Conterra Ag Capital. Providing industry leading agricultural loan servicing and wholesale lending to lending partners nationwide

|

|

|

- Wilfred Jones

- 5 years ago

- Views:

Transcription

1

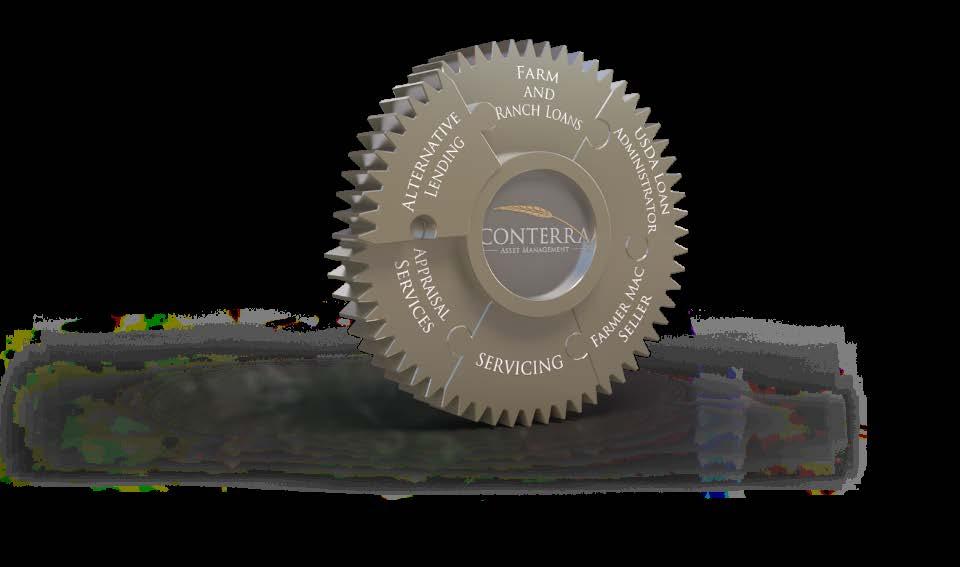

2 Conterra Ag Capital Conterra supports American Agriculture through creative financial solutions. Providing industry leading agricultural loan servicing and wholesale lending to lending partners nationwide Focused solely on agriculture Experienced team of ag finance professionals Headquartered in Des Moines, Iowa National footprint $2.8 billion of assets 2

3 Conterra Across America Home office: West Des Moines, Iowa Field Offices: Missouri, Illinois, North Carolina, Arizona, and Oregon 3

4 Conterra Ag Capital Our understanding of agricultural finance has driven us to develop knowledge-based lending programs that offer tailored solutions for borrowers across the risk spectrum. Traditional Lending Alternative Lending Specialized Lending 4

5 Financing Options Traditional Farm & Ranch CR 1.25:1 TDC 1.25:1 LTV% < 65% DA% 50% Alternative Fund CR 1.0:1 TDC 1.10:1 LTV < 65% DA% 60% Specialized Fund Collateral Coverage EBITDA Coverage *A list of abbreviations can be found on slide 12: Underwriting Guidelines 5

6 Farmer Mac Seller and Central Servicer

7 Farmer Mac Loans Farmer Mac Seller Loan packaging with no additional fee Non-Farmer Mac Seller Sell to Farmer Mac through Conterra 7

8 Alternative/Specialized Lending

9 Alternative Lending Conterra has established several funds with a focus on loans that do not meet traditional lending standards Transitional financing Debt restructures Bridge loans and special circumstances All Conterra Fund loans are held in portfolio and managed by Conterra 9

10 Conterra Fund The predominant alternative lending program and is intended as transitional finance: Loans are secured by first mortgages on ag real estate Can take a subordinate position to Farmer Mac for loans Loan size range from $500,000 - $10,000,000 Working capital can be built into the structure Analysis weighted on post-close financials and a supported proforma Lending partner shares in origination fees and field servicing fees over the life of the loan 10

11 Rates and Terms Conterra Fund loans are individually priced, recognizing the circumstances of each borrower Loans are priced to risk Up to 5-year terms, variable or fixed rates Monthly, quarterly, semi-annual payment frequencies Amortizations up to 30 years, level principal payments or interest-only options All loans require a first lien position on agricultural real estate, or second lien position behind Farmer Mac 11

12 Conterra Fund Underwriting Guidelines Current Ratio (CR): 1.0:1 Debt to Asset Ratio (DA): <60% Total Debt Coverage Ratio(TDC): 1.1:1 Loan to Value (LTV): 65% FICO(all borrowers): 660 Primary Residence of Total Appraised Value: 30% It is preferred the Borrower be a legal entity and the majority of collateral must be owned by the entity May include case-specific covenants 12

13 Partnership with Conterra Referral Relationship Introduce the borrower to Conterra Conterra pays a portion of the origination fee to the lending partner Correspondent Relationship Gather financial information from borrower Write narrative Collect information per loan covenants Inspections (as requested) Conterra splits origination fee with the lender and pays field servicing over the life of the loan 13

14 How We Enhance Your Business: Manage Credit Risk Additional Product Offering Fee Income Customer Retention 14

15 Benefits to Lender: Manage credit risk and improve portfolio quality All Conterra loans are held in portfolio and managed by Conterra Conterra finances real estate, lender retains operating loans and other business with the client Fee income through shared origination fees and servicing fees Online portal that allows lender to monitor the loan s performance Custom billing options allow you to stay in front of your customer 15

16 How it Works: 1. Lender submits loan application and supporting documents 2. Conterra reviews and underwrites 3. Conterra holds Credit Committee for loan approval 4. Upon approval, a Preliminary Loan Approval (PLA) will be issued by Conterra 5. Borrower agrees to terms and conditions set forth in PLA, signs and returns to Conterra 6. Borrower remits due diligence fee 7. Conterra orders USPAP-conforming appraisal and title 8. Conterra reviews title and appraisal 9. Conterra completes all loan documentation and schedules closing 10. Loan closes in the name of Conterra Agricultural Capital LLC 11. Conterra services loan and sends billing 12. Field servicing fees are paid to Lender upon payment received from Borrower 16

17 Required Documents for Application Conterra Loan Application Loan Application Proof of Identification Credit Authorization Form Financial Information Balance Sheet Audited Financial statements (3 yrs min) Tax Returns (3 yrs min) Proforma Income and Expense Credit Verifications Paystubs or W2 for offfarm income (2 most recent) Balance statements from major lenders Asset verifications Access Loan Application and Checklist at Contact underwriting team for assistance. 17

18 Conterra Fund Loan Example Midwest Operation (at submission) Loan Amount: $2,381,978 Loan to Value: 24.34% Current Ratio: 0.94 Debt-to-Asset Ratio: 29.39% Avg TDC Ratio:.75 FICO: 656,716,702,641,734 Situation: A debt restructure will reduce the annual total principal and interest. This will help relieve cash flow pressures and consolidate outstanding debt, as only an operating note will remain outside of the Conterra note. Midwest Operation (post-close) Loan Amount: $4,000,000 Loan to Value: 51.84% Current Ratio: 3.63 Debt-to-Asset Ratio: 29.91% TDC Ratio: 2.01 Terms: 7.25% fixed, 3-year balloon, interest only, semi-annual payment Collateral for this loan consists of +/- 2,470 acres. 18

19 Midwest Operation Use of Proceeds: Refinance Real Estate - $2,475,697 Refinance Non-Real Estate - $1,446,769 Working Capital - $18,128 Closing Fees - $20,000 Origination Fees - $39,406 Correspondent received 0.50% field servicing fee and a 50/50 split of origination 19

