Bank Accounting Essentials

|

|

|

- Edwina Short

- 6 years ago

- Views:

Transcription

1 Your State Association Presents Bank Accounting Essentials Program Materials Use this document to follow along with the webinar presentation. Please test your system before the broadcast. Be sure to print enough copies for all listeners. Friday, June 17, 2016 Presenter: Eileen Iles Technical Support (for faster service please submit inquiries via or online): (Registration & Tech Support): - Phone- (877) FOR ADDITIONAL ASSISTANCE PLEASE REFER TO OUR FAQs

2 Bank Accounting Essentials Presented By Your State Banking Association 1

3 KEY TOPICS Accounting Information System Defining Accounting and Role of Accounting in Decision Making Forms of Business Organizations Decision Makers: The Users of Accounting Information Accounting Equation of Assets, Liabilities, Equity, Income, and Expenses Generally Accepted Accounting Principles Introduction of Financial Statements: Balance Sheet, Income Statement, Statement of Stockholders Equity, Statement of Comprehensive Income, Statement of Cash Flows Recording Financial Transactions Double-Entry System of Debits and Credits Recording and Posting Transactions Measuring Financial Income Accrual Accounting The Basics of Financial Statements Reading and Understanding the Financial Statements Basic Techniques to Analyzing the Financial Statements and Evaluating the Financial Condition 2 2

4 Definition of Accounting Accounting is an information system that identifies, records, and communicates the economic events of an organization to interested users. Users of accounting information may be internal or external to the organization. 3 3

5 Role of Accounting in Decision Making Accounting information system tracks and reports the results of the business activities: Financing borrowing money or selling shares of stock to investors. To whom the company owes money are creditors. Creditors claims on the business are liabilities. A corporation may also obtain funds by selling shares of stock to investors. Creditors have legal right to be paid in accordance to the terms of the agreement. Creditor claims are required to be paid before ownership claims. Payments to stockholders are called dividends. Dividends are paid as long as the corporation has sufficient cash to pay creditors. Also, once stock is issued, the corporation has no obligation to buy the shares of stock back. Investing Once the cash is obtained, assets may be purchased for the operations of the business. Assets may be purchased also for the purpose of investing for the business. Operating After the assets are obtained, the organization may begin its operating activities. Revenue is the increase of assets arising from the sale of a product or service. Expenses are the cost of assets consumed or services used in the process of generating revenue. When revenue exceeds expenses, net income is the result. 4 4

6 Forms of Business Organizations Sole Proprietorship a business owned by one individual. A sole proprietorship is simple to establish and is owner controlled. Sole proprietor is legally liable for all debts of the business. Partnership a business owned by more than one individual. A partnership is also simple to establish and the control is shared. Partners are legally liable for all debts of the partnership. Corporation a business organization that is a separate legal entity owned by stockholders. A corporation is relatively easier to raise funds and transfer ownership. Corporate stockholders are not legally liable for all debts of the corporation. 5 5

7 Decision Makers: The Users of Accounting Information Individuals that have an interest in the ongoing activities of he business are the users of the accounting information. Internal users includes departmental personnel, management, Board of Directors. Questions asked by internal users include: o Is profitability sufficient to pay bonuses? o Is cash sufficient to pay the bills? o Which products or services are profitable? o What is the value of investments owned by the business? o Have facilities expenses increased from last year? Accounting information that may be provided to internal users are projections of income of services or products, income and expense variance analysis, and forecasts of cash needs. External users include investors, creditors, regulatory agencies, taxing authorities, customers. Questions asked by external users include: o Is the bank complying with regulatory capital requirements? o Is the business complying with tax rules? o Is the business profitable? o Does the bank appear to be sustainable? 6 6

8 Introduction of Financial Statements: Balance Sheet 7 7

9 Introduction of Financial Statements: Balance Sheet, Income Statement, Statement of Cash Flows 8 8

10 Accounting Equation Balance sheet reports assets and claims to the assets at a specific point in time. Assets must be balanced by the claims to the assets. Claims of creditors are liabilities. Claims of owners are stockholders equity. Stockholders equity consists of common stock and retained earnings. Accounting Equation Assets = Liabilities + Stockholders Equity Economic events to be recorded in the financial statements is accounting transactions. An accounting transaction occurs when assets, liabilities, or stockholders equity change as a result of an economic event. The accounting equation must always balance. Each transaction has a dual or double sided effect on the equation. For example, if an asset is increased, there must be a decrease in another asset, or increase in a liability, or increase in stockholders equity. 9 9

11 Accounting Equation Accounting Equation Assets = Liabilities + Stockholders Equity Example ~ On March 5, 2015, purchase of supplies on credit for $4,500. Basic Analysis: Supplies is increased for $4,500. Accounts payable is increased for $4,500. Acctg Equation: Assets = Liabilities + Stockholders Equity Supplies = Accounts Payable $4,500 = $4,500 Example ~ On March 15, 2015, paid employee salaries of $8,100. Basic Analysis: Cash is decreased $8,100. Salaries expense is increased $8,100. Acctg Equation: Assets = Liabilities + Stockholders Equity Cash = Salaries Expense ($8,100) = ($8,100) 10 10

12 Generally Accepted Accounting Principles Preparing financial statements is based on certain assumptions and generally accepted accounting principles ( GAAP ). Assumptions Monetary unit only those transactions or events that can be expressed in money are reflected in the accounting records. Economic entity every economic entity can be identified and accounted for. Time period the life of a business can be reported in time periods and reports covering those periods may be produced. Going concern assumption that the business will remain in operation for the foreseeable future. Otherwise, assets would be valued on balance sheet at liquidation value. Principles Cost principle assets are recorded at cost. Full disclosure principle all circumstances and events that would make a difference to financial statement users should be disclosed. Revenue recognition revenue should be recognized in the period in which it is earned. In a service company, revenue is earned in the period in which it is earned. Matching expenses should be recorded in the time period in which efforts were expended to generate the revenue

13 Introduction of Financial Statements: Balance Sheet, Income Statement, Statement of Retained Earnings, and Statement of Cash Flows Balance Sheet As of a point in time, assets owed by the business and monies owed (liabilities). Income Statement Revenue (interest income, noninterest income) earned and expenses (interest expense, noninterest expense, provision for loan losses) incurred for a period of time. Statement of Retained Earnings Dividends distributed to owners and capital retained in business for future growth. Statement of Cash Flows sources and uses of cash for a period of time. Interrelationships of Financial Statements 12 12

