MODULE 5 GROUP ACCOUNTS AND BUSINESS COMBINATIONS

|

|

|

- Patience Lyons

- 6 years ago

- Views:

Transcription

1 MODULE 5 GROUP ACCOUNTS AND BUSINESS COMBINATIONS

2 Outlines Consolidated statements of financial position, consolidated statements of profit or loss and other comprehensive income, including reserve reconciliations Consolidated statements of cash flow Acquisition and disposal of subsidiaries and associates (both domestic and overseas) during the year. Takeover of partnership and sole traders.

3 Consolidated Balance Sheet Group balance sheet is to combine the information in the balance sheet of the holding company and that of the subsidiary with such adjustments as the directors of the holding company think necessary. Terminologies Before going into details let us consider some of the terminologies that we will be using in relation to the consolidation schedule under the purchase or acquisition method. 1. Cost of Acquisition: - This is the amount paid by the holding company to acquire the shares in the subsidiary and may consist of partly cash, shares, loan stock or debenture. 2. Pre-Acquisition Reserve: - This is the reserve of the subsidiary existing at the date of acquisition of controlling interest by the holding company. 3. Post-Acquisition Reserve: - Is the reserve of the subsidiary generated by it subsequent to the date of acquisition of controlling interest by the holding company.

4 Consolidated Balance Sheet 4) Net Asset: - From the consolidation schedule point of view, it refers to share capital and reserves of the subsidiary at any time. Net assets at the date of acquisition represent the subsidiary s share capital and the pre-acquisition reserve. 5) Goodwill on Consolidation: - This is the difference in consolidation arising when the cost of acquisition paid by the holding company for the shares acquired in the subsidiary is more than the acquired net asset of the subsidiary. Acquired net asset of the subsidiary represents the holding company s share of the net asset of the subsidiary existing at the date of acquisition. 6) Capital Reserve on Consolidation: - This is the difference in consolidation arising when the cost of acquisition paid by the holding company for the shares acquired in the subsidiary is less than the acquired net asset of that company. 7) Minority Interest: - This is the net asset of the subsidiary attributable to interest which is not owned directly or indirectly through subsidiaries by the holding company.

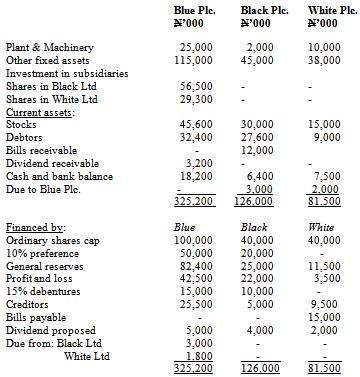

5 Illustration

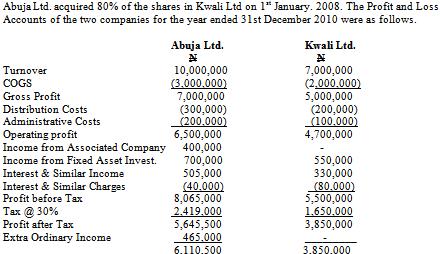

6 Additional Information: 1. Blue Plc. Acquired its 80% interest in Black Plc. when the general reserve and profit and loss account were N15,000,000 and N10,000,000 respectively and its 75% interest in White ltd when the general reserve balance was N5,000,000 and a debit balance of N4,500,000 in the profit and loss account. 2. During the year Blue Plc. transferred a plant costing N2,000,000 to White Ltd at N3,000, Included in the stock of Black Plc. were goods worth N6,000,000 purchased from Blue Plc. It is the policy of Blue Plc. to invoice goods at cost plus 25%. 4. An amount of N200,000 remitted from White Ltd to Blue plc. is still in transit at year end. 5. Part of the bills receivable accepted from White Ltd has been discounted by Black Ltd. 6. Blue Plc. is yet to accrue for its dividend receivable from White Ltd. 7. All the preference shares in Black Ltd are held outside the group. 8. It is group s policy to account for its shares of inters company profits. All shares are denominated in N1 per shares par value. Required: Prepare the Consolidated Balance sheet of Blue group as at 31 st March 2002 show all relevant workings. Ignore adjustments for excess depreciation arising to transfer of plant.

7

8 Workings: 1. Unrealized profit on Plant: N Transfer price of plant 3,000,000 Less: cost of plant (2,000,000) Unrealized profit 1,000, Unrealized profit on stock: Cost + 25 cost = 6,000, cost + 25 cost = 6,000, cost = 600,000,000 Cost = 600,000,000 = N4,800, Unrealized profit = N6,000,000 N4,800,000 = N1,200, Items on Transit: Due to Blue Plc. Black Ltd White Ltd N3,000,000 N2,000,000 N5,000,000

9 Due from: Black Ltd 3,000,000 White Ltd 1,800,000 N4,800,000 Cash in transit N 200,000 Accounting Entry: Dr. Consolidated cash and bank Cr. Due from Black and White Ltd Dividend Receivable from White Ltd 4. Dividend of White Ltd N2,000,000 75% thereof N1,500,000 Accounting Entries: Dr. Dividend receivable Cr. Consolidated profit and Loss

10

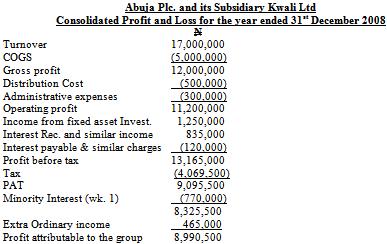

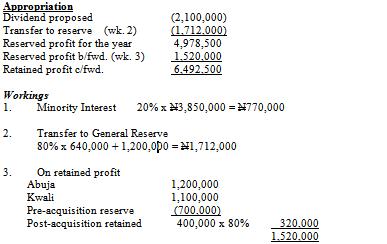

11 Consolidated Profit and Loss Group Profit and Loss Account is to combine the information in the accounts of the holding company and that of the subsidiary with such adjustments as the directors of the holding company think necessary.

12 Illustration

13

14 Solution

15

16 Reorganization of Business Capital Reconstruction (External) The external means of reorganizing the affairs of a company is through amalgamation. Amalgamation is a business combination where in two or more companies come together to form one. This involves the formation of a new company with a different capital structure to salvage the assets of the existing company, which is then wound up. Illustration Below are the balance sheets of Kotan Ltd. and Gora Ltd as at 31 st December, Kotan Ltd. Gora Ltd. Fixed assets: N N Land & Building 3,000,000 2,000,000 M/ vehicle 2,500,000 1,800,000 Furniture 1,500,000 1,200,000 Current assets: Stock 900, ,000 Debtor 100,000 80,000 Bank 1,400,000 1,020,000 9,400,000 6,900,000

17 Financed by: Ordinary share of N2 each 6,000,000 3,000,000 6% preference shares of N1 each 1,200,000 1,000,000 7% debentures 800, ,000 Share premium 400, ,000 General reserves 300,000 1,300,000 Liabilities 700, ,000 9,400,000 6,900,000 On the 1st January 2008, in order to take advantage of the synergy effects of merger, Kotan Ltd and Gora Ltd agreed to merge and form a new company to be known as KotanGora International on the following terms:- 1. The Ordinary shareholders in Kotan Ltd are to receive 8,000,000 ordinary shares of N2 each at N3 in KotanGora International, while the ordinary shareholders of Gora Ltd are to receive 2,000,000 ordinary shares of N2 each in KotanGora International.

18 2. Liquidation expenses is as follows: - Kotan Ltd N80,000 - Gora Ltd N70, The assets of Kotan Ltd. & Gora Ltd are to be taken over by the new company at their book value in addition to any balance in their bank account. 4. The preference shareholders of Kotan Ltd are to receive 900,000 8% preference shares in KotanGora International at the existing book value per shares. The preference shareholders of Gora Ltd are to be given 9% preference shares equal to 110% of their total preference shares in Gora Ltd. 5. The debenture holders in Kotan Ltd & Gora Ltd. are to receive 9,000units and 4,000units of debentures in KotanGora Ltd at par, de-nominated at 8% respectively. 6. The liabilities of the two companies are to be settled in full after deducting 5% discount. Required: 1. Open relevant ledgers to close the book of Kotan Ltd and Gora Ltd. 2. Show the books in the new company i.e. KotanGora International.

19 Solution

20

21

22

23 Valuation of Business/Shares Valuation of business is the determination of the worth, price or cost of a business/shares. A business valuation exercise could be carried out in the following circumstances: a) Take-over bid b)unquoted companies going public c) A scheme of merger d)sale of shares e) Shares being pledged as collateral for a loan by unquoted companies etc. Methods of Valuation i. Net Asset Basis ii. Realizable Value Method iii.replacement Value Method

24 Valuation of Business/Shares Methods of Valuation cont iv. Earnings Basis Method - ARR approach - P/E ratio approach v. Dividend Yield Basis vi. Share Price Basis vii. Berliner Method viii. Super Profit Method ix. Capital Asset Pricing Model Method x. Discounted Future Profit Method In valuing shares (i.e. determining share prices), three theories are utilized: Traditional Theory Chartist Theory Random Walk Theory

25 Illustration

26

27 Illustration 2 A professional valuer estimated the current market value of the freehold property at N64,000 the plant and machinery can be considered as fairly valued at the net book figures. The debentures are secured by a fixed charge. The directors have initiated that it will be their policy for the foreseeable future to retain 75% of the available profits. Above was a balance sheet prepared by the Auditor of NCA Plc. as at 31 st August, You are required to Compute a value for the 30% holdings in the ordinary shares of the company using the methods you explained in (a) above. Assume Company Income Tax to be 50%

28

29

30 Merger Accounting Merger Accounting (Uniting of interests or Pooling of Interest method) is a business combination in which the shareholders of the combining enterprises combine control over the whole of their net assets and operations to achieve a continuing mutual sharing in the risks and benefit attaching to the combined enterprise such that neither party can be identified as the acquirer. Conditions for Adopting Pooling of Interest Method In applying the pooling of interest method: 1. The substantial majority, if not all, of the voting equity shares of the combining enterprises are pooled or exchanged. 2. The fair value of one enterprise is not significantly different from that of the other enterprises. 3. The shareholders of each enterprise maintain substantially the same voting rights and interest in the combined entity, relative to each other, offer the combination as before. 4. It must not be possible to identify an acquirer, that is, the shareholders or managers of one company should not dominate the combined business.