20 Story: Midwest Operation Years of profitability had led the applicants to expand their equipment line in order to utilize depreciation to their limit tax liability. The operation was hindered by falling commodity prices and the additional cost of bringing the owner s children into the operation. The operation showed sufficient cash flow in 2013 and 2016 to service the proposed debt restructure. Two years of losses in 2014 and Losses were largely attributed to poor wheat yields and an expanding equipment line. Leading their existing operating lender to sweep crop proceeds and not renew the line in cash flow showed improvement from the previous two years and harvested crop inventories expanded. Similar yields were expected in A restructure of equipment debt onto the real estate created a $300,000+ reduction in annual debt service obligations. 20

21 Midwest Operation Conditions Prior to Funding First lien on real estate Appraisal providing a loan-tovalue of 52% or below Operating commitment from bank with terms acceptable to Conterra Other standard conditions and review of entity and trust documents Loan Covenants Borrowers to maintain compliance with all environmental and regulatory lays Borrowers are required to receive written approval from lender for all annual capital expenditures, in total exceeding $50,000 Borrowers and guarantors to provide lender with annual financial statements within 90 days of year-end Other standard covenants 21

22 Conterra Fund Loan Example Northwest Livestock (at submission) Loan Amount: $2,581,046 Loan to Value: 56.97% Current Ratio:.74 Debt to Asset Ratio: 58.5% Avg TDC Ratio:.86 FICO: 728,775, 700, 733 Situation: There was a large amount of equipment debt for this size of operation. Need to refinance real estate, operating debt and carryover losses. The operation is at capacity for cattle allowing them to maximize their fixed asset base and cash flow post restructure. Northwest Livestock (post-close) Loan Amount: $2,944,500 Loan to Value: 65% Current Ratio: 1.03 Debt to Asset Ratio: 59% Avg TDC Ratio: 1.67 Terms: 7.75% gross rate, 3-year fixed, 2-year extension upon credit review, 25-year amortization, semiannual pay 22

23 Use of Proceeds Northwest Livestock Refinance Real Estate - $2,581,046 Refi Non-Real Estate -$314,004 Closing Fees - $20,000 Origination Fees - $29,450 Correspondent received 0.25% field servicing fee and a 50/50 split of origination 23

24 Northwest Livestock Financial Highlights: Working capital was tight, however, this risk was mitigated by bank s willingness to extend more commitment if needed through a fully budgeted operating line. Leverage was also higher than ideal but manageable and is expected to improve as the borrowers pay down the operating loss carryover through a 7-year amortization period. The payoff of equipment through the combined loans from Conterra and the bank decreases the demand on the borrower s cash flow, improving the projected TDC. Projected income is reasonable as the area is receiving full water allocations and beef prices have increased over the past year. 24

25 Northwest Livestock Conditions: A qualified appraisal indicating a LTV of 65% or less 1 st lien position on subject property The collateral to be vested in an entity that will be liable on the note. Note is cross defaulted with bank The 3-year term has an annual requalification, if Bank pulls out of operating, Conterra s note becomes due and payable. Conterra s note is contingent upon the approval of the Bank s renewed operating line and restructure of $1 million of the current operating line. Loan Covenants: Conterra to receive a copy of the fully budgeted operating line from Bank each year. Non-Monetary default will result in a 2.50% interest rate increase. 25

26 Conterra Contacts Paul Erickson President & CEO Office: (515) Cell: (515) Nick Stokes Senior Vice President/Managing Director Cell: (217) Toll Free: (855) Tom Stenson Executive Vice President Cell: (828) Toll Free: (855) TJ Roemmich VP Credit Administration Office: (515) Cell: (515) David Denos VP Western Region Cell: (541) Toll Free: (855) (855)

27 Contact Us For More Information Visit: ConterraAg.com Call: (855)

Top 10 Questions to Ask Your Farm Customer!

Farmer Mac Refresh Top 10 Questions to Ask Your Farm Customer! July 2012 Today s Presenters Mike Juergens, Manager, Underwriting Department, Johnston, IA., Michael_Juergens@farmermac.com, 866 452 2617.

Farmer Mac Refresh Top 10 Questions to Ask Your Farm Customer! July 2012 Today s Presenters Mike Juergens, Manager, Underwriting Department, Johnston, IA., Michael_Juergens@farmermac.com, 866 452 2617.

Refresh Webinar Road Show November 19, 2015

Refresh Webinar Road Show 2015 November 19, 2015 Welcome and Introductions Today s Presenters Patrick Kerrigan Director - Business Development Washington, DC pkerrigan@farmermac.com Jim Soppe Assistant

Refresh Webinar Road Show 2015 November 19, 2015 Welcome and Introductions Today s Presenters Patrick Kerrigan Director - Business Development Washington, DC pkerrigan@farmermac.com Jim Soppe Assistant

Refresh Webinar Series: 2018 Road Show Rundown

Refresh Webinar Series: 2018 Road Show Rundown Today s Presenters Larry Jones, Senior Relationship Manager Washington, D.C. Headquarters Phone: 202-872-6604 Scott Steveson, Assistant Manager Credit and

Refresh Webinar Series: 2018 Road Show Rundown Today s Presenters Larry Jones, Senior Relationship Manager Washington, D.C. Headquarters Phone: 202-872-6604 Scott Steveson, Assistant Manager Credit and

Exploring Farm Service Agency Loan Opportunities

Exploring Farm Service Agency Loan Opportunities Refresh Webinar May 2015 Today s Agenda Farm Service Agency Update Randi Sheffer, Guaranteed Loan Branch Chief Jeff King, Loan Servicing Observations from

Exploring Farm Service Agency Loan Opportunities Refresh Webinar May 2015 Today s Agenda Farm Service Agency Update Randi Sheffer, Guaranteed Loan Branch Chief Jeff King, Loan Servicing Observations from

Farmer Mac Refresh: Helpful Hints for Your Farm & Ranch and USDA Guaranteed Loans. February 14, 2018

Farmer Mac Refresh: Helpful Hints for Your Farm & Ranch and USDA Guaranteed Loans February 14, 2018 Today s Presenters Mark Rickels Johnston, Ia. (202) 872-6611 mrickels@farmermac.com John Krummel Senior

Farmer Mac Refresh: Helpful Hints for Your Farm & Ranch and USDA Guaranteed Loans February 14, 2018 Today s Presenters Mark Rickels Johnston, Ia. (202) 872-6611 mrickels@farmermac.com John Krummel Senior

Underwriting Guideline Matrix

: Program / Product Codes: 30 Year Fixed (W130) 15 Year Fixed (W132) Subject to Change Without Notice Valid as of: 12/18/2017 Copyright 2017 Skyline Financial Corp. dba NewLeaf Wholesale, Nationwide Mortgage

: Program / Product Codes: 30 Year Fixed (W130) 15 Year Fixed (W132) Subject to Change Without Notice Valid as of: 12/18/2017 Copyright 2017 Skyline Financial Corp. dba NewLeaf Wholesale, Nationwide Mortgage

Mark Rickels Relationship Manager, Johnston, Ia.,

Michael Juergens Chief Underwriter, Johnston, Ia., 866-452-2617 Michael_Juergens@farmermac.com Mark Rickels Relationship Manager, Johnston, Ia., 202-872-6611 Mark_Rickels@farmermac.com 2 1 10 important

Michael Juergens Chief Underwriter, Johnston, Ia., 866-452-2617 Michael_Juergens@farmermac.com Mark Rickels Relationship Manager, Johnston, Ia., 202-872-6611 Mark_Rickels@farmermac.com 2 1 10 important

USDA Guaranteed Loan Secondary Market Update

USDA Guaranteed Loan Secondary Market Update Refresh Webinar May 2017 Today s Presenters Patrick Kerrigan VP - Business Development Washington, DC 800.879.3276 x5560 pkerrigan@farmermac.com Riley Croghan

USDA Guaranteed Loan Secondary Market Update Refresh Webinar May 2017 Today s Presenters Patrick Kerrigan VP - Business Development Washington, DC 800.879.3276 x5560 pkerrigan@farmermac.com Riley Croghan

AG-AMERICA COMMERCIAL FARM AND RANCH LOAN APPROVAL GUIDE

AG-AMERICA COMMERCIAL FARM AND RANCH Table of Contents CHAPTER 301 LOAN APPROVAL OVERVIEW... 1 301.1 Preliminary Loan Approval... 1 Credit Standards... 1 302.2 Preliminary Loan Approval... 1 1. Loan Application...

