FAC1502 Revision material

|

|

|

- Junior Sutton

- 6 years ago

- Views:

Transcription

1 FAC1502 Revision material

2 PROGRAM Examination issues General problem areas Q & A

3 IMPORTANCE of module This module - foundation of all your studies in accounting Ensure that you understand and know everything contained in this module as everything is important Not only required for the examination, but you WILL need it in future.

4

5

6

7 GOLDEN RULE Accounting CANNOT be studied by merely reading/memorising. You need to practice, practice and practice also!!

8 GENERAL PROBLEM AREAS Accounting cycle Types of journals General ledger accounts VAT issues Adjustments Inventory systems & closing-off procedures Financial statements Property, plant and equipment (PPE) Bank reconciliation

9 ACCOUNTING CYCLE Capture of transaction data on source documents (Daily) Analysing of transactions and journalising (Daily) Posting to ledger(s) (Daily, journal totals monthly) Balancing of accounts and preparing a trial balance (Monthly) Adjustment of accounts and post-adjustment trial balance (Annually) Closing of nominal accounts (Annually) Financial statements and reporting on results (Annually)

10 Cash journals TYPES OF JOURNALS Cash receipts (cash register roll, receipts, cash invoices, deposit slips) Cash payments (cheque counterfoils) Credit journals Sales (duplicate sales invoices) Sales returns (duplicates of credit notes) Purchases (original invoices) Purchases returns (original credit notes) General journal All other (Narrations important refer to source docs)

11 CASH JOURNAL ISSUES Which columns how many? Depends on frequency Sundry accounts What must be recorded in them? Once-off transactions Fol no s? References - Not important for exams

12 CASH JOURNAL ISSUES VAT on settlement discount granted On cash sales no issue On credit sales: VAT on full sales amount already CR to Output VAT with invoice Amount received from debtor is less than invoiced Difference = Settlement discount granted (including VAT) VAT on Settlement discount granted record as Input VAT Inverse for settlement discount received

13 CASH PAYMENTS JOURNAL

14 GENERAL LEDGER ACCOUNTS A general ledger account is shown in the form of a capital T and is referred to as a T-account. The left-hand side is the debit side and the right-hand side is the credit side. Assets and expenses increase on the debit side and decrease on the credit side (debit balance). Liabilities, equity and income increase on the credit side and decrease on the debit side (credit balance). Indicate the name of the contra ledger account in the account in which you are recording the entry. The contra account is the name of the other ledger account which is involved in the transaction: the one account refers to the other.

15 VAT ISSUES Application Calculation

16 VAT (Only basic info) Tax levied by Govt on the supply of goods and services Comprehensive tax virtually on all goods & services Current VAT rate 14% Must register as VAT-vendor if taxable supplies exceeded R in preceding 12 month period Two types of supplies: Taxable supplies: Standard rate (14%) Zero rated (0%) - (Vendor may claim input VAT): e.g. Brown bread Petrol & oil Exempt supplies (Vendor unable to claim input VAT): e.g. Financial services.

17 Output VAT Input VAT = VAT payable to SARS VAT on e.g. settlement discount received when payment is made Output VAT & not deducted from Input VAT. Calculation of VAT on amount excluding VAT: Amount without VAT R100 VAT R 14 Amount VAT inclusive R114 Calculate the VAT amount if VAT was included: Amount VAT inclusive R114 Calculation of VAT: R114 x (14 114) = R14 Amount without VAT R100

18 VAT Calculations Selling price = R228 Selling price includes VAT of 14% Required: Calculate VAT. Value given R228 x

19 VAT Calculations Selling price = R228 Selling price includes VAT of 14% Required: Calculate VAT. Value given R228 x What you have

20 VAT Calculations Selling price = R228 Selling price includes VAT of 14% Required: Calculate VAT. Value given R228 x 114 What you have

21 VAT Calculations Selling price = R228 Selling price includes VAT of 14% Required: Calculate VAT. What you want 228 x 114 What you have

22 VAT Calculations Selling price = R228 Selling price includes VAT of 14% Required: Calculate VAT. What you want R228 x What you have

23 VAT Calculations Selling price = R228 Selling price includes VAT of 14% Required: Calculate VAT. Value given R228 x What you want = R28 What you have

24 VAT Calculations Selling price = R228 Selling price includes VAT Required: Calculate selling price without VAT. What you want R228 x = R200 What you have

25 VAT Calculations If VAT = R28, calculate the selling price including VAT Value given What you want R28 x What you have

26 VAT Calculations If VAT = R28, calculate the selling price including VAT Value given What you want R28 x 14 What you have

27 VAT Calculations If VAT = R28, calculate the selling price including VAT Value given What you want R28 x = R228 What you have

28 VAT transactions Input VAT account: - only Dr entries - except for VAT on purchases returns Output VAT account: - only Cr entries - except for VAT on sales returns

29 Dr VAT Input Cr R 20.4 R Balance b/d Mar 31 Creditors control PRJ2 Bank CPJ VAT control J2 Debtors control CPJ3 21 Creditors control PJ Creditors control J Mar Dr VAT Output Cr 20.4 Mar Mar 31 Debtors control VAT control SRJ2 J2 R 20.4 R Mar 1 Balance 31 Bank Debtors control Creditors control b/d CRJ2 SJ2 CPJ Dr VAT Control Cr R 20.4 VAT Input J Mar 31 VAT Output J2 Balance c/d 504 R Apr 1 Balance b/d 504*

30 ADJUSTMENTS Profit or loss usually determined for financial year of 12 months Income &/or expenditure items not always within this 12 months Accounts must sometimes be adjusted to correct the balances in accounts At the end of a financial period, additional entries (adjustments) without source documents are required. Necessary to comply with the accrual basis of accounting.

31 Adjustments Begin of fin yr 1/1/2010 1/4/2010 1/7/2010 1/9/2010 Fin yr end 31/12/ /6/ /12/2011 Current financial year Next financial year If e.g. expenditure Profit or loss Payment in advance

32 Inventory systems & closing-off procedures Inventory systems Perpetual Periodic Closing-off of nominal accounts Trading account Profit or loss account

33 IMPORTANT FINANCIAL COMPONENTS of a trading concern GROSS PROFIT (determined in the trading account): Difference between sales and the ``cost price of sales' PROFIT FOR THE YEAR/PERIOD The amount which remains from the gross profit after all expenditure necessary to manage the business has been subtracted and other income has been added in the profit or loss account. COST PRICE OF SALES (determined in trading account) Opening inventory + purchases (at cost price) closing inventory (at cost price) Proper accounting for inventory thus important in determining the cost price of sales

34 MARK-UP ON COST PRICE When determining the cost of sales, it is important to establish whether the mark-up was made on the cost price or the selling price since the price that applies is taken to be 100 (100%). Suppose the mark-up of 25% is on the cost price. Thus: Cost price = 100 Mark-up = 25 Selling price = 125

35 Calculate COST PRICE if: Selling price = R Mark-up on cost price = 25% Value given What you want R x = R What you have

36 INVENTORY SYSTEMS Perpetual & Periodic Perpetual (continuous) inventory system the business keep a continuous track of inventory levels for the different inventory items it sells. Ideally suited to a business that sells items that can be easily identified, measured and a value attached to them e.g. Rolls Royce cars. Purchase of inventory is recorded directly into the inventory account at cost price At time of sale, the cost price is transferred from the inventory account to the cost of sales account. Gross profit can thus be determined on each sale.

37 In the perpetual inventory system inventory is an asset Inventory on hand and inventory which is purchased are therefore debited at cost price in the asset account called inventory and a contra account such as creditors or bank is credited When goods are sold, the sales account (income) is credited with the selling price and the contra account such as debtors or bank is debited. AND Goods are taken out of the inventory (asset) account at cost price (inventory account is credited) and debited to the cost of sales (expense) account.

38 Perpetual inventory system SG Ex 8.1

39 At the beginning of the year the only amount relevant is the value of inventory

40

41

42

43

44

45

46

47

48 The gross profit is the difference between sales and cost of sales. The gross profit is transferred to the profit or loss account. Where cost of sales is more than sales, the result is a gross loss.

49 Periodic inventory system The purchase of inventory is recorded in the purchases account and not an inventory account. Inventory returned - recorded in a purchases returns account. Cost of sales is not determined at the time of the recording of the sale but can thus only be determined at the end of the financial period after a physical inventory count has been done.

