DEEPHAVEN MORTGAGE RESPONSIBLE NON-QM LENDING. Heather Carrico

|

|

|

- Cordelia Wilcox

- 5 years ago

- Views:

Transcription

1 DEEPHAVEN MORTGAGE RESPONSIBLE NON-QM LENDING Heather Carrico

2 DEEPHAVEN DIFFERENCE Top 10 Reasons to use Deephaven More investor loan opcons Limited by past consumer credit problems Qualify with alternacve income documentacon Borrowers who were negacvely impacted by housing crisis Outside of agency investor guidelines 1. Personal & Business Bank Stateme 2. Loan Amounts Up to $2.5M 3. DTI Up To 55% 4. Use Cash Out Proceeds as Reserve 5. Credit Scores as Low as Investors with greater than 10 pro 7. Non Warrantable condos 8. Prior Foreclosure or BK 9. No doc Inventor loans 10. No MI on LTVs up to 90%

3 DEEPHAVEN PRODUCTS Expanded-Prime Start here for all owner-occupi and 2nd home borrowers at lea 5 years from a housing event. This is a near-miss product wit our most compeccve pricing. Near-Prime Start here for all owner-occupi and 2nd home borrowers at lea 3 years from a housing event. Non-Prime Start here for all owner-occupi and 2nd home borrowers withi years or less from a housing event. Investment Property Start here for all investment properces and foreign nacona

4 EXPANDED-PRIME Provides lending opportunices to borrowers who are at least 5 years away from previous housing event and/or Bankruptcy Interest Only ARM s 10 year I/O term with 20 year amorczacon Credit score as low as 660 LTV s for PURCHASE and RATE/TERM up to 85% LTV s for CASH OUT up 70% Non-Warrantable Condo s not allowed Max DTI 50% Bank Statement DocumentaCon Allowed 24 months or 12 months Personal and 24 months Business No Excep>ons will be allowed haven Mortgage LLC This material is intended solely for the use of licensed mortgage professionals. DistribuCon to consumers is strictly prohibited. Program and rates are subject to change without nocce. Not available in all states. Terms sub

5 EXPANDED-PRIME

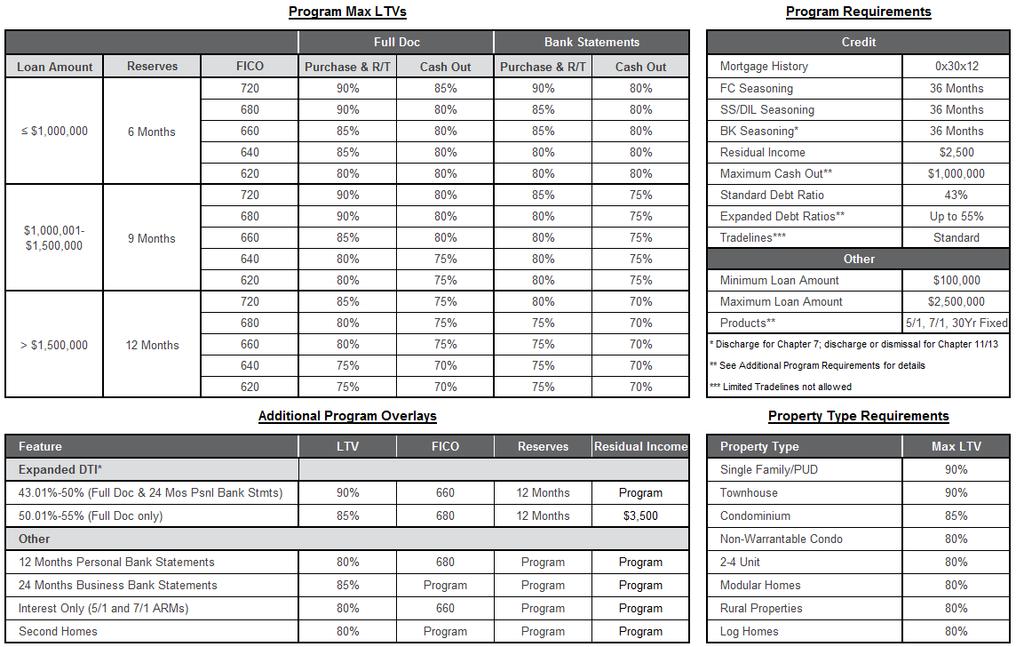

6 NEAR-PRIME Provides lending opportunices to borrowers who may have consumer credit challenges bu whose housing history is more consistent. The program also helps self-employed borrowers who may not qualify using Appendix Q underwricng standards. Interest Only ARM s 10 year I/O term with 30 year AmorCzaCon Credit scores as low as 620 LTV s for PURCHASE and RATE/TERM up to 90% LTV s for CASH OUT up to 85% LTV s for Non-Warrantable Condo up to 80% DTI as high as 55% Bank Statement DocumentaCon Allowed 24 months or 12 months Personal and 24 mon Business haven Mortgage LLC This material is intended solely for the use of licensed mortgage professionals. DistribuCon to consumers is strictly prohibited. Program and rates are subject to change without nocce. Not available in all states. Terms sub

7 NEAR-PRIME

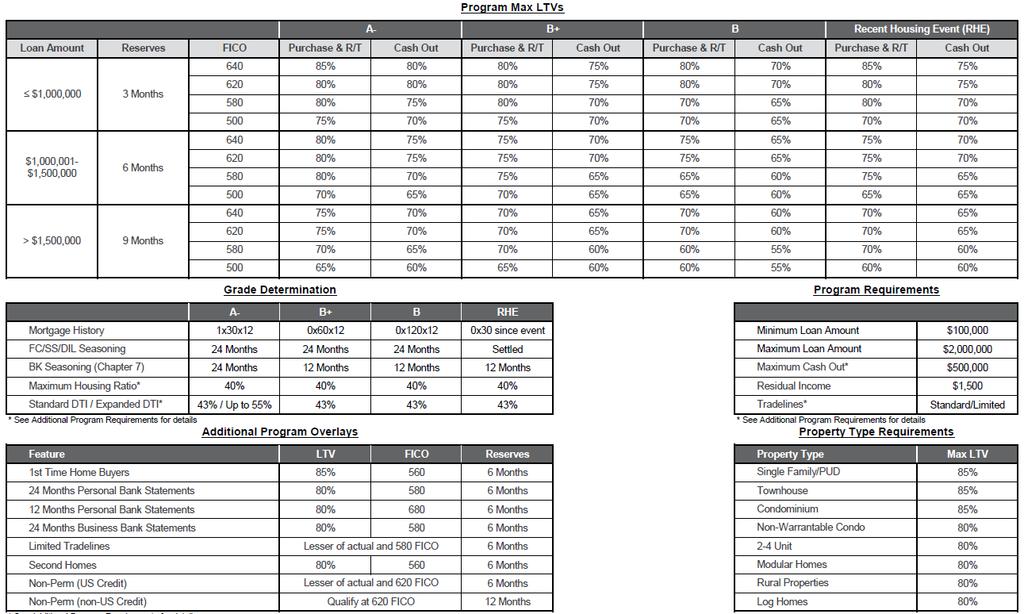

8 NON-PRIME The typical borrower does not qualify for convenconal or government financing due to the recent foreclosure and, possibly, a related bankruptcy. Also helps self-employed borrowers who may not qualify using Appendix Q underwricng standards. Credit scores as low as 500 Interest Only ARM s - 10 year I/O term with 30 year AmorCzaCon LTV s for PURCHASE and RATE/TERM up to 85% LTV s for CASH OUT up to 80% LTV s for Non-Warrantable Condo up to 80% DTI as high as 55% Cash out proceeds as reserves Bank Statement DocumentaCon Allowed 24 months or 12 months Personal and 24 mon Business haven Mortgage LLC This material is intended solely for the use of licensed mortgage professionals. DistribuCon to consumers is strictly prohibited. Program and rates are subject to change without nocce. Not available in all states. Terms sub

9 NON-PRIME

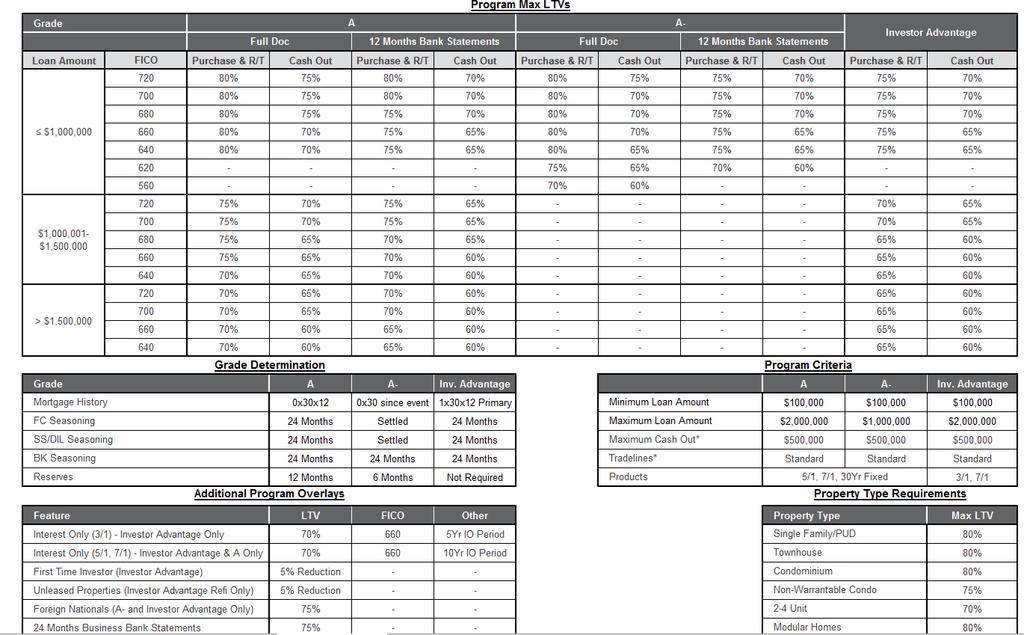

10 INVESTMENT Provides lending opportunices to investors who have been negacvely impacted by the housing crisis. There is no seasoning requirement for a prior housing default Investor A and A- Interest Only ARM s 10 year I/O term with 20 year AmorCzaCon Investor Advantage Interest Only ARM s : 3/1 ARM - 5 year I/O term with 25 year AmorCzaCon 7/1 ARM - 10 year I/O term with 20 year AmorCzaCon Credit scores as low as 560 LTV s for PURCHASE and RATE/TERM up to 80% LTV s for CASH OUT up to 75% LTV for Non-Warrantable Condo up to 75% LTV s for Foreign naconals (A- and Investor Advantage) up to 75% Bank Statement DocumentaCon Allowed: 12 months Personal and 24 months Business haven Mortgage LLC This material is intended solely for the use of licensed mortgage professionals. DistribuCon to consumers is strictly prohibited. Program and rates are subject to change without nocce. Not available in all states. Terms sub

