refinancing web page discussion.notebook January 14, 2016 Mortgage Options REFINANCING

|

|

|

- Flora Moore

- 5 years ago

- Views:

Transcription

1 Mortgage Options REFINANCING

2 Define Refinancing Paying off one loan by obtaining another Generally done to secure better loan terms (Like a lower interest rate)

3 Should You Refinance? Whether or not to refinance depends on your own personal financial situation. There are many mortgage options available can vary according to the interest rate, credit score, lender and loan amount Depends on your situation... the best option may be to do nothing at all.

4 Example: initial loan after 5 years balance was at $55, After some research ~ interest rates dropped Refinanced home with a lower interest rate a shorter loan length AND Larger amount borrowed Pro: Lower Interest rate Shorter Loan Length to 15 years Total Interest Paid Decreased Used the extra cash to pay off Auto - Credit Cards Put remaining in savings as emergency money Cons: Monthly Payment INCREASED by $51.81 MUST repay $75,000 rather than $55,438

5 Points to consider: Do you have the funds that refinancing may require to cover up-front costs and fees? generally include... Attorney's or escrow fees (Yours and your lender's if applicable) Property taxes (to cover tax period to date) Interest (paid from date of closing to 30 days before first monthly payment) Loan Origination fee (covers lenders administrative cost) Recording fees Survey fee First premium of mortgage Insurance (if applicable) Title Insurance (yours and lender's) Loan discount points First payment to escrow account for future real estate taxes and insurance Paid receipt for homeowner's insurance policy (and fire and flood insurance if applicable) Any documentation preparation fees If there is enough equity in the property at the time of refinancing, the owner may choose to finance their closing costs and fees by adding them to their current mortgage balance

6 How long will it take to recover the costs of refinancing? The rule of thumb is that refinancing costs are recovered within 2-3 years If you plan to sell the house or pay it off shortly... you may NOT want to refinance you will not recover the costs

7 Has your income increased substantially? If your income has increased substantially you may be able to afford higher monthly payments This may allow you to shorten the term of your mortgage If... the prevailing interest rate is lower for the shorter term mortgage, refinancing is a good option or... may prefer to make larger principal payments against your current mortgage

8 If you don't stay long enough to recover your costs, refinancing is a bad strategy The longer you stay past your break-even point, the more you'll tip the balance in favor of refinancing

Do I roll the dice and take a chance that the new rates will be the best option? or... Do I wait for them to go lower?")

9 I notice/hear that interest rates have fallen. (I am not guaranteed that they will continue to fall or even stay at the new lower rate) Do I roll the dice and take a chance that the new rates will be the best option? or... Do I wait for them to go lower? If so they may increase and I missed the opportunity or they may in fact go lower and I can save more money! What do you do?

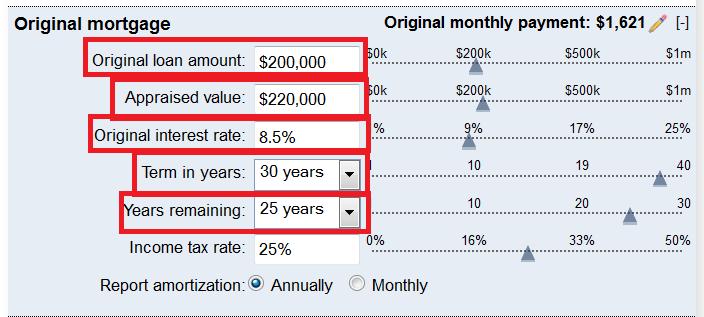

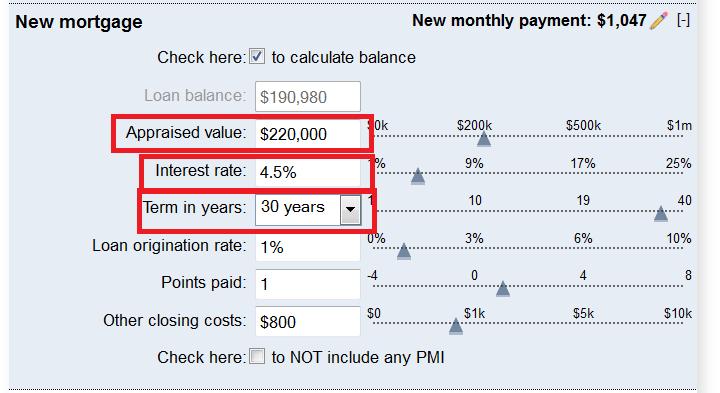

10 Scenarios... You have been paying on your current loan for 5 years Interest rates have fallen by ½ % You look at a new 30 year loan or... do I wait for them to fall by 1% What will I save if I wait? What will I lose if they go back up? You will need information from your original loan to complete these sections... Original Loan Amount = (what you borrowed from the bank) Original interest rate = (lowest rate you found) Appraised value = (the price the house was selling for) Terms in years = (your original loan length) Years remaining = (how many years have you been paying less years original loan was for)

11

12

13 Click on view report to get results and react to the situation Scroll down to Refinancing Summary Click on the minus next to Monthly Payment Breakdown This is the information you will need to respond to for the project

14 You MUST answer the following questions based upon the scenarios given You MUST EXPLAIN 2 pros and 2 cons to each of the scenarios Your total interest paid will increase or decrease by how much? (underline/highlight) What will your new monthly payment be, based on the new mortgage? (underline/highlight) Briefly EXPLAIN why you would, or you would not, refinance given this situation? Scenarios... You have been paying on your current loan for 5 years Interest rates have fallen by ½ % You look at a new 30 year loan or... do I wait for them to fall by 1% What will I save if I wait? What will I lose if they go back up?