14 Introduction of Financial Statements: Balance Sheet 13 13

15 Introduction of Financial Statements: Balance Sheet, Income Statement, Statement of Cash Flows 14 14

16 Introduction of Financial Statements: Income Stmt 15 15

17 16 16

18 Introduction of Financial Statements: Stmt of Comprehensive Income 17 17

19 Introduction of Financial Statements: Consolidated Stmt of Stockholders Equity 18 18

20 Introduction of Financial Statements: Consolidated Stmt of Cash Flows 19 19

21 Introduction of Financial Statements: Consolidated Stmt of Cash Flows 20 20

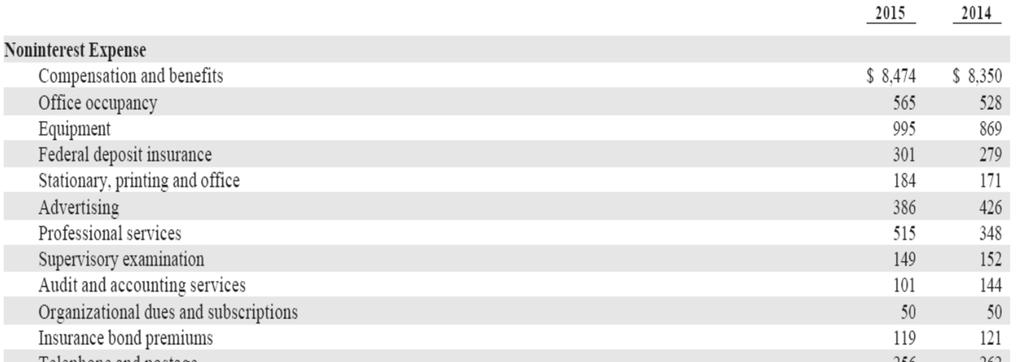

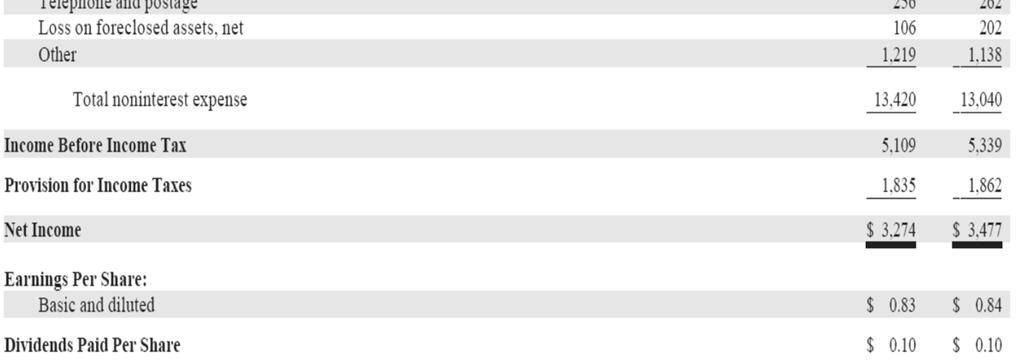

22 The following consolidated statement of income, balance sheet, and changes in stockholders equity were downloaded from investor.shreholder.com for JP Morgan Chase & Co

23 22 22

24 23 23

25 24 24

26 Recording Financial Transactions: Double Entry System of Debits and Credits Accounting information systems use accounts. An account is an individual accounting record of increases and decreases to a specific asset, liability, stockholders equity, income, or expense item. An account consists of the title of the account, left or debit side, and right or credit side. Because the alignment of these items resemble a T, it is referred to as a T account. Debit (Dr.) means left. Credit (Cr.) means right. These terms do not mean increase and decrease. Debit and credit are used in the recording process to indicate where entries are made in accounts. Entering an amount on the left side of an account is called debiting the account and entering an amount on the right side of an account is called crediting the account. When comparing the totals of the debit (left) side and credit (right) side, the account will have a debit balance if the total debits exceed the total credits. Conversely, an account will have a credit balance if the total credits exceed the total debits

27 Recording Financial Transactions: Double Entry System of Debits and Credits Normal Balances: Assets Liabilities Debit Credit Debit Credit Increase Decrease Decrease Increase Normal Balance Normal Balance Contra-Asset (Allow for Loan Losses) Retained Earnings Debit Credit Debit Credit Decrease Increase Decrease Increase Normal Balance Normal Balance 26 26

28 Recording Financial Transactions: Double Entry System of Debits and Credits Normal Balances: Retained Earnings Debit Decrease Credit Increase Normal Balance Income) Expenses(incl Interest Exp, Provision, Noninterest Exp) Revenue (Interest Income, Noninterest Debit Credit Debit Credit Increase Decrease Decrease Increase Normal Balance Normal Balance 27 27

29 Recording Financial Transactions: Double Entry System of Debits and Credits Would Common Stock be increased by debit or credit? What is its normal balance? Common Stock Debit Credit Would Dividends be increased by debit or credit? What is its normal balance? Dividends Debit Credit 28 28

30 Recording Financial Transactions: Double Entry System of Debits and Credits For the Bank, what is the normal balance for Accumulated Depreciation? Accumulated Depreciation Depreciation Expense Debit Credit Debit Credit For the Bank, what is the normal balance for deposits? Deposits Debit Credit 29 29

31 Recording Financial Transactions: Double Entry System of Debits and Credits Example ~ Transaction: Purchase of US Treasury for $10,000. Basic Analysis: US Treasury (Investments) is increased for $10,000. Cash is decreased for $10,000. What is the impact on the Acctg equation? Acctg Equation: Assets = Liabilities + Stockholders Equity How should the transaction be recorded in the T accounts? What accounts should the transaction be recorded to? Account Account Debit Credit Debit Credit 30 30

32 Recording Financial Transactions: Double Entry System of Debits and Credits Example ~ SOLUTION Transaction: Purchase of US Treasury for $10,000. Basic Analysis: US Treasury (Investments) is increased for $10,000. Cash is decreased for $10,000. Acctg Equation: Assets = Liabilities + Stockholders Equity Investments = $10,000 = Cash = ($10,000) = $0 = $0 Dr/Cr Analysis: Debit increases investments. Credit decreases cash. T Accounts: Investments Cash Debit Credit Debit Credit $10,000 $10,

33 Recording Financial Transactions: Double Entry System of Debits and Credits Example ~ Transaction: Purchase of workmans compensation insurance on Jun 1, 2015 expiring Aug 31, Basic Analysis: Acctg Equation: Assets = Liabilities + Stockholders Equity Dr/Cr Analysis: T Accounts: Account Account Debit Credit Debit Credit 32 32

34 Recording Financial Transactions: Double Entry System of Debits and Credits Example ~ SOLUTION Transaction: Purchase of workmans compensation insurance for $6,000 on Jun 1, 2015 expiring Aug 31, Basic Analysis: Workmans compensation insurance increases $6,000. Cash decreases $6,000. Acctg Equation: Assets = Liabilities + Stockholders Equity Prepaid Insurance = $6,000 = Cash = ($6,000) = $0 = $0 Dr/Cr Analysis: Debit increases prepaid insurance. Credit decreases cash. T Accounts: Prepaid Insurance Cash Debit Credit Debit Credit $6,000 $6,

