CheckMyNPV.com Overview for Trusted Advisors

|

|

|

- Nancy McBride

- 5 years ago

- Views:

Transcription

1 Overview CheckMyNPV.com Overview for Trusted Advisors

2 Agenda MHA Overview HAMP Eligibility Criteria NPV Definition CheckMyNPV Overview and Calculator Resources Discussion / Questions 2

3 MHA Overview Making Home Affordable (MHA) Programs Home Affordable Modification Program (HAMP) Second Lien Modification Program (2MP) Home Affordable Refinance Program (HARP) Home Affordable Unemployment Program (UP) Principal Reduction Alternative (PRA) Home Affordable Foreclosure Alternatives (HAFA) 3

4 MHA Enhancements to Help More Homeowners Enhancements designed to provide relief to more homeowners and to accelerate housing market recovery. Expansion of Program Eligibility Extension of Application Deadlines MAKING HOME AFFORDABLE Increase in Investor Incentives for Principal Reduction Help for More Homeowners 4

5 Agenda MHA Overview HAMP Eligibility Criteria NPV Definition CheckMyNPV Overview and Calculator Resources Discussion / Questions 5

6 HAMP Eligibility Criteria Criteria Servicer, Investor, Insurer Origination Unpaid Principal Balance Limits Financial Hardship Guideline HAMP Tier 1 HAMP Tier 2 Guidance applies to MHA-participating servicers of mortgages not owned, guaranteed, or insured by Fannie Mae, Freddie Mac, FHA, VA, or USDA. The mortgage loan is a first lien originated on or before January 1, The unpaid principal balance, prior to capitalization, must be less than or equal to: $729,750 for a one-unit property $934,200 for a two-unit property $1,129,250 for a three-unit property $1,403,400 for a four-unit property The homeowner must be able to document a financial hardship. 6

7 HAMP Eligibility Criteria (continued) Criteria Natural Persons Occupancy Guideline HAMP Tier 1 HAMP Tier 2 The homeowner is a natural person. Mortgage loans made to business entities are not eligible for assistance under HAMP. The mortgage loan is secured by a single family property that is occupied by the homeowner as his or her principal residence. Occupancy The mortgage loan is secured by a single-family property that is used by the homeowner for rental purposes only and not occupied by the homeowner, whether as a principal residence, second home, or vacation home. The homeowner may not own more than five single-family properties in addition to the principal residence

8 Agenda MHA Overview HAMP Eligibility Criteria NPV Definition CheckMyNPV Overview and Calculator Resources Discussion / Questions 8

9 NPV Definition What is Net Present Value (NPV)? NPV compares the value of a dollar today to the value of that same dollar in the future, taking inflation and returns into account ( How Does NPV Apply to Modifications? When considering a homeowner s mortgage, investors will compare the mortgage with and without a modification to see which option produces a higher NPV. If the modified NPV is positive, the servicer must offer the modification to the homeowner. What is the NPV Evaluation Under HAMP? Servicers are required to offer the HAMP modification for an eligible mortgage if the NPV of the mortgage with the HAMP modification is greater than the mortgage as is. Reminder: The NPV evaluation result is one of many eligibility factors that must be considered in determining whether a homeowner qualifies for HAMP. 9

10 Agenda MHA Overview HAMP Eligibility Criteria NPV Definition CheckMyNPV Overview and Calculator Resources Discussion / Questions 10

11 CheckMyNPV Overview Purpose Help homeowners understand the HAMP NPV evaluation process Provide an easy to use tool for homeowners to conduct an NPV selfevaluation of their mortgage Promote and facilitate dialogue between homeowners and servicers 11

12 CheckMyNPV Overview (continued) Where Do Homeowners Get Their Information? A homeowner's Non-Approval Notice containing a list of NPV inputs used by the servicer, if an NPV evaluation was completed. A homeowner's own documents, such as mortgage statements, tax returns, income statements, and other publicly available resources. 12

13 CheckMyNPV Overview (continued) Non-Approval Notice Homeowners receive servicerprovided NPV inputs on the Non- Approval Notice, if an NPV evaluation was completed. These homeowners may use CheckMyNPV.com to review their servicer NPV results using the servicer-provided inputs or enter their own estimated input values and compare the outcomes. 13

14 CheckMyNPV Overview (continued) Homeowner Documents Homeowners without servicerprovided NPV inputs will have to estimate all input values. These homeowners may use the CheckMyNPV.com website, which uses the same underlying formula as that of HAMP servicers, to conduct an NPV evaluation with their own estimated inputs. 14

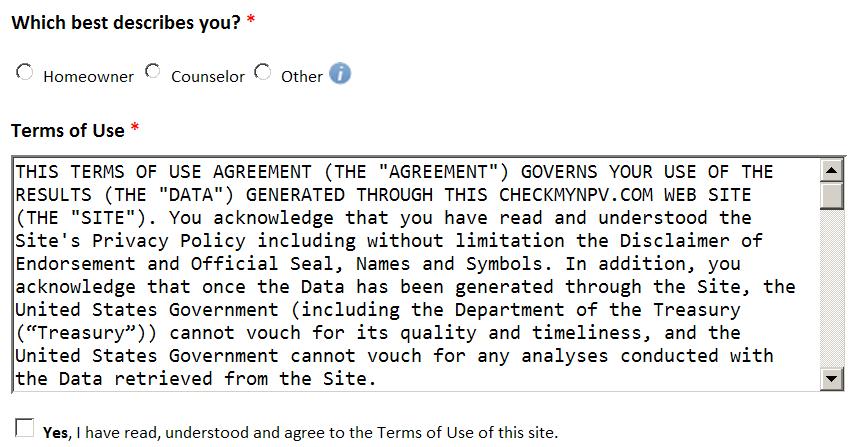

15 CheckMyNPV Calculator Steps to Complete Evaluation 1. Terms of Use Agreement 2. Servicer & Investor Information 3. Homeowner & Property Information 4. Mortgage Information 5. Monthly Payment Information 6. Review & Submit 7. NPV Evaluation Results 15

16 CheckMyNPV Calculator (continued) CheckMyNPV.com Home Page 16

CheckMyNPV.")

17 CheckMyNPV Calculator (continued) CheckMyNPV.com Home Page 17

18 1 Terms of Use Agreement

19 2 Servicer & Investor Information Look-Up Your Investor To determine if Fannie Mae or Freddie Mac is your investor, visit: Look-Up Your Servicer Visit for a complete list of mortgage servicers participating in HAMP. Discount Rate Risk Premium If you know the Discount Rate Risk Premium for your non-gse servicer, enter value here

20 3 Homeowner & Property Information 3 Data Collection Date All mortgage data that changes over time is relative to the data collection date which may not be today. Reside in Property Is this the primary residence of the homeowner? Borrower/Co-borrower Credit Scores Visit to obtain your credit score. Monthly Gross Income The total amount of monthly gross income from all homeowners on the loan

21 3 Homeowner & Property Information (cont.) 3 Reside in Property If no is selected, additional information must be provided. Housing Expense of Primary Residence The total amount of monthly expenses related to maintaining the primary residence. Monthly Gross Rental Income of Property This is the income collected from the tenants. Property Value This is the estimated or the appraised value of the property. Property Valuation Type This is the method used to value the property