11 INVESTMENT

12 EDIT lines elines reporcng for 12+ months elines reporcng for 24+ months, all with accvity in the last 12 months delines used to qualify may not exceed 0x60 in the most recent 12 months ited Tradelines allowed on the Non-Prime product 6 months reserves required, 10% minimum borrower contribucon (see guidelines for all requirements) ans in a deferment period, colleccon or charged-off accounts, accounts discharged through bankruptcy, and thorized user accounts are not considered acceptable trade lines senta>ve Credit Score ry Wage Earner representacve score is use to determine the credit score for the loan aven Mortgage LLC This material is intended solely for the use of licensed mortgage professionals. DistribuCon to consumers is strictly prohibited. Program and rates are subject to change without nocce. Not available in all states. Terms sub

13 RSONAL BANK STATEMENT PROGRAM General Requirements 24 months or 12 months complete bank statements (TransacCon history printouts are not acceptable) IniCal signed 1003 with monthly income disclosed Personal Bank Statements 100% of deposits, averaged over 24 months or 12 months Transfers between personal accounts should be excluded Transfers from a business account into a personal account are acceptable Unusual deposits must be documented Borrowers will qualify off the lower of the following - Income figure listed on Signed 1003 Personal Bank Statement Average (total deposits [minus any disallowed deposits] 24 months or 12 months) aven Mortgage LLC This material is intended solely for the use of licensed mortgage professionals. DistribuCon to consumers is strictly prohibited. Program and rates are subject to change without nocce. Not available in all states. Terms sub

14 SINESS BANK STATEMENT PROGRAM General Requirements 24 months complete Business bank statements (TransacCon history printouts are not acceptable) One of the following is needed: Profit and loss statement covering the same 24 months period prepared by CPA or licensed Tax Preparer Expense Statement prepared by CPA or licensed Tax Preparer and a Borrower Prepared P&L BizMiner Report and a Borrower Prepared P&L IniCal signed 1003 with monthly income disclosed Business Bank Statements Business bank accounts, personal bank accounts addressed to a DBA, or personal accounts with evidence of business expenses can be used for qualificacon Wire transfers and transfers from other accounts must be documented or excluded Statements should show a trend of ending balances that are stable or increasing over Cme Business expenses must be reasonable for the type of business (examples of business with higher expense racos may include construccon companies, builders, restaurants and retail firms) Must own 100% of business aven Mortgage LLC This material is intended solely for the use of licensed mortgage professionals. DistribuCon to consumers is strictly prohibited. Program and rates are subject to change without nocce. Not available in all states. Terms sub

15 BUSINESS BANK STATEMENT PROGRAM CALCULATING QUALIFYING INCOM ION A: 3 rd Party Prepared P&L lifying Income is the lowest of the two following calculacons: t Income from the P&L Example: $420K / 24 = $21K ome Listed on the IniCal Signed 1003 Example: $25K ION B/C: Borrower Prepared P&L along with a 3 rd Party Prepared Expense Statement/BizMiner report for discre>onary Owner Earnings ed on Industry code and loca>on) lifying Income is the lowest of the three following calculacons: t Income using the Expense Statement/BizMiner (Gross Revenue x {1 Expense Statement} ) OR Example: $800K x (1-.40=.60) = $480K/24 = $20K t Income from the P&L Example: $504K/24 = $21K ome Listed on the IniCal Signed 1003 Example: $25K ORTANT ITEMS TO NOTE Total Bank Statement Deposits MUST be within 5% of the Gross Revenue from the P&L P&L must be the same 24 month period as the bank statements aven Mortgage LLC This material is intended solely for the use of licensed mortgage professionals. DistribuCon to consumers is strictly prohibited. Program and rates are subject to change without nocce. Not available in all states. Terms sub

16 ASSET DEPLETIO llowed under Near-Prime ONLY - Rate/Term Refi or Purchases Net of down payment, loan costs and reserves: borrowers must have a minimum of the lesser of a) 1.5 Cmes the loan balance OR b) $1mm in qualified assets Qualified assets include: % of checking/savings/money market accounts 2. 70% of remaining value of stocks/bonds 3. 60% of recrement assets onthly Income = Net Qualified Assets / 120 Months aven Mortgage LLC This material is intended solely for the use of licensed mortgage professionals. DistribuCon to consumers is strictly prohibited. Program and rates are subject to change without nocce. Not available in all states. Terms sub

17 ASSET DEPLETIO CALCULATIO haven Mortgage LLC This material is intended solely for the use of licensed mortgage professionals. DistribuCon to consumers is strictly prohibited. Program and rates are subject to change without nocce. Not available in all states. Terms sub

18 NON - WARRANTABLE CONDOS Commercial Space Fannie No more then 25% of a condo project can be commercial space. Deephaven Up to 30% of the condo project can be commercial space. HOA Dues Fannie No more than 15% of total units in project may be 60 days or more past due. Deephaven No more than 20% of units may be 60 days or more past due. Li>ga>on Fannie If the lender determines that pending licgacon involves minor masers with no impact on the safety, structural soundness, habitability, or funcconal use of the project, the project is eligible provided the licgaco limited to one of the following categories: non-monetary licgacon involving neighbor disputes or rights of quiet enjoyment licgacon for which the claimed amount is known, the insurance carrier has agreed to provide the defen and the amount is covered by the HOA's or co-op corporacon's insurance; or the HOA or co-op is named as the plaincff in a foreclosure accon, or as a plaincff in an accon for past du HOA assessments Deephaven Acceptable as long as the pending lawsuit(s) are not structural in nature, do not affect the marketability of the units and: PotenCal damages do not exceed 25% of the HOA reserves, OR The associacon s insurance policy is sufficient to cover the licgacon

19 NON - WARRANTABLE CONDOS Single En>ty Ownership Fannie Projects in which a single encty owns more than 10% of the project are ineligible (2 4 unit project unit max; 5 20 unit project = 2 units max) Deephaven Allows up to 20% Investor Concentra>on Fannie At least 50% of the total units in the project must be conveyed to principal residence or second hom purchasers (investor occupancy only does not apply to primary or 2 nd home occupancy) Deephaven - Up to 60%. Guidelines specify that higher percentages may be considered under the Investmen Property Program, but does not explicitly say does not apply to primary or 2 nd home occupancy

20 FOREIGN NATIONALS Documenta>on Copies of the borrower s passport and unexpired visa must be obtained The following visa types are allowed as foreign naconals: B-1and B-2, H-2 and H-3, I, J-1 and J-2, O-2, P-1 and P-2 Credit For borrowers with a valid SSN A U.S. credit report should be obtained providing merged credit informacon from the 3 major naconal credit repositories Must meet standard tradeline requirements Qualifying Foreign Credit 3 open accounts with a 2-year history 2-year housing history can be used as a tradeline U.S. credit accounts can be combined with lesers of reference to establish the 3 open accounts

21 FOREIGN NATIONALS Income Salaried foreign naconal borrowers: Leser from employer providing current monthly salary and YTD earnings or 2 months pay stubs with YTD earnings VerificaCon of earnings for the last 2 years Employer to be independently verified Self-Employed foreign naconal borrowers for at least 2 years are allowed: Leser from a CPA providing income for the last 2 years and YTD earnings Self-employed business and CPA are to be independently verified (via LexisNexis, D&B InternaConal Business Search, Google, or other means of verificacon) **All documents must be translated by a cercfied translator Assets 12 months PITIA reserves required for the subject property All funds for the transaccon must be seasoned for 60 days Assets used for down payment and closing costs must also be seasoned in a U.S. depository insctucon for 30 prior to closing Assets held in foreign accounts are eligible for reserves. A 30 day statement is required. Funds to be converte U.S. dollars using the current exchange rate Property Eligible for 2 nd Home and Investment Property must verify any mortgage history for current residence.