15 Given this scenario I would NOT refinance! I will be spending $5,751 MORE with the new loan even though I will save $ per month on my Mortgage - I would wait for rates to go lower!

16 Given this scenario I would refinance! I will be saving $4,202 with the new loan AND I will save $ per month on my Mortgage - I will take this opportunity!

17 Scenarios... You have been paying on your current loan for 5 years Interest rates have fallen by ½ % You look at a new 15 year loan or... do I wait for them to fall by 1% What will I save if I wait? What will I lose if they go back up? You MUST answer the following questions based upon the scenarios given You MUST EXPLAIN 2 pros and 2 cons to each of the scenarios Your total interest paid will increase or decrease by how much? (underline/highlight) What will your new monthly payment be, based on the new mortgage? (underline/highlight) Briefly EXPLAIN why you would, or you would not, refinance given this situation?

18 Given this scenario I will be saving $34,057 with the new loan BUT I will pay $ MORE per month on my Mortgage - I will take this opportunity as long as I can afford the monthly payments!

19 Given this scenario I will be saving $38,386 with the new loan BUT I will pay $ MORE per month on my Mortgage - I will take this opportunity as long as I can afford the monthly payments!

20 Scenarios... You have been paying on your current loan for 13 years Interest rates have fallen by ½ % You look at a new 15 year loan or... do I wait for them to fall by 1% What will I save if I wait? What will I lose if they go back up? Given this scenario I will be saving $8,026 with the new loan AND I will SAVE $15.48 per month on my Mortgage - It is a great opportunity and I will take this opportunity to refinance BUT I would like to wait for rates to go even lower!

21 Given this scenario I will be saving $11,473 with the new loan AND I will SAVE $34.63 per month on my Mortgage - It is a great opportunity and I will take this opportunity to refinance!

How to Refinance Your Mortgage at the Most Competitive Rates

Your Mortgage It is vital to get the best deal on mortgage refinance rates to refinance your mortgage. The following 12 steps are going to help you lock in the lowest possible mortgage refinance rates.

Your Mortgage It is vital to get the best deal on mortgage refinance rates to refinance your mortgage. The following 12 steps are going to help you lock in the lowest possible mortgage refinance rates.

Loan Estimates. with the following requirements: Estimate SMF SMF SMF

Loan Estimates with the following requirements: Estimate SMF SMF SMF Please follow the directions below when completing the Initial Loan Application and Disclosure processes. e e cc e and Locked LE, including

Loan Estimates with the following requirements: Estimate SMF SMF SMF Please follow the directions below when completing the Initial Loan Application and Disclosure processes. e e cc e and Locked LE, including

White Paper Choosing a Mortgage

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 Introduction...

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 Introduction...

a guide to mortgages Go to to learn more about financing your home. 1 of 8

The type of mortgage you choose should be based on your financial situation today, your best estimate of what it will be in the future, how long you plan to own the home or stay in the mortgage and your

The type of mortgage you choose should be based on your financial situation today, your best estimate of what it will be in the future, how long you plan to own the home or stay in the mortgage and your

Housing. Pros and cons of renting. Pros and cons of ownership. Renting vs. owning a home Mortgages Building equity: fact or fiction?

Housing Renting vs. owning a home Mortgages Building equity: fact or fiction? Pros and cons of renting Advantages Low move-in costs You re mobile you can move fairly quickly Even if you break the lease

Housing Renting vs. owning a home Mortgages Building equity: fact or fiction? Pros and cons of renting Advantages Low move-in costs You re mobile you can move fairly quickly Even if you break the lease

Closing Costs Explained

Closing Costs Explained When you apply for a home loan, you will receive a Good Faith Estimate of Settlement Charges, and a booklet that will explain these costs in detail. Loan Origination Fee: This fee

Closing Costs Explained When you apply for a home loan, you will receive a Good Faith Estimate of Settlement Charges, and a booklet that will explain these costs in detail. Loan Origination Fee: This fee

Tips from the Treasurer

Tips from the Treasurer Saving & Investing Money Saving for the Long Term Investing Responsibly City Treasurer Kurt Summers SAVING FOR THE LONG TERM 53 Saving for College Education 529 College Savings

Tips from the Treasurer Saving & Investing Money Saving for the Long Term Investing Responsibly City Treasurer Kurt Summers SAVING FOR THE LONG TERM 53 Saving for College Education 529 College Savings

MORTGAGE FUNDAMENTALS INTRODUCTION READ ME!

INTRODUCTION At Radian, we realize that more and more new people are excited to join the mortgage profession and many have little to no exposure to our industry. The Mortgage Fundamentals series is designed

INTRODUCTION At Radian, we realize that more and more new people are excited to join the mortgage profession and many have little to no exposure to our industry. The Mortgage Fundamentals series is designed

Loan Estimate $ NO. Loan Terms. Loan Amount $ NO. Interest Rate 1.75% NO

Pennsylvania Housing Finance Agency 211 N. Front Street Harrisburg, PA 17101 Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate DATE ISSUED APPLICANTS PROPERTY PROP. VALUE LOAN

Pennsylvania Housing Finance Agency 211 N. Front Street Harrisburg, PA 17101 Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate DATE ISSUED APPLICANTS PROPERTY PROP. VALUE LOAN

TILA RESPA Integrated Disclosure

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-24(G) Mortgage Loan Transaction Loan Estimate Modification to Loan Estimate for Transaction Not Involving Seller Model Form This is a blank model Loan

FEBRUARY 7, 2014 TILA RESPA Integrated Disclosure H-24(G) Mortgage Loan Transaction Loan Estimate Modification to Loan Estimate for Transaction Not Involving Seller Model Form This is a blank model Loan

