SMART MONEY MANAGEMENT

|

|

|

- Gwenda Kathleen Black

- 5 years ago

- Views:

Transcription

1 How much money did you earn last month? When was the last time you borrowed money? Have you opened a savings account? Why do you have to pay interest on a loan? With many tips and useful tools SMART MONEY MANAGEMENT A Basic Financial Literacy Booklet

2 TABLE OF CONTENTS 1. Why do loans cost money? Which services do banks, MFIs and cooperatives offer for you? Financial and liquidity management How to select the right loan for you Be safe and save How to choose financial service providers HOW TO USE THIS BOOK Explains why something is useful and important to know Explains technical terms Summarizes the most important points you should check when making decisions/choices regarding financial services Refers you to related topics and more in-depth information If you want to apply what you have learned in this book, you can find templates in the back that you can use to practice your new skills! If you liked the topics and want to learn more: check out the back of this book where you can find additional stories and information! 2

3 FOREWORD At the moment, financial services in Myanmar are offered by banks, microfinance institutions and cooperatives as well as other providers. Our research has shown that the knowledge of financial services is lower in some parts of Myanmar than in others. Additionally, people from rural areas in Myanmar are particularly interested in learning more about financial services and financial management (especially for their family income and expenses). A number of institutions and people are dedicated to improve financial literacy levels in Myanmar by providing education and training. Our objective with this book is to empower people in their use of financial services by providing basic information and concepts about financial services in Myanmar. ACKNOWLEDGEMENT AND DISCLAIMER This document is supported with financial assistance from Australia, Denmark, the European Union, France, Ireland, Italy, Luxembourg, the Netherlands, New Zealand, Sweden, Switzerland, the United Kingdom, the United States of America, and the Mitsubishi Corporation through the Livelihoods and Food Security Trust Fund (LIFT). We thank their kind contributions to improving the livelihoods and food security of the rural poor in Myanmar. The views expressed herein should not be taken to reflect the official opinion of the LIFT donors. We would like to thank everyone, institutions and people, who supported this project and made this booklet possible. 3

.")

and lend money to")

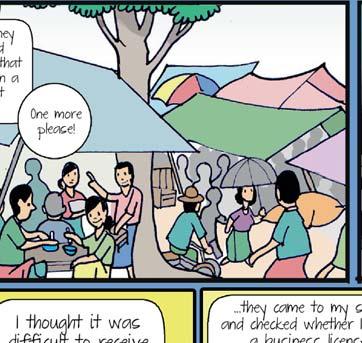

4 Saving & borrowing money 1. WHY DO LOANS COST MONEY? There are many different types of financial institutions. Most relevant in Myanmar at this time are banks as well as cooperatives or micro finance institutions (MFIs). The most basic function of many financial institutions is to collect money from people who do not need their money at the moment (deposits) and lend money to those people currently in need of money (loans), preferably for productive purposes, like in this story: 4

5 Saving & borrowing money 5

6 Saving & borrowing money The bank (or cooperative or MFI) basically borrows money from people (depositors) and uses the money to give loans to other clients or members. The advantage for the depositor is that his/her money is kept safe and earns money, so-called interest, because the financial institution pays the depositor for the right to use his/her money. But the institution also charges money from the people it gives loans to and this, too, is interest. Loan interest rate 1 Deposit interest rate Operating costs 6 The interest charged from the loan recipient, the borrower, is normally higher than the interest paid to the depositor because the financial institution has to make enough money to pay the people who gave their money to the institution, pay for its own costs, put aside some money for the cases that loans are not repaid and generate enough extra money to be able to grow. Financial institutions act as financial intermediaries: they collect deposits from many people and pool these funds to issue loans. This enables financial institutions to also give loans for bigger amounts and longer maturities than the amounts and maturities of some deposits. You might have already noted that in Reserves for lost loans Profit the story above, Daw Hla Hla Oo received more money than Ko Saw Chit put into the financial institution and may have wondered why now you know the answer. The financial institution is using not just Ko Saw Chit s money but also that of other depositors. 1 Only applicable to financial institutions providing loans based on deposits only.

7 Saving & borrowing money It is a key responsibility of financial intermediaries to safeguard the deposits of their clients so that they have to be very careful with regard to whom they give loans. Loans have to be repaid in full and on time so that financial institutions can fulfill their obligations towards their depositors. Financial intermediaries such as banks, cooperatives, MFIs or similar fulfill an extremely important function for the economy as they help to efficiently channel money from people who do not need their money today, like Ko Saw Chit, to those who do, like Daw Hla Hla Oo. One way of doing this involves deposits and loans. Another important function of financial intermediaries is to enable money transfers, i.e. allowing you to send money from point A to point B. This can be domestic transfers, i.e. transfers within the country, as well as international money transfers for example to receive money from a relative working abroad. 7

, to ensure that these institutions will")

8 Saving & borrowing money Licensed financial institutions, such as banks, cooperatives, MFIs, etc. have to follow government rules and are subject to control (regulation and supervision), to ensure that these institutions will keep your money safe, invest it carefully, issue loans at reliable and controlled conditions and, in this way, also increase your money over time. There are many advantages in cooperating with them: The borrower will have reliable loan conditions, i.e. the bank/cooperative/mfi can normally not just ask for the loan back as it pleases. It can also not just change other loan conditions as it wants. This makes life and business easier to plan for the borrower. Usually interest rates are also lower if you borrow from a licensed institution. 8 The depositor will have the assurance that his/her money is kept safely and that he/she will receive the deposited money plus interest after a certain amount of time (according to agreed conditions, you can find more details on these conditions here: 5. Be safe and save).

.")

9 Financial services 2. WHICH SERVICES DO BANKS, MFIS AND COOPERATIVES OFFER FOR YOU? You can choose different savings and loan products from banks, MFIs and cooperatives. In this chapter, we summarize some of the most common products and services you will find in Myanmar. Accounts are used for storing money and for sending and receiving money (e.g. bill payments, receiving and repaying a loan). The most commonly used accounts for individuals include current and savings accounts (please note that not all institutions in Myanmar offer all types of accounts): A loan is money you borrow, e.g. from a bank, with a contractual obligation to repay it with interest, which is the price you have to pay for being allowed to use the money. Loans should be obtained for a specific and productive purpose, but overall, the reason for taking out a loan should be to improve your personal situation or living conditions in a manner which does not jeopardize your current or future financial status, i.e. you should use a loan for productive purposes or at least to invest in things which will not make you worse off in the future. Savings: as you know from Ko Saw Chit s story, you can save money with certain types of financial institutions. There are various options you can choose from and they basically depend on (i) how much money you can deposit, (ii) when you want to access your money that is stored at the institution and (iii) how much money (interest) you want to get paid. You will learn more about this in 5. Be safe and save. 9

