GE20803 DEPOSIT & FINANCING OPERATION OF ISLAMIC BANKING

|

|

|

- Scott Walters

- 6 years ago

- Views:

Transcription

1 GE20803 DEPOSIT & FINANCING OPERATION OF ISLAMIC BANKING FINANCING EVALUATION TECHNIQUE Updated version 24th November 2015 BY DR. HANUDIN AMIN LABUAN FACULTY OF INTERNATIONAL FINANCE UNIVERSITI MALAYSIA SABAH

2 PREAMBLE Appropriate analytical tool is important in credit assessment to determine a correct credit decision Two important techniques are commonly used: The qualitative method The quantitative method

3 5C OF CREDIT Condition Character Collateral Capacity Capital

4 WHAT, WHY, HOW, EXAMPLE CHARACTER? Questions asked: Character means the moral or ethical quality of a person Moral factor/human factor Also means the probability that customers will honor their obligation Borrower s reputation Willingness to pay How long you have lived at current address? How long you have been in your current job? Have you used credit before? What Why Real Activities How CHARACTER Ethical Example Governance Banks consider for people with excellent character to extend loans to them Individuals with ideal character are the most likely to repay the loan Every credit transaction implies a promise to pay

5 As an experienced credit officer of ABC Bank, you are assigned to evaluate the character of each loan applicant. What is your evaluation on Simon and Richard? How do you make the evaluation Points to consider Historical credit records Character reference by a 3rd party etc

6 WHAT, WHY, HOW, EXAMPLE CAPACITY? The ability to pay Capacity means the ability of the borrowers to generate the necessary cash flows to repay the borrowings Person s ability to pay debt when it is due What Real Activities CAPACITY Why Ethical The credit officer should evaluate borrower capacity from the aspects of law and finance The credit officer should determine if borrower has the legal capacity to borrow The credit officer should determine if borrower has capacity to repay loan Questions asked: Do you have legal capacity? Do you have income tax statements? How Example Governance

7 WHAT, WHY, HOW, EXAMPLE CAPITAL? Capital refers to your net worth the value of your assets minus liabilities What Why We need to know the financial worth of a prospective borrower through his net work because net worth symbolizes the success and commitment of the person Questions asked: How much your own minus how much you owe? Real Activities How CAPITAL Ethical Example Governance

8 WHAT, WHY, HOW, EXAMPLE COLLATERAL? Questions asked: Collateral refers to security in the event the borrower does not pay Collateral refers to any asset of a borrower that a lender has a right to take ownership of an use to pay the debt if the borrower is unable to make the loan payments as agreed Do you have collaterals to support your loan? What Why Real Activities How COLLATERAL Ethical Example Governance Ensure sufficient security in case of default To protect the interest of banks A secondary source of repayment of the loan Something of value an asset or property - that you pledge when getting a loan For example, when you buy a home, the home you purchase is often the only collateral available

9 WHAT, WHY, HOW, EXAMPLE CONDITION? When we evaluate a prospective borrower s capacity to borrow, we actually need to evaluate the economic conditions that may affect the borrower s capacity to repay the loan What Why The analysis on economic conditions is to forecast the exposure of the borrower s business to economic changes and interest rate changes Questions asked: Are you able to pay loan during the recession/economic downturn? What is your capacity to repay when the economic is expanding? Real Activities How CONDITION Ethical Example Governance For example, the economic recession that hit the country in mid 1997 as a result of the financial crisis in the region

10 LECTURETTE #1 TRUE/ FALSE QUESTION: 1. Character refers to the probability that customers will attempt to fulfil their obligations 2. Ability of the borrower to generate the necessary cash flows to repay the borrowings is referred as Capacity 3. Conditions deal with any external influences that can affect the ability of the borrowers to honor their obligations to the lenders 4. Collateral is intended to provide lenders with more comfort when providing loan to borrower 5. Capital is the value of your assets minus your liabilities. How much you own (for example, car, real estate, cash and investment) minus how much you owe

was set up by the Credit Bureau of Bank Negara Malaysia Enables Fis")

11 SOURCES OF CREDIT INFORMATION Loan applicant interview To collect information on the character and intention of the applicant Opportunity to evaluate applicant in terms of commitment and motivation Bank records Loan repayment records Current account and savings account balances Factual, it is deemed highly reliable Applicant s business premises Visit to the business premises of the applicant gives the opportunity to verify the existence of the company, the structure, the skillfulness and the details of the company s operating assets and fixed assets To prevent acute fraud Inter-bank references Confirmation from other banks regarding a loan applicant s credit standing is a common banking practice Credit Bureau In Oct. 2001, a borrower database known as Central Credit Record Information System (CCRIS) was set up by the Credit Bureau of Bank Negara Malaysia Enables Fis to acquire information on their prospective borrowers for the purpose of loan application evaluation Financial statements Include income statements, balance sheets and cash flow statements To make quantitative judgement on the applicants capacity to repay their loans More reliable than that obtained from unaudited financial statements

12 RATIO ANALYSIS The purpose of ratio analysis is to examine the financial performance and position of a company Credit officers of banks use ratio analysis to determine if the financial performance and position of a prospective borrower show sufficient loan repayment capacity As such, credit officers use trend analysis to find out if the financial performance and position have improved or deteriorated or remained unchanged over a period of time Four groups of financial ratios used: Liquidity ratios Asset management ratios Financial leverage ratios Profitability ratios

13 RATIO ANALYSIS Ratio Formula Remark Current ratio Current asset/current liabilities Quick ratio (Current asset inventories)/ Current liabilities Average collection period (Account receivable/annual credit sales ) x 365 days A current ratio of 2 is sufficient which implies that every RM1 of current liabilities are protected by RM 2 of current assets. A quick ratio of 1 is sufficient because every RM1 of liabilities is protected by RM1 of quick assets A shorter average collection period is intended. A very short collection period is not necessarily favorable rather it suggests a very restrictive credit and collection policy Inventory turnover Sales/Average inventory High ratio means inventors are quickly swiftly turned into sales suggests better inventory management Debt ratio Total debts/total assets Banks prefer customers with low debt ratio since the lower the debt ratio the lower the debt repayment risk

14 RATIO ANALYSIS Ratio Formula Remark Times interest earned Earnings before interest and taxes/interest payable on loans The higher the ratio, the better it is. No benchmark but the ratio should be at least 2 to give the firm sufficient buffer to pay the interest Gross profit margin Gross margin/sales A gross profit margin of 40% suggests that every $1 of sale costs the business $0.6 in terms of production expenditure and generate $0.4 profit before accounting for any non production costs Operating profit margin EBIT/Sales A high operating profit margin means that the company has good cost control and or that sales are increasing faster than costs Asset turnover Revenue/Total assets Comparing the fixed asset turnover ratio and the total asset turnover ration to determine if there is weakness in the fixed asset and current asset managements Fixed asset turnover Sales/Fixed assets Low ratio indicates that the management failed to utilize fixed assets productively to generate sales ROA ROE After tax earnings/total assets After tax earnings/shareholder s equity The higher the ROA ratio, the higher the company s ability is to generate return by using its assets and vice versa How much profit a company generates with the money shareholders have invested

15 CREDIT SCORING CONSUMER LOAN APPLICATIONS Most lenders have used credit scoring to assess the loan applications they received from customers Advantages handle a large volume of credit applications quickly with minimal labor The basic theory of credit scoring is that lenders and statisticians can identify the financial, economic, and motivational factors that separate good loans from bad loans by observing large groups of people who borrowed in the past

