Name Zapara School of Business Intermediate Accounting 1ACCT 341/541 First Exam, Fall Exam Content:

|

|

|

- Clementine Hamilton

- 6 years ago

- Views:

Transcription

1 La Sierra University Name Zapara School of Business Intermediate Accounting 1ACCT 341/541 First Exam, Fall 2013 Exam Content: Q1 Definitions 6 min 8 pts Q2 Normal account balances 3 min 10 pts Q3 T-account activity 3 min 6 pts Q4 Closing entries 6 min 8 pts Q5 Adjusting journal entries 9 min 9 pts Q6 Adjusting journal entries 20 min 21 pts Q7 Classify various cash flows 5 min 10 pts Q8 Assemble set of financials 25 min 24 pts Q9 Home Depot financials 15 min 12 pts 92 min 108 pts Instructions: 1. Budget your time wisely. 2. Show all work and computations. Incorrect answers on the problems that are accompanied by computations are eligible for partial credit. 3. You may use a calculator and a straight-edge. You may not use your text, any notes, cell phone, computer, etc.. This exam is closed-book, closed-notes, and closed-neighbor. 4. An exam is not important enough to compromise your honor. Please do not cheat. Anyone caught cheating will be severely disciplined. The penalty for cheating on this exam, or facilitating cheating, is a zero for the test. 5. Dr. Albrecht believes that each question has sufficient information to be worked. Please let me know about any typos. 6. If any question calls for words in a solution, use the English language 7. Good luck.

2 Question 1 Define the following terms and provide an example of how each one is used. Adjusting entry Closing entry Question 2 For each account listed below, identify if the normal balance is a debit or credit by circling the best response. 1 Wages Payable Debit Credit 2 Rent Expense Debit Credit 3 Accounts payable Debit Credit 4 Product Inventory Debit Credit 5 Interest Revenue Debit Credit 6 Notes Payable Debit Credit 7 Depreciation Expense Debit Credit 8 Accumulated Depreciation Debit Credit 9 Equipment Debit Credit 10 Prepaid rent Debit Credit 11 Unearned Rent Revenue Debit Credit 12 Common Stock Debit Credit 13 Treasury Stock Debit Credit 14 Operating Expense Debit Credit 15 Accounts Receivable Debit Credit

3 Question 3 For the unnamed account at the left, compute the ending balance and write it in the proper location. For the unnamed account on the left, compute the missing value (designated by?) and write it next to the?

4 Question 4 A few real and nominal accounts have been selected from the accounts of the Lee company. Interest revenue 12,000 Prepaid rent 7,000 Unearned service revenue 18,000 Notes payable 31,000 Dividends 6,000 Accumulated depreciation 28,000 Retained earnings 42,000 Common stock 19,000 Wages payable 25,000 Rent expense 2,000 Required: Prepare the necessary closing journal entries.

5 Question 5 Prepare the necessary adjusting journal entry for each of the following situations. Do not abbreviate account titles, and remember to clearly indent for credit entries. 1. The Bechara Company received prepayments from customers totaling $24 during In the journal entry to record the receipt, Bechara recorded service revenue. At year-end it has $8 of these services remaining to be performed. What is the year-end adjusting entry at December 31, 2013? 2. Merlos Co. paid $12 on April 1, 2013 for 1 year of insurance in advance. In the entry to record the receipt, Merlos debited prepaid insurance and credited cash. Merlos is a calendar-year company. What is the proper adjusting entry to be made at December 31, 2013? 3. Royes Company has performed $3 of services for customers for which it has not been paid nor recorded. What is the proper adjusting entry to be made at December 31, 2013?

6 Question 6 The Sorunke Company has prepared the following list of unadjusted account balances (after transactions but before adjustments) for the year ended December 31, Accounts Payable 12,780 Accounts Receivable 24,511 Accumulated Depreciation 10,000 Capital Stock 31,500 Cash 38,659 Cost of Goods Sold Expense 0 Depreciation Expense 0 Dividends Distributed 3,000 Equipment 26,000 Income Tax Expense 0 Income Taxes Payable 0 Insurance Expense 6,000 Prepaid insurance 0 Product Inventory 35,778 Retained Earnings 33,609 Salaries Expense 11,498 Salaries Payable 0 Sales Revenue 61,300 Service Revenue 0 Supplies 0 Supplies Expense 8,943 Unearned Sales Revenue 5,200 Required: Prepare adjusting entries for the following situations. (1) Accrued service revenue is 3,100. (2) Unearned prepayments by customers at year end total $1,600. (3) Insurance coverage remaining for next year totals $1,300. (4) Supplies on hand total $800. (5) Unsold product inventory totals $625. (6) Accrued salaries total $2,600. (7) Depreciation expense totals $2,000. Total debits, total credits 154,389

7 Problem 7 Which section of statement of cash flows? Identify if the following transactions are accounted for on the Statement of Cash Flows as an operating activity (OA), investing activity (IA), financing activity (FA) or not applicable (NA). Designate inflow or outflow by placing a plus (+) or minus (!) sign in from of your OA, IA or FA answer. Interest paid Sale of used equipment Repaid loan principal Received from customers for cash sales Paid taxes to government Received from customers for payment on accounts receivable Dividends paid Purchased equipment Borrowed money via loan Invested in certificate of deposit Paid to suppliers Credit purchases Received prepayments from customers Received from owners for issuing common stock

8 Question 8 The Lorenzetti Company provides the following accounting information. On the blank sheet of paper provided to you, prepare a complete set of financial statements for Lorenzetti in good form. No abbreviations are allowed. All balance sheet items are for year end unless stated otherwise. For the statement of cash flows, use the section totals instead of individual detail provided for other financial statements. Please make sure you include all necessary totals and sub-totals and these are labeled. Accounts payable Accounts receivable Accumulated items of other comprehensive income Bonds payable (long-term) Building (net) Cash (beginning) Cash (ending) Cash flows from financing activities Cash flows from investing activities (24) Cash flows from operating activities ? Common stock (beginning) Common stock (ending) ? Common stock issued Cost of goods sold expense Depreciation expense Dividends paid Equipment Interest expense Interest payable Interest revenue Inventory Land Long-term investment Notes payable (long-term) Prepaid rent Rent expense Retained earnings (beginning) ? Retained earnings (ending) ? Sales revenue Unearned revenue Wages expense Wages payable

9 When finished with the first eight questions, turn in this booklet. Professor Albrecht will then give you question 9

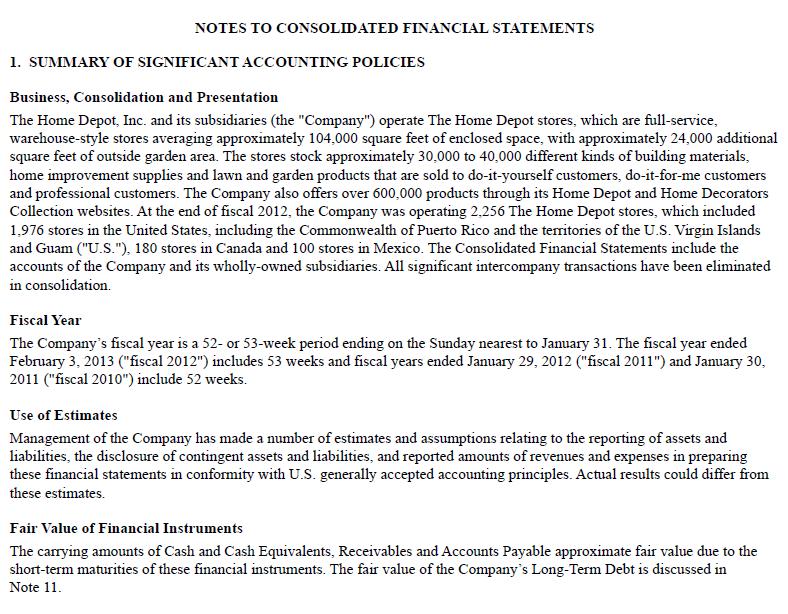

10 Name Question 9 Answer the following questions by referring to the Home Depot financial statements. Referring to data for the most recent fiscal year, what is Home Depot s general or overall balance sheet equation? By what percent did Home Depot s total liabilities change from prior year to most recent year? By what percent did Home Depot s gross profit change from the year prior to the current year? How much was Home Depot s balance of merchandise inventories at year end for the most recent year? What is the retained earnings equation for the most recent year?