10 Financial services THE MOST COMMON TYPES OF SAVINGS AND LOAN PRODUCTS CURRENTLY AVAILABLE IN MYANMAR INCLUDE: Save money with a licensed financial institution* Borrow money from a licensed financial institution* VOLUNTARY SAVINGS COMPULSORY SAVINGS GROUP LOANS If you are a member of a cooperative or an active borrower at an MFI licensed to accept deposits, you can also deposit money with these institutions You can withdraw your savings anytime but may need to inform the MFI in advance about the timing and amount you want to withdraw. You will receive interest on your savings with an MFI. Terms and conditions among MFIs may vary and it is important to compare different offers. At cooperatives, members typically fix regular savings amounts, interest rates and terms and conditions among themselves. You can also open a savings account with a bank. You do not need a lot of money to save with a bank a few thousand kyats can already be enough to open an account. Typically, a bank offers you different interest rates for your deposits, depending how long you put your money into the bank (you can find more details on the different interest rates here: 5. Be safe and save) If you want to borrow from most MFIs or some cooperatives, they require you to deposit a certain amount as a security measure to cover some portion in the case of a potential loan default. Some MFIs set a small amount of compulsory saving and collect every week or every month while others collect the full amount of compulsory saving by the time of loan disbursement. Most loans offered by MFIs and cooperatives are group loans. The idea of group loans is that small groups of borrowers guarantee for each other, i.e. if one group member does not pay, the other group members have to pay for this member as well as paying their own share. Since MFIs and cooperatives do not require collateral, they use this group principle as a control mechanism to make sure that loans are fully repaid. While it may be an advantage that collateral is not required for this type of loan, consider that you also have to bear the repayment risks of your fellow group members. Group loans are disbursed individually. Terms and conditions may vary according to the institution and specific loan product. 10 * Examples based on 2015 data. Note that actual product features might be subject to change.

11 Financial services INDIVIDUAL LOANS Banks typically offer individual loans. Individual means that you do not need to guarantee for other people s loans but you still need to provide the bank with something that will protect the bank in case you would have difficulties in loan repayment. This, typically, are collateral (usually, land or land and buildings) as well as one or more guarantor(s). The loan amounts banks can offer are higher than those MFIs can offer, although the approach of banks may be more bureaucratic than the MFI approach Some MFIs have started to offer individual small business loans in Myanmar. For these loans, you do not need to guarantee for your fellow group members. But the MFI will check the financial situation of your household and your business to see whether you can repay the loan and will also ask you to find guarantors. HP LOANS Banks (as well as some cooperatives and MFIs) offer hire-purchase (HP) loans. HP loans can be used for purchasing a limited range of items, typically for buying equipment. You can apply for this type of loan if you have some, but not all of the money to buy the item (usually, you need to have at least 30% of the purchase price although this share can be lower with some banks). The bank then buys the item on your behalf and you hire it from the bank and can use it. For this you pay. In addition, you will also start paying back the loan to the bank. The goal is that you will fully own the item once you have fully repaid (including interest, fees, commissions etc.), i.e. you purchase the item. Depending on the item in question, hire purchase contracts may run for several years. HP loans can be used for purchasing a limited range of items. Some MFIs and cooperatives also offer HP loans. Guarantor Many of us have been asked at one time or another to act as guarantor for someone else. Maybe you have looked at it as a pure formality, doing your friend or relative a favor that does not cost anything. However, being a guarantor is not a formality. It is a legal obligation that can cause hardship for you and your family if things do not go well: if the primary debtor does not fulfill his/her obligations, i.e. repay the loan on time and in full, you as guarantor will be asked to step in and take over all payments (full outstanding amount plus interest, penalties, court fees, etc.). Ask yourself the following questions before agreeing to become a guarantor: How well do I know the primary debtor? How reliable is he/she? How does the primary debtor plan to repay the loan? Does he/she have the resources to repay the loan? If something went wrong, would I be able to step in and repay the loan? What would this mean for my family, my business and life? Do I really want to accept this role? Many people feel some moral or emotional pressure to accept the role against their intuition. 11 Think carefully before you become a guarantor!

Food Security Policy Project Research Highlights Myanmar

Food Security Policy Project Research Highlights Myanmar December 2017 #9 AGRICULTURAL CREDIT ACCESS AND UTILIZATION IN MYANMAR S DRY ZONE Khun Moe Htun and Myat Su Tin INTRODUCTION This research highlight

Food Security Policy Project Research Highlights Myanmar December 2017 #9 AGRICULTURAL CREDIT ACCESS AND UTILIZATION IN MYANMAR S DRY ZONE Khun Moe Htun and Myat Su Tin INTRODUCTION This research highlight

Assessing payment mechanisms for Myanmar

Whilst cash transfers are becoming increasingly important in the country, their delivery mechanism typically remains manual physical cash delivered by hand. Many other developing countries now use electronic

Whilst cash transfers are becoming increasingly important in the country, their delivery mechanism typically remains manual physical cash delivered by hand. Many other developing countries now use electronic

with the support of Everyday Banking An easy read guide March 2018

with the support of Everyday Banking An easy read guide March 2018 Who is this guide for? This guide has been designed to help anyone who might need more information about everyday banking. We will cover

with the support of Everyday Banking An easy read guide March 2018 Who is this guide for? This guide has been designed to help anyone who might need more information about everyday banking. We will cover

2011 ODA in $ at 2010 prices and rates ODA US$ million (current) %Change 2011/2010 at 2010 prices and exchange

%Change 2011/2010 at 2010 prices and exchange") Net 2011 1 net %GNI 2010 2 net %GNI 2011 US$ million current 2011 in $ at 2010 prices and exchange rates 2010 3 US$ million (current) %Change 2011/2010 at 2010 prices and exchange rates Aid per Citizen

Net 2011 1 net %GNI 2010 2 net %GNI 2011 US$ million current 2011 in $ at 2010 prices and exchange rates 2010 3 US$ million (current) %Change 2011/2010 at 2010 prices and exchange rates Aid per Citizen

This booklet sets out the terms and conditions of your plan how it works, what you can expect us to do, and what we expect you to do.

Plan details for the Personal Protection Menu (December 2012) This booklet sets out the terms and conditions of your plan how it works, what you can expect us to do, and what we expect you to do. Bright

Plan details for the Personal Protection Menu (December 2012) This booklet sets out the terms and conditions of your plan how it works, what you can expect us to do, and what we expect you to do. Bright

Flexible Home Loan. This document sets out your facility s terms and conditions. Some key information about your facility. Terms and Conditions

Flexible Home Loan Terms and Conditions This document sets out your facility s terms and conditions In this document we ve explained the terms and conditions applying to your ANZ Flexible Home Loan. It

Flexible Home Loan Terms and Conditions This document sets out your facility s terms and conditions In this document we ve explained the terms and conditions applying to your ANZ Flexible Home Loan. It

Topic 5 Sources of Finance. N5 Business Management

Topic 5 Sources of Finance N5 Business Management 1 Learning Intentions / Success Criteria Learning Intentions Sources of finance Success Criteria By end of this topic you will be able to describe: sources

Topic 5 Sources of Finance N5 Business Management 1 Learning Intentions / Success Criteria Learning Intentions Sources of finance Success Criteria By end of this topic you will be able to describe: sources

Introduction Slide SET. Host Organization s Name July 30, Business Smart is a business education series developed by

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

UNOFFICIAL TRANSLATION. Government of the Republic of the Union of Myanmar. Microfinance Supervisory Committee. Notification No.