16 PREDICTIVE FACTORS IN AN EXAMPLE OF A CREDIT SCORING MODEL AND THEIR POINT VALUES Factors for predicting credit quality 1. Customer s occupation or line of work Point value Professional or business executive 100 Skilled worker 80 Clerical worker 70 Student 50 Unskilled worker 40 Part-time employee Housing status Owns home 60 Rents home or apartment 40 Lives with friend or relative Credit rating Excellent 100 Average 50 No record 20 Poor 00

17 PREDICTIVE FACTORS IN AN EXAMPLE OF A CREDIT SCORING MODEL AND THEIR POINT VALUES Factors for predicting credit quality 4. Length of time in current job Point value More than 1 year 50 One year or less Length of time at current address More than 1 year 20 One year or less Telephone in home or apartment Yes 20 No Number of dependents reported None 30 One 30 Two 40 Three 40 More than three 20

18 PREDICTIVE FACTORS IN AN EXAMPLE OF A CREDIT SCORING MODEL AND THEIR POINT VALUES Factors for predicting credit quality 8. Deposits accounts held Point value Both checking and savings 40 Savings account only 30 Checking account only 20 None 00

19 LECTURETTE #2 APPLYING 5C TO CURRENT PRACTICE Read the case below Pn Anis, the finance manager of Syarikat Mekar Bhd has submitted the company s loan application to you in your capacity as the loan manager of Bank Nikmat Bhd. She has enclosed the company s financial statements for year 2015 The main business activities of Syarikat Mekar is manufacturing furniture for domestic as well as overseas customers. On overage, the company exports 25% of its furniture products to European and ASEAN countries. Besides, the company sells home decoration supplies and various types of lawn mowers that represent 10% of the company s business activities

20 The main shareholder of the company is En. Mekar who is also the managing director of the company. He holds 55% of the company shares. Others are his wife 10% and child 5% The company has been incorporated 30 years by En. Mekar s father. The company was handled by En. Mekar after his father passed away 10 years ago. En. Mekar is a certified accountant and according to this staff are a hardworking person The company has not borrowed from your bank before but holds current account and fixed deposit account at your bank. You have been informed by Pn Anis that the company wishes to borrow from your bank because it is dissatisfied with the treatment and facility provided by its other bank which is indeed the closest rival of your bank. Pn. Anis has also advised that the purpose of the loan applied for is to increase the working capital of the company

21 Syarikat Mekar Bhd Balance Sheet as at 31 December 2015

22 Syarikat Mekar Bhd Income Statement as at 31 December 2015 You are required to make the credit decision on the loan application of Syarikat Mekar based on 5C credit analysis model

23 Proposed Analysis Character Evaluate the character of the company by making reference to the character of the owner The majority and managing director of the company 55% majority shareholding suggests that En. Mekar is committed and feels responsible for his business Capacity The company s capacity to repay loan, ratio analysis, cash flow statement and pro forma statement Ratio analysis for trend analysis is needed to understand the company capacity to repay debt

24 Average

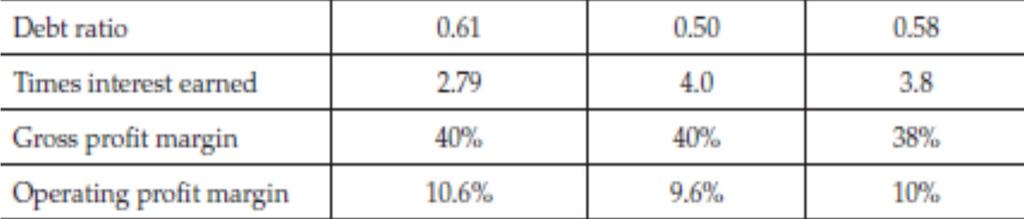

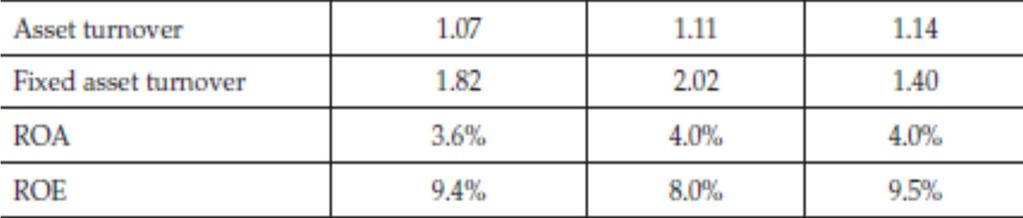

25 Ratio Analysis Average collection period is 36.5 days, the management of account receivable has been consistent. The analysis is meaningful if the information on the CREDIT PERIOD is available Inventory Turnover Ratio appears to have deteriorated from the previous year Besides, the company s performance is worst than the industry average The company s fixed asset management is better than the industry average but has deteriorated from the previous year Based on Total Asset Turnover, it appears that the company s performance in total asset management is worst than the previous year s and the industry average. The deterioration in inventory management leads to the performance The company s ROA has declined, below industry average The company s ROE has improved and closed to the industry average, since ROE > ROA, the company managed to increase shareholders wealth through financial leverage Financial position the company s liquidity is worse than the position in the previous year. It is also below the industry average. This is evident from the current and quick ratio The Quick Ratio has deteriorated significantly due to the weakness in inventory management which has resulted in a large quantity of inventories being held by the company In terms of debt capacity, the company s capacity to pay loan interest has reduced as measured by the times interest earned (TIE) ratio The deterioration is attributed to the increased utilization of loans, as shown by the current ratio and the decline in income generating capacity. The financial risk of the company has increased as evidenced from the increase in debt ratio from 50% to 61%

26 Proposed Analysis Collateral Assets that can be used as collateral consist of current assets such as accounts receivable and inventories and fixed assets En. Mekar and other shareholders can also provide personal guarantee as collateral With all collateral available, compared with the amount of loan applied Conditions Capital It is needed to determine if the furniture business is seasonal business because the volatility in cash flow may affect the company s capacity to repay debts As furniture represents the main products of the company, it is important to focus on the factors that can affect the demand for these products analyze the effect of regional as well as global economic since some of the company s products are exported to European and Asean countries It is difficult to perform since we do not have any comparative figures, nevertheless we should investigate if the capital of the company has increased because that will provide an indication on the financial performance of the company We should review company s working capital position from year to year By making reference to the deterioration in the current ratio and quick ratio, the capital position is expected to have deteriorated too

27 Proposed Analysis From the above analysis, it appears that we are unable to approve the loan application based on5c credit analysis model Why The company s capacity to repay the loan looks very doubtful, deteriorated liquidity, deteriorated profitability and growing financial risk ARE the negative indicators of the company s capacity to repay its debts

Knowledge is a Trust hanudin@ums.edu.")

