IMPORTANT NOTICE NOT FOR DISTRIBUTION TO ANY PERSON OR ADDRESS IN THE UNITED STATES.

|

|

|

- Darren Lester

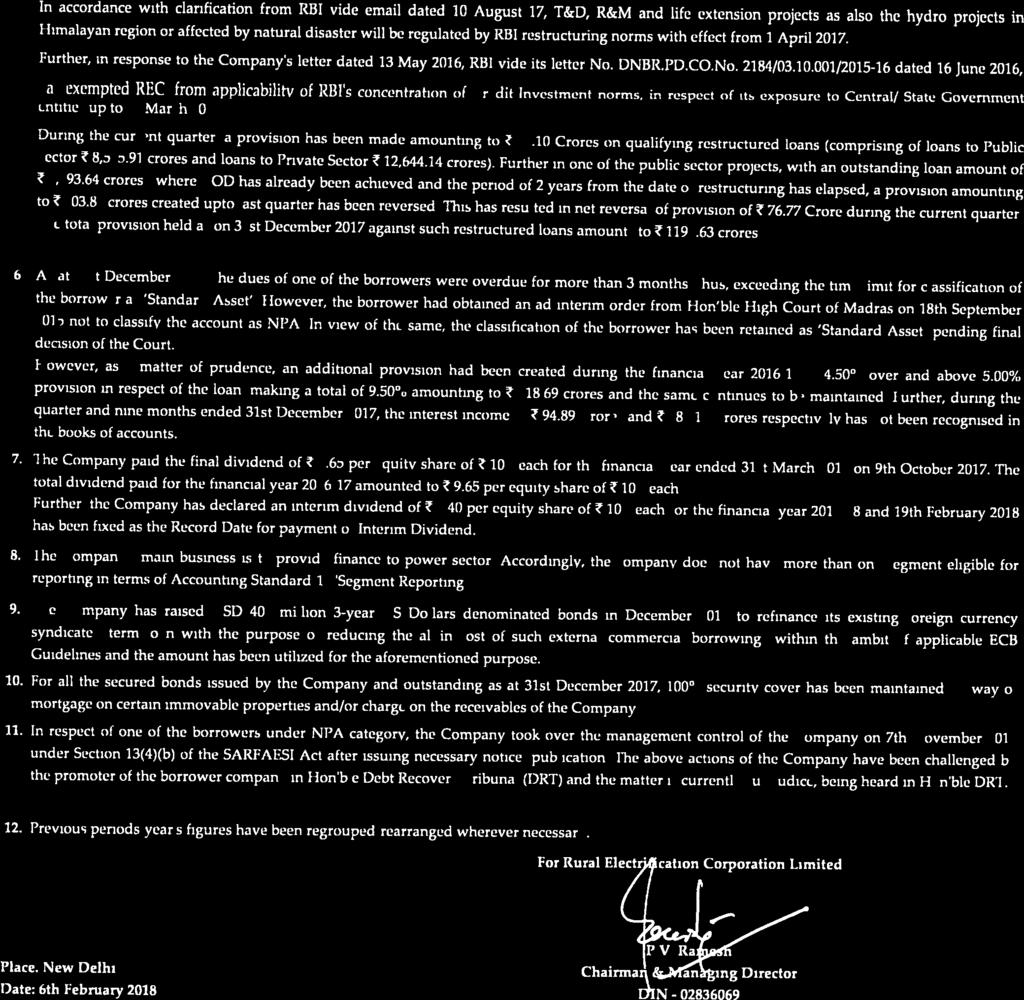

- 6 years ago

- Views:

Transcription

1 IMPORTANT NOTICE NOT FOR DISTRIBUTION TO ANY PERSON OR ADDRESS IN THE UNITED STATES. IMPORTANT: You must read the following before continuing. The following applies to the note offering circular dated 15 March 2018 (together with the offering circular dated 28 February 2018, the Offering Circular) following this page, and you are therefore advised to read this carefully before reading, accessing or making any other use of the Offering Circular. In accessing the Offering Circular, you agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from us as a result of such access. NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER OF SECURITIES FOR SALE IN THE UNITED STATES OR ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. THE SECURITIES HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE SECURITIES ACT), OR THE SECURITIES LAWS OF ANY STATE OF THE U.S. OR OTHER JURISDICTION AND THE SECURITIES MAY NOT BE OFFERED OR SOLD WITHIN THE U.S., EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIES LAWS. THE FOLLOWING OFFERING CIRCULAR MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER, AND IN PARTICULAR, MAY NOT BE FORWARDED TO ANY U.S. ADDRESS. ANY FORWARDING, DISTRIBUTION OR REPRODUCTION OF THIS DOCUMENT IN WHOLE OR IN PART IS UNAUTHORISED. FAILURE TO COMPLY WITH THIS DIRECTIVE MAY RESULT IN A VIOLATION OF THE SECURITIES ACT OR THE APPLICABLE LAWS OF OTHER JURISDICTIONS. ANY INVESTMENT DECISION SHOULD BE MADE ON THE BASIS OF THE TERMS AND CONDITIONS OF THE SECURITIES AND THE INFORMATION CONTAINED IN THE OFFERING CIRCULAR. IF YOU HAVE GAINED ACCESS TO THIS TRANSMISSION CONTRARY TO ANY OF THE FOREGOING RESTRICTIONS, YOU ARE NOT AUTHORISED AND WILL NOT BE ABLE TO PURCHASE ANY OF THE SECURITIES DESCRIBED THEREIN. Confirmation of your Representation: This Offering Circular is being sent at your request and by accepting the and accessing this Offering Circular, you shall be deemed to have represented to us that the electronic mail address that you gave us and to which this has been delivered is not located in the U.S. and that you consent to delivery of such Offering Circular by electronic transmission. You are reminded that this Offering Circular has been delivered to you on the basis that you are a person into whose possession this Offering Circular may be lawfully delivered in accordance with the laws of the jurisdiction in which you are located and you may not, nor are you authorised to, deliver this Offering Circular to any other person. The materials relating to any offering of securities described in the Offering Circular do not constitute, and may not be used in connection with, an offer or solicitation in any place where offers or solicitations are not permitted by law. If a jurisdiction requires that the offering be made by a licensed broker or dealer and the underwriters or any affiliate of the underwriters is a licensed broker or dealer in that jurisdiction, the offering shall be deemed to be made by the underwriters or such affiliate on behalf of the Issuer in such jurisdiction. This Offering Circular has been sent to you in an electronic form. You are reminded that documents transmitted via this medium may be altered or changed during the process of electronic transmission

2 and consequently none of Australia and New Zealand Banking Group Limited, Barclays Bank PLC, Singapore Branch, The Hongkong and Shanghai Banking Corporation Limited, Singapore Branch, Mizuho Securities Asia Limited and MUFG Securities EMEA plc (together, the Joint Lead Managers), nor any person who controls any of them, nor any director, officer, employee, nor any agent of any of them or affiliate of any such person accepts any liability or responsibility whatsoever in respect of any difference between the Offering Circular distributed to you in electronic format and the hard copy version available to you on request from the Joint Lead Managers. You are responsible for protecting against viruses and other destructive items. Your use of this is at your own risk and it is your responsibility to take precautions to ensure that it is free from viruses and other items of a destructive nature. To the fullest extent permitted by law, none of the Joint Lead Managers, nor any person who controls any of them, nor any director, officer, employee, nor any agent of any of them or affiliate of any such person accepts any responsibility for the contents of this Offering Circular or for any other statement, made or purported to be made by the Joint Lead Managers or by any person who controls any of them, or by any director, officer, employee or agent of each of them or affiliate of any such person in connection with the Issuer (as defined in the Offering Circular), or the Offering (as defined in the Offering Circular). The Joint Lead Managers accordingly disclaim all and any liability whether arising in tort or contract or otherwise which any of them might otherwise have in respect of this Offering Circular or any such statement. The Offering Circular has not been and will not be registered, produced or made available to all as an offer document (whether a prospectus in respect of a public offer or an information memorandum or private placement offer letter or other offering material in respect of any private placement under the Companies Act, 2013 or any other applicable Indian laws) with the Registrar of Companies of India or the Securities and Exchange Board of India or any other statutory or regulatory body of like nature in India.

