The Consumer Financial Protection Bureau and Higher Education: What it means to you. March 12, 2013

|

|

|

- Alisha Boyd

- 6 years ago

- Views:

Transcription

1 The Consumer Financial Protection Bureau and Higher Education: What it means to you March 12,

2 Agenda CFPB Overview CFPB & Higher Ed CFPB & Your Business Partners 2

3 Introducing the CFPB 3

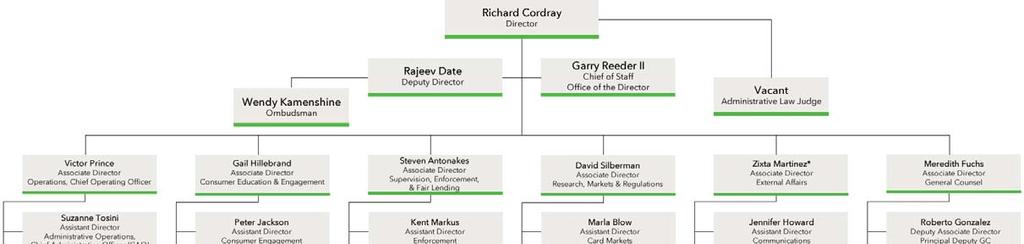

4 Key Players & Relationships Management Richard Cordray, Director Raj Date, Deputy Director Rohit Chopra, Assistant Director Students Holly Petraeus, Assistant Director Servicemember Affairs Relationships Department of Education Department of Treasury Department of Justice Veterans Affairs and Department of Defense 4

5 Role and Responsibilities CFPB established to protect consumers: Conduct rule making, supervision, and enforcement for Federal consumer financial protection laws Restrict unfair, deceptive, or abusive acts or practices Take consumer complaints Promote financial education Research consumer behavior Monitor financial markets for new risks to consumers Enforce laws that outlaw discrimination and other unfair treatment in consumer finance President Obama appointed Rich Cordray to be the first Director of the CFPB in Jan

6 Role and Responsibilities Not regulators of schools, but of financial institutions Seek to arm schools with better tools to evaluate financial institutions offerings When the school is a lender Partnerships with banks High cost private loans Advocating redefinition of disclosure requirements to include TVII (HHS) loans with federal loans 6

7 Statutes Title X Consumer Finance Protection Act of 2010 creates the CFPB Dodd Frank Wall Street Reform and Consumer Protection Act of enacted 7/21/12 Dodd Frank vests primary rulemaking and enforcement to the CFPB for the following eighteen federal consumer protection laws 7

8 Statutes Alternative Mortgage Transaction Parity Act of 1982 (12 U.S.C et seq.) Consumer Leasing Act of 1976 (15 U.S.C et seq.) Electronic Fund Transfer Act (15 U.S.C et seq.) except section 920 Equal Credit Opportunity Act (15 U.S.C et seq.) Fair Credit Billing Act (15 U.S.C et seq.) Fair Credit Reporting Act (15 U.S.C et seq.) except sections 615(e) and 628 of that Act (15 U.S.C. 1681m(e), 1681w) Fair Debt Collection Practices Act (15 U.S.C et seq.) 8

9 Statutes Subsections (b) through (f) of section 43 of the Federal Deposit Insurance Act (12 U.S.C. 1831t(c) (f)) Sections 502 through 509 of the Gramm Leach Bliley Act (15 U.S.C ) except for section 505 as it applies to section 501(b) Home Mortgage Disclosure Act of 1975 (12 U.S.C et seq.) Home Owners Protection Act of 1998 (12 U.S.C et seq.) Home Ownership and Equity Protection Act of 1994 (15 U.S.C note) Interstate Land Sales Full Disclosure Act (15 U.S.C. 1701) 9

10 Statutes Section 626 of the Omnibus Appropriations Act, 2009 (Public Law 111 8); Real Estate Settlement Procedures Act of 1974 (12 U.S.C et seq.); Secure and Fair Enforcement for Mortgage Licensing Act of 2008 (12 U.S.C et seq.); Truth in Lending Act (15 U.S.C et seq.); and Truth in Savings Act (12 U.S.C et seq.). 10

11 2013 Strategic Priorities Greater involvement in the private loan process Requiring school certification of ALL private loans Promote a culture of comparison shopping Financial education Research shows much of the financial literacy efforts are ineffective What is working? Servicing and collections 11

12 2013 Strategic Priorities Not a priority CFPB Examination of schools Requests for Information Section 1021 of the Dodd Frank Act charges the CFPB with collecting, researching, monitoring and publishing information about consumer financial products and services 12

13 CFPB Requests for Information Financial Products Marketed to Students Enrolled in Institutions of Higher Education Focus on campus affinity products Financial products and services that carry an endorsement (either explicit or implicit) or mark of an institution of higher education, e.g., one card student ID purchase cards; disbursement debit cards, etc. Not an investigation of any agreement or school, but a quest to understand how schools enter into these agreements Comments due on or before March 18,

14 CFPB Requests for Information Initiative to Promote Student Loan Affordability Focus on alternative repayment options for private student loan borrowers Concerns about PL debt impact on GDP growth Comments due on or before April 8,

15 CFPB & Higher Ed Resource and advocate vs. regulator Inform policy making Create tools for prospective borrowers Drive students and families to borrow less Address underutilized federal borrowing capacity 15

16 CFPB & Higher Ed 16

17 CFPB & Higher Ed 17

18 CFPB & Higher Ed 18

19 CFPB & Higher Ed 19

20 CFPB & Higher Ed 20

21 CFPB & Higher Ed 21

22 Financial Aid Shopping Sheet Estimated Cost of Attendance Grants and Scholarships Net Costs Work Options Loan Options Other Options

23 Annual Report of the CFPB Student Loan Ombudsman The CFPB received nearly 2,900 public private student loan complaints This is a relatively small number given that there are more than $150 billion in private student loans outstanding The vast majority of the complaints were related to loan servicing and loan modification issues Active duty service members and their families reported that they sometimes experience difficulty exercising their rights under the Service Members Civil Relief Act b4 Source:

24 Slide 23 b4 I recommend we try to avoid using full sentences on the slides bhoblitz, 1/23/2013

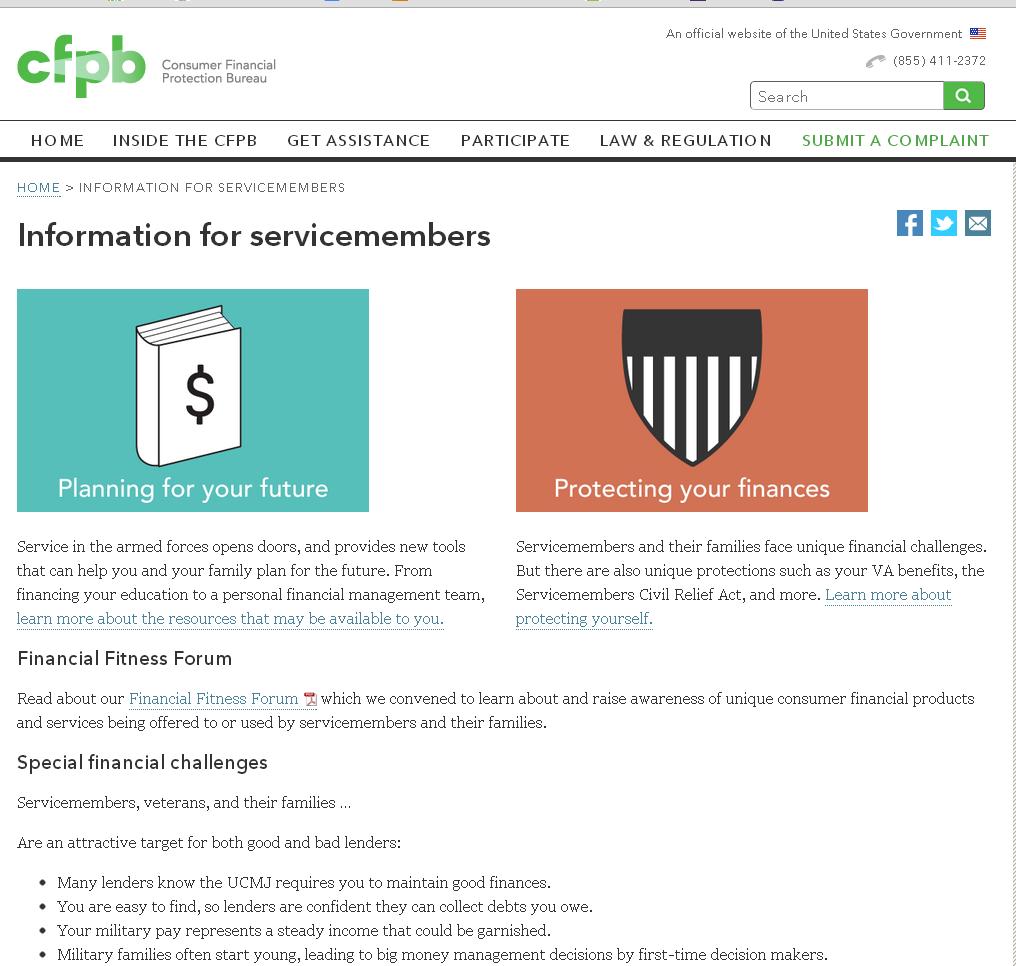

25 Servicemember Affairs Focus on Planning for Your Future & Protecting Your Finances Planning for Your Future Helping you save Dollars for degrees Protecting Your Finances Accessing your VA benefits Deployment and your credit card 24

26 Servicemember Affairs Financial Fitness Forum: September 2012 Learn about and raise awareness of unique military friendly products already being offered by financial institutions Start a dialogue between the financial services industry and the military services about how to best serve those who serve our country 25

27 Servicemember Affairs 26

28 Impacted Business Processes Private Loans Debit/Campus Cards Banking Collection Agencies

29 Private Loans Lender Requirements Statutory Regulatory Institutional Requirements TILA

30 Debit Cards Student Refunds Who issues cards Students accounts Fees Vendors and Issues

31 NACUBO s Best Practices: Debit Cards Keep Students First Encourage Students to Use Financial Institutions Offer Choices

32 NACUBO s Best Practices: Debit Cards Encourage Electronic Refunds Utilize a Competitive Process and Limit Exclusivity Engage Students in the Vendor Selection Process

33 NACUBO s Best Practices: Debit Cards Comply with Federal and State Regulations Negotiate Low or No Fee Options and Convenient Services for Students Avoid Unscrupulous Marketing Make Contracts Transparent

34 Banking Financial relationships/conditions in contracts. Impact on students/families Monopoly?

35 Collection Agencies CFPB requirements on third party debt collectors. Impact on colleges/universities. What you should look for?

36 Resources CFPB Website CFPB RFI: Alternative Repayment Options for Private Student Loan Borrowers CFPB RFI: Financial Products Marketed to Students the deal/request for informationregarding financial products marketed to students enrolled in institutions of highereducation/ Private Student Loan Report Updated 8/29/ student loans report/ Financial Aid Shopping Sheet: letter/ CFPB,_ED_Issue_Final_Version_of_Financial_Aid_Shopping_Sheet.aspx

37 Thank you for your time! Barbara Hoblitzell David Glezerman Betsy Burton-Strunk 36

Consumer Finance Protection Bureau. About this presentation. The CFPB 1/26/2012

Consumer Finance Protection Bureau Annual Conference Coalition of Higher Education Assistance Organizations John Dean Washington Partners, LLC January 2012 About this presentation This presentation is

Consumer Finance Protection Bureau Annual Conference Coalition of Higher Education Assistance Organizations John Dean Washington Partners, LLC January 2012 About this presentation This presentation is

Presentation to COHEAO

Presentation to COHEAO Rohit Chopra CFPB Student Loan Ombudsman July 30, 2012 Cleveland Consumer Financial Protection Bureau http://www.consumerfinance.gov Establishment of the CFPB In July 2010, the Dodd-Frank

Presentation to COHEAO Rohit Chopra CFPB Student Loan Ombudsman July 30, 2012 Cleveland Consumer Financial Protection Bureau http://www.consumerfinance.gov Establishment of the CFPB In July 2010, the Dodd-Frank

Consumer Financial Protection Bureau Update

Consumer Financial Protection Bureau Update Patricia Scherschel February 2016 Student Lending Program Manager Installment Lending and Collections Markets Division of Research, Markets, and Regulations

Consumer Financial Protection Bureau Update Patricia Scherschel February 2016 Student Lending Program Manager Installment Lending and Collections Markets Division of Research, Markets, and Regulations

CFPB Supervision and Examination Process

Background Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the Act) 1 established the Consumer Financial Protection Bureau (CFPB) and authorizes it to supervise certain

Background Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the Act) 1 established the Consumer Financial Protection Bureau (CFPB) and authorizes it to supervise certain

