AN INVESTMENT IN THE NOTES INVOLVES A HIGH DEGREE OF RISK. YOU SHOULD CAREFULLY CONSIDER THE RISK FACTORS BEGINNING ON PAGE 14 BEFORE INVESTING.

|

|

|

- David Wiggins

- 5 years ago

- Views:

Transcription

1 U.S.$ 2,500,000,000 Programme for the Issuance of Loan Participation Notes to be issued by, but with limited recourse to, Russian Standard Finance S.A. for the sole purpose of financing loans to Joint Stock Company "Russian Standard Bank" Under the Programme for the Issuance of Loan Participation Notes (the "Programme") described in this base prospectus (the "Base Prospectus"), Russian Standard Finance S.A., a public limited liability company (société anonyme) established under the laws of the Grand Duchy of Luxembourg whose registered office is at 2, Boulevard Konrad Adenauer, L-1115 Luxembourg, registered with the Register of Commerce and Companies of Luxembourg under number B (the "Issuer"), subject to compliance with all relevant laws, regulations and directives, may from time to time issue loan participation notes (the "Notes") on the terms and conditions set out herein, as such terms and conditions are supplemented by a final terms (each a "Final Terms") for each issue or in a separate prospectus specific to such issue (the "Drawdown Prospectus") as described under "Supplemental Base Prospectus and Drawdown Prospectus" below. In the case of Notes which are the subject of a Drawdown Prospectus, each reference in this Base Prospectus to information being specified or identified in the relevant Final Terms shall be read and construed as a reference to such information being specified or identified in the relevant Drawdown Prospectus unless the context requires otherwise. The aggregate principal amount of Notes outstanding under the Programme will not at any time exceed U.S.$ 2,500,000,000 (or the equivalent in other currencies). This Base Prospectus supersedes any previous Base Prospectus relating to the Programme and any supplements thereto. Any Notes issued under the Programme on or after the date of this Base Prospectus shall be issued pursuant to this Base Prospectus. This Base Prospectus does not affect any Notes issued under the Programme prior to the date hereof. Notes will be issued in Series (as defined in "Overview of the Programme") and the sole purpose of issuing each Series will be to finance either a senior loan (a "Senior Loan") or a subordinated loan (a "Subordinated Loan" and, together with a Senior Loan, the "Loans" and each a "Loan") to Joint Stock Company "Russian Standard Bank" ("RSB" or the "Borrower") as borrower, on the terms of either: (i) in relation to a Senior Loan, an amended and restated facility agreement between the Issuer and RSB dated 26 September 2012 (the "Facility Agreement"), as amended and supplemented by a loan supplement to be entered into in respect of each Loan on or before each issue date ("Issue Date") of the relevant Series (each a "Loan Supplement" and, together with the Facility Agreement, the "Senior Loan Agreement" which expression shall include any other or further loan agreement entered into between the Issuer and RSB in connection with the issue of any Series under the Programme and set out in a supplement to this Base Prospectus or in a Drawdown Prospectus) or (ii) in relation to a Subordinated Loan, a subordinated loan agreement between the Issuer and RSB, to be entered into on or before the Issue Date of the relevant Series (the "Subordinated Loan Agreement"). In this Base Prospectus, "Loan Agreement" shall mean either (i) a Senior Loan Agreement (in respect of a Senior Loan) or (ii) a Subordinated Loan Agreement (in respect of a Subordinated Loan), as applicable. The relevant Final Terms in respect of the issue of any Series of Notes will specify whether a Loan being financed by such Series of Notes is a Senior Loan (such Series of Notes being a "Senior Series") or a Subordinated Loan (such Series of Notes being a "Subordinated Series"). Subject as provided in an amended and restated principal trust deed dated 26 September 2012, as supplemented by a supplemental trust deed in respect of each Series of Notes ("Trust Deed"), the Issuer will charge, in favour of Deutsche Trustee Company Limited (the "Trustee") as trustee, by way of a first fixed charge as security for its payment obligations in respect of each Series of Notes and under the Trust Deed, certain of its rights and interests under the relevant Loan Agreement and the relevant Account (as defined in "Description of the Transaction"). In addition, the Issuer will assign certain of its administrative rights under the relevant Loan Agreement to the Trustee. In each case where amounts of principal, interest and additional amounts (if any) are stated to be payable in respect of a Series of Notes, the obligation of the Issuer to make any such payment shall constitute an obligation only to account to the noteholders of such Series of Notes (the "Noteholders"), on each date upon which such amounts of principal, interest and additional amounts (if any) are due in respect of such Series of Notes, for an amount equivalent to all principal, interest and additional amounts (if any) actually received from RSB by or for the account of the Issuer pursuant to the relevant Loan Agreement excluding, however, any amounts paid in respect of Reserved Rights (as defined in the "Terms and Conditions of the Notes"). The Issuer will have no other financial obligation under the Notes. Noteholders will be deemed to have accepted and agreed that they will be relying solely and exclusively on the credit and financial standing of RSB in respect of the payment obligations of the Issuer under the Notes. Other than as described in this Base Prospectus and the Trust Deed, the Noteholders have no proprietary or other direct interest in the Issuer's rights under or in respect of the relevant Loan Agreement or the relevant Loan. Subject to the terms of the Trust Deed, no Noteholder will have any rights to enforce any of the provisions in the relevant Loan Agreement or have direct recourse to RSB except through action by the Trustee. AN INVESTMENT IN THE NOTES INVOLVES A HIGH DEGREE OF RISK. YOU SHOULD CAREFULLY CONSIDER THE RISK FACTORS BEGINNING ON PAGE 14 BEFORE INVESTING. THE NOTES AND LOANS (TOGETHER, THE "SECURITIES") HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933 (THE "SECURITIES ACT"), AND, SUBJECT TO CERTAIN EXCEPTIONS, MAY NOT BE OFFERED OR SOLD WITHIN THE UNITED STATES OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS (AS DEFINED IN REGULATION S UNDER THE SECURITIES ACT ("REGULATION S")). THE NOTES OF EACH SERIES MAY BE OFFERED AND SOLD (I) WITHIN THE UNITED STATES TO QUALIFIED INSTITUTIONAL BUYERS ("QIBs"), AS DEFINED IN RULE 144A UNDER THE SECURITIES ACT ("RULE 144A"), THAT ARE ALSO QUALIFIED PURCHASERS ("QPs"), AS DEFINED IN SECTION 2(A)(51) OF THE U.S. INVESTMENT COMPANY ACT OF 1940 (THE "INVESTMENT COMPANY ACT") IN RELIANCE ON THE EXEMPTION FROM REGISTRATION PROVIDED BY RULE 144A (THE "RULE 144A NOTES") AND (II) TO NON-U.S. PERSONS IN OFFSHORE TRANSACTIONS IN RELIANCE ON - 1 -

2 REGULATION S (THE "REGULATION S NOTES"). THE ISSUER HAS NOT BEEN AND WILL NOT BE REGISTERED UNDER THE INVESTMENT COMPANY ACT. PROSPECTIVE PURCHASERS ARE HEREBY NOTIFIED THAT SELLERS OF THE NOTES MAY BE RELYING ON THE EXEMPTION FROM THE PROVISIONS OF SECTION 5 OF THE SECURITIES ACT PROVIDED BY RULE 144A. FOR A DESCRIPTION OF THESE AND CERTAIN FURTHER RESTRICTIONS, SEE "SUBSCRIPTION AND SALE" AND "TRANSFER RESTRICTIONS". The Base Prospectus has been approved by the Central Bank of Ireland, as competent authority under Directive 2003/71/EC (as amended, inter alia, by Directive 2010/73/EU) (the "Prospectus Directive"). The Central Bank of Ireland only approves this Base Prospectus as meeting the requirements imposed under Irish and EU law pursuant to the Prospectus Directive. Application will be made to the Irish Stock Exchange (the "Irish Stock Exchange") for Notes issued under the Programme within 12 months of the Base Prospectus to be admitted to the Official List (the "Official List") and trading on its regulated market (the "Main Securities Market"). The Main Securities Market is a regulated market for the purposes of Directive 2004/39/EC. Such approval relates only to the Notes which are to be admitted to trading on the regulated market of the Irish Stock Exchange or other regulated markets for the purposes of Directive 2004/39/EC or which are to be offered to the public in any Member State of the European Economic Area. The Central Bank of Ireland has been requested by the Issuer to provide the United Kingdom Financial Services Authority with a certificate of approval attesting that the Base Prospectus has been drawn up in accordance with the Prospectus Directive so that the Notes issued under the Programme may be listed on the regulated market of the London Stock Exchange. Application may be made for Notes issued under the Programme to be admitted to trading on the regulated market of the London Stock Exchange. Unlisted Notes may also be issued pursuant to the Programme. The relevant Final Terms in respect of the issue of any Notes will specify whether or not such Notes will be listed on the Irish Stock Exchange (or any other stock exchange) and admitted to trading on the Main Securities Market (or any other market). Reference in this Base Prospectus to Notes being "listed" (and all related references) shall mean that such Notes have been admitted to trading on the regulated market of the Irish Stock Exchange. Regulation S Notes of each Series will initially be represented by interests in a permanent global note in fully registered form (each a "Regulation S Global Note") without interest coupons, which will be deposited with a common depositary for, and registered in the name of a nominee of, Euroclear Bank SA/NV ("Euroclear") and Clearstream Banking, société anonyme ("Clearstream, Luxembourg"), on its Issue Date. Beneficial interests in a Regulation S Global Note will be shown on, and transfers thereof will be effected only through records maintained by, Euroclear or Clearstream, Luxembourg and their respective participants. Rule 144A Notes of each Series will initially be represented by interests in a permanent global note in fully registered form (each a "Rule 144A Global Note" and, together with any Regulation S Global Note for the relevant Series of Notes, the "Global Notes") without interest coupons, which will be deposited with a custodian for, and registered in the name of a nominee of, The Depository Trust Company ("DTC") on its Issue Date. Beneficial interests in a Rule 144A Global Note will be shown on, and transfers thereof will be effected only through records maintained by, DTC and its participants. See "Summary of the Provisions Relating to the Notes in Global Form". Individual definitive Notes in registered form will only be available in certain limited circumstances as described herein. The Notes will be in denominations in aggregate principal amount, for Rule 144A Notes, of at least U.S.$200,000 (or the equivalent in other currencies) and integral multiples of U.S.$1,000 (or the equivalent in other currencies) in excess thereof, and for Regulation S Notes, of at least EUR100,000 (or the equivalent in other currencies) and integral multiples of EUR1,000 (or the equivalent in other currencies) in excess thereof, save that unless otherwise permitted by then current laws and regulations, Notes which have a maturity of less than one year and in respect of which the issue proceeds are to be accepted by the Issuer in the United Kingdom or whose issue otherwise would constitute a contravention of section 19 of the Financial Services and Markets Act 2000 (the "FSMA") will have a minimum denomination of GBP100,000 (or its equivalent in other currencies). Arrangers and Permanent Dealers Citigroup Goldman Sachs International J.P. Morgan UBS Investment Bank VTB Capital The date of this Base Prospectus is 26 September