50 No cost of sales account as the cost of sales is determined in the Trading account A purchases and purchases returns accounts are kept A physical inventory count is essential The opening balance on the inventory account (asset) is held in the books throughout the financial period, which is usually a year, without any other entries.

51 Inventory purchased is recorded (debited) at cost price in the purchases account (expenditure) and the contra account, for instance creditors or bank, is credited. The purchases account is closed off at the end of the financial year, to the trading account by means of a general journal entry (debit trading account and credit purchases account). When goods are sold, the sales account (income) is credited with the selling price and the contra account, say bank or debtors, is debited.

52 A physical inventory count is undertaken to determine the closing inventory (usually at cost price). To record this figure, the inventory account is debited and the trading account is credited. In this system a cost of sales account is not kept. In the trading account the opening inventory is added to purchases. Closing inventory is deducted (the trading account is credited) and the cost of sales is calculated.

53 Periodic inventory system SG Ex 8.2 Inventory on 1 January 20.1 Transactions for year up to 31 December 20.1: Credit purchases Cash purchases Credit sales (mark-up on cost price is 25%) Cash sales (mark-up on cost price is 25%) Inventory on 31 December 20.1 R

54

55

56 CLOSING-OFF of NOMINAL ACCOUNTS To determine the financial result of an entity, the nominal accounts are closed by means of closing journals and transferred to the trading account (a nominal account) in the case of trading entities and/or to the profit or loss account. The gross profit, as determined, is debited to the trading account and credited to the profit or loss account. All the other nominal accounts with balances such as rent income, telephone expenses, rent expenses and salaries are (closed off) and the profit or loss account is accordingly debited or credited. The difference between the debit and credit sides of the profit or loss account results in the profit or loss which is, in turn, transferred to the capital account. The profit or loss account is therefore, also closed off.

57 TRIAL BALANCE Pre-adjustment trial balance test the correctness of the entries after the posting to the general ledger Test the requirements of the double-entry principle. Post-adjustment trial balance After the journalised adjustments have been posted. Post-closing trial balance after the closing journal entries have been posted to the ledger. all the nominal accounts are closed and the profit or loss as well as drawings are transferred to the capital account. All that remains in the trial balance are the assets, liabilities and equity accounts - items in the SFP.

58 Financial statements (sole proprietorship) Simplest form of business Limited legislation re establishment Drawings use of profit from business for personal use Statement of profit or loss and other comprehensive income Statement of changes in equity Statement of financial position.

59 SG: Revision exercise 2, p301 TRIAL BALANCE OF PETER PUMPKIN AS AT 28 FEBRUARY 20.1

60 ADDITIONAL INFORMATION: (a) Stationery on hand at 28 February 20.1, R150. (b) An allowance for credit losses of R405 on outstanding trade debtors' balances must be created. (c) Rent income amounts to R1 500 per month and the rental has been charged for the full financial year. (d) Provide for interest still outstanding on mortgage bond. (e) Provide for depreciation on furniture and fittings at 15% per annum on cost price.

61 Required: (1) Prepare the statement of profit or loss and other comprehensive income of Peter Pumpkin for the year ended 28 February (2) Prepare the statement of changes in equity of Peter Pumpkin for the year ended 28 February (3) Prepare the statement of financial position of Peter P otatoes as at 28 February (4) Show the note on Property, Plant and Equipment for the year ended 28 February 20.1.

62 WHAT IS REQUIRED TO ENSURE SUCCESS? KNOW THE FORMATS

63 WHERE TO BEGIN? 1. Read the requirements 2. Format the required statements: Statement of Profit or Loss and Other Comprehensive Income Statement of Changes in Equity Statement of Financial Position PPE note. 3. Deal with the Additional Information 4. Ensure that you tick-off all the items in the TB as well as the Additional information.

64 Issues to note: TRIAL BALANCE OF PETER P OTATOES AS AT 28 FEBRUARY 20.1

65 ADDITIONAL INFORMATION: (a) Stationery on hand at 28 February 20.1, R150. Stationery on hand = Closing inventory Record: Profit or Loss: Subtract from 28 Feb 20.1 TP balance: Thus, R1 150 R150 = R1 000 expensed Report: SFP (current asset): SComp Inc: Expense Inventory - R1 000 SFP: Current Asset - Inventory - R150

66 ADDITIONAL INFORMATION: (b) An allowance for credit losses of R405 on outstanding trade debtors' balances must be created. Record: Profit or Loss: Increase operating expenses Report: SComp Inc: Credit losses SFP: Decrease Trade receivables (Debtors) with allowance for credit losses

67 ADDITIONAL INFORMATION: (c) Rent income amounts to R1 500 per month and the rental has been charged for the full financial year Adjustment: Rent income/month = R1 500 Thus, rent income/year = R TB - Rent income = R Thus Rent income in arrears = R1 500 Record: Profit or Loss (12 months) = R Report: SComp Inc: Income R SFP: Trade receivables: + R1 500

68 ADDITIONAL INFORMATION: (d) Provide for interest still outstanding on mortgage bond. 15% Mortgage bond = R Annual interest on mortgage bond: R x 15% = R4 500 Record: Profit or Loss: Finance charges R4 500 Report: SComp Inc: Expense R4 500 SFP: Current liabilities: Trade payables R4 500

69 ADDITIONAL INFORMATION: (e) Provide for depreciation on furniture and fittings at 15% per annum on cost price. Furniture and fittings (cost) = R Depreciation: R x 15% = R6 300 Record: Profit or Loss (Dr)Depr R6 300 Acc Depr (Cr) R6 300 Report: S Comp Income: Depreciation R6 300 PPE Note: Depreciation R6 300 SFP: PPE less Depreciation R6 300

70 (1) STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 28 FEBRUARY 20.1

71

72

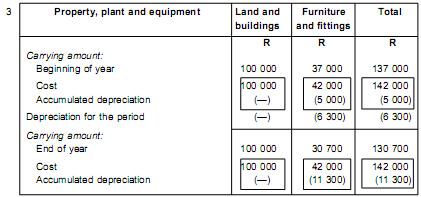

73

74 Property, plant & equipment Cost price of PPE Depreciation Disclosure in Fin statements

75 Property, plant and equipment (PPE) Have an operating lifespan of more than one year and can be used over and over again Tangible assets (can see & touch): e.g. buildings & machinery Become obsolete Depreciate over expected economic life No longer operate economically - replaced

76 Cost price of PPE The cost price of PPE consists of: purchase price, including all expenses incurred in getting the asset to the premises installation costs including, for example, the wages of the business's own technical personnel any other expenses incurred in getting the asset operational Cost price (historical cost price) - remain constant throughout the life of the asset. Financing costs on loans raised to acquire the asset are not included in the cost price of the asset.

77 Depreciation methods Straight line method Cost price is written of over the expected useful life (in years) of the asset. Diminishing balance method In this case a fixed percentage of the carrying amount is written off annually. Production unit method In this case the units produced by the machine are written off annually as a percentage of the units the machine is expected to produce over its total life span.

78 JOURNAL ENTRIES GENERAL JOURNAL The depreciable amount is the cost of the asset less its residual value. The residual value is the expected value (e.g. scrap value, trade-in value) of the asset at the end of its useful life.

79 Statement of Fin. Position Only the carrying amount is shown on the face of the statement of financial position. A detailed reconciliation of movements in the carrying amount from the beginning to the end of the financial period is shown in a note.

80 Note on PPE

81 Example PPE

82 Example PPE (continue)

83 BANK RECONCILIATIONS Bank reconciliation statement could be seen as an extension of the bank statement Balance the bank account in the books of the business with the bank statement Two steps: the business's records are updated to account for actual transactions recorded by the bank statement, and record those transactions to which the bank must still attend to in the bank reconciliation statement Favourable bank balance - debit side of the bank account & credit side of bank statement. Unfavourable or overdrawn bank balance - credit side of the bank account & debit side of the bank statement (indicated by DT, DR or OD).

84 Procedure - reconciliation process If a bank recon was completed for the previous month the bank statement must first be compared with that bank recon to ascertain whether the outstanding items and corrections have been done by the bank. Compare items on the debit side of the bank recon with entries on the debit side of the bank statement and credit entries on the recon with credit entries on the statement. Compare the amounts in the cash receipts journal for the current month with the entries on the credit side of the bank statement. Compare the amounts in the cash payments journal for the current month with entries on the debit side of the bank statement

85 Exercise 9.1 (p174)

86

87

88 Bank statement

89 Suggested solution: SG, Exercise 9.1, p174

90

91

92

93

94

95

96 GENERAL QUESTIONS

97 The End!!

resources controlled - as a result of past events - future economic benefits expected to flow

Discussion class notes : FAC1503 Financial accounting the provision of financial information to mainly external parties recording of transactions and the preparation of financial statements Management

Discussion class notes : FAC1503 Financial accounting the provision of financial information to mainly external parties recording of transactions and the preparation of financial statements Management

TERMINOLOGY. Statement of comprehensive income for the year ended.. Income statement for the year ended.