Home Equity Loans and Lines of Credit

Thorley Wealth Management, Inc. Elizabeth Thorley, MS, CFP, CLU, AIF CEO & President 1478 Marsh Road Pittsford, NY 14534 585-512-8453 x203 Fax: 585.625.0477 ethorley@thorleywm.com www.thorleywm.com Home

Thorley Wealth Management, Inc. Elizabeth Thorley, MS, CFP, CLU, AIF CEO & President 1478 Marsh Road Pittsford, NY 14534 585-512-8453 x203 Fax: 585.625.0477 ethorley@thorleywm.com www.thorleywm.com Home

GENERAL FINANCING QUESTIONS

GENERAL FINANCING QUESTIONS 1. What is a Mortgage? Tips for Homebuyers Generally speaking, a mortgage is a loan obtained to purchase real estate. The "mortgage" itself is a lien (a legal claim) on the

GENERAL FINANCING QUESTIONS 1. What is a Mortgage? Tips for Homebuyers Generally speaking, a mortgage is a loan obtained to purchase real estate. The "mortgage" itself is a lien (a legal claim) on the

SEVEN LIFE-DEFINING FINANCIAL DECISIONS

SEVEN LIFE-DEFINING FINANCIAL DECISIONS A Joint Project of The Actuarial Foundation and WISER, the Women's Institute for a Secure Retirement 4 HOME OWNERSHIP, DEBT, AND CREDIT Buying a home is one of the

SEVEN LIFE-DEFINING FINANCIAL DECISIONS A Joint Project of The Actuarial Foundation and WISER, the Women's Institute for a Secure Retirement 4 HOME OWNERSHIP, DEBT, AND CREDIT Buying a home is one of the

Reducing the Cost of Debt

Reducing the Cost of Debt What is reducing the cost of debt? As the old adage goes: "A penny saved is a penny earned." And though it may sound trite, it is true. If you carry a large amount of debt, one

Reducing the Cost of Debt What is reducing the cost of debt? As the old adage goes: "A penny saved is a penny earned." And though it may sound trite, it is true. If you carry a large amount of debt, one

How to Stop and Avoid Foreclosure in Today's Market

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Steps to Homeownership

Steps to Homeownership Introduction Steps to Homeownership Learn the steps you will take to becoming a homeowner. Gain an understanding of key terms used in the homebuying process. Freddie Mac 2008 2 A

Steps to Homeownership Introduction Steps to Homeownership Learn the steps you will take to becoming a homeowner. Gain an understanding of key terms used in the homebuying process. Freddie Mac 2008 2 A

The Federal Reserve Board

The Federal Reserve Board A Consumer s Guide to Mortgage Refinancings Board of Governors of the Federal Reserve System www.federalreserve.gov 0608 A Consumer s Guide to Mortgage Refinancings i Table of

The Federal Reserve Board A Consumer s Guide to Mortgage Refinancings Board of Governors of the Federal Reserve System www.federalreserve.gov 0608 A Consumer s Guide to Mortgage Refinancings i Table of

FRB:A Consumer's Guide to Mortgage Lock-Ins. All About Lock-Ins Ask About Lock-Ins Complaints About Lock-Ins State and Federal Agencies

Page 1 of 5 All About Lock-Ins Ask About Lock-Ins Complaints About Lock-Ins State and Federal Agencies When you?re looking for a mortgage, you?re likely to shop among lenders for the most favorable interest

Page 1 of 5 All About Lock-Ins Ask About Lock-Ins Complaints About Lock-Ins State and Federal Agencies When you?re looking for a mortgage, you?re likely to shop among lenders for the most favorable interest

The power of borrowing like a boss

The power of borrowing like a boss Borrowing can help you do some pretty wonderful things. Like getting that home that s right for you and your family (or family to be!). The place where you ll make memories

The power of borrowing like a boss Borrowing can help you do some pretty wonderful things. Like getting that home that s right for you and your family (or family to be!). The place where you ll make memories

First Time Home Buyer Guide. Are you ready to learn the steps to homeownership?

First Time Home Buyer Guide Are you ready to learn the steps to homeownership? Is this your first time going through the home buying process? If so, don t worry, this guide is designed to answer any questions

First Time Home Buyer Guide Are you ready to learn the steps to homeownership? Is this your first time going through the home buying process? If so, don t worry, this guide is designed to answer any questions

HOME FINANCING BASICS

HOME FINANCING BASICS PRESENTED TO: OMEGA PSI PHI FRATERNITY, INC. 2005 LEADERSHIP CONFERENCE PRESENTED BY: GRANT BUSINESS STRATEGIES, INC. Copyright 2005 by Grant mortgage services All rights reserved.

HOME FINANCING BASICS PRESENTED TO: OMEGA PSI PHI FRATERNITY, INC. 2005 LEADERSHIP CONFERENCE PRESENTED BY: GRANT BUSINESS STRATEGIES, INC. Copyright 2005 by Grant mortgage services All rights reserved.