Government of the Republic of the Union of Myanmar Notification No. (1/2016) Naypyitaw, the 11 th Waning of Wakhaung, 1378 ME (29 th August, 2016) 1. In exercising the powers conferred upon it by section

Government of the Republic of the Union of Myanmar Notification No. (1/2016) Naypyitaw, the 11 th Waning of Wakhaung, 1378 ME (29 th August, 2016) 1. In exercising the powers conferred upon it by section

How Does the Banking System Work? (EA)

") How Does the Banking System Work? (EA) What do you notice when you enter a bank? Perhaps you pass an automated teller machine in the lobby. ATMs can dispense cash, accept deposits, and make transfers from

How Does the Banking System Work? (EA) What do you notice when you enter a bank? Perhaps you pass an automated teller machine in the lobby. ATMs can dispense cash, accept deposits, and make transfers from

A guide to your second charge mortgage

Second charge mortgages DECEMBER 2016 A guide to your second charge mortgage Mortgage terms and conditions Introduction This booklet contains the second charge mortgage terms and conditions for Paragon

Second charge mortgages DECEMBER 2016 A guide to your second charge mortgage Mortgage terms and conditions Introduction This booklet contains the second charge mortgage terms and conditions for Paragon

EOCNOMICS- MONEY AND CREDIT

EOCNOMICS- MONEY AND CREDIT Banks circulate the money deposited by customers in the banks by lending it out to businesses at a rate of interest as a credit, which then acts as the income of the bank....

EOCNOMICS- MONEY AND CREDIT Banks circulate the money deposited by customers in the banks by lending it out to businesses at a rate of interest as a credit, which then acts as the income of the bank....

International Money and Banking: 2. Banks and Financial Intermediation

International Money and Banking: 2. Banks and Financial Intermediation Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Banks and Financial Intermediation Spring 2018 1 / 15 Banks While

International Money and Banking: 2. Banks and Financial Intermediation Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Banks and Financial Intermediation Spring 2018 1 / 15 Banks While

Dollars & Cents FREE. Issue 07 October 2015 Foresters Group & Kyabra Community Association TAKE ME I M

Dollars & Cents TAKE ME I M FREE Issue 07 October 2015 Foresters Group & Kyabra Community Association Planning ahead for Christmas It s never too early to think about saving money for the festive season.

Dollars & Cents TAKE ME I M FREE Issue 07 October 2015 Foresters Group & Kyabra Community Association Planning ahead for Christmas It s never too early to think about saving money for the festive season.

Warehouse Money Visa Card Terms and Conditions

Warehouse Money Visa Card Terms and Conditions 1 01 Contents 1. About these terms 6 2. How to read this document 6 3. Managing your account online 6 4. Managing your account online things you need to

Warehouse Money Visa Card Terms and Conditions 1 01 Contents 1. About these terms 6 2. How to read this document 6 3. Managing your account online 6 4. Managing your account online things you need to

N A T I O N A L B A N K P.O. BOX 5550 LICENSING AND SUPERVISION OF THE BUSINESS OF MICRO-FINANCING INSTITUTIONS

TELEGRAPHIC ADDRESS ¾ =ƒäåá wn?^ v ADDIS ABABA PLEASE ADDRESS ANYREPLY TO N A T I O N A L B A N K P.O. BOX 5550 TELEX 21020 CODES USED PETERSON 3 rd & 4 th ED. BENTLEY'S 2 nd PHRASE A. B. C. 6 th EDITION

TELEGRAPHIC ADDRESS ¾ =ƒäåá wn?^ v ADDIS ABABA PLEASE ADDRESS ANYREPLY TO N A T I O N A L B A N K P.O. BOX 5550 TELEX 21020 CODES USED PETERSON 3 rd & 4 th ED. BENTLEY'S 2 nd PHRASE A. B. C. 6 th EDITION

Trefzger, FIL 240 & FIL 404 Assignment: Debt and Equity Financing and Form of Business Organization

Trefzger, FIL 240 & FIL 404 Assignment: Debt and Equity Financing and Form of Business Organization Please read the following story that provides insights into debt (lenders) and equity (owners) financing.

Trefzger, FIL 240 & FIL 404 Assignment: Debt and Equity Financing and Form of Business Organization Please read the following story that provides insights into debt (lenders) and equity (owners) financing.

THIS HANDY LITTLE GUIDE EXPLORES THE BASICS OF CREDIT SCORING AND CREDIT REPORTING IN AUSTRALIA. TABLE OF CONTENTS

CREDIT MADE SIMPLE THIS HANDY LITTLE GUIDE This handy little guide explores the basics of credit scoring and credit reporting in Australia. EXPLORES THE BASICS OF CREDIT SCORING AND CREDIT REPORTING IN

CREDIT MADE SIMPLE THIS HANDY LITTLE GUIDE This handy little guide explores the basics of credit scoring and credit reporting in Australia. EXPLORES THE BASICS OF CREDIT SCORING AND CREDIT REPORTING IN

YOUR MONEY, YOUR GOALS. A financial empowerment toolkit

YOUR MONEY, YOUR GOALS A financial empowerment toolkit Consumer Financial Protection Bureau December 2016 About the Consumer Financial Protection Bureau The Consumer Financial Protection Bureau (CFPB)

YOUR MONEY, YOUR GOALS A financial empowerment toolkit Consumer Financial Protection Bureau December 2016 About the Consumer Financial Protection Bureau The Consumer Financial Protection Bureau (CFPB)

MONEY AND CREDIT VERY SHORT ANSWER TYPE QUESTIONS [1 MARK]

![MONEY AND CREDIT VERY SHORT ANSWER TYPE QUESTIONS [1 MARK]](/thumbs/76/74334829.jpg "MONEY AND CREDIT VERY SHORT ANSWER TYPE QUESTIONS [1 MARK]") MONEY AND CREDIT VERY SHORT ANSWER TYPE QUESTIONS [1 MARK] 1. What is collateral? Collateral is an asset that the borrower owns such as land, building, vehicle, livestock, deposits with the banks and uses

MONEY AND CREDIT VERY SHORT ANSWER TYPE QUESTIONS [1 MARK] 1. What is collateral? Collateral is an asset that the borrower owns such as land, building, vehicle, livestock, deposits with the banks and uses

Toolkit 2 Borrowing Wisely

Toolkit 2 Borrowing Wisely Questions to Think About Before Borrowing Borrowing money is not necessarily a bad thing and done sensibly it can be a good investment for your future. Some good reasons to borrow

Toolkit 2 Borrowing Wisely Questions to Think About Before Borrowing Borrowing money is not necessarily a bad thing and done sensibly it can be a good investment for your future. Some good reasons to borrow

Name: Preview. Use the word bank to fill in the missing letters. Some words may be used more than once. Circle any words you already know.