3 This Base Prospectus (including the financial statements attached thereto) comprises a base prospectus for the purposes of Article 5.4 of Directive 2003/71/EC (the "Prospectus Directive") and for the purpose of giving information with respect to RSB and its consolidated subsidiaries taken as a whole (the "Group"), the Issuer, the Loan Agreements and the Notes. In addition, RSB, having made all reasonable enquiries, confirms that (i) this Base Prospectus contains all information with respect to RSB, the Group, the Issuer, the Loan Agreements and the Notes that is material in the context of the issue and offering of the Notes; (ii) the statements contained in the Base Prospectus are in every respect true and accurate and not misleading; (iii) the opinions, expectations and intentions expressed in this Base Prospectus are honestly held, have been reached after considering all relevant circumstances and are based on reasonable assumptions; (iv) there are no other facts with respect to RSB, the Group, the Issuer, the Loan Agreements or the Notes the omission of which would, in the context of the issue and offering of the Notes, make any statement in this Base Prospectus misleading in any respect; and (v) all reasonable enquiries have been made by RSB to ascertain such facts and to verify the accuracy of all such information and statements. RSB accepts responsibility accordingly. Each of RSB and the Issuer accepts responsibility for all information in this Base Prospectus. To the best of the knowledge and belief of RSB and the Issuer (which have taken all reasonable care to ensure that such is the case), the information contained in this Base Prospectus is in accordance with the facts and does not omit anything likely to affect the import of such information. This Base Prospectus has been filed with and approved by the Central Bank of Ireland as required by the Prospectus (Directive 2003/71/EC) Regulations 2005 (the "Prospectus Regulations"). The credit ratings in this Base Prospectus have been issued by Fitch Ratings CIS Limited ("Fitch"), Moody's Investors Service Limited ("Moody's") and Standard & Poor's Credit Market Services Europe Limited ("Standard & Poor's") (together, the "Rating Agencies"). As of the date of this Base Prospectus, Fitch, Moody's and Standard & Poor's are established in the European Union and registered under Regulation (EU) No 1060/2009, as amended (the "CRA Regulation"). Series of Notes issued under the Programme may be rated or unrated. Where a Series of Notes is rated, such rating will not necessarily be the same as the rating described above or the rating(s) assigned to Notes already issued. Where a Series of Notes is rated, the applicable rating(s) will be specified in the relevant Final Terms. Whether or not each credit rating applied for in relation to a relevant Series of Notes will be (1) issued by a credit rating agency established in the European Union and registered (or which has applied for registration and not been refused) under the CRA Regulation, or (2) issued by a credit rating agency which is not established in the European Union but will be endorsed by a credit rating agency which is established in the European Union and registered under the CRA Regulation or (3) issued by a credit rating agency which is not established in the European Union but which is certified under the CRA Regulation will be disclosed in the Final Terms. NO REPRESENTATION OR WARRANTY, EXPRESS OR IMPLIED, IS MADE BY CITIGROUP GLOBAL MARKETS LIMITED, GOLDMAN SACHS INTERNATIONAL, J.P. MORGAN SECURITIES PLC, UBS LIMITED OR VTB CAPITAL PLC (THE "ARRANGERS"), ANY DEALER (AS DEFINED HEREIN), THE TRUSTEE OR ANY OF THEIR RESPECTIVE AFFILIATES OR ANY PERSON ACTING ON THEIR BEHALF AS TO THE ACCURACY OR COMPLETENESS OF THE INFORMATION CONTAINED IN THIS BASE PROSPECTUS. NOTHING CONTAINED IN THIS BASE PROSPECTUS IS, OR SHALL BE RELIED UPON AS, A PROMISE OR REPRESENTATION, WHETHER AS TO THE PAST OR THE FUTURE. EACH PERSON CONTEMPLATING MAKING AN INVESTMENT IN THE NOTES MUST MAKE ITS OWN INVESTIGATION AND ANALYSIS OF THE CREDITWORTHINESS OF RSB AND THE ISSUER AND ITS OWN DETERMINATION OF THE SUITABILITY OF ANY SUCH INVESTMENT, WITH PARTICULAR REFERENCE TO ITS OWN INVESTMENT OBJECTIVES AND EXPERIENCE, AND ANY OTHER FACTORS WHICH MAY BE RELEVANT TO IT IN CONNECTION WITH SUCH INVESTMENT

4 Certain information and data (which may include estimates and approximations) contained in the sections titled "Business" and "Overview of the Banking Sector and Banking Regulation in Russia" of this Base Prospectus were derived from publicly available information, including press releases and filings under various regulatory and securities laws. In particular, certain information and data contained in this Base Prospectus were derived from the web sites of RosBusinessConsulting, European Card Acquiring Forum and the Agency for Deposit Insurance (the "Deposit Insurance Agency"). Each of RSB and the Issuer accepts responsibility that such publicly available information and data have been accurately reproduced and, as far as RSB and the Issuer are aware and are able to ascertain from information published by such third parties, no facts have been omitted which would render such information inaccurate or misleading. However, RSB and the Issuer have relied on the accuracy of such publicly available information and data without carrying out an independent verification. Certain information and data (which may include estimates and approximations) contained in the sections titled "Presentation of the Financial Information", "Risk Factors", "Management's Discussion and Analysis of Financial Condition and Results of Operations" and "Overview of the Banking Sector and Banking Regulation in Russia" of this Base Prospectus were derived from official data published by Russian government agencies. In particular, certain information and data contained in this Base Prospectus were derived from the web sites of the Central Bank of Russia ("CBR"), the Ministry for Economic Development of Russia and the Federal State Statistics Service of Russia. Each of RSB and the Issuer accepts responsibility that such official data have been accurately reproduced and, as far as RSB and the Issuer are aware and able to ascertain from information published by such Russian government agencies, no facts have been omitted which would render such information inaccurate or misleading. However, the official data published by Russian federal, regional and local governments is substantially less complete or researched than data published by governmental agencies of Western countries. Official statistics may also be compiled on different bases than those used in Western countries. Any discussion of matters relating to Russia in this Base Prospectus may, therefore, be subject to uncertainty due to concerns about the completeness or reliability of available official and public information. The veracity of some official data released by the Russian government may be questionable. See "Risk Factors- Risks Related to Russia Neither the Issuer nor RSB has independently verified official data from Russian government agencies, nor have they independently verified information regarding the banking sector". The language of this Base Prospectus is English. Certain technical terms and legislative references have been cited in their original language so that the correct technical meaning may be ascribed to them. This Base Prospectus does not constitute an offer of, or an invitation by or on behalf of the Issuer, RSB, the Arrangers or the Dealers to subscribe for or purchase any Series of Notes. The distribution of this Base Prospectus and the offering of the Notes in certain jurisdictions may be restricted by law. Persons into whose possession this Base Prospectus comes are required by the Issuer, RSB, the Arrangers and the Dealers to inform themselves about and to observe any such restrictions. In particular, the Notes have not been and will not be registered under the Securities Act. Subject to certain exceptions, the Notes may not be offered or sold in the United States or to, or for the account or benefit of, U.S. persons. For a description of certain further restrictions on offers and sales of the Notes and distribution of this Base Prospectus, see "Subscription and Sale". Neither the Issuer nor RSB intends to provide any post-issuance transaction information regarding the Notes or the performance of any Loan. No person is authorised to provide any information or to make any representation not contained in this Base Prospectus, and any information or representation not so contained must not be relied upon as having been authorised by or on behalf of the Issuer, RSB, the Trustee, the Arrangers or the Dealers. The delivery of this document at any time does not imply that the information contained in it is correct as at any time subsequent to its date. Without limitation to the generality of the foregoing, the contents of RSB's website or any other website referred to in this Base Prospectus as at the date hereof or as at any other date do not form any part of this Base Prospectus (and, in particular, are not incorporated by reference herein). IN CONNECTION WITH THE ISSUE OF ANY SERIES OF NOTES, THE DEALER OR - 4 -