GENERAL ISSUES Textbook 3 rd edition Admission to exam: Submission of 1 st assignment Year/examination mark: Ass 1: 50% of 10% Ass 2: 50% of 10% If you obtain 60% for Ass 1 and 0% for Ass 2, your year

GENERAL ISSUES Textbook 3 rd edition Admission to exam: Submission of 1 st assignment Year/examination mark: Ass 1: 50% of 10% Ass 2: 50% of 10% If you obtain 60% for Ass 1 and 0% for Ass 2, your year

TRINITY TUTORIALS EXAM PACK AND STUDY NOTES

TRINITY TUTORIALS EXAM PACK AND STUDY NOTES THIS PACK CONSISTS OF PAST EXAM PAPERS FROM MAY 2009 NOVEMBER 2013 AND THEIR SUGGESTED SOLUTIONS PLUS NOTES WHICH WILL HELP THE STUDENT TO UNDERSTAND AND APPRECIATE

TRINITY TUTORIALS EXAM PACK AND STUDY NOTES THIS PACK CONSISTS OF PAST EXAM PAPERS FROM MAY 2009 NOVEMBER 2013 AND THEIR SUGGESTED SOLUTIONS PLUS NOTES WHICH WILL HELP THE STUDENT TO UNDERSTAND AND APPRECIATE

FAC 1503 DISCUSSION CLASS

FAC 1503 DISCUSSION CLASS False words are not only evil in themselves, but they infect the soul with evil. PLATO; GREEK AUTHOR & PHILOSOPHER (427 BC - 347 BC) Objectives You (student) must be able to:

FAC 1503 DISCUSSION CLASS False words are not only evil in themselves, but they infect the soul with evil. PLATO; GREEK AUTHOR & PHILOSOPHER (427 BC - 347 BC) Objectives You (student) must be able to:

FANLING LUTHERAN SECONDARY SCHOOL

FANLING LUTHERAN SECONDARY SCHOOL 2012 2013 2 nd Term Examination S.5 BUSINESS, ACCOUNTING AND FINANCIAL STUDIES Accounting Module Date : 20th June, 2013 Time allowed: 8:30 am - 11:00 am (2 hour 30 minutes)

FANLING LUTHERAN SECONDARY SCHOOL 2012 2013 2 nd Term Examination S.5 BUSINESS, ACCOUNTING AND FINANCIAL STUDIES Accounting Module Date : 20th June, 2013 Time allowed: 8:30 am - 11:00 am (2 hour 30 minutes)

CONTROL ACCOUNTS. The debtors control and creditors control accounts facilitates accounting control over the debtors and creditors accounts.

CONTROL ACCOUNTS SPECIFIC OUTCOMES Post to the general ledger, debtors ledger and creditors ledger from the subsidiary books and balance ledger accounts where necessary. Reconcile the control accounts

CONTROL ACCOUNTS SPECIFIC OUTCOMES Post to the general ledger, debtors ledger and creditors ledger from the subsidiary books and balance ledger accounts where necessary. Reconcile the control accounts

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2)

") MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Particulars Rs. Opening written down value of machine 1,00,000 Cost of new machine

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Particulars Rs. Opening written down value of machine 1,00,000 Cost of new machine

ACCOUNTING INTERVIEW QUESTIONS

www.globalcma.in Learning Platform for Cost Accountants (CMA) 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction

www.globalcma.in Learning Platform for Cost Accountants (CMA) 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction

MGT101 All Solved Past Papers of Mid Term Exam in one file By

MGT101 All Solved Past Papers of Mid Term Exam in one file By http://vustudents.ning.com MIDTERM EXAMINATION 7 th Dec 2009 MGT101- Financial Accounting Question No: 1 Income of the business includes: Cash

MGT101 All Solved Past Papers of Mid Term Exam in one file By http://vustudents.ning.com MIDTERM EXAMINATION 7 th Dec 2009 MGT101- Financial Accounting Question No: 1 Income of the business includes: Cash

MIDTERM EXAMINATION MGT101- Financial Accounting (Session - 5) Time: 60 min Marks: 50

Time: 60 min Marks: 50") MIDTERM EXAMINATION MGT101- Financial Accounting (Session - 5) Time: 60 min Marks: 50 Question No: 1 ( Marks: 1 ) - Please choose one An accounting system is used by a business to: Analyze transactions

MIDTERM EXAMINATION MGT101- Financial Accounting (Session - 5) Time: 60 min Marks: 50 Question No: 1 ( Marks: 1 ) - Please choose one An accounting system is used by a business to: Analyze transactions

Index. Assets (continued) scrapping or disposal trading-in Auditing Profession Act 26 of

scrapping or disposal trading-in Auditing Profession Act 26 of") Index A Accounts balancing... 61 incomplete records... 369 Accounting balancing an account... 61 basic accounting equation... 27 cycle... 130 definition... 4, 13 developments... 5 domains... 14 function...

Index A Accounts balancing... 61 incomplete records... 369 Accounting balancing an account... 61 basic accounting equation... 27 cycle... 130 definition... 4, 13 developments... 5 domains... 14 function...

Directorate: Curriculum FET ACCOUNTING. PREPARATION FOR GRADE 10 Workbook

Directorate: Curriculum FET ACCOUNTING PREPARATION FOR GRADE 10 Workbook Activity 1.1 Baseline assessment Concept Answer Definition Asset A Book of first entry where information is recorded from the source

Directorate: Curriculum FET ACCOUNTING PREPARATION FOR GRADE 10 Workbook Activity 1.1 Baseline assessment Concept Answer Definition Asset A Book of first entry where information is recorded from the source

GOLDEN RULES. 1.) The following are elements of financial statements:

The following are elements of financial statements:") GOLDEN RULES 1.) The following are elements of financial statements: Elements by which the financial position (assets = equity + liabilities) is measured: (1) Assets (2) Liabilities (3) Equity Elements

GOLDEN RULES 1.) The following are elements of financial statements: Elements by which the financial position (assets = equity + liabilities) is measured: (1) Assets (2) Liabilities (3) Equity Elements

ACCOUNTING JUNE EXAMINATION GRADE 11

1 ACCOUNTING JUNE EXAMINATION 2015 GRADE 11 MARKS: 300 TIME: 3 HOURS This Question paper consists of 13 pages and 11 pages Answer book INSTRUCTIONS AND INFORMATION 2 1. You are provided with a question

1 ACCOUNTING JUNE EXAMINATION 2015 GRADE 11 MARKS: 300 TIME: 3 HOURS This Question paper consists of 13 pages and 11 pages Answer book INSTRUCTIONS AND INFORMATION 2 1. You are provided with a question

This question paper consists of 5 pages. PLEASE NOTE:

This question paper consists of 5 pages. PLEASE NOTE: 1. Ensure that you are writing the correct examination paper. 2. Ensure that you are handed the correct examination answer book (BLUE) by the invigilator.

This question paper consists of 5 pages. PLEASE NOTE: 1. Ensure that you are writing the correct examination paper. 2. Ensure that you are handed the correct examination answer book (BLUE) by the invigilator.