22 4 Mortgage Information 4 Total First Mortgage Debt The beginning balance to calculate the terms of the proposed modification. Remaining Term on Your Mortgage Number of months that are left to be billed on the mortgage. Mortgage Insurance Coverage Percent Percentage of coverage provided by mortgage insurance. Modification Fees Paid by Investor The fees and costs paid by the investor for a HAMP modification

23 4 Mortgage Information (continued) 4 Do you have a fixed rate mortgage If mortgage is not fixed, enter No. Is your principal and interest payment scheduled to reset within 120 days from Data Collection Date? Enter either Yes or No. Next Payment Reset Date The date on which the next principal and interest payment is due. Next Reset Rate The expected interest rate on the mortgage at the next payment reset date

24 5 Monthly Payment Information Real Estate Taxes Monthly cost of real estate or property taxes. Real estate taxes may be part of the monthly escrow payment. Hazard and Flood Insurance Monthly cost of the homeowner s hazard and flood insurance coverage. This may also be a part of the monthly escrow payment. Homeowner Association Fees and Escrow Shortage Monthly homeowner or condominium association (HOA) fee payments, plus any monthly escrow shortages. If there are none, enter 0. Months Past Due Number of mortgage payments needed to be paid for the mortgage to be considered current, as of the Data Collection Date. Imminent Default The mortgage is current or less than 30 days past due and the homeowner has suffered a hardship that puts them at risk of not being able to make future payments. 24

25 6 Review & Submit Important After clicking Calculate, a homeowner can not save any information or go back to the screens so they may want to print, save a copy as a PDF, or this page to themselves. If all the information provided in this summary is correct, the homeowner may submit by clicking Calculate Information That You Provided Information That You Provided

26 7 NPV Evaluation Results 7 May Be Eligible Based on the information you provided you may be eligible for a HAMP modification. Be sure to save a copy of the information below and share it with your mortgage servicer to discuss options available to you. Please note, CheckMyNPV.com provides only an estimate of a servicer's NPV evaluation. While the NPV formula used is required to be the same as your mortgage servicer's, differences in input data and other industry-related data may result in different outputs. Your session has ended and you will not be able to run an NPV evaluation without completing this process again NPV Evaluation Results A summary of a homeowner's NPV evaluation results based on the information that was provided. For system errors, further instructions are provided based on homeowner selfidentification. 26

27 7 NPV Evaluation Results (continued) Information Calculated For You Provides the key financial mortgage terms of the proposed HAMP modification you may be eligible for. Information That You Provided A display of every field directly entered by the homeowner

28 7 NPV Evaluation Results (continued) Important information regarding NPV Evaluation results Reminder notifies homeowners of the possible limitations of results provided by the calculator

29 Agenda MHA Overview HAMP Eligibility Criteria NPV Definition CheckMyNPV Overview and Calculator Resources Discussion / Questions 29

30 CheckMyNPV.com Resources Quick Start Guide Documents and information that the homeowner will need to begin using CheckMyNPV.com Glossary of Terms Definitions to many of the terms used on the site. Frequently Asked Questions Detailed explanation of HAMP and NPV, plus answers to common homeowner inquiries. Sample HAMP Non-Approval Notice An example of the NON-APPROVAL document that the mortgage servicer may have sent to the homeowner. Input Worksheet A complete listing of all the input fields on CheckMyNPV.com Income Worksheet Instructions and worksheet for calculating monthly gross income. Information Icons (i) These are located next to the input fields. Hovering the cursor over these icons reveals further information. Total First Mortgage Debt Worksheet Interactive worksheet to obtain a rough estimate of the principal balance used by the servicer. 30

")

31 CheckMyNPV.com Resources (continued) Input Worksheet 31

32 CheckMyNPV.com Resources (continued) Income Worksheet 32

33 Industry Resources Resources HAMP Solution Center (866) HOPE Hotline HOPE Fannie Mae (800) 7Fannie KnowYourOptions.com Freddie Mac (800) Freddie, select option 2 FreddieMac.com FHA Loans FHA National Servicing Center USDA RHS Loan Centralized Servicing Center (877) HUD.gov/offices/hsg/sfh/nsc/nschome.cfm (800) VA Loans (877) HomeLoans.va.gov 33

34 Learn More About MHA Visit HMPadmin.com for official guidance, learning opportunities, newsletters, and more. 34

35 Register for MHA Training Webinars are conducted regularly on MHA program fundamentals, resources, and more. Register today at HMPadmin.com. 35

")

36 Escalate Difficult-to-Resolve Cases Trusted advisors escalate cases to HMPadmin.com. Follow up by phone to (866)

37 Subscribe to the MHA enewsletter Includes program updates, outreach events, homeowner resources, plus learning and partnership opportunities. 37

38 Understand MHA Options Find information on MHA programs and participating mortgage companies. 38

39 Visit MHAStorefront.com Order MHA brochures and posters. Have them shipped to you at no cost. 39

40 Discussion/Questions Thank You! U.S. Department of the Treasury Homeownership Preservation Office 40

CheckMyNPV.com Overview for Trusted Advisors

Overview CheckMyNPV.com Overview for Trusted Advisors Agenda 1 2 3 4 5 MHA Overview NPV Definition CheckMyNPV Overview and Calculator Resources Discussion / Questions 2 MHA Overview Making Home Affordable

Overview CheckMyNPV.com Overview for Trusted Advisors Agenda 1 2 3 4 5 MHA Overview NPV Definition CheckMyNPV Overview and Calculator Resources Discussion / Questions 2 MHA Overview Making Home Affordable

Understanding the Terms of a HAMP Modification: Interest Rate Increase, Impact, and Resources. Training Presentation for Trusted Advisors

Understanding the Terms of a HAMP Modification: Interest Rate Increase, Impact, and Resources Training Presentation for Trusted Advisors Making Making Home Making Home Affordable Home Affordable Affordable

Understanding the Terms of a HAMP Modification: Interest Rate Increase, Impact, and Resources Training Presentation for Trusted Advisors Making Making Home Making Home Affordable Home Affordable Affordable

Making Home Affordable

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

Making Home Affordable Working Together to Help Homeowners

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

HAMP Trusted Advisor 1

Home Affordable Modification Program ( ) Training for Trusted Advisors Making Home Affordable February February 2016 2016 Objectives 1 MHA Program Highlights 2 Overview 3 Eligibility Criteria 4 Protections

Home Affordable Modification Program ( ) Training for Trusted Advisors Making Home Affordable February February 2016 2016 Objectives 1 MHA Program Highlights 2 Overview 3 Eligibility Criteria 4 Protections

Home Affordable Modification Program (HAMP )

") Home Affordable Modification Program (HAMP ) Training for Trusted Advisors Objectives 1 2 3 4 5 6 Step 1 Step 2 Step 3 Step 4 Step 5 7 8 MHA Program Highlights HAMP Overview Eligibility Criteria Protections

Home Affordable Modification Program (HAMP ) Training for Trusted Advisors Objectives 1 2 3 4 5 6 Step 1 Step 2 Step 3 Step 4 Step 5 7 8 MHA Program Highlights HAMP Overview Eligibility Criteria Protections

MHA Case Escalation Process. Training Presentation for Trusted Advisors

MHA Case Escalation Process Training Presentation for Trusted Advisors 1 MHA Case Escalations Process Objectives Type of Mortgage Loan - Determines Escalation Path Escalation Contacts Definition of an