5 DEALERS (IF ANY) NAMED AS THE STABILISING MANAGER(S) (OR PERSONS ACTING ON BEHALF OF ANY STABILISING MANAGER(S)) IN THE APPLICABLE FINAL TERMS MAY OVER-ALLOT NOTES OR EFFECT TRANSACTIONS WITH A VIEW TO SUPPORTING THE MARKET PRICE OF THE NOTES AT A LEVEL HIGHER THAN THAT WHICH MIGHT OTHERWISE PREVAIL. HOWEVER, THERE IS NO ASSURANCE THAT THE STABILISING MANAGER(S) (OR PERSONS ACTING ON BEHALF OF A STABILISING MANAGER) WILL UNDERTAKE STABILISATION ACTION. ANY STABILISATION ACTION MAY BEGIN ON OR AFTER THE DATE ON WHICH ADEQUATE PUBLIC DISCLOSURE OF THE FINAL TERMS OF THE OFFER OF THE RELEVANT SERIES OF NOTES AND, IF BEGUN, MAY BE ENDED AT ANY TIME, BUT IT MUST END NO LATER THAN THE EARLIER OF 30 DAYS AFTER THE ISSUE DATE OF THE RELEVANT SERIES OF NOTES AND 60 DAYS AFTER THE DATE OF THE ALLOTMENT OF THE RELEVANT SERIES OF NOTES. ANY STABILISATION ACTION OR OVERALLOTMENT MUST BE CONDUCTED BY THE STABILISING MANAGER(S) (OR PERSONS ACTING ON BEHALF OF A STABILISING MANAGER) IN ACCORDANCE WITH ALL APPLICABLE LAWS AND RULES

6 FORWARD-LOOKING STATEMENTS Some statements in this Base Prospectus, as well as written and oral statements that RSB and its officers make from time to time in reports, filings, news releases, conferences, teleconferences, web postings or otherwise, may be deemed to be "forward-looking statements". Forward-looking statements include statements concerning RSB's plans, objectives, goals, strategies and future operations and performance and the assumptions underlying these forward-looking statements. RSB uses the words "anticipates", "estimates", "expects", "believes", "intends", "plans", "may", "will", "should" and other similar expressions to identify forward-looking statements. These forward-looking statements are contained in "Risk Factors", "Management's Discussion and Analysis of Financial Condition and Results of Operations", "Business" and other sections of this Base Prospectus. RSB has based these forward-looking statements on the current views of its management with respect to future events and financial performance. These views reflect the best judgment of the management of RSB but involve uncertainties and are subject to certain risks, the occurrence of which could cause actual results to differ materially from those RSB predicts in its forward-looking statements and from its past results, performance or achievements. Although RSB believes that the estimates and the projections reflected in its forward-looking statements are reasonable, if one or more risks or uncertainties were to materialise or occur, including those which RSB has identified in this Base Prospectus, or if any underlying assumptions prove to be incomplete or inaccurate, its results of operations may vary from those it expected, estimated or projected. Forward-looking statements that may be made by RSB from time to time (but that are not included in this document) may also include projections or expectations of interest income, net interest income, operating income (or loss), net profit (or loss) (including on a per share basis), dividends, capital structure or other financial items or ratios. By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that the predictions, forecasts, projections and other forward-looking statements will not be achieved. You should be aware that a number of important factors could cause actual results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such forward-looking statements. These factors include: the health of the global and Russian economies, including the Russian banking sector; inflation, interest rate fluctuations and exchange rate fluctuations in Russia; the ability of RSB to refinance its indebtedness on reasonable terms or at all; RSB's ability to maintain its collection rate on overdue loans; prices for securities issued by Russian entities; RSB's ability to maintain its liquidity levels; the effects of, and changes in, the policy of the federal government of Russia (the "Russian Government") and regulations promulgated by the CBR; the effects of competition in the geographic and business areas in which RSB conducts its operations; the effects of changes in laws, regulations and taxation or accounting standards or practices in the jurisdictions where RSB conducts its operations; RSB's ability to maintain or increase market share for its products and services and control expenses; - 6 -

7 acquisitions or divestitures; technological changes; and RSB's success at managing the risks associated with the aforementioned factors. This list of important factors is not exhaustive. When reviewing forward-looking statements, the investors should carefully consider the foregoing factors and other uncertainties and events, especially in light of the political, economic, social and legal environment in which RSB operates. Such forward-looking statements speak only as at the date on which they are made, and are not subject to any continuing obligations under the listing guidelines of the Irish Stock Exchange. Accordingly RSB is not obliged to, and does not intend to, update or revise any forward-looking statements made in this Base Prospectus whether as a result of new information, future events or otherwise. All subsequent written or oral forward-looking statements attributable to RSB, or persons acting on RSB's behalf, are expressly qualified in their entirety by the cautionary statements contained throughout this Base Prospectus. As a result of these risks, uncertainties and assumptions, a prospective purchaser of the Notes should not place reliance on these forward-looking statements

8 ENFORCEABILITY OF JUDGMENTS RSB is a joint stock company organised under the laws of Russia. The majority of RSB's directors and executive officers reside in Russia. Substantially all the assets of RSB are located in Russia. As far as RSB is aware, part of the assets of RSB's directors and executive officers are located in Russia. As a result, the Trustee, acting on behalf of the Noteholders, may not be able to effect service of process, or enforce any court judgement obtained, in the United Kingdom or the United States on or against RSB or any of RSB's directors or executive officers named in this Base Prospectus. However, RSB will appoint a process agent for the service of legal process in England and Wales. Subject to the terms of the Trust Deed, no Noteholder will have any entitlement to enforce any provisions of the relevant Loan Agreement, or have direct recourse to RSB, except through action by the Trustee. Neither the Issuer nor the Trustee will be required to enter into proceedings to enforce payment from RSB under the relevant Loan Agreement, unless it has been indemnified and/or secured by the Noteholders to its satisfaction against all liabilities, proceedings, claims and demands to which it may thereby become liable and all costs, charges and expenses, which it may incur in connection therewith. Similarly, it may not be possible to obtain or enforce English or United States court judgments in Russia against RSB or its directors or executive officers. Courts in Russia will only recognise judgments rendered by a court in any jurisdiction outside Russia if an international treaty providing for the recognition and enforcement of judgments in civil cases exists between Russia and the country where the judgment is rendered. No such treaty for the reciprocal enforcement of foreign court judgments in civil and commercial matters exists between Russia and most Western jurisdictions (including the United Kingdom, Luxembourg and the United States), which may require new proceedings to be brought in Russia in respect of a judgment already obtained in any such jurisdiction against RSB or its directors or executive officers. In addition, Russian courts have limited experience in the enforcement of foreign court judgments. The limitations described above, including the general procedural grounds set out in Russian legislation for the refusal to recognise and enforce foreign court judgments in Russia, may significantly delay the enforcement of any such judgment, or deprive the Noteholders or the Trustee of effective legal recourse for claims under the Notes relating to the relevant Loan. Each Loan Agreement will be governed by English law and will provide that if any dispute or proceeding arises from or in connection with such Loan Agreement, such dispute or proceedings will be settled by arbitration in accordance with the Rules of the LCIA (formerly the London Court of International Arbitration) (the "LCIA Rules"). The place of such arbitration shall be London, England. Russia and the United Kingdom are parties to the United Nations (New York) Convention on the Recognition and Enforcement of Foreign Arbitral Awards of 1958 (the "New York Convention"). Consequently, Russian courts should generally recognise and enforce in Russia an arbitral award from an arbitral tribunal in the United Kingdom, on the basis of the rules of the New York Convention (subject to qualifications provided for in the New York Convention and compliance with Russian procedural regulations and other procedures and requirements established by Russian legislation). The Arbitrazh Procedural Code of Russia dated 24 July 2002 (the "Arbitrazh Procedural Code") sets out the procedure for the recognition and enforcement of foreign arbitral awards by Russian courts. The Arbitrazh Procedural Code also contains an exhaustive list of grounds for the refusal of recognition and enforcement of foreign arbitral awards by Russian courts, which grounds are broadly similar to those provided by the New York Convention. The Arbitrazh Procedural Code and other Russian procedural legislation could change, and other grounds for Russian courts to refuse the recognition and enforcement of foreign courts' judgments and foreign arbitral awards could arise in the future. In practice, reliance upon international treaties may meet resistance or a lack of understanding on the part of a Russian court or other officials, thereby introducing delay and unpredictability into the process of enforcing any foreign judgment or any foreign arbitral award in Russia

9 Furthermore, any arbitral award pursuant to arbitration proceedings in accordance with the LCIA Rules and the application of English law to each Loan Agreement may be limited by the mandatory provisions of Russian laws relating to the exclusive jurisdiction of Russian courts and the application of Russian laws with respect to bankruptcy, winding up or liquidation of Russian companies and credit organisations in particular. Each Loan Agreement will provide for the Issuer to elect for disputes to be settled in the courts of England and Wales as an alternative to arbitration

