(Wales) Civil Legal Advice (Freephone)

|

|

|

- Jeffrey O’Brien’

- 6 years ago

- Views:

Transcription

1 ANNEX 1 INFORMATION SHEET You have received this notice because a business intends to take you to court in relation to a debt. This notice tells you what to do next, including how to avoid court action. Please read it carefully. What should I do now to make sure I am not taken to court unnecessarily? Read the enclosed letter from the business very carefully. Think about whether you owe the debt and whether the amount is correct. The letter should provide information about how much money you owe and any interest and fees added to the debt. If it doesn t, ask the business for more information. Once you have read the letter, consider the following options. Seeking debt advice. If you are in financial difficulty or need advice to help you work out whether you owe the debt, or how you might pay the debt, contact a debt advisor (particularly if you haven t been in contact with the business for a number of years). The following organisations offer free, impartial and non-judgemental advice: Citizens Advice (England) (Wales) Civil Legal Advice StepChange Debt Charity (Freephone) National Debtline (Freephone) AdviceUK Christians Against Poverty (Freephone) It is recommended that you get debt advice if you have any doubt about whether you owe the debt or whether you can pay it now. If you don t have a copy of the agreement (contract) between you and the business, and you need this to decide what to do next or to help you get debt advice, you can ask the business to provide you with a copy. Speaking to the business. If you agree you owe the debt and want to talk to the business about payment terms, or if you have any questions or concerns, get in touch with the business as soon as possible. Their contact details should be in the letter they sent you. 1

2 Filling in the Reply Form. If you have not been able to resolve the matter by speaking to the business, you should fill in the Reply Form that was provided with the letter from the business, and then send it back to the business. You should complete the Reply Form with as much information as possible to avoid court action being taken against you. How long do I have to fill in the Reply Form? You only have 30 days from the date at the top of the letter from the business to send back the Reply Form. If the business does not get your Reply Form within 30 days, it could take you to court in relation to the debt. Make sure you allow time for posting. If a court orders you to pay an amount of money (called having judgment entered against you ), details of the judgment will usually be entered on the Register of Judgments, Orders and Fines. Most entries stay on the Register for six years unless you pay the amount you owe within one month of the judgment. Organisations such as banks, building societies and credit companies use the information on the Register when someone applies for credit, such as a loan or overdraft. It helps them decide whether or not that person would be able to pay off a debt. What happens if I fill in and return the Reply Form in time? If you return the Reply Form within 30 days, you and the business will have at least a further 30 days to discuss the debt, or for you to seek debt advice, before the business takes you to court. During that time you should discuss with the business how you can resolve the matter, ideally without going to court. If you request more information in the Reply Form, the business must wait at least 30 days after it gives you that information before taking you to court. Where can I find out more? This Information Sheet is a summary of your rights and responsibilities under the Pre- Action Protocol for Debt Claims. Where a business and an individual disagree about a debt claim, the Protocol tells them what they should do before they go to court. If you want to know more, the full Protocol is available at: 2

3 REPLY FORM YOU HAVE 30 DAYS FROM THE DATE AT THE TOP OF THE ENCLOSED LETTER TO FILL IN AND RETURN THIS FORM. IF YOU DON T, IT COULD RESULT IN COURT PROCEEDINGS. If you have any questions or would like to discuss the debt, please call the business that sent you this form as soon as possible. Full name: Address and postcode: Contact telephone numbers: address: Reference: SECTION 1: Do you owe the debt? Fill in one of the boxes in this section. Use more pages if you need to. It is recommended that you get debt advice if you have any doubt about whether you owe the debt and whether you can pay it now, or if you want advice on any rights and protections you may have. Box G below asks about debt advice. BOX A I agree I owe the debt. Tick this box if you agree you owe the debt and agree the amount of the debt is correct. IF YOU WILL PAY THE DEBT, GO TO SECTION 2. IF YOU NEED DEBT OR LEGAL ADVICE, GO TO SECTION 3. BOX B I owe some of the debt, but not all of it. Tick this box if you agree you owe some of the debt, but not all of it, for example if you think too much interest has been added or you haven t been credited for payments you made in the past. The amount of debt I owe to you is.. Say how much you think you owe. I don t owe any more than this because Explain on a separate piece of paper why you don t owe all of the debt. Give as much detail as possible and provide copies of any supporting documents. IF YOU WILL PAY THE PART OF THE DEBT YOU OWE, GO TO SECTION 2. IF YOU NEED DEBT OR LEGAL ADVICE, GO TO SECTION 3. OTHERWISE, GO TO SECTION 4. 3

4 BOX C I don t know whether I owe the debt. Tick this box if you re not sure whether you owe the debt and/or you need help from a debt adviser to work out whether you should pay. NOW GO TO SECTION 3. BOX D I dispute the debt. Tick this box if you don t owe the debt, for example because the debt should be paid by someone else, because you have already paid it, or because there is a legal problem with the credit agreement. I dispute the debt because Explain on a separate piece of paper why you dispute the debt. Give as much detail as possible and provide copies of any supporting documents. NOW GO TO SECTION 4. SECTION 2: How will you pay? Only complete this section if you ticked Box A or Box B in Section 1 and you want to pay now. The letter from the business will tell you how to pay. Keep a record of the payments you make. BOX E I will pay what I owe now. Tick this box if you agree that you owe all or part of the debt and you are able to pay what you owe now. You should pay using the payment details in the letter from the business. Keep a copy of any proof of payment you receive. BOX F I will pay, but I need time to pay. Tick this box if you agree that you owe all or part of the debt, but you can t pay right now. If you offer to make repayments, you must be able to afford them. You should consider getting debt advice about how much you can afford to repay. If you are seeking debt advice, complete Section 3. My proposals for repayment are... Explain on a separate piece of paper how you intend to pay the debt. Say how much you could pay now and how you will pay the remainder. For example, say how much you could pay each week, fortnight or month and when your first payment would be made. I have provided a Financial Statement showing my current financial situation: Yes No To help the business ensure you can afford your proposed repayments, fill out the Financial Statement that is attached to this form. You should also attach a copy of any budget or financial statement that a debt advice organisation has helped you prepare. SECTION 3: Do you intend to get, or are you already getting, debt advice? 4

5 Only complete this section if you are getting debt advice about whether you owe the debt or whether you can afford to pay. BOX G I am getting or intend to get debt advice. I am getting advice from Insert the name and contact details of the person or organisation giving you advice. I am getting advice about Explain on a separate piece of paper what you are getting advice about, for example whether you owe the debt or how you could pay. I have an appointment with an adviser on... If you have an appointment with a debt adviser, give the appointment date and time. I can t obtain advice within 30 days of returning this Reply Form because. If it will take you longer than 30 days to get debt advice, explain on a separate piece of paper the reason for the delay and when you expect advice will be available. NOW COMPLETE SECTION 4. SECTION 4: What documents are you sending with this form? What information do you need? Complete the boxes below if you want to provide or get more information. BOX H I have provided documents. Tick this box if you want to provide documents about the debt, for example you might want to provide a letter showing you have an appointment for debt advice or a receipt showing you paid some of the debt. I have enclosed the following documents... Describe on a separate piece of paper the documents you have provided and why they are important. BOX I I need more documents or information. Tick this box if you need more information, such as copies of documents you don t currently have. I need a copy of.. Additional documents or information that you might need could include: A copy of the written contract for the debt A full statement of account, including details of all interest and charges included on the outstanding balance of the debt, explaining how they have been calculated, and any payments already made toward the debt A calculation of the interest claimed The annual or daily rate of interest 5