31 The Companies and Allied Matters Act 1990 also provides that: at least 90% of the nominal value of the relevant shares in the company acquired is held by the acquirer. not less than 90% of the fair value of the total consideration given for the equity share capital is in form of equity share capital. Illustration On 1 January, 2008, Dennis Plc. acquired the whole of the ordinary shares of Ahmed Plc. The shareholders of Ahmed Plc. received one share of Dennis Plc. in exchange for one share in Ahmed Plc. The price of the ordinary shares of Dennis Plc. on 1 st January 2008 was N3.50. The fair value of the fixed assets of Ahmed Plc. on 31 December, 2007 was N10,800,000. The summarized balance sheets of the two companies at 31 st December 2003 are as follows:

32 Solution

33

34

35 Workings Note: The reserves of Ahmed Plc. are not consolidated under acquisition because they are all pre-acquisition.

36 Dissolution Of Partnership It is a common saying that everything with a beginning must have an end. It is in recognition of this that the duration of the partnership is usually stated in the Deed of Partnership. Many factors can lead to the dissolution of partnership. Reasons for Dissolution 1. Expiration of the time fixed in the Deed of Partnership for the existence of the partnership 2. Where a court of law ordered the dissolution of the partnership following litigation from one of the partners, creditors or any other interest groups 3. The bankruptcy of one of the partners may lead to liquidation 4. The death or retirement of a partner 5. Where one partner gives notice to the other on his intention to dissolve the partnership 6. The business is consistently running at a loss 7. Where the partnership is converted to a limited liability company to replace the existing partnership. In such cases the partners take shares in the new company equivalent to his capital in the partnership business For whatever reason, the dissolution of the partnership is synonymous with liquidation. The principles of liquidation apply in the dissolution of partnership. On the dissolution of partnership the entire assets of the company are sold.

37 Legal Framework for Dissolution The legal procedure is that all amounts realized from the sale of the assets of the partnership will be used to offset the liabilities of the partnership in the following sequence. 1. Outside creditors: In partnership dissolution the amount realized from the asset will be used to discharge the creditors. Where this is not enough, the personal property of individual ordinary partners will be sold to offset the debt 2. If there is any balance after settling the outside creditors, the loan made by the partner to the business will be redeemed 3. If there is any balance after that, then the partners capital will be paid 4. Any balance remaining in form of profit will be distributed to the partners in their profit sharing ratios. Accounting Framework for Dissolution In dissolving partnership business, accurate bookkeeping is maintained. The following accounting entries will be necessary to be adhered to: Transfer all balances in the current account for each partner to his capital account. With this step, Current Account ceases to exist. Keep a separate account for all the loan made by the partners to the business Open Realization Account Dr: Realization Account with the Book value of the assets (except cash) Cr: The individual asset account. With this entry, the Asset Account is closed.

38 When any asset is sold: Dr: Bank or cash with the value of sales Cr: Realization Account with the sales value If any partner is allowed to take over any Asset Dr: The Partner s Capital Account Cr: Realization Account with the agreed value Costs or expenses incurred in the dissolution process Dr: Realization Account Cr: Bank or Cash Where a partner incurred cost or expenses to assist in the dissolution Dr: Realization Account Cr: Partners Capital Account Where creditors are paid off Dr: Creditors Account Cr: Realization Account (Bank or Cash) Where a Discount is received from creditors Dr: Creditors Account Cr: Realization Account (Bank or Cash) Where any loan to a partner is settled Dr: Partners loan Accounts Cr: Bank or Cash

39 Illustration

40

41 Solution

42

43

44 Bankruptcy Of Partnership Where partnerships are declared bankrupt, the same statement of affairs and deficiency account are prepared as in individuals. However, separate Statement of affairs and Deficiency Accounts will be prepared for the firm and for the partners individually. For example, if there are three partners in a firm of partnership, upon bankruptcy of such partnership, four (4) Statements of affairs and Deficiency accounts will be prepared (i.e. one for the firm and one each for three partners). Other matters to be considered are as follows: 1. Where a partner guarantees the firm s liability with his asset, the realizable value of the asset will be used to reduce the creditor s liability with the firm. Any balance will be ranked. 2. Any surplus form the Statement of Affairs of the partner(s) is transferred to the firm 3. If any surplus still exists in the firm s estate after paying all the creditors, it will be shared amongst the partners in their profit sharing ratio.

45 Illustration Aju and Ayu are in partnership trading under Abuja. The financial position of the firm prior to the petition against her is as follows: Book Value (N) Estimated to Realize (N) ASSETS Freehold Property: Abuja firm 11,000 12,000 Aju: 7,000 8,500 Plant and Machinery: Abuja firm 3,000 1,000 Furniture and Fittings: Abuja firm 1, Aju: 1, Ayu: 1,800 1,100 Stock In Trade: Abuja firm 8,000 5,900 Trade Debtors: Abuja firm 12,000 Investment: Aju 1,500 1,300 Ayu 2,000 1,800

46 LIABILITIES: N Mortgage on Freehold property: Abuja firm 6,000 Aju: 5,000 Bank Overdraft Abuja firm 7,000 Sundry Creditors Abuja firm 20,000 Aju: 1,000 Ayu: 3,000 Of the sundry creditors N1,100 of the firms are preferential while N300 and N500 are preferential for Aju and Ayu respectively. Of the Trade Debtors, N5,000 are estimated to be good and N1,000 bad. Of the remaining debts, about 50% are expected to be paid. The firm s bank overdraft is secured: i. by a second mortgage on the firm s premises ii. by the deposits of Aju s private investment and his personal guarantee. A petition was lodged against the firm on 31 st December, Required: Prepare the Statement of Affairs and Deficiency account for the firm and the partners separate estates.

47 Solution

48

49

2. Dr. Realization a/c Cr.")

3. Dr. Purchase Consideration a/c Cr. Realization a/c (with the purchase consideration as calculated) 4. Dr. Liabilities and Expenses a/c (with the liabilities and expenses taken Cr.")

7. Dr. Liabilities a/c Cr. Bank/Cash a/c (with any liability paid off by the partnership firm) Cr.")

50 Conversion of Partnerships to Companies Accounting Entries 1. Dr. Realization a/c Cr. Assets a/c (with the book value of each asset to be realized and taken over except Bank/Cash balance if not taken) 2. Dr. Realization a/c Cr. Cash/Bank a/c (with dissolution expenses paid by the partnership) Cr. Partners Capital a/c (with the part paid by the partners) Cr. Realization a/c (with the part paid by the new company) 3. Dr. Purchase Consideration a/c Cr. Realization a/c (with the purchase consideration as calculated) 4. Dr. Liabilities and Expenses a/c (with the liabilities and expenses taken Cr. Partner s Cap a/c over which is not part of Purchase consideration) 5. Dr. Cash/Bank a/c Cr. Realization a/c (with proceeds on realization of assets not taken over) 6. Dr. Partners Capital a/c Cr. Realization a/c (with value of assets taken over by partners) 7. Dr. Liabilities a/c Cr. Bank/Cash a/c (with any liability paid off by the partnership firm) Cr. Partners Capital a/c (with the part paid by the partners) Cr. Realization a/c (with the discount received)

51 8. a) Dr. Partners Current a/c Cr. Partners Capital a/c (with the credit balance in the Current a/c) b) Dr. Partners Capital a/c Cr. Partners Current a/c (with the debit balance in the current a/c) 9. a) Dr. Realization a/c Cr. Partners Capital a/c (with the distribution of profit in realization on the basis of their profit sharing ratio) b) Dr. Partners Capital a/c Cr. Realization a/c (with any loss on realization) 10. Dr. Cash/Bank a/c (with the cash payment on take-over) Dr. Securities e.g. Ord. Shares, Pref. Shares, Debenture (with the securities issued by the company) Cr. Purchase Consideration New Firm 11. Dr. Partners Capital a/c Cr. Securities a/c (with the agreed share of the securities among the partners) 12. a) Dr. Bank/Cash a/c Cr. Partners Capital a/c (with any cash introduced) b) Dr. Partners Capital a/c Cr. Bank a/c (with any amount due to them)

of the Partnership as 31 st December 2007 is as follows: Additional Information is relevant: On 1 st January 2008, the Partnership agreed to convert")

52 Illustration Ade, Leye and Jola have been in partnership business sharing profit and loss in the ratio 3:2:3. The Financial Statement (Balance Sheet) of the Partnership as 31 st December 2007 is as follows: Additional Information is relevant: On 1 st January 2008, the Partnership agreed to convert partnership into limited liability known as Jolede Ltd. with an Authorized Share Capital of 10,000,000 shares of N1 each.