10 PRESENTATION OF FINANCIAL AND OTHER INFORMATION Presentation of Financial Information The financial information of the Group set forth herein (i) as of and for the six months ended 30 June 2012 and 2011 has, unless otherwise indicated, been derived from the Group's unaudited interim condensed consolidated financial information as of and for the six months ended 30 June 2012 and the related notes thereto (the "Interim Financial Statements"), and (ii) as of and for the years ended 31 December 2011, 2010 and 2009 has, unless otherwise indicated, been derived from the Group's audited consolidated financial statements as of and for the years ended 31 December 2011 and 2010 and the related notes thereto (the "Annual Financial Statements" and, together with the Interim Financial Statements, the "Financial Statements"). The Annual Financial Statements have been prepared in accordance with International Financial Reporting Standards ("IFRS") as promulgated by the International Accounting Standards Board. The Interim Financial Statements have been prepared in accordance with International Accounting Standard 34 ("IAS 34") "Interim Financial Reporting". The Issuer's audited financial statements as of and for the years ended 31 December 2011, 2010 and 2009 have been prepared in accordance with generally accepted accounting principles in Luxembourg. The Issuer's audited financial statements as of and for the years ended 31 December 2011, 2010 and 2009 have been filed with the Central Bank of Ireland and are incorporated by reference herein. Currency In this Base Prospectus, the following currency terms are used: "EUR", "Euro" or " " means the currency introduced at the start of the third stage of European economic and monetary union and as defined in Article 2 of Council Regulation (EC) No. 974/98 of 3 May 1998 on the introduction of the euro, as amended; "GBP" means the lawful currency of the United Kingdom; "RUB", "Russian rouble", "Rouble" or "rouble" means the lawful currency of Russia; "UAH" means the lawful currency of the Ukraine; and "U.S. Dollar", "USD" or "US$" means the lawful currency of the United States. Exchange Rates The table below sets forth, for the periods indicated, certain information regarding the exchange rate between the Rouble and the U.S. Dollar, based on the official exchange rate quoted by the CBR. Fluctuations in the exchange rate between the Rouble and the U.S. Dollar in the past are not necessarily indicative of fluctuations that may occur in the future. The Group's Financial Statements are presented in Russian roubles, the Group's functional currency. Solely for the convenience of the reader, certain financial information has been translated into U.S. Dollars at the conversion rate quoted by the CBR as of the indicated date. RSB does not make any representation that the Rouble amounts referred to in this Base Prospectus could have been or could be converted into U.S. Dollars at the below exchange rates, at any other rate or at all. High Low Average (1) Period end (2) Rouble/U.S. Dollar Year ended 31 December

11 High Low Average (1) Period end (2) Rouble/U.S. Dollar Month ended January February March April May June July August September 2012 (3) (1) The average of the exchange rates on the last business day of each full month during the relevant period. (2) The period end rates are quoted for the last business day of the relevant period. (3) Data as of 25 September Source: CBR Rounding Some numerical figures included in this Base Prospectus have been subject to rounding adjustments. Accordingly, numerical figures shown as totals in certain tables may not be an arithmetic aggregation of the figures that preceded them. Market Share Information In this Base Prospectus, RSB and the Issuer refer to information regarding RSB's business and the market in which RSB operates. RSB and the Issuer obtained this information in part from various third party sources and in part from RSB's own internal estimates. RSB and the Issuer have obtained market and industry data relating to RSB's business from providers of industry and market data, primarily the CBR. Industry publications, surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable. Each of RSB and the Issuer has relied on the accuracy of the information from industry publications, surveys and forecasts without carrying out an independent verification thereof and cannot guarantee their accuracy or completeness. Each of RSB and the Issuer confirms that such third party information has been accurately reproduced and, as far as each of RSB and the Issuer is aware and is able to ascertain from information published by such third parties, no facts have been omitted from the information in this Base Prospectus that would render it inaccurate or misleading. In addition, RSB has made statements in this Base Prospectus regarding the Russian banking industry and its position in this industry based on RSB's own experience and investigation of market conditions. RSB cannot provide assurances that any of its assumptions regarding the banking industry are accurate or correctly reflect the position of other banks in the industry, and its statements have not been verified by any independent sources

12 ADDITIONAL INFORMATION Neither the Issuer nor RSB is required to file periodic reports under Section 13 or 15 of the U.S. Securities Exchange Act of 1934, as amended (the "Exchange Act"). For so long as either the Issuer or RSB is not a reporting company under Section 13 or 15(d) of the Exchange Act, or exempt from reporting pursuant to Rule 12g3-2(b) thereunder, the Issuer or RSB will, upon request, furnish to each holder or beneficial owner of Notes that are "restricted securities" (within the meaning of Rule 144(a)(3) under the Securities Act) and to each prospective purchaser thereof designated by such holder or beneficial owner upon request of such holder, beneficial owner or prospective purchaser, in connection with a transfer or proposed transfer of any such Notes pursuant to Rule 144A under the Securities Act or otherwise, the information required to be delivered pursuant to Rule 144A(d)(4) under the Securities Act

13 CONTENTS FORWARD-LOOKING STATEMENTS... 6 ENFORCEABILITY OF JUDGMENTS... 8 PRESENTATION OF FINANCIAL AND OTHER INFORMATION ADDITIONAL INFORMATION RISK FACTORS DOCUMENTS INCORPORATED BY REFERENCE SUPPLEMENTAL BASE PROSPECTUS AND DRAWDOWN PROSPECTUS OVERVIEW OF THE PROGRAMME DESCRIPTION OF THE TRANSACTIONS USE OF PROCEEDS CAPITALISATION SELECTED CONSOLIDATED FINANCIAL INFORMATION MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS BUSINESS ASSET, LIABILITY AND RISK MANAGEMENT MANAGEMENT SHAREHOLDING RELATED PARTY TRANSACTIONS THE ISSUER THE FACILITY AGREEMENT TERMS AND CONDITIONS OF THE NOTES FORM OF FINAL TERMS SUMMARY OF PROVISIONS RELATING TO THE NOTES IN GLOBAL FORM TAXATION CERTAIN ERISA CONSIDERATIONS SUBSCRIPTION AND SALE TRANSFER RESTRICTIONS GENERAL INFORMATION OVERVIEW OF THE BANKING SECTOR AND BANKING REGULATION IN RUSSIA INDEX TO FINANCIAL STATEMENTS

14 RISK FACTORS An investment in the Notes involves a high degree of risk. Prospective investors should consider carefully, among other things, the risks set forth below and the other information contained in this Base Prospectus prior to making any investment decision with respect to the Notes. The risks highlighted below could have a material adverse effect on the Group's business, financial condition, results of operations or prospects which, in turn, could have a material adverse effect on RSB's ability to service its payment obligations under the relevant Loan Agreement and, as a result, the ability of the Issuer to make payments under the Notes. In addition, the value of the Notes could decline due to any of these risks, and prospective investors may lose some or all of their investment. Prospective investors should note that the risks described below are not the only risks RSB and the Issuer face. These are the risks RSB considers material. There may be additional risks that RSB currently considers immaterial or of which it is currently unaware, and any of these risks could have similar effects to those set forth above. Risks Related to the Issuer The Issuer is a special purpose vehicle and as such its ability to make payments will rely on RSB's ability to service its payment obligations under the relevant Loan Agreement. This will rely on RSB's business, financial condition, results of operations and prospects which may be adversely affected by the risks highlighted below. Risks Related to RSB's Business and the Banking Sector The instability of the global economy and financial markets could have a material adverse effect on RSB's business, financial conditions, results of operations and prospects and on the value of the Notes Beginning in the second half of 2008 and continuing into 2009, the global economy experienced a significant downturn, the effects of which continue to some degree until present. In response to the financial crisis affecting the global banking sector and financial markets and the threats to the ability of investment banks and other financial institutions to continue as going concerns, governments in the United States, Europe and elsewhere implemented and continue to implement significant rescue packages, which include, among other things, the recapitalisation of banks through state purchases of common and preferred equity securities, the state guarantees of certain forms of bank debt, the purchase of distressed assets from banks and other financial institutions by the state and the provision of guarantees of distressed assets held by banks and other financial institutions by various governments. Despite these actions, the volatility and market disruption in the global banking sector has continued to a degree unprecedented in recent history. In 2010, concerns about sovereign debt, in particular sovereign debt of certain member states of the EU, further disrupted the global credit markets. In May 2010, Greece received a 110 billion bailout from the International Monetary Fund (the "IMF") and the EU. This resulted in widening credit spreads, reduced liquidity and reduced access to funding in the global financial markets. A risk of contagious effects of the Greek sovereign debt crisis on other countries, in particular Spain, Portugal and Ireland, has intensified these adverse effects on the global financial markets. In November 2010, Ireland agreed a 85 billion bailout, and in May 2011, Portugal agreed a 78 billion bailout with the EU and the IMF. In March 2012, a second Greek bailout was agreed in the amount of 130 billion. In June 2012, Spain requested and was granted a bailout package in the amount of 100 billion. The funds were made available directly to the Spanish banks. In June 2012, Cyprus also requested a bailout. Due to high sovereign debt levels, ongoing or anticipated economic recessions, high unemployment, falling housing prices and budget deficits across most Southern-European countries, challenging economic conditions and volatility of financial markets may continue in the short term or beyond. Doubts have also been raised about the fiscal stability of the United Kingdom, Japan and the United States. On 5 August 2011, the rating agency Standard & Poor s Rating Services, a division of The McGraw Hill Companies, Inc. ("S&P"), downgraded the United States' credit rating from "AAA"