A Brief Overview of Actions Taken by the Consumer Financial Protection Bureau (CFPB) in Its First Year

in Its First Year") A Brief Overview of Actions Taken by the Consumer Financial Protection Bureau (CFPB) in Its First Year Sean M. Hoskins Analyst in Financial Economics August 29, 2012 CRS Report for Congress Prepared for

A Brief Overview of Actions Taken by the Consumer Financial Protection Bureau (CFPB) in Its First Year Sean M. Hoskins Analyst in Financial Economics August 29, 2012 CRS Report for Congress Prepared for

CFPB: A Review of Supervisory Activities

CFPB: A Review of Supervisory Activities Roberta Torian University of North Carolina Law School Center for Banking and Finance Banking Law Institute Charlotte, N.C. 22 March 2013 DRAFT v2 1 Authority The

CFPB: A Review of Supervisory Activities Roberta Torian University of North Carolina Law School Center for Banking and Finance Banking Law Institute Charlotte, N.C. 22 March 2013 DRAFT v2 1 Authority The

Examination Procedures

After completing the risk assessment and examination scoping, examiners should use these procedures, in conjunction with the compliance management system Exam Date: Exam ID No. Prepared By: Reviewer: Docket

After completing the risk assessment and examination scoping, examiners should use these procedures, in conjunction with the compliance management system Exam Date: Exam ID No. Prepared By: Reviewer: Docket

Preparing for a CFPB Examination or Investigation

Preparing for a CFPB Examination or Investigation Association of Credit Counseling Professionals Fall 2013 Conference November 14, 2013, 9:15 am 10:30 am ET Tampa, Florida Jonathan L. Pompan, Esq. Venable

Preparing for a CFPB Examination or Investigation Association of Credit Counseling Professionals Fall 2013 Conference November 14, 2013, 9:15 am 10:30 am ET Tampa, Florida Jonathan L. Pompan, Esq. Venable

What You Need to Know About the CFPB s Short-Term, Small- Dollar Lending Examination Procedures

What You Need to Know About the CFPB s Short-Term, Small- Dollar Lending Examination Procedures Richard P. Eckman Timothy R. McTaggart Pepper Hamilton LLP John C. Soffronoff, Jr. ICS Risk Advisors September

What You Need to Know About the CFPB s Short-Term, Small- Dollar Lending Examination Procedures Richard P. Eckman Timothy R. McTaggart Pepper Hamilton LLP John C. Soffronoff, Jr. ICS Risk Advisors September

Recent Developments: Consumer Financial Protection Bureau

Recent Developments: Consumer Financial Protection Bureau The Banking Institute University of North Carolina School of Law Center for Banking and Finance March 30, 2012 Reginald J. Brown Eric J. Mogilnicki

Recent Developments: Consumer Financial Protection Bureau The Banking Institute University of North Carolina School of Law Center for Banking and Finance March 30, 2012 Reginald J. Brown Eric J. Mogilnicki

CFPB Enforcement Actions

CFPB Enforcement Actions ABA LAMP Committee CLE New Orleans, LA November 5, 2015 Angela Martin Senior Enforcement Attorney Military Affairs Liaison Note: This document was used in support of a live discussion.

CFPB Enforcement Actions ABA LAMP Committee CLE New Orleans, LA November 5, 2015 Angela Martin Senior Enforcement Attorney Military Affairs Liaison Note: This document was used in support of a live discussion.

Table of Contents CLICK ANY TITLE TO GO DIRECTLY TO THAT SECTION. SUBTITLE A: Bureau of Consumer Financial Protection

Venable CFPB monitor Please contact our attorneys in our CFPB Task Force if you have any questions regarding this information. Table of Contents CLICK ANY TITLE TO GO DIRECTLY TO THAT SECTION Last updated

Venable CFPB monitor Please contact our attorneys in our CFPB Task Force if you have any questions regarding this information. Table of Contents CLICK ANY TITLE TO GO DIRECTLY TO THAT SECTION Last updated

CFPB Compliance Bulletin Date: July 31, 2017

1700 G Street NW, Washington, DC 20552 CFPB Compliance Bulletin 2017-01 Date: July 31, 2017 Subject: Phone Pay Fees The Consumer Financial Protection Bureau (CFPB or Bureau) issues this Compliance Bulletin

1700 G Street NW, Washington, DC 20552 CFPB Compliance Bulletin 2017-01 Date: July 31, 2017 Subject: Phone Pay Fees The Consumer Financial Protection Bureau (CFPB or Bureau) issues this Compliance Bulletin

Consumer Financial Protection Bureau

Consumer Financial Protection Bureau Opportunity Finance Network September 28, 2017 Disclaimer This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the

Consumer Financial Protection Bureau Opportunity Finance Network September 28, 2017 Disclaimer This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the

3/11/2013. Federal Trade Commission Section 5(a) of the Federal Trade Commission Act

of the Federal Trade Commission Act") Paul Huck, Partner, Hunton & Williams LLP Robert Clements, Senior Assistant Attorney General Office of Attorney General, State of Florida The Society of Corporate Compliance and Ethics 2013 South Atlantic

Paul Huck, Partner, Hunton & Williams LLP Robert Clements, Senior Assistant Attorney General Office of Attorney General, State of Florida The Society of Corporate Compliance and Ethics 2013 South Atlantic

The CFPB. What Lenders And Servicers Must Know. Joseph M. Welch, Esq.

The CFPB What Lenders And Servicers Must Know Jason E. Goldstein, Esq. 18400 Von Karman Avenue, Suite 800 Irvine, California 92612 0514 (949) 224 6235 jgoldstein@buchalter.com Joseph M. Welch, Esq. 18400

The CFPB What Lenders And Servicers Must Know Jason E. Goldstein, Esq. 18400 Von Karman Avenue, Suite 800 Irvine, California 92612 0514 (949) 224 6235 jgoldstein@buchalter.com Joseph M. Welch, Esq. 18400

STUDENT LOANS. Oversight of Servicemembers' Interest Rate Cap Could Be Strengthened

United States Government Accountability Office Report to Ranking Member, Committee on Homeland Security and Governmental Affairs, U.S. Senate November 2016 STUDENT LOANS Oversight of Servicemembers' Interest

United States Government Accountability Office Report to Ranking Member, Committee on Homeland Security and Governmental Affairs, U.S. Senate November 2016 STUDENT LOANS Oversight of Servicemembers' Interest