35 Recording Financial Transactions: Recording and Posting Transactions Steps to recording transactions: 1. Analyze the transaction. 2. Enter the transaction into a journal. Companies use different journals based on the nature of the transaction. Though each business has a general journal. Transactions are entered into a journal before they are transferred to the accounts. The journal discloses the complete transaction, provides a chronological record of transactions, and helps to locate errors because the journal allows to readily see the debits and credits. 3. Transfer the journal information to the appropriate accounts in the general ledger

36 Bank General Journal 2015 Date Account Titles and Explanations Debit Credit Jul 01 Cash Common Stock Cash invested in Bank by investors $100,000 $100,000 Jul 03 Investments Cash Purchase of investments $20,000 $20,000 Jul 05 Supplies Cash Purchase of supplies $11,000 $11,000 Jul 07 Cash Other Liability Received deposit in advance from commercial customer $3,000 $3,

37 Bank General Ledger Account Account No Cash 1000 Date 2015 Account Titles and Explanations Debit Credit Balance $125,000 Jul 01 Cash invested in business $100,000 Jul 03 Purchase of investments $20,000 Jul 05 Purchase of supplies $11,000 Jul 07 Received customer deposit in advance $3,000 Jul 15 Purchase of equipment $150,000 Jul 15 Jul 31 Payment of salaries $22,000 $25,000 Loans 1200 Jul 31 $130,000 Supplies 1300 $129,000 Jul 05 Purchase of supplies $11,000 Jul 31 $140,000 Equipment 1500 $250,000 Jul 15 Purchase of equipment $150,000 Jul 31 $400,000 Land 3000 Jul 31 $300,000 Building 3100 Jul 31 $480,

38 Recording Financial Transactions: Recording and Posting Transactions Example ~ Transaction: Purchase of workmans compensation insurance for $6,000 on Jun 1, 2015 expiring Aug 31, Basic Analysis: Workmans compensation insurance increases $6,000. Cash decreases $6,000. Journal Entry: Jun 1 Prepaid Insurance $6,000 Cash $6,000 Purchase of workmans comp prepaid insurance. Posting to Accounts in General Ledger: Prepaid Insurance Cash Jun 1 $6,000 Jun 1 $6,

39 Recording Financial Transactions: Recording and Posting Transactions Example ~ Transaction: Purchase of US Treasury for $10,000. Basic Analysis: US Treasury (Investments) is increased for $10,000. Cash is decreased for $10,000. Journal Entry: Jun 1 Investments $10,000 Cash $10,000 Purchase of US Treasury investment. Posting to Accounts in General Ledger: Investments Cash Jun 1 $10,000 Jun 1 $10,

40 Measuring Financial Income: Accrual Accounting Accrual Basis Accounting - Transactions that change a business financial statements are recorded in the period in which the event occurs and not the period in which the business receives or pays cash. Revenues are recognized when earned and expenses are recognized when incurred. Cash Basis Accounting revenue is recorded when cash is received. Expenses are recorded when cash is paid. Example ~ Received payment of $14,000 in May 2015 for interest income due as of April What is the impact on the income statement under cash basis? April 2015 May 2015 Interest Income $14,000 increase Expense 0 Net Income $14,000 increase In which month does the cash get recorded? What is the impact on the balance sheet for April and May 2015? April 2015 May 2015 Assets (Cash) $14,000 increase 39 39

41 Measuring Financial Income: Accrual Accounting Accrual Basis Accounting - Transactions that change a business financial statements are recorded in the period in which the event occurs and not the period in which the business receives or pays cash. Revenues are recognized when earned and expenses are recognized when incurred. Cash Basis Accounting revenue is recorded when cash is received. Expenses are recorded when cash is paid. Example ~ Received payment of $14,000 in May 2015 for interest income due as of April What is the impact on the income statement under accrual basis? April 2015 May 2015 Interest Income Expense Net Income $14,000 increase $14,000 increase In which month does the cash get recorded? What is the impact on the balance sheet for April and May 2015? April 2015 May 2015 Assets (Accrued Int Receiv)$14,000 increase Assets (Cash) Assets (Accrued Int Receivable) $14,000 increase $14,000 decrease 40 40

42 Measuring Financial Income: Accrual Accounting Accrual Basis Accounting - Transactions that change a business financial statements are recorded in the period in which the event occurs and not the period in which the business receives or pays cash. Revenues are recognized when earned and expenses are recognized when incurred. Cash Basis Accounting revenue is recorded when cash is received. Expenses are recorded when cash is paid. Example ~ Bank owes deposit customers total of $200,000 interest for month of April. Interest is credited to customer statements 5 th day of following month. What is the impact on the income statement under cash basis? April 2015 May 2015 Expense Net Income $200,000 increase $200,000 decrease In which month does the cash get recorded? What is the impact on the balance sheet for April and May 2015? April 2015 May 2015 Assets (Cash) $200,000 decrease 41 41

43 Measuring Financial Income: Accrual Accounting Accrual Basis Accounting - Transactions that change a business financial statements are recorded in the period in which the event occurs and not the period in which the business receives or pays cash. Revenues are recognized when earned and expenses are recognized when incurred. Cash Basis Accounting revenue is recorded when cash is received. Expenses are recorded when cash is paid. Example ~ Bank owes deposit customers total of $200,000 interest for month of April. Interest is credited to customer statements 5 th day of following month. What is the impact on the income statement under accrual basis? April 2015 May 2015 Interest Income Expense Net Income $200,000 increase $200,000 decrease In which month does the cash get recorded? What is the impact on the balance sheet for April and May 2015? April 2015 May 2015 Liabs (Accrued Int Pay)$200,000 increase Assets 2016 Crowe (Cash) Horwath LLP Assets (Accrued Int Pay) $200,000 decrease $200,000 decrease 42 42

44 Measuring Financial Income: Accrual Accounting Accrual Basis Accounting - Transactions that change a business financial statements are recorded in the period in which the event occurs and not the period in which the business receives or pays cash. Revenues are recognized when earned and expenses are recognized when incurred. Cash Basis Accounting revenue is recorded when cash is received. Expenses are recorded when cash is paid. Example ~ Paid employee compensation of $23,000 on May 1, 2015 for work performed in April What is the impact on the income statement under cash basis? April 2015 May 2015 Revenue Expense Net Income $23,000 increase $23,000 decrease In which month does the cash get recorded? What is the impact on the balance sheet for April and May 2015? April 2015 May 2015 Assets (Cash) $23,000 decrease 43 43

45 Measuring Financial Income: Accrual Accounting Accrual Basis Accounting - Transactions that change a business financial statements are recorded in the period in which the event occurs and not the period in which the business receives or pays cash. Revenues are recognized when earned and expenses are recognized when incurred. Cash Basis Accounting revenue is recorded when cash is received. Expenses are recorded when cash is paid. Example ~ Paid employee compensation of $23,000 on May 1, 2015 for work performed in April What is the impact on the income statement under accrual basis? Revenue Expense $23,000 increase Net Income ($23,000) April 2015 May 2015 In which month does the cash get recorded? What is the impact on the balance sheet for April and May 2015? April 2015 May 2015 Liabilities (Accrued Compensation)$23,000 increase Assets (Cash) $23,000 decrease Liabilities (Accrued Compensation) $23,000 decrease 44 44