22 DOWN PAYMENT AND ASSETS Minimum Borrower Contribu>on Borrowers must contribute a minimum of 5% of their own funds toward the down payment on purchase transaccons 10% contribucon required for the following: No housing history Loans amount > $424,100 2 nd Homes Limited trade lines Gi[ Funds Gi funds are allowed a er the borrower has made the minimum required borrower contribucon towards the down payment

23 DOWN PAYMENT AND ASSETS PITIA Reserves All transaccons require a minimum of 3 months reserves 6-12 month reserves are required for certain transaccons. Refer to the specific matrix and guidel Re>rement Accounts Vested funds from recrement accounts (IRA/Keogh and 401(k) accounts) are acceptable for down payment, closing costs, and reserves 100% of the vested amount may be used ReCrement accounts that do not allow any type of withdrawal may not be considered Funds do not have to be withdrawn to use for reserves

24 RESIDUAL INCOME AND PAYMENT SHOCK Residual Income Payment Shock $2,500 is required for Expanded-Prime product 150% max payment shock on primary residence transac>ons $2,500 is required for Near-Prime product $1,500 is required for Non-Prime product Up to 250% allowed with compensa>ng factor Addi>onal $150 per dependent is also required

25 ATIO GRID haven Mortgage LLC This material is intended solely for the use of licensed mortgage professionals. DistribuCon to consumers is strictly prohibited. Program and rates are subject to change without nocce. Not available in all states. Terms sub

26 INVESTOR ADVANTAGE Credit scores as low as 640 with a maximum $2,000,000 loan amount Investor Advantage designed for experienced investors with no income and no employment verificacon. Invertor Advantage Interest Only ARM s only 3/1 with 5 year I/O and 25 year AmorCzaCon, 7/1 I/O with 20 year AmorCzaCon LTV s for PURCHASE and Rate/Term up to 75% LTV s for CASH OUT up to 70%

27 INVESTOR ADVANTAGE ROAD MAP Addi>onal forms Required a. Business Purpose Affidavit 2 copies required 1 signed at applicacon and another signed AND notarized at closing b. Fannie Mae form 3170, 1-4 Family Rider c. Personal Guaranty if vested in an LLC

28 INVESTOR ADVANTAGE ROAD MAP We will accept a 1003 and ask that the following seccons not be completed: a. SecCon IV Employment InformaCon b. SecCon V Monthly Income and Combined Housing Expense InformaCon

29 FAQ - INVESTOR ADVANTAGE QUALIFICATIONS Credit Score Credit Reports should be supplied for all borrowers and/or guarantors If two borrowers, the lower of the two middle credit scores will be used for RepresentaCve Loan Score Tradelines 3 tradelines reporcng for 12+ months, OR 2 tradelines reporcng for 24+ months All with accvity in the last 12 months Late Payments Rolling late payments are not permised Employment / Income There is no employment verificacon or income analysis required There is no Debt-to-Income (DTI) or Debt Service Coverage RaCo (DSCR) requirement

appraisals are required for loans > $1,500,000 A Clear Capital Collateral Desk Analysis (CDA) is required for all")

30 FAQ - INVESTOR ADVANTAGE QUALIFICATIONS Documenta>on Full asset documentacon is required for purchase transaccons to evidence sufficient funds to clos Assets must be sourced or seasoned for 60 days Gi[ Funds Not permised Reserves There is no reserve requirement Appraisal Two (2) appraisals are required for loans > $1,500,000 A Clear Capital Collateral Desk Analysis (CDA) is required for all transaccons

31 CENARIO DESK General uideline ues>ons nswered Excep>on Requests Credit Review Complex Income calcula>on ques>ons The Deephaven Mortgage Scenario Desk is designed to help you quickly determine whi borrowers are likely to qualify for our progra Deephaven s experienced mortgage professionals are here to help at any step al the way! Quick Ques>ons? Call: scenario@deephavenmortgage.com haven Mortgage LLC This material is intended solely for the use of licensed mortgage professionals. DistribuCon to consumers is strictly prohibited. Program and rates are subject to change without nocce. Not available in all states. Terms sub

Non-QM Value & Benefit

z z 1 Non-QM Value & Benefit More investor loan op0ons Borrowers who were nega0vely impacted by housing crisis Limited by past consumer credit problems Outside of agency investor guidelines Qualify with

z z 1 Non-QM Value & Benefit More investor loan op0ons Borrowers who were nega0vely impacted by housing crisis Limited by past consumer credit problems Outside of agency investor guidelines Qualify with

The Non-QM. Investor Advantage Program. Presented by Nations Direct Mortgage. Intended for mortgage professionals. Not intended for consumers.

The Non-QM Investor Advantage Program Presented by Nations Direct Mortgage Investor Advantage NO Income NO Reserves NO Debt Coverage Ratio NO Limitation on Financed Properties NO Prepayment Penalty Investor

The Non-QM Investor Advantage Program Presented by Nations Direct Mortgage Investor Advantage NO Income NO Reserves NO Debt Coverage Ratio NO Limitation on Financed Properties NO Prepayment Penalty Investor

The Non-QM. Investor Advantage Program. Presented by Nations Direct Mortgage. Intended for mortgage professionals. Not intended for consumers.

The Non-QM Investor Advantage Program Presented by Nations Direct Mortgage Investor Advantage What is the Investor Advantage program? The Investor Advantage Credit Grade is designed for investment, nonowner

The Non-QM Investor Advantage Program Presented by Nations Direct Mortgage Investor Advantage What is the Investor Advantage program? The Investor Advantage Credit Grade is designed for investment, nonowner

Fannie Mae High Balance Matrix

Revision: July 16, 2016 (Product Information Center, 949-390-2684, www.jmaclending.com Finance Type Purchas and Rate/Term Refinances Cash Out Refinances Occupancy Owner Occupied Owner Occupied Term Property

Revision: July 16, 2016 (Product Information Center, 949-390-2684, www.jmaclending.com Finance Type Purchas and Rate/Term Refinances Cash Out Refinances Occupancy Owner Occupied Owner Occupied Term Property

Full Doc. 24 Months 12 Months

Leverage Prime Primary Residence FICO Loan Amount 720+ 2,000,001-2,500,000 2,500,001-3,000,000 6-719 2,000,001-2,500,000 2,500,001-3,000,000 660-679 Full Doc 24 Months 12 Months Purch / RT Refi Cash Out

Leverage Prime Primary Residence FICO Loan Amount 720+ 2,000,001-2,500,000 2,500,001-3,000,000 6-719 2,000,001-2,500,000 2,500,001-3,000,000 660-679 Full Doc 24 Months 12 Months Purch / RT Refi Cash Out

Expanded Prime Matrix

Expanded Prime Matrix Loan Amount FICO Purch. & R/T Purch. & R/T 50% DTI or 24 Mos Bank Stmts Minimum Loan Amount $100,000 $1,000,000 $1,000,001- $1,500,000 Program Max LTVs > $1,500,000 12 Months 720

Expanded Prime Matrix Loan Amount FICO Purch. & R/T Purch. & R/T 50% DTI or 24 Mos Bank Stmts Minimum Loan Amount $100,000 $1,000,000 $1,000,001- $1,500,000 Program Max LTVs > $1,500,000 12 Months 720

theexpanded Prime Matrix

theexpanded Prime Matrix Program Max LTVs Loan Amount FICO Purch. & R/T Purch. & R/T 50% DTI or 24 Mos Bank Stmts Minimum Loan Amount $100,000 $1,000,000 $1,000,001-,000 720 90% FICO 700 Maximum Loan Amount

theexpanded Prime Matrix Program Max LTVs Loan Amount FICO Purch. & R/T Purch. & R/T 50% DTI or 24 Mos Bank Stmts Minimum Loan Amount $100,000 $1,000,000 $1,000,001-,000 720 90% FICO 700 Maximum Loan Amount

STATED INCOME PROGRAM

Fully Amortized 7/1 Portfolio ARM Product Mix Primary Residence, Second Home and Investment Property Purchase, Rate & Term Refinance and Cash-Out Refinance STATED INCOME PROGRAM Rate Guide as of 5/23/2018

Fully Amortized 7/1 Portfolio ARM Product Mix Primary Residence, Second Home and Investment Property Purchase, Rate & Term Refinance and Cash-Out Refinance STATED INCOME PROGRAM Rate Guide as of 5/23/2018

STATED INCOME PROGRAM

Fully Amortized 5/1 & 7/1 Portfolio ARM Product Mix Primary Residence, Second Home and Investment Property Purchase, Rate & Term Refinance and Cash-Out Refinance STATED INCOME PROGRAM Rate Guide as of

Fully Amortized 5/1 & 7/1 Portfolio ARM Product Mix Primary Residence, Second Home and Investment Property Purchase, Rate & Term Refinance and Cash-Out Refinance STATED INCOME PROGRAM Rate Guide as of

Highland Expanded Prime Matrix

Highland Expanded Prime Matrix Program Max LTVs Loan Amount FICO Purch. & R/T Purch. & R/T 50% DTI or 24 Mos Bank Stmts Minimum Loan Amount $300,000 $1,000,000 $1,000,001-,000 720 90% FICO 700 Maximum

Highland Expanded Prime Matrix Program Max LTVs Loan Amount FICO Purch. & R/T Purch. & R/T 50% DTI or 24 Mos Bank Stmts Minimum Loan Amount $300,000 $1,000,000 $1,000,001-,000 720 90% FICO 700 Maximum

ClearEdge Core Full Doc/ Express Doc/Bank Statements

ClearEdge Core Full Doc/ Express Doc/Bank Statements / Cash-Out Owner / Second Home / Non-Owner Loan Amount Credit Score LTV/CLTV Recent Credit Event** LTV/CLTV 680 90 Purchase Only 85 $1.5 MM 640 85 80

ClearEdge Core Full Doc/ Express Doc/Bank Statements / Cash-Out Owner / Second Home / Non-Owner Loan Amount Credit Score LTV/CLTV Recent Credit Event** LTV/CLTV 680 90 Purchase Only 85 $1.5 MM 640 85 80

Bank Statement Program Guidelines

Bank Statement Programs Calculation/Documentation The Bank Statement Income option is designed to qualify a borrower by analyzing cash flow from the borrower s bank accounts. Option One: 12 months Personal

Bank Statement Programs Calculation/Documentation The Bank Statement Income option is designed to qualify a borrower by analyzing cash flow from the borrower s bank accounts. Option One: 12 months Personal