Testimony of Stephen Agostini Chief Financial Officer,

Testimony of Stephen Agostini Chief Financial Officer, Consumer Financial Protection Bureau Before the House Financial Services Committee, Subcommittee on Oversight and Investigation June 18, 2013 Thank

Testimony of Stephen Agostini Chief Financial Officer, Consumer Financial Protection Bureau Before the House Financial Services Committee, Subcommittee on Oversight and Investigation June 18, 2013 Thank

A Brief Overview of the CFPB

A Brief Overview of the CFPB May 2011 Tara Sugiyama Potashnik tspotashnik@venable.com 2008 Venable LLP 1 Overview How we ended up with the CFPB Who is covered by the CFPB How the CFPB is structured CFPB

A Brief Overview of the CFPB May 2011 Tara Sugiyama Potashnik tspotashnik@venable.com 2008 Venable LLP 1 Overview How we ended up with the CFPB Who is covered by the CFPB How the CFPB is structured CFPB

Mortgage Banking. Solutions in Compliance, Transactions, and Defense. Attorney Advertising

Mortgage Banking Solutions in Compliance, Transactions, and Defense Attorney Advertising The mortgage banking industry is changing rapidly. We offer broad regulatory experience, formidable skill in litigation,

Mortgage Banking Solutions in Compliance, Transactions, and Defense Attorney Advertising The mortgage banking industry is changing rapidly. We offer broad regulatory experience, formidable skill in litigation,

The CFPB s First Anniversary: A Look Back at What is has Accomplished and Where it is Headed December 13, 2012

The CFPB s First Anniversary: A Look Back at What is has Accomplished and Where it is Headed December 13, 2012 Alan S. Kaplinsky, Practice Leader Consumer Financial Services Group Ballard Spahr LLP 1735

The CFPB s First Anniversary: A Look Back at What is has Accomplished and Where it is Headed December 13, 2012 Alan S. Kaplinsky, Practice Leader Consumer Financial Services Group Ballard Spahr LLP 1735

Fair Lending TILA and RESPA Integrated Disclosures ( TRID ) and Consumer Financial Protection Bureau ( CFPB )

and Consumer Financial Protection Bureau ( CFPB )") Fair Lending TILA and RESPA Integrated Disclosures ( TRID ) and Consumer Financial Protection Bureau ( CFPB ) Presented by Anthony J. Sylvester, Esq. Craig L. Steinfeld, Esq. Sherman Wells Sylvester &

Fair Lending TILA and RESPA Integrated Disclosures ( TRID ) and Consumer Financial Protection Bureau ( CFPB ) Presented by Anthony J. Sylvester, Esq. Craig L. Steinfeld, Esq. Sherman Wells Sylvester &

SUMMARY: The Bureau is reissuing its guidance on service providers, formerly titled CFPB

Billing Code: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION Compliance Bulletin and Policy Guidance; 2016-02, Service Providers AGENCY: Bureau of Consumer Financial Protection. ACTION: Compliance Bulletin

Billing Code: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION Compliance Bulletin and Policy Guidance; 2016-02, Service Providers AGENCY: Bureau of Consumer Financial Protection. ACTION: Compliance Bulletin

CFPB Update. GCOR XI April 5, Operational Risk & The Risk Management. The Risk Management Association JOIN. ENGAGE. LEAD.

1 CFPB Update GCOR XI April 5, 2017 Edward J. DeMarco, Jr., General Counsel & Director W. Bernard Mason, Regulatory Relations Liaison -- Operational Risk & The Risk Management Regulatory Relations Association

1 CFPB Update GCOR XI April 5, 2017 Edward J. DeMarco, Jr., General Counsel & Director W. Bernard Mason, Regulatory Relations Liaison -- Operational Risk & The Risk Management Regulatory Relations Association

November Private Education Loan Ombudsman ( 1035) 4.2 Private Education Loans and Private Education Lenders

4.2 Private Education Loans and Private Education Lenders") This is the fourth in a series of user guides that will be published by Morrison & Foerster. The user guides provide an in depth discussion on specific topics raised by the Dodd-Frank Act. For our Dodd-Frank

This is the fourth in a series of user guides that will be published by Morrison & Foerster. The user guides provide an in depth discussion on specific topics raised by the Dodd-Frank Act. For our Dodd-Frank

RESPA/TILA Integration

RESPA/TILA Integration 1 Presented by: Richard Hogan, Vice President & Associate General Counsel Tracy Pandolfo, Director Agent Services Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

RESPA/TILA Integration 1 Presented by: Richard Hogan, Vice President & Associate General Counsel Tracy Pandolfo, Director Agent Services Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

Examination Procedures

Examination Procedures Education Loan Examination Procedures After completing the risk assessment and examination scoping, examiners should use these procedures to conduct an education loan examination.

Examination Procedures Education Loan Examination Procedures After completing the risk assessment and examination scoping, examiners should use these procedures to conduct an education loan examination.

2012 Winston & Strawn LLP

2012 Winston & Strawn LLP The CFPB: Current Enforcement Priorities and Investigation Readiness Brought to you by Winston & Strawn s Financial Services practice group 2012 Winston & Strawn LLP Today s elunch

2012 Winston & Strawn LLP The CFPB: Current Enforcement Priorities and Investigation Readiness Brought to you by Winston & Strawn s Financial Services practice group 2012 Winston & Strawn LLP Today s elunch

SUMMARY: The Bureau of Consumer Financial Protection (CFPB or Bureau) is publishing this agenda

is publishing this agenda") This document is scheduled to be published in the Federal Register on 06/09/2016 and available online at http://federalregister.gov/a/2016-12931, and on FDsys.gov BUREAU OF CONSUMER FINANCIAL PROTECTION

This document is scheduled to be published in the Federal Register on 06/09/2016 and available online at http://federalregister.gov/a/2016-12931, and on FDsys.gov BUREAU OF CONSUMER FINANCIAL PROTECTION

SEMI-ANNUAL REPORT OF THE BUREAU OF CONSUMER FINANCIAL PROTECTION HEARING CONTENTS: SEPTEMBER 29, 2015 COMPILED FROM:

SEPTEMBER 29, 2015 SEMI-ANNUAL REPORT OF THE BUREAU OF CONSUMER FINANCIAL PROTECTION UNITED STATES HOUSE OF REPRESENTATIVES, COMMITTEE ON FINANCIAL SERVICES ONE HUNDRED AND FOURTEENTH CONGRESS, FIRST SESSION