53 The terms of the conversion is as follows: all the assets are to be taken over at their book value by the new company except bank/cash. After conversion the company is to revalue the following assets: a. Land and Building N4,500,000 b. Furniture N 920,000 Loan is to be settled in full by the partnership while creditors agreed for 50% discount. Dissolution Expenses N80,000 The company is to issue the following securities to compensate the partners for the asset taken over: 4,000,000 Ordinary Shares of N1 each; 8% Debenture amounting to N3,000,000. These securities are to be shared among the partners in the ratio of their capital contribution. Required: 1. Prepare relevant ledgers to close the book of the partnership. 2. Prepare the balance sheet of the new company Jolede immediately after conversion.

54 Solution

55

56

57 Bankruptcy of Sole Trader Bankruptcy proceedings are guided by the Bankruptcy Act of Bankruptcy is a proceeding initiated by a creditor or group of creditors in the Federal High Court seeking the assistance of the court in declaring the debtor bankrupt. Bankruptcy situation can be conferred on oneself or by a creditor. Debtors who are unable to meet their financial obligations, partnerships, married women, unmarried women, the estate of the deceased debtors, infants (in respect of necessaries or in respect of taxation) can be declared bankrupt except companies, lunatics, foreigners, deceased debtors. Acts of Bankruptcy Before a person can be declared bankrupt, it is necessary that he shall have committed an act of bankruptcy which is classified thus: a conveyance or assignment of all the debtor s property to a trustee for the benefit of his creditors generally a conveyance of any property of any person with the intention of deceiving or delaying creditors. A fraudulent preference.

58 Where a debtor departs his dwelling house (absent himself) If execution is levied, and the goods, having been seized by the bailiff, are sold or held for 21 days. Where a debtor files with the court a declaration of inability to pay his debts If the debtor fails to comply with bankruptcy notice. If the debtor give notice to any of his creditors that he has suspended, or is about to suspend payment of his debts. Conditions for a valid petition The debt owing by the debtor to the petitioning creditor(s) must not be less than N2,000. The debt is a liquidated sum, payable either immediately or at some certain future times. The act of bankruptcy on which the petition is based has occurred within three months of the presentation of the petition. If the petitioning creditor holds any security i.e. a secured creditor, he shall state in his petition either that he is willing to give up his security for the benefit of all creditors in the event of the debtor being adjudged bankrupt, or give an estimate of the value of his security. The debtor must ordinarily be a resident in Nigeria, or must have been so resident within a period not less than 12 months.

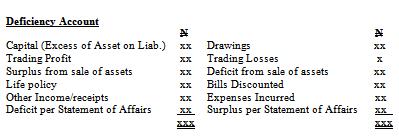

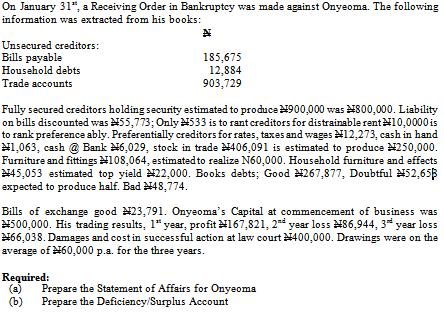

59 Accounting Statements: Bankruptcy Accounts involves the preparation of the Statement of Affairs of the debtor and to properly account and report on the activities of the trustee in the administration of the bankrupt s affairs. Statement of Affairs: is like the Balance Sheet. It shows the assets and liabilities but the assets are valued at estimated realizable values rather than at their historical costs. The liabilities are classified according to their priority in the settlement of the debts. Deficiency Accounts: explains by means of figures how the deficiency or surplus in the Statement of Affairs is arrived at.

60

61

62 Illustration

63 Solution

64

65 Review Questions 1) Ade and Jola have been in Partnership business sharing profit and loss in the ratio 1:2 for the past five years. The latest balance of the Balance Sheet as at 31 st Dec is as follows:

66 i. On 1 st January 2009, they agreed to admit Obalola as a partner on the following terms: Obalola is to introduce Capital of N3,000,000. ii. The Partner is to introduce goodwill at a value of N1,500,000 which is to be shown in the books. iii. The following assets are to be revalued: Land and Building N3,200,000 Furniture N 580,000 Motor Vehicle N3,000,000 iv. 20% is to be written off as bad debt. v. Stock - N310,000. vi. The new sharing profit ratio should be in their capital contribution. Required: a) As a Professional Accountant of ANAN, carry out all relevant entries to record the above transaction. b) Prepare a Realized Balance Sheet after the admission of Obalola Ltd.

67 2) Adebayo and Adejola are in partnership sharing profits and losses in the ratio 3:2. Their partnership agreement also provided that interest on capital shall be 10% per annum, that Adebayo shall receive N6,000 and Adejola N5,000 as salaries. The following lists of balances are extracted from their books as at 31 st December 2005.

68 You are required to prepare: a. A Trading, Profit and Loss Account for the year ended 31 st December b. Balance sheet as at that date.

69 3) Immediately prior to its conversion into a Limited Company, the Balance Sheet of Kings and Jude, who shared profits and losses 3/5 and 2/5, disclosed.

70

71 5) EZENWUGO and CHINWE Limited decided to issue 400,000 N1 Ordinary Shares at N1.20 each. The terms of issue are 30k on application, 45k (including the premium) on allotment, 20k to be called one month after allotment, with the final call of 25k being made four months after allotment. On December 29 th Applications were received for 60,000 shares. On 1 st January, the shares were allotted so that every applicant received two thirds of the number of shares applied for. Excess application monies were held against the amount due on allotment. On January 4 th the cash due on allotment was received. February 1 st, the first call was made and February 3 rd the cash was received. On May 1, the second call was made and cash was received. Required: Make the necessary Journal and Ledger entries to record these transactions. 6) JIRE and NISSI Limited advertised an issue of 750,000 12% Preference Shares of N1 each to be issued at N1.50 per share. Application for 1,370,000 shares were received with the correct application money of 30k per share, 70k per share (including premium) was due on allotment while 25k per share was due on each of the remaining two calls. All amounts due were received. Application money for 120,000 shares was refunded to unsuccessful applicants and the remaining applicants were allotted shares on a pro-rata basis.

72 You are required to: 1. Open all necessary ledger accounts and post the above transactions 2. Calculate the number of shares issued to Peter, James and John who applied for 275,000, 180,000 and 50,000 shares respectively and were among the successful applicants. 7) Olabode Limited issued N200,000 9% debentures at 110 on January, The terms under which the debentures were issued provided that a sinking fund be set up for the redemption of the debentures 5 years later. The sum to be set aside every year should be such that when invested annually at a compound interest rate of 15% per annum will amount to N240,000 at the due date of redemption of the debentures. Interest is paid on the debentures on 31 st March and 30 th September, every year. The debentures were redeemed on 31 st December, 2004 at a premium of 12%. To provide cash for the redemption, the sinking fund investment was sold for N220,000. You are required to show the following Accounts: 9% Debentures A/c, Sinking Fund A/c, Sinking Fund Investment A/c, Redemption A/c, Sinking Fund Investment Disposal A/c

73 8) Kwall Ltd. has a capital base of N5,000,000 (shares of N100 each) as at 31 st December The company s profit after tax for the same year stood at N700,000. Assume the market value of the company s value was N400 each and a dividend of 4% was declared for the year to 31/12/2003. Determine the following in respect of the company; i. Market value of the company s ordinary shares ii. Price Earnings Ratio iii. Earnings per share iv. Dividend yield v. Value of the retained profit 9) The following information was extracted from the balance sheet of a new company on the Second Tier Securities Market (Cash n Carry Plc.) Total fixed Assets 10,000,000 Closing stock 1,000,000 The financial analyst interested in investing in the company compiled the following ratios in respect of the company: Gross Margin 25% Net profit/sales 20% Stock Turnover ratio 10% Net profit/capital 20% Closing capital to total liabilities 50% Fixed assets to capital 5.4 Fixed Assets to total current assets 5.7 Required: Prepare Trading, Profit and Loss Account and a Balance Sheet of Cash n Carry Plc. for the Year ended 31 st December 2003.

74 References Adejola, P. A (2010): Revision Pack on Advanced Corporate Reporting for Professionals, Conversion and Undergraduate Students, Danladi Press, Abuja. Adejola, P. A., Financial Accounting and Reporting Standards for Students and Professionals, Revised Edition (2011) Aborode, R. Advanced Financial Accounting, Lagos: Masterstroke Consulting Okwoli, A. A., Principles of Financial Accounting, 3 rd Edition, Jos: Gogo International Ltd.