3 NOTE OFFERING CIRCULAR Rural Electrification Corporation Limited (incorporated with limited liability in the Republic of India) Issue of U.S.$300,000, per cent. Notes due 2028 issued pursuant to the U.S.$3,000,000,000 Medium Term Note Programme The U.S.$300,000, per cent. Notes due 2028 (the Notes) will be issued by Rural Electrificaton Corporation Limited (the Issuer or REC), pursuant to its U.S.$3,000,000,000 Medium Term Note Programme (the Programme). The Notes will bear interest at the rate of per cent. per annum from and including 22 March 2018 up to and including 22 March 2028 and interest will be payable semi-annually on 22 September and 22 March of each year, commencing on 22 September 2018 (the Offering). The Notes will mature on 22 March Prior to maturity, the Notes may be redeemed by the Issuer, in whole, but not in part, in the event of certain changes in Indian tax law. See "Terms and Conditions of the Notes". The Notes will constitute the direct, unconditional and (subject to Condition 4) unsecured obligations of the Issuer and will rank pari passu, without any preference among themselves with all other outstanding unsecured and unsubordinated obligations of the Issuer, present and future, but, in the event of insolvency, only to the extent permitted by applicable laws relating to creditors rights. Application will be made to the London Stock Exchange for the Notes to be admitted to the London Stock Exchange s International Securities Market (ISM). The ISM is not a regulated market for the purposes of Directive 2004/39/EC. The ISM is a market designated for professional investors. Notes admitted to trading on the ISM are not admitted to the Official List of the UKLA. The London Stock Exchange has not approved or verified the contents of the Offering Circular. Application will be made to the Singapore Exchange Securities Trading Limited (the SGX-ST). Final permission to list the Notes will be granted when the Notes have been admitted to the Official List of the SGX-ST (the SGX Official List). The SGX-ST assumes no responsibility for the correctness of any of the statements made or opinions expressed or reports contained herein. Admission to the SGX Official List of the SGX-ST and quotation of the Notes on the SGX-ST are not to be taken as an indication of the merits of the Issuer or the Notes. For so long as any Notes are listed on the SGX-ST and the rules of the SGX-ST so require, such Notes will be traded on the SGX-ST in a minimum board lot size of S$200,000 or its equivalent in other currencies. Investing in the Notes involves risks. See "Risk Factors" in the Original Offering Circular (as defined herein) for a discussion of certain factors to be considered in connection with an investment in the Notes. The Notes have been rated BBB- by Fitch Ratings Limited and Baa3 by Moody s. Such ratings of the Notes do not constitute a recommendation to buy, sell or hold the Notes and may be subject to revision or withdrawal at any time by either such rating organisation. Each such rating should be evaluated independently of any other rating of the Notes, of the Issuer's other securities or of the Issuer. The Notes have not been and will not be registered under the U.S. Securities Act of 1933, as amended (the Securities Act) and may not be offered or sold in the United States unless the Notes are registered under the Securities Act or an exemption from the registration requirements of the Securities Act is available. The Notes will not be transferable except in accordance with the restrictions described under "Transfer Restrictions" in the Original Offering Circular. The Notes offered outside the United States in reliance on Regulation S (the Regulation S Notes) will be evidenced by a Regulation S Global Note (as defined in the Original Offering Circular) deposited with a common depositary for Euroclear Bank SA/NV (Euroclear) and Clearstream Banking S.A. (Clearstream, Luxembourg), and registered in the name of a nominee of such common depositary. It is expected that delivery of the Regulation S Global Note will be made on 22 March 2018 or such later date as may be agreed (the Closing Date) by the Issuer and the Joint Lead Managers. The Classification of Financial Instrument (CFI) code assigned to the Notes is DTZXFB. The Financial Instrument Short Name (FISN) code assigned to the Notes is RURAL ELECTRIFI/4.625EMTN For the purposes of the Notes only, this offering circular (the Note Offering Circular) is supplemental to, and should be read in conjunction with, the offering circular dated 28 February 2018 (the Original Offering Circular) (the Original Offering Circular together with this Note Offering Circular, the Offering Circular). Words and expressions defined in the Original Offering Circular shall have the same meanings where used in this Note Offering Circular unless the context otherwise requires or unless otherwise stated herein. Joint Lead Managers ANZ BARCLAYS HSBC Mizuho Securities MUFG The date of this Note Offering Circular is 15 March 2018.

4 TABLE OF CONTENTS PAGE ABOUT THIS DOCUMENT... S-1 RECENT DEVELOPMENTS... S-2 USE OF PROCEEDS... S-3 PRICING SUPPLEMENT... S-4 TAXATION... S-10 OFFERING CIRCULAR DATED 28 FEBRUARY ANNEX A

5 ABOUT THIS DOCUMENT In the event of any conflict between the description of the Notes in this Note Offering Circular and the description of the Notes in the Original Offering Circular, the description of the Notes in this Note Offering Circular shall prevail. The Issuer accepts responsibility for the information contained in this Note Offering Circular. Having taken all reasonable care to ensure that such is the case, the information contained in this Note Offering Circular is, to the best of the Issuer s knowledge, in accordance with the facts and contains no omission likely to affect its import. Furthermore, the issuance of the Notes which would be eligible for electronic settlement, is in accordance with all applicable Indian laws and is duly authorised by the Issuer s constitutional documents as well as other applicable statutory and other consents. There has been no significant change in the financial or trading position of the Issuer or of the Issuer and its subsidiaries on a consolidated basis (the Group) since the date of the most recently published figures for the nine months ended 31 December 2017 and no material adverse change in the financial position or prospects of the Issuer or of the Group since the date of the most recently published audited accounts as at 31 March There are no governmental, legal or arbitration proceedings (including any proceedings which are pending or threatened) of which the Issuer is aware in the 12 months preceding the date of this document which may have or have in such period had a significant effect on the financial position or profitability of the Issuer or of the Group. As at the date of this Note Offering Circular, there are no potential conflicts of interest between any duties owed to the Issuer by the directors of the Issuer and the private interests and/or other duties owed by these individuals and there are no arrangements, known to the Issuer, the operation of which may at a subsequent date result in a change in control of the Issuer. Furthermore, as of the date of this Note Offering Circular, there are no material contracts that have been entered into outside the ordinary course of the Issuer s business, which could result in any group member being under an obligation or entitlement that would be material to the Issuer s ability to meet its obligation under the Notes to the Noteholders. S-1

6 RECENT DEVELOPMENTS Further to hedging activities undertaken by REC in January in respect of the U.S.$400,000, per cent. Notes due 2020 issued by it in December 2017, as at the date hereof, 79.81% of the ECBs have been hedged until maturity. S-2

7 USE OF PROCEEDS The net proceeds of the Notes will be applied to finance projects in the power infrastructure sector in India, in accordance with the ECB Guidelines. S-3

8 PRICING SUPPLEMENT MiFID II product governance/professional investors and ECPs only target market Solely for the purposes of the manufacturer s product approval process, the target market assessment in respect of the Notes has led to the conclusion that: (i) the target market for the Notes is eligible counterparties and professional clients only, each as defined in Directive 2014/65/EU (as amended, MiFID II); and (ii) all channels for distribution of the Notes to eligible counterparties and professional clients are appropriate. Any person subsequently offering, selling or recommending the Notes (a distributor) should take into consideration the manufacturer's target market assessment; however, a distributor subject to MiFID II is responsible for undertaking its own target market assessment in respect of the Notes (by either adopting or refining the manufacturer's target market assessment) and determining appropriate distribution channels. 15 March 2018 Rural Electrification Corporation Limited Legal entity identifier (LEI): B4YRYWAMIJZ374 Issue of U.S.$300,000, per cent. Notes due 2028 under the U.S.$3,000,000,000 Medium Term Note Programme This document constitutes the Pricing Supplement relating to the issue of Notes described herein. Terms used herein shall be deemed to be defined as such for the purposes of the Conditions set forth in the Offering Circular dated 28 February 2018 (the Offering Circular). This Pricing Supplement contains the final terms of the Notes and must be read in conjunction with such Offering Circular. 1. Issuer: Rural Electrification Corporation Limited 2. (a) Series Number: 01 (b) Tranche Number: 01 (c) Date on which the Notes will be consolidated and form a single Series: Not Applicable 3. Specified Currency or Currencies: U.S. dollars (U.S.$) 4. Aggregate Nominal Amount: (a) Series: U.S.$300,000,000 (b) Tranche: U.S.$300,000, Issue Price: per cent. of the Aggregate Nominal Amount 6. (a) Specified Denominations: U.S.$200,000 and integral multiples of U.S.$1,000 in excess thereof (b) Calculation Amount (and in relation to calculation of interest in global form see Conditions): U.S.$1, (a) Issue Date: 22 March 2018 S-4