11 In general, on what day does Home Depot s accounting year start and on what day does it end? What is the largest expense for the most recent year and what is the amount? How much did Home Depot pay in dividends during the most recent fiscal year? Who is the audit firm for Home Depot? Copy the first 10 words of the sentence that gives the auditor s opinion. How much was Home Depot s cash flow from financing activities for the most recent fiscal year? Is this amount a net inflow or net outflow? What was the largest item in investing activities for the current year? How much is it?

12

13

14

15

16

17

18 Intermediate ACCT 1 (341/541) Fall, 2013 Exam 1 Solutions Q1 Q2 Q3 Q4 Q5 Q6 Q7 Q8 Q9 Accounting cycle definitions Debit or credit account balances T-account computations Closing entries Adjusting entries Adjusting entries Classification into section of statement of cash flows Sorting items into financial statement and organized presentations Identifying items from Home Depot s financial statements

19 Question 1 Define the following terms and provide an example of how each one is used. Adjusting entry a journal entry made at the end of an accounting period to divide revenues and expenses related to the passage of time into the current period and next period. These can be either an accrual, or an adjustment made to a prepayment. An example of an adjustment for an accrual expense item is: Wages expense Wages payable X X Closing entry when nominal accounts (one period accumulators) have their balances transferred to Retained Earnings. The purposes of closing entries are to (1) update retained earnings, and (2) prepare the nominal accounts with a zero balance to start accumulating during the next period. Revenues, expenses and dividends get closed. Revenue Retained earnings Retained earnings Expense Retained earnings Dividends X X X X X X For the most part, student definitions were vague and incomplete. Frequently, definitions did not distinguish adjusting entries from closing entries.

20 Question 2 For each account listed below, identify if the normal balance is a debit or credit by circling the best response. Question 4 1 Wages Payable Credit 2 Rent Expense Debit 3 Accounts payable Credit 4 Product Inventory Debit 5 Interest Revenue Credit 6 Notes Payable Credit 7 Depreciation Expense Debit 8 Accumulated Depreciation Credit 9 Equipment Debit 10 Prepaid rent Debit 11 Unearned Rent Revenue Credit 12 Common Stock Credit 13 Treasury Stock Debit 14 Operating Expense Debit 15 Accounts Receivable Debit Interest revenue 12,000 Prepaid rent 7,000 Unearned service revenue 18,000 Notes payable 31,000 Dividends 6,000 Accumulated depreciation 28,000 Retained earnings 42,000 Common stock 19,000 Wages payable 25,000 Rent expense 2,000 Prepare the necessary closing journal entries. Interest revenue 12,000 Retained earnings 12,000 Retained earnings 2,000 Rent expense 2,000 Retained earnings 6,000 Dividends 6,000

21 Question 5 1. The Bechara Company received prepayments from customers totaling $24 during In the journal entry to record the receipt, Bechara recorded service revenue. At year-end it has $8 of these services remaining to be performed. What is the year-end adjusting entry at December 31, 2013? Service revenue 8 Unearned service revenue 8 2. Merlos Co. paid $12 on April 1, 2013 for 1 year of insurance in advance. In the entry to record the receipt, Merlos debited prepaid insurance and credited cash. Merlos is a calendar-year company. What is the proper adjusting entry to be made at December 31, 2013? Insurance expense 9 Prepaid insurance 9 3. Royes Company has performed $3 of services for customers for which it has not been paid nor recorded. What is the proper adjusting entry to be made at December 31, 2013? Accounts receivable 3 Service revenue 3 Question 6 1. Accounts receivable 3,100 Service revenue 3, Unearned sales revenue 3,600 Sales revenue 3, Prepaid insurance 1,300 Insurance expense 1, Supplies 800 Supplies expense Cost of goods sold expense 35,153 Product inventory 35, Salaries expense 2,600 Salaries payable 2, Depreciation expense 2,000 Accumulated depreciation 2,000

22 Problem 7 Which section of statement of cash flows? Identify if the following transactions are accounted for on the Statement of Cash Flows as an operating activity (OA), investing activity (IA), financing activity (FA) or not applicable (NA). Designate inflow or outflow by placing a plus (+) or minus (!) sign in from of your OA, IA or FA answer.! OA Interest paid + IA Sale of used equipment! FA Repaid loan principal + OA Received from customers for cash sales! OA Paid taxes to government + OA Received from customers for payment on accounts receivable! FA Dividends paid! IA Purchased equipment + FA Borrowed money via loan! IA Invested in certificate of deposit! OA Paid to suppliers NA Credit purchases + OA Received prepayments from customers + FA Received from owners for issuing common stock

23 Question 8 Balance sheet Assets Current assets Cash 17 given Accounts receivable 55 given Inventory 39 given Prepaid rent 8 given Total 119 Long-term investments 16 given Property, plant, equipment Land 41 given Building 38 given Equipment 62 given Total 141 Total assets 276 Liabilities Current Liabilities Accounts payable 19 given Interest payable 12 given Wages payable 12 given Unearned revenue 26 given Total 69 Long-term Liabilities Note payable (long term) 41 given Bonds payable (long term) 43 given Total 84 Total liabilities 153 Stockholders equity Common stock 63 from CS equation on Changes in SHE Retained earnings 58 by subtraction after CS is figured out Accumulated items of OCI 2 given Total SHE 123 Total liabilities & SHE 276

24 Income statement Interest revenue 6 given Sales revenue 310 given Total 316 Depreciation expense 13 given Rent expense 17 given Wages expense 7 given Cost of Goods sold expense 236 given Interest expense 5 given Total 278 Net income 38 Statement of cash flows Operating activities 6 by subtraction Investing activities (24) given Financing activities 11 given Net change in cash (7) + Beginning cash 24 given Ending cash 17 given Statement of changes in stockholders equity Beginning common stock 40 given Issue common stock 23 given Ending common stock 63 by subtraction Beginning retained earnings 33 by subtraction after ERE is figured out Net income 38 from income statement Dividends paid (13) given Ending retained earnings 58 from balance sheet

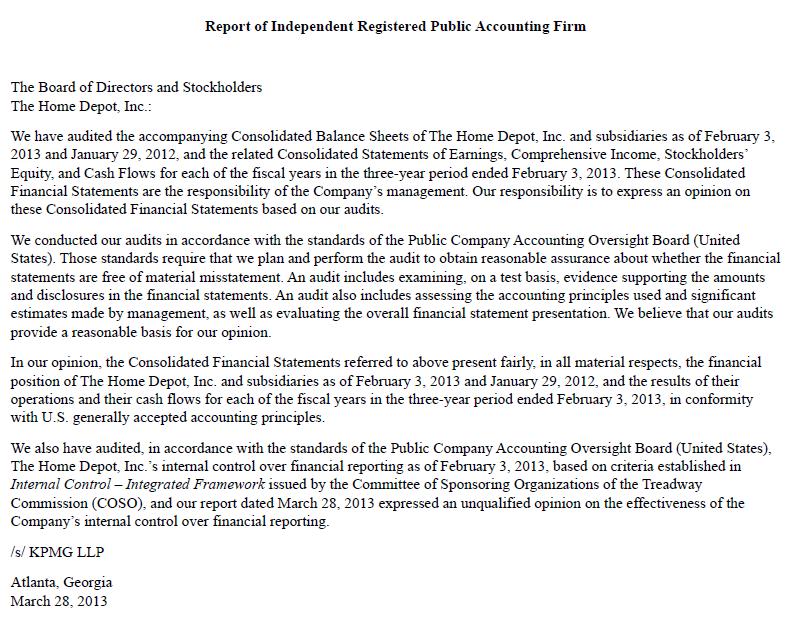

25 Question 9 Referring to data for the most recent fiscal year, what is Home Depot s general or overall balance sheet equation? Assets = Liabilities + SHE $ billion = $ billion + $ billion or $41,084,000,000 = ,000,000 + $17,777,000,000 By what percent did Home Depot s total liabilities change from prior year to most recent year? / = = 3.03% increase By what percent did Home Depot s gross profit change from the year prior to the current year? / = = 6.51% increase How much was Home Depot s balance of merchandise inventories at year end for the most recent year? $ billion or $10,710,000,000 What is the retained earnings equation for the most recent year? Beginning retained earnings + net income! dividends = ending retained earnings $ billion + $4.535 billion! $1.743 billion = $ billion In general, on what day does Home Depot s accounting year start and on what day does it end? The Company s fiscal year is a 52- or 53-week period ending on the Sunday nearest to January 31. What is the largest expense for the most recent year and what is the amount? Cost of sales = $ billion How much did Home Depot pay in dividends during the most recent fiscal year? $1.743 billion Who is the audit firm for Home Depot? KPMG, LLP Copy the first 10 words of the sentence that gives the auditor s opinion. In our opinion, the Consolidated Financial Statements referred to above present fairly, in all material respects, the financial position of The Home Depot, Inc. and subsidiaries as of February 3, 2013 and January 29, 2012, and the results of their operations and their cash flows for each of the fiscal years in the three-year period ended February 3, 2013, in conformity with U.S. generally accepted accounting principles. How much was Home Depot s cash flow from financing activities for the most recent fiscal year? Is this amount a net inflow or net outflow? $5.034 billion outflow What was the largest item in investing activities for the current year? How much is it? Capital expenditures $1.312 billion outflow