INTERNAL RECONSTRUCTION

5 INTERNAL RECONSTRUCTION Learning Objectives After studying this chapter, you will be able to: Understand the meaning of term reconstruction. Sub-divide and consolidate shares. Convert shares into stock

5 INTERNAL RECONSTRUCTION Learning Objectives After studying this chapter, you will be able to: Understand the meaning of term reconstruction. Sub-divide and consolidate shares. Convert shares into stock

6 Amalgamation. 1. Meaning of Amalgamation. Learning Objectives. After studying this chapter, you will be able to

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

6 Amalgamation. 1. Meaning of Amalgamation. Learning Objectives. After studying this chapter, you will be able to

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

Internal Reconstruction

5 Internal Reconstruction Learning Objectives After studying this chapter, you will be able to: Understand the meaning of term reconstruction. Sub-divide and consolidate shares. Convert shares into stock

5 Internal Reconstruction Learning Objectives After studying this chapter, you will be able to: Understand the meaning of term reconstruction. Sub-divide and consolidate shares. Convert shares into stock

PARTNERSHIP ACCOUNTS

CHAPTER-2 Q. 1. Thin, Short and Fat were in partnership sharing profits and losses in the ratio of 2 : 2 : 1. On 30th September, 2012 their Balance Sheet was as follows : Capital Accounts : Premises 50,000

CHAPTER-2 Q. 1. Thin, Short and Fat were in partnership sharing profits and losses in the ratio of 2 : 2 : 1. On 30th September, 2012 their Balance Sheet was as follows : Capital Accounts : Premises 50,000

6 Amalgamation of Companies

6 Amalgamation of Companies Learning Objectives After studying this chapter, you will be able to: Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept

6 Amalgamation of Companies Learning Objectives After studying this chapter, you will be able to: Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept

FANLING LUTHERAN SECONDARY SCHOOL

FANLING LUTHERAN SECONDARY SCHOOL 2012 2013 2 nd Term Examination S.5 BUSINESS, ACCOUNTING AND FINANCIAL STUDIES Accounting Module Date : 20th June, 2013 Time allowed: 8:30 am - 11:00 am (2 hour 30 minutes)

FANLING LUTHERAN SECONDARY SCHOOL 2012 2013 2 nd Term Examination S.5 BUSINESS, ACCOUNTING AND FINANCIAL STUDIES Accounting Module Date : 20th June, 2013 Time allowed: 8:30 am - 11:00 am (2 hour 30 minutes)

3 Advanced Issues in Partnership Accounts

3 Advanced Issues in Partnership Accounts Unit 1: Dissolution of firms Question 1 X and Y carrying on business in partnership sharing Profit and Losses equally, wished to dissolve the firm and sell the

3 Advanced Issues in Partnership Accounts Unit 1: Dissolution of firms Question 1 X and Y carrying on business in partnership sharing Profit and Losses equally, wished to dissolve the firm and sell the

Pre-Board Exam 01. Accountancy. Class: XII. Q1. What do you mean by drawings against capital and how will you treat it in partnership accounts?

Max. Marks: 80 Instructions: Pre-Board Exam 01 Accountancy Class: XII 1. Question paper consists of 25 questions. 2. All questions are compulsory.. Attempt all parts of a question together.. State question

Max. Marks: 80 Instructions: Pre-Board Exam 01 Accountancy Class: XII 1. Question paper consists of 25 questions. 2. All questions are compulsory.. Attempt all parts of a question together.. State question

UNIT 4 : AMALGAMATION AND RECONSTRUCTION

Company Accounts 3.1 UNIT 4 : AMALGAMATION AND RECONSTRUCTION (A) Write short notes on : Question 1 Amalgamation and Absorption of companies a comparison.(3 marks)(intermediate Nov. 1994) Answer In accounting

Company Accounts 3.1 UNIT 4 : AMALGAMATION AND RECONSTRUCTION (A) Write short notes on : Question 1 Amalgamation and Absorption of companies a comparison.(3 marks)(intermediate Nov. 1994) Answer In accounting

Internal Reconstruction

5 Internal Reconstruction BASIC CONCEPTS Reconstruction is a process by which affairs of a company are reorganized by revaluation of assets, reassessment of liabilities and by writing off the losses already

5 Internal Reconstruction BASIC CONCEPTS Reconstruction is a process by which affairs of a company are reorganized by revaluation of assets, reassessment of liabilities and by writing off the losses already

INTERNAL RECONSTRUCTION

CHAPTER-4 Q. 1. Green Limited had decided to reconstruct the Balance Sheet since it has accumulated huge losses. The following is the summarized Balance Sheet of the Company on 31.3.2012 before reconstruction

CHAPTER-4 Q. 1. Green Limited had decided to reconstruct the Balance Sheet since it has accumulated huge losses. The following is the summarized Balance Sheet of the Company on 31.3.2012 before reconstruction

Time allowed : 3 hours Maximum marks : 100. Total number of questions : 8 Total number of printed pages : 11 PART A

: 1 : RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 11 NOTE : All working notes should be shown distinctly. PART A (Answer Question

: 1 : RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 11 NOTE : All working notes should be shown distinctly. PART A (Answer Question

XII ACCOUNTING REGULAR / PRIVATE. S.Hussain

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

AMALGAMATION, ABSORPTION AND RECONSTRUCTION

CHAPTER-5 AMALGAMATION, ABSORPTION AND RECONSTRUCTION Q. 1. The following is the summarized Balance Sheet of A Ltd. as on 31.3.2012 Liabilities Assets 14,000 Equity shares of Sundry assets 18,00,000 100

CHAPTER-5 AMALGAMATION, ABSORPTION AND RECONSTRUCTION Q. 1. The following is the summarized Balance Sheet of A Ltd. as on 31.3.2012 Liabilities Assets 14,000 Equity shares of Sundry assets 18,00,000 100

UNIT - 1: DISSOLUTION OF PARTNERSHIP FIRMS. Go through the circumstances in which a partnership is dissolved.

CHAPTER 15 PARTNERSHIP ACCOUNTS UNIT - 1: DISSOLUTION OF PARTNERSHIP FIRMS LEARNING OUTCOMES After studying this chapter, you will be able to r r r r Go through the circumstances in which a partnership

CHAPTER 15 PARTNERSHIP ACCOUNTS UNIT - 1: DISSOLUTION OF PARTNERSHIP FIRMS LEARNING OUTCOMES After studying this chapter, you will be able to r r r r Go through the circumstances in which a partnership

Pre-Board Exam 02. Accountancy. Class : XII

Pre-Board Exam 02 Accountancy Class : XII Max. Marks: 80 Duration : hours Instructions:. Question paper consists of 25 questions. 2. All questions are compulsory.. Attempt all parts of a question together..

Pre-Board Exam 02 Accountancy Class : XII Max. Marks: 80 Duration : hours Instructions:. Question paper consists of 25 questions. 2. All questions are compulsory.. Attempt all parts of a question together..

cum interest. Journalise the transaction. (iv) Swaminathan owed to Subramanium the following sums :

Swaminathan owed to Subramanium the following sums :") Question 1 (i) (ii) PAPER 1 : ACCOUNTING Answer all questions Wherever appropriate, suitable assumption(s) should be made by the candidates. Working notes should form part of the answer A and B are partners

Question 1 (i) (ii) PAPER 1 : ACCOUNTING Answer all questions Wherever appropriate, suitable assumption(s) should be made by the candidates. Working notes should form part of the answer A and B are partners

Certificate in Book-keeping and Accounts

Certificate in Book-keeping and Accounts ASE2007 Level 2 Monday 8 April 2013 Time allowed: 3 hours Information There are 5 questions in this question paper. All questions carry equal marks. Instructions

Certificate in Book-keeping and Accounts ASE2007 Level 2 Monday 8 April 2013 Time allowed: 3 hours Information There are 5 questions in this question paper. All questions carry equal marks. Instructions

XII ACCOUNTING REGULAR / PRIVATE. S.Hussain

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

Revisionary Test Paper_Final_Syllabus 2008_Dec2013

Question No.1(a) Paper 16 Advanced Financial Accounting & Reporting What is 'discontinuing operations' as per AS-24? Answer: As per Para 3 of the standard, a discontinuing operation is a component of an

Question No.1(a) Paper 16 Advanced Financial Accounting & Reporting What is 'discontinuing operations' as per AS-24? Answer: As per Para 3 of the standard, a discontinuing operation is a component of an

QUESTION BANK ( ) Class XII Subject:- ACCOUNTANCY

Class XII Subject:- ACCOUNTANCY") QUESTION BANK (2017-2018) Class XII Subject:- ACCOUNTANCY 1. Give any one rule in absence of partnership deed. 1 2. Write two items of debit side of partner s current Accounts. 1 3. Mention two items that

QUESTION BANK (2017-2018) Class XII Subject:- ACCOUNTANCY 1. Give any one rule in absence of partnership deed. 1 2. Write two items of debit side of partner s current Accounts. 1 3. Mention two items that

MTP_Intermediate_Syllabus 2016_Dec 2017_Set 2 Paper 5- Financial Accounting

Paper 5- Financial Accounting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 5- Financial Accounting Full Marks : 100 Time allowed:

Paper 5- Financial Accounting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 5- Financial Accounting Full Marks : 100 Time allowed:

Accountancy Class-XII Assignment

Chapter 1 Accounting For fundamentals Accountancy Class-XII Assignment 2017-18 Q1. Lata and Mamta are partners with capital of Rs. 3,00,000 and Rs. 2,00,000 respectively sharing profits as Lata 70% and

Chapter 1 Accounting For fundamentals Accountancy Class-XII Assignment 2017-18 Q1. Lata and Mamta are partners with capital of Rs. 3,00,000 and Rs. 2,00,000 respectively sharing profits as Lata 70% and

ACCOUNTANCY CLASS XII DESIGN OF THE QUESTION PAPER. Times : 3Hours Maximum Marks 80 S. NO. OBJECTIVES MARKS % OF MARKS. 1.