INVESTOR SOLUTION IS series DSCR PROGRAM

INVESTOR SOLUTION IS series DSCR PROGRAM Program Limits DSCR >= 1.15 DSCR < 1.15 / No Ratio Loan Amount FICO Purch & R/T Cash-out Purch & R/T Cash Out 720 80% 75% 75% 70%

INVESTOR SOLUTION IS series DSCR PROGRAM Program Limits DSCR >= 1.15 DSCR < 1.15 / No Ratio Loan Amount FICO Purch & R/T Cash-out Purch & R/T Cash Out 720 80% 75% 75% 70%

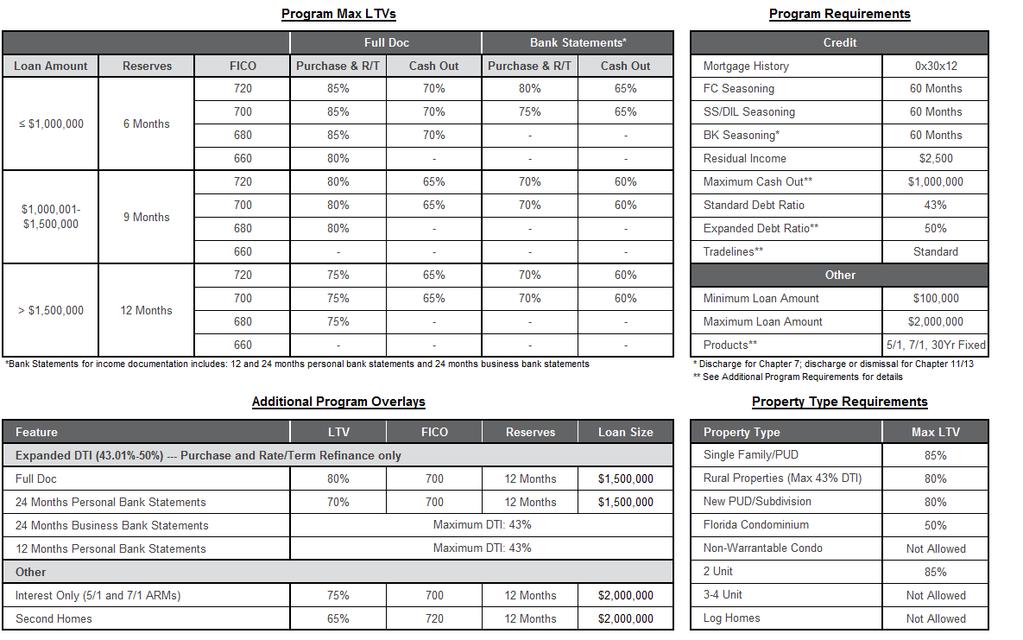

Expanded-Prime Matrix

ExpandedPrime Matrix Email: wholesalelock@deephavenmortgage.com Phone: (844) 3469475 Program Max LTVs Program Requirements Bank Statements* Loan Amount Reserves FICO Mortgage History 0x30x12 FC Seasoning

ExpandedPrime Matrix Email: wholesalelock@deephavenmortgage.com Phone: (844) 3469475 Program Max LTVs Program Requirements Bank Statements* Loan Amount Reserves FICO Mortgage History 0x30x12 FC Seasoning

Expanded Prime Matrix

Expanded Prime Matrix Program Max LTVs Primary and Second Homes Program Requirements Alternative Doc Enhanced Debt Ratio Loan Amount FICO Purch. & R/T Purch. & R/T 50% DTI or 24 Mos Bank Stmts Minimum

Expanded Prime Matrix Program Max LTVs Primary and Second Homes Program Requirements Alternative Doc Enhanced Debt Ratio Loan Amount FICO Purch. & R/T Purch. & R/T 50% DTI or 24 Mos Bank Stmts Minimum

ULTRA JUMBO (UJ series) FULL DOC PROGRAM

FULL DOC PROGRAM") ULTRA JUMBO (UJ series) FULL DOC PROGRAM Purchase and Rate/Term Refinance Owner Occupied Investment Property FICO Loan Amt SFR, Condos, PUDs Second Home 2-4 Family SFR, Condo, PUDs & 2-4 Family LTV CLTV

ULTRA JUMBO (UJ series) FULL DOC PROGRAM Purchase and Rate/Term Refinance Owner Occupied Investment Property FICO Loan Amt SFR, Condos, PUDs Second Home 2-4 Family SFR, Condo, PUDs & 2-4 Family LTV CLTV

Full Doc Program Guidelines

Full Doc Programs Calculation/Documentation The full doc program is used to qualify a borrower by analyzing the source of their income for stability and continuity Wage Earners Income derived from a consistent

Full Doc Programs Calculation/Documentation The full doc program is used to qualify a borrower by analyzing the source of their income for stability and continuity Wage Earners Income derived from a consistent

Portfolio Wholesale Fees

https://correspondent.axosbank.com PORTFOLIO ARM - BORROWER PAID 5/1 LIBOR ARM 6/2/6 (JP51, JP51IO) 7/1 LIBOR ARM 6/2/6 (JP71) 10/1 LIBOR ARM 6/2/6 (JP101) Base Rate 21 Day 30 Day 45 Day 60 Day Base Rate

https://correspondent.axosbank.com PORTFOLIO ARM - BORROWER PAID 5/1 LIBOR ARM 6/2/6 (JP51, JP51IO) 7/1 LIBOR ARM 6/2/6 (JP71) 10/1 LIBOR ARM 6/2/6 (JP101) Base Rate 21 Day 30 Day 45 Day 60 Day Base Rate

Portfolio Wholesale Fees

https://correspondent.axosbank.com PORTFOLIO ARM - BORROWER PAID 5/1 LIBOR ARM 6/2/6 (JP51, JP51IO) 7/1 LIBOR ARM 6/2/6 (JP71) 10/1 LIBOR ARM 6/2/6 (JP101) Base Rate 21 Day 30 Day 45 Day 60 Day Base Rate

https://correspondent.axosbank.com PORTFOLIO ARM - BORROWER PAID 5/1 LIBOR ARM 6/2/6 (JP51, JP51IO) 7/1 LIBOR ARM 6/2/6 (JP71) 10/1 LIBOR ARM 6/2/6 (JP101) Base Rate 21 Day 30 Day 45 Day 60 Day Base Rate

ditech BUSINESS LENDING JUMBO PRODUCTS

1. PRODUCT DESCRIPTION Conventional Jumbo fixed rate and ARM mortgages Fixed Rate: 15 and 30 year terms 5/1 LIBOR ARM: 30 year term Fully amortizing Qualified Mortgage (QM) Safe Harbor loans are permitted

1. PRODUCT DESCRIPTION Conventional Jumbo fixed rate and ARM mortgages Fixed Rate: 15 and 30 year terms 5/1 LIBOR ARM: 30 year term Fully amortizing Qualified Mortgage (QM) Safe Harbor loans are permitted

Specialty Products Underwriting Guidelines

Specialty Products Underwriting Guidelines Non-Warrantable Condos SE Bank Solutions Foreign Nationals Recent Housing Event Investor Loan SPECIALTY PRODUCT UNDERWRITING GUIDELINES (INCLUDES: NON-WARRANTABLE

Specialty Products Underwriting Guidelines Non-Warrantable Condos SE Bank Solutions Foreign Nationals Recent Housing Event Investor Loan SPECIALTY PRODUCT UNDERWRITING GUIDELINES (INCLUDES: NON-WARRANTABLE

Portfolio Libor Arms Guidelines

Portfolio Libor Arms Guidelines Effective Date: 02/21/2017 Loans meeting the parameters outlined in this guideline matrix must be consistent with the Dodd Frank Wall Street Reform and Consumer Protection

Portfolio Libor Arms Guidelines Effective Date: 02/21/2017 Loans meeting the parameters outlined in this guideline matrix must be consistent with the Dodd Frank Wall Street Reform and Consumer Protection

FULL DOC. PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO. Owner Occupied (O/O) 1 unit 80% 80% unit (see MI section below) 95% 95% 700

1 unit 80% 80% unit (see MI section below) 95% 95% 700") FULL DOC PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO PURCHASE Owner Occupied (O/O) 1 unit (see MI section below) 95% 95% 700 1 unit (see MI section below) 97% 97% 720 2 units (see MI section below) 95%

FULL DOC PURPOSE/OCCUPANCY/UNITS LTV CLTV Minimum FICO PURCHASE Owner Occupied (O/O) 1 unit (see MI section below) 95% 95% 700 1 unit (see MI section below) 97% 97% 720 2 units (see MI section below) 95%

JUMBO PRIME PROGRAM (FIXED & ARM)

") JUMBO PRIME PROGRAM (FIXED & ARM) PRIMARY RESIDENCE Purchase & Rate/Term Refinance (1),(2) Units Min. FICO LTV/CLTV/ HCLTV Max. DTI Max. Loan Amount 700 80% 43% 1 unit 680 80% 35% 680 70% 43% 740 80% 43%

JUMBO PRIME PROGRAM (FIXED & ARM) PRIMARY RESIDENCE Purchase & Rate/Term Refinance (1),(2) Units Min. FICO LTV/CLTV/ HCLTV Max. DTI Max. Loan Amount 700 80% 43% 1 unit 680 80% 35% 680 70% 43% 740 80% 43%

PRODUCT GUIDELINES LENDER PAID MORTGAGE INSURANCE PROGRAM (LPMI) PROGRAM CODES: C30FLPMI, H30FLPMI

PROGRAM CODES: C30FLPMI, H30FLPMI") Occupancy Purpose Max Loan Amount Maximum LTV/ CLTV LOAN AMOUNTS

Occupancy Purpose Max Loan Amount Maximum LTV/ CLTV LOAN AMOUNTS

WesLend Advantage Non-QM ITIN

SECTION 1: MATRIX: Highlight: Uses the borrowers Individual Taxpayer Identification Number, (ITIN) in lieu of a Social Security number Credit Scores NOT Required Credit Report is pulled with every ITIN

SECTION 1: MATRIX: Highlight: Uses the borrowers Individual Taxpayer Identification Number, (ITIN) in lieu of a Social Security number Credit Scores NOT Required Credit Report is pulled with every ITIN

EXPANDED ACCESS PROGRAM GUIDE Version 3.6 effective 8/14/2017. Table of Contents

Version 3.6 - updated 8/14/2017 Table of Contents EXPANDED ACCESS PROGRAM GUIDE Version 3.6 effective 8/14/2017 1 OVERVIEW...4 2 UNDERWRITING CRITERIA...4 3 PRODUCT ELIGIBILITY...5 3.1 AVAILABLE PRODUCTS...