6 A description of the nature and amount of any administrative charges included in the debt A copy of the notice of assignment of the debt Signature. Date /.../. Print name. Sign and date this Reply Form once you ve filled it in. Then send it to the address given in the letter from the business. Make sure you keep a copy of this form for reference in the future. If your circumstances change, please update the business as soon as possible. 6

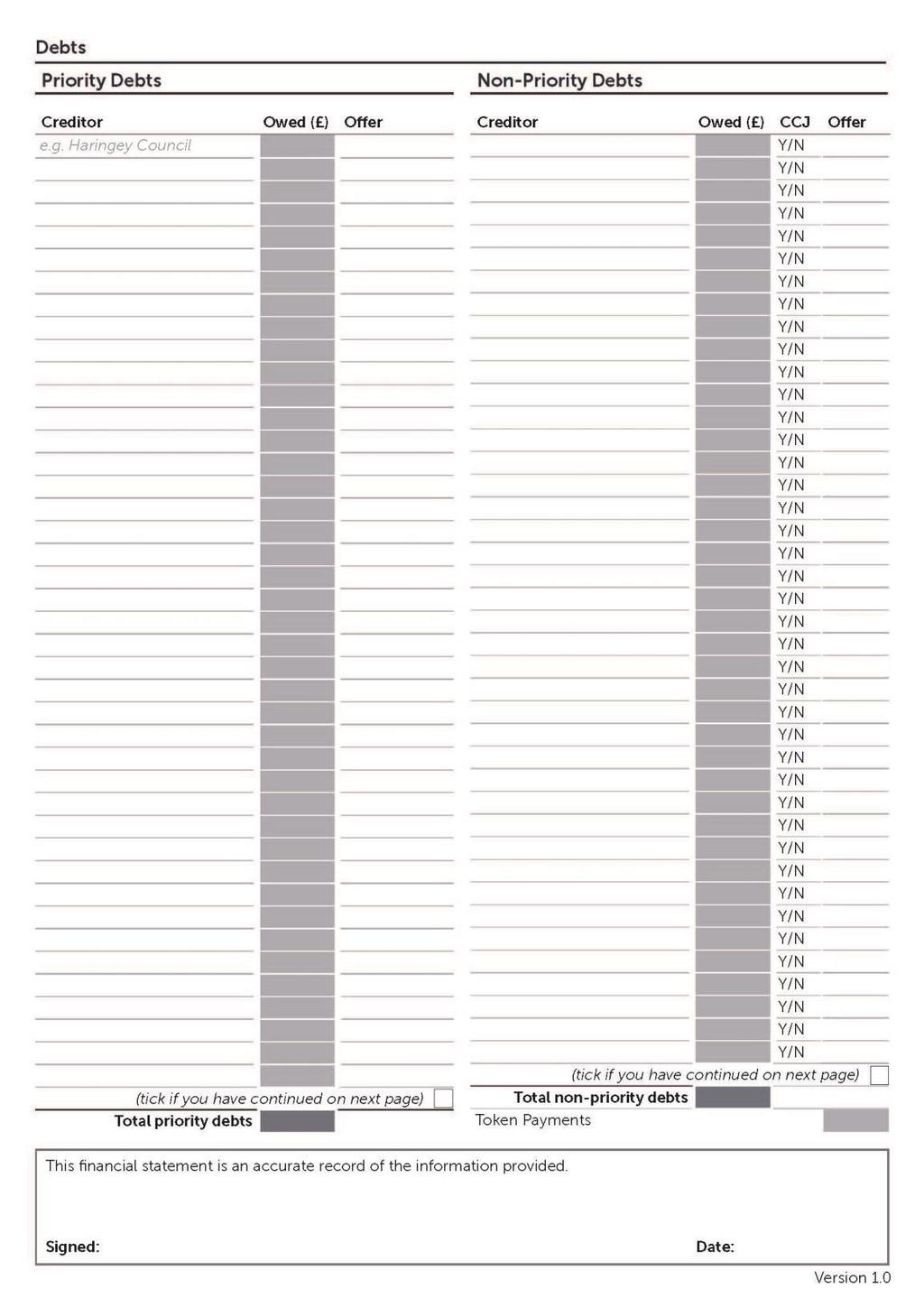

7 ANNEX 2 STANDARD FINANCIAL STATEMENT 7

8 8

9 9

10 Reproduced with permission of the Money Advice Service 10

The Pre-Action Protocol for Debt Claims is made by the Master of the Rolls as Head of Civil Justice. The Protocol comes into force on 1 October 2017

The Pre-Action Protocol for Debt Claims is made by the Master of the Rolls as Head of Civil Justice. The Protocol comes into force on 1 October 2017 The Right Honourable Sir Terence Etherton Master of

The Pre-Action Protocol for Debt Claims is made by the Master of the Rolls as Head of Civil Justice. The Protocol comes into force on 1 October 2017 The Right Honourable Sir Terence Etherton Master of

Interest Rates, Charges & Important Information

Interest Rates, Charges & Important Information Guide To Changes We are making some changes to this brochure. The changes will come into effect on 6th April 2018 and will apply to all St. James s Place

Interest Rates, Charges & Important Information Guide To Changes We are making some changes to this brochure. The changes will come into effect on 6th April 2018 and will apply to all St. James s Place

Interest rates, charges and important information

Interest rates, charges and important information Guide to Changes: We are making some changes to this brochure. The changes will come into effect on 6 April 2018 and will apply to all Intelligent Finance

Interest rates, charges and important information Guide to Changes: We are making some changes to this brochure. The changes will come into effect on 6 April 2018 and will apply to all Intelligent Finance

Dealing with debt. A guide for customers

Dealing with debt A guide for customers How you can get help Banks are here to help you run your finances smoothly in a complicated world. You can get help in good and bad times. Banks understand that

Dealing with debt A guide for customers How you can get help Banks are here to help you run your finances smoothly in a complicated world. You can get help in good and bad times. Banks understand that

Interest rates, charges and important information

Interest rates, charges and important information CONTENTS Savings 1 Current Accounts 9 International Payment Services 13 Mortgages 14 Important Information 15 Savings Intelligent Finance isaver Intelligent

Interest rates, charges and important information CONTENTS Savings 1 Current Accounts 9 International Payment Services 13 Mortgages 14 Important Information 15 Savings Intelligent Finance isaver Intelligent