AG-AMERICA COMMERCIAL FARM AND RANCH Table of Contents CHAPTER 301 LOAN APPROVAL OVERVIEW... 1 301.1 Preliminary Loan Approval... 1 Credit Standards... 1 302.2 Preliminary Loan Approval... 1 1. Loan Application...

Portfolio Product Review

Farmer Mac Refresh Portfolio Product Review May 19, 2016 Solutions Ag Bankers Trust Transactions types available to Farmer Mac approved Sellers: Loan purchases Transfer of credit and ALM risk from lender

Farmer Mac Refresh Portfolio Product Review May 19, 2016 Solutions Ag Bankers Trust Transactions types available to Farmer Mac approved Sellers: Loan purchases Transfer of credit and ALM risk from lender

Agribusiness Lending Internal Control Questionnaire

Agribusiness Lending Internal Control Questionnaire Completed by: Date Completed: 1. Has the institution established policies that are appropriate for the complexity and scope of the agricultural lending

Agribusiness Lending Internal Control Questionnaire Completed by: Date Completed: 1. Has the institution established policies that are appropriate for the complexity and scope of the agricultural lending

AG-AMERICA COMMERCIAL FARM AND RANCH LENDING GUIDE

AG-AMERICA COMMERCIAL FARM AND RANCH Table of Contents 201 GENERAL OVERVIEW - CREDIT STANDARDS AND GUIDES... 1 Responsibility at Loan Origination... 1 Age of Documents... 1 Summary... 1 Farm and Ranch

AG-AMERICA COMMERCIAL FARM AND RANCH Table of Contents 201 GENERAL OVERVIEW - CREDIT STANDARDS AND GUIDES... 1 Responsibility at Loan Origination... 1 Age of Documents... 1 Summary... 1 Farm and Ranch

Texas Cash-out Program Guide Fixed Rate

Texas Cash-out Program Guide Fixed Rate Wholesale Lending July 20, 2015 Program Overview... 2 Employee Loan Policy... 2 Credit Philosophy... 2 Ability to Repay and Qualified Mortgage... 2 Program Parameters...

Texas Cash-out Program Guide Fixed Rate Wholesale Lending July 20, 2015 Program Overview... 2 Employee Loan Policy... 2 Credit Philosophy... 2 Ability to Repay and Qualified Mortgage... 2 Program Parameters...

2018 ICBA Regulator Panel Agricultural Lending

2018 ICBA Regulator Panel Agricultural Lending March 15, 2018 Keith Osborne ADC Wichita Field Office 1 Agenda Agricultural Lending Risk Management Practices Risk Rating Agricultural Loans References Questions

2018 ICBA Regulator Panel Agricultural Lending March 15, 2018 Keith Osborne ADC Wichita Field Office 1 Agenda Agricultural Lending Risk Management Practices Risk Rating Agricultural Loans References Questions

APPENDIX B - CONSUMER LOAN POLICY. Table of Contents

APPENDIX B - CONSUMER LOAN POLICY Table of Contents 1. CONSUMER LOAN POLICY... 1 2. STANDARD UNDERWRITING... 1 3. REFERRAL SOURCES... 4 4. UNDERWRITING OF EXISTING LOANS:... 4 5. UNDERWRITING LOAN POLICY

APPENDIX B - CONSUMER LOAN POLICY Table of Contents 1. CONSUMER LOAN POLICY... 1 2. STANDARD UNDERWRITING... 1 3. REFERRAL SOURCES... 4 4. UNDERWRITING OF EXISTING LOANS:... 4 5. UNDERWRITING LOAN POLICY

Jumbo Non-Conforming Products (Series-49)

") Jumbo Non-Conforming Products (Series-49) This guide provides parameters for standard fixed rate and 5/1, 7/1, and 10/1 adjustable rate, fully amortizing, nonconforming products for primary residence up

Jumbo Non-Conforming Products (Series-49) This guide provides parameters for standard fixed rate and 5/1, 7/1, and 10/1 adjustable rate, fully amortizing, nonconforming products for primary residence up

Associated Non-Conforming Adjustable Rate Mortgage Program TPO Originations

1. Product Description Associated Bank s Non-Conforming ARM Program allows Associated to offer customized underwriting solutions based on the borrower s individual credit with Associated Bank and other

1. Product Description Associated Bank s Non-Conforming ARM Program allows Associated to offer customized underwriting solutions based on the borrower s individual credit with Associated Bank and other

LOAN REGISTRATION Type In Form Note: Partial Packages Will NOT Be Reviewed!

LOAN REGISTRATION Type In Form Note: Partial Packages Will NOT Be Reviewed! (Check One) Borrower Broker/Banker Contact Name Date Company Phone Cell Address Fax City, State, Zip: E-Mail Borrower Information

LOAN REGISTRATION Type In Form Note: Partial Packages Will NOT Be Reviewed! (Check One) Borrower Broker/Banker Contact Name Date Company Phone Cell Address Fax City, State, Zip: E-Mail Borrower Information

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Conforming Balance Primary Residence

Texas Cash-Out Program Conforming Balance Summary Product Types 30yr & 15yr Fixed Only For Conforming Loan Amounts, view State/County limits: https://www.fanniemae.com/singlefamily/loan-limits Conforming

Texas Cash-Out Program Conforming Balance Summary Product Types 30yr & 15yr Fixed Only For Conforming Loan Amounts, view State/County limits: https://www.fanniemae.com/singlefamily/loan-limits Conforming

") ; LOAN AMOUNTS

; LOAN AMOUNTS CONFORMING PRODUCTS: Eligible on Mammoth, Acadia, Cascades and Yosemite. ARM Rate ( Purchase & Rate/Term Refinances)-Fannie Mae DU

-Fannie Mae DU") CONFORMING PRODUCTS: Eligible on Mammoth, Acadia, Cascades and Yosemite Fixed Rate (Purchase & Rate/Term Refinances) Fannie Mae DU Occupancy Owner Occupied Second Home Investment Property Property Type

CONFORMING PRODUCTS: Eligible on Mammoth, Acadia, Cascades and Yosemite Fixed Rate (Purchase & Rate/Term Refinances) Fannie Mae DU Occupancy Owner Occupied Second Home Investment Property Property Type

Non-Agency Jumbo 5/1 LIBOR ARM PRODUCT CODE A512

Product Overview: This is a variable rate mortgage product, without negative amortization, whereby the interest rate and payment is adjusted in accordance with the specified index. Index: The index used

Product Overview: This is a variable rate mortgage product, without negative amortization, whereby the interest rate and payment is adjusted in accordance with the specified index. Index: The index used

RESIDENTIAL CONSTRUCTION LENDING POLICY

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

RESIDENTIAL CONSTRUCTION LENDING POLICY GENERAL INFORMATION The purpose of this policy is to state different types of construction loans offered by ASSURANCE FINANCIAL, and to set forth procedures and

Monday, June 19, 2017 Ag Law Rooms: Ag Lien Update: Loan Workout Concerns and Lender Liability Issues in Today s Ag Economy 3:15 p.m.