26 La Sierra University Name Zapara School of Business Intermediate Accounting 1ACCT 341/541 Second Exam, Fall 2013 Exam Content: Q1 Definition relevance 8 min 6 pts Q2 Definition asset 8 min 6 pts Q3 Expense matching/recognition principle 10 min 9 pts Q4 Income statement puzzle 10 min 10 pts Q5 Organizing a balance sheet 15 min 18 pts Q5 Multiple step Inc. Stmt. common size 30 min 28 pts 81 min 77 pts Instructions: 1. Budget your time wisely. 2. Show all work and computations. Incorrect answers on the problems that are accompanied by computations are eligible for partial credit. 3. You may use a calculator and a straight-edge. You may not use your text, any notes, cell phone, computer, etc.. This exam is closed-book, closed-notes, and closed-neighbor. 4. An exam is not important enough to compromise your honor. Please do not cheat. Anyone caught cheating will be severely disciplined. The penalty for cheating on this exam, or facilitating cheating, is a zero for the test. 5. Dr. Albrecht believes that each question has sufficient information to be worked. Please let me know about any typos. 6. If any question calls for words in a solution, use the English language 7. Good luck.

27 Question 1 In the chapter on accounting concepts and theory, relevance was put forth as one of the basic concepts of accounting. As best you can, define and describe relevance. Why is the term relevance important in accounting? Question 2 In the chapter on accounting concepts and theory, asset was put forth as one of the basic elements of accounting. As best you can, define and describe asset. Why is the term asset important in accounting?

28 Question 3 List and describe the different aspects of what Professor Albrecht calls the expense matching principle. It is also called the expense recognition principle. For each of the parts of the principle, describe it in a sentence or two and then provide an example.

29 Question 4 Reconstructing an income statement. The Chen Company has released only a few clues about its earnings for the most recent year. Cost of goods sold expense $300,000 Net income as a percentage of sales 36 % Gross margin as a percentage of sales 60 % Gain $75,000 Income tax expense as a percentage of pre-tax income 20% Operating expenses as a percentage of gross margin % (25/60) Required: Using the above clues, prepare a multiple step income statement in good form. The income statement should include a columns for labels, numbers and common size percentages.

30 Question 5 Organizing a balance sheet. An accountant at the Van Putten Company dropped the balance sheet and all the items got horribly mixed up. Your task is to prepare a classified balance sheet complete with subtotals and totals and all necessary headings. Loans payable (non-current) 625 Equipment 422 Treasury stock (59) Accounts and other payables 318 Investments in stock of other companies (non-current) 412 Bonds payable (non-current) 10 Accumulated items of other comprehensive income 360 Copyrights 27 Accounts receivable 157 Common stock 905 Inventories 233 Retained earnings 570 Land 311 Cash & equivalents 732 Services or products owed 165 Trading securities (short-term investments) 81 Funds and fixed term investments (non-current 30 Prepaid and other 61 Patents 59 Current maturities of long-term debt 290 Buildings 659

31 Question 6 The Richardson Company, a manufacturer of metal attachments for furniture, has reported the following income statements in single-step format Sales revenue 9,000,000 7,000,000 6,000,000 Gains 0 500, ,000 Interest revenue 55,000 50,000 40,000 Total revenues and gains 9,055,000 7,550,000 6,640,000 Cost of sales 4,000,000 3,250,000 3,000,000 Selling expenses 1,080, , ,000 Losses 3,000, , ,000 Administrative expenses 400, , ,000 Interest expense 22,000 20,000 18,000 R&D expenses 1,500, , ,000 Total expenses and losses 10,002,000 5,700,000 4,918,000 Pre-tax income (947,000) 1,850,000 1,722,000 Income tax expense (142,050) 277, ,300 Net income (804,950) 1,572,500 1,463,700 Required: (1) On a separate sheet of paper, rearrange the income statements into multiple-step format. (2) Perform a vertical (common size) analysis on your multiple-step income statements. Please show tenths of a percentage (e.g., 23.4%). This may be in a column immediately to the right of the number. (3) Perform an horizontal analysis on sales revenue. (4) Comment on the trends you discern in your analyses. Be sure to mention the gross margin percentage in your discussion. Which was the best year, in your opinion?

32 Intermediate ACCT 1 (341/541) Fall, 2013 Exam 2 Solutions Question 1 In the chapter on accounting concepts and theory, relevance was put forth as one of the basic concepts of accounting. As best you can, define and describe relevance. Why is the term relevance important in accounting? Relevance is one of two fundamental characteristics of accounting information. Representational faithfulness is the other. Accounting information is expected to be relevant to user decisions. Relevant information pertains to decisions being made by financial statement users. If it pertains to a user decision, relevant information has at least one of three qualities: (1) it provides new information useful in making predictions about some future business operation, (2) it provides meaningful confirmation for something known before, and (3) it is material, or large enough to make a difference in the decision. All financial accounting disclosures should be relevant to decisions being made by financial statement users. If so, then the benefit from providing the information exceeds the cost of providing it. If accounting information is not relevant, then it should not be included in financial reports. Question 2 In the chapter on accounting concepts and theory, asset was put forth as one of the basic elements of accounting. As best you can, define and describe asset. Why is the term asset important in accounting? An asset is a resource that is going to be used in business operations in order to generate revenues. If resources don t in any way help in generating revenues, funds should not be spent to acquire the resources. For an asset to be recorded in the accounts and reported in the financial statements, it should possess all of the following three characteristics. First, it should have expected future benefit. In other words, it should help in generating a future revenue. Second, it should be controllable by the company. The company is able to specify who is to use the asset, and can prevent unauthorized parties from using it. Third, the asset should be present as a result of an exchange transaction. In other words, the company either has received the asset, or it has paid for the asset and is awaiting its arrival. Asset is important in accounting because it is one of the building block elements, and is essential for the balance sheet and generating new revenue.

33 Question 3 List and describe the different aspects of what Professor Albrecht calls the expense matching principle. For each of the parts of the principle, describe it in a sentence or two and then provide an example. The expense matching principle is where the costs of conducting business (and therefore the costs of generating revenue) are matched to the revenue that results from spending money. The costs are recognized as expense in the period in which revenue is recognized. First the revenue is put on the income statement, then the related costs. The cause and effect relationship can seldom be conclusively demonstrated, but many costs appear to be related to particular revenues and recognizing them as expenses accompanies recognition of the revenue. Examples of expenses that are recognized by associating cause and effect are sales commissions and cost of products sold or services provided. Systematic and rational allocation means that in the absence of a direct means of associating cause and effect, and where the asset provides benefits for several periods, its cost should be allocated to the periods in a systematic and rational manner. Examples of expenses that are recognized in a systematic and rational manner are depreciation of plant assets, amortization of intangible assets, and allocation of rent and insurance. Some costs are immediately expensed because the costs have no discernible future benefits or the allocation among several accounting periods is not considered to serve any useful purpose. Examples include officers salaries, most selling costs, amounts paid to settle lawsuits, and costs of resources used in unsuccessful efforts.