Preview. Use the word bank to fill in the missing letters. Some words may be used more than once. Circle any words you already know. Advance Organizer Banks, Credit & the Economy Preview. Use the word

Preview. Use the word bank to fill in the missing letters. Some words may be used more than once. Circle any words you already know. Advance Organizer Banks, Credit & the Economy Preview. Use the word

Recommendation of the Council concerning Consumer Protection in the Field of Consumer Credit

Recommendation of the Council concerning Consumer Protection in the Field of Consumer Credit OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD.

Recommendation of the Council concerning Consumer Protection in the Field of Consumer Credit OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD.

The Common Sense Guide: HECM

The Common Sense Guide: HECM Home Equity Conversion Mortgage Prepared by: Ed O Connor Ed O Connor, NMLS# 17212 Your Credit Union Trusted Resource FHA made the program WE make the difference! 1 Steps to

The Common Sense Guide: HECM Home Equity Conversion Mortgage Prepared by: Ed O Connor Ed O Connor, NMLS# 17212 Your Credit Union Trusted Resource FHA made the program WE make the difference! 1 Steps to

CARE BY VOLVO YOU GET THE BEST OF THE CAR. WE WILL TAKE CARE OF EVERYTHING ELSE.

YOU GET THE BEST OF THE CAR. WE WILL TAKE CARE OF EVERYTHING ELSE. 1 CONTENTS Care by Volvo is an entirely new driving experience. One where we take care of everything, so you can simply sit back, relax

YOU GET THE BEST OF THE CAR. WE WILL TAKE CARE OF EVERYTHING ELSE. 1 CONTENTS Care by Volvo is an entirely new driving experience. One where we take care of everything, so you can simply sit back, relax

BUSINESS MENU PLAN LIFE OR CRITICAL ILLNESS COVER

BUSINESS MENU PLAN LIFE OR CRITICAL ILLNESS COVER Plan details - January 2018 Protection - Business Menu Plan WE GIVE THIS BOOKLET OF TERMS AND CONDITIONS TO EVERYONE WHO BUYS LIFE OR CRITICAL ILLNESS

BUSINESS MENU PLAN LIFE OR CRITICAL ILLNESS COVER Plan details - January 2018 Protection - Business Menu Plan WE GIVE THIS BOOKLET OF TERMS AND CONDITIONS TO EVERYONE WHO BUYS LIFE OR CRITICAL ILLNESS

Personal Lending Products

Personal Lending Products Terms and conditions Applies from 15th July 2017 Introduction The details of your credit facilities are set out in the agreement which comes with this booklet. The agreement

Personal Lending Products Terms and conditions Applies from 15th July 2017 Introduction The details of your credit facilities are set out in the agreement which comes with this booklet. The agreement

BANKING. Q&A with OFFSHORE STEVEN GOLDBURD ABOUT AND THE ATTORNEY

Q&A with ATTORNEY STEVEN GOLDBURD ABOUT OFFSHORE BANKING AND THE There was big news last week about Bank Leumi s $400 million deal with the Department of Justice due to allegations of tax evasion. Yes.

Q&A with ATTORNEY STEVEN GOLDBURD ABOUT OFFSHORE BANKING AND THE There was big news last week about Bank Leumi s $400 million deal with the Department of Justice due to allegations of tax evasion. Yes.

Home Loan Agreement - Details

Home Loan Agreement - Details Date: To: [Date] ( Disclosure Date ) [Customer details] Thank you for submitting your signed loan application to us on [date]. We, Bank of China (New Zealand) Limited ( Bank

Home Loan Agreement - Details Date: To: [Date] ( Disclosure Date ) [Customer details] Thank you for submitting your signed loan application to us on [date]. We, Bank of China (New Zealand) Limited ( Bank

Treasurer s Savings Account

Please keep for future reference Contact us Page 1 of 4 Treasurer s Savings Account Key Facts Document (including Financial Services Compensation Scheme (FSCS) Information Sheet & Exclusions List) Effective

Please keep for future reference Contact us Page 1 of 4 Treasurer s Savings Account Key Facts Document (including Financial Services Compensation Scheme (FSCS) Information Sheet & Exclusions List) Effective

Business Everyday Saver

Please keep for future reference Contact us Page 1 of 5 Business Everyday Saver Key Facts Document (including Financial Services Compensation Scheme (FSCS) Information Sheet & Exclusions List) Effective

Please keep for future reference Contact us Page 1 of 5 Business Everyday Saver Key Facts Document (including Financial Services Compensation Scheme (FSCS) Information Sheet & Exclusions List) Effective

Client Saver. Please keep for future reference

Please keep for future reference Page 1 of 4 Client Saver Key Facts Document (including Financial Services Compensation Scheme (FSCS) Information Sheet & Exclusions List) Effective from 1 January 2019

Please keep for future reference Page 1 of 4 Client Saver Key Facts Document (including Financial Services Compensation Scheme (FSCS) Information Sheet & Exclusions List) Effective from 1 January 2019

CONSUMER CREDIT made easy

BANK OF ITALY GUIDES CONSUMER CREDIT made easy OPTIONS and COSTS Consumer RIGHTS Useful CONTACTS Consumer credit from A to Z consumer credit Consumer credit is money lent for the purchase of goods and

BANK OF ITALY GUIDES CONSUMER CREDIT made easy OPTIONS and COSTS Consumer RIGHTS Useful CONTACTS Consumer credit from A to Z consumer credit Consumer credit is money lent for the purchase of goods and

Business Reward Saver (Issue 9)

") Please keep for future reference Contact us Page 1 of 5 Business Reward Saver (Issue 9) Key Facts Document (including Financial Services Compensation Scheme (FSCS) Information Sheet & Exclusions List)

Please keep for future reference Contact us Page 1 of 5 Business Reward Saver (Issue 9) Key Facts Document (including Financial Services Compensation Scheme (FSCS) Information Sheet & Exclusions List)

HSBC Mortgage Loan Terms and Conditions Edition

HSBC Mortgage Loan Terms and Conditions 2017 Edition 2 IMPORTANT PLEASE READ THIS FIRST These conditions are an important part of the legal agreement between us for your mortgage. We recommend that you

HSBC Mortgage Loan Terms and Conditions 2017 Edition 2 IMPORTANT PLEASE READ THIS FIRST These conditions are an important part of the legal agreement between us for your mortgage. We recommend that you

Mortgage Conditions nd Edition

Mortgage Conditions 2004 2nd Edition Summary of main points Parts 1 and 2 Part 1 GENERAL MORTGAGE CONDITIONS applies to your mortgage in every case. Part 2 - FLEXIBLE OPTIONS CONDITIONS applies if your

Mortgage Conditions 2004 2nd Edition Summary of main points Parts 1 and 2 Part 1 GENERAL MORTGAGE CONDITIONS applies to your mortgage in every case. Part 2 - FLEXIBLE OPTIONS CONDITIONS applies if your

SLAYING THE DEBT DRAGON

FLIP (Financial Literacy in Practice) SLAYING THE DEBT DRAGON March 2018 SLAYING THE DEBT DRAGON how to get out of debt OVERVIEW This resource introduces students to the basic concepts of debt, with a

FLIP (Financial Literacy in Practice) SLAYING THE DEBT DRAGON March 2018 SLAYING THE DEBT DRAGON how to get out of debt OVERVIEW This resource introduces students to the basic concepts of debt, with a

The Easy Picture Guide to Insurance for People Living Independently. Your Money Your Insurance

for People Living Independently Your Money Your Insurance 2 This guide is all about insurance. Insurance is something you buy to make sure if something goes wrong, you will get money to put things right.

for People Living Independently Your Money Your Insurance 2 This guide is all about insurance. Insurance is something you buy to make sure if something goes wrong, you will get money to put things right.

