December 2011 Dr. Veerinderjeet Singh 2 Agenda 3 Overview of Malaysia Corporate Tax Tax Incentives Other Taxes Example: Malaysia as a Holding Company Labuan

Structuring Investments into Malaysia Tax Issues December 2011 Dr. Veerinderjeet Singh 2 Agenda 3 Overview of Malaysia Corporate Tax Tax Incentives Other Taxes Example: Malaysia as a Holding Company Labuan

RAMCO SYSTEMS SDN. BHD. (Formerly known as Ramcosystems Sdn. Bhd.) Company No.: W (Incorporated in Malaysia)

Company No.: W (Incorporated in Malaysia)") RAMCO SYSTEMS SDN. BHD. (Formerly known as Ramcosystems Sdn. Bhd.) Company No.: 342313W (Incorporated in Malaysia) FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2018 1 RAMCO SYSTEMS SDN. BHD. (Formerly

RAMCO SYSTEMS SDN. BHD. (Formerly known as Ramcosystems Sdn. Bhd.) Company No.: 342313W (Incorporated in Malaysia) FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2018 1 RAMCO SYSTEMS SDN. BHD. (Formerly

MEGA ALT ARM (MA5/1)

") MEGA ALT ARM (MA5/1) Product Description General Loan Production Descriptions (Asset Qualifier) Product Description Eligible Property Type Eligible States Index Term Margin/Floor/Caps Income/Employment

MEGA ALT ARM (MA5/1) Product Description General Loan Production Descriptions (Asset Qualifier) Product Description Eligible Property Type Eligible States Index Term Margin/Floor/Caps Income/Employment

STANDARD MORTGAGE TERMS. Filed By: PARADIGM QUEST INC. Filing Date: November 30, Filing Number: MT070114

STANDARD MORTGAGE TERMS Filed By: PARADIGM QUEST INC. Filing Date: November 30, 2007 Filing Number: MT070114 These STANDARD MORTGAGE TERMS shall be deemed to be included in every Mortgage which incorporates

STANDARD MORTGAGE TERMS Filed By: PARADIGM QUEST INC. Filing Date: November 30, 2007 Filing Number: MT070114 These STANDARD MORTGAGE TERMS shall be deemed to be included in every Mortgage which incorporates

: Review of Corporate Income Tax Rate for Small and Medium Enterprises (SME)

") Appendix 1 Appendix 2 Appendix 3 Appendix 4 Appendix 5 Appendix 6 Appendix 7 TAX MEASURES : Review of Corporate Income Tax Rate for Small and Medium Enterprises (SME) : Review of Income Tax Treatment on

Appendix 1 Appendix 2 Appendix 3 Appendix 4 Appendix 5 Appendix 6 Appendix 7 TAX MEASURES : Review of Corporate Income Tax Rate for Small and Medium Enterprises (SME) : Review of Income Tax Treatment on

Professional Level Options Module, Paper P6 (CYP) 1 Memorandum

1 Memorandum") Answers Professional Level Options Module, Paper P6 (CYP) Advanced Taxation (Cyprus) June 2017 Answers 1 Memorandum To: Tax partner From: Tax assistant Date: 31 August 2016 Client: Anna Protos, Protos

Answers Professional Level Options Module, Paper P6 (CYP) Advanced Taxation (Cyprus) June 2017 Answers 1 Memorandum To: Tax partner From: Tax assistant Date: 31 August 2016 Client: Anna Protos, Protos

Session of SENATE BILL No. 20. By Committee on Financial Institutions and Insurance 1-12

Session of SENATE BILL No. By Committee on Financial Institutions and Insurance - 0 0 AN ACT concerning financial institutions; relating to the state banking code; amending K.S.A. Supp. -0, -0, -0 and

Session of SENATE BILL No. By Committee on Financial Institutions and Insurance - 0 0 AN ACT concerning financial institutions; relating to the state banking code; amending K.S.A. Supp. -0, -0, -0 and

1. HSBC Bank Malaysia Berhad (Company No V) will be referred to as HSBC Bank.

will be referred to as HSBC Bank.") HSBC Cash Instalment Plan Programme Terms & Conditions (June 2016 Edition) Notice is hereby given pursuant to Clause 26 below that interest on the Cash Instalment Plan will not be counted towards reduction

HSBC Cash Instalment Plan Programme Terms & Conditions (June 2016 Edition) Notice is hereby given pursuant to Clause 26 below that interest on the Cash Instalment Plan will not be counted towards reduction