34 Question 4 Reconstructing an income statement. Cost of goods sold expense $300,000 Net income as a percentage of sales 36 % Gross margin as a percentage of sales 60 % Gain $75,000 Income tax expense as a percentage of pre-tax income 20% Operating expenses as a percentage of gross margin % (25/60) Sales 750, % = 300,000/.4 Cost of goods sold expense 300,000 40% = 100%!60% Gross Margin 450,000 60% = 750,000*.6 Selling & Administrative 187,500 25% Operating income 262,500 35% Gain 75,000 10% = Pre-tax income 337,500 45% Income tax expense 67,500 9% = 20% of pretax Net Income 270,000 36%

35 Question 5 Loans payable (non-current) 625 Equipment 422 Treasury stock (59) Accounts and other payables 318 Investments in stock of other companies (non-current) 412 Bonds payable (non-current) 10 Accumulated items of other comprehensive income 360 Copyrights 27 Accounts receivable 157 Common stock 905 Inventories 233 Retained earnings 570 Land 311 Cash & equivalents 732 Services or products owed 165 Trading securities (short-term investments) 81 Funds and fixed term investments (non-current 30 Prepaid and other 61 Patents 59 Current maturities of long-term debt 290 Buildings 659 Assets Liabilities Current Assets Current Liabilities Cash & equivalents 732 Accounts & other payables 318 Trading securities 81 Current maturities of long-term debt 290 Accounts receivable 157 Services or products owed 165 Inventories 233 Total 773 Prepaid & other 61 Noncurrent Liabilities Total 1,264 Notes payable 625 Noncurrent Investments Bonds payable 10 Funds & fixed term investments 30 Total 635 Stock of other companies 412 Total Liabilities 1,408 Total 442 Property, Plant & Equipment Stockholders Equity Land 311 Common stock 905 Building 659 Retained earnings 570 Equipment 422 Accumulated items of OCI 360 Total 1,392 Treasury stock (59) Intangibles Total Stockholders Equity 1,776 Patents 59 Copy rights 27 Total Liabililties & Stockholders Equity 3,184 Total 86 Total assets 3,184

36 Question 6 (1) On a separate sheet of paper, rearrange the income statements into multiple-step format. (2) Perform a vertical (common size) analysis on your multiple-step income statements. Please show tenths of a percentage (e.g., 23.4%). This may be in a column immediately to the right of the number. (3) Perform an horizontal analysis on sales revenue Sales revenue 9,000, % 7,000, % 6,000, % Cost of sales 4,000, % 3,250, % 3,000, % Gross margin 5,000, % 3,750, % 3,000, % Selling expenses 1,080, % 980, % 900, % Administrative expenses 400, % 350, % 300, % R&D expenses 1,500, % 900, % 600, % Operating income 2,020, % 1,520, % 1,200, % Other Gains 0 0.0% 500, % 600, % Interest revenue 55, % 50, % 40, % Losses (3,000,000) -33.3% (200,000) -2.9% (100,000) -1.7% Interest expense (22,000) -0.2% (20,000) -0.3% (18,000) -0.3% Pre-tax income (947,000) -10.5% 1,850, % 1,722, % Income tax expense (142,050) -1.6% 277, % 258, % Net income (804,950) -8.9% 1,572, % 1,463, % Chng revenue % Chng revenue % (4) Comment on the trends you discern in your analyses. Be sure to mention the gross margin percentage in your discussion. Which was the best year, in your opinion? Sales are going up at an increasing rate. Both the gross margin and operating income are increasing. The operating expense of selling are going down (good sign when sales increase). Also, the operating expense of R&D is going up (a good sign as that reflects an investment in the future. The one negative is that 2011 had a large one time loss, in contrast to 2009 & 2010 that showed moderate one time gains. Take away the one time gains and losses, then 2011 is the best year by far. All the key indicators are going up.

37 La Sierra University Name Zapara School of Business Intermediate Accounting 1ACCT 341/541 Final Exam, Fall 2013 Exam Content: Q1 Revenue recognition principle 12 min 12 pts Q2 Revenue recognition problem 10 min 12 pts Q3 PV/FV computations 10 min 12 pts Q4 A more complex PV/FV problem 15 min 20 pts Q5 Loan with amortization table, entries 12 min 12 pts Q6 Cash or bank rec 20 min 16 pts Q7 AR & allowance for uncollectibles 5 min 8 pts 84 min 92 pts Instructions: 1. Budget your time wisely. 2. Show all work and computations. Incorrect answers on the problems that are accompanied by computations are eligible for partial credit. 3. You may use a calculator and a straight-edge. You may not use your text, any notes, cell phone, computer, etc.. This exam is closed-book, closed-notes, and closed-neighbor. 4. An exam is not important enough to compromise your honor. Please do not cheat. Anyone caught cheating will be severely disciplined. The penalty for cheating on this exam, or facilitating cheating, is a zero for the test. 5. Dr. Albrecht believes that each question has sufficient information to be worked. Please let me know about any typos. 6. If any question calls for words in a solution, use the English language 7. Good luck.

how and why the revenue recognition principle permits recognizing revenue at the time of a sale for credit.")

38 Question 1 Revenue Recognition Principle Explain the revenue recognition principle. In addition, explain: 1) how and why the revenue recognition principle permits recognizing revenue at the time of a sale for credit. 2) how and why the revenue recognition principle permits recognizing revenue before the point of sale for precious minerals or agricultural products 3) how and why the revenue recognition principle permits recognizing revenue after the point of sale when cash collection is problematic.

39 Question 2 Revenue recognition under different methods. Lee Company manufactures and sells widgets. In 2011, Lee manufactured 3,000 units at a cost of $80 each. In 2012, Lee manufactured 5,000 units at a cost of $80 each. In 2013, Lee manufactured 1,000 units at a cost of $80 each. During 2011, Lee sold 2,000 units. During 2012, Lee sold 4,000 units. During 2013, Lee sold the remaining 3,000 units. Each unit has a selling price of $125. During 2011, Lee collected $50,000 from customers. During 2012, Lee collected $200,000. During 2013, Lee collected $700,000 from customers. During 2014, Lee collected the remaining $175,000 from customers. Required: Complete income statements for 2011, 2012, 2013, and 2014 under the following revenue recognition alternatives. 1. Revenue is recognized when cash is collected (installment sales method). Revenue Expense Income Total 2. Revenue is recognized when production is complete. Revenue Expense Income Total 3. Revenue is recognized at the point of sale. Revenue Expense Income Total 4. Revenue is recognized under the cost recovery method. Revenue Expense Income Total

40 Question 3 PV/FV computations Compute answers to the following questions. I recommend that you show all work by creating and filling in a table of input values. PV FV N I PMT Type (1) Today, December 12, 2013 (12/12/2013 in mm/dd/year format), you deposit $ into an account earning 1.4% interest. You intend to make six more deposits of $ into the account, on 12/12/2014, 12/12/2015, 12/12/2016, 12/12/2017, 12/12/2018 and 12/12/2019. To how much will the account grow by 12/12/2020? Interest is compounded annually. [Your answer should be taken to two decimal places.] (2) Today, December 12, 2013, you borrow $53,176 for the purchase of production equipment and agree to make semi-annual repayments of the same amount for 6 years at 8% interest. The first payment is scheduled on 12/12/2013. If the loan is completely repaid after the final payment, then how much is each payment? [Your answer should be taken to two decimal places.] (3) Today, December 12, 2013, you borrow $61,221 for the purchase of production equipment and agree to make annual repayments of the same amount for 7 years at an 8% annual rate of interest. The first payment is scheduled on 12/12/2014. If the loan is completely repaid after the final payment (12/12/2020), then how much is each payment? [Your answer should be taken to two decimal places.]

41 (4) Today December 12, 2013, you borrow $9,312 to purchase a used car and agree to make five annual payments of the same amount, $2,371.15, after which the car loan will be completely paid off. The first payment is to due on 12/12/2014. What interest rate is being charged on the loan? [Your answer should be taken to two decimal places pp.pp%.] (5) $6, is being invested today, December 12, 2013 in an account earning an annual rate of 4.28%, compounded semi-annually. How many six month periods will it take the account to grow to $14,278.15? [Your answer should be taken to one decimal place.]

42 Question 4 Complex PV/FV problem. On December 12, 2013, Bayona makes the first of six (6) equal annual deposits of $13,125 into an investment fund. The last is scheduled for December 12, On December 12, 2023, Bayona is to make an additional deposit of unspecified amount (X). Beginning on December 12, 2031, Bayona is to make the first eight annual withdrawals of $47,522, after which the fund will be exhausted. The interest rate 5.25% compounded annually for the time up to 12/12/2020. After 12/12/2020, the interest rate is 7.32%. Required: Calculate the amount of the additional deposit X on December 12, Clearly designate it as the final answer. Please show all work.