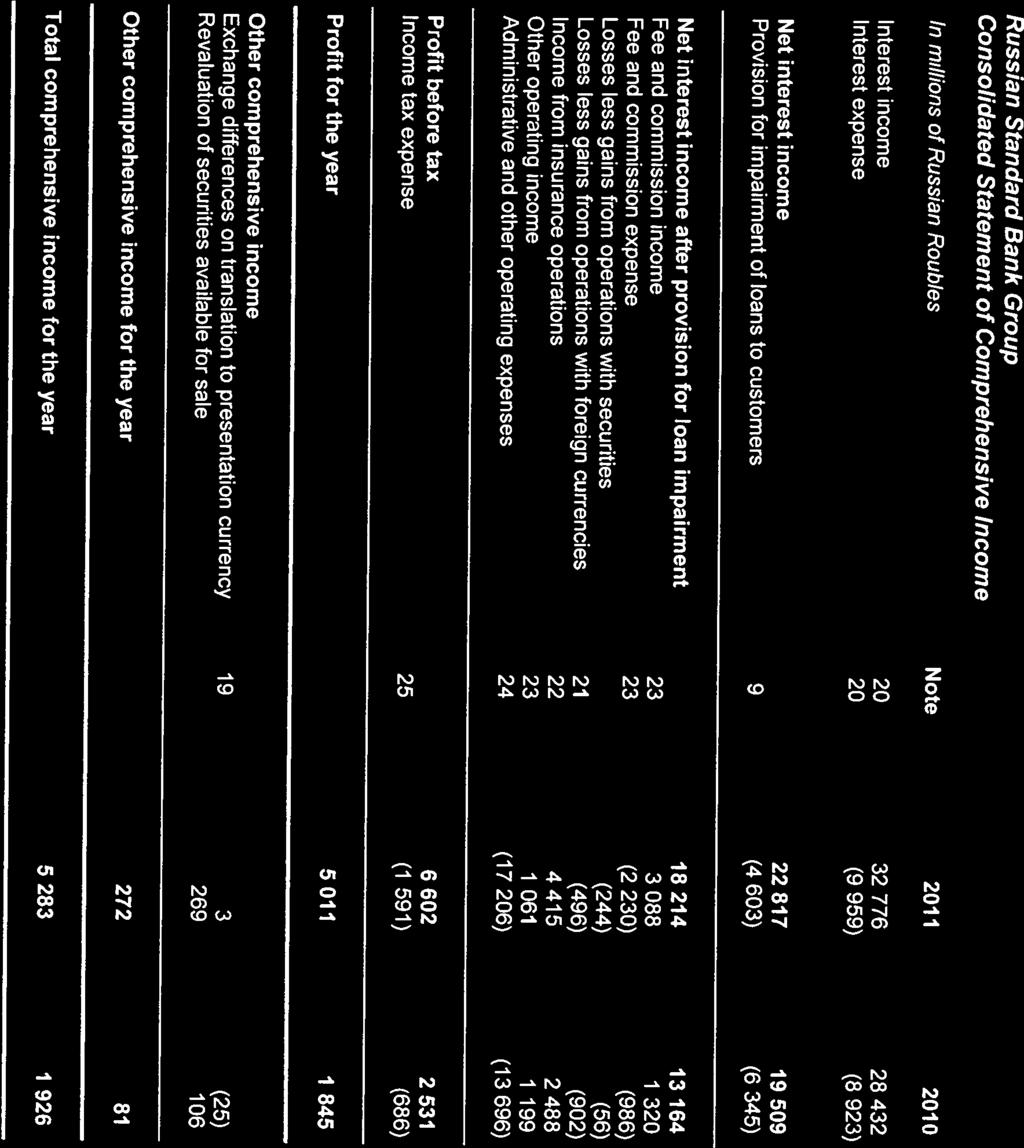

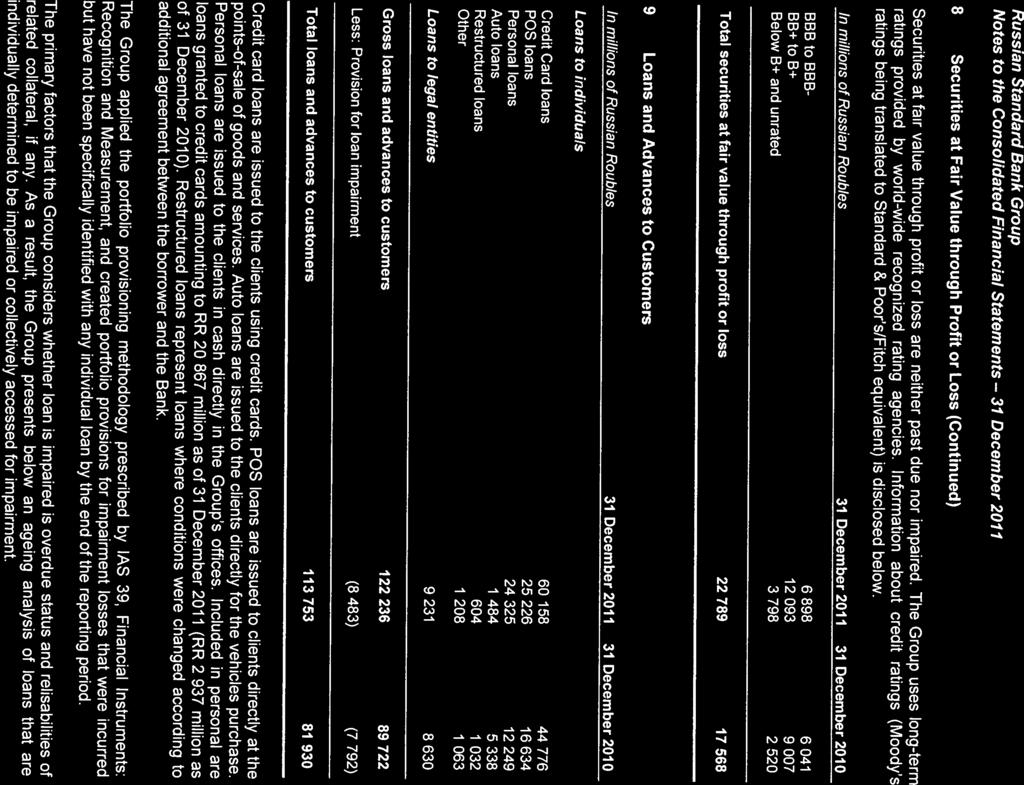

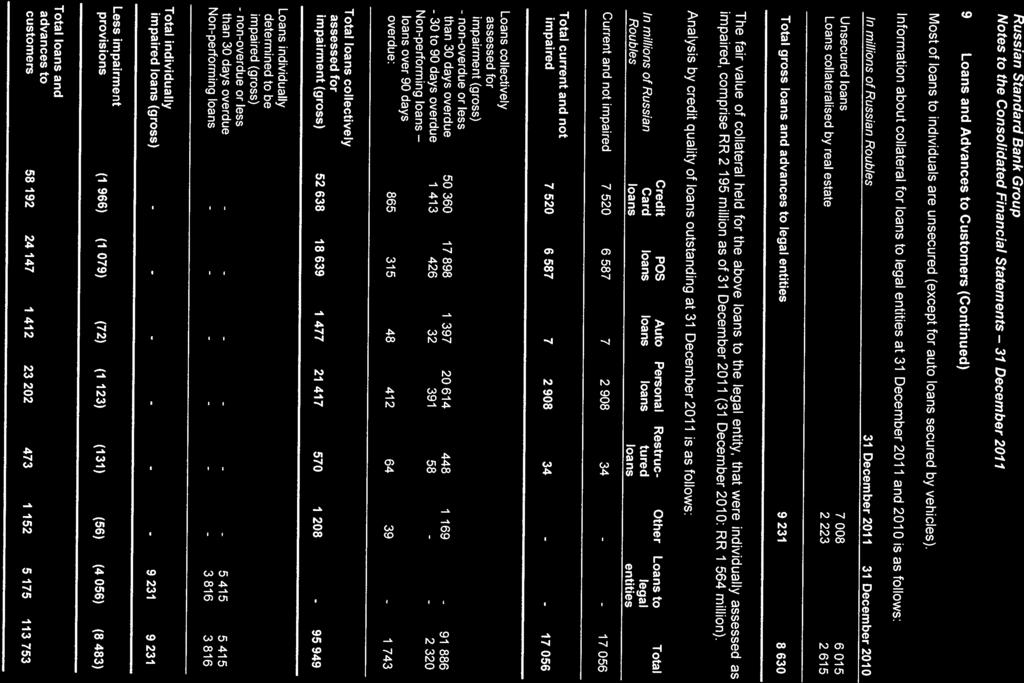

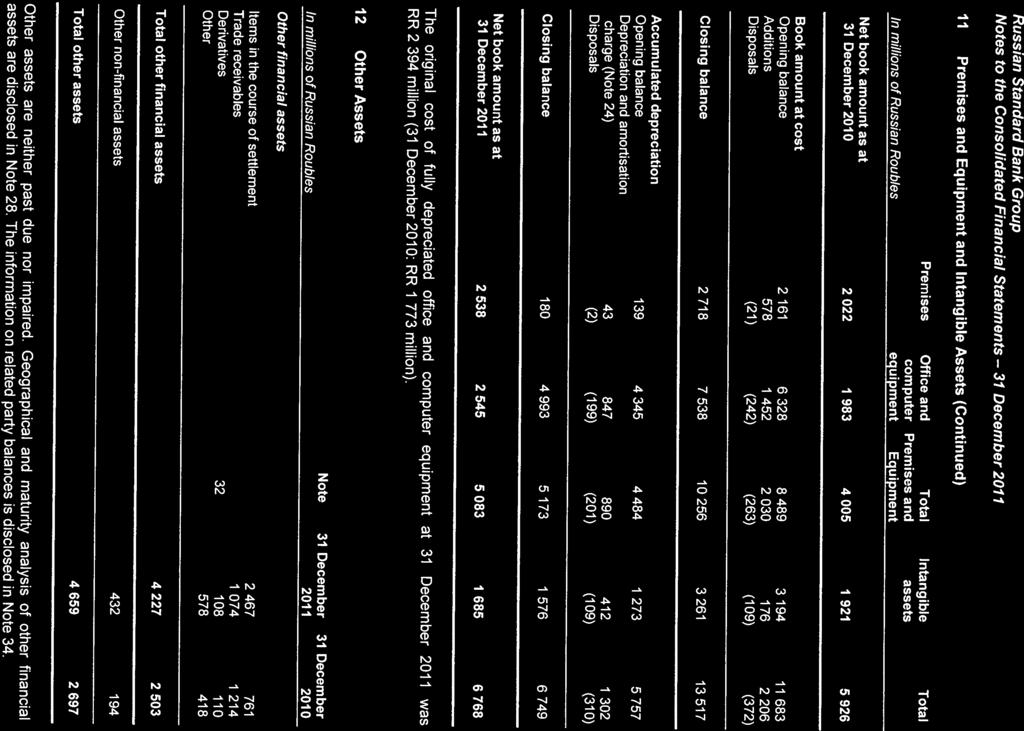

15 to "AA+" with a "negative" outlook amid uncertainties regarding the country's fiscal policy and budget deficit reduction plan, which marks the first time a rating agency has downgraded the United States' credit rating. As a result of risk aversion by investors following these developments, demand for, and values of, securities of emerging markets issuers have decreased and may continue to further decrease in the future. Disruption in the global credit markets has had a negative impact on investor confidence and has negatively affected the interbank markets and debt issuance in terms of volume, maturity and credit spreads. Among the sectors of the global credit markets experiencing particular difficulty due to the impact of the global financial and economic crisis are those associated with sub-prime mortgagebacked securities, asset-backed securities, collateralised debt obligations, leveraged finance and complex structured securities. Continued or intensified turmoil in global credit markets may adversely affect RSB's business, financial condition, results of operations and prospects and the value of the Notes. RSB is subject to risks associated with the credit quality and recovery of loans to customers and market counterparties. Changes in the creditworthiness of RSB s borrowers and counterparties, or in their behaviour, or arising from systemic risks in the Russian or global financial systems, could significantly reduce the value of RSB s assets and increase RSB s write-downs and provisions for impairment losses. As is the case with nearly all other Russian banks, the global financial and economic crisis had an adverse impact on RSB s loan portfolio and certain other types of assets, giving rise to significantly increased impairment charges, write-offs and allowance for loan impairment. A decrease in the employment rate and/or disposable income in Russia, a decrease in corporate liquidity, an increase in the number of corporate and/or personal insolvencies, decreases in RSB's net interest income due to the contraction of its loan portfolio and increased funding costs, decrease in fee and commission income due to the suspension of certain of RSB's consumer finance operations, decreases in RSB's ability to generate growth in its portfolio of credit products as a result of customers' reduced creditworthiness arising out of uncertainties about their future income and ability to absorb higher interest rates, and other factors have reduced in the past and may reduce in the future the ability of RSB's customers to repay loans, which could have a material adverse effect on RSB's business, financial condition, results of operations and prospects and on the value of the Notes. In addition, demand for RSB's consumer finance products is dependent on sales of consumer goods. Unfavourable changes in economic conditions in Russia may result in a decrease in consumer spending and disposable income, and hence a decline in consumer finance lending. Prior to the onset of the global financial and economic crisis in the second half of 2008, RSB's loan portfolio expanded significantly and in line with the general expansion of the Russian economy. However, the crisis resulted in the contraction of the Russian and global economies, dislocation of credit and financial markets and decreases in exports and prices of Russian commodities, which adversely affected the growth of the Russian economy. RSB's loan portfolio was also significantly impacted. RSB's net loan portfolio decreased by 35.7 per cent. from RUB 144,671 million as of 31 December 2008 to RUB 92,985 million as of 31 December 2009 (mainly due to a significant decrease in the amount of new loans issued), further decreasing by 11.9 per cent. to RUB 81,930 million as of 31 December The crisis also had an adverse effect on RSB's non-performing loans (loans that are more than 90 days overdue). Non-performing loans increased from 3.2 per cent. of RSB's gross consumer loan portfolio as of 31 December 2008 to 5.4 per cent. as of 31 December 2009 and then further increased to 5.9 per cent. as of 31 December Reflecting these developments, RSB's allowance for loan impairment increased by 9.8 per cent. from RUB 8,628 million as of 31 December 2008 to RUB 9,476 million as of 31 December RSB's allowance for loan impairment increased from 5.6 per cent. of its gross loan portfolio as of 31 December 2008 to 9.2 per cent. as of 31 December Furthermore, as of 31 December 2011, RSB had loans that had been restructured due to borrowers' financial difficulties in the aggregate amount of RUB 604 million, or 0.5 per cent. of RSB's gross consumer loan portfolio, as compared to RUB 1,032 million, or 1.2 per cent. of RSB's gross consumer loan portfolio, as of 31 December 2010 and RUB 1,810 million, or 1.8 per cent. of RSB's gross consumer loan portfolio, as of 31 December RSB's interest income was also