Mortgage Conditions 2007

Mortgage Conditions 2007 Summary of main points Parts 1 and 2 Part 1 GENERAL MORTGAGE CONDITIONS applies to your mortgage in every case. Part 2 flexible options CONDITIONS applies if your mortgage includes

Mortgage Conditions 2007 Summary of main points Parts 1 and 2 Part 1 GENERAL MORTGAGE CONDITIONS applies to your mortgage in every case. Part 2 flexible options CONDITIONS applies if your mortgage includes

Key Features of the Flexible Protection Plan

Key Features of the Flexible Protection Plan LV= Personal Sick Pay The Financial Conduct Authority is a financial services regulator. It requires us, LV=, to give you this important information to help

Key Features of the Flexible Protection Plan LV= Personal Sick Pay The Financial Conduct Authority is a financial services regulator. It requires us, LV=, to give you this important information to help

Frequently Asked Questions for Chapter 13 Bankruptcy

Frequently Asked Questions for Chapter 13 Bankruptcy What is going to happen now that I have filed a Chapter 13 bankruptcy? Since you have just filed a Chapter 13 Bankruptcy, you probably have a lot of

Frequently Asked Questions for Chapter 13 Bankruptcy What is going to happen now that I have filed a Chapter 13 bankruptcy? Since you have just filed a Chapter 13 Bankruptcy, you probably have a lot of

No Credit Needed. Debt Reduction Guide. For more information about debt reduction visit: No Credit Needed. All Rights Reserved.

No Credit Needed Debt Reduction Guide For more information about debt reduction visit: No Credit Needed All Rights Reserved. Copyright 2008 by Up In Three, LLC All Rights Reserved. Copyright 2008 Up In

No Credit Needed Debt Reduction Guide For more information about debt reduction visit: No Credit Needed All Rights Reserved. Copyright 2008 by Up In Three, LLC All Rights Reserved. Copyright 2008 Up In

Hang Seng Credit Card Benefits Directory

Hang Seng Credit Card Benefits Directory Content 1. Important Points to Remember Page 1 2. Customer Privileges - Hang Seng Credit Card Membership Rewards Programme Page 2 - Online Shopping Security Page

Hang Seng Credit Card Benefits Directory Content 1. Important Points to Remember Page 1 2. Customer Privileges - Hang Seng Credit Card Membership Rewards Programme Page 2 - Online Shopping Security Page

Understanding Your Benefits. The Utah Retirement System

Understanding Your Benefits The Utah Retirement System y Retirement System An Overview The difference between a Defined Contribution Plan and a Defined Benefit Plan How URS provides a combination of both

Understanding Your Benefits The Utah Retirement System y Retirement System An Overview The difference between a Defined Contribution Plan and a Defined Benefit Plan How URS provides a combination of both

LV= LIFE LV LIFE INSURANCE. Plan Conditions Document reference: LVLI4

LV= LIFE LV LIFE INSURANCE INSURANCE Plan Conditions Document reference: LVLI4 LV= Life Insurance Plan Conditions Welcome to LV=, and thank you for choosing LV= Life Insurance These conditions and your

LV= LIFE LV LIFE INSURANCE INSURANCE Plan Conditions Document reference: LVLI4 LV= Life Insurance Plan Conditions Welcome to LV=, and thank you for choosing LV= Life Insurance These conditions and your

Myanmar Global Leaders Programme 2018 THE FUTURE OF FINANCE FOR MYANMAR S UNBANKED. Executive Summary

Myanmar Global Leaders Programme 2018 THE FUTURE OF FINANCE FOR MYANMAR S UNBANKED Executive Summary FINANCIAL INCLUSION An estimated 2 billion adults worldwide do not have a basic financial account.

Myanmar Global Leaders Programme 2018 THE FUTURE OF FINANCE FOR MYANMAR S UNBANKED Executive Summary FINANCIAL INCLUSION An estimated 2 billion adults worldwide do not have a basic financial account.

Personal Lending Products

Personal Lending Products Terms and Conditions Introduction The details of your credit facilities are set out in the agreement which comes with this booklet. The agreement also sets out the specific terms

Personal Lending Products Terms and Conditions Introduction The details of your credit facilities are set out in the agreement which comes with this booklet. The agreement also sets out the specific terms

What You Need to Know About Your HECM After Closing

What You Need to Know About Your HECM After Closing www.reversemortgage.org INDEX How do I know who my Servicer is?... 2 Staying in touch... 2 Receiving payments from your HECM... 2 Occupancy... 3 Property

What You Need to Know About Your HECM After Closing www.reversemortgage.org INDEX How do I know who my Servicer is?... 2 Staying in touch... 2 Receiving payments from your HECM... 2 Occupancy... 3 Property

Student Loans Company. Repaying your student loan

Student Loans Company Repaying your student loan Contents Page Introduction 3 How much do I repay? 4 Do I pay interest on my loan? 6 How do I repay? 7 When will I get a statement? 11 Coming to the end

Student Loans Company Repaying your student loan Contents Page Introduction 3 How much do I repay? 4 Do I pay interest on my loan? 6 How do I repay? 7 When will I get a statement? 11 Coming to the end

Student Loan Consolidation: Getting Out of Debt

Student Loan Consolidation: Getting Out of Debt Introduction When we talk about college graduation, several promising life changes occur in our minds potential careers, independence as well as new beginnings.

Student Loan Consolidation: Getting Out of Debt Introduction When we talk about college graduation, several promising life changes occur in our minds potential careers, independence as well as new beginnings.

Income Tax Planning for Expat Entrepreneurs. Olivier Wagner, CPA 1040 Abroad

Income Tax Planning for Expat Entrepreneurs Olivier Wagner, CPA 1040 Abroad Who is this presentation addressed to? u US Citizens and green card holders u Living outside the US u Self-employed or start-up

Income Tax Planning for Expat Entrepreneurs Olivier Wagner, CPA 1040 Abroad Who is this presentation addressed to? u US Citizens and green card holders u Living outside the US u Self-employed or start-up

GUIDELINES FOR FINANCIAL REPORTING

GUIDELINES FOR FINANCIAL REPORTING FOR PROJECTS FUNDED BY THE OLOF PALME INTERNATIONAL CENTER Revised 2017-11-07 1. FORMS AND TEMPLATES FOR THE REPORTING... 3 2. DEPOSITING OF FUNDS... 4 3. INTEREST...