Closing Disclosure $ NO

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Consumer's Guide To Mortgage Settlement Costs

Consumer's Guide To Mortgage Settlement Costs Of all the steps in buying a home or refinancing a loan, the mortgage closing or settlement probably causes more confusion and uncertainty for the borrower

Consumer's Guide To Mortgage Settlement Costs Of all the steps in buying a home or refinancing a loan, the mortgage closing or settlement probably causes more confusion and uncertainty for the borrower

Closing Disclosure. Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued Closing Date Disbursement Date Settlement

The Complete Guide to Bridging Loans

Bridging Loans Hotline Call 0117 313 6058 The Complete Guide to Bridging Loans Need to move fast? Mortgage chain issues? Buying an auction property? Seeking development finance? READ HERE Contact Us Tel:

Bridging Loans Hotline Call 0117 313 6058 The Complete Guide to Bridging Loans Need to move fast? Mortgage chain issues? Buying an auction property? Seeking development finance? READ HERE Contact Us Tel:

DEFINITION OF COMMON TERMS

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

Borrowing on Home Equity

ABCs of Mortgages Series Borrowing on Home Equity Smart mortgage decisions start here Table of Contents Overview 1 What are the different options? 2 1. Refinancing 3 2. Borrowing amounts you prepaid 4

ABCs of Mortgages Series Borrowing on Home Equity Smart mortgage decisions start here Table of Contents Overview 1 What are the different options? 2 1. Refinancing 3 2. Borrowing amounts you prepaid 4

Closing Information Transaction Information Loan Information. VA Property Lender Loan ID # MIC #

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Reducing the Cost of Debt

Taddei, Ludwig & Associates, Inc. Kirk Ludwig, ChFC, CFP Scot Elrod Diane McCracken, ChFC Matt Taddei, CLU, CFP 999 Fifth Ave., Suite 230 San Rafael, CA 94901 415-456-2292 scot@tlafinancial.com www.tlafinancial.com

Taddei, Ludwig & Associates, Inc. Kirk Ludwig, ChFC, CFP Scot Elrod Diane McCracken, ChFC Matt Taddei, CLU, CFP 999 Fifth Ave., Suite 230 San Rafael, CA 94901 415-456-2292 scot@tlafinancial.com www.tlafinancial.com

Bond evaluation. Lecture 7 Shahid Iqbal

Bond evaluation Lecture 7 Shahid Iqbal Have you ever borrowed money??? Of course you have! Whether we hit our parents up for a few bucks to buy candy as children or asked the bank for a mortgage, most

Bond evaluation Lecture 7 Shahid Iqbal Have you ever borrowed money??? Of course you have! Whether we hit our parents up for a few bucks to buy candy as children or asked the bank for a mortgage, most

HARP Refinance Guide. How You can Benefit from the HARP Program

HARP Refinance Guide How You can Benefit from the HARP Program Contents How HARP Can Help You You Might Qualify for HARP but Not Know It HARP Qualification Basics HARP History HARP 1.0 HARP 2.0 HARP 3.0

HARP Refinance Guide How You can Benefit from the HARP Program Contents How HARP Can Help You You Might Qualify for HARP but Not Know It HARP Qualification Basics HARP History HARP 1.0 HARP 2.0 HARP 3.0

Refinancing? Compare Your Loan Options

Refinancing? Compare Your Loan Options Introduction At this point, you know refinancing could help you in a number of ways. Maybe you ve even pinned down why you want to refi. Chances are, you want to

Refinancing? Compare Your Loan Options Introduction At this point, you know refinancing could help you in a number of ways. Maybe you ve even pinned down why you want to refi. Chances are, you want to

A Complete Guide to Help You Buy, Build or Refinance Your Home myhonorbank.com

Homebuyer s Guide A Complete Guide to Help You Buy, Build or Refinance Your Home myhonorbank.com 877.325.8031 Mortgage Programs With every season, there is a time to reflect on your stage in life and your

Homebuyer s Guide A Complete Guide to Help You Buy, Build or Refinance Your Home myhonorbank.com 877.325.8031 Mortgage Programs With every season, there is a time to reflect on your stage in life and your

Credit and Credit Cards

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

How to Stop and Avoid Foreclosure in Today's Market

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

Closing Disclosure $ $ Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

Where should my money go First? Here s advice from the financial professionals at Schwab.

Where should my money go First? Here s advice from the financial professionals at Schwab. Start with the basics. In an ideal world, you d have enough money to pay all your bills and save for retirement

Where should my money go First? Here s advice from the financial professionals at Schwab. Start with the basics. In an ideal world, you d have enough money to pay all your bills and save for retirement

A Better guide to mortgage refinance

A Better guide to mortgage refinance If you re a homeowner, you might be hearing everyone from neighbors to news anchors talking about refinancing. But what exactly is a mortgage refinance? How do you

A Better guide to mortgage refinance If you re a homeowner, you might be hearing everyone from neighbors to news anchors talking about refinancing. But what exactly is a mortgage refinance? How do you

Keeping Finances Under Control. How to Manage Debt so it Doesn t Manage You

Keeping Finances Under Control How to Manage Debt so it Doesn t Manage You Seminar Objectives What is DEBT? What are the types of debt? What is good debt? What is bad debt? What are the benefits and costs?

Keeping Finances Under Control How to Manage Debt so it Doesn t Manage You Seminar Objectives What is DEBT? What are the types of debt? What is good debt? What is bad debt? What are the benefits and costs?

First Time Homebuyer s Guide from SunTrust Mortgage, Inc.

First Time Homebuyer s Guide from SunTrust Mortgage, Inc. Advantages of Homeownership A home is an investment which can appreciate (increase in value) over time Many homeowners realize significant tax

First Time Homebuyer s Guide from SunTrust Mortgage, Inc. Advantages of Homeownership A home is an investment which can appreciate (increase in value) over time Many homeowners realize significant tax

Are You Mortgage Ready? Preparing Your Finances for Homeownership. Foundation Communities Financial Coaching Program

Are You Mortgage Ready? Preparing Your Finances for Homeownership. Foundation Communities Financial Coaching Program Do you want to know if you are ready to buy a home? The following guide will help you

Are You Mortgage Ready? Preparing Your Finances for Homeownership. Foundation Communities Financial Coaching Program Do you want to know if you are ready to buy a home? The following guide will help you

Closing Disclosure $ % $ $ $ $ Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Issued Borrower

When Your Home Is On The Line:

When Your Home Is On The Line: What You Should Know About Home Equity Lines of Credit More and more lenders are offering home equity lines of credit. By using the equity in your home, you may qualify for