16 significantly adversely affected by the crisis, decreasing by 33.9 per cent. from RUB 51,311 million for the year ended 31 December 2008 to RUB 33,937 million for the year ended 31 December As a result, RSB's net interest income decreased by 44.8 per cent. from RUB 37,454 million in 2008 to RUB 20,690 million in RSB's interest income and net interest income decreased further by 16.2 per cent. and 5.7 per cent., respectively, in 2010 as compared to The ongoing uncertainty over the euro-zone debt crisis, concerns about the health of the global economy and particularly the economies of the European Union, United States and China, and the resulting volatility in the global financial markets continue to pose risks to the global economic environment. No assurance can be given that a further economic downturn or financial crisis will not occur, or that the measures taken or that will be taken in the future to support the banking system and to overcome the crisis, will be sufficient to restore stability in the global banking sector and financial markets in the short term or beyond. If the state of the Russian and/or the global economy deteriorates again, this may lead to weakening consumer spending, falling corporate profitability and increased insolvencies. Although RSB does not have direct exposure to Eurozone sovereign debt, continuing uncertainty in the international financial markets, or the default or a significant decline in the credit rating of one or more sovereigns or financial institutions, could adversely impact RSB's business and operating results as a result of: impact on the Russian economy and/or financial markets; decreases in the business activity and disposable income of the Russian population and reduced demand for RSB's loan products, which may result in a decrease in the size of RSB's loan portfolio, leading to a decline in RSB's interest income and fee and commission income; deterioration of creditworthiness of customers, resulting in impairments on assets and/or collateral as well as increased levels of non-performing loans and amounts of loan impairment charges; and increases in funding costs (leading to an increase in interest expense) and reduced, or complete lack of, access to capital markets due to unfavourable market conditions and increased competition for deposits. If any of the above events were to occur, this could have a material adverse effect on RSB's business, results of operations, financial conditions and prospects. Turmoil in financial markets has already adversely affected, and may continue to adversely affect, the Russian economy, the Russian banking industry in general and RSB in particular In December 2008, due in large part to the impact of the global financial and economic crisis that began in the second half of 2008, S&P downgraded Russia's foreign currency sovereign credit rating from BBB+/A-2 to BBB/A-3. Moody's Investor Services, Inc. ("Moody's") changed its outlook to "stable" from "positive" on Russia's key ratings in December In February 2009, Fitch downgraded its long-term sovereign rating for the Russian Federation from "BBB+/A-2" to "BBB/A- 3", with "negative" outlook, stating that the lower ratings reflected risks associated with the sharp reversal in external portfolio and other investment flows, which increased the cost and difficulty of meeting the country's external financing needs. In January 2010, Fitch changed its outlook from "negative" to "stable". In October 2011, Moody's adjusted its outlook for the Russian banking system from "stable" to "negative". The change reflected concerns that market volatility was weakening Russia's operating environment, which could negatively affect Russian banks through a system-wide liquidity contraction, slower credit growth and pressures on asset quality over the next 12 to 18 months. In January 2012, the World Bank cut its 2012 global economy growth forecast to 2.5 per cent. from 3.6 per cent., and the Russian economy growth forecast to 3.5 per cent. from 4.0 per cent., though the IMF raised the Russian economy growth forecast back to 4.0 per cent. in April In January 2012, Fitch revised the outlook on the Russian Federation's long-term foreign and local currency Issuer Default Ratings (each, individually, an "IDR") to "stable" from "positive" and