GUIDELINES FOR FINANCIAL REPORTING FOR PROJECTS FUNDED BY THE OLOF PALME INTERNATIONAL CENTER Revised 2017-11-07 1. FORMS AND TEMPLATES FOR THE REPORTING... 3 2. DEPOSITING OF FUNDS... 4 3. INTEREST...

Standard Mortgage Terms and Conditions. May 2018 Edition

Standard Mortgage Terms and Conditions May 2018 Edition Terms and Conditions Mortgages Contents Introduction 03 Definitions 04 Interpretation and application 05 Acting in joint names 05 Withdrawal of offer

Standard Mortgage Terms and Conditions May 2018 Edition Terms and Conditions Mortgages Contents Introduction 03 Definitions 04 Interpretation and application 05 Acting in joint names 05 Withdrawal of offer

Money. wisely! Use. Advice! This financial literacy information is useful to employees! Why should you use money wisely?

Use Money wisely! CENTRAL BANK OF LESOTHO BANKA E KHOLO EA LESOTHO This financial literacy information is useful to employees! Why should you use money wisely? Life is getting more and more difficult because

Use Money wisely! CENTRAL BANK OF LESOTHO BANKA E KHOLO EA LESOTHO This financial literacy information is useful to employees! Why should you use money wisely? Life is getting more and more difficult because

Benefits Based Borrowing. A guide for disabled people using their benefits to buy property suited to their needs.

Benefits Based Borrowing A guide for disabled people using their benefits to buy property suited to their needs. Introduction Many disabled people rely on state benefits for part or all of their income

Benefits Based Borrowing A guide for disabled people using their benefits to buy property suited to their needs. Introduction Many disabled people rely on state benefits for part or all of their income

Working Party on Private Pensions

For Official Use DAFFE/AS/PEN/WD(2000)13/REV2 DAFFE/AS/PEN/WD(2000)13/REV2 For Official Use Organisation de Coopération et de Développement Economiques Organisation for Economic Co-operation and Development

For Official Use DAFFE/AS/PEN/WD(2000)13/REV2 DAFFE/AS/PEN/WD(2000)13/REV2 For Official Use Organisation de Coopération et de Développement Economiques Organisation for Economic Co-operation and Development

ANNOUNCEMENT BY THE MANAGEMENT COMMITTEE OF THE DEPOSIT GUARANTEE AND RESOLUTION OF CREDIT AND OTHER INSTITUTIONS SCHEME

This is an unofficial translation, for information purposes only ANNOUNCEMENT BY THE MANAGEMENT COMMITTEE OF THE DEPOSIT GUARANTEE AND RESOLUTION OF Activation of the procedure for the payment of compensation

This is an unofficial translation, for information purposes only ANNOUNCEMENT BY THE MANAGEMENT COMMITTEE OF THE DEPOSIT GUARANTEE AND RESOLUTION OF Activation of the procedure for the payment of compensation

Student Loan Consolidation

STUDENT LOAN CONSOLIDATION: GETTING OUT OF DEBT Legal Disclaimer: While all attempts have been made to verify information provided in this publication, neither the Author nor the Publisher assumes any

STUDENT LOAN CONSOLIDATION: GETTING OUT OF DEBT Legal Disclaimer: While all attempts have been made to verify information provided in this publication, neither the Author nor the Publisher assumes any

Home Discussion: Part 1

1.4.1.A4 Worksheet Home Discussion: Part 1 Total Points Earned 7 Total Points Possible Percentage Name Date Class Directions: Work with a parent, guardian, or adult family member to answer the following

1.4.1.A4 Worksheet Home Discussion: Part 1 Total Points Earned 7 Total Points Possible Percentage Name Date Class Directions: Work with a parent, guardian, or adult family member to answer the following

Selecting the right loan type It is personal

Personal Loan Guide Advertisements that promise to help you solve your financial troubles can be seen everywhere today but one can still not be sure if these companies are safe to be considered. Even when

Personal Loan Guide Advertisements that promise to help you solve your financial troubles can be seen everywhere today but one can still not be sure if these companies are safe to be considered. Even when

OVERCOMING THE CREDIT BARRIER. Clearing the Way to Your Financial Goals

OVERCOMING THE CREDIT BARRIER Clearing the Way to Your Financial Goals Overcoming the Credit Barrier: Clearing the Way to Your Financial Goals was written and designed for The National Foundation for Credit

OVERCOMING THE CREDIT BARRIER Clearing the Way to Your Financial Goals Overcoming the Credit Barrier: Clearing the Way to Your Financial Goals was written and designed for The National Foundation for Credit

Money and Banking Prof. Dr. Surajit Sinha Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur.

Money and Banking Prof. Dr. Surajit Sinha Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur Lecture 39 What I am going to start today is the cooperative banks its amazing

Money and Banking Prof. Dr. Surajit Sinha Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur Lecture 39 What I am going to start today is the cooperative banks its amazing

Terms and Conditions of the Lifestyle Flexible Option Edition 4

Terms and Conditions of the Lifestyle Flexible Option Edition 4 Retirement Investments Insurance Health Contents Section 1: General information 3 Section 2: Cash Reserve 3 Section 3: Interest 4 Section

Terms and Conditions of the Lifestyle Flexible Option Edition 4 Retirement Investments Insurance Health Contents Section 1: General information 3 Section 2: Cash Reserve 3 Section 3: Interest 4 Section

How Hedging Can Substantially Reduce Foreign Stock Currency Risk

Possible losses from changes in currency exchange rates are a risk of investing unhedged in foreign stocks. While a stock may perform well on the London Stock Exchange, if the British pound declines against

Possible losses from changes in currency exchange rates are a risk of investing unhedged in foreign stocks. While a stock may perform well on the London Stock Exchange, if the British pound declines against

Terms and Conditions of the Lifestyle Lump Sum Max - Edition 4

Terms and Conditions of the Lifestyle Lump Sum Max - Edition 4 Retirement Investments Insurance Health Contents Section 1: General information 3 Section 2: Interest 3 Section 3: When you have to repay

Terms and Conditions of the Lifestyle Lump Sum Max - Edition 4 Retirement Investments Insurance Health Contents Section 1: General information 3 Section 2: Interest 3 Section 3: When you have to repay

Workbook 3. Borrowing Money

Workbook 3 Borrowing Money Copyright 2019 ABC Life Literacy Canada First published in 2011 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada gratefully thanks Founding Sponsor TD

Workbook 3 Borrowing Money Copyright 2019 ABC Life Literacy Canada First published in 2011 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada gratefully thanks Founding Sponsor TD

UNIT 6 1 What is a Mortgage?