100 Accounting Interview Questions and Answers

100 Accounting Interview Questions and Answers 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction I decided to

100 Accounting Interview Questions and Answers 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction I decided to

DEBITORS & CREDITORS RECONCILIATIONS (LIVE) 14 MAY 2015 Section A: Summary Content Notes

14 MAY 2015 Section A: Summary Content Notes") DEBITORS & CREDITORS RECONCILIATIONS (LIVE) 14 MAY 2015 Section A: Summary Content Notes An important part of managerial accounting is for a business to keep track of its debtors. The Debtors Control account

DEBITORS & CREDITORS RECONCILIATIONS (LIVE) 14 MAY 2015 Section A: Summary Content Notes An important part of managerial accounting is for a business to keep track of its debtors. The Debtors Control account

GRADE 10 CLASS TEST POSTING TO THE LEDGER 50 minutes; 70 marks

GRADE 10 CLASS TEST POSTING TO THE LEDGER 50 minutes; 70 marks INSTRUCTIONS: 1. You are provided with complete cash journals of Mars & Sons who are a stationery shop that sell to the public at a mark-up

GRADE 10 CLASS TEST POSTING TO THE LEDGER 50 minutes; 70 marks INSTRUCTIONS: 1. You are provided with complete cash journals of Mars & Sons who are a stationery shop that sell to the public at a mark-up

GRADE 11 NOVEMBER 2013 ACCOUNTING

NATIONAL SENIOR CERTIFICATE GRADE 11 NOVEMBER 2013 ACCOUNTING MARKS: 300 TIME: 3 hours This question paper consists of 18 pages. 2 ACCOUNTING (NOVEMBER 2013) INSTRUCTIONS AND INFORMATION 1. This question

NATIONAL SENIOR CERTIFICATE GRADE 11 NOVEMBER 2013 ACCOUNTING MARKS: 300 TIME: 3 hours This question paper consists of 18 pages. 2 ACCOUNTING (NOVEMBER 2013) INSTRUCTIONS AND INFORMATION 1. This question

SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME

GENERAL / SPECIAL DEGREE PROGRAMME") All Rights Reserved No. of Pages - 12 No of Questions - 06 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER I (INTAKE VI GROUP B) END SEMESTER

All Rights Reserved No. of Pages - 12 No of Questions - 06 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER I (INTAKE VI GROUP B) END SEMESTER

GRADE 10 ACCOUNTING CYCLE TEST TERM 2 APRIL marks 60 minutes. QUESTION 1 TRANSACTION ANALYSIS (18 marks; 13 minutes)

") GRADE 10 ACCOUNTING CYCLE TEST TERM 2 APRIL 201 80 marks 60 minutes INSTUCTIONS: 1) Answer on the answer booklet provided. 2) You may use pencil ) No tip-ex is allowed 4) Write neatly QUESTION 1 TRANSACTION

GRADE 10 ACCOUNTING CYCLE TEST TERM 2 APRIL 201 80 marks 60 minutes INSTUCTIONS: 1) Answer on the answer booklet provided. 2) You may use pencil ) No tip-ex is allowed 4) Write neatly QUESTION 1 TRANSACTION

PANCHAKSHARI S PROFESSIONAL ACADEMY PVT LTD (Your Lifelong Knowledge Partner )

") 50 Questions 50 Marks 60 Minutes Rectification of Error Select the best choice to answer the following questions: 1. Which of the following statement is/are correct? (i) A separate suspense account should

50 Questions 50 Marks 60 Minutes Rectification of Error Select the best choice to answer the following questions: 1. Which of the following statement is/are correct? (i) A separate suspense account should

S.5 BUSINESS, ACCOUNTING AND FINANCIAL STUDIES Accounting Module

FANLING LUTHERAN SECONDARY SCHOOL 2015 2016 FIRST TERM EXAM S.5 BUSINESS, ACCOUNTING AND FINANCIAL STUDIES Accounting Module Date : 19th January, 2016 Time allowed: 8:30 am - 10:45 am (2 hour 15 minutes)

FANLING LUTHERAN SECONDARY SCHOOL 2015 2016 FIRST TERM EXAM S.5 BUSINESS, ACCOUNTING AND FINANCIAL STUDIES Accounting Module Date : 19th January, 2016 Time allowed: 8:30 am - 10:45 am (2 hour 15 minutes)

Cycle Test 1: Term 1 Grade 11 Accounting February 2014 BANK RECONCILIATIONS, CREDITORS RECONCILIATIONS, ETHICS AND CONTROLS

Cycle Test 1: Term 1 Grade 11 Accounting February 2014 BANK RECONCILIATIONS, CREDITORS RECONCILIATIONS, ETHICS AND CONTROLS Examiner: J Cansfield Marks: 100 Time: 1 hour Instructions: 1. Answer on this

Cycle Test 1: Term 1 Grade 11 Accounting February 2014 BANK RECONCILIATIONS, CREDITORS RECONCILIATIONS, ETHICS AND CONTROLS Examiner: J Cansfield Marks: 100 Time: 1 hour Instructions: 1. Answer on this

JUNE EXAMINATION PAPER 200 marks 2 hours GRADE 10 ACCOUNTING

JUNE EXAMINATION PAPER 200 marks 2 hours GRADE 10 ACCOUNTING INSTRUCTIONS AND INFORMATION: 1. Answer ALL the questions in the Answer Book provided. 2. Show all workings/calculations in order to achieve

JUNE EXAMINATION PAPER 200 marks 2 hours GRADE 10 ACCOUNTING INSTRUCTIONS AND INFORMATION: 1. Answer ALL the questions in the Answer Book provided. 2. Show all workings/calculations in order to achieve

ACCOUNTING GRADE 10 NOVEMBER 2015

ACCOUNTING GRADE 10 NOVEMBER 2015 MARKS: 300 TIME: 3 HOURS THIS QUESTION PAPER CONSISTS OF 13 PAGES INCLUDING THE COVER PAGE AND AN ANSWER BOOK OF 14 PAGES. 1 INSTRUCTIONS AND INFORMATION Read the following

ACCOUNTING GRADE 10 NOVEMBER 2015 MARKS: 300 TIME: 3 HOURS THIS QUESTION PAPER CONSISTS OF 13 PAGES INCLUDING THE COVER PAGE AND AN ANSWER BOOK OF 14 PAGES. 1 INSTRUCTIONS AND INFORMATION Read the following

REQUIRED: 1.1 Using the information given below correct the bank reconciliation statement. (16) 1.2 Answer the questions that Henry has for you.

1.2 Answer the questions that Henry has for you.") QUESTION 1: Bank Reconciliation Statement (26 Marks; 10 Minutes) Kerry Slack, the owner of Slack Traders asked the bookkeeper Nicola Buck to prepare the bank reconciliation statement for May 2011. Kerry

QUESTION 1: Bank Reconciliation Statement (26 Marks; 10 Minutes) Kerry Slack, the owner of Slack Traders asked the bookkeeper Nicola Buck to prepare the bank reconciliation statement for May 2011. Kerry

THE TRAINING PLACE OF EXCELLENCE Accounts Preparation Practice Assessment: Questions

THE TRAINING PLACE OF EXCELLENCE Accounts Preparation Practice Assessment: Questions Task 1: Non-Current Assets Register The following is a purchase invoice received by NFS Ltd: Invoice 60754 To: NFS Ltd

THE TRAINING PLACE OF EXCELLENCE Accounts Preparation Practice Assessment: Questions Task 1: Non-Current Assets Register The following is a purchase invoice received by NFS Ltd: Invoice 60754 To: NFS Ltd

PROFITS OR LOSS PRIOR TO INCORPORATION

CHAPTER 3 PROFITS OR LOSS PRIOR TO INCORPORATION Learning Objectives After studying this chapter, you will be able to: Account for pre-incorporation profit. Learn various methods for computing profit or

CHAPTER 3 PROFITS OR LOSS PRIOR TO INCORPORATION Learning Objectives After studying this chapter, you will be able to: Account for pre-incorporation profit. Learn various methods for computing profit or

MYOB Bookkeeping Assessment 1A. Journals. (Note: The number of rows in journals won't necessarily match the number of transactions to be posted)

") MYOB Bookkeeping Assessment 1A Journals (Note: The number of rows in journals won't necessarily match the number of transactions to be posted) Sales Journal Date Invoice No Debtor Sales Services $ Sales

MYOB Bookkeeping Assessment 1A Journals (Note: The number of rows in journals won't necessarily match the number of transactions to be posted) Sales Journal Date Invoice No Debtor Sales Services $ Sales

ACCOUNTING PAPER I. 1. This paper consists of 9 pages. Please check that your question paper is complete.

GRADE 11 EXAMINATION NOVEMBER ACCOUNTING PAPER I Time: 2 hours 200 marks PLEASE READ THE FOLLOWING INSTRUCTIONS CAREFULLY 1. This paper consists of 9 pages. Please check that your question paper is complete.

GRADE 11 EXAMINATION NOVEMBER ACCOUNTING PAPER I Time: 2 hours 200 marks PLEASE READ THE FOLLOWING INSTRUCTIONS CAREFULLY 1. This paper consists of 9 pages. Please check that your question paper is complete.