MHA Case Escalation Process Training Presentation for Trusted Advisors 1 MHA Case Escalations Process Objectives Type of Mortgage Loan - Determines Escalation Path Escalation Contacts Definition of an

Making Home Affordable

Making Home Affordable Working Together to Help Homeowners Response to the Crisis MHA is part of Administration approach to promoting stability for housing market, homeowners. Homeowner Affordability and

Making Home Affordable Working Together to Help Homeowners Response to the Crisis MHA is part of Administration approach to promoting stability for housing market, homeowners. Homeowner Affordability and

HAMP. The Hamp Program. Avoid Foreclosure. More Affordable Payments Historically Low Mortgage Rates Help With Upside Down Mortgages

The Program Works to Help Homeowners Avoid Foreclosure Avoid Foreclosure HAMP More Affordable Payments Historically Low Mortgage Rates Help With Upside Down Mortgages What is HAMP? Home Affordable Modification

The Program Works to Help Homeowners Avoid Foreclosure Avoid Foreclosure HAMP More Affordable Payments Historically Low Mortgage Rates Help With Upside Down Mortgages What is HAMP? Home Affordable Modification

Making Home Affordable Base Net Present Value (NPV) Model (v5.02) Training Module for Servicers

Model (v5.02) Training Module for Servicers") Making Home Affordable Base Net Present Value (NPV) Model (v5.02) Training Module for Servicers # Agenda 1 2 3 4 5 6 7 8 9 HAMP Eligibility Criteria Base NPV Model Overview Standard and Alternative Modification

Making Home Affordable Base Net Present Value (NPV) Model (v5.02) Training Module for Servicers # Agenda 1 2 3 4 5 6 7 8 9 HAMP Eligibility Criteria Base NPV Model Overview Standard and Alternative Modification

Standard and Alternative Waterfalls 1

Standard and Alternative Modification Waterfalls Training Presentation for Servicers Agenda 1 2 3 4 5 6 7 8 Overview of Eligibility Tier 1 Standard Modification Waterfall Tier 1 Alternative Modification

Standard and Alternative Modification Waterfalls Training Presentation for Servicers Agenda 1 2 3 4 5 6 7 8 Overview of Eligibility Tier 1 Standard Modification Waterfall Tier 1 Alternative Modification

HAMP AND FHFA (GSE) LOAN MODIFICATION UPDATE July 17, 2012

LOAN MODIFICATION UPDATE July 17, 2012") HAMP AND FHFA (GSE) LOAN MODIFICATION UPDATE July 17, 2012 Diane Thompson, NCLC, Moderator Jeff Gentes, Connecticut Fair Housing Center Lisa Sitkin, Housing and Economic Rights Advocates 0 The World of

HAMP AND FHFA (GSE) LOAN MODIFICATION UPDATE July 17, 2012 Diane Thompson, NCLC, Moderator Jeff Gentes, Connecticut Fair Housing Center Lisa Sitkin, Housing and Economic Rights Advocates 0 The World of

Home Affordable Foreclosure Alternative (HAFA) Eligibility Worksheet

Eligibility Worksheet") Loan Look Up Home Affordable Foreclosure Alternative (HAFA) Eligibility Worksheet HAFA: A Making Home Affordable (MHA) Initiative Determine the type of first lien (Fannie Mae, Freddie Mac or Treasury)

Loan Look Up Home Affordable Foreclosure Alternative (HAFA) Eligibility Worksheet HAFA: A Making Home Affordable (MHA) Initiative Determine the type of first lien (Fannie Mae, Freddie Mac or Treasury)

First Lien Modification Program Home Affordable Modification Program. Phase 1 Engagement

First Lien Modification Program Home Affordable Modification Program Objective The objective of this three part training series is to assist servicers in the execution of the Home Affordable Modification

First Lien Modification Program Home Affordable Modification Program Objective The objective of this three part training series is to assist servicers in the execution of the Home Affordable Modification

HAMP Home Affordable Modification Program UPDATE

HAMP Home Affordable Modification Program UPDATE The whole purpose of HAMP is to try and prevent foreclosures. Homeowners have to prove a hardship and go through a protocol that proves this is a good use

HAMP Home Affordable Modification Program UPDATE The whole purpose of HAMP is to try and prevent foreclosures. Homeowners have to prove a hardship and go through a protocol that proves this is a good use

Freddie Mac Standard Modification Overview for Housing Counselors. Counselor Connection Baltimore, Maryland May 8, 2012

Freddie Mac Standard Modification Overview for Housing Counselors Counselor Connection Baltimore, Maryland May 8, 2012 Objectives Understand how Servicers will apply Freddie Mac requirements for the Standard

Freddie Mac Standard Modification Overview for Housing Counselors Counselor Connection Baltimore, Maryland May 8, 2012 Objectives Understand how Servicers will apply Freddie Mac requirements for the Standard

Fannie Mae and Freddie Mac Have The Same Short Sale Rules and Policies

Fannie Mae and Freddie Mac Have The Same Short Sale Rules and Policies Effective September 1, 2011 There are approximately 3.3 million Americans who are in or close to foreclosure. Fannie Mae and Freddie

Fannie Mae and Freddie Mac Have The Same Short Sale Rules and Policies Effective September 1, 2011 There are approximately 3.3 million Americans who are in or close to foreclosure. Fannie Mae and Freddie

Supplemental Directive August 30, 2013

Supplemental Directive 13-06 August 30, 2013 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 13-06 August 30, 2013 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Specialized Loan Servicing LLC ( SLS ) Home Affordable Foreclosure Alternative (HAFA) Matrix

Home Affordable Foreclosure Alternative (HAFA) Matrix") Specialized Loan Servicing LLC ( SLS ) Home Affordable Foreclosure Alternative (HAFA) Matrix All servicers that have signed agreements with the U.S. Department of the Treasury (Treasury) to participate

Specialized Loan Servicing LLC ( SLS ) Home Affordable Foreclosure Alternative (HAFA) Matrix All servicers that have signed agreements with the U.S. Department of the Treasury (Treasury) to participate

Making Home Affordable

Making Home Affordable Today s Topics: MHA Resources MHA Refinance (HARP) MHA Loan Modifications (HAMP) Other Programs for Borrowers 2 What is Making Home Affordable? Part of President Obama s Homeowner

Making Home Affordable Today s Topics: MHA Resources MHA Refinance (HARP) MHA Loan Modifications (HAMP) Other Programs for Borrowers 2 What is Making Home Affordable? Part of President Obama s Homeowner

MHA Reason Codes and Descriptions

s and s MHA Reason Code 1 Ineligible Mortgage Loan is not eligible for modification under the MHA program because it does not meet one or more of the following basic program eligibility criteria: Mortgage

s and s MHA Reason Code 1 Ineligible Mortgage Loan is not eligible for modification under the MHA program because it does not meet one or more of the following basic program eligibility criteria: Mortgage

Supplemental Directive November 3, Home Affordable Modification Program Borrower Notices

Supplemental Directive 09-08 November 3, 2009 Home Affordable Modification Program Borrower Notices Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility,

Supplemental Directive 09-08 November 3, 2009 Home Affordable Modification Program Borrower Notices Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility,

Making Home Affordable Case Escalation Process Training Presentation for Servicers