Code of practice for recovering domestic water debt

Code of practice for recovering domestic water debt Contents 2 What to do if you can t pay your bill 3 How we can help 5 How to pay 7 What if you don t pay the bill or don t keep to an agreement? 9 What

Code of practice for recovering domestic water debt Contents 2 What to do if you can t pay your bill 3 How we can help 5 How to pay 7 What if you don t pay the bill or don t keep to an agreement? 9 What

Options for dealing with debt

Options for dealing with debt This factsheet explains what you can do if you cannot afford your debts. It gives an overview of the options that you may have, but is not a suitable alternative to speaking

Options for dealing with debt This factsheet explains what you can do if you cannot afford your debts. It gives an overview of the options that you may have, but is not a suitable alternative to speaking

Information about. Support for Mortgage Interest (SMI) benefit ending INFSMI 08/17. Please make sure you read and understand this information booklet

benefit ending INFSMI 08/17. Please make sure you read and understand this information booklet") Information about Support for Mortgage Interest (SMI) benefit ending Please make sure you read and understand this information booklet This information booklet tells you about the SMI benefit ending and

Information about Support for Mortgage Interest (SMI) benefit ending Please make sure you read and understand this information booklet This information booklet tells you about the SMI benefit ending and

Code of practice for recovering domestic water debt

Code of practice for recovering domestic water debt Contents 2 What to do if you can t pay your bill 3 How we can help 5 How to pay 7 What if you don t pay the bill or don t keep to an agreement? 9 What

Code of practice for recovering domestic water debt Contents 2 What to do if you can t pay your bill 3 How we can help 5 How to pay 7 What if you don t pay the bill or don t keep to an agreement? 9 What

Get advice now. Are you worried about your mortgage? New edition

New edition April 2016 Are you worried about your mortgage? Get advice now If you are struggling to pay your mortgage or are worried about an interest rate change, you need to act now to stop your situation

New edition April 2016 Are you worried about your mortgage? Get advice now If you are struggling to pay your mortgage or are worried about an interest rate change, you need to act now to stop your situation

MANAGING DEBT.

MANAGING DEBT www.nwl.co.uk MANAGING DEBT OUR CODE OF PRACTICE: THE COLLECTION OF DEBT FOR DOMESTIC CUSTOMERS The water services we provide to your property have to be paid for, but we know that finding

MANAGING DEBT www.nwl.co.uk MANAGING DEBT OUR CODE OF PRACTICE: THE COLLECTION OF DEBT FOR DOMESTIC CUSTOMERS The water services we provide to your property have to be paid for, but we know that finding

Application Form ScottishPower Hardship Fund

Application Form ScottishPower Hardship Fund ALTERNATIVELY, APPLY ONLINE AT www.sedhardship.fund BEFORE COMPLETING THIS FORM, PLEASE CAREFULLY READ THE NOTES BELOW WHO CAN APPLY FOR AN AWARD? ScottishPower

Application Form ScottishPower Hardship Fund ALTERNATIVELY, APPLY ONLINE AT www.sedhardship.fund BEFORE COMPLETING THIS FORM, PLEASE CAREFULLY READ THE NOTES BELOW WHO CAN APPLY FOR AN AWARD? ScottishPower

Support for Mortgage Interest

Support for Mortgage Interest welfare changes Your support for Mortgage Interest will end on 5 April 2018 You currently get a benefit called Support for Mortgage Interest (SMI) which is also known as

Support for Mortgage Interest welfare changes Your support for Mortgage Interest will end on 5 April 2018 You currently get a benefit called Support for Mortgage Interest (SMI) which is also known as

Application Form ScottishPower Hardship Fund

Application Form ScottishPower Hardship Fund ALTERNATIVELY, APPLY ONLINE AT www.sedhardship.fund BEFORE COMPLETING THIS FORM, PLEASE CAREFULLY READ THE NOTES BELOW WHO CAN APPLY FOR AN AWARD? ScottishPower

Application Form ScottishPower Hardship Fund ALTERNATIVELY, APPLY ONLINE AT www.sedhardship.fund BEFORE COMPLETING THIS FORM, PLEASE CAREFULLY READ THE NOTES BELOW WHO CAN APPLY FOR AN AWARD? ScottishPower

Services for prepayment customers

Services for prepayment customers Introduction A prepayment meter allows you to pay for your gas and electricity as you use it and, if you need to, pay off outstanding debt at an agreed weekly rate taken

Services for prepayment customers Introduction A prepayment meter allows you to pay for your gas and electricity as you use it and, if you need to, pay off outstanding debt at an agreed weekly rate taken

Frequently Asked Questions about Support for Mortgage Interest loans

Frequently Asked Questions about Support for loans General questions What is Support for (SMI)? Why is Support for changing to a loan? Who is offering the loan? At the moment you get a benefit called Interest

Frequently Asked Questions about Support for loans General questions What is Support for (SMI)? Why is Support for changing to a loan? Who is offering the loan? At the moment you get a benefit called Interest

Can t Pay Your Mortgage?

Can t Pay Your Mortgage? Helpful advice from the BSA and the Money Advice Trust Can t Pay Your Mortgage? Having problems paying your mortgage can be one of the most stressful and traumatic problems that

Can t Pay Your Mortgage? Helpful advice from the BSA and the Money Advice Trust Can t Pay Your Mortgage? Having problems paying your mortgage can be one of the most stressful and traumatic problems that

Joint and Several Liability. Partnership responsibilities

Joint and Several Liability Partnership responsibilities If you re going into business with partners, you need to know about Joint and Several Liability. This brochure highlights the main issues. Contents

Joint and Several Liability Partnership responsibilities If you re going into business with partners, you need to know about Joint and Several Liability. This brochure highlights the main issues. Contents

Support with financial difficulties

Support with financial difficulties 0800 781 8558 precisemortgages-customers.co.uk Please read this document carefully As a responsible lender, we want to reassure all our customers that we will treat

Support with financial difficulties 0800 781 8558 precisemortgages-customers.co.uk Please read this document carefully As a responsible lender, we want to reassure all our customers that we will treat

Is A Prepayment Meter For You?

Is A Prepayment Meter For You? If you are considering a prepayment meter you should be aware of the following before making your decision: Prepayment meters ensure that you pay for your electricity up

Is A Prepayment Meter For You? If you are considering a prepayment meter you should be aware of the following before making your decision: Prepayment meters ensure that you pay for your electricity up

Flexible Home Loan. This document sets out your facility s terms and conditions. Some key information about your facility. Terms and Conditions

Flexible Home Loan Terms and Conditions This document sets out your facility s terms and conditions In this document we ve explained the terms and conditions applying to your ANZ Flexible Home Loan. It

Flexible Home Loan Terms and Conditions This document sets out your facility s terms and conditions In this document we ve explained the terms and conditions applying to your ANZ Flexible Home Loan. It

Triodos Bank Organisation application for Depository Receipts in Triodos Bank NV.