SEPTEMBER 29, 2015 SEMI-ANNUAL REPORT OF THE BUREAU OF CONSUMER FINANCIAL PROTECTION UNITED STATES HOUSE OF REPRESENTATIVES, COMMITTEE ON FINANCIAL SERVICES ONE HUNDRED AND FOURTEENTH CONGRESS, FIRST SESSION

Dodd-Frank Chapter X: The Consumer Financial Protection Bureau

Association of Corporate Counsel (ACC) Financial Services Committee Legal Quick Hit Lewis S. Wiener March 23, 2011 Dodd-Frank Chapter X: The Consumer Financial Protection Bureau The Consumer Financial

Association of Corporate Counsel (ACC) Financial Services Committee Legal Quick Hit Lewis S. Wiener March 23, 2011 Dodd-Frank Chapter X: The Consumer Financial Protection Bureau The Consumer Financial

Wall Street Reform and Consumer Financial Protection Act of 2010

Wall Street Reform and Consumer Financial Protection Act of 2010 Federal Preemption August 6, 2010 Presented By Oliver Ireland and Joseph Gabai 2010 Morrison & Foerster LLP All Rights Reserved mofo.com

Wall Street Reform and Consumer Financial Protection Act of 2010 Federal Preemption August 6, 2010 Presented By Oliver Ireland and Joseph Gabai 2010 Morrison & Foerster LLP All Rights Reserved mofo.com

Expert Analysis Understanding the Evolving Legal And Regulatory Landscape for Consumer Marketplace Lending

Westlaw Journal bank & Lender Liability Litigation News and Analysis Legislation Regulation Expert Commentary VOLUME 21, issue 19 / february 8, 2016 Expert Analysis Understanding the Evolving Legal And

Westlaw Journal bank & Lender Liability Litigation News and Analysis Legislation Regulation Expert Commentary VOLUME 21, issue 19 / february 8, 2016 Expert Analysis Understanding the Evolving Legal And

CUNA Short Summary of the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173; Public Law Number ) August 2, 2010

August 2, 2010") CUNA Short Summary of the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173; Public Law Number 111-203) August 2, 2010 Here is a short summary highlighting the provisions of the Dodd-Frank

CUNA Short Summary of the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173; Public Law Number 111-203) August 2, 2010 Here is a short summary highlighting the provisions of the Dodd-Frank

Servicing Update. Key Projects and Improvements. October Kim Wells U.S. Department of Education 1. Agenda

Servicing Update U.S. Department of Education Agenda General Servicing Updates Contract Changes Oversight and Monitoring Key Projects and Improvements Strategies and Future Changes Questions and Answers

Servicing Update U.S. Department of Education Agenda General Servicing Updates Contract Changes Oversight and Monitoring Key Projects and Improvements Strategies and Future Changes Questions and Answers

REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY

POLICY") I. INTRODUCTION A. Background and Overview REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY The Real Estate Settlement Procedures Act of 1974 ( RESPA ), 12 U.S.C. 2601 et seq., is a consumer disclosure

I. INTRODUCTION A. Background and Overview REAL ESTATE SETTLEMENT PROCEDURES ACT ( RESPA ) POLICY The Real Estate Settlement Procedures Act of 1974 ( RESPA ), 12 U.S.C. 2601 et seq., is a consumer disclosure

FINANCIAL SERVICES ENFORCEMENT ACTIONS TRACKER - Q4 2016

FINANCIAL SERVICES ADVISORY AND COMPLIANCE FINANCIAL SERVICES ENFORCEMENT ACTIONS TRACKER - Q 16 In Q 16, the number of regulatory actions increased by approximately 29 percent, driven by a 0 percent increase

FINANCIAL SERVICES ADVISORY AND COMPLIANCE FINANCIAL SERVICES ENFORCEMENT ACTIONS TRACKER - Q 16 In Q 16, the number of regulatory actions increased by approximately 29 percent, driven by a 0 percent increase

CFPB Supervision and Examination Process

Overview Statutory Background Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the Act) 1 established the Consumer Financial Protection Bureau (CFPB) and authorizes it

Overview Statutory Background Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the Act) 1 established the Consumer Financial Protection Bureau (CFPB) and authorizes it

THE CFPB WHAT IT DOES, AND WHY YOU SHOULD CARE

THE CFPB WHAT IT DOES, AND WHY YOU SHOULD CARE Center for Responsible Lending CRL is a nonprofit, non-partisan organization that works to protect homeownership and family wealth by fighting predatory lending

THE CFPB WHAT IT DOES, AND WHY YOU SHOULD CARE Center for Responsible Lending CRL is a nonprofit, non-partisan organization that works to protect homeownership and family wealth by fighting predatory lending

S Analysis of Regulatory Relief for Credit Union

S. 2155 Analysis of Regulatory Relief for Credit Union June 2018 SECTION Minimum Standards for Residential Mortgage Loans (Section 101) Adds a new safe harbor category of Qualified Mortgages (QMs) to Section

S. 2155 Analysis of Regulatory Relief for Credit Union June 2018 SECTION Minimum Standards for Residential Mortgage Loans (Section 101) Adds a new safe harbor category of Qualified Mortgages (QMs) to Section

FINANCIAL SERVICES ENFORCEMENT ACTIONS TRACKER - Q1 2017

FINANCIAL SERVICES ADVISORY AND COMPLIANCE FINANCIAL SERVICES ENFORCEMENT ACTIONS TRACKER - Q1 2017 HIGHLIGHTS FROM Q1 2017: total actions were levied against financial institutions by federal, state,

FINANCIAL SERVICES ADVISORY AND COMPLIANCE FINANCIAL SERVICES ENFORCEMENT ACTIONS TRACKER - Q1 2017 HIGHLIGHTS FROM Q1 2017: total actions were levied against financial institutions by federal, state,

Debt Collection CFPB Reveals Outline for Future Rulemaking

Client Alert Americas FS Regulatory Center of Excellence Debt Collection CFPB Reveals Outline for Future Rulemaking On July 28, 2016, the Consumer Financial Protection Bureau (CFPB or Bureau) released

Client Alert Americas FS Regulatory Center of Excellence Debt Collection CFPB Reveals Outline for Future Rulemaking On July 28, 2016, the Consumer Financial Protection Bureau (CFPB or Bureau) released

2/4/2014. Consumer Financial Protection Bureau Update A New Era of Regulation Begins. A Quick Overview of the CFPB. CFPB Overview (cont.