43 Question 5 Installment Loan. The Zhang Company is borrowing $55,235 from a bank on January 1, The bank is charging 5% interest. The loan is to be paid off in six equal sized annual installments, starting on December 31, 2013 and ending on December 31, [This is called an installment loan] Round all amounts to the nearest dollar. (1) Compute the amount of the annual payment. (2) Prepare an amortization table in good form to account for this loan. Round all amounts to the nearest dollar. (3) Write journal entries needed to account for the loan and payments during 2013 and 2014.

44 Question 6 Bank reconciliation. The Wong Company needs help in constructing a bank reconciliation for April 30: The bank statement for Wong, dated April 30, but not received until May 7, contains the following information: March 31 balance $84,612 April deposits (& other credits) $317,681 April withdrawals (& other debits) $298,337 April 30 balance $103,956 Wong's ledger account for cash has the following information for the past thirty days: March 31 balance $47,094 April additions & debits $328,660 April subtractions & credits $304,005 April 30 balance $71,749 The staff of Wong has assembled the following information for a bank reconciliation as of April 30: * Funds collected by bank: April = $16,132 * Service charges: April $3,877 * NSF checks, informed by bank on: April 30 = $1,895 * Deposits in transit: April 30 = $21,811 * Outstanding checks: April 30 = $43,658 The additional information for a bank reconciliation as of March 31 is: * Funds collected by bank: March = $22,512 * Service charges: March = $4,301 * Deposits in transit: March 31 = $17,212 * Outstanding checks: March 31 = $36,519 Required: Prepare a proof of cash (comprehensive bank reconciliation) as of April 30 for the month of April.

45 Question 6 answer sheet April April Balance Receipts/ Disbursements/ Balance Event/action March 31 additions subtractions April 30 From ledger account True balances April April Balance Receipts/ Disbursements/ Balance Event/action March 31 additions subtractions April 30 From bank statement True balances

46 Question 7 Analyzing Accounts Receivable & Allowance for Uncollectible Accounts. The following information was obtained from the records of Johnson Corporation for the month of May. Allowance for uncollectible accounts May 1 5,000 Allowance for uncollectible accounts May 31? Credit sales for month of May? Cash collections for May 240,000 Bad debt expense for May 26,000 Accounts receivable May 1 28,000 Accounts receivable May 31 43,000 Accounts written off during May 19,000 Required: 1. Compute the amount of credit sales during May. 2. Compute the amount of allowance for uncollectible accounts on May 31.

47 Intermediate ACCT 1 (341/541) Fall, 2013 Final Exam Solutions Question 1 Revenue is generally recognized when (1) realized or realizable, and (2) earned. Being earned is when an exchange of product or service occurs. Sometimes it is considered to occur when the key event necessary for an exchange occurs. Being realized or realizable means that the cash (if not already received) is likely or probable to occur in the future. In a highly developed economy where credit sales are common, a customer s credit worthiness is evaluated through a credit check. If the company determines that it is likely that the customer will pay in the future, revenue is recognized at the point of product/service exchanged despite there not being cash yet. This meets the terms of the revenue recognition principle, because the seller & buyer have closed the deal (contractually agreed to the exchange), and because the revenue is considered realizable (or collectible). In the case of mineral discovery and extraction, and agriculture, revenue is often recognized before an exchange is made between the seller and a buyer. This is because there are well developed markets with sufficient demand that on any given day, any amount of product could be sold if it was taken to market. In this case, the key event is identified as the appropriate revenue recognition point. In the case of mineral discovery and extraction, the key event is discovery of proven reserves. These reserves are kept in the ground until the mining company decides to take the mineral to market and sell it. At this time it is extracted and sold, and revenue is recognized. Buyers in such a market either pay in cash or are sufficiently credit worthy to merit extension of credit. In agriculture, crops cannot be kept in fields until the decision is made to sell, as decomposition will occur. In this case, extraction or harvest must take place when it can. Then harvested grain (or other agriculture produce) are stored until such time as the farmer decides to sell. But because the key event is harvest, revenue is recognized at this time. Sometimes sellers sell to buyers who are credit unworthy. This is the case when durable goods (that can be repossessed and sold to someone else) are sold to the consumer fringe. In this case, exchanging the product is trivial, because the seller will sell to anyone with a pulse. There is uncertainty as to whether the buyer will eventually pay. The uncertainty is resolved when cash payment is eventually made. Revenue is recognized at this time, the point of cash collection.

48 Question 2 Revenue recognition at different times. Lee Company manufactures and sells widgets. In 2011, Lee manufactured 3,000 units at a cost of $80 each. In 2012, Lee manufactured 5,000 units at a cost of $80 each. In 2013, Lee manufactured 1,000 units at a cost of $80 each. During 2011, Lee sold 2,000 units. During 2012, Lee sold 4,000 units. During 2013, Lee sold the remaining 3,000 units. Each unit has a selling price of $125. During 2011, Lee collected $50,000 from customers. During 2012, Lee collected $200,000. During 2013, Lee collected $700,000 from customers. During 2014, Lee collected the remaining $175,000 from customers. 1. Revenue is recognized when cash is collected (installment sales method) Total Revenue 50, , , ,000 1,125,000 Expense 32, , , , ,000 Income 18,000 72, ,000 63, , Revenue is recognized when production is complete Total Revenue 375, , , ,125,000 Expense 240, ,000 80, ,000 Income 135, ,000 45, , Revenue is recognized at the point of sale Total Revenue 250, , , ,125,000 Expense 160, , , ,000 Income 90, , , , Revenue is recognized under the cost recovery method Total Revenue 50, , , ,000 1,125,000 Expense 50, , , ,000 Income , , ,000

49 Question 3 PV/FV computations (1) Today, December 12, 2013 (12/12/2013 in mm/dd/year format), you deposit $ into an account earning 1.4% interest. You intend to make six more deposits of $ into the account, on 12/12/2014, 12/12/2015, 12/12/2016, 12/12/2017, 12/12/2018 and 12/12/2019. To how much will the account grow by 12/12/2020? Interest is compounded annually. [Your answer should be taken to two places.] PV 0 FV? = 1, N 7 I 1.4 PMT Type beg fv one period after final payment (2) Today, December 12, 2013, you borrow $53,176 for the purchase of production equipment and agree to make semi-annual repayments of the same amount for 6 years at an 8% annual rate of interest. The first payment is scheduled on 12/12/2013. If the loan is completely repaid after the final payment, then how much is each payment? [Your answer should be taken to two places.] PV!53,176 FV 0 N 12 6*2 I 4 8/2 PMT? = 5, Type beg pv at time of first payment (3) Today, December 12, 2013, you borrow $61,221 for the purchase of production equipment and agree to make annual repayments of the same amount for 7 years at 8% annual interest. The first payment is scheduled on 12/12/2014. If the loan is completely repaid after the final payment (12/12/2020), then how much is each payment? [Your answer should be taken to two places.] PV!61,221 FV 0 N 7 I 8 PMT? = 11, Type end pv one period before first payment

50 (4) Today December 12, 2013, you borrow $9,312 to purchase a used car and agree to make five annual payments of the same amount, $2,371.15, after which the car loan will be completely paid off. The first payment is to due on 12/12/2014. What interest rate is being charged on the loan? [Your answer should be taken to two places pp.pp%.] PV!9,312 FV 0 N 5 I? = 8.63% PMT 2, Type end pv one period before first payment (5) $6, is being invested today, December 12, 2013 in an account earning an annual rate of 4.28%, compounded semi-annually. How many six month periods will it take the account to grow to $14,278.15? [Your answer should be taken to one place.] PV!6, FV +14, N? = 36.5 I 2.14% 4.28 / 2 PMT 0 Type N/A no payments

51 Question 4 On December 12, 2013, Bayona makes the first of six (6) equal annual deposits of $13,125 into an investment fund. The last is scheduled for December 12, On December 12, 2023, Bayona is to make an additional deposit of unspecified amount (X). Beginning on December 12, 2031, Bayona is to make the first eight annual withdrawals of $47,522, after which the fund will be exhausted. The interest rate 5.25% compounded annually for the time up to 12/12/2020. After 12/12/2020, the interest rate is 7.32%. Required: Calculate the amount of the additional deposit X on December 12, Value of 12/12/2021? value of + X = value of 123,013 + X = 170,935 X = 47,922 PV PV FV? = FV? = FV? = N 6 N 2 N 3 I 5.25 I 5.25 I 7.32 Pmt!13,125 Pmt 0 Pmt 0 type end type N/A type N/A Value of 12/12/2021? PV? = 280,282.45@2030 PV FV 0 N 8 N 7 I 7.32 I 7.32 Pmt!47,522 Pmt 0 type end type N/A