When Your Home Is On The Line: What You Should Know About Home Equity Lines of Credit More and more lenders are offering home equity lines of credit. By using the equity in your home, you may qualify for

Reverse mortgages. A discussion guide. Consumer Financial Protection Bureau

Reverse mortgages A discussion guide Consumer Financial Protection Bureau About this discussion guide This guide gives an overview of many key concepts of reverse mortgages. A qualified reverse mortgage

Reverse mortgages A discussion guide Consumer Financial Protection Bureau About this discussion guide This guide gives an overview of many key concepts of reverse mortgages. A qualified reverse mortgage

Rehab Loans. Rehabber Friendly" Terms

Rehab Loans Home rehab investors are individual entrepreneurs who find housing properties that need rehabilitation. Their sole purpose is to purchase the property, fix it up, and sell or refinance it.

Rehab Loans Home rehab investors are individual entrepreneurs who find housing properties that need rehabilitation. Their sole purpose is to purchase the property, fix it up, and sell or refinance it.

Chapter 4 Debt. Section Credit misdirection

Chapter 4 Debt Section 2 2.1 Credit misdirection Credit Misdirection Lending money to friends or family members is a bad idea. It will strain relationships and in some cases ruin friendships. If you have

Chapter 4 Debt Section 2 2.1 Credit misdirection Credit Misdirection Lending money to friends or family members is a bad idea. It will strain relationships and in some cases ruin friendships. If you have

Closing Information Transaction Information Loan Information. VA Property Loan ID # Lender MIC # Sale Price $

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued

HOME FINANCING GUIDE

HOME FINANCING GUIDE SECTION 1: Mortgage Loans Available Fixed Rate Mortgages A fixed rate mortgage is a home loan with a rate that remains the same over the entire term of the loan, regardless of how

HOME FINANCING GUIDE SECTION 1: Mortgage Loans Available Fixed Rate Mortgages A fixed rate mortgage is a home loan with a rate that remains the same over the entire term of the loan, regardless of how

Bank of america credit card consolidation loans

Bank of america credit card consolidation loans Credit Card Consolidation Loans : Payday Loans Lenders For Bad Credit #[ Credit Card Consolidation Loans ]# Same Day Cash Loans up to $5000. Apply in Minutes.

Bank of america credit card consolidation loans Credit Card Consolidation Loans : Payday Loans Lenders For Bad Credit #[ Credit Card Consolidation Loans ]# Same Day Cash Loans up to $5000. Apply in Minutes.

STEP BY-STEP HOME BUYING GUIDE. Contact us at Phone

STEP BY-STEP HOME BUYING GUIDE Contact us at Phone 513-608-1199 STEP BY-STEP HOME BUYING GUIDE Not to worry, we are with you every step of the way. 1 Start with your credit. Credit reports are kept by

STEP BY-STEP HOME BUYING GUIDE Contact us at Phone 513-608-1199 STEP BY-STEP HOME BUYING GUIDE Not to worry, we are with you every step of the way. 1 Start with your credit. Credit reports are kept by

Toolkit 2 Borrowing Wisely

Toolkit 2 Borrowing Wisely Questions to Think About Before Borrowing Borrowing money is not necessarily a bad thing and done sensibly it can be a good investment for your future. Some good reasons to borrow

Toolkit 2 Borrowing Wisely Questions to Think About Before Borrowing Borrowing money is not necessarily a bad thing and done sensibly it can be a good investment for your future. Some good reasons to borrow

Consolidate credit card debt with bank of america

Home Consolidate credit card debt with bank of america This quarterly newsletter includes market reports on various key industries highlighting recent transaction and market data as well as key industry

Home Consolidate credit card debt with bank of america This quarterly newsletter includes market reports on various key industries highlighting recent transaction and market data as well as key industry

How MucH HoMe can You afford?

chapter 4 How MucH HoMe can You afford? You should know what you can afford before beginning your search for a home. This enables you to focus on realistic choices and saves you time and effort. This section

chapter 4 How MucH HoMe can You afford? You should know what you can afford before beginning your search for a home. This enables you to focus on realistic choices and saves you time and effort. This section

FORECLOSURE PREVENTION

FORECLOSURE PREVENTION 1/1/2012 Resource Guide Brought to you by: NAACP Economic Department 1816 12 th Street, NW Washington DC 20009 www.naacp.org/econ Foreclosure prevention R E S O U R C E G U I D E

FORECLOSURE PREVENTION 1/1/2012 Resource Guide Brought to you by: NAACP Economic Department 1816 12 th Street, NW Washington DC 20009 www.naacp.org/econ Foreclosure prevention R E S O U R C E G U I D E

How to Strategically Manage Your Debt

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

BUYING YOUR FIRST HOME: THREE STEPS TO SUCCESSFUL MORTGAGE SHOPPING MORTGAGES

BUYING YOUR FIRST HOME: THREE STEPS TO SUCCESSFUL MORTGAGE SHOPPING MORTGAGES June 2015 Cat. No.: FC5-22/3-2015E-PDF ISBN: 978-0-660-02848-4 Her Majesty the Queen in Right of Canada (Financial Consumer

BUYING YOUR FIRST HOME: THREE STEPS TO SUCCESSFUL MORTGAGE SHOPPING MORTGAGES June 2015 Cat. No.: FC5-22/3-2015E-PDF ISBN: 978-0-660-02848-4 Her Majesty the Queen in Right of Canada (Financial Consumer

**This slide is automated and set to advance in 3 parts upon click of the mouse**

2 **This slide is automated and set to advance in 3 parts upon click of the mouse** 1. Challenge students to explain in their own words what credit means. 1.Credit represents money advanced which needs