Monday, June 19, 2017 Ag Law Rooms: 312-313 Ag Lien Update: Loan Workout Concerns and Lender Liability Issues in Today s Ag Economy 3:15 p.m. 4:15 p.m. Presented by Robert Hartwig Legal Counsel Iowa Bankers

Monday, June 19, 2017 Ag Law Rooms: 312-313 Ag Lien Update: Loan Workout Concerns and Lender Liability Issues in Today s Ag Economy 3:15 p.m. 4:15 p.m. Presented by Robert Hartwig Legal Counsel Iowa Bankers

CRA PORTFOLIO NON-CONFORMING PROGRAM

LOAN PROGRAM:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 2 AGE OF DOCUMENTS:... 3 APPRAISAL REQUIREMENTS:... 3 ASSUMABILITY:...

LOAN PROGRAM:... 2 LOCK-IN/REGISTRATION:... 2 MINIMUM MORTGAGE:... 2 MAXIMUM MORTGAGE:... 2 MAXIMUM LTV/CLTV:... 2 ADDITIONAL CONSIDERATIONS:... 2 AGE OF DOCUMENTS:... 3 APPRAISAL REQUIREMENTS:... 3 ASSUMABILITY:...

AgriBank, FCB. Quarterly Report September 30, 2007 MANAGEMENT'S DISCUSSION AND ANALYSIS

Quarterly Report September 30, 2007 Copies of quarterly and annual reports are available upon request by contacting, 375 Jackson Street, St. Paul, Minnesota 55101-1810 or by calling (651) 282-8800. Reports

Quarterly Report September 30, 2007 Copies of quarterly and annual reports are available upon request by contacting, 375 Jackson Street, St. Paul, Minnesota 55101-1810 or by calling (651) 282-8800. Reports

CONFORMING UNDERWRTING GUIDELINES DUREFIPLUS PROGRAM - WHOLESALE

Table of Contents APPRAISAL & PROPERTY INFORMATION.... 2 Appraisal Requirements... 2 LTVs > 95%..... 3 Property Inspection Waiver (Property Field work Waiver Requirements).... 3 ELIGIBLE PROPERTIES...

Table of Contents APPRAISAL & PROPERTY INFORMATION.... 2 Appraisal Requirements... 2 LTVs > 95%..... 3 Property Inspection Waiver (Property Field work Waiver Requirements).... 3 ELIGIBLE PROPERTIES...

Adjustable Rate Mortgages (ARMs) Farm and Ranch Loans

Farm and Ranch Loans") Adjustable Rate Mortgages (ARMs) Farm and Ranch Loans 1-Month, 1-Year, 3-Year, 5-Year, 7/1, 10/1 ARMs. All ARMs have 15-year maturities and amortizations of either 15 or 25 years. The initial interest

Adjustable Rate Mortgages (ARMs) Farm and Ranch Loans 1-Month, 1-Year, 3-Year, 5-Year, 7/1, 10/1 ARMs. All ARMs have 15-year maturities and amortizations of either 15 or 25 years. The initial interest

Increase (Decrease) in For the nine months ended September 30, Net Income

in For the nine months ended September 30, Net Income") Copies of quarterly and annual reports are available upon request by contacting AgriBank, FCB, 30 E. 7th Street, Suite 1600, St. Paul, MN 55101 or by calling (651) 282-8800. Reports are also available

Copies of quarterly and annual reports are available upon request by contacting AgriBank, FCB, 30 E. 7th Street, Suite 1600, St. Paul, MN 55101 or by calling (651) 282-8800. Reports are also available

WHY WE AREN T LIKELY TO SEE A REPLAY OF THE 1980s FARM CRISIS

WHY WE AREN T LIKELY TO SEE A REPLAY OF THE 1980s FARM CRISIS Wendong Zhang Assistant Professor, Dept. of Economics Iowa State University Why We Aren t Likely to See A Replay of 1980s Farm Crisis Dr. Wendong

WHY WE AREN T LIKELY TO SEE A REPLAY OF THE 1980s FARM CRISIS Wendong Zhang Assistant Professor, Dept. of Economics Iowa State University Why We Aren t Likely to See A Replay of 1980s Farm Crisis Dr. Wendong

Product Guidelines Freddie Mac Relief Refinance - Open Access

; Important Note: The program has been extended to allow application received dates on or before December 31, 2018 and settlement dates on or before September 30, 2019. Occupancy 1-4 Units 1-4 Units Max

; Important Note: The program has been extended to allow application received dates on or before December 31, 2018 and settlement dates on or before September 30, 2019. Occupancy 1-4 Units 1-4 Units Max

PennyMac Correspondent Group Open Access

PennyMac Correspondent Group Open Access 01.18.18 Overlays to Freddie Mac are underlined The new loan must have an application date on or before December 31, 2018. Mortgage Product Program Eligibility

PennyMac Correspondent Group Open Access 01.18.18 Overlays to Freddie Mac are underlined The new loan must have an application date on or before December 31, 2018. Mortgage Product Program Eligibility

CREDIT IN A CHANGING ENVIRONMENT. Rick Nelson Vice President, Agribusiness

CREDIT IN A CHANGING ENVIRONMENT Rick Nelson Vice President, Agribusiness 1 Who is 100,000 member co-op Headquartered in Louisville Kentucky 1,100 employees 95 offices in Kentucky, Tennessee, Ohio, Indiana

CREDIT IN A CHANGING ENVIRONMENT Rick Nelson Vice President, Agribusiness 1 Who is 100,000 member co-op Headquartered in Louisville Kentucky 1,100 employees 95 offices in Kentucky, Tennessee, Ohio, Indiana

Chapter 15 Real Estate Financing: Practice

Chapter 15 Real Estate Financing: Practice LECTURE OUTLINE: I. Introduction to the Real Estate Financing Market A. Federal Reserve System 1. Created to help maintain sound credit conditions 2. Helps counteract

Chapter 15 Real Estate Financing: Practice LECTURE OUTLINE: I. Introduction to the Real Estate Financing Market A. Federal Reserve System 1. Created to help maintain sound credit conditions 2. Helps counteract

Harnessing Our Strengths. Redefining Tomorrow. SEPTEMBER 30, 2012 QUARTERLY REPORT

Harnessing Our Strengths. Redefining Tomorrow. SEPTEMBER 30, 2012 QUARTERLY REPORT Copies of quarterly and annual reports are available upon request by contacting AgriBank, FCB, 30 E. 7th Street, Suite

Harnessing Our Strengths. Redefining Tomorrow. SEPTEMBER 30, 2012 QUARTERLY REPORT Copies of quarterly and annual reports are available upon request by contacting AgriBank, FCB, 30 E. 7th Street, Suite

Wholesale Lending DU Refi Plus 12/27/2013

Program Code Loan Description Program Type Loan_Type Program Code DU30-105 DU REFI 30 YR FIXED LTV 0-105 FIXED CONV DU20-105 DU REFI 20 YR FIXED LTV 0-105 FIXED CONV DU15-105 DU REFI 15 YR FIXED LTV 0-105

Program Code Loan Description Program Type Loan_Type Program Code DU30-105 DU REFI 30 YR FIXED LTV 0-105 FIXED CONV DU20-105 DU REFI 20 YR FIXED LTV 0-105 FIXED CONV DU15-105 DU REFI 15 YR FIXED LTV 0-105

PRODUCT GUIDELINES LENDER PAID MORTGAGE INSURANCE PROGRAM (LPMI) PROGRAM CODES: C30FLPMI, H30FLPMI

PROGRAM CODES: C30FLPMI, H30FLPMI") Occupancy Purpose Max Loan Amount Maximum LTV/ CLTV LOAN AMOUNTS

Occupancy Purpose Max Loan Amount Maximum LTV/ CLTV LOAN AMOUNTS

Guidelines Correspondent. Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits:

LTV Limits:") Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Second Home Investment & Non- Owner Property Type Condominiums are ineligible for this product.

Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Second Home Investment & Non- Owner Property Type Condominiums are ineligible for this product.

INSIGHTS FROM AGRICULTURAL LENDERS. January 11 th, 2019 Top Farmer Conference Beck Agricultural Center Dr. Brady Brewer

INSIGHTS FROM AGRICULTURAL LENDERS January 11 th, 2019 Top Farmer Conference Beck Agricultural Center Dr. Brady Brewer bebrewer@purdue.edu AGRICULTURAL LENDER SURVEY Survey expectations and past results

INSIGHTS FROM AGRICULTURAL LENDERS January 11 th, 2019 Top Farmer Conference Beck Agricultural Center Dr. Brady Brewer bebrewer@purdue.edu AGRICULTURAL LENDER SURVEY Survey expectations and past results

Credit Evaluation. Assessment of borrower capacity to repay the loan. Assessment of borrower s ability to bring in profits from operations.

Credit Evaluation Credit Evaluation Assessment of borrower capacity to repay the loan. Assessment of borrower s ability to bring in profits from operations. Assessment of project viability. Assessment

Credit Evaluation Credit Evaluation Assessment of borrower capacity to repay the loan. Assessment of borrower s ability to bring in profits from operations. Assessment of project viability. Assessment

The Mortgage Stream. TSX.V: INP May 7, 2018

The Mortgage Stream TSX.V: INP May 7, 2018 1 Background Input Capital is an agriculture commodity streaming company with a focus on canola, the largest and most profitable crop in Canadian agriculture.

The Mortgage Stream TSX.V: INP May 7, 2018 1 Background Input Capital is an agriculture commodity streaming company with a focus on canola, the largest and most profitable crop in Canadian agriculture.

PROGRAM SUMMARY. For additional information, contact:

PROGRAM SUMMARY Contact: For additional information, contact: Patrick Evans (618) 244-2424 ext. 1501 pevans@il-fa.com Lorrie Karcher (618) 244-2424 ext. 1500 lkarcher@il-fa.com An application form may

PROGRAM SUMMARY Contact: For additional information, contact: Patrick Evans (618) 244-2424 ext. 1501 pevans@il-fa.com Lorrie Karcher (618) 244-2424 ext. 1500 lkarcher@il-fa.com An application form may

solid, established, reliable - since 1959 All appraisals must be ordered through Nationwide Property & Appraisal Services

Conforming Overlays solid, established, reliable - since 1959 1/5/17 All appraisals must be ordered through Nationwide Property & Appraisal Services All loans must be DU underwritten and receive an Approve

Conforming Overlays solid, established, reliable - since 1959 1/5/17 All appraisals must be ordered through Nationwide Property & Appraisal Services All loans must be DU underwritten and receive an Approve

AgriBank, FCB and Affiliated Associations

Quarterly Report June 30, 2005 Copies of quarterly and annual reports are available upon request by contacting AgriBank, FCB, 375 Jackson Street, St. Paul, Minnesota 55101-1810 or by calling (651) 282-8800.

Quarterly Report June 30, 2005 Copies of quarterly and annual reports are available upon request by contacting AgriBank, FCB, 375 Jackson Street, St. Paul, Minnesota 55101-1810 or by calling (651) 282-8800.

GMHF Affordable Housing Loan Products

GMHF Affordable Housing Loan Products FOR RENTAL & SINGLE FAMILY AFFORDABLE HOUSING Predevelopment Loans Acquisition Loans Construction /Rehab Loans Tax Credit Bridge Loans Mini Perm & Permanent Loans

GMHF Affordable Housing Loan Products FOR RENTAL & SINGLE FAMILY AFFORDABLE HOUSING Predevelopment Loans Acquisition Loans Construction /Rehab Loans Tax Credit Bridge Loans Mini Perm & Permanent Loans

Non-Conforming Initial Loan Submission Checklist Exhibit 6 8/03/15

Wells Fargo Funding Loan Information Wells Fargo Funding Loan number (required): Borrower name: Subject property address: Contact Information for File Company name: Contact for this file: Phone number:

Wells Fargo Funding Loan Information Wells Fargo Funding Loan number (required): Borrower name: Subject property address: Contact Information for File Company name: Contact for this file: Phone number:

Commercial Real Estate Comparison Pricing Summary

Wells Fargo Bank, N.A. Small Business Administration Lending Commercial Real Estate Comparison Pricing Summary Prepared For: Darrin Boyd - David Moore Property Address: 9755 Westoint Drive Indianapolis,

Wells Fargo Bank, N.A. Small Business Administration Lending Commercial Real Estate Comparison Pricing Summary Prepared For: Darrin Boyd - David Moore Property Address: 9755 Westoint Drive Indianapolis,

Section DU Refi Plus Loan Program

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Product Summary... 2 Features and Benefits... 4 Related Bulletins...

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Product Summary... 2 Features and Benefits... 4 Related Bulletins...

PURCHASE. Max LTV w/o Sec. Fin. Max LTV w/ Sec. Fin. Max TLTV w/ Sec. Fin.

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

Farmer Mac Relationship Managers How Community Banks are Using Farmer Mac to Grow Their Ag Portfolios

Farmer Mac Relationship Managers How Community Banks are Using Farmer Mac to Grow Their Ag Portfolios Refresh Webinar - April 2015 1 Guest Panelist Perry Forst, President & CEO Citizens State Bank Norwood

Farmer Mac Relationship Managers How Community Banks are Using Farmer Mac to Grow Their Ag Portfolios Refresh Webinar - April 2015 1 Guest Panelist Perry Forst, President & CEO Citizens State Bank Norwood

CHOOSING THE RIGHT MORTGAGE PARTNER

CHOOSING THE RIGHT MORTGAGE PARTNER Your mortgage partner should play a vital role in both a seller listing situation and in the case of when working with a buyer. IN THE CASE OF A LISTING Provide seller

CHOOSING THE RIGHT MORTGAGE PARTNER Your mortgage partner should play a vital role in both a seller listing situation and in the case of when working with a buyer. IN THE CASE OF A LISTING Provide seller

Increase (decrease) in For the six months ended June 30, net income

in For the six months ended June 30, net income") Copies of quarterly and annual reports are available upon request by contacting AgriBank, FCB, 30 E. 7th Street, Suite 1600, St. Paul, MN 55101 or by calling (651) 282-8800. Reports are also available

Copies of quarterly and annual reports are available upon request by contacting AgriBank, FCB, 30 E. 7th Street, Suite 1600, St. Paul, MN 55101 or by calling (651) 282-8800. Reports are also available

SUBORDINATION REQUIREMENTS

SUBORDINATION REQUIREMENTS This communication is in response to your request for the (SLS) subordination requirements. Below are the general guidelines for either a refinance or loan modification subordination.

SUBORDINATION REQUIREMENTS This communication is in response to your request for the (SLS) subordination requirements. Below are the general guidelines for either a refinance or loan modification subordination.