28 All praise belongs to Almighty Allah (S.W.T) Knowledge is a Trust hanudin@ums.edu.my MP

TABLE OF CONTENTS. Healthier Black Elders Center

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

Adequacy INTRODUCTION OBJECTIVES

Chapter 9 Capital Adequacy OBJECTIVES At the end of this chapter, you should be able to: 1. explain the relationship between the concept of capital adequacy and the liquidation risk of banks; 2. explain

Chapter 9 Capital Adequacy OBJECTIVES At the end of this chapter, you should be able to: 1. explain the relationship between the concept of capital adequacy and the liquidation risk of banks; 2. explain

Introduction Slide SET. Host Organization s Name July 30, Business Smart is a business education series developed by

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

REVIEW OF BASIC UNDERSTANDING AND ANALYSIS OF FINANCIAL STATEMENTS

REVIEW OF BASIC UNDERSTANDING AND ANALYSIS OF FINANCIAL STATEMENTS Payear Sangiumvibool, Ph.D., CPA (US) ดร. พเย ย เสง ยมว บ ล Webster University Thailand Faculty, Accounting and Management สภาว ชาช พบ

REVIEW OF BASIC UNDERSTANDING AND ANALYSIS OF FINANCIAL STATEMENTS Payear Sangiumvibool, Ph.D., CPA (US) ดร. พเย ย เสง ยมว บ ล Webster University Thailand Faculty, Accounting and Management สภาว ชาช พบ

Understanding the Concept of Borrowing Money

Lesson D1 2 Understanding the Concept of Borrowing Money Unit D. Basic Agribusiness Principles and Skills Problem Area 1. Managing Personal Finances Lesson 2. Understanding the Concept of Borrowing Money

Lesson D1 2 Understanding the Concept of Borrowing Money Unit D. Basic Agribusiness Principles and Skills Problem Area 1. Managing Personal Finances Lesson 2. Understanding the Concept of Borrowing Money

Credit Cards. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage.

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

6/10/2015. Trust & confidence. Convenience. Quality services. Excellent brand. Interest pay-out WHY NEEDED? HOW DOES IT MOBILISE DEPOSITS?

GE20803 DEPOSIT & FINANCING OPERATION OF ISLAMIC BANKING MOBILIZATIONS BY CONVENTIONAL BANKS WHY NEEDED? 1. Deposit mobilization is one of the crucial functions of conventional banks it is a requirement

GE20803 DEPOSIT & FINANCING OPERATION OF ISLAMIC BANKING MOBILIZATIONS BY CONVENTIONAL BANKS WHY NEEDED? 1. Deposit mobilization is one of the crucial functions of conventional banks it is a requirement

Chapter 02 Analysis of Financial Statements

Chapter 02 Analysis of Financial Statements TRUEFALSE 1. The information contained in the annual report is used by investors to form expectations about future earnings and dividends. 2. Noncash assets

Chapter 02 Analysis of Financial Statements TRUEFALSE 1. The information contained in the annual report is used by investors to form expectations about future earnings and dividends. 2. Noncash assets

LOAN CO-APPLICANT FORM

LOAN CO-APPLICANT FORM Thank you for your interest business financing from the NC Rural Center, a non-profit organization focused on self-employment, business creation and economic independence for the

LOAN CO-APPLICANT FORM Thank you for your interest business financing from the NC Rural Center, a non-profit organization focused on self-employment, business creation and economic independence for the

Your Credit. Objectives. An Introduction to Personal Credit. By the end of this presentation you will have a understanding of: 1/19/2016.

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

Presented by SCOTT TRANSUE

Presented by SCOTT TRANSUE Cash vs. accrual Key definitions Balance sheets Income statements Cash flow statements Break-even analysis Today s Agenda Ratios Recognizes transactions when they occur Recognizes

Presented by SCOTT TRANSUE Cash vs. accrual Key definitions Balance sheets Income statements Cash flow statements Break-even analysis Today s Agenda Ratios Recognizes transactions when they occur Recognizes

BUSINESS TOOLS. How Lending Decisions Are Made. How the Five Cs of Credit are used

Every lending institution has a set of credit standards or guidelines that are used to analyze and approve loans. At Northwest Farm Credit Services, these guidelines ensure constructive credit to help

Every lending institution has a set of credit standards or guidelines that are used to analyze and approve loans. At Northwest Farm Credit Services, these guidelines ensure constructive credit to help

Understanding Where You Stand

SMALL BUSINESS Access to Opportunity Understanding Where You Stand A Simple Guide to Your Company s Financial Statements Reading Your Statements Balance Sheets Income Statements Ratios Cash Flow Statements

SMALL BUSINESS Access to Opportunity Understanding Where You Stand A Simple Guide to Your Company s Financial Statements Reading Your Statements Balance Sheets Income Statements Ratios Cash Flow Statements

condition & operating results in a condensed form. Financial statements are used as a

2.1 FINANCIAL ANALYSIS Financial statements are formal records of the financial activities of a business, person or other entity and provide an overview of a business or person s financial condition in

2.1 FINANCIAL ANALYSIS Financial statements are formal records of the financial activities of a business, person or other entity and provide an overview of a business or person s financial condition in

Ratio Analysis for Financial Planning and Management (Relevant to PBE Paper II Management Accounting and Finance)

") Ratio Analysis for Financial Planning and Management (Relevant to PBE Paper II Management Accounting and Finance) Dr Fong Chun Cheong, Steve, School of Business, Macao Polytechnic Institute Introduction

Ratio Analysis for Financial Planning and Management (Relevant to PBE Paper II Management Accounting and Finance) Dr Fong Chun Cheong, Steve, School of Business, Macao Polytechnic Institute Introduction

Online Consumer Lending Training Program

in partnership with Online Consumer Lending Training Program We offer you a low-cost effective, customizable and comprehensive online consumer lending program that provides the core skills necessary to

in partnership with Online Consumer Lending Training Program We offer you a low-cost effective, customizable and comprehensive online consumer lending program that provides the core skills necessary to

CEE National Standards for Financial Literacy

Episode 101 What Is a Biz Kid? Episode 102 What Is Money? Episode 103 How Do You Get Money? Episode 104 What Can You Do with Money? Episode 105 Money Moves Episode 106 Taking Charge of Your Financial Future

Episode 101 What Is a Biz Kid? Episode 102 What Is Money? Episode 103 How Do You Get Money? Episode 104 What Can You Do with Money? Episode 105 Money Moves Episode 106 Taking Charge of Your Financial Future

where you stand A Simple Guide to Your Company s

UNDERSTANDING where you stand A Simple Guide to Your Company s Financial Statements SMALL BUSINESS DEVELOPMENT CENTER OF HAMPTON ROADS, INC. Where business comes to talk business. HAMPTON ROADS CHAMBER

UNDERSTANDING where you stand A Simple Guide to Your Company s Financial Statements SMALL BUSINESS DEVELOPMENT CENTER OF HAMPTON ROADS, INC. Where business comes to talk business. HAMPTON ROADS CHAMBER

Section 7 Credit risk analysis

Section 7 Credit risk analysis A man goes bankrupt gradually, then suddenly. --Ernst Hemingway 1 Learning objectives After studying this chapter, you will understand A typical process of the financial

Section 7 Credit risk analysis A man goes bankrupt gradually, then suddenly. --Ernst Hemingway 1 Learning objectives After studying this chapter, you will understand A typical process of the financial

Rural Loan Financial Indicator Ratios

Rural Loan Financial Indicator Ratios The parameters used in loan analysis describe and compare the situation of a business or project. None in itself is complete but when several are used together, they

Rural Loan Financial Indicator Ratios The parameters used in loan analysis describe and compare the situation of a business or project. None in itself is complete but when several are used together, they

Unit 3: Analysis of Financial Statements (marks=12) Contents mapping:

Contents mapping:") I Unit 3: Analysis of Financial Statements (marks=12) Contents mapping: Financial statements of a company: Statement of Profit and Loss and Balance Sheet in the prescribed form with major headings and

I Unit 3: Analysis of Financial Statements (marks=12) Contents mapping: Financial statements of a company: Statement of Profit and Loss and Balance Sheet in the prescribed form with major headings and