78 ACCOUNTANCY CLASS XII DESIGN OF THE QUESTION PAPER Times : 3Hours Maximum Marks 80 1. Weightage of Objectives S. NO. OBJECTIVES MARKS % OF MARKS 1. Knowledge 16 20% 2. Understanding 56 70% 3. Application

78 ACCOUNTANCY CLASS XII DESIGN OF THE QUESTION PAPER Times : 3Hours Maximum Marks 80 1. Weightage of Objectives S. NO. OBJECTIVES MARKS % OF MARKS 1. Knowledge 16 20% 2. Understanding 56 70% 3. Application

THE TOUGHER YOU PLAY THE HIGHER YOU RISE! 10+2 (Accounts)Test 02 ( 2014) M.Marks : 80

Test 02 ( 2014) M.Marks : 80") PART-A Q.1 Would a charitable dispensary run by 8 members be deemed a partnership firm? Give reason in support of your answer. (1) Q.2 Can a partner be exempted from sharing the losses in a firm? If yes,

PART-A Q.1 Would a charitable dispensary run by 8 members be deemed a partnership firm? Give reason in support of your answer. (1) Q.2 Can a partner be exempted from sharing the losses in a firm? If yes,

PAPER 1 : ACCOUNTING QUESTIONS

PAPER 1 : ACCOUNTING QUESTIONS Profit or Loss Prior to Incorporation 1. A firm which was carrying on business from 1 st January, 2009 gets itself incorporated as a company on 1st May, 2009. The first accounts

PAPER 1 : ACCOUNTING QUESTIONS Profit or Loss Prior to Incorporation 1. A firm which was carrying on business from 1 st January, 2009 gets itself incorporated as a company on 1st May, 2009. The first accounts

ACCOUNTS (858) CLASS XI

CLASS XI") ACCOUNTS (858) Aims: 1. To provide an understanding of the principles of accounts and practice in recording transactions and interpreting individual as well as company accounts. 2. To develop an understanding

ACCOUNTS (858) Aims: 1. To provide an understanding of the principles of accounts and practice in recording transactions and interpreting individual as well as company accounts. 2. To develop an understanding

I.P.C.C. - ACCOUNTANCY

AVERAGE DUE DATE Q. 1. A and B, two partners of a firm, have drawn the following amounts from the firm in the year ending 31st March, 2015: A Date B Date 1 st July 500 12 th June 1,000 30 th September

AVERAGE DUE DATE Q. 1. A and B, two partners of a firm, have drawn the following amounts from the firm in the year ending 31st March, 2015: A Date B Date 1 st July 500 12 th June 1,000 30 th September

SOLUTION: ADVANCED FINANCIAL REPORTING, MAY 2014

SOLUTION 1(a) Goodwill is only calculated when control is gained. In substance, it is like the previously held investment is disposed of and a 70% controlled investment acquired. The previously held investment

SOLUTION 1(a) Goodwill is only calculated when control is gained. In substance, it is like the previously held investment is disposed of and a 70% controlled investment acquired. The previously held investment

Paper-18 : CORPORATE FINANCIAL REPORTING

Paper-18 : CORPORATE FINANCIAL REPORTING 1. (a) Write a note on IFRS. (b) Accounts of R Ltd. show a net profit of `7,20,000 for the third quarter of 2014 after incorporating the following: (i) Bad debts

Paper-18 : CORPORATE FINANCIAL REPORTING 1. (a) Write a note on IFRS. (b) Accounts of R Ltd. show a net profit of `7,20,000 for the third quarter of 2014 after incorporating the following: (i) Bad debts

SUGGESTED SOLUTION CA FINAL MAY 2017 EXAM

SUGGESTED SOLUTION CA FINAL MAY 2017 EXAM FINANCIAL REPORTING Test Code - F M J 4 0 1 5 BRANCH - (MULTIPLE) (Date : ) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel

SUGGESTED SOLUTION CA FINAL MAY 2017 EXAM FINANCIAL REPORTING Test Code - F M J 4 0 1 5 BRANCH - (MULTIPLE) (Date : ) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel

Liabilities Rs. Assets Rs.

MARKING SCHEME SAMPLE QUESTION PAPER -I ACCOUNTANCY Class - XII Set - I Part A Accounting for Not for Profit Organizations, Partnership Firms and Companies 1. Such organisations are formed for providing

MARKING SCHEME SAMPLE QUESTION PAPER -I ACCOUNTANCY Class - XII Set - I Part A Accounting for Not for Profit Organizations, Partnership Firms and Companies 1. Such organisations are formed for providing

Accountancy Set-2 Time allowed: 3 hours Maximum Marks: 90

Accountancy Set-2 Time allowed: 3 hours Maximum Marks: 90 General Instructions: 1) This question paper contains two parts A and B. 2) Part A is compulsory for all. 3) Part B has two options-option-i Analysis

Accountancy Set-2 Time allowed: 3 hours Maximum Marks: 90 General Instructions: 1) This question paper contains two parts A and B. 2) Part A is compulsory for all. 3) Part B has two options-option-i Analysis

The Institute of Chartered Accountants of India

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

` 38,000 in the refurbishment of the premise. These are to be considered as

PAPER 1: FINANCIAL REPORTING Question No.1 is compulsory. Answer any five questions from the remaining six questions. Working notes should form part of the respective answers. Wherever necessary, candidates

PAPER 1: FINANCIAL REPORTING Question No.1 is compulsory. Answer any five questions from the remaining six questions. Working notes should form part of the respective answers. Wherever necessary, candidates

TOPPER SAMPLE PAPER 2

TOPPER Sample Papers 209 TOPPER SAMPLE PAPER 2 ACCOUNTANCY XII Time Allowed - 3 Hrs. Max. Marks - 80 General Instructions:- 1. This question paper contains two parts A & B only. 2. All parts of questions

TOPPER Sample Papers 209 TOPPER SAMPLE PAPER 2 ACCOUNTANCY XII Time Allowed - 3 Hrs. Max. Marks - 80 General Instructions:- 1. This question paper contains two parts A & B only. 2. All parts of questions

ADV. ACCOUNTS MAY QUESTION PAPER

TOPPER S INSTITUTE [IPC-GROUP - II] Adv. Accounts 1 ADV. ACCOUNTS MAY 2017 - QUESTION PAPER Q.1 Answer the following Questions: [4 5 = 20 Marks] Fast Ltd. acquired a patent at a cost of ` 40,00,000 for

TOPPER S INSTITUTE [IPC-GROUP - II] Adv. Accounts 1 ADV. ACCOUNTS MAY 2017 - QUESTION PAPER Q.1 Answer the following Questions: [4 5 = 20 Marks] Fast Ltd. acquired a patent at a cost of ` 40,00,000 for

Answer to MTP_Intermediate_Syllabus2016_June2018_Set 2 Paper 5- Financial Accounting

Paper 5- Financial Accounting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 5- Financial Accounting Full Marks : 100 Time allowed:

Paper 5- Financial Accounting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 5- Financial Accounting Full Marks : 100 Time allowed:

CBSE-XII (2018) CBSE BOARD PAPER WITH SOLUTION ACCOUNTANCY. Candidate must write the Code on the titile page of the answer-book.

CBSE BOARD PAPER WITH SOLUTION ACCOUNTANCY. Candidate must write the Code on the titile page of the answer-book.") CBSE-XII (2018) CBSE BOARD PAPER WITH SOLUTION ACCOUNTANCY Code No. 67/1 Roll.No. Candidate must write the Code on the titile page of the answer-book. Time allowed : 3 hours Maximum Marks : 80 Code number

CBSE-XII (2018) CBSE BOARD PAPER WITH SOLUTION ACCOUNTANCY Code No. 67/1 Roll.No. Candidate must write the Code on the titile page of the answer-book. Time allowed : 3 hours Maximum Marks : 80 Code number

Downloaded from INTERNATIONAL INDIAN SCHOOL-RIYADH

INTERNATIONAL INDIAN SCHOOL-RIYADH ACCOUNTANCY 2014-2015 GRADE 12 WORKSHEET -3 1. A, B are partners sharing profits in the ratio of 5:3.Their balance sheet as on 31 st December 2013 was as follows Balance

INTERNATIONAL INDIAN SCHOOL-RIYADH ACCOUNTANCY 2014-2015 GRADE 12 WORKSHEET -3 1. A, B are partners sharing profits in the ratio of 5:3.Their balance sheet as on 31 st December 2013 was as follows Balance

SHREE GURU KRIPA S INSTITUTE OF MANAGEMENT Guideline Answers for November 2011 Financial Reporting

SHREE GURU KRIPA S INSTITUTE OF MANAGEMENT Guideline Answers for November 2011 Financial Reporting Question No. 1 is Compulsory. Answer any FIVE questions from the remaining SIX questions. Question 1(a)

SHREE GURU KRIPA S INSTITUTE OF MANAGEMENT Guideline Answers for November 2011 Financial Reporting Question No. 1 is Compulsory. Answer any FIVE questions from the remaining SIX questions. Question 1(a)

DESIGN OF THE QUESTION PAPER

DESIGN OF THE QUESTION PAPER SUBJECT : ACCOUNTANCY MAX MARKS : 80 CLASS : XII TIME : 3 HRS. 1. Weightage to Objectives S.NO. OBJECTIVES MARKS % OF MARKS 1. Knowledge 16 20% 2. Understanding 56 70% 3. Application

DESIGN OF THE QUESTION PAPER SUBJECT : ACCOUNTANCY MAX MARKS : 80 CLASS : XII TIME : 3 HRS. 1. Weightage to Objectives S.NO. OBJECTIVES MARKS % OF MARKS 1. Knowledge 16 20% 2. Understanding 56 70% 3. Application

CA - IPCC COURSE MATERIAL

CA - IPCC COURSE MATERIAL Quality Education beyond your imagination... GROUP 2 - GUESS QUESTIONS_34e APPLICABLE FOR MAY 2016 EXAMS INDEX S.No. Chapter Name Starting Page 1. Advanced Accounting 3 2. Auditing

CA - IPCC COURSE MATERIAL Quality Education beyond your imagination... GROUP 2 - GUESS QUESTIONS_34e APPLICABLE FOR MAY 2016 EXAMS INDEX S.No. Chapter Name Starting Page 1. Advanced Accounting 3 2. Auditing

In each case pass the journal entry for goodwill adjustment and analyze the effect on capital of the adjustment.