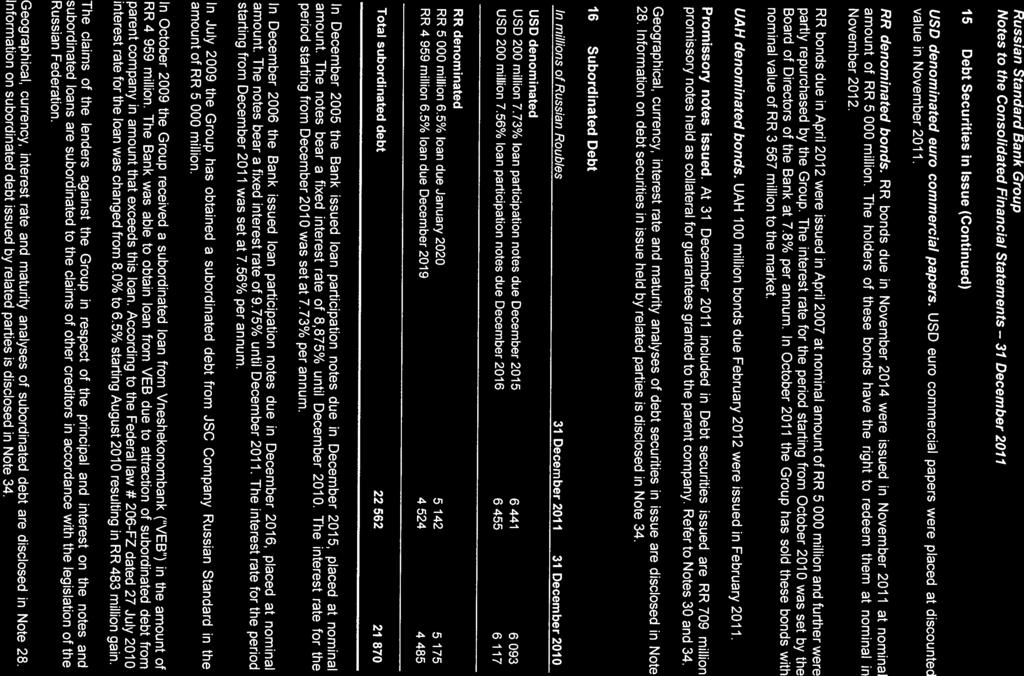

17 affirmed the IDRs at "BBB". The agency has also affirmed Russia's short-term IDR at "F3" and country ceiling at "BBB+". Fitch's revised outlook is based on perceived increased political uncertainty and global economic outlook. In March 2012, Fitch announced it may further lower the Russian sovereign credit rating if the Government does not restrict its budget policy and fails to limit expenditure. There can be no assurance that a future economic crisis will not have a negative effect on investors' confidence in the Russian Federation's markets or economy or the ability of Russian entities to raise capital in the international capital markets, any of which, in turn, could have a material adverse effect on the Russian Federation's economy and/or RSB's business, results of operations, financial condition and prospects. According to the Russian Federal State Statistics Service's latest estimates, Russia's gross domestic product ("GDP") decreased by 7.8 per cent. in This was the first year of negative GDP growth since Russia has also experienced a relatively high level of inflation and a large decrease in equity prices from the levels recorded in May 2008, although equity prices have increased from the low levels reached in the beginning of While Russia's GDP experienced positive growth of 4.0 per cent. in 2010, 4.3 per cent. in 2011 and an estimated 4.4 per cent. in the first half of 2012, there can be no assurance that GDP growth will continue. Furthermore, during the global financial and economic crisis, there were periodic suspensions of Russian stock market trading, extreme volatility in the Russian equity markets and sharp declines in the share prices of Russian financial institutions. The disruptions in the global markets have had a severe impact on liquidity of Russian banks and other financial institutions, as well as the availability of credit and the terms and cost of funding in Russia. Russian banks, including RSB, have experienced a reduction in available financing both in the interbank and short-term funding market, as well as in the longer-term capital markets and through bank finance instruments. The Russian securitisation market has also been largely inaccessible as a result of the crisis. Since October 2008, the Russian Government and the CBR have implemented measures intended to support the liquidity and solvency of Russian banks and to significantly increase the availability of credit to businesses, which have been seen as critical for restoring investor confidence and supporting the medium-term economic growth of the Russian economy. RSB, for example, had unsecured loans from the CBR in the amount of RUB 13,238 million as of 31 December The unsecured lending facility from the CBR was repaid by RSB in In addition, in October 2009, RSB received a subordinated loan from VEB for RUB 4,959 million with a fixed interest rate of 8 per cent. per annum (reduced to 6.5 per cent. per annum from August 2010) maturing in December There can be no assurance, however, that any similar measures, if taken by the Russian Government or the CBR in the future, will be successful in materially improving the liquidity position and financial condition of Russian banks, including RSB, in a time of a financial crisis. RSB could be adversely affected by the deterioration of the commercial soundness and/or the perceived soundness of other financial institutions, which could result in significant systemic liquidity problems, losses or defaults by other financial institutions and counterparties During the global financial and economic crisis, the international and Russian inter-bank lending markets experienced a lack of liquidity and high cost of funds unprecedented in recent history. As a result, RSB has become increasingly subject to the risk of deterioration of the actual or perceived commercial soundness of other financial institutions within and outside Russia. Financial institutions that transact with each other are interrelated as a result of trading, investment, clearing, counterparty and other relationships. This risk is sometimes referred to as "systemic risk" and may adversely affect financial intermediaries, such as clearing agencies, clearing houses, banks, securities firms and exchanges with which RSB interacts on a daily basis, all of which could have an adverse effect on RSB. RSB routinely executes a high volume of transactions with counterparties in the financial services industry, including brokers and dealers, commercial banks, investment banks and other financial institutions. As a result, RSB is exposed to a significant counterparty risk, and this counterparty risk is

18 heightened due to recent financial institutions failures and nationalisations. A default by, or concerns about the stability of, one or more financial institutions could lead to further significant systemic liquidity problems, or losses or defaults by other financial institutions, which could have a material adverse effect on RSB's business, financial condition, results of operations and prospects and the value of the Notes. RSB's ability to grow its business is dependent on having sufficient funding as well as access to various funding sources, and RSB's inability to access such funding at favourable rates, or at all, could adversely affect RSB's business, financial condition, results of operations and prospects and the value of the Notes RSB funds its businesses through a range of sources including customer accounts, issuance of debt securities and bank borrowings. Over the years, RSB has sought to increase the level of retail deposits and the proportion of such deposits in its total liabilities in order to diversify its funding base. As of 30 June 2012 and 31 December 2011, customer accounts represented 68.0 per cent. of RSB's total liabilities, as compared to 57.1 per cent. and 24.3 per cent. as of 31 December 2010 and 2009, respectively. The ongoing availability of retail deposit funding is dependent on a variety of factors outside RSB's control, such as general economic conditions, market volatility, consumer confidence levels in the general economy and the financial services industry, the availability and extent of deposit guarantees and other current laws and regulations affecting deposits (for example, Russia currently entitles depositors who are individuals to withdraw deposits, including term deposits, at any time). In addition, the growth in RSB's deposits is, in part, attributable to the fact that RSB has been offering competitive interest rates on its deposits and has been placing a significant emphasis on customer service. RSB may decide that its strategy of offering higher interest rates is not sustainable in the long-term and it may decide to focus on alternative methods of attracting retail deposits. These and other factors could lead to a reduction in RSB's ability to attract retail deposit funding on appropriate terms in the future. Similar to other deposit-taking institutions, if RSB is unable to attract retail deposits, RSB could be forced to find alternative sources of funding. Such alternative funding may not be available or, if available, may be more expensive, which may adversely impact RSB's ability to achieve its strategic goals to expand its network of branches and grow its loan portfolio. In addition, loss of consumer confidence in RSB's business could lead to retail deposit withdrawals in a short period of time and, if such a risk materialised, it would have an adverse effect on RSB's ability to fund its loan portfolio and its business operations, which in turn would adversely affect RSB's business, financial condition, results of operations and prospects and the value of the Notes. The remainder of RSB's funding is raised in the domestic and international capital markets and interbank markets as well as from syndicated loans and corporate deposits. The current market conditions have significantly reduced RSB's access to funding from private, capital and inter-bank markets at commercially attractive costs. RSB's ability to raise funding from domestic and international markets in amounts sufficient to meet its liquidity needs could be further adversely affected by a number of factors, including any deterioration in Russian and international economic conditions and the state of the Russian and global financial and credit markets. In particular, the tightening of the global credit markets that began in the second half of 2007 as a result of concerns over the U.S. sub-prime mortgage crisis and the valuation and liquidity of asset-backed securities resulted in, among other things, significantly higher inter-bank lending rates, which made financing for banks and financial institutions more difficult to obtain. Any future uncertainty in the Russian or international financial markets or any tightening of credit conditions could restrict RSB's access to funding in the domestic and international credit markets or significantly increase its borrowing costs. If these sources of funding are not available on commercially acceptable terms or at all, RSB's business, financial condition, results of operations, prospects and liquidity position, as well as the value of the Notes, could be materially adversely affected. RSB's ability to continue to access the fixed income capital markets and bank lenders to the extent sufficient to meet its funding needs, including the refinancing of outstanding debt falling due, could be adversely affected by a number of factors, including the current instability in the Russian and international financial markets, the state of the Russian financial and banking system, and changing