Financial Resources Available to Beginning Farmers. Peyton Fair Farm Credit Mid-America Les Humpal UT Extension Danny Morris UT Extension

Financial Resources Available to Beginning Farmers Peyton Fair Farm Credit Mid-America Les Humpal UT Extension Danny Morris UT Extension Financial Resources There are several sources of financial resources

Financial Resources Available to Beginning Farmers Peyton Fair Farm Credit Mid-America Les Humpal UT Extension Danny Morris UT Extension Financial Resources There are several sources of financial resources

Mortgage Insurance Help

Mortgage Insurance Help Address Line 1 Address Line 2 All Other Monthly Payments Amortization Term Amortization Type Application Number Appraisal Value Borrower's First Name Borrower's Last Name Borrower's

Mortgage Insurance Help Address Line 1 Address Line 2 All Other Monthly Payments Amortization Term Amortization Type Application Number Appraisal Value Borrower's First Name Borrower's Last Name Borrower's

BMC Wells Fargo Non Conforming Loan Submission Checklist Loan #: Borower's Name:

Loan Submission Form Current Version Borrower's Email Address Data File (Fannie Mae 3.2 Format) Utah Fee Agreement (Only required on properties located in Utah) Utah Servicing Disclosure (Only required

Loan Submission Form Current Version Borrower's Email Address Data File (Fannie Mae 3.2 Format) Utah Fee Agreement (Only required on properties located in Utah) Utah Servicing Disclosure (Only required

lenders may contact their local County Office or State Office to telephone at

UNITED STATES DEPARTMENT OF AGRICULTURE Farm Service Agency Washington, DC 20250 For: State and County Offices 2-FLP Notice FLP-745 Guaranteed Loan Narrative Q&A s Approved by: Deputy Administrator, Farm

UNITED STATES DEPARTMENT OF AGRICULTURE Farm Service Agency Washington, DC 20250 For: State and County Offices 2-FLP Notice FLP-745 Guaranteed Loan Narrative Q&A s Approved by: Deputy Administrator, Farm

OTHER RESOURCES. Pg. # 353

OTHER RESOURCES Pg. # 353 Pg. # 354 Pg. # 355 Pg. # 356 Pg. # 357 Pg. # 358 Pg. # 359 Pg. # 360 Pg. # 361 Pg. # 362 Pg. # 363 Pg. # 364 Pg. # 365 Pg. # 366 COGO CAPITAL NEEDS CHECKLIST Application Completed

OTHER RESOURCES Pg. # 353 Pg. # 354 Pg. # 355 Pg. # 356 Pg. # 357 Pg. # 358 Pg. # 359 Pg. # 360 Pg. # 361 Pg. # 362 Pg. # 363 Pg. # 364 Pg. # 365 Pg. # 366 COGO CAPITAL NEEDS CHECKLIST Application Completed

Associated Adjustable Rate Mortgage Programs TPO Originations

1. Product Description Associated Mortgage Portfolio Programs allows Associated to offer customized underwriting solutions based on the borrower s individual Credit with Associated Bank and other lenders;

1. Product Description Associated Mortgage Portfolio Programs allows Associated to offer customized underwriting solutions based on the borrower s individual Credit with Associated Bank and other lenders;

FULL DOC. PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO. Owner Occupied (O/O) 1 unit 80% 80% unit (see MI section below) 95% 95% 700

1 unit 80% 80% unit (see MI section below) 95% 95% 700") FULL DOC PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO PURCHASE Owner Occupied (O/O) 1 unit (see MI section below) 95% 95% 700 1 unit (see MI section below) 97% 97% 720 2 units (see MI section below) 95%

FULL DOC PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO PURCHASE Owner Occupied (O/O) 1 unit (see MI section below) 95% 95% 700 1 unit (see MI section below) 97% 97% 720 2 units (see MI section below) 95%

MEGA ALT ARM (MA5/1)

") MEGA ALT ARM (MA5/1) Product Description General Loan Production Descriptions (Asset Qualifier) Product Description Eligible Property Type Eligible States Index Term Margin/Floor/Caps Income/Employment

MEGA ALT ARM (MA5/1) Product Description General Loan Production Descriptions (Asset Qualifier) Product Description Eligible Property Type Eligible States Index Term Margin/Floor/Caps Income/Employment

PennyMac Correspondent Group Freddie Mac Standard and Super Conforming Product Profile Overlays to Freddie Mac are underlined

PennyMac Correspondent Group Freddie Mac Standard and Super Conforming Product Profile 01.01.18 Overlays to Freddie Mac are underlined Agency Finance Type Occupancy Term Freddie Mac - LPA Accept Purchase

PennyMac Correspondent Group Freddie Mac Standard and Super Conforming Product Profile 01.01.18 Overlays to Freddie Mac are underlined Agency Finance Type Occupancy Term Freddie Mac - LPA Accept Purchase

REG Z PORTFOLIO ARMS - Primary Residence. REG Z PORTFOLIO ARMS - Non-Owner Occupied (Cash out or Delayed Finance, Not Business Entity) A+ CREDIT

A+ CREDIT") California Luther Burbank Savings ~ Wholesale Rate Sheet 5/23/2016 8:00 AM PST Lock Desk: 7:30 AM - 4:00 PM PST, Monday - Friday Index: Website www.lutherburbanksavingswholesale.com 1 Yr LIBOR 1.2990%

California Luther Burbank Savings ~ Wholesale Rate Sheet 5/23/2016 8:00 AM PST Lock Desk: 7:30 AM - 4:00 PM PST, Monday - Friday Index: Website www.lutherburbanksavingswholesale.com 1 Yr LIBOR 1.2990%

Rural Lending Initiatives Certified Loan Application Packaging Process Single Close Construction to Perm Financing

Rural Lending Initiatives Certified Loan Application Packaging Process Single Close Construction to Perm Financing Presented by the Mike Buethe Single Family Housing Program Director March 13, 2018 0 THE

Rural Lending Initiatives Certified Loan Application Packaging Process Single Close Construction to Perm Financing Presented by the Mike Buethe Single Family Housing Program Director March 13, 2018 0 THE

Construction and Rehabilitation Construction Financing

Construction and Rehabilitation Construction Financing YOUR INSTRUCTORS Dave Konrad District Manager First Horizon Home Loans Mary Robenalt Porter General Counsel NorthStar Title Services, LLC Course Intro

Construction and Rehabilitation Construction Financing YOUR INSTRUCTORS Dave Konrad District Manager First Horizon Home Loans Mary Robenalt Porter General Counsel NorthStar Title Services, LLC Course Intro

FREELAND LENDING does Not have a hard limit of how many loans someone may have: FREELAND LENDING will fund up to 100% of the Purchase Price

Asset Based Lending FREELAND LENDING does Not require: o W-2's o Bank Statements o Pay Stubs o Tax returns o Job references o Personal financial statements FREELAND LENDING does Not have a hard limit of

Asset Based Lending FREELAND LENDING does Not require: o W-2's o Bank Statements o Pay Stubs o Tax returns o Job references o Personal financial statements FREELAND LENDING does Not have a hard limit of

MAGNOLIA BANK CORRESPONDENT FUNDING RURAL DEVELOPMENT PRODUCT SUMMARY

RURAL DEVELOPMENT FIXED RATE (DELEGATED CLIENTS ONLY) 1. PRODUCT DESCRIPTION USDA Fixed Rate Mortgage 30 year term Fully amortizing 2. PRODUCT CODE 3. INDEX 4. MARGIN 5. ANNUAL/ADJUSTMEN T CAP 6. LIFE

RURAL DEVELOPMENT FIXED RATE (DELEGATED CLIENTS ONLY) 1. PRODUCT DESCRIPTION USDA Fixed Rate Mortgage 30 year term Fully amortizing 2. PRODUCT CODE 3. INDEX 4. MARGIN 5. ANNUAL/ADJUSTMEN T CAP 6. LIFE

Max LTV/CLTV FICO 1 Unit 95/95% /90% 620 Purchase 85/85% 620 Refi 75/75% 2 Units Purchase & Refi- 85/85% 620 N/A N/A 75/75% 620

Revision: October 25, 2016 (Product Information Center, 949-390-2670, www.jmaclending.com) Fixed Rate (Purchase & Rate/Term Refinances) Fannie Mae DU Products: CF30, CF20, CF15, CF10 Occupancy Owner Occupied

Revision: October 25, 2016 (Product Information Center, 949-390-2670, www.jmaclending.com) Fixed Rate (Purchase & Rate/Term Refinances) Fannie Mae DU Products: CF30, CF20, CF15, CF10 Occupancy Owner Occupied