9 (b) Interest Commencement Date: Issue Date 8. Maturity Date: 22 March Interest Basis: per cent. Fixed Rate (further particulars specified below) 10. Redemption/Payment Basis: Redemption at par 11. Change of Interest Basis or Redemption/Payment Basis: Not Applicable 12. Put/Call Options: Not Applicable 13. (a) Status of the Notes: Senior (b) (c) Date of board approval for issuance of Notes obtained: Date of regulatory approval/consent for issuance of Notes obtained: 24 March 2017 Letter no. CO.FED.ECBD.2871/ / dated 29 September 2017 from the Reserve Bank of India and Letter no. CO.FED.ECBD.7726/ / dated 15 March 2018 from the Reserve Bank of India 14. Listing: Singapore Exchange Securities Trading Limited and the International Securities Market of the London Stock Exchange 15. Method of distribution: Syndicated PROVISIONS RELATING TO INTEREST (IF ANY) PAYABLE 16. Fixed Rate Note Provisions: Applicable (a) Rate(s) of Interest: per cent. per annum payable semi-annually in arrear on each Interest Payment Date (b) Interest Payment Date(s): 22 March and 22 September in each year commencing 22 September 2018 up to and including the Maturity Date (c) (d) Fixed Coupon Amount(s) for Notes in definitive form (and in relation to Notes in global form see Conditions): Broken Amount(s) for Notes in definitive form (and in relation to Notes in global form see Conditions): U.S.$ per Calculation Amount Not Applicable (e) Day Count Fraction: 30/360 (f) Determination Date(s): Not Applicable S-5

10 (g) Other terms relating to the method of calculating interest for Fixed Rate Notes: None 17. Floating Rate Note Provisions: Not Applicable 18. Zero Coupon Note Provisions: Not Applicable 19. Index Linked Interest Note Provisions: 20. Dual Currency Interest Note Provisions: Not Applicable Not Applicable PROVISIONS RELATING TO REDEMPTION 21. Issuer Call: Not Applicable 22. Investor Put: Not Applicable 23. Final Redemption Amount: U.S.$1,000 per Calculation Amount 24. Early Redemption Amount payable on redemption for taxation reasons or on event of default and/or the method of calculating the same (if required): U.S.$1,000 per Calculation Amount GENERAL PROVISIONS APPLICABLE TO THE NOTES 25. Form of Notes: Registered Notes: 26. Additional Financial Centres: Not Applicable Registered Global Note (U.S.$300,000,000 nominal amount) registered in the name of a nominee for a common depositary for Euroclear and Clearstream 27. Talons for future Coupons to be attached to Definitive Notes in bearer form (and dates on which such Talons mature): 28. Details relating to Partly Paid Notes: amount of each payment comprising the Issue Price and date on which each payment is to be made and consequences of failure to pay, including any right of the Issuer to forfeit the Notes and interest due on late payment: No Not Applicable 29. Details relating to Instalment Notes: Not Applicable (a) Instalment Amount(s): Not Applicable S-6

11 (b) Instalment Date(s): Not Applicable 30. Permitted Security Interest Date: 15 March 2018 (See Condition 4) 31. Other terms or special conditions: Not Applicable DISTRIBUTION 32. (a) If syndicated, names of Managers: Australia and New Zealand Banking Group Limited Barclays Bank PLC, Singapore Branch The Hongkong and Shanghai Banking Corporation Limited, Singapore Branch Mizuho Securities Asia Limited MUFG Securities EMEA plc (b) Stabilizing Manager(s) (if any): Australia and New Zealand Banking Group Limited Barclays Bank PLC, Singapore Branch The Hongkong and Shanghai Banking Corporation Limited, Singapore Branch Mizuho Securities Asia Limited MUFG Securities EMEA plc 33. If non-syndicated, name of relevant Dealer: 34. Whether TEFRA D or TEFRA C rules applicable or TEFRA rules not applicable: 35. Whether Category 1 or Category 2 applicable in respect of the Notes offered and sold in reliance on Regulation S: Not Applicable TEFRA not applicable Category 1 (Notes offered in reliance on Category 1 must be in registered form) 36. Additional selling restrictions: Not Applicable OPERATIONAL INFORMATION 37. Any clearing system(s) other than Euroclear and Clearstream, Luxembourg and the relevant identification number(s): Not Applicable 38. Delivery: Delivery against payment 39. Additional Paying Agent(s) (if any): Not Applicable ISIN: XS Common Code: S-7

12 LISTING APPLICATION This Pricing Supplement comprises the final terms required to list the issue of Notes described herein pursuant to the U.S.$3,000,000,000 Medium Term Note Programme of Rural Electrification Corporation Limited. S-8

13 RESPONSIBILITY We accept responsibility for the information contained in this Pricing Supplement. Signed on behalf of the Issuer: By: Duly authorized By: Duly authorized S-9

14 TAXATION Investors should carefully consider the following as well as the other information contained in this Note Offering Circular prior to making an investment in the Notes. The following section should be read in conjunction with the Taxation section in the Original Offering Circular. The information provided below does not purport to be a comprehensive description of all tax considerations which may be relevant to a decision to purchase Notes. In particular, the information does not consider any specific facts of circumstances that may apply to a particular purchaser. Neither these statements nor any other statements in this Offering Circular are to be regarded as advice on the tax position of any holder of the Notes or of any person acquiring, selling or otherwise dealing with the Notes or on any tax implications arising from the acquisition, sale or other dealings in respect of the Notes. The statements do not purport to be a comprehensive description of all the tax considerations that may be relevant to a decision to purchase, own or dispose of the Notes and do not purport to deal with the tax consequences applicable to all categories of investors, some of which (such as dealers in securities) may be subject to special rules. Prospective purchasers of Notes are advised to consult their own tax advisers as to the tax consequences of the purchase, ownership and disposal of Notes, including the effect of any state or local taxes, under the tax laws applicable in each country of which they are residents or countries of purchase, holding or disposal of the Notes. Additionally, in view of the number of jurisdictions where local laws may apply, this Offering Circular does not discuss the local tax consequences to a potential holder, purchaser, seller arising from the acquisition, holding or disposal of the Notes. Prospective investors must therefore inform themselves as to any tax, exchange control legislation or other laws and regulations in force relating to the subscription, holding or disposal of Notes at their place of ordinance, and the countries of which they are citizens or countries of purchase, holding or disposal of Notes. In the event of any conflict between the descriptions under Taxation in this Note Offering Circular and the descriptions under Taxation in the Original Offering Circular, the following descriptions in this Note Offering Circular shall prevail. Singapore Taxation The statements below are general in nature and are based on certain aspects of current tax laws in Singapore and administrative guidelines issued by the Monetary Authority of Singapore (the MAS) in force as at the date of this Note Offering Circular and are subject to any changes in such laws or administrative guidelines, or the interpretation of those laws or guidelines, occurring after such date, which changes could be made on a retroactive basis. Neither these statements nor any other statements in this Note Offering Circular are intended or are to be regarded as advice on the tax position of any holder of the Notes or of any person acquiring, selling or otherwise dealing with the Notes or on any tax implications arising from the acquisition, sale or other dealings in respect of the Notes. The statements made herein do not purport to be a comprehensive or exhaustive description of all the tax considerations that may be relevant to a decision to subscribe for, purchase, own or dispose of the Notes and do not purport to deal with the tax consequences applicable to all categories of investors, some of which (such as dealers in securities or financial institutions in Singapore which have been granted the relevant Financial Sector Incentive(s)) may be subject to special rules or tax rates. Holders and prospective holders of the Notes are advised to consult their own tax advisors as to the Singapore or other tax consequences of the acquisition, ownership of or disposal of the Notes, including, in particular, the effect of any foreign, state or local tax laws to which they are subject. It is emphasised that none of the Issuer, the Joint Lead Managers and any other persons involved in the issue of the Notes accepts responsibility for any tax effects or liabilities resulting from the subscription for, purchase, holding or disposal of the Notes. 1. Interest and Other Payments Australia and New Zealand Banking Group Limited, Barclays Bank PLC, Singapore Branch, The Hongkong and Shanghai S-10