19 Russian and international economic conditions generally. The recent global financial and economic crisis was characterised by, among other things, extremely limited opportunities for funding in the capital markets, as well as significantly higher interbank lending rates, making financing more difficult and costly to obtain. In addition, as happened during the crisis, an economic downturn is likely to result in substantial withdrawals of retail deposits (existing Russian legislation allows individuals to withdraw deposits, including term deposits, at any time), which may make funding even more scarce and/or expensive. If RSB is forced to use more expensive funding sources or if other sources of its existing short and long-term funding are not available, RSB's business, financial condition, results of operations, prospects and liquidity position could be materially adversely affected. Any deterioration in the credit rating of RSB could have a material adverse impact on RSB's cost of, and access to, funding As of the date of this Base Prospectus, RSB had a "Ba3" long term rating with a "stable" outlook from Moody's. RSB also had long term and short term ratings of "B+" and "B", respectively, with a "stable" outlook from S&P and a long term rating of "B+" with a "stable" outlook from Fitch. A rating is not a recommendation to buy, sell or hold securities and may be subject to revision, suspension or withdrawal at any time by the assigning rating organisation. There is no assurance that RSB's credit ratings will not be subject to negative rating action at any time by the relevant assigning rating organisation, as was previously the case in 2008 and 2009 as a result of the impact of the global financial and economic crisis on the Russian banking sector in general and on RSB in particular. Such negative rating action could be caused by any of a number of factors, either alone or in combination. Examples of such factors include, without limitation, a downgrade in the sovereign rating of the Russian Federation; a significant deterioration in the operating environment, or in RSB's financial or operational performance or the quality of its assets; liquidity pressures; or a reduction in RSB's capitalisation levels through payment of dividends or otherwise. Any deterioration in RSB's credit ratings could undermine confidence in RSB, limit its access to capital markets and/or increase RSB's cost of funding, which could require RSB to seek alternative and possibly more expensive sources of funding in order to maintain market share or grow RSB's business, thereby affecting RSB's competitiveness and financial condition. Margins on RSB's products may decline in the future, which would have an adverse effect on RSB's business, financial condition, results of operations and prospects and the value of the Notes Intense competition which has developed in Russia for credit card loans, personal loans and point-ofsale ("POS") loans, as well as excess liquidity levels prior to the onset of the global financial and economic crisis, resulted in a considerable downward pressure on RSB's effective and average interest rates on these products, particularly in In addition, as a result of increased volatility in the international and domestic markets, as well as changes in the Russian regulatory environment including the new regulations introduced by the CBR on the disclosure of the effective interest rate charged on consumer lending products and certain calculation procedures, in August 2007 RSB changed the pricing policy of its consumer lending products, including the removal of monthly fees and commissions charged on both new and existing products. Furthermore, in 2007 RSB's retail partners introduced commissions for selling RSB's products through their retail chains. As a result of these developments, in effective interest rates and interest margins on RSB's credit card loans, personal loans, POS loans and other products declined. Although RSB's average interest rate on loans and advances to individuals and net interest margin stabilized at 33.8 per cent. and 18.6 per cent. in 2010, 34.0 per cent. and 18.9 per cent. in 2011, and 34.2 per cent. and 18.7 per cent. in the first half of 2012, respectively, in the medium term RSB believes that margins in its POS loan and likely in its personal loan businesses may contract to levels at which such businesses will be principally used as vehicles for acquiring credit card customers. RSB also expects that interest margins and spreads in its credit card business may decline as a result of increased competition in the credit card market, in particular from state-owned banks. See " Competition in the Russian banking industry and specifically in consumer lending may continue to adversely affect RSB's financial condition and prospects." Although RSB's cost of funding declined in 2010 and 2011, with the average rate on

20 interest-bearing liabilities decreasing from 9.6 per cent. in 2009 to 8.7 per cent. in 2010 and 8.2 per cent. in 2011, it has increased to 8.8 per cent. in the first half of If RSB's cost of funding continues to increase, as a result of ongoing instability in the global financial markets or otherwise, RSB's margins may be adversely affected. Declining margins and/or spreads are likely to adversely affect RSB profitability, which could have a material adverse effect on RSB's business, financial condition, results of operations and prospects and the value of the Notes. RSB's financial condition and results of operations depend on consumers' consumption and income levels as well as consumer understanding of credit products, which are outside RSB's control RSB's business focuses on lending to individuals. As of 30 June 2012, 93.5 per cent. of RSB's gross loan portfolio comprised loans to individuals. Sustainable development of the consumer finance market and the credit card market in Russia is highly dependent on economic stability and growth, increases in consumers' average disposable income and levels of consumer spending. The global financial and economic crisis has impacted and may continue to impact the demand for consumer goods and credit card products. A deterioration in the performance of the Russian economy in the future or stagnation or reduction in levels of personal income, individual purchasing power or consumer confidence (either generally or specifically in respect of the banking sector) may cause the demand for consumer goods and credit products to decrease, resulting in a corresponding decrease in demand for RSB's credit cards and other consumer finance products. The development of the consumer finance market and credit card market in Russia and the growth of RSB's loan portfolio are also dependent on increasing consumer understanding and acceptance of credit products, particularly in smaller population centres outside of Moscow. As a substantial portion of RSB's customer base consists of individuals in a demographic group with relatively little experience or understanding of credit products, there can be no assurance that RSB will be able to maintain and increase consumer acceptance of credit products. RSB's financial condition and results of operations depend on correctly assessing the creditworthiness of its customers and counterparties, and this is not always possible RSB is exposed to credit risk related to its borrowers and counterparties. RSB s business, financial condition, results of operations and prospects depend on an accurate assessment of the creditworthiness of its clients and counterparties, the adequacy of its provisioning levels and the continued management and monitoring of the risks of its loan portfolio. The financial condition, and particularly the level of disposable income, of retail customers in Russia is generally more variable and their credit risk is, on average, less predictable than in more mature markets and economies, which makes assessment more difficult. Therefore, notwithstanding RSB s credit risk evaluation procedures, RSB may be unable to accurately assess the current financial condition of existing or potential borrowers or counterparties and to accurately determine the ability of such borrowers or counterparties to meet their financial obligations to RSB. In addition, the retail lending market in Russia is relatively undeveloped and limited resources are available to Russian banks to ascertain the credit history of individual borrowers. The institution of centralised credit databases in Russia is relatively new, with the first centralised credit bureau established in Russia in June In addition, the quality of information provided by Russian credit bureaus is generally lower than in the U.S. and in many Western countries. As credit bureaus are not widely developed in the Russian Federation, it is particularly difficult to accurately assess the credit risk of individuals. Although RSB uses information from several credit bureaus complemented by data from its internal proprietary database of individuals (including both RSB clients and applicants who are not RSB clients) consisting of over 30 million records as of 30 June 2012, RSB has to rely mostly on information provided by borrowers in making its credit decisions. As a result, the financial condition of private individuals transacting with RSB is difficult to assess and predict with a high degree of certainty. Furthermore, the limited availability of recent and reliable credit information on

21 retail borrowers constrains RSB's ability to detect and prevent fraudulent activities by potential borrowers, including the use of false information in order to obtain credit, which could result in decreased loan recovery by RSB. Limited availability of recent and reliable credit information on retail borrowers may result in RSB's inability to assess and create necessary provisions for credit risk and, as a result, provisions for loan impairment may be insufficient to cover actual losses. Loans and advances to customers net of provision for loan impairment accounted for 63.2 per cent. of RSB's total assets as of 30 June RSB's provision for loan impairment was RUB 11,427 million, or 7.5 per cent. of total loans, as of 30 June As of 30 June 2012, RSB's restructured loans amounted to RUB 574 million and total written-off loans during the six months ended 30 June 2012 amounted to RUB 2,921 million. Material additions to the provision for loan impairment could materially decrease RSB's net income. The actual amount of future provisions for loan losses cannot be determined in advance and may vary from the amounts of past provisions. Any increase in the provision for loan impairment might have a material adverse effect on RSB's financial condition and results of operations. Although RSB has invested substantial time and effort in its risk management strategies when building its existing loan portfolio and has sought to enhance those strategies in light of the current economic conditions, there can be no guarantee that such risk management strategies will protect RSB from increased levels of non-performing loans, particularly when confronted with risks that RSB did not identify or anticipate from its existing portfolio. RSB's non-performing loans were 5.2 per cent. of RSB's gross loans and advances to customers as of 30 June There can be no assurance that RSB's current level of loan recovery will be maintained in the future and failure to accurately assess the credit risk of potential borrowers or acceptance of a higher degree of credit risk in the course of lending operations may result in a deterioration of RSB s loan portfolio and a corresponding increase in loan impairments, which would have a material adverse effect on RSB s business, financial conditions, results of operations and prospects and on the value of the Notes. RSB's risk management policies and procedures may be ineffective RSB's policies and procedures for managing credit risk, market risk, liquidity risk and operational risk may prove ineffective. Some of RSB's methods for managing risk are based upon observations of historical market behaviour and RSB applies statistical techniques to these observations to arrive at quantifications of its potential risk exposures. However, these methods may not accurately quantify RSB's risk exposures, especially in situations that cannot be identified based on its historical data. In particular, if RSB enters new lines of business, historical data may be incomplete. It is also possible that the global financial and economic crisis might have impaired RSB's ability to assess credit exposure and asset values accurately if its models and techniques have become less predictive of future conditions, behaviours and valuations. As additional information becomes available, RSB may need to make additional provisions if default rates are higher than expected. If circumstances arise whereby RSB did not identify, anticipate or correctly evaluate certain risks in developing its statistical models, losses could be greater than the maximum losses envisaged under its risk management system. In addition, certain risks may not be accurately quantified by RSB's risk management systems. If a material deficiency in RSB's risk management or other internal control policies or procedures arises, this may expose it to significant credit, liquidity, market or operational risk, which may in turn have a material adverse effect on RSB's business, financial condition, results of operations and prospects and the value of the Notes. Material deficiencies in RSB's risk management policies or procedures may expose it to significant credit, liquidity, market or operational risk. Deficiencies in respect of credit risk management may lead to RSB not being able to assess accurately default risk on loans provided to its clients. RSB may, therefore, need to make additional provisions if default rates are higher than expected. See " RSB's financial condition and results of operations depend on correctly assessing the creditworthiness of its customers and counterparties, and this is not always possible". Deficiencies in respect of liquidity risk management may result in the inability of RSB to meet its obligations in full when they become