Consumer Financial Protection Bureau Update A New Era of Regulation Begins A Quick Overview of the CFPB The CFPB was created by Title X of the Dodd-Frank Act and became operational on July 21, 2011 Independent

Consumer Financial Protection Bureau Update A New Era of Regulation Begins A Quick Overview of the CFPB The CFPB was created by Title X of the Dodd-Frank Act and became operational on July 21, 2011 Independent

Terms and Conditions of Title IV, HEA Loans

Terms and Conditions of Title IV, HEA Loans Under applicable state law, except as preempted by federal law, you may have certain borrower rights, remedies, and defenses in addition to those stated in the

Terms and Conditions of Title IV, HEA Loans Under applicable state law, except as preempted by federal law, you may have certain borrower rights, remedies, and defenses in addition to those stated in the

Regulation by Enforcement CFPB s Use of UDAAP

Regulation by Enforcement CFPB s Use of UDAAP December 5, 2016 David Piper Cheryl Chang Dodd-Frank Act Dodd-Frank Act Consumer Financial Protection Bureau (CFPB) CFPB has independent rulemaking and enforcement

Regulation by Enforcement CFPB s Use of UDAAP December 5, 2016 David Piper Cheryl Chang Dodd-Frank Act Dodd-Frank Act Consumer Financial Protection Bureau (CFPB) CFPB has independent rulemaking and enforcement

National Federation of Community Development Credit Unions

National Federation of Community Development Credit Unions May 15, 2014 This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the Bureau. It does not constitute

National Federation of Community Development Credit Unions May 15, 2014 This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the Bureau. It does not constitute

United States Senate, Committee on Banking, Housing and Urban Affairs

United States Senate, Committee on Banking, Housing and Urban Affairs October 29, 2013 Housing Finance Reform: Essentials of a Functioning Housing Finance System for Consumers By Laurence E. Platt K&L

United States Senate, Committee on Banking, Housing and Urban Affairs October 29, 2013 Housing Finance Reform: Essentials of a Functioning Housing Finance System for Consumers By Laurence E. Platt K&L

6/21/2013. Section I. Purpose of Course. History and Overview of Mortgage Law, Regulation and Requirements

20 Hour Mortgage Loan Originator Certification Course Purpose of Course Gain historical perspective of mortgage lending Understand contemporary mortgage loan origination process Examine federal rules,

20 Hour Mortgage Loan Originator Certification Course Purpose of Course Gain historical perspective of mortgage lending Understand contemporary mortgage loan origination process Examine federal rules,

THE ENFORCEMENT POWERS OF THE CONSUMER FINANCIAL PROTECTION BUREAU JONATHAN FOXX President and Managing Director Lenders Compliance Group, Inc.

THE ENFORCEMENT POWERS OF THE CONSUMER FINANCIAL PROTECTION BUREAU JONATHAN FOXX President and Managing Director Lenders Compliance Group, Inc. For several months, the Consumer Financial Protection Bureau

THE ENFORCEMENT POWERS OF THE CONSUMER FINANCIAL PROTECTION BUREAU JONATHAN FOXX President and Managing Director Lenders Compliance Group, Inc. For several months, the Consumer Financial Protection Bureau

How to Ace Your CFPB Exam

How to Ace Your CFPB Exam May 25, 2016 Moderator Alan S. Kaplinsky Practice Leader Consumer Financial Services 215.864.8544 kaplinsky@ballardspahr.com Panelists Richard J. Andreano, Jr. Practice Leader

How to Ace Your CFPB Exam May 25, 2016 Moderator Alan S. Kaplinsky Practice Leader Consumer Financial Services 215.864.8544 kaplinsky@ballardspahr.com Panelists Richard J. Andreano, Jr. Practice Leader

SECTION SUMMARY EFFECTIVE DATE Section 101. Minimum Standards for Residential Mortgage Loans

SECTION SUMMARY EFFECTIVE DATE Section 101. Minimum Standards for Residential Mortgage Loans Section 103. Access to Affordable Mortgages. Section 104. Home Mortgage Disclosure Act Adjustment and Study

SECTION SUMMARY EFFECTIVE DATE Section 101. Minimum Standards for Residential Mortgage Loans Section 103. Access to Affordable Mortgages. Section 104. Home Mortgage Disclosure Act Adjustment and Study

RE: Request for Information Regarding the Bureau's Supervision Program (Docket No. CFPB )

") Monica Jackson Office of the Executive Secretary Bureau of Consumer Financial Protection 1700 G Street, NW Washington, DC 20552 RE: Request for Information Regarding the Bureau's Supervision Program (Docket

Monica Jackson Office of the Executive Secretary Bureau of Consumer Financial Protection 1700 G Street, NW Washington, DC 20552 RE: Request for Information Regarding the Bureau's Supervision Program (Docket

Will the CFPB Continue Under The Trump Administration?

Westlaw Journal WHITE-COLLAR CRIME Litigation News and Analysis Legislation Regulation Expert Commentary VOLUME 31, ISSUE 6 / FEBRUARY 2017 EXPERT ANALYSIS Will the CFPB Continue Under The Trump Administration?

Westlaw Journal WHITE-COLLAR CRIME Litigation News and Analysis Legislation Regulation Expert Commentary VOLUME 31, ISSUE 6 / FEBRUARY 2017 EXPERT ANALYSIS Will the CFPB Continue Under The Trump Administration?

CFPB PROPOSED REGULATIONS

CFPB PROPOSED REGULATIONS TILA/RESPA DISCLOSURES For more than 30 years, 2 different disclosure forms to consumers applying for a mortgage Developed by 2 different federal agencies under 2 federal statutes:

CFPB PROPOSED REGULATIONS TILA/RESPA DISCLOSURES For more than 30 years, 2 different disclosure forms to consumers applying for a mortgage Developed by 2 different federal agencies under 2 federal statutes:

Regulatory review RR

Regulatory review RR2012-01 January 12, 2012 REGULATORY REVIEW Table of Contents Final Rule Community Reinvestment Act Regulations... 1 Mortgage Acts and Practices Advertising (CFPB Regulation N) and Mortgage

Regulatory review RR2012-01 January 12, 2012 REGULATORY REVIEW Table of Contents Final Rule Community Reinvestment Act Regulations... 1 Mortgage Acts and Practices Advertising (CFPB Regulation N) and Mortgage

Using technology to increase financial literacy Julia Joggerst, CommonBond

Massachusetts Association of Student Financial Aid Administrators Using technology to increase financial literacy Julia Joggerst, CommonBond 1 Introduction CommonBond Julia Joggerst Director CommonBond

Massachusetts Association of Student Financial Aid Administrators Using technology to increase financial literacy Julia Joggerst, CommonBond 1 Introduction CommonBond Julia Joggerst Director CommonBond