Using Credit Wisely: Curves Ahead

Using Credit Wisely: Curves Ahead What we will cover Types of credit Ownership of credit accounts Credit terms Guidelines for using credit Using credit means greater cost Establishing credit What we will

Using Credit Wisely: Curves Ahead What we will cover Types of credit Ownership of credit accounts Credit terms Guidelines for using credit Using credit means greater cost Establishing credit What we will

Training Manual: The Basics of Financing Agriculture

Training Manual: The Basics of Financing Agriculture Module 3.3 Management Techniques I - Cross-checking Module 3.3 Management Techniques I - Cross-checking Acknowledgement The Agriculture Finance Training

Training Manual: The Basics of Financing Agriculture Module 3.3 Management Techniques I - Cross-checking Module 3.3 Management Techniques I - Cross-checking Acknowledgement The Agriculture Finance Training

Financial Statements, Forecasts, and Planning Chapter 6

C H A P T E R 6 Financial Statements, Forecasts, and Planning Chapter 6 Chapter Objectives Identify the elements of the balance sheet. Identify the elements of the income statement. Discuss the cash flow

C H A P T E R 6 Financial Statements, Forecasts, and Planning Chapter 6 Chapter Objectives Identify the elements of the balance sheet. Identify the elements of the income statement. Discuss the cash flow

Advantages & Disadvantages to Using Credit

Advantages & Disadvantages to Using Credit Advantages to Using Credit Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing cheques Consolidates

Advantages & Disadvantages to Using Credit Advantages to Using Credit Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing cheques Consolidates

Glossary of Financial Terms for Nonprofits

Glossary of Financial Terms for Nonprofits A Accounts payable The amount owed to others for services or merchandise received by the organization. Accounts receivable The amount owed to the organization

Glossary of Financial Terms for Nonprofits A Accounts payable The amount owed to others for services or merchandise received by the organization. Accounts receivable The amount owed to the organization

Sanford C. Bernstein Fund, Inc. California Municipal Portfolio Ticker: California Municipal Class SNCAX

Global Wealth Management AunitofAllianceBernsteinL.P. SUMMARY PROSPECTUS January 31, 2013 Sanford C. Bernstein Fund, Inc. Municipal Portfolio Ticker: SNCAX Before you invest, you may want to review the

Global Wealth Management AunitofAllianceBernsteinL.P. SUMMARY PROSPECTUS January 31, 2013 Sanford C. Bernstein Fund, Inc. Municipal Portfolio Ticker: SNCAX Before you invest, you may want to review the

An analysis of fiscal 2013

2014 Operating Cost Benchmark Report An analysis of fiscal 2013 Prepared by Profit Planning Group Contents Introduction... 1 Executive Summary Overview of Results... 2 Results Summary... 3 Graphical Analysis...

2014 Operating Cost Benchmark Report An analysis of fiscal 2013 Prepared by Profit Planning Group Contents Introduction... 1 Executive Summary Overview of Results... 2 Results Summary... 3 Graphical Analysis...

FINANCIAL RATIOS. LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1. Current Liabilities SAMPLE BALANCE SHEET ASSETS

You want current and quick ratios to be > 1. Current Liabilities SAMPLE BALANCE SHEET ASSETS") FINANCIAL RATIOS ROUND ALL ANSWERS TO TWO DECIMALS UNLESS REQUESTED OTHERWISE IN THE PROBLEM LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1 Current Ratio Quick Ratio

FINANCIAL RATIOS ROUND ALL ANSWERS TO TWO DECIMALS UNLESS REQUESTED OTHERWISE IN THE PROBLEM LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1 Current Ratio Quick Ratio

BUSINESS PLANNING FINANCIAL INFORMATION

BUSINESS PLANNING FINANCIAL INFORMATION Note: There are downloadable templates for each of the tables shown provided on the SCORE website. Visit http://www.sanluisobispo.score.org and click on Templates

BUSINESS PLANNING FINANCIAL INFORMATION Note: There are downloadable templates for each of the tables shown provided on the SCORE website. Visit http://www.sanluisobispo.score.org and click on Templates

FINANCIAL RATIOS 2 Page 1 of 5. The following is information concerning ABC Company and XYZ Company.

FINANCIAL RATIOS 2 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 22,600 42,800 Accounts and Notes Receivable 92,500 101,100

FINANCIAL RATIOS 2 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 22,600 42,800 Accounts and Notes Receivable 92,500 101,100

FINANCIAL RATIOS 3 Page 1 of 5. The following is information concerning ABC Company and XYZ Company.

FINANCIAL RATIOS 3 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 18,700 33,000 Accounts and Notes Receivable 43,000 59,800

FINANCIAL RATIOS 3 Page 1 of 5 The following is information concerning ABC Company and XYZ Company. ABC Company XYZ Company CURRENT ASSETS: Cash 18,700 33,000 Accounts and Notes Receivable 43,000 59,800

GE20803 DEPOSIT & FINANCING OPERATION OF ISLAMIC BANKING

GE20803 DEPOSIT & FINANCING OPERATION OF ISLAMIC BANKING DEPOSIT MOBILIZATION BY ISLAMIC BANKS Updated version 21st October 2015 BY DR. HANUDIN AMIN LABUAN FACULTY OF INTERNATIONAL FINANCE UNIVERSITI MALAYSIA

GE20803 DEPOSIT & FINANCING OPERATION OF ISLAMIC BANKING DEPOSIT MOBILIZATION BY ISLAMIC BANKS Updated version 21st October 2015 BY DR. HANUDIN AMIN LABUAN FACULTY OF INTERNATIONAL FINANCE UNIVERSITI MALAYSIA

Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international financial statements.

Principles of Managerial Finance, 12e (Gitman) Chapter 2 Financial Statements and Analysis Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international

Principles of Managerial Finance, 12e (Gitman) Chapter 2 Financial Statements and Analysis Learning Goal 1: Review the contents of the stockholders' report and the procedures for consolidating international

Assessment: Career Path Interview. Preparing for Higher Education Planning for Higher Education Paying for Higher Education. Applying for a Job

Aligned with the Take Charge Today Advanced Level lesson plans. Advanced Level Course Intro. Money in your Life Financial Decisions Setting Financial Goals Assessment: A Collage of My Life Introduction

Aligned with the Take Charge Today Advanced Level lesson plans. Advanced Level Course Intro. Money in your Life Financial Decisions Setting Financial Goals Assessment: A Collage of My Life Introduction

Disciplined thinking focuses inspiration rather than constricts it. ~ Anonymous

Ratio Analysis Disciplined thinking focuses inspiration rather than constricts it. ~ Anonymous Ratio Analysis compares significant numbers from your financial statements. Rather than focusing on specific

Ratio Analysis Disciplined thinking focuses inspiration rather than constricts it. ~ Anonymous Ratio Analysis compares significant numbers from your financial statements. Rather than focusing on specific

13.1. Reading a Credit Report EXERCISE. THEME 4 Lesson 13: Applying for Credit NAME: CLASS PERIOD:

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

HSC Business Studies. Published Jul 2, BAND 6 HSC BUSINESS STD NOTES. By Tanya (97 ATAR)

") HSC Business Studies Year 2016 Mark 90.00 Pages 200 Published Jul 2, 2017 2016 BAND 6 HSC BUSINESS STD NOTES By Tanya (97 ATAR) Your notes author, Tanya. Tanya achieved an ATAR of 97 in 2016 while attending