1 st Year Examination : Summer FINANCIAL ACCOUNTING l NEW SYLLABUS. PAPER, SOLUTIONS and EXAMINERS REPORT

1 st Year Examination : Summer 2009 FINANCIAL ACCOUNTING l NEW SYLLABUS PAPER, SOLUTIONS and EXAMINERS REPORT NOTES TO USERS ABOUT THESE SOLUTIONS The solutions in this document are published by Accounting

1 st Year Examination : Summer 2009 FINANCIAL ACCOUNTING l NEW SYLLABUS PAPER, SOLUTIONS and EXAMINERS REPORT NOTES TO USERS ABOUT THESE SOLUTIONS The solutions in this document are published by Accounting

ACCOUNTING. Written examination 1. Monday 7 June 2004

Victorian Certificate of Education ACCOUNTING Written examination 1 Monday 7 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

Victorian Certificate of Education ACCOUNTING Written examination 1 Monday 7 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

ACCOUNTING. Written examination 1. Tuesday 11 June 2002

ACCNT EXAM 1A Victorian Certificate of Education ACCOUNTING Written examination 1 Tuesday 11 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION

ACCNT EXAM 1A Victorian Certificate of Education ACCOUNTING Written examination 1 Tuesday 11 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION

Answer to MTP_Foundation_Syllabus 2012_Jun2017_Set 1 Paper 2- Fundamentals of Accounting

Paper 2- Fundamentals of Accounting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 2- Fundamentals of Accounting Full Marks :

Paper 2- Fundamentals of Accounting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 2- Fundamentals of Accounting Full Marks :

ICAN MID DIET LIVE CLASS FOR MAY DIET 2015 FINANCIAL ACCOUNTING Introduction to financial accounting Recording non-current assets and depreciation

ICAN MID DIET LIVE CLASS FOR MAY DIET 2015 FINANCIAL ACCOUNTING Introduction to financial accounting Recording non-current assets and depreciation Compiling financial statement Compiling financial statement

ICAN MID DIET LIVE CLASS FOR MAY DIET 2015 FINANCIAL ACCOUNTING Introduction to financial accounting Recording non-current assets and depreciation Compiling financial statement Compiling financial statement

Prepared and solved by Cyberian www,vuaskari.com

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

CBA Model Question Paper CO2. The difference between an income statement and an income and expenditure account is that

CBA Model Question Paper CO2 Question 1 The difference between an income statement and an income and expenditure account is that A an income and expenditure account is an international term for a Income

CBA Model Question Paper CO2 Question 1 The difference between an income statement and an income and expenditure account is that A an income and expenditure account is an international term for a Income

QUESTION 1: (94 Marks, 56 Minutes)

") QUESTION 1: (94 Marks, 56 Minutes) This question consists of three parts. PART A The following information was found in the books of Lynnwood Auto on 29 February 2008, the last day of the financial year.

QUESTION 1: (94 Marks, 56 Minutes) This question consists of three parts. PART A The following information was found in the books of Lynnwood Auto on 29 February 2008, the last day of the financial year.

GRADE 11 NOVEMBER 2013 ACCOUNTING MARKING GUIDELINE (MEMORANDUM)

") NATIONAL SENIOR CERTIFICATE GRADE 11 NOVEMBER ACCOUNTING MARKING GUIDELINE (MEMORANDUM) MARKS: 300 GENERAL PRINCIPLES: 1. Where calculations are required, award full marks for the final answer. If the

NATIONAL SENIOR CERTIFICATE GRADE 11 NOVEMBER ACCOUNTING MARKING GUIDELINE (MEMORANDUM) MARKS: 300 GENERAL PRINCIPLES: 1. Where calculations are required, award full marks for the final answer. If the

Final accounts for sole traders and partnerships

Osborne Books Tutor Zone Final accounts for sole traders and partnerships Practice assessment 2 Osborne Books Limited, 2013 2 f i n a l a c c o u n t s f o r s o l e t r a d e r s a n d p a r t n e r s

Osborne Books Tutor Zone Final accounts for sole traders and partnerships Practice assessment 2 Osborne Books Limited, 2013 2 f i n a l a c c o u n t s f o r s o l e t r a d e r s a n d p a r t n e r s

Practice exercise solutions

Bookkeeping to Trial Balance Practice exercise solutions Learning Module: Recording credit and sundry transactions Practice exercise 4a Questions regarding the cashbook receipts: (iii) The amount contributed

Bookkeeping to Trial Balance Practice exercise solutions Learning Module: Recording credit and sundry transactions Practice exercise 4a Questions regarding the cashbook receipts: (iii) The amount contributed

GR. 9 EMS REVISION TEST TERM 4

TOTAL: 50 GR. 9 EMS REVISION TEST TERM 4 DURATION: 30 MINUTES QUESTION 1 POSTING TO GENERAL LEDGER AND DEBTOR S LEDGER [28 marks; 18 minutes] Toys 4 Us toy store sells toys to various other toy stores

TOTAL: 50 GR. 9 EMS REVISION TEST TERM 4 DURATION: 30 MINUTES QUESTION 1 POSTING TO GENERAL LEDGER AND DEBTOR S LEDGER [28 marks; 18 minutes] Toys 4 Us toy store sells toys to various other toy stores

Fundamentals of Accounting Resources

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Answers to activities, practice exercises and exam practice questions

Answers to activities, practice exercises and exam practice questions This text has not been through the Cambridge endorsement process. 2 [1] The cheque which Noel cashed was for his personal expenses.

Answers to activities, practice exercises and exam practice questions This text has not been through the Cambridge endorsement process. 2 [1] The cheque which Noel cashed was for his personal expenses.

Financial Accounting

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

New Era Accounting WORKSHEETS

New Era Accounting WORKSHEETS EMS TRAINING WORKSHEETS Page 1 TASK 3 Spreadsheet of Carol s Curls No. Bank ASSETS Hairdressing Equipment Office equipment LIABILITIES Accounts payable OWNERS' EQUITY 1. 2.

New Era Accounting WORKSHEETS EMS TRAINING WORKSHEETS Page 1 TASK 3 Spreadsheet of Carol s Curls No. Bank ASSETS Hairdressing Equipment Office equipment LIABILITIES Accounts payable OWNERS' EQUITY 1. 2.

MGT101- Financial Accounting

MIDTERM EXAMINATION MGT101- Financial Accounting Question No: 1 ( Marks: 1 ) - Please choose one Depreciation arises because of: Fall in the market value of an asset Fall in the value of money Physical

MIDTERM EXAMINATION MGT101- Financial Accounting Question No: 1 ( Marks: 1 ) - Please choose one Depreciation arises because of: Fall in the market value of an asset Fall in the value of money Physical

Profit (P) = Increase or Decrease in Net Assets (I) + Drawings (D) Capital (C) Income Expense = Profit / (Loss) Asset = Liability Capital

= Increase or Decrease in Net Assets (I) + Drawings (D) Capital (C) Income Expense = Profit / (Loss) Asset = Liability Capital") Rule of Double Entry Assets Liability Capital Expense Income DEBIT CREDIT Increase Decrease Accounting Equation Asset = Capital + Liability Capital = Asset Liability = NET ASSETS Business Equation Profit

Rule of Double Entry Assets Liability Capital Expense Income DEBIT CREDIT Increase Decrease Accounting Equation Asset = Capital + Liability Capital = Asset Liability = NET ASSETS Business Equation Profit

INTRODUCTION TO FINANCIAL ACCOUNTING

INTBUS NOVEMBER 2013 EXAMINATION DATE: 6 NOVEMBER 2013 TIME: 09H00 11H00 TOTAL: 100 MARKS DURATION: 2 HOURS PASS MARK: 40% (IFA-01) INTRODUCTION TO FINANCIAL ACCOUNTING THIS EXAMINATION PAPER CONSISTS

INTBUS NOVEMBER 2013 EXAMINATION DATE: 6 NOVEMBER 2013 TIME: 09H00 11H00 TOTAL: 100 MARKS DURATION: 2 HOURS PASS MARK: 40% (IFA-01) INTRODUCTION TO FINANCIAL ACCOUNTING THIS EXAMINATION PAPER CONSISTS

QUESTION 2 IAS 1 (CAF5 A15) Following is the summarised trial balance of Eagles Limited (EL) as at 30 June 2015: Debit Rs. in 000

Following is the summarised trial balance of Eagles Limited (EL) as at 30 June 2015: Debit Rs. in 000") QUESTION 2 IAS 1 (CAF5 A15) Following is the summarised trial balance of Eagles Limited (EL) as at 30 June 2015: Debit Credit Plant 2,500 Acc. depreciation at 1 July 2014 Equipment 700 Plant 1,000 Stock

QUESTION 2 IAS 1 (CAF5 A15) Following is the summarised trial balance of Eagles Limited (EL) as at 30 June 2015: Debit Credit Plant 2,500 Acc. depreciation at 1 July 2014 Equipment 700 Plant 1,000 Stock

CONTROL TEST 1 TOTAL: 70

CONTROL TEST 1 TOTAL: 70 NAME: Question 1 (36 Marks) The following information relates to Always Talking Stores, owned by Ruby Uys Required: Use the information given below to complete the general ledger

CONTROL TEST 1 TOTAL: 70 NAME: Question 1 (36 Marks) The following information relates to Always Talking Stores, owned by Ruby Uys Required: Use the information given below to complete the general ledger

In this module we look at how financial records are balanced and how financial reports are produced, incorporating Balance Day adjustments.