Triodos Bank Organisation application for Depository Receipts in Triodos Bank NV. Important notice In order to complete this application form you need to know what the current sterling price is for each

Triodos Bank Organisation application for Depository Receipts in Triodos Bank NV. Important notice In order to complete this application form you need to know what the current sterling price is for each

Health Cash Benefits Cover claim form

Health Cash Benefits Cover claim form 1 Membership details policyholder s full name policyholder s address Postcode Date of birth D D M M Y Y Y Y Membership number Phone number Email address 2 Patient

Health Cash Benefits Cover claim form 1 Membership details policyholder s full name policyholder s address Postcode Date of birth D D M M Y Y Y Y Membership number Phone number Email address 2 Patient

Guaranteed Pension Annuity

Guaranteed Pension Annuity Key Features Please read this document along with your personal illustration (if you have one) before you decide to buy this plan. It s important you understand how the Guaranteed

Guaranteed Pension Annuity Key Features Please read this document along with your personal illustration (if you have one) before you decide to buy this plan. It s important you understand how the Guaranteed

Help and advice for paying your bills

Help and advice for paying your bills 2 2 2 3 4 5 Contents Introduction How your bills are worked out How to pay your bills Choose your payment scheme Making arrangements to pay How to get help if you

Help and advice for paying your bills 2 2 2 3 4 5 Contents Introduction How your bills are worked out How to pay your bills Choose your payment scheme Making arrangements to pay How to get help if you

Overdraft agreement ANZ Jumpstart account

Your details Our details ANZ Bank New Zealand Limited Our registered office is Ground Floor, ANZ Centre, 23-29 Albert Street, Auckland, 1010. More information about us, including the branch

Your details Our details ANZ Bank New Zealand Limited Our registered office is Ground Floor, ANZ Centre, 23-29 Albert Street, Auckland, 1010. More information about us, including the branch

Five Simple Steps to Managing your Energy Bills. Helping you afford to keep warm

Five Simple Steps to Managing your Energy Bills Helping you afford to keep warm Step One - Try not to panic You have bills from your energy supplier you can t pay, debts building up and you re scared about

Five Simple Steps to Managing your Energy Bills Helping you afford to keep warm Step One - Try not to panic You have bills from your energy supplier you can t pay, debts building up and you re scared about

PAUSE AND THINK BEFORE YOU BORROW

PAUSE AND THINK BEFORE YOU BORROW Short-term loans can help you out of a hole when the unexpected happens and you just don t have enough money to cover the essentials this month. The trouble is, if you

PAUSE AND THINK BEFORE YOU BORROW Short-term loans can help you out of a hole when the unexpected happens and you just don t have enough money to cover the essentials this month. The trouble is, if you

Endowment mortgage complaints

Endowment mortgage complaints Steps to take if you think you may have been mis-sold your endowment mortgage What you can complain about Time limits How compensation is worked out The Money Advice Service

Endowment mortgage complaints Steps to take if you think you may have been mis-sold your endowment mortgage What you can complain about Time limits How compensation is worked out The Money Advice Service

Help someone. with problem debt. A three step referral guide from StepChange Debt Charity. IDENTIFY customers who may need us

Help someone with problem debt A three step referral guide from StepChange Debt Charity 1 2 3 IDENTIFY customers who may need us PREPARE them for the debt advice process REFER them to us for help 1 IDENTIFY:

Help someone with problem debt A three step referral guide from StepChange Debt Charity 1 2 3 IDENTIFY customers who may need us PREPARE them for the debt advice process REFER them to us for help 1 IDENTIFY:

BMI Card application form

Please note that we will be unable to process your BMI Card application if you do not provide a signature in the credit agreement section on page 7. BMI Card application form CREDIT CARD AGREEMENT REGULATED

Please note that we will be unable to process your BMI Card application if you do not provide a signature in the credit agreement section on page 7. BMI Card application form CREDIT CARD AGREEMENT REGULATED

JOINT AND SEVERAL LIABILITY. Partnership responsibilities

JOINT AND SEVERAL LIABILITY Partnership responsibilities June 2016 Contents Why do I need to know about it? 1 What does Joint and Several Liability mean? 1 How do we open a partnership account? 2 How does

JOINT AND SEVERAL LIABILITY Partnership responsibilities June 2016 Contents Why do I need to know about it? 1 What does Joint and Several Liability mean? 1 How do we open a partnership account? 2 How does

Social Rented Housing Application

Social Rented Housing Application The Application Form Completion Notes will explain how to fill out your Application Form and what some of the words and phrases mean. If you have a question about the

Social Rented Housing Application The Application Form Completion Notes will explain how to fill out your Application Form and what some of the words and phrases mean. If you have a question about the

Key Features of the Guaranteed Pension Annuity

Key Features of the Guaranteed Pension Annuity Please read this document along with your personal illustration (if you have one) before you decide to buy this plan. It's important you understand how the

Key Features of the Guaranteed Pension Annuity Please read this document along with your personal illustration (if you have one) before you decide to buy this plan. It's important you understand how the

Money matters: Cancelling contracts

Money matters: Cancelling contracts If you cannot make decisions for yourself, this is called lacking capacity. This factsheet explains what happens if you borrow money from a lender when you lack capacity.

Money matters: Cancelling contracts If you cannot make decisions for yourself, this is called lacking capacity. This factsheet explains what happens if you borrow money from a lender when you lack capacity.

Debt Management Plan Agreement

Debt Management Plan Agreement Introduction Following the review of your financial circumstances which led to our recommendation of a debt management plan (DMP) to deal with your debts, this Agreement

Debt Management Plan Agreement Introduction Following the review of your financial circumstances which led to our recommendation of a debt management plan (DMP) to deal with your debts, this Agreement

Citizens Advice / ABCUL Frequently asked questions for advisers

Citizens Advice / ABCUL 2008 Frequently asked questions for advisers 1 This guide for advisers aims to answer some of the additional questions you may have about TV Licensing. If you need any more help

Citizens Advice / ABCUL 2008 Frequently asked questions for advisers 1 This guide for advisers aims to answer some of the additional questions you may have about TV Licensing. If you need any more help

Basic Debt. Guidance for conversations on basic debt issues. Trainers Notes for basic debt with clients. Citizens Advice financial capability

Basic Debt Guidance for conversations on basic debt issues Trainers Notes for basic debt with clients 1 This session pack has been produced as part of Citizens Advice Financial Skills for Life. Although

Basic Debt Guidance for conversations on basic debt issues Trainers Notes for basic debt with clients 1 This session pack has been produced as part of Citizens Advice Financial Skills for Life. Although

Application for Assure tariff

Application for Assure tariff What is the Assure tariff? The Assure tariff can help household customers on a low income or who are struggling to pay their water charges. It aims to make our bills more

Application for Assure tariff What is the Assure tariff? The Assure tariff can help household customers on a low income or who are struggling to pay their water charges. It aims to make our bills more