HSC Business Studies Year 2016 Mark 90.00 Pages 200 Published Jul 2, 2017 2016 BAND 6 HSC BUSINESS STD NOTES By Tanya (97 ATAR) Your notes author, Tanya. Tanya achieved an ATAR of 97 in 2016 while attending

ANSWERS TO END-OF-CHAPTER QUESTIONS

ANSWERS TO END-OF-CHAPTER QUESTIONS 8/6/12 13.1 a. Financial statement analysis, which focuses on the data contained in a business s financial statements, is designed to assess the financial condition

ANSWERS TO END-OF-CHAPTER QUESTIONS 8/6/12 13.1 a. Financial statement analysis, which focuses on the data contained in a business s financial statements, is designed to assess the financial condition

Credit and Credit Cards

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

The ABC s of Borrowing Money

THE ABC'S OF BORROWING MONEY Legal Disclaimer: While all attempts have been made to verify information provided in this publication, neither the Author nor the Publisher assumes any responsibility for

THE ABC'S OF BORROWING MONEY Legal Disclaimer: While all attempts have been made to verify information provided in this publication, neither the Author nor the Publisher assumes any responsibility for

Chapter 021 Credit and Inventory Management

Multiple Choice Questions 1. The conditions under which a firm sells its goods and services for cash or credit are called the: A. terms of sale. b. credit analysis. c. collection policy. d. payables policy.

Multiple Choice Questions 1. The conditions under which a firm sells its goods and services for cash or credit are called the: A. terms of sale. b. credit analysis. c. collection policy. d. payables policy.

CASH, CREDIT & COLLECTION MANAGEMENT: THE LIFE BLOOD OF THE BUSINESS. Presented by: Osburn & Associates, LLC

CASH, CREDIT & COLLECTION MANAGEMENT: THE LIFE BLOOD OF THE BUSINESS Presented by: Osburn & Associates, LLC DAVID L. OSBURN, MBA, CCRA David Osburn, is the founder of Osburn & Associates, LLC that specializes

CASH, CREDIT & COLLECTION MANAGEMENT: THE LIFE BLOOD OF THE BUSINESS Presented by: Osburn & Associates, LLC DAVID L. OSBURN, MBA, CCRA David Osburn, is the founder of Osburn & Associates, LLC that specializes

Week-2 FINC Analysis of Financial Statements. Balance Sheets

Dr. Ahmed FINC 5000 Week-2 Name Analysis of Financial Statements Balance Sheets Assets 2003 2004 2005e Cash $ 9,000 $ 7,282 $ 14,000 Short-Term Investments. 48,600 20,000 71,632 Accounts Receivable 351,200

Dr. Ahmed FINC 5000 Week-2 Name Analysis of Financial Statements Balance Sheets Assets 2003 2004 2005e Cash $ 9,000 $ 7,282 $ 14,000 Short-Term Investments. 48,600 20,000 71,632 Accounts Receivable 351,200

MODULE J: SMART CHOICES FOR MANAGING CREDIT

MODULE J: SMART CHOICES FOR MANAGING CREDIT 1 Common Sense Economics ~ What Everyone Should Know About Wealth and Prosperity http://commonsenseeconomics.com/ Turn on the learning light! CREDIT, FINANCIAL

MODULE J: SMART CHOICES FOR MANAGING CREDIT 1 Common Sense Economics ~ What Everyone Should Know About Wealth and Prosperity http://commonsenseeconomics.com/ Turn on the learning light! CREDIT, FINANCIAL

1. Determinants of Capital Structure of a Firm

1. Determinants of Capital Structure of a Firm There are numerous factors, both qualitative and quantitative, including the subjective judgment, of financial managers which conjointly determine a firm

1. Determinants of Capital Structure of a Firm There are numerous factors, both qualitative and quantitative, including the subjective judgment, of financial managers which conjointly determine a firm

Bought to you by AS- Level Accounting Unit 2 Revision Notes

A-PDF Watermark DEMO: Purchase from www.a-pdf.com to remove the watermark for more notes visit Bought to you by AS- Level Accounting Unit 2 Revision Notes Types of Business Organisation: Sole Traders:

A-PDF Watermark DEMO: Purchase from www.a-pdf.com to remove the watermark for more notes visit Bought to you by AS- Level Accounting Unit 2 Revision Notes Types of Business Organisation: Sole Traders:

Welcome. 1. Agenda. 2. Ground Rules. 3. Introductions. Charge It Right 2

Charge It Right Welcome 1. Agenda 2. Ground Rules 3. Introductions Charge It Right 2 Objectives Define credit Explain why credit is important Identify the factors creditors look for when making credit

Charge It Right Welcome 1. Agenda 2. Ground Rules 3. Introductions Charge It Right 2 Objectives Define credit Explain why credit is important Identify the factors creditors look for when making credit

Financial Management Masters of Business Administration Study Notes & Tutorial Questions Chapter 7: Analysis & Interpretation of Financial Statement

Financial Management Masters of Business Administration Study Notes & Tutorial Questions Chapter 7: Analysis & Interpretation of Financial 1 INTRODUCTION Financial statement is a data summary on asset,

Financial Management Masters of Business Administration Study Notes & Tutorial Questions Chapter 7: Analysis & Interpretation of Financial 1 INTRODUCTION Financial statement is a data summary on asset,

Business Finance Bachelors of Business Study Notes & Tutorial Questions Chapter 5: Financial Analysis

Business Finance Bachelors of Business Study Notes & Tutorial Questions Chapter 5: Financial Analysis 1 INTRODUCTION Chapter 5: Financial Analysis 2018 Financial statement is a data summary on asset, liability

Business Finance Bachelors of Business Study Notes & Tutorial Questions Chapter 5: Financial Analysis 1 INTRODUCTION Chapter 5: Financial Analysis 2018 Financial statement is a data summary on asset, liability

STATEMENT OF FINANCIAL POSITION ADVANCED LEVEL

STATEMENT OF FINANCIAL POSITION ADVANCED LEVEL WHO IS WEALTHIER? Ian Mitchell Income - $30,000 Income - $85,000 Net Worth - $50,000 Net Worth - $35,000 Let s learn more to answer this question! Take Charge

STATEMENT OF FINANCIAL POSITION ADVANCED LEVEL WHO IS WEALTHIER? Ian Mitchell Income - $30,000 Income - $85,000 Net Worth - $50,000 Net Worth - $35,000 Let s learn more to answer this question! Take Charge

Borrowing. Evaluating the Benefits and Costs of Credit

Unit 9 Borrowing Lesson 9B: Evaluating the Benefits and Costs of Credit Rule 9: Pay on time and in full. While borrowing has both benefits and costs, at times it is an indication that something has gone

Unit 9 Borrowing Lesson 9B: Evaluating the Benefits and Costs of Credit Rule 9: Pay on time and in full. While borrowing has both benefits and costs, at times it is an indication that something has gone

Get ready for FRS 109: Classifying and measuring financial instruments. July 2018

Get ready for FRS 109: Classifying and measuring financial instruments July 2018 Contents Preface 03 1 Overview of classification and measurement requirements 04 2 The business model test 06 2.1 Determining

Get ready for FRS 109: Classifying and measuring financial instruments July 2018 Contents Preface 03 1 Overview of classification and measurement requirements 04 2 The business model test 06 2.1 Determining