Making Home Affordable Case Escalation Process Training Presentation for s August July 2014 2014 Making Home Home Affordable Home Affordable July 2016 Objectives Defining Escalated Cases Commonly Escalated

Making Home Affordable Case Escalation Process Training Presentation for s August July 2014 2014 Making Home Home Affordable Home Affordable July 2016 Objectives Defining Escalated Cases Commonly Escalated

Standard and Alternative Modification Waterfalls 1

HAMP Standard and Alternative Modification Waterfalls Training Presentation for Servicers Agenda Alternative Modification Waterfall References & Resources Discussion & Questions 2 3 Standard and Alternative

HAMP Standard and Alternative Modification Waterfalls Training Presentation for Servicers Agenda Alternative Modification Waterfall References & Resources Discussion & Questions 2 3 Standard and Alternative

Reporting a Notification, Loan Set-Up or Termination for a Short Sale or Deed-in-Lieu *

Reporting a Notification, Loan Set-Up or Termination for a Short Sale or Deed-in-Lieu * Description & Purpose Contents As a condition to receiving the incentive payments offered through the Home Affordable

Reporting a Notification, Loan Set-Up or Termination for a Short Sale or Deed-in-Lieu * Description & Purpose Contents As a condition to receiving the incentive payments offered through the Home Affordable

Making Home Affordable. The Second Lien Modification Program (2MP) for Servicers

for Servicers") Making Home Affordable The Second Lien Modification Program (2MP) for Servicers Agenda 1 2 3 4 5 6 7 8 9 10 11 12 13 Overview Eligibility Lien Matching Process Evaluation 2MP Modification Waterfall 2MP

Making Home Affordable The Second Lien Modification Program (2MP) for Servicers Agenda 1 2 3 4 5 6 7 8 9 10 11 12 13 Overview Eligibility Lien Matching Process Evaluation 2MP Modification Waterfall 2MP

Making Home Affordable Base Net Present Value (NPV) Model (v5.02) Training Module for Servicers

Model (v5.02) Training Module for Servicers") Making Home Affordable Base Net Present Value (NPV) Model (v5.02) Training Module for Servicers # Agenda 1 2 3 4 5 6 7 8 Base NPV Model Overview Standard and Alternative Modification Waterfalls NPV Model

Making Home Affordable Base Net Present Value (NPV) Model (v5.02) Training Module for Servicers # Agenda 1 2 3 4 5 6 7 8 Base NPV Model Overview Standard and Alternative Modification Waterfalls NPV Model

Streamline HAMP Modification Process. Training for Servicers

Streamline HAMP Modification Process Training for Servicers Agenda 1 2 3 64 5 Overview Eligibility Criteria Streamline HAMP Policy and Streamline HAMP NPV Tool Streamline HAMP Process Resources 2 MHA Offers

Streamline HAMP Modification Process Training for Servicers Agenda 1 2 3 64 5 Overview Eligibility Criteria Streamline HAMP Policy and Streamline HAMP NPV Tool Streamline HAMP Process Resources 2 MHA Offers

Supplemental Directive October 18, 2013

Supplemental Directive 13-09 October 18, 2013 Making Home Affordable Program CFPB Mortgage Servicing Regulations In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 13-09 October 18, 2013 Making Home Affordable Program CFPB Mortgage Servicing Regulations In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

2MP Servicer Training 1

Making Home Affordable The Second Lien Modification Program (2MP) for Servicers Agenda 1 2 3 4 5 6 7 8 9 10 11 12 13 Overview Eligibility Lien Matching Process Evaluation 2MP Modification Waterfall 2MPTrial

Making Home Affordable The Second Lien Modification Program (2MP) for Servicers Agenda 1 2 3 4 5 6 7 8 9 10 11 12 13 Overview Eligibility Lien Matching Process Evaluation 2MP Modification Waterfall 2MPTrial

Version 3.4 As of December 15, 2011

Version 3.4 As of December 15, 2011 Table of Contents MHA Handbook v3.4 1 FOREWORD... 12 OVERVIEW... 13 CHAPTER I: MAKING HOME AFFORDABLE PROGRAM (MHA)... 18 1 SERVICER PARTICIPATION IN MHA... 19 1.1 SERVICER

Version 3.4 As of December 15, 2011 Table of Contents MHA Handbook v3.4 1 FOREWORD... 12 OVERVIEW... 13 CHAPTER I: MAKING HOME AFFORDABLE PROGRAM (MHA)... 18 1 SERVICER PARTICIPATION IN MHA... 19 1.1 SERVICER

Navigating the Loan Modification Process Part III. Presented by: Empire Justice Center Kevin Purcell, Esq.

Navigating the Loan Modification Process Part III Presented by: Empire Justice Center Kevin Purcell, Esq. 1 Other MHA Programs HAMP Tier Two Principal Reduction Alternative Home Affordable Unemployment

Navigating the Loan Modification Process Part III Presented by: Empire Justice Center Kevin Purcell, Esq. 1 Other MHA Programs HAMP Tier Two Principal Reduction Alternative Home Affordable Unemployment

Making Home Affordable (MHA) Compensation Last Updated: April 30, 2015

Compensation Last Updated: April 30, 2015") Making Home Affordable (MHA) Compensation Last Updated: April 30, 2015 Program Name Frequency and Timing Payee/Beneficiary Amount Accrual and Notes Servicer Incentive One time Servicer/Servicer Non-GSE

Making Home Affordable (MHA) Compensation Last Updated: April 30, 2015 Program Name Frequency and Timing Payee/Beneficiary Amount Accrual and Notes Servicer Incentive One time Servicer/Servicer Non-GSE

Supplemental Directive November 30, 2012

Supplemental Directive 12-09 November 30, 2012 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 12-09 November 30, 2012 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Home Affordable Modification Program (HAMP )

") Home Affordable Modification Program (HAMP ) Training for Servicers Part 2 of 2 MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure Transition from Home Ownership

Home Affordable Modification Program (HAMP ) Training for Servicers Part 2 of 2 MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure Transition from Home Ownership

Home Affordable Unemployment Program (UP)

") Home Affordable Unemployment Program (UP) Training for Servicers 1 Agenda 1 2 Phase 1 Phase 2 Phase 3 3 4 Overview UP Process Evaluation Phase Forbearance Period Transition Phase Reporting Requirements

Home Affordable Unemployment Program (UP) Training for Servicers 1 Agenda 1 2 Phase 1 Phase 2 Phase 3 3 4 Overview UP Process Evaluation Phase Forbearance Period Transition Phase Reporting Requirements

Freddie Mac Standard and Streamlined Modification. Reference Guide. September 2017

Freddie Mac Standard and Streamlined Modification Reference Guide September 2017 This Page Intentionally Left Blank Table of Contents Introduction... 1 What is a Loan Modification?... 1 Freddie Mac Standard

Freddie Mac Standard and Streamlined Modification Reference Guide September 2017 This Page Intentionally Left Blank Table of Contents Introduction... 1 What is a Loan Modification?... 1 Freddie Mac Standard

HAMP Servicer Training 1

Home Affordable Modification Program (HAMP ) Training for Servicers Part 2 of 2 MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure Transition from Home Ownership

Home Affordable Modification Program (HAMP ) Training for Servicers Part 2 of 2 MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure Transition from Home Ownership