2 **This slide is automated and set to advance in 3 parts upon click of the mouse** 1. Challenge students to explain in their own words what credit means. 1.Credit represents money advanced which needs

Federal Reserve Bank of Philadelphia

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

Manual Mortgage Payment Calculator With Taxes And Pmi And Insurance And Down

Manual Mortgage Payment Calculator With Taxes And Pmi And Insurance And Down Mortgage calculator with graphs, amortization tables, extra payments and PMI. FICO 760+, PMI FICO 720 759, PMI FICO 680 719,

Manual Mortgage Payment Calculator With Taxes And Pmi And Insurance And Down Mortgage calculator with graphs, amortization tables, extra payments and PMI. FICO 760+, PMI FICO 720 759, PMI FICO 680 719,

Buying Your First Home: Three Steps to Successful Mortgage Shopping

ABCs of Mortgages Series Buying Your First Home: Three Steps to Successful Mortgage Shopping Smart mortgage decisions start here Note: FCAC s Mortgage Calculator tool, available at itpaystoknow.gc.ca,

ABCs of Mortgages Series Buying Your First Home: Three Steps to Successful Mortgage Shopping Smart mortgage decisions start here Note: FCAC s Mortgage Calculator tool, available at itpaystoknow.gc.ca,

PERSONAL FINANCE FINAL EXAM REVIEW. Click here to begin

PERSONAL FINANCE FINAL EXAM REVIEW Click here to begin FINAL EXAM REVIEW Once you work through the questions, you will have a good ideas of what will be on the final next week. Click here if you are too

PERSONAL FINANCE FINAL EXAM REVIEW Click here to begin FINAL EXAM REVIEW Once you work through the questions, you will have a good ideas of what will be on the final next week. Click here if you are too

Chapter 26 11/9/2017 1

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

City of Gastonia s Affordable Housing Program Homebuyer s Assistance Program

City of Gastonia s Affordable Housing Program Homebuyer s Assistance Program The program s objective is to provide funds for modest income families for downpayment and closing cost to purchase a home by

City of Gastonia s Affordable Housing Program Homebuyer s Assistance Program The program s objective is to provide funds for modest income families for downpayment and closing cost to purchase a home by

8 Bag of tricks? What s in a Loan officer s. Money talks but credit has an echo. -Bob Thaves

What s in a Loan officer s 8 Bag of tricks? chapter In the world of mortgage lending, there are many different types of loans and loan terms. How can you decide which loan best fits your financial circumstances?

What s in a Loan officer s 8 Bag of tricks? chapter In the world of mortgage lending, there are many different types of loans and loan terms. How can you decide which loan best fits your financial circumstances?

Maximizing Purchasing Power: Make the Most of Your Credit Score

When life happens... Maximizing Purchasing Power: Make the Most of Your Credit Score Consolidated Credit Counseling Services, Inc. 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 How

When life happens... Maximizing Purchasing Power: Make the Most of Your Credit Score Consolidated Credit Counseling Services, Inc. 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 How

Your guide to. Buying and financing. a home FINANCIAL RESOURCES. MidWestOne.com/FinancialResources Member FDIC

Your guide to Buying and financing a home FINANCIAL MidWestOne.com/FinancialResources Your guide to buying and financing a home Whether you re a first-time homebuyer or you re a seasoned pro, purchasing

Your guide to Buying and financing a home FINANCIAL MidWestOne.com/FinancialResources Your guide to buying and financing a home Whether you re a first-time homebuyer or you re a seasoned pro, purchasing

FIRST: GET PRE-APPROVED

The internet is covered in high quality information aimed at helping first time home buyers understand the process of purchasing a house. However, there is one small problem. There are a LOT of steps involved

The internet is covered in high quality information aimed at helping first time home buyers understand the process of purchasing a house. However, there is one small problem. There are a LOT of steps involved

Using Credit. services but do not require payments in full when the service is performed.

Using Credit How would you like to pay for this, cash or charge? Chances are you have heard this question asked. Cash or charge? is really asking you, the buyer, if you want to use the cash or the money

Using Credit How would you like to pay for this, cash or charge? Chances are you have heard this question asked. Cash or charge? is really asking you, the buyer, if you want to use the cash or the money

First Time Home Buying Steps

Buying a home is one of the biggest emotional and financial decisions you'll ever make in your life time. The differences between renting and buying a home are huge, and there are numbers of pros and cons

Buying a home is one of the biggest emotional and financial decisions you'll ever make in your life time. The differences between renting and buying a home are huge, and there are numbers of pros and cons

5 Biggest Mistakes Most Home Buyers Make

5 Biggest Mistakes Most Home Buyers Make And 3 Guaranteed Ways to Get Approved for a Home Loan This Complementary Special Report was prepared by: 2 5 Biggest Mistake Home Buyers Make Purchasing a home

5 Biggest Mistakes Most Home Buyers Make And 3 Guaranteed Ways to Get Approved for a Home Loan This Complementary Special Report was prepared by: 2 5 Biggest Mistake Home Buyers Make Purchasing a home

Overview of Types of Mortgages Available

Overview of Types of Mortgages Available There are many different types of mortgages available to home buyers. They are all thoroughly explained here. But here, for the sake of simplicity, we have boiled

Overview of Types of Mortgages Available There are many different types of mortgages available to home buyers. They are all thoroughly explained here. But here, for the sake of simplicity, we have boiled

YOUR ROAD TO HOME OWNERSHIP Regions Bank.