Version 3.6 - updated 8/14/2017 Table of Contents EXPANDED ACCESS PROGRAM GUIDE Version 3.6 effective 8/14/2017 1 OVERVIEW...4 2 UNDERWRITING CRITERIA...4 3 PRODUCT ELIGIBILITY...5 3.1 AVAILABLE PRODUCTS...

Conventional and Government Program Overlays

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

") ; LOAN AMOUNTS

; LOAN AMOUNTS "Ultra Standard" (Full Doc) & "Ultra 24" (Alt Doc) Eligibility Chart

& Ultra 24 (Alt Doc) Eligibility Chart") Effective Date: 09/19/2017 Loans meeting the parameters outlined in this guideline matrix must be consistent with the Dodd Frank Wall Street Reform and Consumer Protection Act Ability to Repay (ATR). Documentation

Effective Date: 09/19/2017 Loans meeting the parameters outlined in this guideline matrix must be consistent with the Dodd Frank Wall Street Reform and Consumer Protection Act Ability to Repay (ATR). Documentation

Conventional and Government Program Overlays

Financed Properties Minimum Loan Amount $60,000 OVERLAYS All Programs Limited to a maximum of 4 loans to one borrower and up to $1.5MM. Power of Attorney Texas 50(a)(6) & 50(f) Allowed for active duty

Financed Properties Minimum Loan Amount $60,000 OVERLAYS All Programs Limited to a maximum of 4 loans to one borrower and up to $1.5MM. Power of Attorney Texas 50(a)(6) & 50(f) Allowed for active duty

Jumbo Non-Conforming Products (Series-49)

") Jumbo Non-Conforming Products (Series-49) This guide provides parameters for standard fixed rate and 5/1, 7/1, and 10/1 adjustable rate, fully amortizing, nonconforming products for primary residence up

Jumbo Non-Conforming Products (Series-49) This guide provides parameters for standard fixed rate and 5/1, 7/1, and 10/1 adjustable rate, fully amortizing, nonconforming products for primary residence up

Silvergate Expanded % % % % % % % % % %

Silvergate Expanded Silvergate Bank Correspondent Lending (SCL) Non- QM 5/1, 7/1 ARM And Fixed Rate Product Matrix Date 5/10/2018 Loans meeting the parameters outlined in this guideline matrix must be

Silvergate Expanded Silvergate Bank Correspondent Lending (SCL) Non- QM 5/1, 7/1 ARM And Fixed Rate Product Matrix Date 5/10/2018 Loans meeting the parameters outlined in this guideline matrix must be

PREMIER JUMBO PROGRAM GUIDE

\ PREMIER JUMBO PROGRAM GUIDE This document is provided for approved loan sellers only and may not be copied, distributed or disclosed to any other party. All terms herein are subject to change by FundLoans

\ PREMIER JUMBO PROGRAM GUIDE This document is provided for approved loan sellers only and may not be copied, distributed or disclosed to any other party. All terms herein are subject to change by FundLoans

NON-QM MATRIX WHOLESALE DIVISION Sky Park Circle, Ste 100, Irvine, CA rev. March 12, FULL DOC. Min.

SILVER NON-QM MATRIX WHOLESALE DIVISION 17802 Sky Park Circle, Ste 100, Irvine, CA 92614 rev. March 12, 2018 www.ec-tpo.com PRODUCT DESCRIPTION Full doc available for Self Employed and W 2 borrowers 24

SILVER NON-QM MATRIX WHOLESALE DIVISION 17802 Sky Park Circle, Ste 100, Irvine, CA 92614 rev. March 12, 2018 www.ec-tpo.com PRODUCT DESCRIPTION Full doc available for Self Employed and W 2 borrowers 24

Acceptable States. Loan Products. ARM Terms

Program Name: Investor Qualification Product Program Highlights The borrower is qualified based upon the cash flows of the subject property only, regardless of the number of properties owned by the borrower

Program Name: Investor Qualification Product Program Highlights The borrower is qualified based upon the cash flows of the subject property only, regardless of the number of properties owned by the borrower

Conventional and Government Program Overlays. OVERLAYS All Programs

4506-T/1040s Requirements Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses and/or unreimbursed expenses, 2 years of tax transcripts and 2 years 1040s will

4506-T/1040s Requirements Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses and/or unreimbursed expenses, 2 years of tax transcripts and 2 years 1040s will

Max LTV/CLTV FICO 1 Unit 95/95% /90% 620 Purchase 85/85% 620 Refi 75/75% 2 Units Purchase & Refi- 85/85% 620 N/A N/A 75/75% 620

Revision: October 25, 2016 (Product Information Center, 949-390-2670, www.jmaclending.com) Fixed Rate (Purchase & Rate/Term Refinances) Fannie Mae DU Products: CF30, CF20, CF15, CF10 Occupancy Owner Occupied

Revision: October 25, 2016 (Product Information Center, 949-390-2670, www.jmaclending.com) Fixed Rate (Purchase & Rate/Term Refinances) Fannie Mae DU Products: CF30, CF20, CF15, CF10 Occupancy Owner Occupied

First Time Home Buyer not permitted

Just Missed Agency Full Doc Bank Statements Reserves 24 Months 12 Months 24 Months 12 Months Purchase & R/T Cash Out Purchase & R/T Cash Out Purchase & R/T Cash Out Purchase & R/T Cash Out 720+

Just Missed Agency Full Doc Bank Statements Reserves 24 Months 12 Months 24 Months 12 Months Purchase & R/T Cash Out Purchase & R/T Cash Out Purchase & R/T Cash Out Purchase & R/T Cash Out 720+

AmWest Advantage Program Matrix

1 Unit SFR, PUD, and Condos 24 Units AmWest Advantage Program Matrix PRIMARY RESIDENCE, 2ND HOME & INVESTMENT PROPERTIES PROPERTY TYPE MAX LOAN AMOUNT MAX LTV MAX CLTV MIN FICO 75% 720 $1,000,000 70% 680

1 Unit SFR, PUD, and Condos 24 Units AmWest Advantage Program Matrix PRIMARY RESIDENCE, 2ND HOME & INVESTMENT PROPERTIES PROPERTY TYPE MAX LOAN AMOUNT MAX LTV MAX CLTV MIN FICO 75% 720 $1,000,000 70% 680

First Time Home Buyer not permitted. Purchase, R/T, and Debt Consol Only

Just Missed Agency Reserves 24 Months 12 Months 24 Months 12 Months Purchase & R/T Purchase & R/T Purchase & R/T Purchase & R/T 720+

Just Missed Agency Reserves 24 Months 12 Months 24 Months 12 Months Purchase & R/T Purchase & R/T Purchase & R/T Purchase & R/T 720+

Conforming and High Balance Guideline Fannie Mae

Revision: December 18, 2017 (Product Information Center, 949-390-2670, www.jmaclending.com) Fixed Rate (Purchase & Rate/Term Refinances) Products: CF30, CF20, CF15, CF10 Occupancy Owner Occupied Second

Revision: December 18, 2017 (Product Information Center, 949-390-2670, www.jmaclending.com) Fixed Rate (Purchase & Rate/Term Refinances) Products: CF30, CF20, CF15, CF10 Occupancy Owner Occupied Second

JUMBO A PROGRAM GUIDE

TABLE OF CONTENTS 1 OVERVIEW... 3 2 UNDERWRITING CRITERIA... 3 3 PRODUCT ELIGIBILITY... 4 3.1 AVAILABLE PRODUCTS... 4 3.2 ADJUSTABLE RATE CRITERIA... 4 4 PRODUCT MATRIX... 5 4.1 GEOGRAPHY... 5 4.2 MINIMUM

TABLE OF CONTENTS 1 OVERVIEW... 3 2 UNDERWRITING CRITERIA... 3 3 PRODUCT ELIGIBILITY... 4 3.1 AVAILABLE PRODUCTS... 4 3.2 ADJUSTABLE RATE CRITERIA... 4 4 PRODUCT MATRIX... 5 4.1 GEOGRAPHY... 5 4.2 MINIMUM

DTI. Loan Amounts > $3,000,000 Grade. Only Available in the following states: CA, IL, FL, NJ, MD, VA, DC, WA Housing. Full Doc 12 mo & 24 mo

Just Missed Agency Full Doc Bank Statements 24 Months 12 Months 24 Months 12 Months Purchase & R/T Purchase & R/T Purchase & R/T Purchase & R/T 720+

Just Missed Agency Full Doc Bank Statements 24 Months 12 Months 24 Months 12 Months Purchase & R/T Purchase & R/T Purchase & R/T Purchase & R/T 720+

70** 65** 70** N/A 70** N/A

ICON ELITE Reserves 24 Months 12 Months 24 Months 12 Months FICO Loan Amount Purchase & R/T Cash Out Purchase & R/T Cash Out Purchase & R/T Cash Out Purchase & R/T Cash Out

ICON ELITE Reserves 24 Months 12 Months 24 Months 12 Months FICO Loan Amount Purchase & R/T Cash Out Purchase & R/T Cash Out Purchase & R/T Cash Out Purchase & R/T Cash Out

Fannie Mae (DU) Conventional Loan Matrix

Conventional Loan Matrix") PURCHASE/ LIMITED CASH OUT REFINANCES STANDARD and HIGH BALANCE LOAN AMOUNTS Occupancy Maximum* LTV Maximum* CLTV Min FICO* Max Ratios Minimum Cash Investments Mortgage/ Rental History Reserves 1 Unit

PURCHASE/ LIMITED CASH OUT REFINANCES STANDARD and HIGH BALANCE LOAN AMOUNTS Occupancy Maximum* LTV Maximum* CLTV Min FICO* Max Ratios Minimum Cash Investments Mortgage/ Rental History Reserves 1 Unit

SUPER JUMBO PRIMARY RESIDENCE. Min FICO. SFR, Condo* Townhouse PUD, 2 Units. Min FICO. SFR, Condo, Townhouse, PUD, 2 Units SECOND HOMES.