Supplemental Directive September 30, 2014

Supplemental Directive 14-03 September 30, 2014 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 14-03 September 30, 2014 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive January 29, 2015

Supplemental Directive 15-01 January 29, 2015 Making Home Affordable Program MHA Program Updates In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program to stabilize

Supplemental Directive 15-01 January 29, 2015 Making Home Affordable Program MHA Program Updates In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program to stabilize

Making Home Affordable Program Dodd-Frank Certification, Internal Quality Assurance and Verification of Income Update

Supplemental Directive 11-01 February 17, 2011 Making Home Affordable Program Dodd-Frank Certification, Internal Quality Assurance and Verification of Income Update In February 2009, the Obama Administration

Supplemental Directive 11-01 February 17, 2011 Making Home Affordable Program Dodd-Frank Certification, Internal Quality Assurance and Verification of Income Update In February 2009, the Obama Administration

Supplemental Directive December 10, 2013

Supplemental Directive 13-12 December 10, 2013 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 13-12 December 10, 2013 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Workout Hierarchy for Fannie Mae Conventional Loans NOTE: Refer to the Fannie Mae Servicing Guide

Workout Hierarchy for Fannie Mae Conventional Loans The following table is a summary of Fannie Mae workout options available to assist borrowers experiencing financial hardship. The servicer must first

Workout Hierarchy for Fannie Mae Conventional Loans The following table is a summary of Fannie Mae workout options available to assist borrowers experiencing financial hardship. The servicer must first

UNIFORM BORROWER ASSISTANCE FORM

If you are experiencing a temporary or long term hardship and need help, you must complete and submit this form along with other required documentation to be considered for available solutions. On this

If you are experiencing a temporary or long term hardship and need help, you must complete and submit this form along with other required documentation to be considered for available solutions. On this

Retrieving and Interpreting the NPV Test Results

Retrieving and Interpreting the NPV Test Results When determining whether a borrower is eligible for a modification under the Home Affordable Modification Program SM (HAMP ), the loan must be evaluated

Retrieving and Interpreting the NPV Test Results When determining whether a borrower is eligible for a modification under the Home Affordable Modification Program SM (HAMP ), the loan must be evaluated

GUIDING PRINCIPLES FOR THE FUTURE OF LOSS MITIGATION: HOW THE LESSONS LEARNED FROM THE FINANCIAL CRISIS CAN INFLUENCE THE PATH FORWARD

GUIDING PRINCIPLES FOR THE FUTURE OF LOSS MITIGATION: HOW THE LESSONS LEARNED FROM THE FINANCIAL CRISIS CAN INFLUENCE THE PATH FORWARD July 25, 2016 TABLE OF CONTENTS HOW THE LESSONS LEARNED FROM THE FINANCIAL

GUIDING PRINCIPLES FOR THE FUTURE OF LOSS MITIGATION: HOW THE LESSONS LEARNED FROM THE FINANCIAL CRISIS CAN INFLUENCE THE PATH FORWARD July 25, 2016 TABLE OF CONTENTS HOW THE LESSONS LEARNED FROM THE FINANCIAL

Loan Modifications: Determining What Programs are Available. Joseph Rebella Senior Staff Attorney MFY Legal Services, Inc.

Loan Modifications: Determining What Programs are Available Joseph Rebella Senior Staff Attorney MFY Legal Services, Inc. Different Loan Modification Programs The availability of loan modification programs

Loan Modifications: Determining What Programs are Available Joseph Rebella Senior Staff Attorney MFY Legal Services, Inc. Different Loan Modification Programs The availability of loan modification programs

Loan Workout Hierarchy for Fannie Mae Conventional Loans

Loan Workout Hierarchy for Fannie Mae Conventional Loans The following table identifies the Fannie Mae loss mitigation options that are available to assist borrowers experiencing financial hardship. Generally,

Loan Workout Hierarchy for Fannie Mae Conventional Loans The following table identifies the Fannie Mae loss mitigation options that are available to assist borrowers experiencing financial hardship. Generally,

FHFA Perspectives on Foreclosure Prevention and Principal Forgiveness

FHFA Perspectives on Foreclosure Prevention and Principal Forgiveness Edward DeMarco, Acting Director Federal Housing Finance Agency The Brookings Institution April 10, 2012 My goal today is to answer

FHFA Perspectives on Foreclosure Prevention and Principal Forgiveness Edward DeMarco, Acting Director Federal Housing Finance Agency The Brookings Institution April 10, 2012 My goal today is to answer

Home Affordable Modification Program Policies and Procedures Manual

Home Affordable Modification Program Policies and Procedures Manual Policies and procedures herein apply generally to loans subserviced by Franklin Credit Management Corporation, and are integrated with

Home Affordable Modification Program Policies and Procedures Manual Policies and procedures herein apply generally to loans subserviced by Franklin Credit Management Corporation, and are integrated with

Foreclosure Prevention Certification Exam Study Guide Sample Questions With Answers from Previous Exams

Foreclosure Prevention Certification Exam Study Guide Sample Questions With Answers from Previous Exams Exam structure and tips: Structure: the exam is composed of 20-25 questions divided into two parts

Foreclosure Prevention Certification Exam Study Guide Sample Questions With Answers from Previous Exams Exam structure and tips: Structure: the exam is composed of 20-25 questions divided into two parts

Home Affordable Foreclosure Alternatives. September 2011 Making Home Affordable

Home Affordable Foreclosure Alternatives Home Affordable Foreclosure Alternatives HAFA This presentation will cover the following: 1 Overview 2 Advantages 3 Components and Process Phases 4 Resources 5

Home Affordable Foreclosure Alternatives Home Affordable Foreclosure Alternatives HAFA This presentation will cover the following: 1 Overview 2 Advantages 3 Components and Process Phases 4 Resources 5

Freddie Mac Standard and Streamlined Modification Reference Guide. April 2015

Freddie Mac Standard and Streamlined Modification Reference Guide April 2015 Table of Contents Introduction... 1 What is a Loan Modification?... 1 Freddie Mac Standard Modifications... 2 Ineligible Criteria

Freddie Mac Standard and Streamlined Modification Reference Guide April 2015 Table of Contents Introduction... 1 What is a Loan Modification?... 1 Freddie Mac Standard Modifications... 2 Ineligible Criteria

Supplemental Directive December 21, 2017

Supplemental Directive 17-02 December 21, 2017 Making Home Affordable Program Handbook for Servicers Version 5.2 and Administrative Clarifications In February 2009, the Federal Government introduced the

Supplemental Directive 17-02 December 21, 2017 Making Home Affordable Program Handbook for Servicers Version 5.2 and Administrative Clarifications In February 2009, the Federal Government introduced the

Loan Modifications 101 Tara Twomey National Consumer Law Center

Loan ifications 101 Tara Twomey National Consumer Law Center By the time the foreclosure crisis reached its peak in 2008, the climate for loan modifications had changed dramatically from earlier options

Loan ifications 101 Tara Twomey National Consumer Law Center By the time the foreclosure crisis reached its peak in 2008, the climate for loan modifications had changed dramatically from earlier options

Making Home Affordable Program Performance Report Third Quarter 2015

Making Home Affordable PROGRAM PERFORMANCE REPORT THROUGH THE THIRD QUARTER OF 2015 MHA AT-A-GLANCE Approximately 2.5 Million Homeowner Assistance Actions have taken place under Making Home Affordable