15 Banking Corporation Limited, Singapore Branch, Mizuho Securities Asia Limited and MUFG Securities EMEA plc are the distributors of the Notes. Australia and New Zealand Banking Group Limited, Barclays Bank PLC, Singapore Branch and The Hongkong and Shanghai Banking Corporation Limited, Singapore Branch are each a Financial Sector Incentive (Standard Tier) Company for the purposes of the Income Tax Act (Chapter 134 of Singapore) (the Income Tax Act). As the Notes are issued on or before 31 December 2018 and if more than half of the Notes are distributed by a Financial Sector Incentive (Capital Market) Company, a Financial Sector Incentive (Standard Tier) Company or a Financial Sector Incentive (Bond Market) Company, each as defined under the Income Tax Act, the Notes would be qualifying debt securities and subject to certain conditions having been fulfilled (including the furnishing of a return on debt securities in respect of the Notes in the prescribed format within such period as the relevant authorities may specify to the MAS), interest, discount income (not including discount income arising from secondary trading), prepayment fee, redemption premium and break cost (collectively, the Qualifying Income) from the Notes derived by any company or body of persons (as defined in the Income Tax Act) in Singapore is subject to income tax at a concessionary rate of 10 per cent. (except for holders of the relevant Financial Sector Incentive(s) who may be taxed at different rates). However, notwithstanding the foregoing: (A) if during the primary launch of the Notes, the Notes are issued to less than four persons and 50 per cent. or more of the issue of such Notes is beneficially held or funded, directly or indirectly, by related parties of the Issuer, such Notes would not qualify as qualifying debt securities ; and (B) even though the Notes are qualifying debt securities, if, at any time during the tenure of such Notes, 50 per cent. or more of the issue of such Notes is held beneficially or funded, directly or indirectly, by any related party(ies) of the Issuer, Qualifying Income derived from such Notes held by: (i) (ii) any related party of the Issuer; or any other person where the funds used by such person to acquire such Notes are obtained, directly or indirectly, from any related party of the Issuer, shall not be eligible for the concessionary rate of tax as described above. The term related party, in relation to a person, means any other person who, directly or indirectly, controls that person, or is controlled, directly or indirectly, by that person, or where he and that other person, directly or indirectly, are under the control of a common person. For the purposes of the Income Tax Act and this Singapore tax disclosure: (a) (b) (c) break cost means any fee payable by the issuer of the securities on the early redemption of the securities, the amount of which is determined by any loss or liability incurred by the holder of the securities in connection with such redemption; prepayment fee means any fee payable by the issuer of the securities on the early redemption of the securities, the amount of which is determined by the terms of the issuance of the securities; and redemption premium means any premium payable by the issuer of the securities on the redemption of the securities upon their maturity. All foreign-sourced income received in Singapore on or after January 1, 2004 by Singapore tax-resident individuals will be exempt from income tax, provided such foreign-sourced income is not received through a partnership in Singapore. Any person whose interest, discount income, prepayment fee, redemption premium or break cost derived from the Notes is S-11

16 not exempt from Singapore income tax shall include such income in a return of income made under the Income Tax Act. 2. Capital Gains Any gains considered to be in the nature of capital made from the sale of the Notes will not be taxable in Singapore. However, any gains derived by any person from the sale of the Notes which are gains from any trade, business, profession or vocation carried on by that person, if accruing in or derived from Singapore, may be taxable as such gains are considered revenue in nature. Holders of the Notes who apply or are required to apply Singapore Financial Reporting Standard 39 Financial Instruments: Recognition and Measurement (FRS 39) or FRS 109 Financial Instruments (FRS 109) may, for Singapore income tax purposes be required to recognise gains or losses (not being gains or losses in the nature of capital) on the Notes, irrespective of disposal, in accordance with FRS 39 or FRS 109. Please see the section below on Adoption of FRS 39 and FRS 109 Treatment for Singapore income tax purposes. 3. Adoption of FRS 39 and FRS 109 for Singapore income tax purposes Section 34A of the Income Tax Act provides for the tax treatment for financial instruments in accordance with FRS 39 (subject to certain exceptions and opt-out provisions) to taxpayers who are required to comply with FRS 39 for financial reporting purposes. The IRAS has also issued a circular entitled Income Tax Implications Arising from the Adoption of FRS 39 Financial Instruments: Recognition and Measurement and an etaxguide entitled "Income Tax : Income Tax Treatment Arising from Adoption of FRS 109 Financial Instruments". FRS 109 is mandatorily effective for annual periods beginning on or after 1 January 2018, replacing FRS 39. Section 34AA of the Income Tax Act requires taxpayers who comply or who are required to comply with FRS 109 for financial reporting purposes to calculate their profit, loss or expense for Singapore income tax purposes in respect of financial instruments in accordance with FRS 109, subject to certain exceptions. The "opt-out" provisions available under the FRS 39 tax regime will not be similarly available under the new FRS 109 tax regime. Holders of the Notes who may be subject to the tax treatment under Section 34A or 34AA of the Income Tax Act should consult their own accounting and tax advisers regarding the Singapore income tax consequences of their acquisition, holding or disposal of the Notes. 4. Estate Duty Singapore estate duty has been abolished with respect to all deaths occurring on or after 15 February 2008 S-12

17 THE ISSUER Rural Electrification Corporation Limited Core-4, SCOPE Complex 7, Lodhi Road New Delhi India LEGAL ADVISERS To the Joint Lead Managers as to English law Allen & Overy 9th Floor Three Exchange Square Central Hong Kong To the Issuer as to Indian law ZBA 412 Raheja Chambers 213 Nariman Point Mumbai India JOINT LEAD MANAGERS Australia and New Zealand Banking Group Limited 10 Collyer Quay #21-00 Ocean Financial Centre Singapore The Hongkong and Shanghai Banking Corporation Limited, Singapore Branch 21 Collyer Quay, #10-01 HSBC Building Singapore Barclays Bank PLC, Singapore Branch 10 Marina Boulevard #24-01 Marina Bay Financial Centre Tower 2 Singapore Mizuho Securities Asia Limited 14-15/F, K11 Atelier 18 Salisbury Road Tsim Sha Tsui, Kowloon Hong Kong MUFG Securities EMEA plc Ropemaker Place 25 Ropemaker Street London EC2Y 9AJ United Kingdom AUDITORS G.S. Mathur & Co. Chartered Accountants A-160, Defence Colony New Delhi India A.R. & Co. Chartered Accountants A-403, Gayatri Apartments Plot No. 27, Sector-10, Dwarka New Delhi India S-13