52 Question 5 Installment Loan. The Zhang Company is borrowing $55,235 from a bank on January 1, The bank is charging 5% interest. The loan is to be paid off in six equal sized annual installments, starting on December 31, 2013 and ending on December 31, 2018 (1) Compute the amount of the annual payment. (2) Prepare an amortization table in good form to account for this loan. (3) Write journal entries needed to account for the loan and payments during 2013 and PV 55,235 FV 0 N 6 I 5 Pmt 10,882 type end Date Cash Interest Amort Balance Jan 1, ,235 Dec 31, ,882 2,762 8,120 47,115 Dec 31, ,882 2,356 8,526 38,589 Dec 31, ,882 1,929 8,953 29,636 Dec 31, ,882 1,482 9,400 20,236 Dec 31, ,882 1,012 9,870 10,366 Dec 31, , , /1/11 Cash 55,235 Note payable 55,235 12/31/11 Interest expense 2,762 Note payable 8,120 Cash 10,882 12/31/11 Interest expense 2,356 Note payable 8,526 Cash 10,882

53 Question 6 Bank reconciliation. April April Balance Receipts/ Disbursements/ Balance Event/action March 31 additions subtractions April 30 From ledger account 47, , ,005 71,749 collections +22,512 22, , ,132 service charges 4,301 4,301 +3,877 3,877 NSF +1,895 1,895 True balance 65, , ,476 82, 109 April April Balance Receipts/ Disbursements/ Balance Event/action March 31 additions subtractions April 30 From bank statement 84, , , ,956 late deposits + 17,212 17, , ,811 outstanding checks 36,519 36, ,658 43,658 True balance 65, , ,476 82, 109

54 Question 7 Analyzing Accounts Receivable & Allowance for Uncollectible Accounts. Allowance for uncollectible accounts May 1 5,000 Allowance for uncollectible accounts May 31? Credit sales for month of May? Cash collections for May 240,000 Bad debt expense for May 26,000 Accounts receivable May 1 28,000 Accounts receivable May 31 43,000 Accounts written off during May 19, Compute the amount of credit sales during May. Beg AR + credit sales collections write-offs = End AR 28,000 + credit sales 240,000 19,000 = 43,000 credit sales = 274, Compute the amount of allowance for uncollectible accounts on May 31. Beg Allow + bad debt exp write-offs = End Allow 5, ,000 19,000 = End Allow 12,000 = end Allow

Concordia College, Offutt School of Business ACCT 355 First Exam, Fall Name Albrecht. Exam Content:

Concordia College, Offutt School of Business ACCT 355 First Exam, Fall 2011 Name Albrecht Exam Content: Q1 Essay 15 min 18 pts Q2 Short answer 4 min 8 pts Q3 Short answer 4 min 4 pts Q4 Definitions 6 min

Concordia College, Offutt School of Business ACCT 355 First Exam, Fall 2011 Name Albrecht Exam Content: Q1 Essay 15 min 18 pts Q2 Short answer 4 min 8 pts Q3 Short answer 4 min 4 pts Q4 Definitions 6 min

ACCT 356 First Exam Spring, 2011 Albrecht. Name. Exam Content:

ACCT 356 First Exam Spring, 2011 Albrecht Name Exam Content: Q1 Payroll accounting 9 min 12 pts Q2 Loan computations 12 min 20 pts Q3 Installment loan 18 min 25 pts Q4 Non-interest bearing loan 12 min

ACCT 356 First Exam Spring, 2011 Albrecht Name Exam Content: Q1 Payroll accounting 9 min 12 pts Q2 Loan computations 12 min 20 pts Q3 Installment loan 18 min 25 pts Q4 Non-interest bearing loan 12 min

ACCT 356. Spring, 2011 Albrecht. Exam Content:

ACCT 356 First Exam Spring, 2011 Albrecht Name Exam Content: Q1 Payroll accounting 9 min 12 pts Q2 Loan computations 12 min 20 pts Q3 Installment loan 18 min 25 pts Q4 Non-interest bearing loan 12 min

ACCT 356 First Exam Spring, 2011 Albrecht Name Exam Content: Q1 Payroll accounting 9 min 12 pts Q2 Loan computations 12 min 20 pts Q3 Installment loan 18 min 25 pts Q4 Non-interest bearing loan 12 min

PIN# Spring, 2010 (no name, please) Albrecht. Exam Content:

Albrecht. Exam Content:") ACCT 356 First Exam PIN# Spring, 2010 (no name, please) Albrecht Exam Content: Q1 Classification of intangibles 5 min 6 pts Q2 Contingencies 7 min 8 pts Q3 Payroll accounting 9 min 12 pts Q4 Loan computations

ACCT 356 First Exam PIN# Spring, 2010 (no name, please) Albrecht Exam Content: Q1 Classification of intangibles 5 min 6 pts Q2 Contingencies 7 min 8 pts Q3 Payroll accounting 9 min 12 pts Q4 Loan computations

Intermediate Acct 2 SBAD 332 First Exam. Exam Content:

Intermediate Acct 2 SBAD 332 First Exam Name Spring, 2013 Albrecht Exam Content: Q1 Payroll accounting 10 min 10 pts Q2 Installment loan accounting 20 min 26 pts Q3 Interest bearing loan with principal

Intermediate Acct 2 SBAD 332 First Exam Name Spring, 2013 Albrecht Exam Content: Q1 Payroll accounting 10 min 10 pts Q2 Installment loan accounting 20 min 26 pts Q3 Interest bearing loan with principal

Prof Albrecht s Notes Accounting for Bonds Intermediate Accounting 2

Prof Albrecht s Notes Accounting for Bonds Intermediate Accounting 2 Companies need capital to fund the acquisition of various resources for use in business operations. They get this capital from owners

Prof Albrecht s Notes Accounting for Bonds Intermediate Accounting 2 Companies need capital to fund the acquisition of various resources for use in business operations. They get this capital from owners

FAQ: Financial Statements

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

Chapter 13 Statement of Cash Flows Study Guide Solutions Fill-in-the-Blank Equations. Exercises

Chapter 13 Statement of Cash Flows Study Guide Solutions Fill-in-the-Blank Equations 1. Net cash flow from operating activities 2. Change in Cash 3. Cash used to purchase property, plant, and equipment

Chapter 13 Statement of Cash Flows Study Guide Solutions Fill-in-the-Blank Equations 1. Net cash flow from operating activities 2. Change in Cash 3. Cash used to purchase property, plant, and equipment

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES INVESTING ACTIVITIES FINANCING ACTIVITIES

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

Financial Accounting

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

Talking Accounting Definitions

Talking Accounting Definitions Introduction to Accounting week 1 Accounting The information system that measures business activities, processes that information into reports, and communicates the result

Talking Accounting Definitions Introduction to Accounting week 1 Accounting The information system that measures business activities, processes that information into reports, and communicates the result

The Adjustment Process and Financial Statements Irwin/McGraw-Hill

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4)

") MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson. The statement of cash flows is a required component of financial statements.

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

Accounting Basics Introduction To Financial Accounting

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

ACCOUNTING INTERVIEW QUESTIONS

www.globalcma.in Learning Platform for Cost Accountants (CMA) 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction

www.globalcma.in Learning Platform for Cost Accountants (CMA) 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction

Statement of Cash Flows Revisited

21 Statement of Cash Flows Revisited Overview There is not much that is new in this chapter. Rather, this chapter draws on what was learned in Chapter 5 and subsequent chapters with respect to the statement

21 Statement of Cash Flows Revisited Overview There is not much that is new in this chapter. Rather, this chapter draws on what was learned in Chapter 5 and subsequent chapters with respect to the statement

Accounting for Liabilities

CHAPTER 7 Accounting for Liabilities LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Show how notes payable and related interest expense affect financial

CHAPTER 7 Accounting for Liabilities LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Show how notes payable and related interest expense affect financial

100 Accounting Interview Questions and Answers

100 Accounting Interview Questions and Answers 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction I decided to

100 Accounting Interview Questions and Answers 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction I decided to

Professor Authored Problems Intermediate Accounting I Acct 341/541. Accounting Cycle

Professor Authored Problems Intermediate Accounting I Acct 341/541 Accounting Cycle Problem 17 Accounting cycle definitions. Please provide (1) complete, clear, accurate definitions, and (2) a good example.