Advanced Leveraged Buyouts and LBO Models Quiz Questions

Advanced Leveraged Buyouts and LBO Models Quiz Questions Types of Debt Transaction and Operating Assumptions Sources & Uses Pro-Forma Balance Sheet Adjustments Debt Schedules Linking and Modifying the

Advanced Leveraged Buyouts and LBO Models Quiz Questions Types of Debt Transaction and Operating Assumptions Sources & Uses Pro-Forma Balance Sheet Adjustments Debt Schedules Linking and Modifying the

Georgia Banking School Financial Statement Analysis. Dr. Christopher R Pope Terry College of Business University of Georgia

Georgia Banking School Financial Statement Analysis Dr. Christopher R Pope Terry College of Business University of Georgia Introduction Objective My objective is to introduce you to the analysis of financial

Georgia Banking School Financial Statement Analysis Dr. Christopher R Pope Terry College of Business University of Georgia Introduction Objective My objective is to introduce you to the analysis of financial

Chap 14. Evaluating Financial Viability

Chap 14. Evaluating Financial Viability Dr. Jack M. Wilson Distinguished Professor of Higher Education, Emerging Technologies, and Innovation Financial Management Key Questions How are we doing? Are we

Chap 14. Evaluating Financial Viability Dr. Jack M. Wilson Distinguished Professor of Higher Education, Emerging Technologies, and Innovation Financial Management Key Questions How are we doing? Are we

Financial statements aim at providing financial

Accounting Ratios 5 LEARNING OBJECTIVES After studying this chapter, you will be able to : Explain the meaning, objectives and limitations of analysis using accounting ratios; Identify the various types

Accounting Ratios 5 LEARNING OBJECTIVES After studying this chapter, you will be able to : Explain the meaning, objectives and limitations of analysis using accounting ratios; Identify the various types

Personal Credit Fundamentals &

Personal Credit Fundamentals & Your Credit Score Presented by: Harvard University Employees Credit Union Harvard Student Sources of Financial Education Sources of consumer finance education Formal Program

Personal Credit Fundamentals & Your Credit Score Presented by: Harvard University Employees Credit Union Harvard Student Sources of Financial Education Sources of consumer finance education Formal Program

Presented by Dr. Rebecca Neumann for Academic Staff

April 21, 2017 Presented by Dr. Rebecca Neumann for Academic Staff University of Wisconsin Milwaukee Mind your Money, Mind your Future Goals for today: Basic money management skills Tracking expenses Budgeting

April 21, 2017 Presented by Dr. Rebecca Neumann for Academic Staff University of Wisconsin Milwaukee Mind your Money, Mind your Future Goals for today: Basic money management skills Tracking expenses Budgeting

2018 Edition CPA. Preparatory Program. Business Environment and Concepts. Sample Chapters: Working Capital & Activity-Based Costing

2018 Edition CPA Preparatory Program Business Environment and Concepts Sample Chapters: Working Capital & Activity-Based Costing Brian Hock, CMA, CIA and Lynn Roden, CMA HOCK international, LLC P.O. Box

2018 Edition CPA Preparatory Program Business Environment and Concepts Sample Chapters: Working Capital & Activity-Based Costing Brian Hock, CMA, CIA and Lynn Roden, CMA HOCK international, LLC P.O. Box

Credit and Going into Debt A. What is credit?

Lesson 4 standards E.6.1 Explain the basic functions of money. E.6.2 Identify the composition of the money supply of the United States. E.6.3 Explain the roles of financial institutions. E.6.6 Explain

Lesson 4 standards E.6.1 Explain the basic functions of money. E.6.2 Identify the composition of the money supply of the United States. E.6.3 Explain the roles of financial institutions. E.6.6 Explain

BBPW3203 FINANCIAL MANAGEMENT II. Topic 1 Short-term Financing

BBPW3203 FINANCIAL MANAGEMENT II Topic 1 Short-term Financing January 2018 Content 1.1 Short-term financing 1.2 Current assets financing policy 1.3 Advantages and disadvantages of short-term financing

BBPW3203 FINANCIAL MANAGEMENT II Topic 1 Short-term Financing January 2018 Content 1.1 Short-term financing 1.2 Current assets financing policy 1.3 Advantages and disadvantages of short-term financing

FINANCE WITHOUT FEAR. Japanese automakers, 164, 214 Just-in-time inventory, 164, 214. Historical cost, 93, 100 Home equity, 286

A Accounting estimates, 54, 66 Accounting period, 75, 120 Accounting rules, 47 accrual accounting, 63 cost of goods sold. 64 depreciation, 93 examples, 75 interest, 59 plant, property and equipment, 93

A Accounting estimates, 54, 66 Accounting period, 75, 120 Accounting rules, 47 accrual accounting, 63 cost of goods sold. 64 depreciation, 93 examples, 75 interest, 59 plant, property and equipment, 93

Credit Assessment in Determining The Feasibility of Debtors Using Profile Matching

International Journal of Business and Management Invention ISSN (Online): 2319 8028, ISSN (Print): 2319 801X Volume 6 Issue 1 January. 2017 PP 73-79 Credit Assessment in Determining The Feasibility of

International Journal of Business and Management Invention ISSN (Online): 2319 8028, ISSN (Print): 2319 801X Volume 6 Issue 1 January. 2017 PP 73-79 Credit Assessment in Determining The Feasibility of

WORKING CAPITAL ANALYSIS OF SELECT CEMENT COMPANIES IN INDIA

CHAPTER - IV WORKING CAPITAL ANALYSIS OF SELECT CEMENT COMPANIES IN INDIA CHAPTER IV WORKING CAPITAL ANALYSIS OF SELECT CEMENT COMPANIES IN INDIA In this chapter an attempt has been made to analyse the

CHAPTER - IV WORKING CAPITAL ANALYSIS OF SELECT CEMENT COMPANIES IN INDIA CHAPTER IV WORKING CAPITAL ANALYSIS OF SELECT CEMENT COMPANIES IN INDIA In this chapter an attempt has been made to analyse the

CONSOLIDATED ANNUAL REPORT. Fleetwood. Bank Corporation. What you want your bank to be

2016 CONSOLIDATED ANNUAL REPORT Fleetwood Bank Corporation & What you want your bank to be CORPORATE MISSION STATEMENT Our educated and motivated team will become the leading provider of financial services

2016 CONSOLIDATED ANNUAL REPORT Fleetwood Bank Corporation & What you want your bank to be CORPORATE MISSION STATEMENT Our educated and motivated team will become the leading provider of financial services

Credit Cards. The Language of Credit. Student Loans. Installment Loans 12/14/2016

Quick Response Explain how you think credit cards work. How much do you have to pay every month? What happens if you pay late? What kinds of fees are involved? Unit 4 - Good Debt, Bad Debt: Using Credit

Quick Response Explain how you think credit cards work. How much do you have to pay every month? What happens if you pay late? What kinds of fees are involved? Unit 4 - Good Debt, Bad Debt: Using Credit

Essential Standard Understand business credit and risk management.

Essential Standard 5.00 Understand business credit and risk management. 1 Objective 5.01 Understand credit management 2 3 Topics Main types of credit Common advantages and disadvantages of businesses using

Essential Standard 5.00 Understand business credit and risk management. 1 Objective 5.01 Understand credit management 2 3 Topics Main types of credit Common advantages and disadvantages of businesses using

Financial ABV. Accredited in Business Valuation (ABV) Download Full Version :

Download Full Version :") Financial ABV Accredited in Business Valuation (ABV) Download Full Version : http://killexams.com/pass4sure/exam-detail/abv QUESTION: 319 deals with the liquidation of the subject business ownership interest.