Bulletin. TO: All Freddie Mac Sellers and Servicers October 17, 2008

Bulletin TO: All Freddie Mac Sellers and Servicers October 17, 2008 SUBJECTS Selling requirements are amended in this Single-Family Seller/Servicer Guide (Guide) Bulletin. This Bulletin provides final

Bulletin TO: All Freddie Mac Sellers and Servicers October 17, 2008 SUBJECTS Selling requirements are amended in this Single-Family Seller/Servicer Guide (Guide) Bulletin. This Bulletin provides final

Tony Bowers Farm Loan Officer USDA Farm Service Agency 820 Industrial Drive, Suite 1 Sparta, WI 54656

Tony Bowers Farm Loan Officer USDA Farm Service Agency 820 Industrial Drive, Suite 1 Sparta, WI 54656 Farm Business Planning Building a Farm Business Plan Lenders Perspective Financing Options How to Build

Tony Bowers Farm Loan Officer USDA Farm Service Agency 820 Industrial Drive, Suite 1 Sparta, WI 54656 Farm Business Planning Building a Farm Business Plan Lenders Perspective Financing Options How to Build

PREMIER JUMBO PROGRAM GUIDE

\ PREMIER JUMBO PROGRAM GUIDE This document is provided for approved loan sellers only and may not be copied, distributed or disclosed to any other party. All terms herein are subject to change by FundLoans

\ PREMIER JUMBO PROGRAM GUIDE This document is provided for approved loan sellers only and may not be copied, distributed or disclosed to any other party. All terms herein are subject to change by FundLoans

Housing Trust Silicon Valley ( HTSV ) Mortgage Assistance Program (MAP)

Mortgage Assistance Program (MAP)") Housing Trust Silicon Valley ( HTSV ) Mortgage Assistance Program (MAP) Program Description: Housing Trust Silicon Valley s Mortgage Assistance Program (MAP) is an amortizing second loan that is now available

Housing Trust Silicon Valley ( HTSV ) Mortgage Assistance Program (MAP) Program Description: Housing Trust Silicon Valley s Mortgage Assistance Program (MAP) is an amortizing second loan that is now available

SUPER JUMBO PRIMARY RESIDENCE. Min FICO. SFR, Condo* Townhouse PUD, 2 Units. Min FICO. SFR, Condo, Townhouse, PUD, 2 Units SECOND HOMES.

SJ Series SUPER JUMBO PRIMARY RESIDENCE Occupancy Loan Purpose Property Type Min FICO LTV/CLTV Max Loan Amt Primary Residence Purchase & Rate/Term Refinance SFR, Condo* PUD, 2 Units 720 80/80 $2,000,000

SJ Series SUPER JUMBO PRIMARY RESIDENCE Occupancy Loan Purpose Property Type Min FICO LTV/CLTV Max Loan Amt Primary Residence Purchase & Rate/Term Refinance SFR, Condo* PUD, 2 Units 720 80/80 $2,000,000

Farmer Mac 2 Update: A Top-Down Review of the USDA Guaranteed Loan Secondary Market

Farmer Mac 2 Update: A Top-Down Review of the USDA Guaranteed Loan Secondary Market Refresh Webinar September 2016 Today s Presenters Patrick Kerrigan Director of Business Development Farmer Mac 2 Program

Farmer Mac 2 Update: A Top-Down Review of the USDA Guaranteed Loan Secondary Market Refresh Webinar September 2016 Today s Presenters Patrick Kerrigan Director of Business Development Farmer Mac 2 Program

Annoucement Correspondent Lending

Superior Performance Our Commit ment New VP Correspondent Lending Turn Times New Correspondent Team Members Update Guidelines Annoucement 2011 10-25 Correspondent Lending IN THIS ANNCOUNCEMENT 203Ks Updated

Superior Performance Our Commit ment New VP Correspondent Lending Turn Times New Correspondent Team Members Update Guidelines Annoucement 2011 10-25 Correspondent Lending IN THIS ANNCOUNCEMENT 203Ks Updated

Lender Letter LL

Lender Letter LL-2017-05 To: All Fannie Mae Single-Family Sellers High Loan-to-Value Refinance Option September 08, 2017 At the direction of the Federal Housing Finance Agency (FHFA), Fannie Mae will offer

Lender Letter LL-2017-05 To: All Fannie Mae Single-Family Sellers High Loan-to-Value Refinance Option September 08, 2017 At the direction of the Federal Housing Finance Agency (FHFA), Fannie Mae will offer

ClearEdge Core Full Doc/ Express Doc/Bank Statements

ClearEdge Core Full Doc/ Express Doc/Bank Statements / Cash-Out Owner / Second Home / Non-Owner Loan Amount Credit Score LTV/CLTV Recent Credit Event** LTV/CLTV 680 90 Purchase Only 85 $1.5 MM 640 85 80

ClearEdge Core Full Doc/ Express Doc/Bank Statements / Cash-Out Owner / Second Home / Non-Owner Loan Amount Credit Score LTV/CLTV Recent Credit Event** LTV/CLTV 680 90 Purchase Only 85 $1.5 MM 640 85 80

JUMBO A PROGRAM GUIDE

TABLE OF CONTENTS 1 OVERVIEW... 3 2 UNDERWRITING CRITERIA... 3 3 PRODUCT ELIGIBILITY... 4 3.1 AVAILABLE PRODUCTS... 4 3.2 ADJUSTABLE RATE CRITERIA... 4 4 PRODUCT MATRIX... 5 4.1 GEOGRAPHY... 5 4.2 MINIMUM

TABLE OF CONTENTS 1 OVERVIEW... 3 2 UNDERWRITING CRITERIA... 3 3 PRODUCT ELIGIBILITY... 4 3.1 AVAILABLE PRODUCTS... 4 3.2 ADJUSTABLE RATE CRITERIA... 4 4 PRODUCT MATRIX... 5 4.1 GEOGRAPHY... 5 4.2 MINIMUM

Conforming limits - Purchase - Rate and Term Refinances (Loans must have been purchase money A quality mortgage at origination)

") DREAM MAKER FIXED RATE LOW INCOME / LOW FICO WHOLESALE PRODUCT GUIDELINES PRODUCT CODES: C30XO C20XO C15XO C10XO Several states and local municipalities have enacted legislation which define High Cost

DREAM MAKER FIXED RATE LOW INCOME / LOW FICO WHOLESALE PRODUCT GUIDELINES PRODUCT CODES: C30XO C20XO C15XO C10XO Several states and local municipalities have enacted legislation which define High Cost

Preferred Stock, 8.25% Series A Cumulative. Preferred Stock, 7.75% Series B Cumulative. Preferred Stock, 8.50% Series C Cumulative

! UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended or " TRANSITION

! UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended or " TRANSITION

APPENDIX C PRIVATE MARKETS INVESTMENT POLICY

APPENDIX C PRIVATE MARKETS INVESTMENT POLICY Pursuant to Iowa Code 97B, the Iowa Public Employees Retirement System (IPERS) Investment Board (Board) establishes this Private Markets Investment Policy (Policy)

APPENDIX C PRIVATE MARKETS INVESTMENT POLICY Pursuant to Iowa Code 97B, the Iowa Public Employees Retirement System (IPERS) Investment Board (Board) establishes this Private Markets Investment Policy (Policy)

FHLMC PROGRAM LINEUP`

FHLMC PROGRAM LINEUP` Table of Contents Conventional Conforming (fixed & ARM)... 2 Super Conforming Fixed Rate... 5 Super Conforming ARM... 7 Home Possible... 11 Open Access... 16 HomeOne... 18 www.mcfunding.com

FHLMC PROGRAM LINEUP` Table of Contents Conventional Conforming (fixed & ARM)... 2 Super Conforming Fixed Rate... 5 Super Conforming ARM... 7 Home Possible... 11 Open Access... 16 HomeOne... 18 www.mcfunding.com

Best Practices for Borrower Ability to Repay Rules

March 30, 2012 Best Practices for Borrower Ability to Repay Rules by Anna DeSimone President & Founder About one year ago, I published an article entitled Borrower Repayment Ability on the Radar. The article

March 30, 2012 Best Practices for Borrower Ability to Repay Rules by Anna DeSimone President & Founder About one year ago, I published an article entitled Borrower Repayment Ability on the Radar. The article

AgriBank, FCB and Affiliated Associations

Quarterly Report June 30, 2007 Copies of quarterly and annual reports are available upon request by contacting AgriBank, FCB, 375 Jackson Street, St. Paul, Minnesota 55101-1810 or by calling (651) 282-8800.