Professor Authored Problems Intermediate Accounting I Acct 341/541 Accounting Cycle Problem 17 Accounting cycle definitions. Please provide (1) complete, clear, accurate definitions, and (2) a good example.

McGill University Desautels School of Management MGCR 211 INTRODUCTION TO FINANCIAL ACCOUNTING Winter 2014 Professor: Seda Oz

McGill University Desautels School of Management MGCR 211 INTRODUCTION TO FINANCIAL ACCOUNTING Winter 2014 Professor: Seda Oz LAST NAME FIRST NAME STUDENT # FINAL EXAM Thursday - April 24, 2014 VERSION

McGill University Desautels School of Management MGCR 211 INTRODUCTION TO FINANCIAL ACCOUNTING Winter 2014 Professor: Seda Oz LAST NAME FIRST NAME STUDENT # FINAL EXAM Thursday - April 24, 2014 VERSION

CHAPTER 12 STATEMENT OF CASH FLOWS

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

Seminar on Bookkeeping Basics

Seminar on Bookkeeping Basics (Handout) Our materials are copyright AccountingCoach, LLC and are for personal use by the original purchaser only. We do not allow our materials to be reproduced or distributed

Seminar on Bookkeeping Basics (Handout) Our materials are copyright AccountingCoach, LLC and are for personal use by the original purchaser only. We do not allow our materials to be reproduced or distributed

Financial Statement Overview. Introduction

Financial Statement Overview Bankers Insight Group, LLC Jeffery W. Johnson Introduction Financial Statement Analysis is the Cornerstone of a Bank s credit decision making process They report on an economic

Financial Statement Overview Bankers Insight Group, LLC Jeffery W. Johnson Introduction Financial Statement Analysis is the Cornerstone of a Bank s credit decision making process They report on an economic

Analyzing Transactions

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

Some deferred items for which adjusting entries would be made include: Prepaid insurance Prepaid rent Office supplies Depreciation Unearned revenue

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

Debits and Credits CHAPTER

chapter-3.qxd 3//0 3:48 PM Page 45 3 CHAPTER Debits and Credits As you learned in the last chapter, accountants use the accounting equation to analyze a firm s transactions and determine the effects of

chapter-3.qxd 3//0 3:48 PM Page 45 3 CHAPTER Debits and Credits As you learned in the last chapter, accountants use the accounting equation to analyze a firm s transactions and determine the effects of

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Financial Accounting 2016 Exam 3.4 Professors G. Peter and Carolyn R. Wilson

NAME 1 Financial Accounting 2016 Exam 3.4 Professors G. Peter and Carolyn R. Wilson The exam packet is comprised of : 1. This 17-page document, which contains the questions you are to answer. Write all

NAME 1 Financial Accounting 2016 Exam 3.4 Professors G. Peter and Carolyn R. Wilson The exam packet is comprised of : 1. This 17-page document, which contains the questions you are to answer. Write all

Reading & Understanding Financial Statements

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Reading & Understanding Financial Statements. A Guide to Financial Reporting

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Prof Albrecht s Notes Introduction to the Accounting Cycle Intermediate Accounting 1

Prof Albrecht s Notes Introduction to the Accounting Cycle Intermediate Accounting 1 The accounting cycle is accounting process that extends from the very start of an accounting period to the absolute

Prof Albrecht s Notes Introduction to the Accounting Cycle Intermediate Accounting 1 The accounting cycle is accounting process that extends from the very start of an accounting period to the absolute

ADVANCED ACCOUNTING (110)

") Page 1 of 9 Contestant Number: Time: Rank: ADVANCED ACCOUNTING (110) Secondary REGIONAL 2015 Objective & Short Answer: Multiple Choice (20 @ 2 points each) Short Answer (14 @ 3 points each) Production:

Page 1 of 9 Contestant Number: Time: Rank: ADVANCED ACCOUNTING (110) Secondary REGIONAL 2015 Objective & Short Answer: Multiple Choice (20 @ 2 points each) Short Answer (14 @ 3 points each) Production:

Chapter 6 The annual report and accounts. The closure of the accounting cycle and Accounting information disclosed to the public

Chapter 6 The annual report and accounts The closure of the accounting cycle and Accounting information disclosed to the public 1 Six steps in the accounting cycle 1. Analyze transactions from the source

Chapter 6 The annual report and accounts The closure of the accounting cycle and Accounting information disclosed to the public 1 Six steps in the accounting cycle 1. Analyze transactions from the source

CHAPTER 2: FINANCIAL REPORTING MECHANISMS

Department of Management and Law CHAPTER 2: FINANCIAL REPORTING MECHANISMS Prof. Sandro Brunelli, Ph.D. brunelli@economia.uniroma2.it BUSINESS ACTIVITIES AND FINANCIAL STATEMENT ELEMENTS Business Activities

Department of Management and Law CHAPTER 2: FINANCIAL REPORTING MECHANISMS Prof. Sandro Brunelli, Ph.D. brunelli@economia.uniroma2.it BUSINESS ACTIVITIES AND FINANCIAL STATEMENT ELEMENTS Business Activities

Bookkeeping (Explanation)

") Bookkeeping (Explanation) 1. Part 1 Introduction; Bookkeeping: Past and Present 2. Part 2 Accrual Method 3. Part 3 Double-Entry, Debits and Credits 4. Part 4 General Ledger Accounts 5. Part 5 Debits and

Bookkeeping (Explanation) 1. Part 1 Introduction; Bookkeeping: Past and Present 2. Part 2 Accrual Method 3. Part 3 Double-Entry, Debits and Credits 4. Part 4 General Ledger Accounts 5. Part 5 Debits and

ACCT 652 Accounting. Payroll accounting. Payroll accounting Week 8 Liabilities and Present value

11-1 ACCT 652 Accounting Week 8 Liabilities and Present value Some slides Times Mirror Higher Education Division, Inc. Used by permission 2016, Michael D. Kinsman, Ph.D. 1 1 Payroll accounting I am sure

11-1 ACCT 652 Accounting Week 8 Liabilities and Present value Some slides Times Mirror Higher Education Division, Inc. Used by permission 2016, Michael D. Kinsman, Ph.D. 1 1 Payroll accounting I am sure

ACCOUNTING. The Wonder of the Worksheet

ACCOUNTING The Wonder of the Worksheet SAC 2012 P a g e 2 2012 State Group 11 Refer to the Table and to the work sheet. For questions 53 through 59, write the identifying letter of the best response on

ACCOUNTING The Wonder of the Worksheet SAC 2012 P a g e 2 2012 State Group 11 Refer to the Table and to the work sheet. For questions 53 through 59, write the identifying letter of the best response on

1 R E C A L =Revenue, Expense, Capital, Assets, Liability Decrease Increase R Revenue D Debit C Credit E Expense C Credit D Debit C Capital D Debit C Credit A Assets C Credit D Debit L Liability D Debit

1 R E C A L =Revenue, Expense, Capital, Assets, Liability Decrease Increase R Revenue D Debit C Credit E Expense C Credit D Debit C Capital D Debit C Credit A Assets C Credit D Debit L Liability D Debit

CHAPTER 12. Statement of Cash Flows. Study Objectives

CHAPTER 12 Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of

CHAPTER 12 Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of

CHAPTER 3 Selected Solutions. The Accounting Information System. Brief Topics Questions Exercises Exercises Problems

CHAPTER 3 Selected Solutions The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Brief Topics Questions Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5,

CHAPTER 3 Selected Solutions The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Brief Topics Questions Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5,

Twin Valley School District. What is the purpose and importance of accounting? Who are the users of accounting information?

Twin Valley School District Subject/Course: Advanced Accounting Course Objective: Students need to become familiar with financial accounting information and reports in order to make financial decisions.

Twin Valley School District Subject/Course: Advanced Accounting Course Objective: Students need to become familiar with financial accounting information and reports in order to make financial decisions.