Introduction In this module we look at how financial records are balanced and how financial reports are produced, incorporating Balance Day adjustments. At the end of each accounting period an organisation

Introduction In this module we look at how financial records are balanced and how financial reports are produced, incorporating Balance Day adjustments. At the end of each accounting period an organisation

BANK RECONCILIATION. Make supplementary entries in the cash receipts journal and the cash payments journal.

BANK ECONCILIATION SPECIFIC OUTCOMES _ Compare entries in the bank statement with entries in the cash receipts journal, cash payments journal and the bank reconciliation statement of the previous month.

BANK ECONCILIATION SPECIFIC OUTCOMES _ Compare entries in the bank statement with entries in the cash receipts journal, cash payments journal and the bank reconciliation statement of the previous month.

Part-I. Choose the correct answer: 20x1=20

Higher secondary second year Accountancy Model Question paper - II Time: 2.30 hrs Marks:90 Part-I Choose the correct answer: 20x1=20 1. Trial balance shows sundry debtors Rs.75,000/- as on 31.12.2005.

Higher secondary second year Accountancy Model Question paper - II Time: 2.30 hrs Marks:90 Part-I Choose the correct answer: 20x1=20 1. Trial balance shows sundry debtors Rs.75,000/- as on 31.12.2005.

Composed & Solved Hafiz Salman Majeed

FINALTERM EXAMINATION Fall 2008 MGT101- Financial Accounting (Session - 4) Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset

FINALTERM EXAMINATION Fall 2008 MGT101- Financial Accounting (Session - 4) Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset

MARK SCHEME for the May/June 2010 question paper for the guidance of teachers 9706 ACCOUNTING

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Subsidiary Level and GCE Advanced Level MARK SCHEME for the May/June 2010 question paper for the guidance of teachers 9706 ACCOUNTING 9706/23

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Subsidiary Level and GCE Advanced Level MARK SCHEME for the May/June 2010 question paper for the guidance of teachers 9706 ACCOUNTING 9706/23

SIR MICHELANGELO REFALO

SIR MICHELANGELO REFALO SIXTH FORM Half-Yearly Exam 2015 Subject: ACCOUNTING ADV 1 st Time: 3 hrs Section A Answer all the questions in this section 1. Some clubs operate life membership schemes. (a) How

SIR MICHELANGELO REFALO SIXTH FORM Half-Yearly Exam 2015 Subject: ACCOUNTING ADV 1 st Time: 3 hrs Section A Answer all the questions in this section 1. Some clubs operate life membership schemes. (a) How

Paper Reference. Paper Reference(s) 4305/01 London Examinations IGCSE. Friday 3 November 2006 Afternoon Time: 2 hours 30 minutes

4305/01 London Examinations IGCSE. Friday 3 November 2006 Afternoon Time: 2 hours 30 minutes") Centre No. Candidate No. Paper Reference(s) 4305/01 London Examinations IGCSE Accounting Paper 1 Friday 3 November 2006 Afternoon Time: 2 hours 30 minutes Materials required for examination Nil Paper Reference

Centre No. Candidate No. Paper Reference(s) 4305/01 London Examinations IGCSE Accounting Paper 1 Friday 3 November 2006 Afternoon Time: 2 hours 30 minutes Materials required for examination Nil Paper Reference

VCE ACCOUNTING CLARIFICATION OF METHODS What terminology is going to be used in the June and November examinations in 2004?

VCE ACCOUNTING CLARIFICATION OF METHODS 2003 2006 What terminology is going to be used in the June and November eaminations in 2004? Terms to be used in eaminations Terms that will not be used in eaminations

VCE ACCOUNTING CLARIFICATION OF METHODS 2003 2006 What terminology is going to be used in the June and November eaminations in 2004? Terms to be used in eaminations Terms that will not be used in eaminations

XI ACCOUNTING REGULAR / PRIVATE. S.Hussain

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

ITL Public School Annual Examination ( ) Accountancy (Set -A)- answer key

Accountancy (Set -A)- answer key") ITL Public School Annual Examination (204-5) Accountancy (Set -A)- answer key Date: Class: XI Time: hrs M. M: 90 General Instructions:. All questions are compulsory 2. Marks for each question are indicated

ITL Public School Annual Examination (204-5) Accountancy (Set -A)- answer key Date: Class: XI Time: hrs M. M: 90 General Instructions:. All questions are compulsory 2. Marks for each question are indicated

QUESTION 1: Bank Reconciliation Statement (26 Marks; 10 Minutes) Slack Traders. Credit deposit not yet credited by the bank

Slack Traders. Credit deposit not yet credited by the bank") QUESTION 1: Bank Reconciliation Statement (26 Marks; 10 Minutes) Slack Traders Bank reconciliation statement on 31 May 2011 Debit Credit Debit balance as per bank statement 185 Credit deposit not yet credited

QUESTION 1: Bank Reconciliation Statement (26 Marks; 10 Minutes) Slack Traders Bank reconciliation statement on 31 May 2011 Debit Credit Debit balance as per bank statement 185 Credit deposit not yet credited

ACCOUNTING AND FINANCE

ACCBUS4 JUNE 2013 EXAMINATION DATE: 3 JUNE 2013 TIME: 09H00 12H00 TOTAL: 100 MARKS DURATION: 3 HOURS PASS MARK: 40% (BUS-AF) ACCOUNTING AND FINANCE THIS EXAMINATION PAPER CONSISTS OF 4 SECTIONS: SECTION

ACCBUS4 JUNE 2013 EXAMINATION DATE: 3 JUNE 2013 TIME: 09H00 12H00 TOTAL: 100 MARKS DURATION: 3 HOURS PASS MARK: 40% (BUS-AF) ACCOUNTING AND FINANCE THIS EXAMINATION PAPER CONSISTS OF 4 SECTIONS: SECTION

AccountAbility Edutools, USA, 2013, All Rights Reserved

(INX) LEDGER MANIA STUDENT INSTRUCTIONS Ledger Mania is an interactive classroom activity used to demonstrate the accounting cycle of a sole proprietorship or corporation. Students will physically record

(INX) LEDGER MANIA STUDENT INSTRUCTIONS Ledger Mania is an interactive classroom activity used to demonstrate the accounting cycle of a sole proprietorship or corporation. Students will physically record

ACCOUNTING. Written examination 1

Victorian Certificate of Education ACCOUNTING Written examination 1 Tuesday 10 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

Victorian Certificate of Education ACCOUNTING Written examination 1 Tuesday 10 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

Sample Question Paper Code-254 ELEMENTS OF BOOK KEEPING & ACCOUNTANCY Class-IX

Sample Question Paper Code-254 ELEMENTS OF BOOK KEEPING & ACCOUNTANCY Class-IX Summative Assessment-II March 2011 Examination Design of Question paper Time Allowed : 3 Hrs Maximum Marks : 80 01. Weightage

Sample Question Paper Code-254 ELEMENTS OF BOOK KEEPING & ACCOUNTANCY Class-IX Summative Assessment-II March 2011 Examination Design of Question paper Time Allowed : 3 Hrs Maximum Marks : 80 01. Weightage

Bookkeeping and Accounting 1

BOOBUS1 JUNE 2013 EXAMINATION DATE: 12 JUNE 2013 TIME: 14H00 16H30 TOTAL: 100 MARKS DURATION: 2½ HOURS PASS MARK: 40% (QL-11 / AU-55) Bookkeeping and ing 1 THIS EXAMINATION PAPER CONSISTS OF 2 SECTIONS:

BOOBUS1 JUNE 2013 EXAMINATION DATE: 12 JUNE 2013 TIME: 14H00 16H30 TOTAL: 100 MARKS DURATION: 2½ HOURS PASS MARK: 40% (QL-11 / AU-55) Bookkeeping and ing 1 THIS EXAMINATION PAPER CONSISTS OF 2 SECTIONS:

ACCOUNTING I Accounting reporting (ACN102N) (Module 2)

(Module 2)") ACN102N/202/2/2007 DEPATMENT OF FINANCIAL ACCOUNTING ACCOUNTING I Accounting reporting (ACN102N) (Module 2) Tutorial letter 202/2/2007 Dear student Enclosed the solution to Assignment 02/2007, the October

ACN102N/202/2/2007 DEPATMENT OF FINANCIAL ACCOUNTING ACCOUNTING I Accounting reporting (ACN102N) (Module 2) Tutorial letter 202/2/2007 Dear student Enclosed the solution to Assignment 02/2007, the October

An error is an irregularity in the accounting records that renders the financial statements not valid.