18 RURAL ELECTRIFICATION CORPORATION LIMITED S-14

19 ANNEX A OFFERING CIRCULAR DATED 28 FEBRUARY 2018

20 IMPORTANT NOTICE NOT FOR DISTRIBUTION TO ANY PERSON OR ADDRESS IN THE UNITED STATES IMPORTANT: You must read the following before continuing. The following applies to the offering circular (the Offering Circular) following this page, and you are therefore advised to read this carefully before reading, accessing or making any other use of the Offering Circular. In accessing the Offering Circular, you agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from us as a result of such access. NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER OF SECURITIES FOR SALE IN THE UNITED STATES OR ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. THE SECURITIES HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE SECURITIES ACT), OR THE SECURITIES LAWS OF ANY STATE OF THE U.S. OR OTHER JURISDICTION AND THE SECURITIES MAY NOT BE OFFERED OR SOLD WITHIN THE UNITED STATES OR, IN CERTAIN CIRCUMSTANCES, TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS (AS DEFINED IN REGULATION S UNDER THE SECURITIES ACT), EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIES LAWS. THE OFFERING CIRCULAR MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER, AND IN PARTICULAR, MAY NOT BE FORWARDED TO ANY U.S. ADDRESS OR, IN CERTAIN CIRCUMSTANCES, TO ANY U.S. PERSON. ANY FORWARDING, DISTRIBUTION OR REPRODUCTION OF THIS DOCUMENT IN WHOLE OR IN PART IS UNAUTHORISED. FAILURE TO COMPLY WITH THIS DIRECTIVE MAY RESULT IN A VIOLATION OF THE SECURITIES ACT OR THE APPLICABLE LAWS OF OTHER JURISDICTIONS. Confirmation of your Representation: The Offering Circular is being sent at your request and by accepting the and accessing the Offering Circular, you shall be deemed to have represented to us that the electronic mail address that you gave us and to which this has been delivered is not located in the United States and that you consent to delivery of such offering circular by electronic transmission. You are reminded that the Offering Circular has been delivered to you on the basis that you are a person into whose possession the Offering Circular may be lawfully delivered in accordance with the laws of jurisdiction in which you are located and you may not, nor are you authorised to, deliver the offering circular to any other person. The materials relating to any offering of securities described in the Offering Circular do not constitute, and may not be used in connection with, an offer or solicitation in any place where offers or solicitations are not permitted by law. If a jurisdiction requires that the offering be made by a licensed broker or dealer and the underwriters or any affiliate of the underwriters is a licensed broker or dealer in that jurisdiction, the offering shall be deemed to be made by the underwriters or such affiliate on behalf of our Company in such jurisdiction. The Offering Circular has been sent to you in an electronic form. You are reminded that documents transmitted via this medium may be altered or changed during the process of electronic transmission and consequently the Dealers (as defined in the Offering Circular), nor any person who controls each of them nor any director, officer, employee nor agent of each of them or affiliate of any such person, do not accept any liability or responsibility whatsoever in respect of any difference between the Offering Circular distributed to you in electronic format and the hard copy version available to you on request from the Dealer. The Offering Circular has not been and will not be registered, produced or made available to all as an offer document (whether a prospectus in respect of a public offer or an information memorandum or private placement offer letter or other offering material in respect of any private placement under the Companies Act, 2013 or any other applicable Indian laws) with the Registrar of Companies of India or the SEBI or any other statutory or regulatory body of like nature in India. In addition, holders and beneficial owners shall be responsible for compliance with restrictions on the ownership of the Rupee Denominated Notes imposed from time to time by applicable laws or by any regulatory authority or otherwise. In this context, holders and beneficial owners of Rupee Denominated Notes shall be deemed to have acknowledged, represented and agreed that such holders and beneficial owners are eligible to purchase the Rupee Denominated Notes under applicable laws and regulations and are not prohibited under any applicable law or regulation from acquiring, owning or selling the Rupee Denominated Notes. Potential investors should seek independent advice and verify compliance with Financial Action Task Force (FATF) Requirements prior to any purchase of the Rupee Denominated Notes. Multilateral financial institutions and regional financial institutions from FATF compliant countries can purchase Rupee Denominated Notes. The holders and beneficial owners of Rupee Denominated Notes shall be deemed to confirm that for so long as they hold any Rupee Denominated Notes, they will meet the FATF Requirements and will not be an offshore branch of an Indian bank. Further, all Noteholders represent and agree that the Rupee Denominated Notes will not be offered or sold on the secondary market to any person who does not comply with the FATF Requirements or which is an offshore branch of an Indian bank.

21 You are responsible for protecting against viruses and other destructive items. Your use of this is at your own risk and it is your responsibility to take precautions to ensure that it is free from viruses and other items of a destructive nature.

22 OFFERING CIRCULAR Rural Electrification Corporation Limited (incorporated with limited liability in the Republic of India) U.S.$3,000,000,000 Medium Term Note Programme Under this U.S.$3,000,000 Medium Term Note Programme (the Programme), Rural Electrification Corporation Limited (our Company) may from time to time issue notes (the Notes) denominated in any currency agreed between us and the relevant Dealer (as defined below). Notes may be issued in bearer or registered form (respectively, Bearer Notes and Registered Notes). The maximum aggregate nominal amount of all Notes from time to time outstanding under the Programme will not exceed U.S.$3,000,000,000 (or its equivalent in other currencies calculated as described herein), subject to increase as described herein. The Notes may be issued on a continuing basis to one or more of the Dealers specified under Summary of the Programme and any additional Dealer appointed under the Programme from time to time by us (each a Dealer and together the Dealers), which appointment may be for a specific issue or on an on-going basis. References in this Offering Circular to the relevant Dealer shall, in the case of an issue of Notes being (or intended to be) subscribed by more than one Dealer, be to all Dealers agreeing to subscribe to such Notes. Approval-in-principle has been granted for the listing and quotation of Notes that may be issued pursuant to the Programme and which are agreed at or prior to the time of issue thereof to be so listed on the Singapore Exchange Securities Trading Limited (the SGX-ST). Such permission will be granted when such Notes have been admitted to the Official List of the SGX-ST (the Official List). The SGX-ST assumes no responsibility for the correctness of any of the statements made or opinions expressed or reports contained herein. Admission to the Official List and quotation of any Notes on the SGX-ST are not to be taken as an indication of our merits, the Programme or the Notes. Notice of the aggregate nominal amount of Notes, interest (if any) payable in respect of Notes, the issue price of Notes and any other terms and conditions not contained herein which are applicable to each Tranche (as defined under Terms and Conditions of the Notes ) of Notes will be set out in a pricing supplement (the Pricing Supplement) which, with respect to Notes to be listed on the SGX-ST, will be delivered to the SGX-ST on or before the date of issue of the Notes of such Tranche. The Programme provides that Notes may be listed on such other or further stock exchange(s) as may be agreed between us and the relevant Dealer. We may also issue unlisted Notes. We may agree with any Dealer and the Principal Paying Agent (as defined herein) that Notes may be issued in a form not contemplated by the Terms and Conditions of the Notes herein, in which event (in the case of Notes intended to be listed on the SGX-ST) a supplementary Offering Circular, if appropriate, will be made available which will describe the effect of the agreement reached in relation to such Notes. See Risk Factors for a discussion of certain factors to be considered in connection with an investment in the Notes. Notes to be listed on the SGX-ST will be accepted for clearance through Euroclear Bank SA/NV (Euroclear) and Clearstream Banking S.A. (Clearstream, Luxembourg). Each Tranche of Bearer Notes of each series (as defined in Form of the Notes ) will initially be represented by either a temporary bearer global note (a Temporary Bearer Global Note) or a permanent bearer global note (a Permanent Bearer Global Note and, together with a Temporary Bearer Global Note, the Bearer Global Notes, and each a Bearer Global Note) as indicated in the applicable Pricing Supplement, which, in either case, will be delivered on or prior to the original issue date of the Tranche to a common depositary (the Common Depositary) for Euroclear and Clearstream, Luxembourg. On and after the date (the Exchange Date) which, for each Tranche in respect of which a Temporary Bearer Global Note is issued, is 40 days after the Temporary Bearer Global Note is issued, interests in such Temporary Bearer Global Note will be exchangeable (free of charge) upon a request as described therein either for (i) interests in a Permanent Bearer Global Note of the same Series or (ii) definitive Bearer Notes of the same Series. Registered Notes sold in an offshore transaction within the meaning of Regulation S (Regulation S) under the U.S. Securities Act of 1933, as amended (the Securities Act), which will be sold outside the United States (the U.S.) and, in certain circumstances, only to non-u.s. persons (as defined in Regulation S), will initially be represented by a global note in registered form, without receipts or coupons, (a Registered Global Note) deposited with a common depositary for Euroclear and Clearstream, Luxembourg, and registered in the name of a nominee of such common depositary. Prior to expiry of the distribution compliance period (as defined in Regulation S) (the Distribution Compliance Period) (if any) applicable to each Tranche of Notes, beneficial interests in a Registered Global Note may not be offered or sold to, or for the account or benefit of, a U.S. person, save as otherwise provided in the Terms and Conditions of the Notes and may not be held otherwise than through Euroclear or Clearstream, Luxembourg. The applicable Pricing Supplement will specify that a Permanent Bearer Global Note will be exchangeable for definitive Bearer Notes in certain limited circumstances. This Offering Circular has not been and will not be registered as a prospectus or a statement in lieu of a prospectus in respect of a public offer, information memorandum or private placement offer letter or any other offering material with the Registrar of Companies in India in accordance with the Companies Act, 1956, as amended and replaced from time to time, the Companies Act, 2013, as amended and other applicable Indian laws for the time being in force. This Offering Circular has not been and will not be reviewed or approved by any regulatory authority in India, including, but not limited to, the Securities and Exchange Board of India, any Registrar of Companies or any stock exchange in India. This Offering Circular and the Notes are not and should not be construed as an advertisement, invitation, offer or sale of any securities whether to the public or by way of private placement to any person resident in India. The Notes have not been and will not be, offered or sold to any person resident in India. If you purchase any of the Notes, you will be deemed to have acknowledged, represented and agreed that you are eligible to purchase the Notes under applicable laws and regulations and that you are not prohibited under any applicable law or regulation from acquiring, owning or selling the Notes. See Subscription and Sale. The Notes have not been and will not be registered under the U.S. Securities Act of 1933, as amended (the Securities Act) or with any securities regulatory authority of any state or other jurisdiction of the United States and are subject to U.S. tax law requirements. Subject to certain exceptions, the Notes may not be offered, sold or delivered within the United States or, in certain circumstances, to U.S. persons (as defined in Regulation S under the Securities Act). See Subscription and Sale. Joint Arrangers Barclays MUFG Dealers Barclays MUFG The date of this Offering Circular is 28 February 2018.