TILA-RESPA Integrated Disclosure (TRID) Rule a.k.a. Know Before You Owe. with New Haven Middlesex Association of REALTORS

Rule a.k.a. Know Before You Owe. with New Haven Middlesex Association of REALTORS") TILA-RESPA Integrated Disclosure (TRID) Rule a.k.a. Know Before You Owe with New Haven Middlesex Association of REALTORS July 16, 2015 Jeremy Potter, General Counsel and Chief Compliance Officer, Norcom

TILA-RESPA Integrated Disclosure (TRID) Rule a.k.a. Know Before You Owe with New Haven Middlesex Association of REALTORS July 16, 2015 Jeremy Potter, General Counsel and Chief Compliance Officer, Norcom

Re: Request for Information Regarding Bureau Enforcement Processes (Docket No. CFPB )

") May 14, 2018 By Electronic Submission Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552 www.regulations.gov Jan Stieger, CMP,

May 14, 2018 By Electronic Submission Ms. Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552 www.regulations.gov Jan Stieger, CMP,

Student Loans & Service Members

PF SMS icons PF SMS icons Student Loans & Service Members https://learn.extension.org/events/3014 This material is based upon work supported by the National Institute of Food and Agriculture, U.S. Department

PF SMS icons PF SMS icons Student Loans & Service Members https://learn.extension.org/events/3014 This material is based upon work supported by the National Institute of Food and Agriculture, U.S. Department

Jim Nussle President & CEO. Phone:

Jim Nussle President & CEO 99 M Street SE Suite 300 Washington, DC 20003-3799 Phone: 202-508-6745 jnussle@cuna.coop March 11, 2019 The Honorable Mike Crapo Chairman Committee on Banking, Housing and Urban

Jim Nussle President & CEO 99 M Street SE Suite 300 Washington, DC 20003-3799 Phone: 202-508-6745 jnussle@cuna.coop March 11, 2019 The Honorable Mike Crapo Chairman Committee on Banking, Housing and Urban

CFPB Announces Proposal For Restricting Payday Lending With Potentially Significant Compliance Ramifications

April 2015 CFPB Announces Proposal For Restricting Payday Lending With Potentially Significant Compliance Ramifications I. Summary. On March 26, 2015, the Consumer Financial Protection Bureau (CFPB) announced

April 2015 CFPB Announces Proposal For Restricting Payday Lending With Potentially Significant Compliance Ramifications I. Summary. On March 26, 2015, the Consumer Financial Protection Bureau (CFPB) announced

Short-Term, Small-Dollar Lending

Commonly Known as Payday Lending Exam Date: Prepared By: Reviewer: Docket #: Entity Name: [Click&type] [Click&type] [Click&type] [Click&type] [Click&type] These examination procedures apply to the short-term,

Commonly Known as Payday Lending Exam Date: Prepared By: Reviewer: Docket #: Entity Name: [Click&type] [Click&type] [Click&type] [Click&type] [Click&type] These examination procedures apply to the short-term,

March 23, Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552

March 23, 2015 Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552 Re: Prepaid Accounts under the Electronic Fund Transfer Act (Regulation

March 23, 2015 Monica Jackson Office of the Executive Secretary Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20552 Re: Prepaid Accounts under the Electronic Fund Transfer Act (Regulation

Regulatory Influences to the Motor Vehicle Service Contract and Ancillary Product Industry

Regulatory Influences to the Motor Vehicle Service Contract and Ancillary Product Industry Aaron E. Lunt, JD, CPCU, ARe Assistant General Counsel, Head of Regulatory Affairs The Warranty Group August 29,

Regulatory Influences to the Motor Vehicle Service Contract and Ancillary Product Industry Aaron E. Lunt, JD, CPCU, ARe Assistant General Counsel, Head of Regulatory Affairs The Warranty Group August 29,

Consumer Finance Protection Bureau

******************************************************** III. Consumer Finance Protection Bureau Susan M Camp Stocks - Washington, D.C. ********************************************************** III-1

******************************************************** III. Consumer Finance Protection Bureau Susan M Camp Stocks - Washington, D.C. ********************************************************** III-1

Payday Lending Provision 2007 Defense Authorization Bill

Payday Lending Provision 2007 Defense Authorization Bill Overview H.R. 5122, the John Warner National Defense Authorization Act for Fiscal Year 2007, includes a provision (Subtitle F, Section 670) originally

Payday Lending Provision 2007 Defense Authorization Bill Overview H.R. 5122, the John Warner National Defense Authorization Act for Fiscal Year 2007, includes a provision (Subtitle F, Section 670) originally

Fair & Responsible Lending in the Regulatory Crosshairs

Fair & Responsible Lending in the Regulatory Crosshairs Legal Counsel to the Financial Services Industry Minnesota Banking Law Institute April 5, 2013 Andrea K. Mitchell Partner Lori J. Sommerfield Counsel

Fair & Responsible Lending in the Regulatory Crosshairs Legal Counsel to the Financial Services Industry Minnesota Banking Law Institute April 5, 2013 Andrea K. Mitchell Partner Lori J. Sommerfield Counsel

The Consumer Financial Protection Bureau at Five: A Survey of the Bureau's Activities

NORTH CAROLINA BANKING INSTITUTE Volume 21 Issue 1 Article 9 3-1-2017 The Consumer Financial Protection Bureau at Five: A Survey of the Bureau's Activities Donald C. Lampe Ryan J. Richardson Follow this

NORTH CAROLINA BANKING INSTITUTE Volume 21 Issue 1 Article 9 3-1-2017 The Consumer Financial Protection Bureau at Five: A Survey of the Bureau's Activities Donald C. Lampe Ryan J. Richardson Follow this

CFPB Update. COHEAO Annual Conference. January 29, 2018 Arlington, VA. Heather S. Klein, Associate

CFPB Update COHEAO Annual Conference January 29, 2018 Arlington, VA John L. Culhane, Jr., Partner Consumer Financial Services Group Higher Education Group 215.864.8535 culhane@ballardspahr.com Heather

CFPB Update COHEAO Annual Conference January 29, 2018 Arlington, VA John L. Culhane, Jr., Partner Consumer Financial Services Group Higher Education Group 215.864.8535 culhane@ballardspahr.com Heather

TITLE 28 LENDING AND CONSUMER PROTECTION ACT

TITLE 28 LENDING AND CONSUMER PROTECTION ACT CHAPTER 1 TITLE, POLICY AND PURPOSE OF THIS ORDNANCE Section 28-1-1. TITLE. This title may be known and cited as the Flandreau Santee Sioux Tribal Lending and