HSBC Premier Credit Card. Terms and conditions

HSBC Premier Credit Card Terms and conditions 2 Credit Card Agreement regulated by the Consumer Credit Act 1974. This agreement is made up of the key terms and the additional terms. Key Terms How much

HSBC Premier Credit Card Terms and conditions 2 Credit Card Agreement regulated by the Consumer Credit Act 1974. This agreement is made up of the key terms and the additional terms. Key Terms How much

Code of Practice. Services. for pre-payment customers

Services for pre-payment customers Contents 2 Introduction 2 When will a prepayment meter be installed in your home? 3 How to use your prepayment meter 3 Where to make payments 3 What happens if the machine

Services for pre-payment customers Contents 2 Introduction 2 When will a prepayment meter be installed in your home? 3 How to use your prepayment meter 3 Where to make payments 3 What happens if the machine

PEGASUS WHOLE OF LIFE PLAN

KEY FACTS OF OUR PEGASUS WHOLE OF LIFE PLAN January 2018 Important information you should read Protection Pegasus Whole of Life WHAT S INSIDE See if our plan is right for you 3 The aims of our plan 3 Your

KEY FACTS OF OUR PEGASUS WHOLE OF LIFE PLAN January 2018 Important information you should read Protection Pegasus Whole of Life WHAT S INSIDE See if our plan is right for you 3 The aims of our plan 3 Your

Taking a lump sum from a plan already in Drawdown

Taking a lump sum from a plan already in Drawdown (only use this form if you are requesting a withdrawal of less than 50,000) What this form is for 0817 Only use this form if you have a Self Invested Personal

Taking a lump sum from a plan already in Drawdown (only use this form if you are requesting a withdrawal of less than 50,000) What this form is for 0817 Only use this form if you have a Self Invested Personal

Are you in financial hardship?

Are you in financial hardship? Am I in financial hardship? You are in financial hardship if it s difficult to make your loan or lease payments or your other financial obligations. Your financial hardship

Are you in financial hardship? Am I in financial hardship? You are in financial hardship if it s difficult to make your loan or lease payments or your other financial obligations. Your financial hardship

and the details of anyone complaining with you surname title title first name(s) occupation (if retired, previous occupation)

occupation (if retired, previous occupation)") our ref Financial Ombudsman Service Ltd, July 2011 complaint form Please use this form to tell us about your complaint so we can see if we re able to help you. If you re not sure about anything or have

our ref Financial Ombudsman Service Ltd, July 2011 complaint form Please use this form to tell us about your complaint so we can see if we re able to help you. If you re not sure about anything or have

Agreement terms M&S CREDIT CARD. Key terms

M&S CREDIT CARD Agreement terms Credit Card Agreement regulated by the Consumer Credit Act 1974. This agreement is made up of the key terms and the additional terms. Key terms How much can you borrow?

M&S CREDIT CARD Agreement terms Credit Card Agreement regulated by the Consumer Credit Act 1974. This agreement is made up of the key terms and the additional terms. Key terms How much can you borrow?

TELEPHONE Anglian Water: Hartlepool Water: WRITE Anglian Water Customer Services PO Box 4994 Lancing BN11 9AL

TELEPHONE Anglian Water: 0800 169 3630 Hartlepool Water: 0800 051 8969 WRITE Anglian Water Customer Services PO Box 4994 Lancing BN11 9AL 24 HOUR EMERGENCY LINE 03457 145 145 LEAK LINE 0800 771 881 WEBSITE

TELEPHONE Anglian Water: 0800 169 3630 Hartlepool Water: 0800 051 8969 WRITE Anglian Water Customer Services PO Box 4994 Lancing BN11 9AL 24 HOUR EMERGENCY LINE 03457 145 145 LEAK LINE 0800 771 881 WEBSITE

SF318MAY2018 Page 1 of 5. Authorisation for a Manual Transfer to a Current Account ( Transfer )

") Authorisation for a Manual Transfer to a Current Account ( Transfer ) Use this Form to transfer to a Nationwide current account from one of the following: a current account with another UK bank or building

Authorisation for a Manual Transfer to a Current Account ( Transfer ) Use this Form to transfer to a Nationwide current account from one of the following: a current account with another UK bank or building

Please get back in touch if you are reading this some months after the publication date, in case it has been updated. Background 2

A guide to Permitted Work April 2016 The information in this factsheet is correct at the date of publication. However, the Government has announced a number of reforms that will affect welfare benefits

A guide to Permitted Work April 2016 The information in this factsheet is correct at the date of publication. However, the Government has announced a number of reforms that will affect welfare benefits

You and your joint account

You and your joint account A guide for customers Cover image: HD Connelly, 2010 Used under license from Shutterstock.com. How can this leaflet help me? This document will help if you currently hold or

You and your joint account A guide for customers Cover image: HD Connelly, 2010 Used under license from Shutterstock.com. How can this leaflet help me? This document will help if you currently hold or

Mortgage Terms and Conditions (T&Cs)

") Mortgage Terms and Conditions (T&Cs) Banking with Atom is straightforward, so we ve split our T&Cs into three manageable chunks: General T&Cs; Product T&Cs; and product specific documents, based on the

Mortgage Terms and Conditions (T&Cs) Banking with Atom is straightforward, so we ve split our T&Cs into three manageable chunks: General T&Cs; Product T&Cs; and product specific documents, based on the

General Mortgage Conditions

General Mortgage Conditions England and Wales 2013 Introduction Over the following pages, you ll find the general conditions of your mortgage. This booklet is very important because it forms part of the

General Mortgage Conditions England and Wales 2013 Introduction Over the following pages, you ll find the general conditions of your mortgage. This booklet is very important because it forms part of the

APPLICATION FOR FINANCIAL ASSISTANCE

APPLICATION FOR FINANCIAL ASSISTANCE ALTERNATIVELY APPLY ONLINE VIA THE FUND S WEBSITE WWW.NPOWERENERGYFUND.COM before COMPLETING THE APPLICATION form, PLEASE CAREfULLY READ THE NOTES below. When you have

APPLICATION FOR FINANCIAL ASSISTANCE ALTERNATIVELY APPLY ONLINE VIA THE FUND S WEBSITE WWW.NPOWERENERGYFUND.COM before COMPLETING THE APPLICATION form, PLEASE CAREfULLY READ THE NOTES below. When you have

INSTANT SAVER 2 ACCOUNT

INSTANT SAVER 2 ACCOUNT Provided by Scottish Widows Bank SUMMARY BOX PLEASE READ THIS SUMMARY BOX BEFORE YOU COMPLETE THE APPLICATION AND THEN KEEP IT FOR YOUR RECORDS. DON T RETURN IT WITH THE APPLICATION.

INSTANT SAVER 2 ACCOUNT Provided by Scottish Widows Bank SUMMARY BOX PLEASE READ THIS SUMMARY BOX BEFORE YOU COMPLETE THE APPLICATION AND THEN KEEP IT FOR YOUR RECORDS. DON T RETURN IT WITH THE APPLICATION.