23 We accept responsibility for the information contained in this Offering Circular. To the best of our knowledge and belief (having taken all reasonable care to ensure that such is the case) the information contained in this Offering Circular is in accordance with the facts and does not omit anything that would make the statements therein, in light of the circumstances under which they were made, misleading. We, having made all reasonable enquiries, confirm that this Offering Circular contains or incorporates all information which is material in the context of the Programme and the Notes, that the information contained or incorporated in this Offering Circular is true and accurate in all material respects and is not misleading, that the opinions and intentions expressed in this Offering Circular are honestly held and that there are no other facts the omission of which would make this Offering Circular or any of such information or the expression of any such opinions or intentions misleading. We accept responsibility accordingly. No person is or has been authorised by us to give any information or to make any representation other than those contained in this Offering Circular or any other information supplied in connection with the Programme or the Notes and, if given or made by any other person, such information or representations must not be relied upon as having been authorised by us, the Joint Arrangers, the Dealers or the Principal Paying Agent. Neither the Joint Arrangers, the Dealers nor the Principal Paying Agent (as defined herein) has separately verified the information contained herein. Accordingly, no representation, warranty or undertaking, express or implied, is made and, to the fullest extent permitted by law, no responsibility or liability is accepted by the Joint Arrangers or the Dealers, the Principal Paying Agent or any of them as to the accuracy or completeness of the information contained or incorporated in this Offering Circular, or for any other statement, made or purported to be made by the Joint Arrangers or the Dealers or on their behalf in connection with us or the Programme or any other information provided by us in connection with the Programme. The Joint Arrangers, the Dealers and the Principal Paying Agent accordingly disclaim all and any liability whether arising in tort or contract or otherwise (save as referred to above) which they might otherwise have in respect of this Offering Circular or any such statement. Neither this Offering Circular nor any other information supplied in connection with the Programme or any Notes (i) is intended to provide the basis of any credit or other evaluation or (ii) should be considered as a recommendation by us, the Joint Arrangers or the Dealers or the Principal Paying Agent that any recipient of this Offering Circular or any other information supplied in connection with the Programme or any Notes should purchase any of the Notes. Each investor contemplating purchasing Notes should make its own independent investigation of the financial condition and affairs, and its own appraisal of the creditworthiness, of us. Neither this Offering Circular nor any other information supplied in connection with the Programme or the issue of any Notes constitutes an offer or invitation by or on behalf of our Company, the Joint Arrangers or the Dealers or the Principal Paying Agent to any person to subscribe for or to purchase any Notes. Neither the delivery of this Offering Circular nor the offering, sale or delivery of any Notes shall in any circumstances imply that the information contained herein concerning us is correct at any time subsequent to the date hereof or that any other information supplied in connection with the Programme is correct as of any time subsequent to the date indicated in the document containing the same. The Joint Arrangers, the Dealers and the Principal Paying Agent expressly do not undertake to review the financial condition or affairs of our Company during the life of the Programme or to advise any investor in the Notes of any information coming to their attention. Investors should review, inter alia, the most recently published documents incorporated by reference into this Offering Circular when deciding whether or not to purchase any Notes. MiFID II product governance/target market The Pricing Supplement in respect of any Notes may include a legend entitled "MiFID II Product Governance", which will outline the target market assessment in respect of the Notes and which channels for distribution of the Notes are appropriate. Any person subsequently offering, selling or recommending the Notes (a distributor) should take into consideration the target market assessment; however, a distributor subject to Directive 2014/65/EU (as amended, MiFID II) is responsible for undertaking its own target market assessment in respect of the Notes (by either adopting or refining the target market assessment) and determining appropriate distribution channels. ii

24 A determination will be made in relation to each issue about whether, for the purpose of the MiFID Product Governance rules under EU Delegated Directive 2017/593 (the MiFID Product Governance Rules), any Dealer subscribing for any Notes is a manufacturer in respect of such Notes, but otherwise neither the Joint Arrangers nor the Dealers nor any of their respective affiliates will be a manufacturer for the purpose of the MiFID Product Governance Rules. IMPORTANT EEA RETAIL INVESTORS If the Pricing Supplement in respect of any Notes includes a legend entitled "Prohibition of Sales to EEA Retail Investors", the Notes are not intended to be offered, sold or otherwise made available to and should not be offered, sold or otherwise made available to any retail investor in the European Economic Area (EEA). For these purposes, a retail investor means a person who is one (or more) of: (i) a retail client as defined in point (11) of Article 4(1) of MiFID II; (ii) a customer within the meaning of Directive 2002/92/EC (as amended, the Insurance Mediation Directive), where that customer would not qualify as a professional client as defined in point (10) of Article 4(1) of MiFID II; or (iii) not a qualified investor as defined in Directive 2003/71/EC (as amended, the Prospectus Directive). Consequently no key information document required by Regulation (EU) No 1286/2014 (as amended, the PRIIPs Regulation) for offering or selling the Notes or otherwise making them available to retail investors in the EEA has been prepared and therefore offering or selling the Notes or otherwise making them available to any retail investor in the EEA may be unlawful under the PRIIPs Regulation. This Offering Circular does not constitute an offer to sell or the solicitation of an offer to buy any Notes in any jurisdiction to any person to whom it is unlawful to make the offer or solicitation in such jurisdiction. The distribution of this Offering Circular and the offer or sale of Notes may be restricted by law in certain jurisdictions. Our Company, the Joint Arrangers, the Dealers and the Principal Paying Agent do not represent that this Offering Circular may be lawfully distributed, or that any Notes may be lawfully offered, in compliance with any applicable registration or other requirements in any such jurisdiction, or pursuant to an exemption available thereunder, or assume any responsibility for facilitating any such distribution or offering. In particular, no action has been taken by our Company, the Joint Arrangers, the Dealers or the Principal Paying Agent which would permit a public offering of any Notes or distribution of this Offering Circular in any jurisdiction where action for that purpose is required. Accordingly, no Notes may be offered or sold, directly or indirectly, and neither this Offering Circular nor any advertisement or other offering material may be distributed or published in any jurisdiction, except under circumstances that will result in compliance with any applicable laws and regulations. Persons into whose possession this Offering Circular or any Notes may come must inform themselves about, and observe, any such restrictions on the distribution of this Offering Circular and the offering and sale of Notes. In particular, there are restrictions on the distribution of this Offering Circular and the offer or sale of Notes in the United States, the European Economic Area (including the United Kingdom, Italy and the Netherlands), India, Singapore, Japan and Hong Kong, see Subscription and Sale. None of our Company, the Joint Arrangers, the Dealers and the Principal Paying Agent makes any representation to any investor in the Notes regarding the legality of its investment under any applicable laws. Any investor in the Notes should be able to bear the economic risk of an investment in the Notes for an indefinite period of time. There are restrictions on the offer and sale of the Notes in the United Kingdom. All applicable provisions of the Financial Services and Market Act 2000 (FSMA) with respect to anything done by any person in relation to the Notes in, from or otherwise involving the United Kingdom must be complied with. See Subscription and Sale. In connection with the offering of any series of Notes, each Dealer is acting or will act for us in connection with the offering and will not be responsible to anyone other than us for providing the protections afforded to clients of that Dealer nor for providing advice in relation to any such offering. For a description of other restrictions, see Subscription and Sale. iii

25 PRESENTATION OF FINANCIAL AND OTHER INFORMATION We maintain our financial books and records and prepare our financial statements in Rupees in accordance with generally accepted accounting principles in the Republic of India (Indian GAAP) which differ in certain important respects from International Financial Reporting Standards (IFRS). For a discussion of the principal differences between Indian GAAP and IFRS as they relate to us, see Summary of Significant Differences Between Indian GAAP And IFRS. Unless otherwise stated, all financial data contained herein is that of our Company on a non-consolidated basis. The consolidated and nonconsolidated financial statements for the years ended 31 March 2015, 2016 and 2017 and the financial statements for the nine months ended 31 December 2017, on a non-consolidated basis, included in this Offering Circular have been audited or reviewed as appropriate, by the auditors as set out in paragraph 7 of the section entitled General Information. iv