SJ Series SUPER JUMBO PRIMARY RESIDENCE Occupancy Loan Purpose Property Type Min FICO LTV/CLTV Max Loan Amt Primary Residence Purchase & Rate/Term Refinance SFR, Condo* PUD, 2 Units 720 80/80 $2,000,000

SJ Series SUPER JUMBO PRIMARY RESIDENCE Occupancy Loan Purpose Property Type Min FICO LTV/CLTV Max Loan Amt Primary Residence Purchase & Rate/Term Refinance SFR, Condo* PUD, 2 Units 720 80/80 $2,000,000

1100 Series Portfolio Products. Table of Contents

1100 Series Portfolio Products Table of Contents PRODUCT PAGE NUMBER Expanded Ratio Program 2 Debt Ratio to 55%, fixed and ARM, LTV to 80% Asset Inclusion to Income Program 5 Assets as Future Income, no

1100 Series Portfolio Products Table of Contents PRODUCT PAGE NUMBER Expanded Ratio Program 2 Debt Ratio to 55%, fixed and ARM, LTV to 80% Asset Inclusion to Income Program 5 Assets as Future Income, no

HomePath Program Guidelines

The following guidelines apply to all DIRECTORS MORTGAGE s HomePath loan programs. All loans must adhere to the criteria of these guidelines. This guide addresses the specific areas needed to facilitate

The following guidelines apply to all DIRECTORS MORTGAGE s HomePath loan programs. All loans must adhere to the criteria of these guidelines. This guide addresses the specific areas needed to facilitate

Solutions Non-QM Program Guidelines

Solutions Non-QM Program Guidelines Revised 7/16/2018 rev. 10 (Click the link to go straight to the section) 1 Program Summary 11 Underwriting Method 21 Geographic Restrictions 2 Product Codes 12 Credit

Solutions Non-QM Program Guidelines Revised 7/16/2018 rev. 10 (Click the link to go straight to the section) 1 Program Summary 11 Underwriting Method 21 Geographic Restrictions 2 Product Codes 12 Credit

ditech BUSINESS LENDING JUMBO AA PRODUCT CORRESPONDENT LENDING

ditech BUSINESS LENDING JUMBO AA PRODUCT CORRESPONDENT LENDING See attached Client Guide Supplement: The Client Guide Supplement is to be used in conjunction with the Product Matrix and the Jumbo Chapter

ditech BUSINESS LENDING JUMBO AA PRODUCT CORRESPONDENT LENDING See attached Client Guide Supplement: The Client Guide Supplement is to be used in conjunction with the Product Matrix and the Jumbo Chapter

Core Seconds S Year Fixed S Year Fixed

TABLE OF CONTENTS PRODUCT DESCRIPTION Page # Product Description 3 ELIGIBILITY Occupancy 3 Underwriting Methods 3 Documentation Requirements 3 Transaction Types 3 Eligible Property Types, Ineligible Property

TABLE OF CONTENTS PRODUCT DESCRIPTION Page # Product Description 3 ELIGIBILITY Occupancy 3 Underwriting Methods 3 Documentation Requirements 3 Transaction Types 3 Eligible Property Types, Ineligible Property

EXTENDED JUMBO (FIXED & ARM)

") EXTENDED JUMBO (FIXED & ARM) PURCHASE AND RATE TERM REFINANCE 1,3,4 Occupancy Units Min. FICO LTV/CLTV Loan Amount 740 90/90 Purch only $1,000,000 720 85/85 Purch only $2,000,000 80/90 $2,500,000 1 80/90

EXTENDED JUMBO (FIXED & ARM) PURCHASE AND RATE TERM REFINANCE 1,3,4 Occupancy Units Min. FICO LTV/CLTV Loan Amount 740 90/90 Purch only $1,000,000 720 85/85 Purch only $2,000,000 80/90 $2,500,000 1 80/90

AUS Approved Eligible / Accept Eligible - Up to 50% Maximum DTI. AUS Approved Eligible / Accept Eligible - Up to 50% Maximum DTI 620*

; PURCHASE & RATE/TERM REFINANCE - FIXED RATE Occupancy Max Loan Amount Maximum LTV Maximum CLTV Min FICO Max Ratios Minimum Cash Investments Mortgage/Rental History Reserves Primary 1 Unit $453,100 95%*

; PURCHASE & RATE/TERM REFINANCE - FIXED RATE Occupancy Max Loan Amount Maximum LTV Maximum CLTV Min FICO Max Ratios Minimum Cash Investments Mortgage/Rental History Reserves Primary 1 Unit $453,100 95%*

Product Guidelines CONVENTIONAL CONFORMING FIXED PROGRAM

; PURCHASE & RATE/TERM REFINANCE - FIXED RATE Occupancy Max Loan Amount Maximum LTV Maximum CLTV Min FICO Max Ratios Minimum Cash Investments Mortgage/Rental History Reserves Primary 1 Unit $484,350 95%*

; PURCHASE & RATE/TERM REFINANCE - FIXED RATE Occupancy Max Loan Amount Maximum LTV Maximum CLTV Min FICO Max Ratios Minimum Cash Investments Mortgage/Rental History Reserves Primary 1 Unit $484,350 95%*

Malibu Non-Agency Matrix

Revision: May 1, 2018 (Product Information Center, 949-390-2684, www.jmaclending.com PURCHASE AND R&T REFINANCE FIXED RATE AND FULLY AMORTIZING ARMs CASH-OUT REFINANCE Occupancy Units Max Loan Amount LTV/CLTV

Revision: May 1, 2018 (Product Information Center, 949-390-2684, www.jmaclending.com PURCHASE AND R&T REFINANCE FIXED RATE AND FULLY AMORTIZING ARMs CASH-OUT REFINANCE Occupancy Units Max Loan Amount LTV/CLTV

High-Cost Area (High Balance) Loan Amounts

Loan Amounts") Program Qualifications Eligible loans are conforming and high balance loans receiving a DU Version 10.0 or later Approve/Eligible. Maximum Loan Amounts Conforming Maximum Loan Amounts Units Continental

Program Qualifications Eligible loans are conforming and high balance loans receiving a DU Version 10.0 or later Approve/Eligible. Maximum Loan Amounts Conforming Maximum Loan Amounts Units Continental

Orion Lending Alt A. Edge. Program Guidelines and Matrices

Orion Lending Alt A Edge Program Guidelines and Matrices Table of Contents Section 1 Overview & Underwriting Criteria... 4 Section 2 - Underwriting Criteria... 4 Section 3 Product Eligibility... 6 3.1

Orion Lending Alt A Edge Program Guidelines and Matrices Table of Contents Section 1 Overview & Underwriting Criteria... 4 Section 2 - Underwriting Criteria... 4 Section 3 Product Eligibility... 6 3.1

Premium Jumbo Fixed & 10/1 ARM

Last Update 11/29/2017 Primary (Purchase & Rate/Term NO MI OPTION) Primary (Purchase) Primary (Rate/Term Ref.) Loan Amt LTV/CLTV Min Fico DTI Reserves Loan Amt LTV/CLTV Min Fico DTI Reserves Loan Amt LTV/CLTV

Last Update 11/29/2017 Primary (Purchase & Rate/Term NO MI OPTION) Primary (Purchase) Primary (Rate/Term Ref.) Loan Amt LTV/CLTV Min Fico DTI Reserves Loan Amt LTV/CLTV Min Fico DTI Reserves Loan Amt LTV/CLTV

Fannie & High BalanceGuidelines

Fannie & High BalanceGuidelines Agency Finance Type Occupancy Term High balance and transactions with non-occupant coborrowers are limited to 95% LTV/CLTV. High Balance Cash Out Transactions are limited

Fannie & High BalanceGuidelines Agency Finance Type Occupancy Term High balance and transactions with non-occupant coborrowers are limited to 95% LTV/CLTV. High Balance Cash Out Transactions are limited

ELIGIBILITY MATRIX & SUMMARY GUIDELINES 15 & 30 YR Fixed Rates

Revised 6/2/2014 Changes from prior versions are in red font Overlays to Fannie guidelines are underlined Correspondent Lending Jumbo "Premier" Fixed Rate and ARM Product Profile Based on a Fannie Mae

Revised 6/2/2014 Changes from prior versions are in red font Overlays to Fannie guidelines are underlined Correspondent Lending Jumbo "Premier" Fixed Rate and ARM Product Profile Based on a Fannie Mae

PREMIUM: JUMBO TIER 2 PROGRAM

PREMIUM: JUMBO TIER 2 PROGRAM Introduction: This program is intended for borrowers with good credit and higher documented liabilities, when the Debt to Income ratio (DTI) can be allowed up to 50%. Program