Making Home Affordable PROGRAM PERFORMANCE REPORT THROUGH THE THIRD QUARTER OF 2015 MHA AT-A-GLANCE Approximately 2.5 Million Homeowner Assistance Actions have taken place under Making Home Affordable

Chase Home Affordable Foreclosure Alternative (HAFA) Matrix

Matrix") Chase Home Affordable Foreclosure Alternative (HAFA) Matrix All servicers that have signed agreements with the U.S. Department of the Treasury (Treasury) to participate in the Home Affordable Modification

Chase Home Affordable Foreclosure Alternative (HAFA) Matrix All servicers that have signed agreements with the U.S. Department of the Treasury (Treasury) to participate in the Home Affordable Modification

Version 2.0 As of September 22, 2010

Version 2.0 As of September 22, 2010 MHA Handbook v2.0 1 FOREWORD... 6 OVERVIEW... 7 CHAPTER I: MAKING HOME AFFORDABLE PROGRAM (MHA)... 11 1 SERVICER PARTICIPATION IN MHA... 12 1.1 SERVICER PARTICIPATION

Version 2.0 As of September 22, 2010 MHA Handbook v2.0 1 FOREWORD... 6 OVERVIEW... 7 CHAPTER I: MAKING HOME AFFORDABLE PROGRAM (MHA)... 11 1 SERVICER PARTICIPATION IN MHA... 12 1.1 SERVICER PARTICIPATION

BORROWER FREQUENTLY ASKED QUESTIONS

BORROWER FREQUENTLY ASKED QUESTIONS Revised: June 8, 2010 What is "Making Home Affordable" all about? The Making Home Affordable Program is part of the Obama Administration's broad, comprehensive strategy

BORROWER FREQUENTLY ASKED QUESTIONS Revised: June 8, 2010 What is "Making Home Affordable" all about? The Making Home Affordable Program is part of the Obama Administration's broad, comprehensive strategy

Servicemember Financial Protection

Servicemember Financial Protection Outlook Live Webinar September 10, 2012 An Interagency Discussion of Recent Servicemember Financial Protection Guidance and Compliance with the Servicemembers Civil Relief

Servicemember Financial Protection Outlook Live Webinar September 10, 2012 An Interagency Discussion of Recent Servicemember Financial Protection Guidance and Compliance with the Servicemembers Civil Relief

WORRIED. about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA)

") WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) About HAFA Keeping families in their homes is a top priority for REALTORS. While there are loan

WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) About HAFA Keeping families in their homes is a top priority for REALTORS. While there are loan

National Foreclosure Mitigation Counseling Program Funding Announcement for Round 9 Funds

National Foreclosure Mitigation Counseling Program Funding Announcement for Round 9 Funds Revised January 22, 2015 National Foreclosure Mitigation Counseling Program Round 9 Funding Announcement October

National Foreclosure Mitigation Counseling Program Funding Announcement for Round 9 Funds Revised January 22, 2015 National Foreclosure Mitigation Counseling Program Round 9 Funding Announcement October

MODIFICATION REQUEST FORM HARP / Distressed Modifications / Traditional Modifications

MODIFICATION REQUEST FORM HARP / Distressed Modifications / Traditional Modifications United Guaranty Residential Insurance Company P. O. Box 21367 Greensboro, NC 27420-1367 Phone: 888.822.5584 (select

MODIFICATION REQUEST FORM HARP / Distressed Modifications / Traditional Modifications United Guaranty Residential Insurance Company P. O. Box 21367 Greensboro, NC 27420-1367 Phone: 888.822.5584 (select

UNIFORM BORROWER ASSISTANCE FORM

If you are experiencing a temporary or long-term hardship and need help, you must complete and submit this form along with other required documentation to be considered for available solutions. On this

If you are experiencing a temporary or long-term hardship and need help, you must complete and submit this form along with other required documentation to be considered for available solutions. On this

Version 3.0 As of December 2, 2010

Version 3.0 As of December 2, 2010 Table of Contents MHA Handbook v3.0 1 FOREWORD... 10 OVERVIEW... 11 CHAPTER I: MAKING HOME AFFORDABLE PROGRAM (MHA)... 16 1 SERVICER PARTICIPATION IN MHA... 17 1.1 SERVICER

Version 3.0 As of December 2, 2010 Table of Contents MHA Handbook v3.0 1 FOREWORD... 10 OVERVIEW... 11 CHAPTER I: MAKING HOME AFFORDABLE PROGRAM (MHA)... 16 1 SERVICER PARTICIPATION IN MHA... 17 1.1 SERVICER

Supplemental Directive March 1, 2013

Supplemental Directive 13-01 March 1, 2013 Making Home Affordable Program Making Home Affordable Outreach and Borrower Intake Project In February 2009, the Obama Administration introduced the Making Home

Supplemental Directive 13-01 March 1, 2013 Making Home Affordable Program Making Home Affordable Outreach and Borrower Intake Project In February 2009, the Obama Administration introduced the Making Home

HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL V5.0 MODEL DOCUMENTATION

MODEL V5.0 MODEL DOCUMENTATION") HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL V5.0 MODEL DOCUMENTATION UPDATE: OCTOBER 2, 2014 Contents Table of Contents I. Overview... 3 II. Significant Model Changes from Version

HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL V5.0 MODEL DOCUMENTATION UPDATE: OCTOBER 2, 2014 Contents Table of Contents I. Overview... 3 II. Significant Model Changes from Version

If you need assistance, contact us immediately at: Dear PNC Mortgage Customer: Take the First Step

We are here to help Dear : We know how challenging it can be when you re experiencing difficulty in keeping your mortgage payments current. Whether your situation is temporary or long-term, PNC Mortgage

We are here to help Dear : We know how challenging it can be when you re experiencing difficulty in keeping your mortgage payments current. Whether your situation is temporary or long-term, PNC Mortgage

PERSONAL FINANCIAL ANALYSIS

1 PERSONAL FINANCIAL ANALYSIS If you are experiencing a temporary or long-term hardship and need help, you must complete and submit this form along with other required documentation to be considered for

1 PERSONAL FINANCIAL ANALYSIS If you are experiencing a temporary or long-term hardship and need help, you must complete and submit this form along with other required documentation to be considered for

Servicing and Loss Mitigation. Jennifer Schultz, Esq. Community Legal Services, Inc W. Erie Ave. Philadelphia, PA

Servicing and Loss Mitigation Jennifer Schultz, Esq. Community Legal Services, Inc. 1410 W. Erie Ave. Philadelphia, PA 19140 jschultz@clsphila.org What kind of loan do you have? FHA GSE Origination-based

Servicing and Loss Mitigation Jennifer Schultz, Esq. Community Legal Services, Inc. 1410 W. Erie Ave. Philadelphia, PA 19140 jschultz@clsphila.org What kind of loan do you have? FHA GSE Origination-based

Freddie Mac Flex Modification. Reference Guide. September 2017

Freddie Mac Flex Modification Reference Guide September 2017 This Page Intentionally Left Blank Table of Contents Introduction... 1 When to Implement the Flex Modification... 1 Eligibility Requirements