26 CERTAIN DEFINITIONS In this Offering Circular, references to India are to the Republic of India, references to the Government or GoI are to the Government of India and references to the RBI are to the Reserve Bank of India. References to specific data applicable to particular subsidiaries or other consolidated entities are made by reference to the name of that particular entity. References to Fiscal or Fiscal Year are to the year ended March 31. Unless the context otherwise indicates, all references to the Issuer, REC, our Company or the Company are to Rural Electrification Corporation Limited on a non-consolidated basis. Industry and market share data in this Offering Circular are derived from data prepared by the Central Electricity Authority (the CEA) which is the nodal government agency for planning, advising and monitoring the Indian power sector, the Ministry of Power, the Government of India (the MoP), the Planning Commission of India and from industry publications. Industry publications generally state that the information contained in those publications has been obtained from sources believed to be reliable but that their accuracy and completeness are not guaranteed and their reliability cannot be assured. Although we believe that the industry data used in this Offering Circular is reliable and take responsibility for the accurate extraction of such data from publicly available sources, it has not been independently verified by us, the Joint Arrangers, the Dealers or the Principal Paying Agent. As used in this Offering Circular, the terms, 10th Plan, 11th Plan, 12th Plan and 13th Plan refer to the five-year plans of the Government, and mean the Tenth Five Year Plan covering the period fiscal , the Eleventh Five Year Plan covering the period fiscal , the Twelfth Five Year Plan covering the period and the Thirteenth Five Year Plan covering the period , respectively. All references in this Offering Circular to U.S. dollars, U.S.$ and USD refer to United States dollars, to Rupee, Rupees, Rs. and refer to Indian Rupees and to SGD refers to Singapore dollars. In addition, references to Sterling refers to pounds sterling and to euro, EUR and refer to the currency introduced at the start of the third stage of European economic and monetary union pursuant to the Treaty on the Functioning of the European Community, as amended. References to lakhs and crores in our financial statements are to the following: One lakh... One crore... Ten crores... One hundred crores ,000 (one hundred thousand) 10,000,000 (ten million) 100,000,000 (one hundred million) 1,000,000,000 (one thousand million or one billion) In this Offering Circular, where information has been presented in millions or billions of units, amounts may have been rounded, in the case of information presented in millions, to the nearest ten thousand or one hundred thousand units or, in the case of information presented in billions, one, ten or one hundred million units. Accordingly, the totals of columns or rows of numbers in tables may not be equal to the apparent total of the individual items and actual numbers may differ from those contained herein due to rounding. v

27 FORWARD-LOOKING STATEMENTS We have included statements in this Offering Circular which contain words or phrases such as will, would, aimed, is likely, are likely, believe, expect, expected to, will continue, will achieve, anticipate, estimate, intend, plan, contemplate, seek to, seeking to, target, propose to, future, objective, goal, projected, should, can, could, may and similar expressions or variations of such expressions, that are forward-looking statements. Actual results may differ materially from those suggested by the forward-looking statements due to certain risks or uncertainties associated with our expectations with respect to, but not limited to, regulatory changes relating to the power sector in India and our ability to respond to them, our ability to successfully implement our strategy, our growth and expansion, including our ability to complete our capacity expansion plans, technological changes, our exposure to market risks, general economic and political conditions in India which have an impact on our business activities or investments, the monetary and fiscal policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices or other rates or prices, the performance of the financial markets in India and globally, changes in domestic and foreign laws, regulations and taxes and changes in competition in the our industry. For a further discussion on the factors that could cause actual results to differ, see the discussion under Risk Factors contained in this Offering Circular. vi

28 ENFORCEMENT OF FOREIGN JUDGMENTS IN INDIA Our Company is a limited liability public company incorporated under the laws of India. All of our directors and executive officers named herein are residents of India and all or a substantial portion of our assets and such persons are located in India. As a result, it may not be possible for investors to effect service of process on us or such persons in jurisdictions outside of India, or to enforce against it judgments obtained in courts outside of India predicated upon civil liabilities of our Company or such directors and executive officers under laws other than Indian law. India is not a signatory to any international treaty in relation to the recognition or enforcement of foreign judgments. The statutory basis for recognition and enforcement of foreign judgments is provided for under section 13 and section 44A of the Indian Code of Civil Procedure, 1908 as amended (the Civil Code). Section 13 of the Civil Code provides that a foreign judgment shall be conclusive as to any matter thereby directly adjudicated upon except: (i) where it has not been pronounced by a court of competent jurisdiction; (ii) where it has not been given on the merits of the case; (iii) where it appears on the face of the proceedings to be founded on an incorrect view of international law or a refusal to recognise the law of India in cases where such law is applicable; (iv) where the proceedings in which the judgment was obtained were opposed to natural justice; (v) where it has been obtained by fraud; or (vi) where it sustains a claim founded on a breach of any law in force in India. Section 44A of the Civil Code provides that where a foreign judgment has been rendered by a superior court (as defined in such section) in any country or territory outside India which the GOI has by notification declared to be a reciprocating territory, it may be enforced in India by proceedings in execution as if the judgment had been rendered by the relevant court in India. Under the Civil Code, a court in India will upon the production of any document purporting to be a certified copy of a foreign judgment, presume that the judgment was pronounced by a court of competent jurisdiction, unless the contrary appears on record but such presumption may be displaced by proving want of jurisdiction. However, section 44A of the Civil Code is applicable only to monetary decrees not being in the nature of any amounts payable in respect of taxes or other charges of a like nature or in respect of a fine or other penalty and is not applicable to arbitration awards, even if such awards are enforceable as a decree or judgment. The United Kingdom has been declared by the GOI to be a reciprocating territory and the High Courts in England as the relevant superior courts for the purposes of section 44A of the Civil Code. Accordingly, a judgment of a superior court in the United Kingdom may be enforceable by proceedings in execution, and a judgment not of a superior court, by a new suit resulting in a judgment or order. The United States has not been declared by the GOI to be a reciprocating territory for the purposes of section 44A of the Civil Code. Accordingly, a judgment by a court in the United States may be enforced only by a new suit upon the judgment and not by proceedings in execution. The suit must be brought in India within three years from the date of the judgment in the same manner as any other suit filed to enforce a civil liability in India. It is unlikely that a court in India would award damages on the same basis as a foreign court if an action is brought in India. Furthermore, it is unlikely that an Indian court would enforce a foreign judgment if it viewed the amount of damages awarded as excessive or inconsistent with Indian practice. A party seeking to enforce a foreign judgment in India is required to obtain approval from the RBI under the Foreign Exchange Management Act, 1999 to repatriate outside India any amount recovered pursuant to execution. Any judgment in a foreign currency would be converted into Rupees on the date of the judgment and not on the date of the payment. Also, a party may file suit in India against our Company, our directors or our executive officers as an original action predicated upon the provisions of the federal securities laws in the United States. vii

29 GLOSSARY OF TERMS USED IN THIS OFFERING CIRCULAR Below are certain terms used in this Offering Circular. Company-related terms the Company/our Company/REC... we/us/our... Articles/Articles of Association... Board/Board of Directors... Shares... Memorandum/ Memorandum of Association... Rural Electrification Corporation Limited, a public limited company incorporated under the Companies Act, The corporate identification number of our Company is L40101DL1969GOI Our Company together with our subsidiaries, associates and our joint venture on a consolidated basis Articles of Association of our Company as amended from time to time Board of Directors of our Company unless otherwise specified Equity Shares of our Company of the face value of 10 each unless otherwise specified Memorandum of Association of our Company as amended from time to time Conventional and General Terms or Abbreviations or Rs. or Rupees... Indian Rupees (the lawful currency of India) $ or US$ or U.S.$ or USD... United States dollar (the lawful currency of the United States of America) or Euro or EUR... Euro (the official and lawful currency of European Union, which consists of 19 of the 28 member states i.e. Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, the Netherlands, Portugal, Slovakia, Slovenia, and Spain) Companies Act... AGM... AS... Bankruptcy Code... BPL... BSE... CARE... CBDT... CEO... Companies Act, 2013, as amended Additional General Manager Accounting Standards as notified under the Companies Act and as applicable to the Company The Insolvency and Bankruptcy Code, 2016, as amended Below Poverty Line BSE Limited CARE Ratings Central Board of Direct Taxes Chief Executive Officer viii