QUESTION 1 (a) An error is an irregularity in the accounting records that renders the financial statements not valid. i. List five (5) accounting errors that do not affect the agreement of the trial balance.

QUESTION 1 (a) An error is an irregularity in the accounting records that renders the financial statements not valid. i. List five (5) accounting errors that do not affect the agreement of the trial balance.

PART A RAM SLAM LTD STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 28 FEBRUARY 2014

PART A RAM SLAM LTD STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 28 FEBRUARY 2014 Depreciation -69 000 1 Interest on leased asset -25 920 2 Taxation 26 578 Current 16 800

PART A RAM SLAM LTD STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 28 FEBRUARY 2014 Depreciation -69 000 1 Interest on leased asset -25 920 2 Taxation 26 578 Current 16 800

Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an):

- Please choose one Wages outstanding given in the trial balance will be treated as a (an):") Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset Liability Revenue Deferred expense Question No: 2 ( Marks: 1 ) - Please choose

Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset Liability Revenue Deferred expense Question No: 2 ( Marks: 1 ) - Please choose

Practice exercise solutions

Bookkeeping to Trial Balance Practice exercise solutions Learning Module: An introduction to business, bookkeeping and accounting Practice exercise 1a (ii) (iii) (iv) (v) (vi) (vii) (viii) (ix) (x) D M

Bookkeeping to Trial Balance Practice exercise solutions Learning Module: An introduction to business, bookkeeping and accounting Practice exercise 1a (ii) (iii) (iv) (v) (vi) (vii) (viii) (ix) (x) D M

COMSATS Institute of Information Technology Abbottabad

COMSATS Institute of Information Technology Abbottabad Department of Management Sciences Terminal Section A Class: Date: Subject: Accounting Instructor: Zaheer A. Swati Time Allowed: 30 Minutes Max Marks:

COMSATS Institute of Information Technology Abbottabad Department of Management Sciences Terminal Section A Class: Date: Subject: Accounting Instructor: Zaheer A. Swati Time Allowed: 30 Minutes Max Marks:

1 R E C A L =Revenue, Expense, Capital, Assets, Liability Decrease Increase R Revenue D Debit C Credit E Expense C Credit D Debit C Capital D Debit C Credit A Assets C Credit D Debit L Liability D Debit

1 R E C A L =Revenue, Expense, Capital, Assets, Liability Decrease Increase R Revenue D Debit C Credit E Expense C Credit D Debit C Capital D Debit C Credit A Assets C Credit D Debit L Liability D Debit

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 4 Recording Transactions Chapter 3 - Recording Transactions Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this week s study,

ACC100 Introduction to Accounting Week 4 Recording Transactions Chapter 3 - Recording Transactions Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this week s study,

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Sole Trader Final Accounts

All questions copyright of Cambridge International Examinations 1 Sole Trader Final Accounts All questions copyright of Cambridge International Examinations 2 2 1 Amah Retto's ledger accounts for the year

All questions copyright of Cambridge International Examinations 1 Sole Trader Final Accounts All questions copyright of Cambridge International Examinations 2 2 1 Amah Retto's ledger accounts for the year

ACCOUNTING. Written examination 1. Monday 6 June 2005

Victorian CertiÞcate of Education ACCOUNTING Written examination 1 Monday 6 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

Victorian CertiÞcate of Education ACCOUNTING Written examination 1 Monday 6 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

Unit 10 : YEAR-END ADJUSTMENTS

Unit 10 : YEAR-END ADJUSTMENTS Slide 1.2 INTRODUCTION The most important point, which must be understood at the outset, is that all these adjustments have an impact on both the income statement/profit

Unit 10 : YEAR-END ADJUSTMENTS Slide 1.2 INTRODUCTION The most important point, which must be understood at the outset, is that all these adjustments have an impact on both the income statement/profit

Accounting Technicians Ireland First Year Examination: May 2017 Paper: FINANCIAL ACCOUNTING Tuesday 9 May a.m. to p.m.

Accounting Technicians Ireland First Year Examination: May 2017 Paper: FINANCIAL ACCOUNTING Tuesday 9 May 2017 9.30 a.m. to 12.30 p.m. INSTRUCTIONS TO CANDIDATES PLEASE READ CAREFULLY Candidates must indicate

Accounting Technicians Ireland First Year Examination: May 2017 Paper: FINANCIAL ACCOUNTING Tuesday 9 May 2017 9.30 a.m. to 12.30 p.m. INSTRUCTIONS TO CANDIDATES PLEASE READ CAREFULLY Candidates must indicate

PRINCE LIMITED You are provided with information for the financial year ended 28 February 2015.

REVISING ADJUSTMENTS FOR THE BALANCE SHEET (LIVE) Section B: Exam Questions Question 1 CONCEPTS GAAP PRINCIPLES 27 AUGUST 2015 REQUIRED: Choose an explanation from COLUMN B that matches a concept in COLUMN

REVISING ADJUSTMENTS FOR THE BALANCE SHEET (LIVE) Section B: Exam Questions Question 1 CONCEPTS GAAP PRINCIPLES 27 AUGUST 2015 REQUIRED: Choose an explanation from COLUMN B that matches a concept in COLUMN

ACCOUNTING: PAPER I INFORMATION BOOKLET

NATIONAL SENIOR CERTIFICATE EXAMINATION NOVEMBER ACCOUNTING: PAPER I Time: 2 hours 200 marks INFORMATION BOOKLET PLEASE TURN OVER Page ii of x QUESTION 1 ASSET MANAGEMENT (15 marks, 12 minutes) Information

NATIONAL SENIOR CERTIFICATE EXAMINATION NOVEMBER ACCOUNTING: PAPER I Time: 2 hours 200 marks INFORMATION BOOKLET PLEASE TURN OVER Page ii of x QUESTION 1 ASSET MANAGEMENT (15 marks, 12 minutes) Information

COMSATS Institute of Information Technology Abbottabad

COMSATS Institute of Information Technology Abbottabad Department of Management Sciences Terminal Section A: Spring 2017 Class: BBA 2 Date: 21-07-2017 Subject: Accounting I Instructor: Zaheer Swati Time

COMSATS Institute of Information Technology Abbottabad Department of Management Sciences Terminal Section A: Spring 2017 Class: BBA 2 Date: 21-07-2017 Subject: Accounting I Instructor: Zaheer Swati Time

ACCOUNTING. Written examination 1. Tuesday 9 June 2009

Victorian Certificate of Education ACCOUNTING Written examination 1 Tuesday 9 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

Victorian Certificate of Education ACCOUNTING Written examination 1 Tuesday 9 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

GRADE 10 ASSESSMENT TEST: 1 HOUR ACCOUNTING. Enter the correct source document next to the relevant journal in the space provided below:

GRADE 10 ASSESSMENT TEST: 1 HOUR ACCOUNTING QUESTION ONE (10 MARKS) Enter the correct source document next to the relevant journal in the space provided below: Source Document: Receipt Bank Statement Credit

GRADE 10 ASSESSMENT TEST: 1 HOUR ACCOUNTING QUESTION ONE (10 MARKS) Enter the correct source document next to the relevant journal in the space provided below: Source Document: Receipt Bank Statement Credit

Required: Draw up a three-column cash book to record the above transactions and balance off the cash book at the end of the month.