YOUR ROAD TO HOME OWNERSHIP 3 REGIONS NEXT STEP This information is general in nature and is not intended to be legal, tax, or financial advice. Although Regions believes this information to be accurate,

YOUR ROAD TO HOME OWNERSHIP 3 REGIONS NEXT STEP This information is general in nature and is not intended to be legal, tax, or financial advice. Although Regions believes this information to be accurate,

MORTGAGE PREPAYMENT MADE EASY

MORTGAGE PREPAYMENT MADE EASY A GUIDE TO PAYING OFF YOUR HOME SOONER Welcome to easy, more personal banking. 1.877.560.0100 alterna.ca 1.866.560.0120 alternabank.ca Together Alterna Savings and Alterna

MORTGAGE PREPAYMENT MADE EASY A GUIDE TO PAYING OFF YOUR HOME SOONER Welcome to easy, more personal banking. 1.877.560.0100 alterna.ca 1.866.560.0120 alternabank.ca Together Alterna Savings and Alterna

Wellesley College Faculty Mortgage Program for the Purchase of a New Home Frequently Asked Questions (FAQs)

") Wellesley College Faculty Mortgage Program for the Purchase of a New Home Frequently Asked Questions (FAQs) What is the structure of the Wellesley College mortgage? The mortgage program combines a traditional

Wellesley College Faculty Mortgage Program for the Purchase of a New Home Frequently Asked Questions (FAQs) What is the structure of the Wellesley College mortgage? The mortgage program combines a traditional

State of New Jersey Department of Banking & Insurance. Annual Report Worksheet for Residential Mortgage Lenders. Year Ending December 31, 2017

State of New Jersey Department of Banking & Insurance for Residential Mortgage Lenders New Jersey Department of Banking & Insurance Division of Banking Attn: Sharon Davis -- 5 th floor 20 West State Street

State of New Jersey Department of Banking & Insurance for Residential Mortgage Lenders New Jersey Department of Banking & Insurance Division of Banking Attn: Sharon Davis -- 5 th floor 20 West State Street

Pro Strategies Help Manual / User Guide: Last Updated March 2017

Pro Strategies Help Manual / User Guide: Last Updated March 2017 The Pro Strategies are an advanced set of indicators that work independently from the Auto Binary Signals trading strategy. It s programmed

Pro Strategies Help Manual / User Guide: Last Updated March 2017 The Pro Strategies are an advanced set of indicators that work independently from the Auto Binary Signals trading strategy. It s programmed

10 Errors to Avoid When Refinancing

10 Errors to Avoid When Refinancing I just refinanced from a 3.625% to a 3.375% 15 year fixed mortgage with Rate One (No financial relationship, but highly recommended.) If you are paying above 4% and

10 Errors to Avoid When Refinancing I just refinanced from a 3.625% to a 3.375% 15 year fixed mortgage with Rate One (No financial relationship, but highly recommended.) If you are paying above 4% and

Closing Disclosure $ NO $1, $ a month. Loan Terms. Projected Payments. Costs at Closing

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 8/15/2015 Closing Date 8/31/2015 Disbursement

Closing Disclosure This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Information Date Issued 8/15/2015 Closing Date 8/31/2015 Disbursement

The Basics. What Is a Mortgage? What Does My Mortgage Payment Include? Mortgage Payment Breakdown

The Basics What Is a Mortgage? A mortgage is a loan secured by real estate. In other words, in return for the funds necessary to purchase a home, a lender gets your promise to pay back the funds over a

The Basics What Is a Mortgage? A mortgage is a loan secured by real estate. In other words, in return for the funds necessary to purchase a home, a lender gets your promise to pay back the funds over a

Opportunity Knocks Property Solutions Helping Create Your Opportunities Rent-to-Own Information www.okpropertysolutions.com WHAT IS RENT-to-OWN? Text Here If you are reading this document, you are likely

Opportunity Knocks Property Solutions Helping Create Your Opportunities Rent-to-Own Information www.okpropertysolutions.com WHAT IS RENT-to-OWN? Text Here If you are reading this document, you are likely

Are You Receiving 8-10% Interest on your Investments?

Are You Receiving 8-10% Interest on your Investments? If your answer to the above questions is no, you will want to pay very special attention. The following information could significantly increase the

Are You Receiving 8-10% Interest on your Investments? If your answer to the above questions is no, you will want to pay very special attention. The following information could significantly increase the

MORTGAGE FUNDAMENTALS - Answer Key

Mortgage Process You would have captured these notes while watching the Mortgage Process video. Q: Where does the mortgage process begin? A: The borrower generally speaks with a Mortgage Loan Officer and

Mortgage Process You would have captured these notes while watching the Mortgage Process video. Q: Where does the mortgage process begin? A: The borrower generally speaks with a Mortgage Loan Officer and

1003 form Commonly used mortgage loan application developed by Fannie Mae. Sometimes called the Uniform Residential Loan Application.

GLOSSARY 1003 form Commonly used mortgage loan application developed by Fannie Mae. Sometimes called the Uniform Residential Loan Application. Acceptance A verbal or written acceptance of an offer to buy

GLOSSARY 1003 form Commonly used mortgage loan application developed by Fannie Mae. Sometimes called the Uniform Residential Loan Application. Acceptance A verbal or written acceptance of an offer to buy

Transaction Information. Tennessee Housing Development Agency

Tennessee Housing Development Agency Second Mortgage Loan This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Disclosure Closing Information

Tennessee Housing Development Agency Second Mortgage Loan This form is a statement of final loan terms and closing costs. Compare this document with your Loan Estimate. Closing Disclosure Closing Information

Understanding Debt Problems & Solutions

Understanding Debt Problems & Solutions The Debt Landscape 40% of Americans live on 110% of their income Total U.S. household debt = $11.2 trillion Finances are one of the top five causes of divorce Money

Understanding Debt Problems & Solutions The Debt Landscape 40% of Americans live on 110% of their income Total U.S. household debt = $11.2 trillion Finances are one of the top five causes of divorce Money

12-Step Home Mortgage Steps

1 You should review your credit report for any errors before submitting your mortgage application. Your credit report is used by banks and other lending institutions to determine your creditworthiness.