Financial ABV Accredited in Business Valuation (ABV) Download Full Version : http://killexams.com/pass4sure/exam-detail/abv QUESTION: 319 deals with the liquidation of the subject business ownership interest.

Exercises Corporate Finance

Exercises Financial Accounting I) Consider the following business case. Prepare the financial statements (balance sheet, income statement, cash flow statement) for the year 01. You decide to open a beverage

Exercises Financial Accounting I) Consider the following business case. Prepare the financial statements (balance sheet, income statement, cash flow statement) for the year 01. You decide to open a beverage

Maximizing Purchasing Power: Make the Most of Your Credit Score

When life happens... Maximizing Purchasing Power: Make the Most of Your Credit Score Consolidated Credit Counseling Services, Inc. 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 How

When life happens... Maximizing Purchasing Power: Make the Most of Your Credit Score Consolidated Credit Counseling Services, Inc. 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 How

Gary A. Hachfeld, David B. Bau, & C. Robert Holcomb, Extension Educators

Balance Sheet Agricultural Business Management Gary A. Hachfeld, David B. Bau, & C. Robert Holcomb, Extension Educators Financial Management Series #1 6/2017 A complete set of financial statements for

Balance Sheet Agricultural Business Management Gary A. Hachfeld, David B. Bau, & C. Robert Holcomb, Extension Educators Financial Management Series #1 6/2017 A complete set of financial statements for

FINANCIAL STATEMENTS ANALYSIS - AN INTRODUCTION

Financial Statements Analysis - An Introduction 27 FINANCIAL STATEMENTS ANALYSIS - AN INTRODUCTION You have already learnt about the preparation of financial statements i.e. Balance Sheet and Trading and

Financial Statements Analysis - An Introduction 27 FINANCIAL STATEMENTS ANALYSIS - AN INTRODUCTION You have already learnt about the preparation of financial statements i.e. Balance Sheet and Trading and

The Basics. What Is a Mortgage? What Does My Mortgage Payment Include? Mortgage Payment Breakdown

The Basics What Is a Mortgage? A mortgage is a loan secured by real estate. In other words, in return for the funds necessary to purchase a home, a lender gets your promise to pay back the funds over a

The Basics What Is a Mortgage? A mortgage is a loan secured by real estate. In other words, in return for the funds necessary to purchase a home, a lender gets your promise to pay back the funds over a

MGT201 - Financial Management FAQs By

MGT201 - Financial Management FAQs By Explain me in detail with example what is "double taxation"? Answer: Double taxation occurs when tax is paid more than once on the same taxable income or asset. For

MGT201 - Financial Management FAQs By Explain me in detail with example what is "double taxation"? Answer: Double taxation occurs when tax is paid more than once on the same taxable income or asset. For

LESSON 6 RATIO ANALYSIS CONTENTS

LESSON 6 RATIO ANALYSIS CONTENTS 6.0 Aims and Objectives 6.1 Introduction 6.2 Definition 6.3 How the Accounting Ratios are Expressed? 6.4 Purpose, Utility & Limitations of Ratio Analysis 6.5 Classification

LESSON 6 RATIO ANALYSIS CONTENTS 6.0 Aims and Objectives 6.1 Introduction 6.2 Definition 6.3 How the Accounting Ratios are Expressed? 6.4 Purpose, Utility & Limitations of Ratio Analysis 6.5 Classification

MODULE 4 // HOW CREDITWORTHY ARE YOU? HALL OF FAME: AGES 18+

MODULE 4 // HOW CREDITWORTHY ARE YOU? HALL OF FAME: AGES 18+ MODULE 4 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial management

MODULE 4 // HOW CREDITWORTHY ARE YOU? HALL OF FAME: AGES 18+ MODULE 4 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial management

Eurasia: Economics & Business, 11(17), November 2018 DOI

, November 2018 DOI") UDC 334 COMPANY S FINANCIAL PERFORMANCE ANALYSIS BY USING DUPONT SYSTEM METHOD AT PHARMACEUTICAL COMPANY LISTED ON INDONESIA STOCK EXCHANGE: A STUDY AT PT MERCK TBK OVER THE PERIOD 2012-2016 Husaini Achmad,

UDC 334 COMPANY S FINANCIAL PERFORMANCE ANALYSIS BY USING DUPONT SYSTEM METHOD AT PHARMACEUTICAL COMPANY LISTED ON INDONESIA STOCK EXCHANGE: A STUDY AT PT MERCK TBK OVER THE PERIOD 2012-2016 Husaini Achmad,

Capital Speedboat Session 2. Charting your way through troubling waters FARIN & Associates Inc. Agenda

Capital Speedboat 2013 - Session 2 Charting your way through troubling waters 1 Agenda Session 2 Defining Stress Tests Stress vs. Scenario Testing Sensitivity Testing Scenarios Silos Scenario Testing Building

Capital Speedboat 2013 - Session 2 Charting your way through troubling waters 1 Agenda Session 2 Defining Stress Tests Stress vs. Scenario Testing Sensitivity Testing Scenarios Silos Scenario Testing Building

CHAPTER 4. ANALYSIS AND INTERPRETATION OF DATA Ratio Analysis - Meaning of Ratio (A) Return on Investment Ratios

Return on Investment Ratios") CHAPTER 4 ANALYSIS AND INTERPRETATION OF DATA Ratio Analysis - Meaning of Ratio (A) Return on Investment Ratios - Concept of Return on Investment - Advantages of ROI - Limitations of ROI - Evaluation of

CHAPTER 4 ANALYSIS AND INTERPRETATION OF DATA Ratio Analysis - Meaning of Ratio (A) Return on Investment Ratios - Concept of Return on Investment - Advantages of ROI - Limitations of ROI - Evaluation of

P2.T6. Credit Risk Measurement & Management. Jonathan Golin and Philippe Delhaise, The Bank Credit Analysis Handbook

P2.T6. Credit Risk Measurement & Management Jonathan Golin and Philippe Delhaise, The Bank Credit Analysis Handbook Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com Golin,

P2.T6. Credit Risk Measurement & Management Jonathan Golin and Philippe Delhaise, The Bank Credit Analysis Handbook Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com Golin,

BRANCH OFFICE QUESTIONNAIRE

BRANCH OFFICE QUESTIONNAIRE Microfinance Due Diligence Questionnaire with Loan Application Name of the Institution. Country... Analyst:. TABLE OF CONTENTS A. General Questions... 3 B. Underwriting Process

BRANCH OFFICE QUESTIONNAIRE Microfinance Due Diligence Questionnaire with Loan Application Name of the Institution. Country... Analyst:. TABLE OF CONTENTS A. General Questions... 3 B. Underwriting Process

Strategic Management. Concepts and Cases. Strategic Management. Fred R. David Forest R. David

Strategic Management Concepts and Cases For these Global Editions, the editorial team at Pearson has collaborated with educators across the world to address a wide range of subjects and requirements, equipping

Strategic Management Concepts and Cases For these Global Editions, the editorial team at Pearson has collaborated with educators across the world to address a wide range of subjects and requirements, equipping

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Performance Measurement & the Planning & Control System The higher direction of an organization requires a clear

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Performance Measurement & the Planning & Control System The higher direction of an organization requires a clear

If you're like most Americans, owning your own home is a major

How the Fannie Mae Foundation can help. If you're like most Americans, owning your own home is a major part of the American dream. The Fannie Mae Foundation wants to help you understand the steps you have

How the Fannie Mae Foundation can help. If you're like most Americans, owning your own home is a major part of the American dream. The Fannie Mae Foundation wants to help you understand the steps you have

YOU ARE NOT ALONE Hello, my name is <name> and I m <title>.