In each case pass the journal entry for goodwill adjustment and analyze the effect on capital of the adjustment. Example 1: Goodwill adjustment Three partners A, B and C run a partnership business. A has

In each case pass the journal entry for goodwill adjustment and analyze the effect on capital of the adjustment. Example 1: Goodwill adjustment Three partners A, B and C run a partnership business. A has

QUESTION BANK ( ) Class XII Subject:- ACCOUNTANCY

Class XII Subject:- ACCOUNTANCY") QUESTION BANK (2011-2012) Class XII Subject:- ACCOUNTANCY 1. State two characteristics of Not for profit organization. 1 2. Give any one point of difference between a Cash Book and receipts and Payments

QUESTION BANK (2011-2012) Class XII Subject:- ACCOUNTANCY 1. State two characteristics of Not for profit organization. 1 2. Give any one point of difference between a Cash Book and receipts and Payments

ACCOUNTANCY. Std.: XII- Com. (As per new pattern) Time : 3 Hrs. 80. General Instructions:

Time : 3 Hrs. 80. General Instructions:") ACCOUNTANCY Time : 3 Hrs. 80 M.M.: Std.: XII- Com. (As per new pattern) General Instructions: 1. This question paper contains two parts A and B. 2. All parts of a question should be attempted at one place.

ACCOUNTANCY Time : 3 Hrs. 80 M.M.: Std.: XII- Com. (As per new pattern) General Instructions: 1. This question paper contains two parts A and B. 2. All parts of a question should be attempted at one place.

KENDRIYA VIDYALAYA SANGATHAN-KOLKATA REGION 2ND PRE-BOARD EXAMINATION: SUB: ACCOUNTANCY TIME ALLOWED: 3 HOURS M.M :80

KENDRIYA VIDYALAYA SANGATHAN-KOLKATA REGION 2ND PRE-BOARD EXAMINATION: 2014-15 SUB: ACCOUNTANCY TIME ALLOWED: 3 HOURS M.M :80 General Instructions: 1. This question paper contains two parts- A and B. 2.

KENDRIYA VIDYALAYA SANGATHAN-KOLKATA REGION 2ND PRE-BOARD EXAMINATION: 2014-15 SUB: ACCOUNTANCY TIME ALLOWED: 3 HOURS M.M :80 General Instructions: 1. This question paper contains two parts- A and B. 2.

LOYOLA COLLEGE (AUTONOMOUS), CHENNAI B.com. DEGREE EXAMINATION COMMERCE

, CHENNAI B.com. DEGREE EXAMINATION COMMERCE") LOYOLA COLLEGE (AUTONOMOUS), CHENNAI 600 034 B.com. DEGREE EXAMINATION COMMERCE FOURTH SEMESTER NOVEMBER 2013 CO 4502/CO 4500 COMPANY ACCOUNTS Date : 11/11/2013 Dept. No. Max. : 100 Marks Time : 1:00-4:00

LOYOLA COLLEGE (AUTONOMOUS), CHENNAI 600 034 B.com. DEGREE EXAMINATION COMMERCE FOURTH SEMESTER NOVEMBER 2013 CO 4502/CO 4500 COMPANY ACCOUNTS Date : 11/11/2013 Dept. No. Max. : 100 Marks Time : 1:00-4:00

CBSE XII ACCOUNTANCY MOST IMPORTANT QUESTIONS

www.topperlearning.com 1 CBSE Class XII Accountancy Most Important Questions SECTION A Chapter 1: Accounting for Partnership Firms Fundamental 1. The Capital Accounts of A and B stood at 4,00,000 and 3,00,000

www.topperlearning.com 1 CBSE Class XII Accountancy Most Important Questions SECTION A Chapter 1: Accounting for Partnership Firms Fundamental 1. The Capital Accounts of A and B stood at 4,00,000 and 3,00,000

Time allowed : 3 hours Maximum marks : 100. Total number of questions : 6 Total number of printed pages : 10

Roll No... : 1 : 325 Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 10 NOTE : 1. Answer ALL Questions. 2. All working notes should be shown distinctly.

Roll No... : 1 : 325 Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 10 NOTE : 1. Answer ALL Questions. 2. All working notes should be shown distinctly.

SUGGESTED SOLUTION. Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022)

, Mumbai 69. Tel : (022)") SUGGESTED SOLUTION Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e Ans. 1 (a) Computation of Weighted Average Number of Shares Outstanding

SUGGESTED SOLUTION Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e Ans. 1 (a) Computation of Weighted Average Number of Shares Outstanding

QATAR REINSURANCE COMPANY LIMITED (PREVIOUSLY KNOWN AS QATAR REINSURANCE COMPANY LLC) BERMUDA

BERMUDA") (PREVIOUSLY KNOWN AS QATAR REINSURANCE COMPANY LLC) BERMUDA CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT FOR THE YEAR ENDED DECEMBER 31, 2015 CONSOLIDATED FINANCIAL STATEMENTS AND

(PREVIOUSLY KNOWN AS QATAR REINSURANCE COMPANY LLC) BERMUDA CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT FOR THE YEAR ENDED DECEMBER 31, 2015 CONSOLIDATED FINANCIAL STATEMENTS AND

APPENDIX A. Financial Statements. City of Toronto Sinking Funds December 31, 2016

APPENDIX A Financial Statements City of Toronto Sinking Funds December 31, 2016 DRAFT July @@, 2017 Independent Auditor s Report To the Members of Council of City of Toronto We have audited the accompanying

APPENDIX A Financial Statements City of Toronto Sinking Funds December 31, 2016 DRAFT July @@, 2017 Independent Auditor s Report To the Members of Council of City of Toronto We have audited the accompanying

Solved Answer Acc._Paper_5 CA Ipcc May

Solved Answer Acc._Paper_5 CA Ipcc May. 2010 1 Qn. 1. Answer the following questions : [ 10 x 2 = 20 marks ] (i) A Company had issued 20,000, 13% Convertible debentures of Rs.100 each on 1st April, 2007.

Solved Answer Acc._Paper_5 CA Ipcc May. 2010 1 Qn. 1. Answer the following questions : [ 10 x 2 = 20 marks ] (i) A Company had issued 20,000, 13% Convertible debentures of Rs.100 each on 1st April, 2007.

Revisionary Test Paper_Dec 2018

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) 1. Multiple Choice Questions: Objectives (i) Mittal Ltd. has provided the following information: Depreciation as per accounting records

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) 1. Multiple Choice Questions: Objectives (i) Mittal Ltd. has provided the following information: Depreciation as per accounting records

SAMPLE PAPER-II ACCOUNTANCY CLASS XII

SAMPLE PAPER-II ACCOUNTANCY CLASS XII Part A: Accounting for Not-For Profit Organizations, Partnership Firms & Companies Q.1. How is life membership fees are treated in the accounts of a non-profit organization?

SAMPLE PAPER-II ACCOUNTANCY CLASS XII Part A: Accounting for Not-For Profit Organizations, Partnership Firms & Companies Q.1. How is life membership fees are treated in the accounts of a non-profit organization?

Part-I. Choose the correct answer: 20x1=20

Higher secondary second year Accountancy Model Question paper - II Time: 2.30 hrs Marks:90 Part-I Choose the correct answer: 20x1=20 1. Trial balance shows sundry debtors Rs.75,000/- as on 31.12.2005.

Higher secondary second year Accountancy Model Question paper - II Time: 2.30 hrs Marks:90 Part-I Choose the correct answer: 20x1=20 1. Trial balance shows sundry debtors Rs.75,000/- as on 31.12.2005.

Bharatiya Vidya Bhavan s V.M Public School Vadodara. Accountancy. Class XII Sample Paper-6

Bharatiya Vidya Bhavan s V.M Public School Vadodara Accountancy Class XII 2017-18 Sample Paper-6 Set-6 TIME: 3 HOURS MARKS: 80 GENERAL INSTRUCTIONS: 1. This question paper contains three parts A, B & C.

Bharatiya Vidya Bhavan s V.M Public School Vadodara Accountancy Class XII 2017-18 Sample Paper-6 Set-6 TIME: 3 HOURS MARKS: 80 GENERAL INSTRUCTIONS: 1. This question paper contains three parts A, B & C.

Financial Statements of Companies

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

KENDRIYA VIDYALAYA ERNAKULAM REGION MODEL PAPER ACCOUNTANCY Class XII Time 3.hrs M.Marks 80 PART A

KENDRIYA VIDYALAYA ERNAKULAM REGION MODEL PAPER ACCOUNTANCY Class XII Time 3.hrs M.Marks 80 PART A 1. What are the circumstances in which the capital balances of the partners fluctuate, when the capitals

KENDRIYA VIDYALAYA ERNAKULAM REGION MODEL PAPER ACCOUNTANCY Class XII Time 3.hrs M.Marks 80 PART A 1. What are the circumstances in which the capital balances of the partners fluctuate, when the capitals

PAPER 1: ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR NOVEMBER, 2015 EXAMINATION

PAPER 1: ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR NOVEMBER, 2015 EXAMINATION A. Applicable for November, 2015 examination (i) Companies Act, 2013 (ii) The relevant

PAPER 1: ACCOUNTING PART I: ANNOUNCEMENTS STATING APPLICABILITY & NON-APPLICABILITY FOR NOVEMBER, 2015 EXAMINATION A. Applicable for November, 2015 examination (i) Companies Act, 2013 (ii) The relevant

Prepare the necessary journal entries to correct the above. Narrations are not required.