1 You should review your credit report for any errors before submitting your mortgage application. Your credit report is used by banks and other lending institutions to determine your creditworthiness.

AKE ONTROL OF OUR ORTGAGE HERE S OPE

AKE ONTROL OF OUR ORTGAGE HERE S OPE A FREE COMMUNITY WORKSHOP FOR HOMEOWNERS STRATEGIES FOR TAKING CONTROL OF YOUR MORTGAGE Hosted by: Presented by Curved poster, PAUL A. BLUCHER OF BLUCHER LAW advertisement,

AKE ONTROL OF OUR ORTGAGE HERE S OPE A FREE COMMUNITY WORKSHOP FOR HOMEOWNERS STRATEGIES FOR TAKING CONTROL OF YOUR MORTGAGE Hosted by: Presented by Curved poster, PAUL A. BLUCHER OF BLUCHER LAW advertisement,

Reverse Mortgage Authorization Form

Reverse Mortgage Authorization Form Conflict of Interest Disclosure Cambridge Credit Counseling Corp provides counseling to help you make an informed decision concerning reverse mortgage products. We will

Reverse Mortgage Authorization Form Conflict of Interest Disclosure Cambridge Credit Counseling Corp provides counseling to help you make an informed decision concerning reverse mortgage products. We will

Home Affordable Refinance FAQs May 12, 2009

Home Affordable Refinance FAQs May 12, 2009 The Making Home Affordable Program includes a new initiative Home Affordable Refinance to assist homeowners in refinancing their mortgages. The primary expectation

Home Affordable Refinance FAQs May 12, 2009 The Making Home Affordable Program includes a new initiative Home Affordable Refinance to assist homeowners in refinancing their mortgages. The primary expectation

Take control of your auto loan

Take control of your auto loan A step-by-step guide Consumer Financial Protection Bureau How can this guide help you? While many people shop around for the best deal they can get on their vehicle, not

Take control of your auto loan A step-by-step guide Consumer Financial Protection Bureau How can this guide help you? While many people shop around for the best deal they can get on their vehicle, not

Mortgage Facts: How to Get the Best Home Loan Deal

Mortgage Facts: How to Get the Best Home Loan Deal By BizMove Management Training Institute Other free books by BizMove that may interest you: Free starting a business books Free management skills books

Mortgage Facts: How to Get the Best Home Loan Deal By BizMove Management Training Institute Other free books by BizMove that may interest you: Free starting a business books Free management skills books

UNIT 6 1 What is a Mortgage?

UNIT 6 1 What is a Mortgage? A mortgage is a legal document that pledges property to the lender as security for payment of a debt. In the case of a home mortgage, the debt is the money that is borrowed

UNIT 6 1 What is a Mortgage? A mortgage is a legal document that pledges property to the lender as security for payment of a debt. In the case of a home mortgage, the debt is the money that is borrowed

FAQs About RESPA for Industry

FAQs About RESPA for Industry Scope of RESPA 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien

FAQs About RESPA for Industry Scope of RESPA 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien

Integrated Disclosure Vocabulary List. Term Definition as of 8/1/2015 Adjustments and Other Credits

Integrated Disclosure Vocabulary List Term Definition as of 8/1/2015 Adjustments and Other Credits Application (triggering RESPA and TILA early disclosures) Included in this is the total amount of all

Integrated Disclosure Vocabulary List Term Definition as of 8/1/2015 Adjustments and Other Credits Application (triggering RESPA and TILA early disclosures) Included in this is the total amount of all

WHO QUALIFIES FOR FRESH START HOUSING PROGRAM

Keep in mind that in order to qualify for FRESH START there are some very important guidelines, which must be followed. Below is a brief list of the primary underwriting guidelines. Homeowners must have

Keep in mind that in order to qualify for FRESH START there are some very important guidelines, which must be followed. Below is a brief list of the primary underwriting guidelines. Homeowners must have

Residential Mortgage Ontario

Residential Mortgage Ontario Filing No. 200834 Set of Standard Charge Terms Land Registration Reform Act Filed by Bank of Montreal The following set of standard charge terms shall be deemed to be included

Residential Mortgage Ontario Filing No. 200834 Set of Standard Charge Terms Land Registration Reform Act Filed by Bank of Montreal The following set of standard charge terms shall be deemed to be included

MCC PROGRAM FREQUENTLY ASKED QUESTIONS Q.

MCC PROGRAM FREQUENTLY ASKED QUESTIONS Q. What is an MCC? A. An MCC is a federal income tax credit designed to assist persons better afford individual ownership of housing. With an MCC, the qualified homebuyer

MCC PROGRAM FREQUENTLY ASKED QUESTIONS Q. What is an MCC? A. An MCC is a federal income tax credit designed to assist persons better afford individual ownership of housing. With an MCC, the qualified homebuyer

Pay off auto loan fast

P ford residence southampton, ny Pay off auto loan fast You need a car and you don't have the cash to pay for it. If you have to finance your car, finance it the smart way. Here's how to pay your loan

P ford residence southampton, ny Pay off auto loan fast You need a car and you don't have the cash to pay for it. If you have to finance your car, finance it the smart way. Here's how to pay your loan

Once we have received and evaluated your information, we will contact you regarding your options and next steps.

We Are Here to Help You It is critical that you work with us on a resolution for any issues that affect your ability to make timely mortgage payments, whether your challenges are temporary or long term.

We Are Here to Help You It is critical that you work with us on a resolution for any issues that affect your ability to make timely mortgage payments, whether your challenges are temporary or long term.