ENGIE Prepayment. A Guide to your prepayment meter

ENGIE Prepayment A Guide to your prepayment meter 1 An introduction to prepayment Welcome to prepayment from all of us here at ENGIE. This guide is here to give you lots of information about prepayment

ENGIE Prepayment A Guide to your prepayment meter 1 An introduction to prepayment Welcome to prepayment from all of us here at ENGIE. This guide is here to give you lots of information about prepayment

A guide to your mortgage

A guide to your mortgage Residential mortgages PAGE 1 OF 40 A straightforward guide to your new Paragon mortgage This guide takes you through what happens when you purchase a new home and take out a mortgage

A guide to your mortgage Residential mortgages PAGE 1 OF 40 A straightforward guide to your new Paragon mortgage This guide takes you through what happens when you purchase a new home and take out a mortgage

OUR RELEVANT LIFE PLAN

KEY FACTS OF OUR RELEVANT LIFE PLAN January 2018 Important information you should read Protection Relevant Life WHAT S INSIDE See if our plan is right for you 3 The aims of our plan 3 Your commitment 4

KEY FACTS OF OUR RELEVANT LIFE PLAN January 2018 Important information you should read Protection Relevant Life WHAT S INSIDE See if our plan is right for you 3 The aims of our plan 3 Your commitment 4

Triodos Bank. Current Account switch guide

Triodos Bank. Current Account switch guide About the service The Current Account Switch Service makes switching current accounts to Triodos Bank from another UK bank or building society simple, reliable

Triodos Bank. Current Account switch guide About the service The Current Account Switch Service makes switching current accounts to Triodos Bank from another UK bank or building society simple, reliable

/19 TERMS & CONDITIONS Student loans - a guide to terms and conditions

www.studentfinanceni.co.uk 2018 /19 TERMS & CONDITIONS Student loans - a guide to terms and conditions Contents 1 What s this guide about? 2 2 Your loan contract 2 3 Who does what? 3 4 Your responsibilities

www.studentfinanceni.co.uk 2018 /19 TERMS & CONDITIONS Student loans - a guide to terms and conditions Contents 1 What s this guide about? 2 2 Your loan contract 2 3 Who does what? 3 4 Your responsibilities

Paying for care and support

Paying for care and support Adult Social Care Hull City Council This handbook is all about paying for social care services in Hull. It tells you about the financial assessment process and explains what

Paying for care and support Adult Social Care Hull City Council This handbook is all about paying for social care services in Hull. It tells you about the financial assessment process and explains what

KEY FEATURES OF LEGAL & GENERAL S PENSION ANNUITY.

PENSION ANNUITIES KEY FEATURES OF LEGAL & GENERAL S PENSION ANNUITY. HELPING YOU MAKE THE RIGHT DECISIONS FOR YOUR FUTURE This is an important document that you should keep in a safe place. 02 KEY FEATURES

PENSION ANNUITIES KEY FEATURES OF LEGAL & GENERAL S PENSION ANNUITY. HELPING YOU MAKE THE RIGHT DECISIONS FOR YOUR FUTURE This is an important document that you should keep in a safe place. 02 KEY FEATURES

payment protection insurance: consumer questionnaire

our ref: By completing the PPI Questionnaire we will have all the information we need to assess your complaint. Don t worry if you can t remember all of the information, or you do not have any paperwork,

our ref: By completing the PPI Questionnaire we will have all the information we need to assess your complaint. Don t worry if you can t remember all of the information, or you do not have any paperwork,

APPLiCAtion for financial ASSiStAnCE

charity number 1106218 APPLiCAtion for financial ASSiStAnCE alternatively apply online via the trust s website www.britishgasenergytrust.org.uk Before completing the application form, please carefully

charity number 1106218 APPLiCAtion for financial ASSiStAnCE alternatively apply online via the trust s website www.britishgasenergytrust.org.uk Before completing the application form, please carefully

Managing your finances (general)

") Managing your finances (general) This Infosheet covers some of the things you may need to think about as a myeloma patient regarding your finances, and resources for further help and advice. A diagnosis

Managing your finances (general) This Infosheet covers some of the things you may need to think about as a myeloma patient regarding your finances, and resources for further help and advice. A diagnosis

MORTGAGE PRODUCT TRANSFER SERVICE

MORTGAGE PRODUCT TRANSFER SERVICE Everything you need to know about using our service WELCOME Thank you for choosing to use our product transfer service. When it comes to renewing a customer s mortgage,

MORTGAGE PRODUCT TRANSFER SERVICE Everything you need to know about using our service WELCOME Thank you for choosing to use our product transfer service. When it comes to renewing a customer s mortgage,

About your application

Savings Business savings Fixed Term Deposit About your application About your application Account name What is the interest rate? Business Fixed Term Deposit You can find the rate in our Fixed Term Deposit

Savings Business savings Fixed Term Deposit About your application About your application Account name What is the interest rate? Business Fixed Term Deposit You can find the rate in our Fixed Term Deposit

Debt recovery. We want to help.

Debt recovery We want to help www.bristolwater.co.uk 1 www.wessexwater.co.uk As a Bristol Water and Wessex Water customer, you are entitled to a high level of service from us and our billing company Bristol

Debt recovery We want to help www.bristolwater.co.uk 1 www.wessexwater.co.uk As a Bristol Water and Wessex Water customer, you are entitled to a high level of service from us and our billing company Bristol

Student loans a guide to terms and conditions

2018/19 Student loans a guide to terms and conditions /SFWales /SF_Wales /SFWFILM 1 What s this guide about? 3 2 Your loan contract 3 3 Who does what? 4 4 Your responsibilities 5 5 Your repayment plan

2018/19 Student loans a guide to terms and conditions /SFWales /SF_Wales /SFWFILM 1 What s this guide about? 3 2 Your loan contract 3 3 Who does what? 4 4 Your responsibilities 5 5 Your repayment plan

KEY FEATURES OF LEGAL & GENERAL S PENSION ANNUITY.

PENSION ANNUITIES KEY FEATURES OF LEGAL & GENERAL S PENSION ANNUITY. HELPING YOU MAKE THE RIGHT DECISIONS FOR YOUR FUTURE This is an important document that you should keep in a safe place. 02 KEY FEATURES

PENSION ANNUITIES KEY FEATURES OF LEGAL & GENERAL S PENSION ANNUITY. HELPING YOU MAKE THE RIGHT DECISIONS FOR YOUR FUTURE This is an important document that you should keep in a safe place. 02 KEY FEATURES

Your guide to being a a trustee trustee. Your role and responsibilities

Your guide to being a a trustee trustee Your role and responsibilities Your guide to being a trustee Introduction You ve been asked to be a trustee. If you haven t done this before, you re probably wondering

Your guide to being a a trustee trustee Your role and responsibilities Your guide to being a trustee Introduction You ve been asked to be a trustee. If you haven t done this before, you re probably wondering

KEY FEATURES OF LEGAL & GENERAL S PENSION ANNUITY.