46 Problem from Transaction Analysis to Posting to General Ledger Example ~ Transaction: On Jul 1, 2015, received invoice from Ad Agency for ad placed in magazine on May 16, 2015 to advertise new Bank product. Basic Analysis: Acctg Equation: Assets = Liabilities + Stockholders Equity Dr/Cr Analysis: T Accounts: 45 45

47 Problem from Transaction Analysis to Posting to General Ledger Example ~ Transaction: On Jul 1, 2015, received invoice from Ad Agency for ad placed in magazine on May 16, Journal Entry: Posting: 46 46

48 Problem from Transaction Analysis to Posting to General Ledger - Solution Example ~ SOLUTION Transaction: On Jul 1, 2015, received invoice from Ad Agency for ad placed in magazine on May 16, 2015 for $2,600 to advertise Bank s new product. Basic Analysis: Owe for advertising invoice $2,600. Acctg Equation: Assets = Liabilities + Stockholders Equity = Accounts Payable + $2,600 Advertising expense ($2,600) $0 = $0 Dr/Cr Analysis: Debit increases advertising expense. Credit increases accounts payable. T Accounts: Advertising expense Accounts payable Debit Credit Debit Credit $2,600 $2,

49 Problem from Transaction Analysis to Posting to General Ledger - Solution Example ~ SOLUTION Transaction: On Jul 1, 2015, received invoice from Ad Agency for ad placed in magazine on May 16, Journal Entry: Jul 01 Advertising expense $2,600 Accounts payable $2,600 Receipt of invoice for ad. Posting to Accounts in General Ledger: Advertising expense Accounts payable Jul 01 $2,600 Jul 01 $2,

50 Problem from Transaction Analysis to Posting to General Ledger Example ~ Transaction: On Jul 18, 2015, a customer deposited $1,050 at the Bank. For the Bank, what is the transaction? Basic Analysis: Acctg Equation: Assets = Liabilities + Stockholders Equity Dr/Cr Analysis: T Accounts: 49 49

51 Problem from Transaction Analysis to Posting to General Ledger Example ~ Transaction: On Jul 18, 2015, a customer deposited $1,050 at the Bank in a money market account. For the Bank, what is the transaction? Journal Entry: Posting to Accounts in General Ledger: 50 50

52 Problem from Transaction Analysis to Posting to General Ledger - Solution Example ~ Solution Transaction: On Jul 18, 2015, a customer deposited $1,050 at the Bank in a money market. For the Bank, what is the transaction? Basic Analysis: Bank received cash. Cash increased. Bank owes the customer the money back at some point. Acctg Equation: Assets = Liabilities + Stockholders Equity Cash = Deposits $1,050=$1,050 Dr/Cr Analysis: Debit increases cash. Credit increases liabilities (deposits). T Accounts: Cash Deposits (MMA) Debit Credit Debit Credit $1,050 $1,

53 Journal Entries Example Transaction: On Jul 18, 2015, a customer withdrew $3,100 from their savings account. For the Bank, what is the transaction? Journal Entry: Jul 18 Example Transaction: On Jul 31, 2015, a customer closed their NOW account. Balance was $2,200. $.92 interest owed. For the Bank, what is the transaction? Journal Entry: Jul

54 Journal Entries - Solution Example Transaction: On Jul 18, 2015, a customer withdrew $3,100 from their savings account. For the Bank, what is the transaction? Journal Entry: Jul 18 Deposits (Sav) $3,100 Cash $3,100 Withdrew funds from Savings account. Example Transaction: On Jul 31, 2015, a customer closed their NOW account. Balance was $2,200. $.92 interest owed. For the Bank, what is the transaction? Journal Entry: Jul 31 Deposits (NOW) $2,200 Interest Pay $.92 Cash $2, Withdrew funds from Savings account. Jul 31 Interest Exp (NOW) $.92 Interest Pay $.92 System auto accrues interest

55 Basics of Financial Statements: Basic Techniques to Analyzing the Financial Statements and Evaluating the Financial Condition Three basic tools to analyzing financial statements is: 1. Horizontal analysis 2. Vertical analysis 3. Ratio analysis Horizontal analysis evaluate financial statement data over period of time. The purpose is to determine the increase or decrease as a percentage of dollars or percentage. Percentage Change = (Current year amount Base year amount) / (Base year amount) Vertical analysis evaluate financial statement data that expresses each item in a financial statement as a percent of a base amount. Total assets (and total liabilities and equity) is stated as 100% and other data items are compared to total assets (total liabilities and equity)

56 Basics of Financial Statements: Basic Techniques to Analyzing the Financial Statements and Evaluating the Financial Condition Horizontal Analysis Bank Balance Sheet Horizontal Analysis Increase (Decrease) Amount % Cash % Int bearing deposits % Int bearing time deposits % Avail for sale securities % Loans, net of allow for loan losses % Premises and equipment FHLB Stock Foreclosed assets Accrued interest receivable Bank owned life insurance Mortgage servicing rights Deferred income taxes Other Total Assets Deposits Demand Savings, NOW Certificates of deposit Brokered certif of deps Repurchase agreements FHLB advances Advances from borrowers for taxes and ins Accrued post retirement benefit obligation Accrued interest pay Other Total Liabilities Common Stock Addl paid in capital Unearned ESOP Retained earnings Accum other comprehensive income, net of tax Total Stockholders Equity Total Liabs and Stockholders Equity

57 Basics of Financial Statements: Basic Techniques to Analyzing the Financial Statements and Evaluating the Financial Condition Horizontal Analysis - Solution Bank Balance Sheet Horizontal Analysis Increase (Decrease) Amount % Cash % Int bearing deposits % Int bearing time deposits % Avail for sale securities % Loans, net of allow for loan losses % Premises and equipment % FHLB Stock % Foreclosed assets % Accrued interest receivable % Bank owned life insurance % Mortgage servicing rights % Deferred income taxes % Other % Total Assets % Deposits Demand % Savings, NOW % Certificates of deposit % Brokered certif of deps % Repurchase agreements % FHLB advances % Advances from borrowers for taxes and ins % Accrued post retirement benefit obligation % Accrued interest pay % Other % Total Liabilities % Common Stock % Addl paid in capital % Unearned ESOP % Retained earnings % Accum other comprehensive income, net of tax % Total Stockholders Equity % Total Liabs and Stockholders Equity % 56 56