Freddie Mac Flex Modification Reference Guide September 2017 This Page Intentionally Left Blank Table of Contents Introduction... 1 When to Implement the Flex Modification... 1 Eligibility Requirements

Loss Mitigation Application

Loss Mitigation Application If you are experiencing a financial hardship and need help, please complete this form. In order to recommend you for a loss mitigation program, we must receive the following

Loss Mitigation Application If you are experiencing a financial hardship and need help, please complete this form. In order to recommend you for a loss mitigation program, we must receive the following

NEIGHBORHOOD HOUSING & DEVELOPMENT CORPORATION 633 NW 8 TH AVE. GAINESVILLE, FL TELEPHONE (352) FAX (352)

FAX (352)") NEIGHBORHOOD HOUSING & DEVELOPMENT CORPORATION 633 NW 8 TH AVE. GAINESVILLE, FL 32601 TELEPHONE (352)380-9119 FAX (352)380-9170 WWW.GNHDC.ORG Dear Homeowner, We re so glad you took that tough first step

NEIGHBORHOOD HOUSING & DEVELOPMENT CORPORATION 633 NW 8 TH AVE. GAINESVILLE, FL 32601 TELEPHONE (352)380-9119 FAX (352)380-9170 WWW.GNHDC.ORG Dear Homeowner, We re so glad you took that tough first step

Making Home Affordable Program Performance Report Second Quarter 2014

Making Home Affordable PROGRAM PERFORMANCE REPORT THROUGH THE SECOND QUARTER OF 2014 MHA AT-A-GLANCE More than 2.1 Million Homeowner Assistance Actions have taken place under Making Home Affordable (MHA)

Making Home Affordable PROGRAM PERFORMANCE REPORT THROUGH THE SECOND QUARTER OF 2014 MHA AT-A-GLANCE More than 2.1 Million Homeowner Assistance Actions have taken place under Making Home Affordable (MHA)

Supplemental Directive January 28, Home Affordable Modification Program Program Update and Resolution of Active Trial Modifications

Supplemental Directive 10-01 January 28, 2010 Home Affordable Modification Program Program Update and Resolution of Active Trial Modifications Background In Supplemental Directive 09-01, the Treasury Department

Supplemental Directive 10-01 January 28, 2010 Home Affordable Modification Program Program Update and Resolution of Active Trial Modifications Background In Supplemental Directive 09-01, the Treasury Department

Foreclosure Diversion Program Information Session. Understanding and Preparing for Mediation

Foreclosure Diversion Program Information Session Understanding and Preparing for Mediation *For more detailed information and additional resources, go to the Pine Tree Legal website at www.ptla.org/foreclosure-prevention-toolkit

Foreclosure Diversion Program Information Session Understanding and Preparing for Mediation *For more detailed information and additional resources, go to the Pine Tree Legal website at www.ptla.org/foreclosure-prevention-toolkit

WORRIED. about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA)

") WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) Keeping families in their homes is a top priority for REALTORS. Unfortunately, it is not always

WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) Keeping families in their homes is a top priority for REALTORS. Unfortunately, it is not always

The deadline for implementation by servicers was April 5, Mortgage delinquent or default is reasonably foreseeable.

1. What is HAFA? The Home Affordable Foreclosure Alternatives Program, known as HAFA, is designed to help owners (referred to below as borrowers) who are unable to retain their home under the Home Affordable

1. What is HAFA? The Home Affordable Foreclosure Alternatives Program, known as HAFA, is designed to help owners (referred to below as borrowers) who are unable to retain their home under the Home Affordable

Property Information. Address:

Member Number: Account Number: If you are having mortgage payment challenges, please complete and submit this application, along with the required documentation, to General Electric Credit Union via mail:

Member Number: Account Number: If you are having mortgage payment challenges, please complete and submit this application, along with the required documentation, to General Electric Credit Union via mail:

Making Home Affordable Program Principal Reduction Alternative Update

Supplemental Directive 10-14 October 15, 2010 Making Home Affordable Program Principal Reduction Alternative Update In February 2009, the Obama Administration introduced the Making Home Affordable Program

Supplemental Directive 10-14 October 15, 2010 Making Home Affordable Program Principal Reduction Alternative Update In February 2009, the Obama Administration introduced the Making Home Affordable Program

Lisa Sitkin National Housing Law Project May 23, 2017

Helping Your Clients Avoid Foreclosure after HAMP: A Refresher and Update on the California Homeowner Bill of Rights and Related Regulations and Programs 1 Lisa Sitkin National Housing Law Project May

Helping Your Clients Avoid Foreclosure after HAMP: A Refresher and Update on the California Homeowner Bill of Rights and Related Regulations and Programs 1 Lisa Sitkin National Housing Law Project May

Early Delinquency Intervention Workbook

Early Delinquency Intervention Workbook If you are having financial difficulties, being able to maintain a mortgage payment can be stressful. In such trying times, it can be hard to make rational decisions

Early Delinquency Intervention Workbook If you are having financial difficulties, being able to maintain a mortgage payment can be stressful. In such trying times, it can be hard to make rational decisions

Know Your Products. Marc Kaplan, Sr. VP Retail Sales

Know Your Products Marc Kaplan, Sr. VP Retail Sales 1 Product Overview Agenda 1. Fannie Mae Federal National Mortgage Association (FNMA) 2. Freddie Mac Federal Home Loan Mortgage Corp. (FHLMC) 3. FHA Federal

Know Your Products Marc Kaplan, Sr. VP Retail Sales 1 Product Overview Agenda 1. Fannie Mae Federal National Mortgage Association (FNMA) 2. Freddie Mac Federal Home Loan Mortgage Corp. (FHLMC) 3. FHA Federal

Uniform Borrower Assistance Form

Uniform Borrower Assistance Form If you are experiencing a temporary or long term hardship and need help, you must complete and submit this form along with other required documentation to be considered

Uniform Borrower Assistance Form If you are experiencing a temporary or long term hardship and need help, you must complete and submit this form along with other required documentation to be considered

TEACHERS RETIREMENT BOARD INVESTMENT COMMITTEE. SUBJECT: Home Loan Program 2012 Mid-Year Report CONSENT: X ATTACHMENT(S): 1

: 1") TEACHERS RETIREMENT BOARD INVESTMENT COMMITTEE SUBJECT: Home Loan Program 2012 Mid-Year Report ITEM NUMBER: 4c CONSENT: X ATTACHMENT(S): 1 ACTION: DATE OF MEETING: September 7, 2012 INFORMATION: X PRESENTER(S):

TEACHERS RETIREMENT BOARD INVESTMENT COMMITTEE SUBJECT: Home Loan Program 2012 Mid-Year Report ITEM NUMBER: 4c CONSENT: X ATTACHMENT(S): 1 ACTION: DATE OF MEETING: September 7, 2012 INFORMATION: X PRESENTER(S):

[Address of Borrower] [Loan #] [Date] RE: Acknowledgement of Request for Short Sale

![[Address of Borrower] [Loan #] [Date] RE: Acknowledgement of Request for Short Sale](/thumbs/90/103076486.jpg "[Address of Borrower] [Loan #] [Date] RE: Acknowledgement of Request for Short Sale") [Name of Servicer] [Address of Servicer] [Loan #] [Servicer FAX] [Servicer Email] [Name of Borrower] [Name of Co-Borrower] [Address of Borrower] [Borrower Phone] [Borrower Email] [Date] RE: Acknowledgement

[Name of Servicer] [Address of Servicer] [Loan #] [Servicer FAX] [Servicer Email] [Name of Borrower] [Name of Co-Borrower] [Address of Borrower] [Borrower Phone] [Borrower Email] [Date] RE: Acknowledgement

Example H.O.M.E. Report- Beta1 of 42.