30 CERC... CGSL... CHF... CoR... CPSE... CPSU... CPUs... CRAR... CRISIL... CSPDCL... CSR... DDG... Debt Recovery Act... Central Electricity Regulatory Commission Classic Global Securities Limited Swiss franc (the currency and legal tender of Switzerland and Liechtenstein) Certificate of Registration Central Public Sector Enterprise Central Public Sector Undertaking Central Power Utilities Capital to Risk Weighted Assets Ratio CRISIL Limited Chhattisgarh State Power Distribution Company Limited Corporate Social Responsibility Decentralised Distributed Generation The Recovery of Debts Due to Banks and Financial Institutions Act, 1993, as amended Depositories Act... The Depositories Act, 1996 Depository(ies)... DIN... DPE... DRT... DSIJ... EESL... ERP... ESCOs... F&A... FDI... FEMA... FII... CDSL and NSDL Director Identification Number Department of Public Enterprises, Ministry of Heavy Industries & Public Enterprises Debt Recovery Tribunal Dalal Street Investment Journal Energy Efficiency Services Limited Enterprise Resource Planning Energy Service Companies Finance and Accounts Foreign Direct Investment Foreign Exchange Management Act, 1999, as amended Foreign Institutional Investor ix

31 FIMMDA... Fin... Financial Year/Fiscal/FY... GDP... Gen... GST Act... GoI or Government... HDFC... HR... HRM... HVDS... IA... ICRA... IEX... Fixed Income Money Market and Derivative Association of India Finance Period of 12 months ended 31 March of that particular year Gross Domestic Product Generation The Good and Services Tax Act, 2017, as amended Government of India HDFC Bank Limited Human Resources Human Resource Management High Voltage Distribution Systems Internal Audit ICRA Limited Indian Energy Exchange Limited Income Tax Act/IT Act... Income Tax Act, 1961 India... Indian GAAP... IPO... IRDA... IREDA... IRRPL... IT... ITAT... JICA... KfW... kv... kwh... Republic of India Generally accepted accounting principles followed in India Initial Public Offer Insurance Regulatory and Development Authority Indian Renewable Energy Development Agency Limited India Ratings and Research Private Limited Information Technology Income Tax Appellate Tribunal Japan International Cooperation Agency Kreditanstalt fur Wiederaufbau Kilo Volt kilowatt hour x

32 KYC... LIBOR... LIC... Listing Agreement... MCA... MoF... MoP... MoU... MTL... NBFC... NBFC-ND... NBFC-ND-SI... NEF... NRI... NSE... NTP... PAT... PFC... PGCIL... PSE... RBI... RECPDCL... RECTPCL... RGGVY... Know Your Customer London Inter-Bank Offer Rate Life Insurance Corporation of India The agreement for listing of equity and debt securities on the Stock Exchange Ministry of Corporate Affairs, Government of India Ministry of Finance, Government of India Ministry of Power, Government of India Memorandum of Understanding Medium Term Loan Non-Banking Financial Company, as defined under applicable RBI guidelines Non-Deposit Taking NBFC Systemically Important Non-Deposit Taking NBFC National Electricity Fund Non-Resident Indians i.e. a Person resident outside India, as defined under FEMA, and who is a citizen of India or a Person of Indian origin and such term as defined under the Foreign Exchange Management (Transfer or Issue of Security by a Person Resident Outside India) Regulations, 2000, as amended National Stock Exchange of India Limited National Tariff Policy Profit After Tax Power Finance Corporation Limited Power Grid Corporation of India Limited Public Sector Enterprise Reserve Bank of India REC Power Distribution Company Limited REC Transmission Projects Company Limited Rajeev Gandhi Grameen Vidyutikaran Yojna xi

33 RMC... RoC... RTI... SARFAESI/Securitisation Act... SBF... SBI... SEBI... SEBI Debt Regulations... SLR Bonds... STL... STUs... T&D... TFL... u/s... UCX... USA... Risk Management Committee Registrar of Companies, National Capital Territory of Delhi and Haryana Right to Information Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002, as amended Small is Beautiful Fund State Bank of India Securities and Exchange Board of India SEBI (Issue and Listing of Debt Securities) Regulations, 2008, as amended Bonds that qualify under statutory liquidity ratio to be maintained by banks/other institutions as prescribed by the RBI from time to time Short Term Loan State Transmission Utilities Transmission and Distribution Transitional Finance Loan under Section Universal Commodity Exchange Limited United States of America Business/Industry-Related Terms ADB... ALCO... APDRP... AT&C... CAGR... CEA... CIRE... CKms... Asian Development Bank Asset Liability Management Committee Accelerated Power Development and Reform Programme Aggregate Technical and Commercial Compounded Annual Growth Rate Central Electricity Authority Central Institute for Rural Electrification Corporation Circuit Kilometres xii

34 DISCOM/Discom... DPE... DDUGJY... ECBs... GENCO... IFC... IPP... ISO... ITP... MNRE... MW... NHPC... NPAs... NTPC... PSU... PV... R-APDRP... SEB(s)... SERC... SPU... SPV... TRANSCO... UMPP... Distribution Company Department of Public Enterprises, Government of India Deen Dayal Upadhaya Gram Jyoti Yojana External Commercial Borrowings Generation Company Infrastructure Finance Company Independent Power Producer International Organization for Standardization Independent Transmission Project(s) Ministry of New and Renewable Energy Mega Watts NHPC Limited Non-Performing Assets NTPC Limited Public Sector Undertaking Photovoltaic Restructured Accelerated Power Development and Reform Programme State Electricity Boards State Electricity Regulatory Commission State Power Utility(ies) Special Purpose Vehicle Transmission Company Ultra Mega Power Project xiii

35 CONTENTS Page DOCUMENTS INCORPORATED BY REFERENCE... 1 GENERAL DESCRIPTION OF THE PROGRAMME... 2 SUMMARY OF THE PROGRAMME... 3 FORM OF PRICING SUPPLEMENT TERMS AND CONDITIONS OF THE NOTES USE OF PROCEEDS CAPITALISATION RISK FACTORS BUSINESS ASSETS AND LIABILITIES MANAGEMENT INDUSTRY OVERVIEW REGULATIONS AND POLICIES TAXATION SUBSCRIPTION AND SALE SUMMARY OF SIGNIFICANT DIFFERENCES BETWEEN INDIAN GAAP AND IFRS GENERAL INFORMATION INDEX TO FINANCIAL STATEMENTS... F-1 In connection with the issue of any Tranche of Notes, the Dealer or Dealers (if any) named as the Stabilisation Manager(s) (or persons acting on behalf of any Stabilisation Manager(s)) in the applicable Pricing Supplement may over-allot or effect transactions with a view to supporting the market price of the Notes of the Series (as defined below) of which such Tranche forms part at a level higher than that which might otherwise prevail. However, stabilisation may not necessarily occur. Any stabilisation action may begin on or after the date on which adequate public disclosure of the terms of the offer of the relevant Tranche of Notes is made and, if begun, may cease at any time, but it must end no later than the earlier of 30 days after the issue date of the relevant Tranche of Notes and 60 days after the date of the allotment of the relevant Tranche of Notes. Any stabilisation action or over-allotment must be conducted by the relevant Stabilisation Manager(s) (or persons acting on behalf of any Stabilisation Manager(s)) in accordance with all applicable laws and rules. xiv

36 DOCUMENTS INCORPORATED BY REFERENCE The following documents published or issued from time to time after the date hereof shall be deemed to be incorporated in, and to form part of, this Offering Circular: (a) (b) our most recently published audited consolidated and non-consolidated annual financial statements and, if published later, the most recently published audited or reviewed, as the case may be, our interim non-consolidated financial results of, (see General Information for a description of the financial statements currently published by us); and all supplements or amendments to this Offering Circular circulated by us from time to time. Any statement contained herein or in a document which is deemed to be incorporated by reference herein shall be deemed to be modified or superseded for the purpose of this Offering Circular to the extent that a statement contained in any such subsequent document which is deemed to be incorporated by reference herein modifies or supersedes such earlier statement (whether expressly, by implication or otherwise). Any statement so modified or superseded shall not be deemed, except as so modified or superseded, to constitute a part of this Offering Circular. We will provide, without charge, to each person to whom a copy of this Offering Circular has been delivered, upon the request of such person, a copy of any or all of the documents deemed to be incorporated herein by reference unless such documents have been modified or superseded as specified above. Requests for such documents should be directed to us at our office set out at the end of this Offering Circular. In addition, such documents will be available free of charge from the principal office of the principal paying agent in London (which for the time being is The Bank of New York Mellon, London Branch) (the Principal Paying Agent) for the Notes listed on the SGX-ST. If the terms of the Programme are modified or amended in a manner which would make this Offering Circular, as so modified or amended, inaccurate or misleading, to an extent which is material in the context of the Programme, a new offering circular will be prepared. 1