58 Basics of Financial Statements: Basic Techniques to Analyzing the Financial Statements and Evaluating the Financial Condition Vertical Analysis Bank Balance Sheet Vertical Analysis Amount % Amount % Cash % Int bearing deposits 751 0% 116 Int bearing time deposits 250 0% 250 Avail for sale securities % Loans, net of allow for loan losses % Premises and equipment % 5124 FHLB Stock % 5425 Foreclosed assets 50 0% 436 Accrued interest receivable % 1788 Bank owned life insurance % 8025 Mortgage servicing rights 505 0% 506 Deferred income taxes % 2059 Other 379 0% 489 Total Assets % Deposits Demand % Savings, NOW % Certificates of deposit % Brokered certif of deps % Total Deposits % Repurchase agreements % 2324 FHLB advances % Advances from borrowers for taxes and ins 955 0% 997 Accrued post retirement benefit obligation % 2387 Accrued interest pay 65 0% 96 Other % 2110 Total Liabilities % Common Stock 41 0% 44 Addl paid in capital % Unearned ESOP % Retained earnings % Accum other comprehensive income, net of tax 999 0% 1081 Total Stockholders Equity % Total Liabs and Stockholders Equity %

59 Basics of Financial Statements: Basic Techniques to Analyzing the Financial Statements and Evaluating the Financial Condition Vertical Analysis - Solution Bank Balance Sheet Vertical Analysis Amount % Amount % Cash % % Int bearing deposits 751 0% 116 0% Int bearing time deposits 250 0% 250 0% Avail for sale securities % % Loans, net of allow for loan losses % % Premises and equipment % % FHLB Stock % % Foreclosed assets 50 0% 436 0% Accrued interest receivable % % Bank owned life insurance % % Mortgage servicing rights 505 0% 506 0% Deferred income taxes % % Other 379 0% 489 0% Total Assets % % Deposits Demand % % Savings, NOW % % Certificates of deposit % % Brokered certif of deps % % Total Deposits % % Repurchase agreements % % FHLB advances % % Advances from borrowers for taxes and ins 955 0% 997 0% Accrued post retirement benefit obligation % % Accrued interest pay 65 0% 96 0% Other % % Total Liabilities % % Common Stock 41 0% 44 0% Addl paid in capital % % Unearned ESOP % % Retained earnings % % Accum other comprehensive income, net of tax 999 0% % Total Stockholders Equity % % Total Liabs and Stockholders Equity % % 58 58

60 Basics of Financial Statements: Basic Techniques to Analyzing the Financial Statements and Evaluating the Financial Condition Ratio Analysis Ratio analysis includes liquidity, solvency, and profitability ratios. Liquidity ratios measure the business short term ability to pay its obligations as due and meet unexpected needs for cash. Current ratio: Current assets/current Liabilities Current cash debt coverage ratio: Cash provided by operations/avg current liabilities 59 59

61 Basics of Financial Statements: Basic Techniques to Analyzing the Financial Statements and Evaluating the Financial Condition Ratio Analysis Compute each liquidity ratio for Bank for Current ratio: Current assets/current Liabilities Current cash debt coverage ratio: Cash provided by operations/avg current liabilities Assume cash provided by operations = $ 296,

62 Basics of Financial Statements: Basic Techniques to Analyzing the Financial Statements and Evaluating the Financial Condition Ratio Analysis - Solution Compute each liquidity ratio for Bank for 2015 Current ratio: Current assets/current Liabilities (Cash+Int bearing deposits+avail for sale securities) = $12, ,630= $183,854 Current liabilities (Demand, savings/now, advances from borrowers, accrued payables) = $17, , ,759 = $171,606 Current ratio = 1.07 Current cash debt coverage ratio: Cash provided by operations/avg current liabilities Assume cash provided by operations = $ 296,000 Avg current liabilities = ($20,847+20,185)/2 = $171,606 Current cash debt coverage =

63 Basics of Financial Statements: Basic Techniques to Analyzing the Financial Statements and Evaluating the Financial Condition Ratio Analysis Ratio analysis includes liquidity, solvency, and profitability ratios. Solvency ratios measure the business ability to survive over a long period of time. Debt to total assets ratio: Total debt/total assets Cash debt coverage ratio: Cash provided by operations/avg total liabilities Free cash flow ratio: Cash provided by operations Capital expenditures Dividends paid 62 62

64 Basics of Financial Statements: Basic Techniques to Analyzing the Financial Statements and Evaluating the Financial Condition Ratio Analysis - Solution Compute each solvency ratio for Bank for 2015 Solvency ratios measure the business ability to survive over a long period of time. Debt to total assets ratio: Total debt/total assets $483,232/$563,668 =.86 Cash debt coverage ratio: Cash provided by operations/avg total liabilities Assume cash provided by operations = $ 296,000 $296,000/(($483, )/2) =.62 Free cash flow ratio: Cash provided by operations Capital expenditures Dividends paid Assume cash provided by operations = $ 296,000 Assume dividends paid and capital expenditures = $0 $296,

65 Basics of Financial Statements: Basic Techniques to Analyzing the Financial Statements and Evaluating the Financial Condition Ratio Analysis Compute each profitability ratio for the Bank for Profitability ratios measure the income or success of a business for a period of time. Return on Assets: Net Income/Avg Assets Return on Equity: Net Income/Avg Equity 64 64

66 Basics of Financial Statements: Basic Techniques to Analyzing the Financial Statements and Evaluating the Financial Condition Ratio Analysis - Solution Compute each profitability ratio for the Bank for Profitability ratios measure the income or success of a business for a period of time. Return on Assets: Net Income/Avg Assets $3,274/(($563,668+$551,343)/2) =.0059 Return on Equity: Net Income/Avg Equity $3,274/(($80,436+82,086)/2)=

67 Questions? Thank YOU for your attendance and participation!! 66 66

Principles of Accounting II

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Accounting Basics Introduction To Financial Accounting

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

CHAPTER 8 REVIEW EXERCISES (continued) Exercise 7, p. 326 A. Year Ended December 31, 20 8 BALANCE SHEET INCOME STATEMENT ADJUSTMENTS TRIAL BALANCE

Exercise 7, p. 326 A. Year Ended December 31, 20 8 BALANCE SHEET INCOME STATEMENT ADJUSTMENTS TRIAL BALANCE") Exercise 7, p. 326 A. Oakville Journal Worksheet Year Ended December, 28 TRIAL BALANCE ACCOUNTS ADJUSTMENTS INCOME STATEMENT BALANCE SHEET Bank Accounts Receivable Prepaid Insurance Land Buildings Acc.

Exercise 7, p. 326 A. Oakville Journal Worksheet Year Ended December, 28 TRIAL BALANCE ACCOUNTS ADJUSTMENTS INCOME STATEMENT BALANCE SHEET Bank Accounts Receivable Prepaid Insurance Land Buildings Acc.

Business Background Management is responsible for preparing...