UNIT 6 1 What is a Mortgage? A mortgage is a legal document that pledges property to the lender as security for payment of a debt. In the case of a home mortgage, the debt is the money that is borrowed

UNIT 6 1 What is a Mortgage? A mortgage is a legal document that pledges property to the lender as security for payment of a debt. In the case of a home mortgage, the debt is the money that is borrowed

General Mortgage Conditions

General Mortgage Conditions England and Wales 2013 Introduction Over the following pages, you ll find the general conditions of your mortgage. This booklet is very important because it forms part of the

General Mortgage Conditions England and Wales 2013 Introduction Over the following pages, you ll find the general conditions of your mortgage. This booklet is very important because it forms part of the

Information for mortgage customers. Mortgages

Information for mortgage customers. Mortgages Hello. This is your guide to TSB mortgages. This guide provides lots of information about our mortgages. Some of it is relevant to everyone but some of it

Information for mortgage customers. Mortgages Hello. This is your guide to TSB mortgages. This guide provides lots of information about our mortgages. Some of it is relevant to everyone but some of it

Brought to you by. party PARTY LIST PARTY SONG HAPPY BIRTHDAY BANNER DJ FLASHY PARTY HIRE PARTY STORE

HAPPY BIRTHDAY BANNER DJ FLASHY PARTY HIRE PARTY STORE PARTY SONG I Make Money Too Save Money for the Long Term Brought to you by LIST PARTY party This Activity Answers The Question... PAGE 2 In addition

HAPPY BIRTHDAY BANNER DJ FLASHY PARTY HIRE PARTY STORE PARTY SONG I Make Money Too Save Money for the Long Term Brought to you by LIST PARTY party This Activity Answers The Question... PAGE 2 In addition

About. Direct Payments

About Direct Payments March 2017 2 About Direct Payments 3 The purpose of this booklet is to offer advice and information to anyone receiving a direct payment or for people considering taking a direct

About Direct Payments March 2017 2 About Direct Payments 3 The purpose of this booklet is to offer advice and information to anyone receiving a direct payment or for people considering taking a direct

Individual Voluntary Arrangements (IVAs)

") BRIEFING PAPER Number CPB5165, 6 April 2016 Individual Voluntary Arrangements (IVAs) By Lorraine Conway Inside: 1. Introduction 2. Alternatives to bankruptcy 3. Characteristics of an IVA 4. Who is eligible

BRIEFING PAPER Number CPB5165, 6 April 2016 Individual Voluntary Arrangements (IVAs) By Lorraine Conway Inside: 1. Introduction 2. Alternatives to bankruptcy 3. Characteristics of an IVA 4. Who is eligible

Finance Self Study Guide for Staff of Micro Finance Institutions CASH FLOW MANAGEMENT

Finance Self Study Guide for Staff of Micro Finance Institutions LESSON 6 CASH FLOW MANAGEMENT Objectives: Central to financial management of a micro-finance organization is effective management of its

Finance Self Study Guide for Staff of Micro Finance Institutions LESSON 6 CASH FLOW MANAGEMENT Objectives: Central to financial management of a micro-finance organization is effective management of its

Mortgage Conditions: These conditions and the mortgage offer are important documents. Please keep them safe.

Mortgage Conditions: 2009 These conditions and the mortgage offer are important documents. Please keep them safe. This booklet contains the terms and conditions which apply to your mortgage. These conditions:

Mortgage Conditions: 2009 These conditions and the mortgage offer are important documents. Please keep them safe. This booklet contains the terms and conditions which apply to your mortgage. These conditions:

The FOS Approach to Joint Facilities and Family Violence

The FOS Approach to Joint Facilities and Family Violence 1 At a glance 2 1.1 Scope 2 1.2 Summary 2 2 In detail 3 2.1 Issues that may arise with joint facilities 3 2.2 Understanding and responding to family

The FOS Approach to Joint Facilities and Family Violence 1 At a glance 2 1.1 Scope 2 1.2 Summary 2 2 In detail 3 2.1 Issues that may arise with joint facilities 3 2.2 Understanding and responding to family

Name of Document PURCHASE ORDER DELIVERY NOTE. Shows a list of transactions and the amount owed at the end of the month The Customer

Topic Area : Flow & Purpose of Financial Documents Purchase Order Delivery Note Name of Document PURCHASE ORDER DELIVERY NOTE GRN INVOICE Purpose of Document Used by the purchaser to order goods from a

Topic Area : Flow & Purpose of Financial Documents Purchase Order Delivery Note Name of Document PURCHASE ORDER DELIVERY NOTE GRN INVOICE Purpose of Document Used by the purchaser to order goods from a

c» BALANCE c» Financially Empowering You Credit Matters Podcast

Credit Matters Podcast [Music plays] Nikki: You re listening to Credit Matters. Hi. I m Nikki, your host for today s podcast. In today s world credit does matter. In fact, getting and using credit is part

Credit Matters Podcast [Music plays] Nikki: You re listening to Credit Matters. Hi. I m Nikki, your host for today s podcast. In today s world credit does matter. In fact, getting and using credit is part

Unofficial Consolidation

CENTRAL BANK (SUPERVISION AND ENFORCEMENT) ACT 2013 (SECTION 48) (LENDING TO SMALL AND MEDIUM-SIZED ENTERPRISES) REGULATIONS 2015 (S.I. No. 585 of 2015) Unofficial Consolidation This document is an unofficial

CENTRAL BANK (SUPERVISION AND ENFORCEMENT) ACT 2013 (SECTION 48) (LENDING TO SMALL AND MEDIUM-SIZED ENTERPRISES) REGULATIONS 2015 (S.I. No. 585 of 2015) Unofficial Consolidation This document is an unofficial

Notes. The American Center for Credit Education. Promotional Copy. CheckWise by the American Center for Credit Education

The American Center for Credit Education CheckWise by the American Center for Credit Education 2007 by Rushmore Consumer Credit Resource Center (RCCRC) Published by the American Center for Credit Education

The American Center for Credit Education CheckWise by the American Center for Credit Education 2007 by Rushmore Consumer Credit Resource Center (RCCRC) Published by the American Center for Credit Education

PERSONAL MENU PLAN LIFE OR CRITICAL ILLNESS COVER

PERSONAL MENU PLAN LIFE OR CRITICAL ILLNESS COVER Plan details - January 2018 Protection - Personal Menu Plan WE GIVE THIS BOOKLET OF TERMS AND CONDITIONS TO EVERYONE WHO BUYS LIFE OR CRITICAL ILLNESS

PERSONAL MENU PLAN LIFE OR CRITICAL ILLNESS COVER Plan details - January 2018 Protection - Personal Menu Plan WE GIVE THIS BOOKLET OF TERMS AND CONDITIONS TO EVERYONE WHO BUYS LIFE OR CRITICAL ILLNESS

A survival guide to Dealing with tax credit overpayments

A survival guide to Dealing with tax credit overpayments Making sense of the law and your rights Introduction If you ve received a letter saying you ve been overpaid tax credits and demanding repayment

A survival guide to Dealing with tax credit overpayments Making sense of the law and your rights Introduction If you ve received a letter saying you ve been overpaid tax credits and demanding repayment

Part 4: Borrowing Money and Using Credit

Part 4: Borrowing Money and Using Credit CHAPTER 11: Borrowing Money Let s discuss... $ Why people borrow more money today than in the past $ Why people borrow money $ Types of debt/credit $ The cost

Part 4: Borrowing Money and Using Credit CHAPTER 11: Borrowing Money Let s discuss... $ Why people borrow more money today than in the past $ Why people borrow money $ Types of debt/credit $ The cost