PENSION ANNUITIES KEY FEATURES OF LEGAL & GENERAL S PENSION ANNUITY. HELPING YOU MAKE THE RIGHT DECISIONS FOR YOUR FUTURE This is an important document that you should keep in a safe place. 02 KEY FEATURES

PENSION ANNUITIES KEY FEATURES OF LEGAL & GENERAL S PENSION ANNUITY. HELPING YOU MAKE THE RIGHT DECISIONS FOR YOUR FUTURE This is an important document that you should keep in a safe place. 02 KEY FEATURES

Single contribution application form

65A59 CORE INVESTMENTS (PERSONAL PENSION) Single contribution application form You ll need to complete this application form if you want to apply a single contribution to your existing Pension Portfolio

65A59 CORE INVESTMENTS (PERSONAL PENSION) Single contribution application form You ll need to complete this application form if you want to apply a single contribution to your existing Pension Portfolio

3 YEAR FIXED TERM DEPOSIT ACCOUNT

3 YEAR FIXED TERM DEPOSIT ACCOUNT Provided by Scottish Widows Bank SUMMARY BOX PLEASE READ THIS SUMMARY BOX BEFORE YOU COMPLETE THE APPLICATION AND THEN KEEP IT FOR YOUR RECORDS. DON T RETURN IT WITH THE

3 YEAR FIXED TERM DEPOSIT ACCOUNT Provided by Scottish Widows Bank SUMMARY BOX PLEASE READ THIS SUMMARY BOX BEFORE YOU COMPLETE THE APPLICATION AND THEN KEEP IT FOR YOUR RECORDS. DON T RETURN IT WITH THE

MBNA customer questionnaire: Payment Protection Insurance. Section A: about you. Our reference:

MBNA customer questionnaire: Payment Protection Insurance Please complete all sections of the questionnaire as fully as possible, so that your complaint can be assessed quickly. We aim to provide a response

MBNA customer questionnaire: Payment Protection Insurance Please complete all sections of the questionnaire as fully as possible, so that your complaint can be assessed quickly. We aim to provide a response

KEY FEATURES OF LEGAL & GENERAL S PENSION ANNUITY.

PENSION ANNUITIES KEY FEATURES OF LEGAL & GENERAL S PENSION ANNUITY. HELPING YOU MAKE THE RIGHT DECISIONS FOR YOUR FUTURE This is an important document that you should keep in a safe place. 02 KEY FEATURES

PENSION ANNUITIES KEY FEATURES OF LEGAL & GENERAL S PENSION ANNUITY. HELPING YOU MAKE THE RIGHT DECISIONS FOR YOUR FUTURE This is an important document that you should keep in a safe place. 02 KEY FEATURES

Combined Home Loan. This document sets out your loan or facility s terms and conditions. Some key information about your loan or facility

Combined Home Loan Terms and Conditions This document sets out your loan or facility s terms and conditions In this document we ve explained the terms and conditions applying to your ANZ Home Loan or ANZ

Combined Home Loan Terms and Conditions This document sets out your loan or facility s terms and conditions In this document we ve explained the terms and conditions applying to your ANZ Home Loan or ANZ

Triodos Bank. Current Account switch guide

Triodos Bank. Current Account switch guide 1 About the service The Current Account Switch Service makes switching current accounts to Triodos Bank from another UK bank or building society simple, reliable

Triodos Bank. Current Account switch guide 1 About the service The Current Account Switch Service makes switching current accounts to Triodos Bank from another UK bank or building society simple, reliable

CAF CHARITABLE LEGACY SERVICE. Making it simple to leave a lasting impression

CAF CHARITABLE LEGACY SERVICE Making it simple to leave a lasting impression Contents This guide explains how we deal with the gifts received through the CAF Charitable Legacy Service so it is important

CAF CHARITABLE LEGACY SERVICE Making it simple to leave a lasting impression Contents This guide explains how we deal with the gifts received through the CAF Charitable Legacy Service so it is important

Frequently Asked Questions (FAQs) Learners

Learners") Frequently Asked Questions (FAQs) Learners Advanced Learner Loans are for learners aged 19 and over studying at Levels 3 to 6. In this document we answer questions you might have. If you need more information

Frequently Asked Questions (FAQs) Learners Advanced Learner Loans are for learners aged 19 and over studying at Levels 3 to 6. In this document we answer questions you might have. If you need more information

Universal Credit. everything you need to know. Guide for people living in Supported Accommodation

Universal Credit everything you need to know Guide for people living in Supported Accommodation Is this the right guide for me? The rules for getting help with your rent under Universal Credit are different

Universal Credit everything you need to know Guide for people living in Supported Accommodation Is this the right guide for me? The rules for getting help with your rent under Universal Credit are different

Please complete: Please note the Contract comprises of the Pre-Contract Information, Terms & Conditions and Letter of Authority

Please complete: GG 1 x Account Details GG 1 x Reasons For Complaint GG A Letter of Authority for each company Q. I don t have any account numbers or documentation, can I still claim? A. Yes! All you need

Please complete: GG 1 x Account Details GG 1 x Reasons For Complaint GG A Letter of Authority for each company Q. I don t have any account numbers or documentation, can I still claim? A. Yes! All you need

WTC 4. Tax Credit Penalties How tax credit enquiries are settled

Tax Credit Penalties How tax credit enquiries are settled 1 of 13 Contents Introduction Why have you sent me this leaflet? 3 What if I claim as part of a couple? 4 What if I have special needs? 4 During

Tax Credit Penalties How tax credit enquiries are settled 1 of 13 Contents Introduction Why have you sent me this leaflet? 3 What if I claim as part of a couple? 4 What if I have special needs? 4 During

Additional contribution application form

65A6 CORE INVESTMENTS (PERSONAL PENSION) Additional application form You ll need to complete this application form to apply an additional to your Pension Portfolio Plan with Royal London. 1 Important information

65A6 CORE INVESTMENTS (PERSONAL PENSION) Additional application form You ll need to complete this application form to apply an additional to your Pension Portfolio Plan with Royal London. 1 Important information

Terms and conditions. Your questions answered

Terms and conditions Your questions answered Your agreement with us is made up of the following: 1. This document it explains how your account operates. 2. Our Rates and fees leaflet we may charge you

Terms and conditions Your questions answered Your agreement with us is made up of the following: 1. This document it explains how your account operates. 2. Our Rates and fees leaflet we may charge you

Important information to help people in mortgage arrears

Important information to help people in mortgage arrears September 2015 Contents Talk to your Lender 3 Explore your Options 4 Contact a Trusted Third Party for Advice - MABS (Money Advice & Budgeting Service)

Important information to help people in mortgage arrears September 2015 Contents Talk to your Lender 3 Explore your Options 4 Contact a Trusted Third Party for Advice - MABS (Money Advice & Budgeting Service)

how to complain Introduction SEPT 2015 STAGE ONE REFEREE APPEAL

how to complain SEPT 2015 GREATER MANCHESTER PENSION FUND Introduction We have produced this factsheet to tell you about the complaints procedure for the Local Government Pension Scheme (LGPS). Briefly,

how to complain SEPT 2015 GREATER MANCHESTER PENSION FUND Introduction We have produced this factsheet to tell you about the complaints procedure for the Local Government Pension Scheme (LGPS). Briefly,

A charity founded over 150 years ago, we re independent so you can be. The information in this factsheet applies to England only.