COPYRIGHTED MATERIAL CHAPTER 1. The reporting requirements of the income statement, FINANCIAL STATEMENT REPORTING: THE INCOME STATEMENT

CHAPTER 1 FINANCIAL STATEMENT REPORTING: THE INCOME STATEMENT The reporting requirements of the income statement, balance sheet, statement of changes in cash flows, and interim reporting guidelines must

CHAPTER 1 FINANCIAL STATEMENT REPORTING: THE INCOME STATEMENT The reporting requirements of the income statement, balance sheet, statement of changes in cash flows, and interim reporting guidelines must

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Chapter 2 Review of the Accounting Process

True/False Questions 1. Owners' equity can be expressed as assets minus liabilities. True Learning Objective: 1 Level of Learning: 1 2. Debits increase asset accounts and decrease liability accounts. True

True/False Questions 1. Owners' equity can be expressed as assets minus liabilities. True Learning Objective: 1 Level of Learning: 1 2. Debits increase asset accounts and decrease liability accounts. True

Learning Objectives. Chapter 5. Balance Sheet. Learning Objective 1, 2, 3. Liquidity. Chapter Overview. Balance Sheet and Statement of Cash Flows

Chapter 5 Balance Sheet and Statement of Cash Flows Campbell, Coca-Cola, American Airlines, Borders Learning Objectives 1. Explain uses, limitations of a balance sheet 2. Identify major classifications

Chapter 5 Balance Sheet and Statement of Cash Flows Campbell, Coca-Cola, American Airlines, Borders Learning Objectives 1. Explain uses, limitations of a balance sheet 2. Identify major classifications

Financial Accounting. Final Exam

06169700 Financial Accounting Final Exam When you feel confident that you have mastered the material in Financial Accounting, complete the following exam by answering the questions and compiling your answers

06169700 Financial Accounting Final Exam When you feel confident that you have mastered the material in Financial Accounting, complete the following exam by answering the questions and compiling your answers

1. On Jan 1, 2003 Wilbur Retailers purchases merchandise on account for $349,000.

Name ID# Accounting 15.501/516 Spring 2004 Midterm 1 Exam Guidelines 1. Fill in your name above. Exams without names will not be graded. If you do not have an ID number, leave the corresponding space blank.

Name ID# Accounting 15.501/516 Spring 2004 Midterm 1 Exam Guidelines 1. Fill in your name above. Exams without names will not be graded. If you do not have an ID number, leave the corresponding space blank.

Disclaimer: This resource package is for studying purposes only EDUCATON

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

4-1 COMPLETING THE ACCOUNTING CYCLE

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an):

- Please choose one Wages outstanding given in the trial balance will be treated as a (an):") Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset Liability Revenue Deferred expense Question No: 2 ( Marks: 1 ) - Please choose

Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset Liability Revenue Deferred expense Question No: 2 ( Marks: 1 ) - Please choose

Name: Question Marks Suggested Time minutes minutes minutes minutes minutes

Name: MEMORIAL UNIVERSITY OF NEWFOUNDLAND FACULTY OF BUSINESS BUSINESS 6100 TERM TEST # 1 - Value - 21% of your final grade Term test #1 2015 Version 2 Question Marks Suggested Time 1 20 15 minutes 2 10

Name: MEMORIAL UNIVERSITY OF NEWFOUNDLAND FACULTY OF BUSINESS BUSINESS 6100 TERM TEST # 1 - Value - 21% of your final grade Term test #1 2015 Version 2 Question Marks Suggested Time 1 20 15 minutes 2 10

SU 3.1 Property, Plant, and Equipment

Part 1 Study Unit 3 SU 3.1 Property, Plant, and Equipment Overview Property, plant and equipment are also referred to as fixed assets, or capital assets. Last more than 1 year. Are for production or benefit

Part 1 Study Unit 3 SU 3.1 Property, Plant, and Equipment Overview Property, plant and equipment are also referred to as fixed assets, or capital assets. Last more than 1 year. Are for production or benefit

4. If cash is collected in advance for services, the revenue is recognized when the services are rendered.

ANSWERS TO QUESTIONS - CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting events in the period when such events occur, regardless of when cash is received or paid. The goal is

ANSWERS TO QUESTIONS - CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting events in the period when such events occur, regardless of when cash is received or paid. The goal is

Q1 Written biases and uncertainties 20 min 20 pts

ACCT Cost Accounting Exam 1 February 2008 Albrecht BGSU PIN# Q1 Written biases and uncertainties 20 min 20 pts Q2 Cost behavior 8 min 9 pts Q3 Cost behavior 9 min 9 pts Q4 Graphing cost patterns 5 min

ACCT Cost Accounting Exam 1 February 2008 Albrecht BGSU PIN# Q1 Written biases and uncertainties 20 min 20 pts Q2 Cost behavior 8 min 9 pts Q3 Cost behavior 9 min 9 pts Q4 Graphing cost patterns 5 min

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2)

") MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Particulars Rs. Opening written down value of machine 1,00,000 Cost of new machine

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Particulars Rs. Opening written down value of machine 1,00,000 Cost of new machine

MGT101 All Solved Past Papers of Mid Term Exam in one file By

MGT101 All Solved Past Papers of Mid Term Exam in one file By http://vustudents.ning.com MIDTERM EXAMINATION 7 th Dec 2009 MGT101- Financial Accounting Question No: 1 Income of the business includes: Cash

MGT101 All Solved Past Papers of Mid Term Exam in one file By http://vustudents.ning.com MIDTERM EXAMINATION 7 th Dec 2009 MGT101- Financial Accounting Question No: 1 Income of the business includes: Cash

Practice Multiple Choice Questions

FINAL EXAM REVIEW The comprehensive final exam consists of 50 questions, approximately 2/3 of which are from chapters 10 through 12. The remaining questions are from chapters 1 through 9. The questions

FINAL EXAM REVIEW The comprehensive final exam consists of 50 questions, approximately 2/3 of which are from chapters 10 through 12. The remaining questions are from chapters 1 through 9. The questions

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything!

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything! What We Will Do in This Session: 1. Gauge your level of confidence regarding this topic area 2. Review

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything! What We Will Do in This Session: 1. Gauge your level of confidence regarding this topic area 2. Review

ACCOUNTING COMPETENCY EXAM SAMPLE EXAM. 2. The financial statement or statements that pertain to a stated period of time is (are) the:

the:") ACCOUNTING COMPETENCY EXAM SAMPLE EXAM 1. The accounting process does not include: a. interpreting d. observing b. reporting e. classifying c. purchasing 2. The financial statement or statements that pertain

ACCOUNTING COMPETENCY EXAM SAMPLE EXAM 1. The accounting process does not include: a. interpreting d. observing b. reporting e. classifying c. purchasing 2. The financial statement or statements that pertain

In addition, sample interview questions for the position are enclosed for your review and information.

July 31, 2014 City of Mount Pleasant Tennessee Ms. Holly Alsup Finance Director 100 Public Square Mount Pleasant, Tennessee 38474 VIA ELECTRONIC MAIL Dear Ms. Alsup: Responsive to your request, the following

July 31, 2014 City of Mount Pleasant Tennessee Ms. Holly Alsup Finance Director 100 Public Square Mount Pleasant, Tennessee 38474 VIA ELECTRONIC MAIL Dear Ms. Alsup: Responsive to your request, the following

Financial Accounting (Corporation)

") Financial Accounting (Corporation) This course covers the topics shown below. Students navigate learning paths based on their level of readiness. Institutional users may customize the scope and sequence

Financial Accounting (Corporation) This course covers the topics shown below. Students navigate learning paths based on their level of readiness. Institutional users may customize the scope and sequence

4. If cash is collected in advance for services, the revenue is recognized when the services are rendered.

ANSWERS TO QUESTIONS - CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting events in the period when such events occur, regardless of when cash is received or paid. The goal is

ANSWERS TO QUESTIONS - CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting events in the period when such events occur, regardless of when cash is received or paid. The goal is

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT. (Manual Case, and Working Papers) Scott Osborne, CPA

Scott Osborne, CPA") DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

Chapter 3. The Balance Sheet and Financial Disclosures

Chapter 3 The Balance Sheet and Financial Disclosures AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Chapter 3 The Balance Sheet and Financial Disclosures AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Guide to Bookkeeping Concepts

Guide to Bookkeeping Concepts Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Guide to Bookkeeping Concepts Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Chapter 02 - Analyzing and Recording Transactions. Chapter Outline