Correction of errors HKDSE (2017, 5) (Correction of errors) ABC Limited drafted a trial balance as at 31 December 2016, before the preparation of the closing entries. As the trial balance did not agree,

Correction of errors HKDSE (2017, 5) (Correction of errors) ABC Limited drafted a trial balance as at 31 December 2016, before the preparation of the closing entries. As the trial balance did not agree,

ACCOUNTS MAY QUESTION PAPER

TOPPER S INSTITUTE [IPC-GROUP - I] Accounts 1 ACCOUNTS MAY 2017 - QUESTION PAPER Q.1 (b) (c) (d) ABC Financial Services Ltd. is engaged in the business of financial services and is undergoing tight liquidity

TOPPER S INSTITUTE [IPC-GROUP - I] Accounts 1 ACCOUNTS MAY 2017 - QUESTION PAPER Q.1 (b) (c) (d) ABC Financial Services Ltd. is engaged in the business of financial services and is undergoing tight liquidity

PAPER 5 : ADVANCED ACCOUNTING

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

Limited Companies Question: Explain the meaning of the following terms so as to make clear the differences between them: Ordinary Shares are

Limited Companies Explain the meaning of the following terms so as to make clear the differences between them: Ordinary Shares are certificates of ownership to a company. They are issued to shareholders

Limited Companies Explain the meaning of the following terms so as to make clear the differences between them: Ordinary Shares are certificates of ownership to a company. They are issued to shareholders

Required: Draw up a three-column cash book to record the above transactions and balance off the cash book at the end of the month.

Chapter 1 Books of original entry and ledgers (I) Mary Company had the following transactions during the month November 2014: Nov 3 Credit purchases from: Hilary Lam $13,580, Tammy Yiu $55,500. 5 Credit

Chapter 1 Books of original entry and ledgers (I) Mary Company had the following transactions during the month November 2014: Nov 3 Credit purchases from: Hilary Lam $13,580, Tammy Yiu $55,500. 5 Credit

DISCLAIMER. The Institute of Chartered Accountants of India

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

FINAL CA May 2018 Financial Reporting

FINAL CA May 2018 Financial Reporting Test Code F5 Branch: Andheri Date: 10.12.2017 (50 Marks) Note: All questions are compulsory. Question 1 (9 marks) Value Added Statement of Pradeep Ltd. for the period

FINAL CA May 2018 Financial Reporting Test Code F5 Branch: Andheri Date: 10.12.2017 (50 Marks) Note: All questions are compulsory. Question 1 (9 marks) Value Added Statement of Pradeep Ltd. for the period

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING

: GROUP I PAPER 1: ACCOUNTING") MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING 1 Test Series: March, 2018 SUGGESTED ANSWERS/HINTS 1. (a) Constructing or acquiring a new asset may result in incremental costs that would

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING 1 Test Series: March, 2018 SUGGESTED ANSWERS/HINTS 1. (a) Constructing or acquiring a new asset may result in incremental costs that would

Model Test Paper - 2 IPCC Group- I Paper - 1 Accounting May Answer : Provisions: According to AS 10, Property, Plant and Equipment: 1.

Model Test Paper - 2 IPCC Group- I Paper - 1 Accounting May - 2017 1. (a) M/s Progressive Company Limited has not charged depreciation for the year ended on 31 st March, 2012, in respect of a spare bus

Model Test Paper - 2 IPCC Group- I Paper - 1 Accounting May - 2017 1. (a) M/s Progressive Company Limited has not charged depreciation for the year ended on 31 st March, 2012, in respect of a spare bus

Page Std:- XII. Sub: - Accountancy Practice Paper Time:- 3 Hours Max.Marks:- 80

Page - 1 D.A.V. PUBLIC SCHOOL, NEW PANVEL Plot No. 267, 268, Sector-10, New Panvel, Navi Mumbai-410206 (Maharashtra). Phone 022-27451793, 27468211, Telefax- 27482276 Email- davschoolnp@vsnl.net, www.davnewpanvel.com

Page - 1 D.A.V. PUBLIC SCHOOL, NEW PANVEL Plot No. 267, 268, Sector-10, New Panvel, Navi Mumbai-410206 (Maharashtra). Phone 022-27451793, 27468211, Telefax- 27482276 Email- davschoolnp@vsnl.net, www.davnewpanvel.com

SAMPLE PAPER-III ACCOUNTANCY CLASS XII

SAMPLE PAPER-III ACCOUNTANCY CLASS XII PART-A : Accounting for Not for profit Organisation, Partnership and Company Q.1. How do you treat amount received from individual as per will in the final Accounts

SAMPLE PAPER-III ACCOUNTANCY CLASS XII PART-A : Accounting for Not for profit Organisation, Partnership and Company Q.1. How do you treat amount received from individual as per will in the final Accounts

1,200 9,700 20,000 35,000 50,000 1,15,900

50 QUESTIONS OF ACCOUNTANCY CLASS 12 Ques 1 A and B are partners in a firm sharing profits and losses in the ratio of 2 : 1. They decide to take C into partnership for 1/5 th share on 1 st April 2011.

50 QUESTIONS OF ACCOUNTANCY CLASS 12 Ques 1 A and B are partners in a firm sharing profits and losses in the ratio of 2 : 1. They decide to take C into partnership for 1/5 th share on 1 st April 2011.

14 Issues in Partnership Accounts

14 Issues in Partnership Accounts Question 1 Ram, Rahim and Robert are partners, sharing Profits and Losses in the ratio of 5 : 3 : 2. It was decided that Robert would retire on 31.3.2005 and in his place

14 Issues in Partnership Accounts Question 1 Ram, Rahim and Robert are partners, sharing Profits and Losses in the ratio of 5 : 3 : 2. It was decided that Robert would retire on 31.3.2005 and in his place

Paper-5: FINANCIAL ACCOUNTING

Paper5: FINANCIAL ACCOUNTING Time Allowed: 3 Hours Full Marks : 100 Whenever necessary, suitable assumptions should be made and indicate in answer by the candidates. Working Notes should be form part of

Paper5: FINANCIAL ACCOUNTING Time Allowed: 3 Hours Full Marks : 100 Whenever necessary, suitable assumptions should be made and indicate in answer by the candidates. Working Notes should be form part of

Time allowed : 3 hours Maximum Marks : 80

Time allowed : 3 hours Maximum Marks : 80 General Instructions: (i) This question paper contains three parts A, B, and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can attempt only

Time allowed : 3 hours Maximum Marks : 80 General Instructions: (i) This question paper contains three parts A, B, and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can attempt only

LOYOLA COLLEGE (AUTONOMOUS), CHENNAI B.Com. DEGREE EXAMINATION COMMERCE THIRD SEMESTER NOVEMBER 2014 CO COMPANY ACCOUNTS SECTION A

, CHENNAI B.Com. DEGREE EXAMINATION COMMERCE THIRD SEMESTER NOVEMBER 2014 CO COMPANY ACCOUNTS SECTION A") LOYOLA COLLEGE (AUTONOMOUS), CHENNAI 600 034 B.Com. DEGREE EXAMINATION COMMERCE THIRD SEMESTER NOVEMBER 2014 CO 3502 - COMPANY ACCOUNTS Date : 31/10/2014 Time : 09:00-12:00 Dept. No. SECTION A Max. : 100

LOYOLA COLLEGE (AUTONOMOUS), CHENNAI 600 034 B.Com. DEGREE EXAMINATION COMMERCE THIRD SEMESTER NOVEMBER 2014 CO 3502 - COMPANY ACCOUNTS Date : 31/10/2014 Time : 09:00-12:00 Dept. No. SECTION A Max. : 100

Solved Answer Accounts CA IPCC Dec by Arvind Jain 1

Solved Answer Accounts CA IPCC Dec. 2009 by Arvind Jain 1 1. (i) On 1st April, 2008, Chhotu started business with an initial Capital of Rs. 70,000. On 1st October, 2008, he introduced additional capital

Solved Answer Accounts CA IPCC Dec. 2009 by Arvind Jain 1 1. (i) On 1st April, 2008, Chhotu started business with an initial Capital of Rs. 70,000. On 1st October, 2008, he introduced additional capital

MODULE 4 DEVELOPMENT OF INTERNATIONAL ACCOUNTING

MODULE 4 DEVELOPMENT OF INTERNATIONAL ACCOUNTING Outlines Economic Factors Influencing International Accounting Environmental Factors Shaping National Accounting Accounting in Less-developed Countries

MODULE 4 DEVELOPMENT OF INTERNATIONAL ACCOUNTING Outlines Economic Factors Influencing International Accounting Environmental Factors Shaping National Accounting Accounting in Less-developed Countries

Downloaded from

QUESTION PAPER (055) CLASS-XII Time allowed 3 hours Maximum Marks 80 General Instructions: 1) This question paper contains two parts A and B. 2) Part A is compulsory for all. 3) Part B has two options-financial