PREMIUM: JUMBO TIER 2 PROGRAM Introduction: This program is intended for borrowers with good credit and higher documented liabilities, when the Debt to Income ratio (DTI) can be allowed up to 50%. Program

Product Matrix Carrington Flexible Advantage Plus Program

Program Max LTVs Program Maximum LTVs Primary Investment Full Doc Alternative Doc Full Doc Alternative Doc Program Requirements Loan Amount Reserves FICO Purch & R/T Cash Out Purch & R/T Cash Out Purch

Program Max LTVs Program Maximum LTVs Primary Investment Full Doc Alternative Doc Full Doc Alternative Doc Program Requirements Loan Amount Reserves FICO Purch & R/T Cash Out Purch & R/T Cash Out Purch

Fannie Mae Conforming and High Balance

Primary Purchase or 620 620 Second Home 1 Fixed 97% 1,2 / ARM 90% 2 Fixed 85% / ARM 75% 3-4 Fixed 75% / ARM 65% 1 Fixed 80% / ARM 75% 2-4 Fixed 75% / ARM 65% Purchase or 620 1 Fixed 90% / ARM 80% 620 1

Primary Purchase or 620 620 Second Home 1 Fixed 97% 1,2 / ARM 90% 2 Fixed 85% / ARM 75% 3-4 Fixed 75% / ARM 65% 1 Fixed 80% / ARM 75% 2-4 Fixed 75% / ARM 65% Purchase or 620 1 Fixed 90% / ARM 80% 620 1

PRODUCT GUIDELINES CONVENTIONAL CONFORMING HIGH BALANCE PROGRAM (DU ONLY)

") PURCHASE, RATE &TERM REFINANCE - FIXED RATE Occupancy Max Loan Amount LTV CLTV Min FICO Max Ratios Minimum Cash Investments Mortgage/Rental History Reserves 90%* 90%* 620 75.0% 75.0% 75.0% 75.0% 620 620

PURCHASE, RATE &TERM REFINANCE - FIXED RATE Occupancy Max Loan Amount LTV CLTV Min FICO Max Ratios Minimum Cash Investments Mortgage/Rental History Reserves 90%* 90%* 620 75.0% 75.0% 75.0% 75.0% 620 620

Non Conforming JUMBO Programs

Non Conforming JUMBO Programs Select QM Eligibility Matrix Fixed Rate and Hybrid ARM Products Primary Residence Purchase, Rate and Term Transaction Type Units FICO LTV/CLTV/HCLTV Loan Amount 1 760 85%

Non Conforming JUMBO Programs Select QM Eligibility Matrix Fixed Rate and Hybrid ARM Products Primary Residence Purchase, Rate and Term Transaction Type Units FICO LTV/CLTV/HCLTV Loan Amount 1 760 85%

JUMBO PRIME PROGRAM JUMBO PRIME PROGRAM

JUMBO PRIME PROGRAM PRIMARY RESIDENCE Purchase & Rate/Term Refinance Units Max. Loan Amount (1) LTV CLTV Min. FICO Max. Cash-Out $2,000,000 80% 80% 740 $1,750,000 80% 80% 720 $2,000,000 75% 75% 720 $2,250,000

JUMBO PRIME PROGRAM PRIMARY RESIDENCE Purchase & Rate/Term Refinance Units Max. Loan Amount (1) LTV CLTV Min. FICO Max. Cash-Out $2,000,000 80% 80% 740 $1,750,000 80% 80% 720 $2,000,000 75% 75% 720 $2,250,000

Conventional and Government Program Overlays. OVERLAYS All Programs

4506-T/1040s Requirements Asset Verification Comparable Sales Credit Inquiries Delinquent Child Support Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses

4506-T/1040s Requirements Asset Verification Comparable Sales Credit Inquiries Delinquent Child Support Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses

TCF HELOCs. Combined 1 CLTV

TCF HELOCs MiMutual works directly with TCF to be able to offer simultaneous secondary financing in the form of a HELOC. These are not permitted to be submitted through the correspondent channel they must

TCF HELOCs MiMutual works directly with TCF to be able to offer simultaneous secondary financing in the form of a HELOC. These are not permitted to be submitted through the correspondent channel they must

Product Matrix Carrington Flexible Advantage Program

Program Maximum LTVs Primary Residence and Second Homes A B C Program Requirements Loan Amount Reserves FICO Purchase & R/T Cash Out Purchase & R/T Cash Out Purchase & R/T Cash Out Minimum Loan Amount

Program Maximum LTVs Primary Residence and Second Homes A B C Program Requirements Loan Amount Reserves FICO Purchase & R/T Cash Out Purchase & R/T Cash Out Purchase & R/T Cash Out Minimum Loan Amount

(TC) TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE

TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE") AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

Product Guidelines Freddie Mac Relief Refinance - Open Access

; Important Note: The program has been extended to allow application received dates on or before December 31, 2018 and settlement dates on or before September 30, 2019. Occupancy 1-4 Units 1-4 Units Max

; Important Note: The program has been extended to allow application received dates on or before December 31, 2018 and settlement dates on or before September 30, 2019. Occupancy 1-4 Units 1-4 Units Max

CONFORMING FIXED FNMA HOMESTYLE RENOVATION GUIDELINES

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

Program Restrictions Debt Consolidation Refinance DTI Residency Housing 0x30x12 Applies to Primary Residences only

Icon Elite Maximum LTVs Standard Doc Alt Doc Other Doc Restrictions Second Homes Reserve Requirements FICO Loan Amount Purchase & R/T Cash Out Purchase & R/T Cash Out Max LTV/CLTV: 85% Loan Amounts

Icon Elite Maximum LTVs Standard Doc Alt Doc Other Doc Restrictions Second Homes Reserve Requirements FICO Loan Amount Purchase & R/T Cash Out Purchase & R/T Cash Out Max LTV/CLTV: 85% Loan Amounts

EZ ELITE (EZE series) FIXED & ARM P&L PROGRAM

FIXED & ARM P&L PROGRAM") EZ ELITE (EZE series) FIXED & ARM P&L PROGRAM Primary Residence, Second Home & Investment Properties Purpose Property Type Max Loan Amount Max LTV Max CLTV Min FICO Purchase & Rate/Term Refinance Cash

EZ ELITE (EZE series) FIXED & ARM P&L PROGRAM Primary Residence, Second Home & Investment Properties Purpose Property Type Max Loan Amount Max LTV Max CLTV Min FICO Purchase & Rate/Term Refinance Cash

THE LSMG JUMBO PRODUCT

THE LSMG JUMBO PRODUCT Primary Residence: Purchase Property Type 2-unit Max LTV/CLTV/ Max Loan Min Loan Amount 2 Amount 3 Min FICO Score 4 Max 85% 6 $1,000,000 760 36% / 43% 80% $1,500,000 720 40% / 43%

THE LSMG JUMBO PRODUCT Primary Residence: Purchase Property Type 2-unit Max LTV/CLTV/ Max Loan Min Loan Amount 2 Amount 3 Min FICO Score 4 Max 85% 6 $1,000,000 760 36% / 43% 80% $1,500,000 720 40% / 43%

Jumbo Select Underwriting Guidelines

Jumbo Select Underwriting Guidelines Jumbo Select Underwriting Guidelines Table of Contents Table of Contents Eligibility Requirements 5 Available Products 5 Qualifying Rate 5 Eligible Property Types 5

Jumbo Select Underwriting Guidelines Jumbo Select Underwriting Guidelines Table of Contents Table of Contents Eligibility Requirements 5 Available Products 5 Qualifying Rate 5 Eligible Property Types 5

WHOLESALE Non-Agency Jumbo Fixed and ARM Fixed: T Year fixed rate, T Year fixed rate ARM: A500-5/1 ARM. A522-7/1 ARM and A527-10/1 ARM

Transaction Type Units Min-Maximum Loan Amt. Non-Agency Fixed and ARM Jumbo Matrix 1 WHOLESALE BUSINESS CHANNEL ONLY Maximum Min. LTV 3 FICO Min.# Mos. Verified PITIA Maximum DTI Maximum Cash Out 4 1 Primary

Transaction Type Units Min-Maximum Loan Amt. Non-Agency Fixed and ARM Jumbo Matrix 1 WHOLESALE BUSINESS CHANNEL ONLY Maximum Min. LTV 3 FICO Min.# Mos. Verified PITIA Maximum DTI Maximum Cash Out 4 1 Primary

Premium Jumbo 7/1 & 5/1 ARM

Premium Jumbo 7/1 & 5/1 ARM Program Codes: PJ 7/1 & PJ 5/1 ARM Purchase and Rate/Term Refinance Primary (Purchase) Primary (Rate/Term Ref.) Max Loan Amt Max LTV/CLTV Min Fico DTI Reserves Max Loan Amt

Premium Jumbo 7/1 & 5/1 ARM Program Codes: PJ 7/1 & PJ 5/1 ARM Purchase and Rate/Term Refinance Primary (Purchase) Primary (Rate/Term Ref.) Max Loan Amt Max LTV/CLTV Min Fico DTI Reserves Max Loan Amt

ULTRA JUMBO (DU) - UJDU series FULL DOC PROGRAM

- UJDU series FULL DOC PROGRAM") ULTRA JUMBO (DU) - UJDU series The Ultra Jumbo DU option utilizes Fannie Mae Desktop Underwriter (DU) over its manual underwriting counterpart. The loan is underwritten to the more restrictive of the Ultra

ULTRA JUMBO (DU) - UJDU series The Ultra Jumbo DU option utilizes Fannie Mae Desktop Underwriter (DU) over its manual underwriting counterpart. The loan is underwritten to the more restrictive of the Ultra

CONFORMING FIXED FNMA HOMESTYLE RENOVATION GUIDELINES

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

SPECIALTY LENDING MATRICES. CONTACT INFORMATION:

SPECIALTY LENDING MATRICES CONTACT INFORMATION: Pricing: Loan Registration: Guideline Support: Wholesale Support Desk: lockdesk@greenboxloans.com register@greenboxloans.com scenario@greenboxloans.com wholesalesupport@greenboxloans.com

SPECIALTY LENDING MATRICES CONTACT INFORMATION: Pricing: Loan Registration: Guideline Support: Wholesale Support Desk: lockdesk@greenboxloans.com register@greenboxloans.com scenario@greenboxloans.com wholesalesupport@greenboxloans.com

Conventional Loan Program - Quick Reference Guide

Loan Program - Quick Reference Guide Eligible Products LTV/(H)CLTV Matrices and Freddie Only Products 5/1 and 7/1 ARMS, 15 and 30 year Fully Amortizing Fixed Rate Fannie Only Products 5/1 and 7/1 ARMS,

Loan Program - Quick Reference Guide Eligible Products LTV/(H)CLTV Matrices and Freddie Only Products 5/1 and 7/1 ARMS, 15 and 30 year Fully Amortizing Fixed Rate Fannie Only Products 5/1 and 7/1 ARMS,

CONFORMING LIBOR ARMS PROGRAM HIGHLIGHTS

Program Summary Loan Term & Program Category A 30 year conforming conventional LIBOR ARM that is fixed for the initial 3, 5, or 7 years then rolls into a one year ARM for the remainder of the loan term.