Quarterly Report June 30, 2007 Copies of quarterly and annual reports are available upon request by contacting AgriBank, FCB, 375 Jackson Street, St. Paul, Minnesota 55101-1810 or by calling (651) 282-8800.

Settlement Disclosure Form

Settlement Disclosure Form This form is a statement of final loan terms and actual settlement costs. Settlement information Date 11/9/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd,

Settlement Disclosure Form This form is a statement of final loan terms and actual settlement costs. Settlement information Date 11/9/2011 Agent Martha Jones Location ABC Settlement 54321 Random Blvd,

CoBank District 2016 Financial Information

CoBank District 2016 Financial Information Introduction and District Overview CoBank, ACB (CoBank, the Bank, we, our, or us) is one of the four banks of the Farm Credit System (System) and provides loans,

CoBank District 2016 Financial Information Introduction and District Overview CoBank, ACB (CoBank, the Bank, we, our, or us) is one of the four banks of the Farm Credit System (System) and provides loans,

West Town Bancorp, Inc.

Report on Consolidated Financial Statements Contents Page Independent Auditor's Report... 1-2 Consolidated Financial Statements Consolidated Balance Sheets... 3 Consolidated Statements of Income... 4 Consolidated

Report on Consolidated Financial Statements Contents Page Independent Auditor's Report... 1-2 Consolidated Financial Statements Consolidated Balance Sheets... 3 Consolidated Statements of Income... 4 Consolidated

AIG Investments Underwriting Guidelines

AIG Investments Underwriting Guidelines September 18, 2017 MC-2-A987H-1016 2017 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated. The Underwriting

AIG Investments Underwriting Guidelines September 18, 2017 MC-2-A987H-1016 2017 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated. The Underwriting

FHA Streamline Offering 8/15/14

FHA Streamline Offering 8/15/14 Streamline Basics All FHA to FHA refinances are eligible for a Streamline offering Streamlines can be structured with or without an appraisal and with or without credit

FHA Streamline Offering 8/15/14 Streamline Basics All FHA to FHA refinances are eligible for a Streamline offering Streamlines can be structured with or without an appraisal and with or without credit

Chapter 41 Transfers of Ownership

Chapter 41 Transfers of Ownership 41.1 Transfers of Ownership in the Property or in the Borrower (04/29/16) As used in this Chapter 41, the term transferee refers to The new Borrower if the proposed transaction

Chapter 41 Transfers of Ownership 41.1 Transfers of Ownership in the Property or in the Borrower (04/29/16) As used in this Chapter 41, the term transferee refers to The new Borrower if the proposed transaction

Guidelines Correspondent Loan Program: 5/1 LIBOR ARM 2/2/5 Interest Only Dollar Bank (1590) LTV Limits:

LTV Limits:") Loan Program: 5/1 LIBOR ARM 2/2/5 Interest Only Dollar Bank (1590) LTV Limits: PURCHASE and NO CASH-OUT REFINANCE MORTGAGES Occupancy Primary Residence Second Home Investment & Non- Owner Occupied Property

Loan Program: 5/1 LIBOR ARM 2/2/5 Interest Only Dollar Bank (1590) LTV Limits: PURCHASE and NO CASH-OUT REFINANCE MORTGAGES Occupancy Primary Residence Second Home Investment & Non- Owner Occupied Property

Economic Development Course December 8, 2015

Economic Development Course December 8, 2015 Financing Economic Development Federal Program Gary W. Smith President and CEO Chester County Economic Development Council 1 IDA Tax Exempt Program Private

Economic Development Course December 8, 2015 Financing Economic Development Federal Program Gary W. Smith President and CEO Chester County Economic Development Council 1 IDA Tax Exempt Program Private

QuickLink Credit Application and Account Agreement

QuickLink Credit Application and Account Agreement *For quicker processing of your application, please apply online at Grower.Raboag.com* (1) Line of Business Information Beef Cattle Corn Cotton Dairy

QuickLink Credit Application and Account Agreement *For quicker processing of your application, please apply online at Grower.Raboag.com* (1) Line of Business Information Beef Cattle Corn Cotton Dairy

Farm Credit Southeast Missouri, ACA

Quarterly Report June 30, 2018 MANAGEMENT'S DISCUSSION AND ANALYSIS The following commentary reviews the consolidated financial condition and consolidated results of operations of and its subsidiaries

Quarterly Report June 30, 2018 MANAGEMENT'S DISCUSSION AND ANALYSIS The following commentary reviews the consolidated financial condition and consolidated results of operations of and its subsidiaries

Clearinghouse Rule PROPOSED ORDER OF THE OFFICE OF CREDIT UNIONS REPEALING AND RECREATING RULES

Clearinghouse Rule 17-063 PROPOSED ORDER OF THE OFFICE OF CREDIT UNIONS REPEALING AND RECREATING RULES The Wisconsin Office of Credit Unions proposes an order to repeal and recreate ch. DFI CU 72 relating

Clearinghouse Rule 17-063 PROPOSED ORDER OF THE OFFICE OF CREDIT UNIONS REPEALING AND RECREATING RULES The Wisconsin Office of Credit Unions proposes an order to repeal and recreate ch. DFI CU 72 relating

HUD 242 HOSPITAL FINANCING

HUD 242 HOSPITAL FINANCING Prepared by Bedford Lending 1 Mission To support affordable financing of needed hospital projects by reducing the cost of capital Supports HUD s community development mission

HUD 242 HOSPITAL FINANCING Prepared by Bedford Lending 1 Mission To support affordable financing of needed hospital projects by reducing the cost of capital Supports HUD s community development mission

Section Jumbo Solution Second Mortgage

- In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 3 Loan Terms... 4 Assumptions... 4 Eligible First and Second Mortgage Products...

- In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 3 Loan Terms... 4 Assumptions... 4 Eligible First and Second Mortgage Products...

MODIFICATION REQUEST FORM HARP / Distressed Modifications / Traditional Modifications

MODIFICATION REQUEST FORM HARP / Distressed Modifications / Traditional Modifications United Guaranty Residential Insurance Company P. O. Box 21367 Greensboro, NC 27420-1367 Phone: 888.822.5584 (select

MODIFICATION REQUEST FORM HARP / Distressed Modifications / Traditional Modifications United Guaranty Residential Insurance Company P. O. Box 21367 Greensboro, NC 27420-1367 Phone: 888.822.5584 (select

Housing Trust Silicon Valley ( HTSV ) Closing Cost Assistance (CCAP) Program

Closing Cost Assistance (CCAP) Program") Housing Trust Silicon Valley ( HTSV ) Closing Cost Assistance (CCAP) Program Program Description: The Housing Trust Silicon Valley s Closing Cost Assistance Program may be used for down payment and/or

Housing Trust Silicon Valley ( HTSV ) Closing Cost Assistance (CCAP) Program Program Description: The Housing Trust Silicon Valley s Closing Cost Assistance Program may be used for down payment and/or