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

SOLUTIONS Learning Goal 8

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 5 Adjusting Entries and the Trial Balance Chapter 4 Adjusting entries Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this

ACC100 Introduction to Accounting Week 5 Adjusting Entries and the Trial Balance Chapter 4 Adjusting entries Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this

SOLUTIONS. Learning Goal 14

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

Module 3 Exhibits and Key Terms. Table of Contents. 1 Principles of Accounting Adjustments for Financial Reporting

Table of Contents Exhibit 14: Cash basis and accrual basis of accounting compared... 2 Exhibit 15: Summary fiscal year ending by Month... 2 Exhibit 16: Two classes and four types of adjusting entries...

Table of Contents Exhibit 14: Cash basis and accrual basis of accounting compared... 2 Exhibit 15: Summary fiscal year ending by Month... 2 Exhibit 16: Two classes and four types of adjusting entries...

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

2. Which of the following is an external user of accounting information? A) Labor unions. B) Finance directors. C) Company officers. D) Managers.

Labor unions. B) Finance directors. C) Company officers. D) Managers.") Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

REVIEW Which of the following would be classified as external users of financial statements?

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

Accounting Cycle Review Problem. Michelle Clark. Accounting 1110 Section 401. Fall 2014

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

4-1 COMPLETING THE ACCOUNTING CYCLE

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

Chapter 3 Question Review 1

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 2 Review of the Accounting Process

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Disclaimer: This resource package is for studying purposes only EDUCATON

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Chapter 2 Review of the Accounting Process

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Ch.2 A Review of the Accounting Cycle

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

Chapter 4: Completing the Accounting Cycle

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

Seminar on Bookkeeping Basics

Seminar on Bookkeeping Basics (Handout) Our materials are copyright AccountingCoach, LLC and are for personal use by the original purchaser only. We do not allow our materials to be reproduced or distributed

Seminar on Bookkeeping Basics (Handout) Our materials are copyright AccountingCoach, LLC and are for personal use by the original purchaser only. We do not allow our materials to be reproduced or distributed

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

Chapter 1. assembled and processed

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

Work4Me. Algorithmic Version. Problem Six. Adjusting Entries, Closing Entries, and Financial Analysis. 1 st Web-Based Edition

Work4Me Algorithmic Version 1 st Web-Based Edition Problem Six Adjusting Entries, Closing Entries, and Financial Analysis Page 1 Emory Legal Services, Incorporated CHART OF ACCOUNTS Problem 6 ASSETS REVENUE

Work4Me Algorithmic Version 1 st Web-Based Edition Problem Six Adjusting Entries, Closing Entries, and Financial Analysis Page 1 Emory Legal Services, Incorporated CHART OF ACCOUNTS Problem 6 ASSETS REVENUE

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

Accounting 1A Class Notes Chapter 3 The Adjusting Process

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

Talking Accounting Definitions

Talking Accounting Definitions Introduction to Accounting week 1 Accounting The information system that measures business activities, processes that information into reports, and communicates the result

Talking Accounting Definitions Introduction to Accounting week 1 Accounting The information system that measures business activities, processes that information into reports, and communicates the result

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

*Define and differentiate the accrual method and cash method of recording transactions.

Accounting 1 *Define and differentiate the terms accounting, auditing, and bookkeeping: --Accounting the process of recording, reporting and analyzing financial transactions. --Bookkeeping the process

Accounting 1 *Define and differentiate the terms accounting, auditing, and bookkeeping: --Accounting the process of recording, reporting and analyzing financial transactions. --Bookkeeping the process

Adjusting The Accounts

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

Chapter 4 Question Review 1

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

Analyzing Transactions

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

Question 1: What is the relationship between a transaction, a journal, a ledger, and a chart of accounts? A transaction is the record used to reflect the activity of a business. These transactions are

1

www.accountancyknowledge.com 1 CIMA C02 Fundamental of Financial Accounting Overview of Financial Accounting www.accountancyknowledge.com 2 Definitions of Accounting Accounting is the language of the business

www.accountancyknowledge.com 1 CIMA C02 Fundamental of Financial Accounting Overview of Financial Accounting www.accountancyknowledge.com 2 Definitions of Accounting Accounting is the language of the business

AccountingCoach.com Financial Ratios

AccountingCoach.com Financial Ratios All underlined words are defined in the attached Glossary (Pages 13 20). Introduction to Financial Ratios When analyzing computing financial ratios and when doing other

AccountingCoach.com Financial Ratios All underlined words are defined in the attached Glossary (Pages 13 20). Introduction to Financial Ratios When analyzing computing financial ratios and when doing other

BUSS 1030 ACCOUNTING, BUSINESS AND SOCIETY NOTES

WEEK 1 BUSS 1030 ACCOUNTING, BUSINESS AND SOCIETY NOTES Accounting information system measuring business activity, processes data into reports and communicates results to decision makers (ethics important

WEEK 1 BUSS 1030 ACCOUNTING, BUSINESS AND SOCIETY NOTES Accounting information system measuring business activity, processes data into reports and communicates results to decision makers (ethics important

1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.

Adjusting the Accounts

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

After studying this chapter, you should be able to: adjusted account balances.

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

Week 3. Topic 3 Chapter 3. ACT102 Introduction to Accounting. Accounting for end of financial period adjustments 21/02/2018

ACT102 Introduction to Accounting Week 3 Accounting for end of financial period adjustments Topic 3 Chapter 3 2 RECAP Topic 2: Recording Business Transactions The accounting equation must always balance

ACT102 Introduction to Accounting Week 3 Accounting for end of financial period adjustments Topic 3 Chapter 3 2 RECAP Topic 2: Recording Business Transactions The accounting equation must always balance

True / False Questions

Chapter 02 Transaction Analysis True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers. True False 2. In order for information

Chapter 02 Transaction Analysis True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers. True False 2. In order for information

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

GAAP AND REVISION. DEFINITION OF ELEMENTS OF FINANCIAL STATEMENTS Revision concepts

GAAP AND REVISION INTRODUCE THE GENERALLY ACCEPTED ACCOUNTING PRINCIPLES (GAAP) Accounting standards The Conceptual Framework Accounting concepts & principles CONCEPTUAL FRAMEWORK Describes objective of

GAAP AND REVISION INTRODUCE THE GENERALLY ACCEPTED ACCOUNTING PRINCIPLES (GAAP) Accounting standards The Conceptual Framework Accounting concepts & principles CONCEPTUAL FRAMEWORK Describes objective of

Financial Accounting. (Exam)

") Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Investing and Financing Decisions and the Accounting System

Investing and Financing Decisions and the Accounting System Chapter 2 Conceptual Framework Objective of Financial Reporting To provide useful economic information to external users for decision making

Investing and Financing Decisions and the Accounting System Chapter 2 Conceptual Framework Objective of Financial Reporting To provide useful economic information to external users for decision making

The Accounting Cycle. End of the Period C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

Curriculum Document for Business Education

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

The Adjustment Process and Financial Statements Irwin/McGraw-Hill

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

FAQ: Financial Statements

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

ANSWER ALL MULTIPLE CHOICE ON YOUR SCANTRON AND WRITE YOUR TEST COLOR ON THE SCANTRON.