Carer s Allowance You may not think of yourself as a carer, but if you look after someone else you might qualify for extra money to help meet your costs. This factsheet explains what Carer s Allowance

Carer s Allowance You may not think of yourself as a carer, but if you look after someone else you might qualify for extra money to help meet your costs. This factsheet explains what Carer s Allowance

2017/ 18. Student loansa guide to terms and conditions.

2017/ 18 Student loansa guide to terms and conditions www.studentfinanceni.co.uk Contents 1 What s this guide about? 2 2 Your loan contract 2 3 Who does what? 3 4 Your responsibilities 4 5 Your repayment

2017/ 18 Student loansa guide to terms and conditions www.studentfinanceni.co.uk Contents 1 What s this guide about? 2 2 Your loan contract 2 3 Who does what? 3 4 Your responsibilities 4 5 Your repayment

Taking money from my pension. A guide to taking cash sums and a flexible income from your Legal & General pension pot.

Taking money from my pension A guide to taking cash sums and a flexible income from your Legal & General pension pot. Workplace DC Pensions Contents 3 INTRODUCTION 4 OPTIONS 6 THINGS TO CONSIDER 7 TAX

Taking money from my pension A guide to taking cash sums and a flexible income from your Legal & General pension pot. Workplace DC Pensions Contents 3 INTRODUCTION 4 OPTIONS 6 THINGS TO CONSIDER 7 TAX

BANKRUPTCY. Freephone. FACTSHEET 10 (2018)

") What is Bankruptcy? Freephone 0800 083 8018 1 FACTSHEET 10 (2018) Bankruptcy is a way of dealing with debts that you cannot pay. Whilst you are bankrupt any assets that you have might be used to pay off

What is Bankruptcy? Freephone 0800 083 8018 1 FACTSHEET 10 (2018) Bankruptcy is a way of dealing with debts that you cannot pay. Whilst you are bankrupt any assets that you have might be used to pay off

Money Matters Guide. A guide to setting up and managing a home. Useful information Please keep safe. Tenant Aftercare Guide

Money Matters Guide A guide to setting up and managing a home Useful information Please keep safe Tenant Aftercare Guide Contents Page Setting up the Essentials Who to Tell When You Move In 1 Rent 2 Council

Money Matters Guide A guide to setting up and managing a home Useful information Please keep safe Tenant Aftercare Guide Contents Page Setting up the Essentials Who to Tell When You Move In 1 Rent 2 Council

A charity founded over 150 years ago, we re independent so you can be. The information in this factsheet applies to England only.

Carer s Allowance You may not think of yourself as a carer, but if you look after someone else you might qualify for extra money to help meet your costs. This factsheet explains what Carer s Allowance

Carer s Allowance You may not think of yourself as a carer, but if you look after someone else you might qualify for extra money to help meet your costs. This factsheet explains what Carer s Allowance

Important Information

Important Information Your AA Loan Agreement explained Your proposed AA Loan Agreement is regulated by the Financial Services and Markets Act 2000 and by the Consumer Credit Act 1974, (the Acts ). The

Important Information Your AA Loan Agreement explained Your proposed AA Loan Agreement is regulated by the Financial Services and Markets Act 2000 and by the Consumer Credit Act 1974, (the Acts ). The

The information in this factsheet applies to England only.

Carer s Allowance You may not think of yourself as a carer, but if you look after someone else you might qualify for extra money to help meet your costs. This factsheet explains what Carer s Allowance

Carer s Allowance You may not think of yourself as a carer, but if you look after someone else you might qualify for extra money to help meet your costs. This factsheet explains what Carer s Allowance

Over 50s Life Cover Terms and Conditions

Over 50s Life Cover Terms and Conditions Contents How does my Over 50s Life Cover work?... page 3 How to make a claim... page 5 Making changes... page 7 How to complain... page 9 Cancelling your policy...

Over 50s Life Cover Terms and Conditions Contents How does my Over 50s Life Cover work?... page 3 How to make a claim... page 5 Making changes... page 7 How to complain... page 9 Cancelling your policy...

SIPP a guide to accessing your pension

SIPP a guide to accessing your pension The Financial Conduct Authority is the independent financial services regulator. It requires us, AJ Bell Management Limited, to give you this important information

SIPP a guide to accessing your pension The Financial Conduct Authority is the independent financial services regulator. It requires us, AJ Bell Management Limited, to give you this important information

Terms and conditions for our current accounts

Terms and conditions for our current accounts Your agreement with us is made up of the following: 1. This document it explains the general terms and conditions for your account and how it will operate.

Terms and conditions for our current accounts Your agreement with us is made up of the following: 1. This document it explains the general terms and conditions for your account and how it will operate.

THINGS YOU SHOULD KNOW ABOUT GUARANTEES

THINGS YOU SHOULD KNOW ABOUT GUARANTEES Contact Guarantees...5 1. What is a guarantee?... 5 2. How do I know how much the debtor is borrowing and how the credit charges are worked out?... 5 3. What documents

THINGS YOU SHOULD KNOW ABOUT GUARANTEES Contact Guarantees...5 1. What is a guarantee?... 5 2. How do I know how much the debtor is borrowing and how the credit charges are worked out?... 5 3. What documents

IMPORTANT DOCUMENT PLEASE READ WESLEYAN CAPITAL INVESTMENT BOND

IMPORTANT DOCUMENT PLEASE READ WESLEYAN CAPITAL INVESTMENT BOND FOR POLICIES ISSUED FROM 1 JANUARY 2013 02 Wesleyan Capital Investment Bond KEY FEATURES OF THE CAPITAL INVESTMENT BOND The Financial Conduct

IMPORTANT DOCUMENT PLEASE READ WESLEYAN CAPITAL INVESTMENT BOND FOR POLICIES ISSUED FROM 1 JANUARY 2013 02 Wesleyan Capital Investment Bond KEY FEATURES OF THE CAPITAL INVESTMENT BOND The Financial Conduct

Personal and Private Banking Keeping You Informed

Personal and Private Banking Keeping You Informed 28 November 2008 Keeping you informed: 1. Changes to Terms and Conditions, Fees Leaflet and User Guide for Personal and Private Banking We are making some

Personal and Private Banking Keeping You Informed 28 November 2008 Keeping you informed: 1. Changes to Terms and Conditions, Fees Leaflet and User Guide for Personal and Private Banking We are making some