Chapter 1 Books of original entry and ledgers (I) Mary Company had the following transactions during the month November 2014: Nov 3 Credit purchases from: Hilary Lam $13,580, Tammy Yiu $55,500. 5 Credit

Chapter 1 Books of original entry and ledgers (I) Mary Company had the following transactions during the month November 2014: Nov 3 Credit purchases from: Hilary Lam $13,580, Tammy Yiu $55,500. 5 Credit

ACCOUNTING AND FINANCE

ACCBUS4 NOVEMBER 2012 EXAMINATION DATE: 5 NOVEMBER 2012 TIME: 09H00 12H00 TOTAL: 100 MARKS DURATION: 3 HOURS PASS MARK: 40% (BUS-AF / PD-58) ACCOUNTING AND FINANCE THIS EXAMINATION PAPER CONSISTS OF 2

ACCBUS4 NOVEMBER 2012 EXAMINATION DATE: 5 NOVEMBER 2012 TIME: 09H00 12H00 TOTAL: 100 MARKS DURATION: 3 HOURS PASS MARK: 40% (BUS-AF / PD-58) ACCOUNTING AND FINANCE THIS EXAMINATION PAPER CONSISTS OF 2

Date of Homework assigned: 7 Apr 2014 Due date: 16 Apr 2014 Exercise book: Book 1

2013-2014 / F.4 BAFS / HA11 / P.1 TWGHs Wong Fut Nam College Form 4 Business, Accounting and Financial Studies Homework Assignment 11 FA Ch1-3 Preparation of Financial Statements for Sole Proprietorships

2013-2014 / F.4 BAFS / HA11 / P.1 TWGHs Wong Fut Nam College Form 4 Business, Accounting and Financial Studies Homework Assignment 11 FA Ch1-3 Preparation of Financial Statements for Sole Proprietorships

ACCOUNTING. Written examination 2. Thursday 7 November 2002

ACCNT EXAM 2A Victorian Certificate of Education ACCOUNTING Written examination 2 Thursday 7 November 2002 Reading time: 11.45 am to 12.00 noon (15 minutes) Writing time: 12.00 noon to 1.30 pm (1 hour

ACCNT EXAM 2A Victorian Certificate of Education ACCOUNTING Written examination 2 Thursday 7 November 2002 Reading time: 11.45 am to 12.00 noon (15 minutes) Writing time: 12.00 noon to 1.30 pm (1 hour

WEEK 7 to 12: FINANCIAL ACCOUNTING FOR BUSINESS Accounting Cycle ACCOUNTING CYCLE STEP 1: RECOGNISE & RECORD TRANSACTIONS

WEEK 7 to 12: FINANCIAL ACCOUNTING FOR BUSINESS Accounting Cycle ACCOUNTING CYCLE STEP 1: RECOGNISE & RECORD TRANSACTIONS EXTERNAL TRANSACTIONS INTERNAL TRANSACTIONS NON-TRANSACTIONAL EVENTS Involves an

WEEK 7 to 12: FINANCIAL ACCOUNTING FOR BUSINESS Accounting Cycle ACCOUNTING CYCLE STEP 1: RECOGNISE & RECORD TRANSACTIONS EXTERNAL TRANSACTIONS INTERNAL TRANSACTIONS NON-TRANSACTIONAL EVENTS Involves an

GRADE 11 NOVEMBER 2013 ACCOUNTING ANSWER BOOK

SURNAME AND NAME: NATIONAL SENIOR CERTIFICATE GRADE 11 NOVEMBER ACCOUNTING ANSWER BOOK QUESTION MAX. MARKS 1 50 2 100 3 40 4 30 5 35 6 45 TOTAL 300 MARKS OBTAINED MODERATION This answer book consists of

SURNAME AND NAME: NATIONAL SENIOR CERTIFICATE GRADE 11 NOVEMBER ACCOUNTING ANSWER BOOK QUESTION MAX. MARKS 1 50 2 100 3 40 4 30 5 35 6 45 TOTAL 300 MARKS OBTAINED MODERATION This answer book consists of

P.G. Diploma in Banking and Finance EXAMINATION, 2017 BANKS, FINANCIAL INSTITUTIONS AND FINANCIAL MARKETS. Paper I

Total No. of Questions 5] [Total No. of Printed Pages 2 Seat No. [5179]-1 P.G. Diploma in Banking and Finance EXAMINATION, 2017 BANKS, FINANCIAL INSTITUTIONS AND FINANCIAL MARKETS Paper I Time : Three

Total No. of Questions 5] [Total No. of Printed Pages 2 Seat No. [5179]-1 P.G. Diploma in Banking and Finance EXAMINATION, 2017 BANKS, FINANCIAL INSTITUTIONS AND FINANCIAL MARKETS Paper I Time : Three

Shri Shahu Mandir Mahavidyalaya, Pune - 9

The main Advantages of a Computerized Accounting system are listed below: 1. Speed: Data entry onto the computer with its formatted screens and built-in databases of customers and supplier details and

The main Advantages of a Computerized Accounting system are listed below: 1. Speed: Data entry onto the computer with its formatted screens and built-in databases of customers and supplier details and

Adjusted Trial Balance Another Company Ltd - for period 01/04/2013 to 31/03/2014

Adjusted Trial Balance Another Company Ltd - for period 01/04/2013 to 31/03/2014 Account Quantity Client bal. DR CR Final Last Period Status Accounts 10+ *** FARM LIVESTOCK ACCOUNTS [100-169] *** - Livestock

Adjusted Trial Balance Another Company Ltd - for period 01/04/2013 to 31/03/2014 Account Quantity Client bal. DR CR Final Last Period Status Accounts 10+ *** FARM LIVESTOCK ACCOUNTS [100-169] *** - Livestock

QUESTION 1: Bank Reconciliation Statement (26 Marks; 10 Minutes)

") QUESTION 1: Bank Reconciliation Statement (26 Marks; 10 Minutes) SlackTraders Bank reconciliation statement on 31 May 2011 Debit Credit 1.2 1.2.1 1.2.2 1.2.3 QUESTION 2: Fixed Assets (50 Marks; 30 Minutes)

QUESTION 1: Bank Reconciliation Statement (26 Marks; 10 Minutes) SlackTraders Bank reconciliation statement on 31 May 2011 Debit Credit 1.2 1.2.1 1.2.2 1.2.3 QUESTION 2: Fixed Assets (50 Marks; 30 Minutes)

Assets - GL reconciliation

Another Company Ltd Assets - GL reconciliation Assets values are calculated based on: Control group Cost Accumulated depreciation Closing WDV Account GL balance Asset balance Variance Account GL balance

Another Company Ltd Assets - GL reconciliation Assets values are calculated based on: Control group Cost Accumulated depreciation Closing WDV Account GL balance Asset balance Variance Account GL balance

Question Paper Financial Accounting -I (MB131): October 2007

: October 2007") Page 1 of 20 Question Paper Financial Accounting -I (MB131): October 2007 Answer all questions. Marks are indicated against each question. 1. Which of the following is a current asset? Building Goodwill

Page 1 of 20 Question Paper Financial Accounting -I (MB131): October 2007 Answer all questions. Marks are indicated against each question. 1. Which of the following is a current asset? Building Goodwill

ACCA F3. Provided by Academy of Professional Accounting (APA) Financial Accounting (FA) 财务会计第十二讲. ACCA Lecturer: Carrie NI

Financial Accounting (FA) 财务会计第十二讲. ACCA Lecturer: Carrie NI") Professional Accounting Education Provided by Academy of Professional Accounting (APA) ACCA F3 Financial Accounting (FA) 财务会计第十二讲 ACCA Lecturer: Carrie NI ACCAspace 中国 ACCA 特许公认会计师教育平台 Copyright ACCAspace.com

Professional Accounting Education Provided by Academy of Professional Accounting (APA) ACCA F3 Financial Accounting (FA) 财务会计第十二讲 ACCA Lecturer: Carrie NI ACCAspace 中国 ACCA 特许公认会计师教育平台 Copyright ACCAspace.com

Income Revenue: Total Sales ( x 30% x 60%) x 100/ Subscription Fees ( x 12/15 x 100/114)

x 100/ Subscription Fees ( x 12/15 x 100/114)") FAC2601 May/June 2013 Solution QUESTION 1 FIND ME LTD STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 28 FEBRUARY 2013 R Revenue 5 210 000 Cost Of Sales (55%) (2 865 000)

FAC2601 May/June 2013 Solution QUESTION 1 FIND ME LTD STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 28 FEBRUARY 2013 R Revenue 5 210 000 Cost Of Sales (55%) (2 865 000)