Program Summary Loan Term & Program Category A 30 year conforming conventional LIBOR ARM that is fixed for the initial 3, 5, or 7 years then rolls into a one year ARM for the remainder of the loan term.

10, 15, 20, 25 & 30 YR Fixed Rates

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

CONFORMING UNDERWRTING GUIDELINES DUREFIPLUS PROGRAM - WHOLESALE

Table of Contents APPRAISAL & PROPERTY INFORMATION.... 2 Appraisal Requirements... 2 LTVs > 95%..... 3 Property Inspection Waiver (Property Field work Waiver Requirements).... 3 ELIGIBLE PROPERTIES...

Table of Contents APPRAISAL & PROPERTY INFORMATION.... 2 Appraisal Requirements... 2 LTVs > 95%..... 3 Property Inspection Waiver (Property Field work Waiver Requirements).... 3 ELIGIBLE PROPERTIES...

PMI (4764) pmi-us.com

pmi-us.com") 800.966.4PMI (4764) AnswerCenter@pmigroup.com pmi-us.com NON-DISTRESSED PMI MARKETS ELIGIBILITY MATRIX FULL DOC STANDARD JUMBO LOANS* Owner-Occupied Purchase Only Owner-Occupied Purchase or Rate/ Term

800.966.4PMI (4764) AnswerCenter@pmigroup.com pmi-us.com NON-DISTRESSED PMI MARKETS ELIGIBILITY MATRIX FULL DOC STANDARD JUMBO LOANS* Owner-Occupied Purchase Only Owner-Occupied Purchase or Rate/ Term

SIERRA CLASSIC JUMBO Fixed and ARM Matrix ( 1)(10)(11) RETAIL BUSINESS CHANNEL ONLY

(10)(11) RETAIL BUSINESS CHANNEL ONLY") SIERRA CLASSIC JUMBO Fixed and ARM Matrix ( 1)(10)(11) RETAIL BUSINESS CHANNEL ONLY Loan Purpose Property Type Owner Occupied Properties Minimum Credit Score (1) LTV/CLTV (2)(3)(8) Maximum Loan Amount

SIERRA CLASSIC JUMBO Fixed and ARM Matrix ( 1)(10)(11) RETAIL BUSINESS CHANNEL ONLY Loan Purpose Property Type Owner Occupied Properties Minimum Credit Score (1) LTV/CLTV (2)(3)(8) Maximum Loan Amount

FREDDIE MAC PRODUCT PROFILE

This product may only be used when one of the following exists: A Non-occupying co-borrower is on the loan and blended ratios are being used. The occupying borrower must have the ability to at least make

This product may only be used when one of the following exists: A Non-occupying co-borrower is on the loan and blended ratios are being used. The occupying borrower must have the ability to at least make

SUPER JUMBO ADVANTAGE 500 SERIES

SUPER JUMBO ADVANTAGE 500 SERIES Product Description Programs Non-Arms Length Transaction 500 Series Super Jumbo Advantage Retail Only 15 yr fixed 30 yr fixed 5/1 ARM 7/1 ARM 10/1 ARM ARM (if applicable)

SUPER JUMBO ADVANTAGE 500 SERIES Product Description Programs Non-Arms Length Transaction 500 Series Super Jumbo Advantage Retail Only 15 yr fixed 30 yr fixed 5/1 ARM 7/1 ARM 10/1 ARM ARM (if applicable)

ULTRA JUMBO (DU) - UJDU series FULL DOC PROGRAM

- UJDU series FULL DOC PROGRAM") ULTRA JUMBO (DU) - UJDU series The Ultra Jumbo DU option utilizes Fannie Mae Desktop Underwriter (DU) over its manual underwriting counterpart. The loan is underwritten to the more restrictive of the Ultra

ULTRA JUMBO (DU) - UJDU series The Ultra Jumbo DU option utilizes Fannie Mae Desktop Underwriter (DU) over its manual underwriting counterpart. The loan is underwritten to the more restrictive of the Ultra

JUMBO PRODUCT MATRIX

JUMBO PRODUCT MATRIX PRODUCT DESCRIPTION Non Conforming Fixed Rate OR; Non Convertible ARMs 5/1, 7/1 and 10/1 LIBOR ARM with a 2.25% Margin and 5/2/5 Caps No prepayment penalty Escrow waivers allowed for

JUMBO PRODUCT MATRIX PRODUCT DESCRIPTION Non Conforming Fixed Rate OR; Non Convertible ARMs 5/1, 7/1 and 10/1 LIBOR ARM with a 2.25% Margin and 5/2/5 Caps No prepayment penalty Escrow waivers allowed for

PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE. Reserves

Click Here For PDF Version Full/Alternative Documentation 1-2 Unit 1 Unit 3-4 Unit PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Maximum Qualifying Ratios Required MI Minimum LTV CLTV Loan Amount

Click Here For PDF Version Full/Alternative Documentation 1-2 Unit 1 Unit 3-4 Unit PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Maximum Qualifying Ratios Required MI Minimum LTV CLTV Loan Amount

Portfolio Wholesale Fees. Lender Paid Comp. calculate by dividing 4000 by the loan amount and multiplying. LTV Eligibility Matrix

Axos Bank Wholesale Borrower Paid SFR Ratesheet Lock Desk Wholesale Sales Inquiries Monday, October 22, 2018 Lock Requests: PORTFOLIO ARM - BORROWER PAID 5/1 LIBOR ARM 6/2/6 (JP51, JP51IO) 7/1 LIBOR ARM

Axos Bank Wholesale Borrower Paid SFR Ratesheet Lock Desk Wholesale Sales Inquiries Monday, October 22, 2018 Lock Requests: PORTFOLIO ARM - BORROWER PAID 5/1 LIBOR ARM 6/2/6 (JP51, JP51IO) 7/1 LIBOR ARM

PROGRAM CODES:HP10, HP15, HP20, HP30, HPJ30

HomePath Mortgage HomePath Mortgage is available for purchase transactions of eligible FannieMae REO properties. It is a fixed rate product for loans from $50,000 to the conforming limit. All loans must

HomePath Mortgage HomePath Mortgage is available for purchase transactions of eligible FannieMae REO properties. It is a fixed rate product for loans from $50,000 to the conforming limit. All loans must

PRODUCT MATRICES. For Information on any of our products, please contact:

Correspondent Lending PRODUCT MATRICES March 2016 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing,

Correspondent Lending PRODUCT MATRICES March 2016 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing,

Elite Plus Jumbo Fixed and ARM Program Guidelines

Elite Plus Jumbo Fixed and ARM Program Guidelines Revised 6/12/2018 rev. 13 (Click the link to go straight to the section) 1 Program Summary 11 Underwriting Method 21 Max Financed Properties 2 Product

Elite Plus Jumbo Fixed and ARM Program Guidelines Revised 6/12/2018 rev. 13 (Click the link to go straight to the section) 1 Program Summary 11 Underwriting Method 21 Max Financed Properties 2 Product

Correspondent Lending Chase DU/LP Overlay Matrix

Agency Collateral Overlays 2070 & 2075 Appraisals CB12-18 The Fannie Mae Desktop Underwriter Property Inspection Report 2075 and Freddie Mac Loan Prospector Property Inspection Report 2070 do not contain

Agency Collateral Overlays 2070 & 2075 Appraisals CB12-18 The Fannie Mae Desktop Underwriter Property Inspection Report 2075 and Freddie Mac Loan Prospector Property Inspection Report 2070 do not contain

Guideline Reference Applies to ALL Products

Guideline Reference Applies to ALL Products 4506-T CG Ch 5E Loan Documents & Notes CG Ch 6F Employment & Documentation CG Ch 7G FHA Employment & Evaluation & Documentation Product summaries IRS Form 4506T

Guideline Reference Applies to ALL Products 4506-T CG Ch 5E Loan Documents & Notes CG Ch 6F Employment & Documentation CG Ch 7G FHA Employment & Evaluation & Documentation Product summaries IRS Form 4506T

DU Refi Plus. Eligibility Matrix Loan Amount & LTV Limitations

This matrix is intended as an aid to assist in determining if a property/loan qualifies for the DU Refi Plus program. It is not intended as a replacement for the full DU Refi Plus guidelines. Users are

This matrix is intended as an aid to assist in determining if a property/loan qualifies for the DU Refi Plus program. It is not intended as a replacement for the full DU Refi Plus guidelines. Users are