Name: Perm # TEST VERSION: A Class: Date: ANSWER ALL MULTIPLE CHOICE ON YOUR SCANTRON AND WRITE YOUR TEST COLOR ON THE SCANTRON. THERE IS ONLY ONE PROBLEM-- ANSWER IT IN THE SPACE PROVIDED ON THIS EXAM.

Name: Perm # TEST VERSION: A Class: Date: ANSWER ALL MULTIPLE CHOICE ON YOUR SCANTRON AND WRITE YOUR TEST COLOR ON THE SCANTRON. THERE IS ONLY ONE PROBLEM-- ANSWER IT IN THE SPACE PROVIDED ON THIS EXAM.

Understanding Accounting & Financial Statements

This image cannot currently be displayed. Accounting Principles INDE-Engineering Economy Understanding Accounting & Financial Statements Presented By: Magdy Akladios, PhD, PE, CSP, CPE, CSHM ACCOUNTING

This image cannot currently be displayed. Accounting Principles INDE-Engineering Economy Understanding Accounting & Financial Statements Presented By: Magdy Akladios, PhD, PE, CSP, CPE, CSHM ACCOUNTING

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book Patrizia Tettamanzi Sophie Goodman Source: Kimmel/Weygandt/Kieso Financial Accounting

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book Patrizia Tettamanzi Sophie Goodman Source: Kimmel/Weygandt/Kieso Financial Accounting

Rocco Sabino MBA, CPA

Rocco Sabino MBA, CPA Rocco.Sabino@Stonybrook.edu Agenda: I. Understanding Financial Information Ø Financial Statements q Income Statement It s all about earning income How does Human Resource (HR) affect

Rocco Sabino MBA, CPA Rocco.Sabino@Stonybrook.edu Agenda: I. Understanding Financial Information Ø Financial Statements q Income Statement It s all about earning income How does Human Resource (HR) affect

THE ACCOUNTING INFORMATION SYSTEM

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

Presented by: Meredith Mostochuk, CBA

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

Presented by: Meredith Mostochuk, CBA Types of Businesses Definition of a Business: An organization in which goods and services are exchanged for one another, or for money, on the basis of their perceived

ACCT1006 Notes TYPES OF FINANCIAL STATEMENTS

ACCT1006 Notes TYPES OF FINANCIAL STATEMENTS - 4 financial statements o Statement of changes in equity Changes in OE s capital, reserves, and earnings How aspects in OE change over the period o Statement

ACCT1006 Notes TYPES OF FINANCIAL STATEMENTS - 4 financial statements o Statement of changes in equity Changes in OE s capital, reserves, and earnings How aspects in OE change over the period o Statement

Accounting 1. Lesson Plan. Name: Terry Wilhelmi Day/Date:

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Financial Statements and End-of-Fiscal-Period Entries Unit: 4 Chapter 27 for a Corporation I. Objective(s): By the end of today s lesson,

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Financial Statements and End-of-Fiscal-Period Entries Unit: 4 Chapter 27 for a Corporation I. Objective(s): By the end of today s lesson,

Chapter 4: Completing the Accounting Cycle. Learning Objective 2 Prepare financial statements from adjusted account balances.

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

Fill-in-the-Blank Equations. Exercises

Chapter 3 The Adjusting Process Study Guide Solutions 1. Net book value Fill-in-the-Blank Equations 2. Depreciation expense 3. Supplies expense 4. Expense Exercises 1. Determine if each of the following

Chapter 3 The Adjusting Process Study Guide Solutions 1. Net book value Fill-in-the-Blank Equations 2. Depreciation expense 3. Supplies expense 4. Expense Exercises 1. Determine if each of the following

Do you subscribe to any magazines? Most of us subscribe

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

Topic notes 7: General Ledger

Topic notes 7: General Ledger Balance Day Adjustments 1. Accrued Expense 2. Prepaid Expense 3. Accrued Income 4. Income Received in Advance 5. Bad Debts & Doubtful Debts 6. Depreciation 7. Leave Entitlements

Topic notes 7: General Ledger Balance Day Adjustments 1. Accrued Expense 2. Prepaid Expense 3. Accrued Income 4. Income Received in Advance 5. Bad Debts & Doubtful Debts 6. Depreciation 7. Leave Entitlements

Unit five: Adjusting the accounts Accruals and Prepayments

Unit five: Adjusting the accounts Accruals and Prepayments اسم الطالب:... رقم الطالب:... الصف:... المدرسة:... الرقم التسلسلي Uploaded By: Ayman Ayyad (Danger3) Prepare by T. Abdul Jalil Alaiwi Uploaded

Unit five: Adjusting the accounts Accruals and Prepayments اسم الطالب:... رقم الطالب:... الصف:... المدرسة:... الرقم التسلسلي Uploaded By: Ayman Ayyad (Danger3) Prepare by T. Abdul Jalil Alaiwi Uploaded

Record Transactions in the Journal. Copy (post) to the Ledger. Prepare the Trial Balance

to the Ledger. Prepare the Trial Balance") Explain accounts, journals, and ledgers as they relate to recording transactions and describe common accounts Chapter 2 Record Transactions in the Journal 2 Basic summary device Detailed record of increases

Explain accounts, journals, and ledgers as they relate to recording transactions and describe common accounts Chapter 2 Record Transactions in the Journal 2 Basic summary device Detailed record of increases

Accounting Terms Chap 1-8

Accounting Terms Chap - TERM DEFINITION CHAPTER Account Account balance A record that summarizes all the transactions pertaining to a single item in the equation. The difference between the increases and

Accounting Terms Chap - TERM DEFINITION CHAPTER Account Account balance A record that summarizes all the transactions pertaining to a single item in the equation. The difference between the increases and

Key Learning: Students will review basic accounting concepts learned in the first level course.

Student Learning Map for Unit Topic: Review of Accounting I Concepts Rev. 1/14 Key Learning: Students will review basic accounting concepts learned in the first level course. How does a business organize

Student Learning Map for Unit Topic: Review of Accounting I Concepts Rev. 1/14 Key Learning: Students will review basic accounting concepts learned in the first level course. How does a business organize

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

Important Terminology

Important Terminology Recognition When we "recognize" a revenue or expense, it means that we record the amount in our general ledger and the amount is included in our income statement. Deferral When we

Important Terminology Recognition When we "recognize" a revenue or expense, it means that we record the amount in our general ledger and the amount is included in our income statement. Deferral When we

THE ACCOUNTING INFORMATION SYSTEM

2 THE ACCOUNTING INFORMATION SYSTEM DISCUSSION QUESTIONS 1. The conceptual framework of accounting is the collection of general concepts that logically flow from the objective of financial reporting to

2 THE ACCOUNTING INFORMATION SYSTEM DISCUSSION QUESTIONS 1. The conceptual framework of accounting is the collection of general concepts that logically flow from the objective of financial reporting to