So I know why you re here: I bet you ve got some questions about your money: what to do with it, how to make the most of it and how to hopefully get more of it. You ve got questions and the good news is

So I know why you re here: I bet you ve got some questions about your money: what to do with it, how to make the most of it and how to hopefully get more of it. You ve got questions and the good news is

Consolidated Financial Results April 1, 2009 June 30, 2009

Consolidated Financial Results April 1, 2009 June August 5, 2009 In preparing its consolidated financial information, ORIX Corporation and its subsidiaries have complied with accounting principles generally

Consolidated Financial Results April 1, 2009 June August 5, 2009 In preparing its consolidated financial information, ORIX Corporation and its subsidiaries have complied with accounting principles generally

P2.T6. Credit Risk Measurement & Management. Jonathan Golin and Philippe Delhaise, The Bank Credit Analysis Handbook

P2.T6. Credit Risk Measurement & Management Jonathan Golin and Philippe Delhaise, The Bank Credit Analysis Handbook Bionic Turtle FRM Study Notes Reading 42 By David Harper, CFA FRM CIPM www.bionicturtle.com

P2.T6. Credit Risk Measurement & Management Jonathan Golin and Philippe Delhaise, The Bank Credit Analysis Handbook Bionic Turtle FRM Study Notes Reading 42 By David Harper, CFA FRM CIPM www.bionicturtle.com

Risk Management for Non-Banking Financial Institutions

Risk Management for Non-Banking Financial Institutions Portfolio Approach Application for Leasing Companies Definition of Risk Risk is represented by the likelihood that the reality differs from initial

Risk Management for Non-Banking Financial Institutions Portfolio Approach Application for Leasing Companies Definition of Risk Risk is represented by the likelihood that the reality differs from initial

GENERAL FINANCING QUESTIONS

GENERAL FINANCING QUESTIONS 1. What is a Mortgage? Tips for Homebuyers Generally speaking, a mortgage is a loan obtained to purchase real estate. The "mortgage" itself is a lien (a legal claim) on the

GENERAL FINANCING QUESTIONS 1. What is a Mortgage? Tips for Homebuyers Generally speaking, a mortgage is a loan obtained to purchase real estate. The "mortgage" itself is a lien (a legal claim) on the

ANALYSIS OF FINANCIAL STATEMENTS

ANALYSIS OF FINANCIAL STATEMENTS 1. Basic concept of financial statement analysis 2. Liquidity ratios 3. Asset management ratios 4. Debt management ratios 5. Profitability ratios 6. Market value ratios

ANALYSIS OF FINANCIAL STATEMENTS 1. Basic concept of financial statement analysis 2. Liquidity ratios 3. Asset management ratios 4. Debt management ratios 5. Profitability ratios 6. Market value ratios

Quiz Bomb. Page 1 of 12

Page 1 of 12 Quiz Bomb Indicate whether the following statements are True or False. Support your answer with reason: 1. Public finance is the study of money management of individual. False. Public finance

Page 1 of 12 Quiz Bomb Indicate whether the following statements are True or False. Support your answer with reason: 1. Public finance is the study of money management of individual. False. Public finance

COMMUNITY SAVINGS BANCORP, INC. (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 (Mark One) FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 (Mark One) FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

Accounting Advance Certificate in Business Administration Study Notes & Practice Questions Chapter 2: Financial Ratios

Accounting Advance Certificate in Business Administration Study Notes & Practice Questions Chapter 2: Financial Ratios 1 INTRODUCTION Chapter 2: Financial Ratios 2014 Financial statement is a data summary

Accounting Advance Certificate in Business Administration Study Notes & Practice Questions Chapter 2: Financial Ratios 1 INTRODUCTION Chapter 2: Financial Ratios 2014 Financial statement is a data summary

Training Manual: The Basics of Financing Agriculture

Training Manual: The Basics of Financing Agriculture Module 2.1 Basics of the Balance Sheet Module 2.1 Basics of the Balance Sheet Acknowledgement The Agriculture Finance Training Manual is part of AgriFin

Training Manual: The Basics of Financing Agriculture Module 2.1 Basics of the Balance Sheet Module 2.1 Basics of the Balance Sheet Acknowledgement The Agriculture Finance Training Manual is part of AgriFin

READY, SET, GO FOR IT! Preparing For Your Financial Future COLLEGE BANC. Financial Literacy Workbook, Grades 9-12

READY, SET, GO FOR IT! Preparing For Your Financial Future COLLEGE BANC Financial Literacy Workbook, Grades 9-12 FINANCIAL PLANNING Financial planning is about defining and following a set of steps in

READY, SET, GO FOR IT! Preparing For Your Financial Future COLLEGE BANC Financial Literacy Workbook, Grades 9-12 FINANCIAL PLANNING Financial planning is about defining and following a set of steps in

CHAPTER - VI RATIO ANALYSIS 6.3 UTILITY OF RATIO ANALYSIS 6.4 LIMITATIONS OF RATIO ANALYSIS 6.5 RATIO TABLES, CHARTS, ANALYSIS AND

CHAPTER - VI RATIO ANALYSIS 6.1 INTRODUCTION 6.2 NATURE OF RATIO 6.3 UTILITY OF RATIO ANALYSIS 6.4 LIMITATIONS OF RATIO ANALYSIS 6.5 RATIO TABLES, CHARTS, ANALYSIS AND INTERPRETATION OF DIFFERENT RATIOS

CHAPTER - VI RATIO ANALYSIS 6.1 INTRODUCTION 6.2 NATURE OF RATIO 6.3 UTILITY OF RATIO ANALYSIS 6.4 LIMITATIONS OF RATIO ANALYSIS 6.5 RATIO TABLES, CHARTS, ANALYSIS AND INTERPRETATION OF DIFFERENT RATIOS

CHAPTER 7 ACCOUNTING FOR RECEIVABLES

CHAPTER 7 ACCOUNTING FOR RECEIVABLES Key Terms and Concepts to Know Accounts Receivable: Result from sales on account (credit sales), not cash sales. May also result from credit card sales if there is

CHAPTER 7 ACCOUNTING FOR RECEIVABLES Key Terms and Concepts to Know Accounts Receivable: Result from sales on account (credit sales), not cash sales. May also result from credit card sales if there is

FIRST BANK OF KENTUCKY CORPORATION Maysville, Kentucky. CONSOLIDATED FINANCIAL STATEMENTS December 31, 2016 and 2015

Maysville, Kentucky CONSOLIDATED FINANCIAL STATEMENTS Maysville, Kentucky CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL STATEMENTS CONSOLIDATED BALANCE SHEETS...

Maysville, Kentucky CONSOLIDATED FINANCIAL STATEMENTS Maysville, Kentucky CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL STATEMENTS CONSOLIDATED BALANCE SHEETS...

Introduction The Goals and Nature of Credit Analysis

Chapter 1 Introduction The Goals and Nature of Credit Analysis Credit analysis is an art, not a science. The goal of credit analysis is to make a judgment about an obligor s ability and willingness to

Chapter 1 Introduction The Goals and Nature of Credit Analysis Credit analysis is an art, not a science. The goal of credit analysis is to make a judgment about an obligor s ability and willingness to