BNM TARGET LENDING TO THE PRIORITY SECTOR HOUSING LOAN PRODUCT DISCLOSURE SHEET

BNM TARGET LENDING TO THE PRIORITY SECTOR HOUSING LOAN PRODUCT DISCLOSURE SHEET Bank : Affin Bank Berhad Product : BNM Target Lending to the Priority Sector Housing Loan Date : 20 February 2018 1. What

BNM TARGET LENDING TO THE PRIORITY SECTOR HOUSING LOAN PRODUCT DISCLOSURE SHEET Bank : Affin Bank Berhad Product : BNM Target Lending to the Priority Sector Housing Loan Date : 20 February 2018 1. What

Brief Guide on Doing Business in Malaysia

Brief Guide on Doing Business in Malaysia Several exciting developments have taken place in the Malaysian corporate landscape, including the liberalisation of sectors, which were traditionally somewhat

Brief Guide on Doing Business in Malaysia Several exciting developments have taken place in the Malaysian corporate landscape, including the liberalisation of sectors, which were traditionally somewhat

GUIDELINES ON THE ESTABLISHMENT OF LABUAN INTERNATIONAL COMMODITY TRADING COMPANY UNDER THE GLOBAL INCENTIVES FOR TRADING PROGRAMME

GUIDELINES ON THE ESTABLISHMENT OF LABUAN INTERNATIONAL COMMODITY TRADING COMPANY UNDER THE GLOBAL INCENTIVES FOR TRADING PROGRAMME 1.0 Introduction 1.1 The Guidelines on the Establishment of Labuan International

GUIDELINES ON THE ESTABLISHMENT OF LABUAN INTERNATIONAL COMMODITY TRADING COMPANY UNDER THE GLOBAL INCENTIVES FOR TRADING PROGRAMME 1.0 Introduction 1.1 The Guidelines on the Establishment of Labuan International

Subordinated Class E Sukuk Ijarah

(i) Profit rental rate : Senior Class Sukuk Ijarah The profit rental rate of any Senior Class Sukuk Ijarah issued under the Sukuk Ijarah Programme shall be based on a fixed rate to be determined prior

(i) Profit rental rate : Senior Class Sukuk Ijarah The profit rental rate of any Senior Class Sukuk Ijarah issued under the Sukuk Ijarah Programme shall be based on a fixed rate to be determined prior

Investment Management Mandate

Investment Management Mandate This Investment Mandate authorises Merchant West Capital Markets (Pty) Ltd; Registration Number 1999/000113/07 (hereinafter referred to as Merchant West) to make investment

Investment Management Mandate This Investment Mandate authorises Merchant West Capital Markets (Pty) Ltd; Registration Number 1999/000113/07 (hereinafter referred to as Merchant West) to make investment

Classic Home Loans, Bridge Loans, APlus Accounts and Personal Loans secured by residential immovable property to residents of Malta

Pre-contractual General Information Sheet Classic Home Loans, Bridge Loans, APlus Accounts and Personal Loans secured by residential immovable property to residents of Malta 1. Lender identity, geographical

Pre-contractual General Information Sheet Classic Home Loans, Bridge Loans, APlus Accounts and Personal Loans secured by residential immovable property to residents of Malta 1. Lender identity, geographical

FAIR TRADING (RETIREMENT VILLAGES INTERIM CODE) REGULATIONS 2018

REGULATIONS 2018") Westrn Australia Fair Trading Act 2010 FAIR TRADING (RETIREMENT VILLAGES INTERIM CODE) REGULATIONS 2018 GOVERNMENT GAZETTE, WA 29 March 2018 Retirement Villages Interim Code 2018 Page 1 As at 1 April 2018

Westrn Australia Fair Trading Act 2010 FAIR TRADING (RETIREMENT VILLAGES INTERIM CODE) REGULATIONS 2018 GOVERNMENT GAZETTE, WA 29 March 2018 Retirement Villages Interim Code 2018 Page 1 As at 1 April 2018

Mobility matters The essential UK tax guide for individuals on international assignment abroad

www.pwc.co.uk Mobility matters The essential UK tax guide for individuals on international assignment abroad December 2017 Contents 1 Determining your UK tax liability 1.1 What impact will my overseas

www.pwc.co.uk Mobility matters The essential UK tax guide for individuals on international assignment abroad December 2017 Contents 1 Determining your UK tax liability 1.1 What impact will my overseas