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

Chapter 2 The Accounting Information System

Financial Accounting Making the Connection 1st Edition by Spiceland Chapter 2 The Accounting Information System REVIEW QUESTIONS Question 2-1 External transactions are transactions between the company

Financial Accounting Making the Connection 1st Edition by Spiceland Chapter 2 The Accounting Information System REVIEW QUESTIONS Question 2-1 External transactions are transactions between the company

Graded Project. Lesson 1: Business Accounting and You OVERVIEW INSTRUCTIONS

Lesson 1: Business Accounting and You OVERVIEW The focus of this project is for the student to keep a set of books through an accounting period to perform the following functions: Set up the books of accounting

Lesson 1: Business Accounting and You OVERVIEW The focus of this project is for the student to keep a set of books through an accounting period to perform the following functions: Set up the books of accounting

ADVANCED ACCOUNTING (110) Secondary

Secondary") Page 1 of 10 Contestant Number: Time: Rank: ADVANCED ACCOUNTING (110) Secondary REGIONAL 2017 Multiple Choice (20 @ 2 points each) Short Answers (18 @ 3 points each) Problems: Job 1 Classifying Accounts

Page 1 of 10 Contestant Number: Time: Rank: ADVANCED ACCOUNTING (110) Secondary REGIONAL 2017 Multiple Choice (20 @ 2 points each) Short Answers (18 @ 3 points each) Problems: Job 1 Classifying Accounts

Learning Objective. LO1 Prepare an income statement for a merchandising business organized as a corporation.

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 4 Recording Transactions Chapter 3 - Recording Transactions Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this week s study,

ACC100 Introduction to Accounting Week 4 Recording Transactions Chapter 3 - Recording Transactions Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this week s study,

CHAPTER 3 Adjusting the Accounts

Solutions Manual Financial and Managerial Accounting, 2nd Edition Weygandt Kimmel Kieso Completed Instant download SOLUTIONS MANUAL for Financial and Managerial Accounting, 2nd Edition by Jerry J. Weygandt,

Solutions Manual Financial and Managerial Accounting, 2nd Edition Weygandt Kimmel Kieso Completed Instant download SOLUTIONS MANUAL for Financial and Managerial Accounting, 2nd Edition by Jerry J. Weygandt,

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

The Accounting Cycle Accruals and Deferrals

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

The Expanded Ledger: Revenue, Expense, and Drawings

Revenue, Expense, and Drawings Remember the following before proceeding to the next slide!! Up until now, we have been recording transactions to the Capital account in the Owner s Equity section. Here

Revenue, Expense, and Drawings Remember the following before proceeding to the next slide!! Up until now, we have been recording transactions to the Capital account in the Owner s Equity section. Here

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

www.assignmentstudio.net WhatsApp: +61-424-295050 Toll Free: 1-800-794-425 Email: contact@assignmentstudio.net Follow us on Social Media Facebook: https://www.facebook.com/assignmentstudio Twitter: https://twitter.com/assignmentstudi

www.assignmentstudio.net WhatsApp: +61-424-295050 Toll Free: 1-800-794-425 Email: contact@assignmentstudio.net Follow us on Social Media Facebook: https://www.facebook.com/assignmentstudio Twitter: https://twitter.com/assignmentstudi

Chapter 2--Analyzing Transactions

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

Chapter 2--Analyzing Transactions Student: 1. Accounts are records of increases and decreases in individual financial statement items. 2. A chart of accounts is a listing of accounts that make up the journal.

download from https://testbankgo.eu/p/

CHAPTER 3 ADJUSTING THE ACCOUNTS SUMMARY OF QUESTIONS BY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 C 9. 2 C 17. 5 C 25. 5 K 33. 3

CHAPTER 3 ADJUSTING THE ACCOUNTS SUMMARY OF QUESTIONS BY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 C 9. 2 C 17. 5 C 25. 5 K 33. 3

Extra Practice for Block 1

Extra Practice for Block 1 Source: Harrison, Walter T., Jr., and Charles T. Horngren. Financial Accounting. 3rd ed. Boston: Pearson, 2008. Print. Custom Edition. Chapter 1 p.26-27 1. Which of the following

Extra Practice for Block 1 Source: Harrison, Walter T., Jr., and Charles T. Horngren. Financial Accounting. 3rd ed. Boston: Pearson, 2008. Print. Custom Edition. Chapter 1 p.26-27 1. Which of the following

Chapter 2 Recording Business Transactions

Horngren's Accounting, The Financial Chapters 11th Edition Solutions Manual Miller-Nobles Solutions Manual, Answer key, Instructor's resource Manual, Try It Solutions, Working Papers Solutions are include.

Horngren's Accounting, The Financial Chapters 11th Edition Solutions Manual Miller-Nobles Solutions Manual, Answer key, Instructor's resource Manual, Try It Solutions, Working Papers Solutions are include.

Accounting for. Sole Proprietorship. 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

Accounts. Date Description Increase Decrease Balance. Jan. 1, 20X3 Balance forward $ 50,000. Jan. 2, 20X3 Collected receivable $ 10,000 60,000

Accounting System A system where transactions and events are reliably processed and summarized into financial statements and reports Manual or Automated Basic Processing Tools: Accounts Debits and Credits

Accounting System A system where transactions and events are reliably processed and summarized into financial statements and reports Manual or Automated Basic Processing Tools: Accounts Debits and Credits

Fundamentals of Accounting Resources

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

ECON 3A---FALL 2007 MIDTERM #2 ANSWER QUESTIONS #1-25 ON GREEN SCANTRON AND THE REST IN THE SPACE PROVIDED-PLEASE.

ECON 3A---FALL 2007 MIDTERM #2 Name: PERM #: ANSWER QUESTIONS #1-25 ON GREEN SCANTRON AND THE REST IN THE SPACE PROVIDED-PLEASE. 1. Gross profit equals the difference between A) net sales revenues and

ECON 3A---FALL 2007 MIDTERM #2 Name: PERM #: ANSWER QUESTIONS #1-25 ON GREEN SCANTRON AND THE REST IN THE SPACE PROVIDED-PLEASE. 1. Gross profit equals the difference between A) net sales revenues and

Dealership Financial Statement Analysis: The Advanced Course

Dealership Financial Statement Analysis: The Advanced Course With Ron Sompels, CPAstrong Moderated by Mike Bowers, Executive Editor at DealersEdge Ron Sompels, CPAstrong Ron Sompels, CPA: Ronald Sompels

Dealership Financial Statement Analysis: The Advanced Course With Ron Sompels, CPAstrong Moderated by Mike Bowers, Executive Editor at DealersEdge Ron Sompels, CPAstrong Ron Sompels, CPA: Ronald Sompels

Section A: Multiple-Choice Questions (2 marks each; Total 30 marks)

") Name: Student ID: Section A: Multiple-Choice Questions (2 marks each; Total 30 marks) Choose the one best answer. 1. The accounting process involves all of the following except ( d ) a. identifying economic