Example H.O.M.E. Report- Beta1 of 42. PREPARED BY: BORROWER(s): PROPERTY ADDRESS: DIY Internal Demo Company, 123 swe 12 ave, miami, FL 33167, (786) 787-8878 (Phone), (987) 897-8978 (fascimile) HAMP Example

Example H.O.M.E. Report- Beta1 of 42. PREPARED BY: BORROWER(s): PROPERTY ADDRESS: DIY Internal Demo Company, 123 swe 12 ave, miami, FL 33167, (786) 787-8878 (Phone), (987) 897-8978 (fascimile) HAMP Example

Fannie Mae Flex Modification. 1. Welcome Intro. 1.1 Welcome. 1.2 Objectives. Notes: Notes: Published by Articulate Storyline

Fannie Mae Flex Modification 1. Welcome Intro 1.1 Welcome Notes: Welcome, and thank you for taking time to view the Fannie Mae Flex Modification course. 1.2 Objectives Notes: Published by Articulate Storyline

Fannie Mae Flex Modification 1. Welcome Intro 1.1 Welcome Notes: Welcome, and thank you for taking time to view the Fannie Mae Flex Modification course. 1.2 Objectives Notes: Published by Articulate Storyline

HUD US DEPT OF HOUSING & URBAN DEVELOPMENT: Fannie Mae & Freddie Mac s Flex Modification Program

Final Transcript HUD US DEPT OF HOUSING & URBAN DEVELOPMENT: Fannie Mae & Freddie Mac s Flex Modification Program SPEAKERS Virginia Holman Lorraine Griscavage-Frisbee Jeff Zitelman Bryan Camilli PRESENTATION

Final Transcript HUD US DEPT OF HOUSING & URBAN DEVELOPMENT: Fannie Mae & Freddie Mac s Flex Modification Program SPEAKERS Virginia Holman Lorraine Griscavage-Frisbee Jeff Zitelman Bryan Camilli PRESENTATION

What is the Servicing Alignment Initiative? Overview:

Servicing Alignment Initiative: Freddie Mac Requirements Overview for Housing Counselors Orlando, September 27, 2011 What is the Servicing Alignment Initiative? Overview: Freddie Mac launched a comprehensive

Servicing Alignment Initiative: Freddie Mac Requirements Overview for Housing Counselors Orlando, September 27, 2011 What is the Servicing Alignment Initiative? Overview: Freddie Mac launched a comprehensive

Bank of america loan modification help

Bank of america loan modification help The Borg System is 100 % Bank of america loan modification help Get the home loan help you need now. If you're having trouble paying your mortgage, Bank of America

Bank of america loan modification help The Borg System is 100 % Bank of america loan modification help Get the home loan help you need now. If you're having trouble paying your mortgage, Bank of America

EARLY DELINQUENCY INTERVENTION WORKBOOK

EARLY DELINQUENCY INTERVENTION WORKBOOK If you are having financial difficulties, being able to maintain a mortgage payment can be stressful. In such trying times, it can be hard to make rational decisions

EARLY DELINQUENCY INTERVENTION WORKBOOK If you are having financial difficulties, being able to maintain a mortgage payment can be stressful. In such trying times, it can be hard to make rational decisions

Freddie Mac Principal Reduction Modification Quick Reference

Freddie Mac Principal Reduction Modification Quick Reference The Freddie Mac Principal Reduction Modification is a temporary offering designed to assist those borrowers who are most at risk of foreclosure

Freddie Mac Principal Reduction Modification Quick Reference The Freddie Mac Principal Reduction Modification is a temporary offering designed to assist those borrowers who are most at risk of foreclosure

Supplemental Directive June 3, Home Affordable Modification Program Modification of Loans with Principal Reduction Alternative

Supplemental Directive 10-05 June 3, 2010 Home Affordable Modification Program Modification of Loans with Principal Reduction Alternative Background In Supplemental Directive 09-01, the Treasury Department

Supplemental Directive 10-05 June 3, 2010 Home Affordable Modification Program Modification of Loans with Principal Reduction Alternative Background In Supplemental Directive 09-01, the Treasury Department

Supplemental Directive December 10, Making Home Affordable Program Program End Date and Administrative Clarifications

Supplemental Directive 18-01 December 10, 2018 Making Home Affordable Program Program End Date and Administrative Clarifications In February 2009, the Making Home Affordable (MHA) Program was introduced

Supplemental Directive 18-01 December 10, 2018 Making Home Affordable Program Program End Date and Administrative Clarifications In February 2009, the Making Home Affordable (MHA) Program was introduced

Bulletin. TO: All Freddie Mac Servicers December 12, 2008

Bulletin TO: All Freddie Mac Servicers December 12, 2008 SUBJECTS Servicing requirements are provided in this Single-Family Seller/Servicer Guide (Guide) Bulletin. With this Bulletin we are: Providing

Bulletin TO: All Freddie Mac Servicers December 12, 2008 SUBJECTS Servicing requirements are provided in this Single-Family Seller/Servicer Guide (Guide) Bulletin. With this Bulletin we are: Providing

All of the changes announced in this Bulletin are effective immediately unless otherwise noted.

TO: Freddie Mac Servicers June 13, 2018 2018-9 SUBJECT: SERVICING UPDATES This Guide Bulletin announces: Forbearance plan requirements Consolidation and restructuring of our requirements for short-term,

TO: Freddie Mac Servicers June 13, 2018 2018-9 SUBJECT: SERVICING UPDATES This Guide Bulletin announces: Forbearance plan requirements Consolidation and restructuring of our requirements for short-term,

HAMP Resolution Matrix

Homeowner HAMP Eligibility Issues HAMP Resolution Matrix 1 (1) Verify whether the property is owner occupied (for HAMP Tier 2 rental properties, must have missed 2 or more payments). Homeowner is (2) Verify

Homeowner HAMP Eligibility Issues HAMP Resolution Matrix 1 (1) Verify whether the property is owner occupied (for HAMP Tier 2 rental properties, must have missed 2 or more payments). Homeowner is (2) Verify

Keep Your Home California. Foreclosure Prevention Programs

Keep Your Home California Foreclosure Prevention Programs Keep Your Home California Program Objectives Help prevent avoidable foreclosures for eligible low and moderate income homeowners Address financial

Keep Your Home California Foreclosure Prevention Programs Keep Your Home California Program Objectives Help prevent avoidable foreclosures for eligible low and moderate income homeowners Address financial

Home Affordable Refinance (DU Refi Plus and Refi Plus) FAQs

FAQs") Home Affordable Refinance (DU Refi Plus and Refi Plus) FAQs February 3, 2015 The Home Affordable Refinance Program (HARP) is designed to assist homeowners in refinancing their mortgages even if they owe

Home Affordable Refinance (DU Refi Plus and Refi Plus) FAQs February 3, 2015 The Home Affordable Refinance Program (HARP) is designed to assist homeowners in refinancing their mortgages even if they owe