The Cost of Payday Loans

The Cost of Payday Loans Table of Contents What is a payday loan? 1 How does a payday loan work? 2 How and when do I pay back the loan? 4 How does a payday loan affect my credit report? 4 How much will

The Cost of Payday Loans Table of Contents What is a payday loan? 1 How does a payday loan work? 2 How and when do I pay back the loan? 4 How does a payday loan affect my credit report? 4 How much will

Mortgage Terms and Conditions (T&Cs)

") Mortgage Terms and Conditions (T&Cs) Banking with Atom is straightforward, so we ve split our T&Cs into three manageable chunks: General T&Cs; Product T&Cs; and product specific documents, based on the

Mortgage Terms and Conditions (T&Cs) Banking with Atom is straightforward, so we ve split our T&Cs into three manageable chunks: General T&Cs; Product T&Cs; and product specific documents, based on the

Oikocredit International Support Foundation Plans, Objectives and Activities for the period 2014 to 2018

Oikocredit International Support Foundation Plans, Objectives and Activities for the period 2014 to 2018 1. Introduction and purpose of Oikocredit and the Foundation Oikocredit Oikocredit (the Society)

Oikocredit International Support Foundation Plans, Objectives and Activities for the period 2014 to 2018 1. Introduction and purpose of Oikocredit and the Foundation Oikocredit Oikocredit (the Society)

Being a Guarantor. This booklet will help you understand all that is involved in being a Guarantor.

is a big responsibility and can have serious consequences. It is important to understand exactly what you are getting yourself into and what the impact of signing the agreement may be. can be a helpful

is a big responsibility and can have serious consequences. It is important to understand exactly what you are getting yourself into and what the impact of signing the agreement may be. can be a helpful

Support for Mortgage Interest

Support for Mortgage Interest welfare changes Your support for Mortgage Interest will end on 5 April 2018 You currently get a benefit called Support for Mortgage Interest (SMI) which is also known as

Support for Mortgage Interest welfare changes Your support for Mortgage Interest will end on 5 April 2018 You currently get a benefit called Support for Mortgage Interest (SMI) which is also known as

Global Environment Facility

Global Environment Facility LDCF/SCCF Council Meeting November 16, 2007 GEF/LDCF.SCCF.3/Inf.2 November 9, 2007 STATUS REPORT ON THE CLIMATE CHANGE FUNDS AS OF SEPTEMBER 30, 2007 (Prepared by the Trustee)

Global Environment Facility LDCF/SCCF Council Meeting November 16, 2007 GEF/LDCF.SCCF.3/Inf.2 November 9, 2007 STATUS REPORT ON THE CLIMATE CHANGE FUNDS AS OF SEPTEMBER 30, 2007 (Prepared by the Trustee)

MR. MUHAMMAD AZEEM - PAKISTAN

HTTP://WWW.READYFOREX.COM MR. MUHAMMAD AZEEM - PAKISTAN How to become a successful trader? How to win in forex trading? What are the main steps and right way to follow in trading? What are the rules to

HTTP://WWW.READYFOREX.COM MR. MUHAMMAD AZEEM - PAKISTAN How to become a successful trader? How to win in forex trading? What are the main steps and right way to follow in trading? What are the rules to

What if I need to borrow money or access credit?

What if I need to borrow money or access credit? Before you borrow money the first thing to think about is whether you can afford it. The best way to check out what will be affordable for you is to do

What if I need to borrow money or access credit? Before you borrow money the first thing to think about is whether you can afford it. The best way to check out what will be affordable for you is to do

MODULE J: SMART CHOICES FOR MANAGING CREDIT

MODULE J: SMART CHOICES FOR MANAGING CREDIT 1 Common Sense Economics ~ What Everyone Should Know About Wealth and Prosperity http://commonsenseeconomics.com/ Turn on the learning light! CREDIT, FINANCIAL

MODULE J: SMART CHOICES FOR MANAGING CREDIT 1 Common Sense Economics ~ What Everyone Should Know About Wealth and Prosperity http://commonsenseeconomics.com/ Turn on the learning light! CREDIT, FINANCIAL

spin-free guide to bonds Investing Risk Equities Bonds Property Income

spin-free guide to bonds Investing Risk Equities Bonds Property Income Contents Explaining the world of bonds 3 Understanding how bond prices can rise or fall 5 The different types of bonds 8 Bonds compared

spin-free guide to bonds Investing Risk Equities Bonds Property Income Contents Explaining the world of bonds 3 Understanding how bond prices can rise or fall 5 The different types of bonds 8 Bonds compared

State of Michigan 401(k) & 457 Plan Highlights. Saving Today, Planning for Tomorrow

& 457 Plan Highlights. Saving Today, Planning for Tomorrow") Saving Today, Planning for Tomorrow The Michigan Public School Employees Retirement System provides competitive benefits and encourages you to take full advantage of them to plan for your future. Your

Saving Today, Planning for Tomorrow The Michigan Public School Employees Retirement System provides competitive benefits and encourages you to take full advantage of them to plan for your future. Your

Understanding Your Credit Card Essentials

Understanding Your Credit Card Essentials 7.4.2.F1 Twenty-one year old Jenny felt rich when she received her first credit card during her junior year of college. She charged $2,500, her credit limit, the

Understanding Your Credit Card Essentials 7.4.2.F1 Twenty-one year old Jenny felt rich when she received her first credit card during her junior year of college. She charged $2,500, her credit limit, the

MODULE 7: Borrowing Basics PARTICIPANT GUIDE

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

Know the score: how positive data could impact your next credit application

1 Know the score: how positive data could impact your next credit application Credit applications and your data When you apply for credit in Australia, the credit provider will usually ask for your permission

1 Know the score: how positive data could impact your next credit application Credit applications and your data When you apply for credit in Australia, the credit provider will usually ask for your permission

Claim form for Winter Fuel Payment for past winters 1998/99, 1999/00, 2000/01, 2001/02, 2002/03 and 2003/04

Winter Fuel Payment If you get in touch with us, please tell us this reference number Our phone number is Code Number Ext If you have a textphone, you can call on Code Number Date Claim form for Winter

Winter Fuel Payment If you get in touch with us, please tell us this reference number Our phone number is Code Number Ext If you have a textphone, you can call on Code Number Date Claim form for Winter

3. Pensions. Introduction. What types of social insurance contributions are there?

Introduction There are 3 different types of pensions you may be entitled to. There are two pensions that are based on the amount of social insurance contributions you ve paid, Retirement Pension and Old

Introduction There are 3 different types of pensions you may be entitled to. There are two pensions that are based on the amount of social insurance contributions you ve paid, Retirement Pension and Old

ANZ ASSURED & PERSONAL OVERDRAFT

ANZ ASSURED & PERSONAL OVERDRAFT TERMS AND CONDITIONS 12.2017 Introduction If you are thinking about obtaining a personal credit facility from ANZ or have any questions about your existing facility, simply

ANZ ASSURED & PERSONAL OVERDRAFT TERMS AND CONDITIONS 12.2017 Introduction If you are thinking about obtaining a personal credit facility from ANZ or have any questions about your existing facility, simply