QUESTION PAPER (055) CLASS-XII Time allowed 3 hours Maximum Marks 80 General Instructions: 1) This question paper contains two parts A and B. 2) Part A is compulsory for all. 3) Part B has two options-financial

MODEL EXAMINATION (DECEMBER 2017) SET-I Subject: ACCOUNTANCY

SET-I Subject: ACCOUNTANCY") Code No. : 055 CLASS: XII MODEL EXAMINATION (DECEMBER 207) SET-I Subject: ACCOUNTANCY Time: hrs. MAX. MARKS: 80 Name Roll No. General Instructions:. This question paper consists of two parts A and B. This

Code No. : 055 CLASS: XII MODEL EXAMINATION (DECEMBER 207) SET-I Subject: ACCOUNTANCY Time: hrs. MAX. MARKS: 80 Name Roll No. General Instructions:. This question paper consists of two parts A and B. This

PROFITS OR LOSS PRIOR TO INCORPORATION

CHAPTER 3 PROFITS OR LOSS PRIOR TO INCORPORATION Learning Objectives After studying this chapter, you will be able to: Account for pre-incorporation profit. Learn various methods for computing profit or

CHAPTER 3 PROFITS OR LOSS PRIOR TO INCORPORATION Learning Objectives After studying this chapter, you will be able to: Account for pre-incorporation profit. Learn various methods for computing profit or

Accountancy. Time Allowed: 3 hours Maximum : The question paper consists of Part A and Part B

Sample Paper (CBSE) Series SC/SP Accountancy Code No. SP-16 Time Allowed: 3 hours Maximum : 80 General Instructions: 1. All questions are compulsory. 2. The question paper consists of Part A and Part B

Sample Paper (CBSE) Series SC/SP Accountancy Code No. SP-16 Time Allowed: 3 hours Maximum : 80 General Instructions: 1. All questions are compulsory. 2. The question paper consists of Part A and Part B

UNIVERSITY OF BOLTON INSTITUTE OF MANAGEMENT ACCOUNTANCY SEMESTER ONE EXAMINATIONS 2017/18 FINANCIAL ACCOUNTING AND REPORTING MODULE NO: ACC5001

[IOM05] UNIVERSITY OF BOLTON INSTITUTE OF MANAGEMENT ACCOUNTANCY SEMESTER ONE EXAMINATIONS 2017/18 FINANCIAL ACCOUNTING AND REPORTING MODULE NO: ACC5001 Date: Tuesday 16 th January 2018 Time: 10:00 13:00

[IOM05] UNIVERSITY OF BOLTON INSTITUTE OF MANAGEMENT ACCOUNTANCY SEMESTER ONE EXAMINATIONS 2017/18 FINANCIAL ACCOUNTING AND REPORTING MODULE NO: ACC5001 Date: Tuesday 16 th January 2018 Time: 10:00 13:00

Note: Question 1 is compulsory. Attempt any five from the rest.

INTER CA MAY 2018 PAPER 5 :ADVANCED ACCOUTING Branch: Multiple Date: Question 1 (5 marks each) Note: Question 1 is compulsory. Attempt any five from the rest. A) Trilochan Ltd are Heavy Engineering Contractors

INTER CA MAY 2018 PAPER 5 :ADVANCED ACCOUTING Branch: Multiple Date: Question 1 (5 marks each) Note: Question 1 is compulsory. Attempt any five from the rest. A) Trilochan Ltd are Heavy Engineering Contractors

TRANS-NATIONWIDE EXPRESS PLC PERIOD ENDED MARCH 31, 2016 TABLE OF CONTENTS. Statement of Accounting Policies

TABLE OF CONTENTS CONTENTS PAGE Statement of Accounting Policies 2 -- 8 Statement of comprehensive income 9 Statement of financial position 10 Statement of changes in equity 11 Statement of cash flow 12

TABLE OF CONTENTS CONTENTS PAGE Statement of Accounting Policies 2 -- 8 Statement of comprehensive income 9 Statement of financial position 10 Statement of changes in equity 11 Statement of cash flow 12

Paper-12 : COMPANY ACCOUNTS & AUDIT

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an):

- Please choose one Wages outstanding given in the trial balance will be treated as a (an):") Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset Liability Revenue Deferred expense Question No: 2 ( Marks: 1 ) - Please choose

Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset Liability Revenue Deferred expense Question No: 2 ( Marks: 1 ) - Please choose

Professor Vipin Conversion of Partnership into Company. Meaning

Meaning Conversion of Partnership into Company For various reasons, an existing partnership may sell its entire business to an existing Joint Stock Company. It can also convert itself into a Joint Stock

Meaning Conversion of Partnership into Company For various reasons, an existing partnership may sell its entire business to an existing Joint Stock Company. It can also convert itself into a Joint Stock

Free of Cost ISBN : Solved. Scanner. Appendix. IPCC Gr. II. (Solution of Nov & Questions of May )

") Free of Cost ISBN : 978-93-5034-547-4 Solved Scanner Appendix IPCC Gr. II (Solution of Nov - 2012 & Questions of May - 2013) Paper - 5 : Advanced Accounting Solution of Nov - 2012 Chapter - 2 : Accounting

Free of Cost ISBN : 978-93-5034-547-4 Solved Scanner Appendix IPCC Gr. II (Solution of Nov - 2012 & Questions of May - 2013) Paper - 5 : Advanced Accounting Solution of Nov - 2012 Chapter - 2 : Accounting

ACCOUNTANCY MODEL TEST PAPER-1

ACCOUNTANCY MODEL TEST PAPER-1 Q1- Is it correct that interest on capital is payable whether there is profit or loss in the business? (1) Q2-*-K,L & M were partners sharing profits in the ratio of 3:2:1.

ACCOUNTANCY MODEL TEST PAPER-1 Q1- Is it correct that interest on capital is payable whether there is profit or loss in the business? (1) Q2-*-K,L & M were partners sharing profits in the ratio of 3:2:1.

School of Distance Education UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION. B Com. III Semester. Core Course CORPORATE ACCOUNTING QUESTION BANK

UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION B Com (2011 Admission Onwards) III Semester Core Course CORPORATE ACCOUNTING QUESTION BANK 1. is an artificial person created by law A. Firm B. Sole trader

UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION B Com (2011 Admission Onwards) III Semester Core Course CORPORATE ACCOUNTING QUESTION BANK 1. is an artificial person created by law A. Firm B. Sole trader

ACCOUNTS (Three hours) (Candidates are allowed additional 15 minutes for only reading the paper. They must NOT start writing during this time.

(Candidates are allowed additional 15 minutes for only reading the paper. They must NOT start writing during this time.") ACCOUNTS (Three hours) (Candidates are allowed additional 15 minutes for only reading the paper. They must NOT start writing during this time.) ----------------------------------------------------------------------------------------------------------------

ACCOUNTS (Three hours) (Candidates are allowed additional 15 minutes for only reading the paper. They must NOT start writing during this time.) ----------------------------------------------------------------------------------------------------------------

NABTEB Past Questions and Answers - Uploaded online

QUESTION 1 NATIONAL BUSINESS AND TECHNICAL EXAMINATION BOARD NBC MAY/JUNE 2005 FINANCIAL ACCOUNTING (a) Differentiate between preference shares and ordinary shares of a company. (b) Explain the following

QUESTION 1 NATIONAL BUSINESS AND TECHNICAL EXAMINATION BOARD NBC MAY/JUNE 2005 FINANCIAL ACCOUNTING (a) Differentiate between preference shares and ordinary shares of a company. (b) Explain the following

General Reserve 10,000 Discount on issue of Debentures

PAPER 5 : ADVANCED ACCOUNTING QUESTIONS Answer the following (Give adequate working notes in support of your answer): 1. (i) On 31 st March, 2010 Maya Bank Ltd. finds that: (1) On a term loan of 2 crores,

PAPER 5 : ADVANCED ACCOUNTING QUESTIONS Answer the following (Give adequate working notes in support of your answer): 1. (i) On 31 st March, 2010 Maya Bank Ltd. finds that: (1) On a term loan of 2 crores,

PAPER 5 : ADVANCED ACCOUNTING

Question 1 PAPER 5 : ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Wherever necessary, suitable assumption(s) may be made and disclosed by

Question 1 PAPER 5 : ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Wherever necessary, suitable assumption(s) may be made and disclosed by

Issues in Partnership Accounts

14 Issues in Partnership Accounts BASIC CONCEPTS Partnership is defined as the relationship between persons who have agreed to share the profit or loss of a business carried on by all or any of them acting

14 Issues in Partnership Accounts BASIC CONCEPTS Partnership is defined as the relationship between persons who have agreed to share the profit or loss of a business carried on by all or any of them acting

Time allowed : 3 hours Maximum marks : 100. Total number of questions : 8 Total number of printed pages : 12

: 1 : 222 Roll No... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 12 NOTE : All working notes should be shown distinctly. PART A (Answer Question

: 1 : 222 Roll No... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 12 NOTE : All working notes should be shown distinctly. PART A (Answer Question

Test Series: March, 2018

MOCK TEST PAPER INTERMEDIATE (NEW) : GROUP II PAPER 5 : ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any four questions from the remaining five questions. 1 Test Series: March, 2018 Wherever

MOCK TEST PAPER INTERMEDIATE (NEW) : GROUP II PAPER 5 : ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any four questions from the remaining five questions. 1 Test Series: March, 2018 Wherever