TITLE 28 LENDING AND CONSUMER PROTECTION ACT CHAPTER 1 TITLE, POLICY AND PURPOSE OF THIS ORDNANCE Section 28-1-1. TITLE. This title may be known and cited as the Flandreau Santee Sioux Tribal Lending and

Amendments to Federal Mortgage Disclosure Requirements under the Truth in Lending

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1026 [Docket No. CFPB-2017-0018] RIN 3170-AA61 Amendments to Federal Mortgage Disclosure Requirements under the Truth in Lending

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1026 [Docket No. CFPB-2017-0018] RIN 3170-AA61 Amendments to Federal Mortgage Disclosure Requirements under the Truth in Lending

Trendspotting the CFPB: What s Coming and How Institutions Can Prepare

Trendspotting the CFPB: What s Coming and How Institutions Can Prepare Courtney H. Gilmer Baker Donelson Center Suite 800 211 Commerce Street Nashville, TN 37201 615.726.5747 cgilmer@bakerdonelson.com

Trendspotting the CFPB: What s Coming and How Institutions Can Prepare Courtney H. Gilmer Baker Donelson Center Suite 800 211 Commerce Street Nashville, TN 37201 615.726.5747 cgilmer@bakerdonelson.com

Federal Mortgage Disclosure Requirements under the Truth in Lending Act (Regulation Z)

") BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1026 [Docket No. CFPB-2017-0018] RIN 3170-AA71 Federal Mortgage Disclosure Requirements under the Truth in Lending Act (Regulation

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION 12 CFR Part 1026 [Docket No. CFPB-2017-0018] RIN 3170-AA71 Federal Mortgage Disclosure Requirements under the Truth in Lending Act (Regulation

Mortgage Servicing. Examination Objectives

Mortgage Servicing After completing the risk assessment and examination scoping, examiners should use these procedures, in conjunction with the compliance Exam Date: Prepared By: Reviewer: Docket #: Entity

Mortgage Servicing After completing the risk assessment and examination scoping, examiners should use these procedures, in conjunction with the compliance Exam Date: Prepared By: Reviewer: Docket #: Entity

CFPB Readiness Series: GLBA and Regulation P

CFPB Readiness Series: GLBA and Regulation P Who is KirkpatrickPrice? KirkpatrickPrice is a licensed CPA firm, providing assurance services to over 250 clients in more than 40 states, Canada, Asia and

CFPB Readiness Series: GLBA and Regulation P Who is KirkpatrickPrice? KirkpatrickPrice is a licensed CPA firm, providing assurance services to over 250 clients in more than 40 states, Canada, Asia and

The Unique Role of Non-Banks in Emerging Payments: The laws that apply; the rewards and the risks. ACC Legal Quick Hit

The Unique Role of Non-Banks in Emerging Payments: The laws that apply; the rewards and the risks. ACC Legal Quick Hit Judith Rinearson, Bryan Cave LLP Keith Omsberg, Official Payments Corporation Cheryl

The Unique Role of Non-Banks in Emerging Payments: The laws that apply; the rewards and the risks. ACC Legal Quick Hit Judith Rinearson, Bryan Cave LLP Keith Omsberg, Official Payments Corporation Cheryl

Education Loan Examination Procedures

CFPB Education Loan Examination Procedures Education Loan Education Loan Examination Procedures After completing the risk assessment and examination scoping, examiners should use these procedures, in conjunction

CFPB Education Loan Examination Procedures Education Loan Education Loan Examination Procedures After completing the risk assessment and examination scoping, examiners should use these procedures, in conjunction

SHAPING THE FUTURE. CFPB HOLDING ITS FIRE

1 of 5 10/23/2014 9:53 AM October 3, 2014 - In This Issue: News from AFSA SHAPING THE FUTURE. AFSA SPEAKS OUT AGAINST PENTAGON PROPOSAL CFPB HOLDING ITS FIRE CFPB TARGETS PRICE DISPARITY APPEALS COURT

1 of 5 10/23/2014 9:53 AM October 3, 2014 - In This Issue: News from AFSA SHAPING THE FUTURE. AFSA SPEAKS OUT AGAINST PENTAGON PROPOSAL CFPB HOLDING ITS FIRE CFPB TARGETS PRICE DISPARITY APPEALS COURT

Through the Crystal Ball: Predicting Important CFPB Developments in 2015

Through the Crystal Ball: Predicting Important CFPB Developments in 2015 April 2, 2015 Moderator Alan S. Kaplinsky Practice Leader Consumer Financial Services 215.864.8544 kaplinsky@ballardspahr.com Panelists

Through the Crystal Ball: Predicting Important CFPB Developments in 2015 April 2, 2015 Moderator Alan S. Kaplinsky Practice Leader Consumer Financial Services 215.864.8544 kaplinsky@ballardspahr.com Panelists

Higher Education Opportunity Act

July 1, 2008 Schools Maximum duration of eligibility for students receiving a Pell Grant for the first time on or after July 1, 2008. (DCL page 104) Unsubsidized Stafford Loan Limits for loans first disbursed

July 1, 2008 Schools Maximum duration of eligibility for students receiving a Pell Grant for the first time on or after July 1, 2008. (DCL page 104) Unsubsidized Stafford Loan Limits for loans first disbursed

The Funnel Effect of The Dodd-Frank Act

The Funnel Effect of The Dodd-Frank Act 2012 NCHER Knowledge Symposium The Dodd-Frank Effect Model Increases in Regulation Lawsuits Financial Industry Reaction Complaints Customer Confusion 1 The Dodd-Frank

The Funnel Effect of The Dodd-Frank Act 2012 NCHER Knowledge Symposium The Dodd-Frank Effect Model Increases in Regulation Lawsuits Financial Industry Reaction Complaints Customer Confusion 1 The Dodd-Frank

Fair Lending Issues and Hot Topics

Fair Lending Issues and Hot Topics Outlook Live Webinar November 2, 2011 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

Fair Lending Issues and Hot Topics Outlook Live Webinar November 2, 2011 Non-Discrimination Working Group of the Financial Fraud Enforcement Task Force Visit us at www.consumercomplianceoutlook.org informational

4/11/2018. TILA-RESPA Integrated Disclosures, Part 4 - Completing the Closing Disclosure. Outlook Live Webinar- November 18, 2014

Outlook Live Webinar- November 18, 2014 TILA-RESPA Integrated Disclosures, Part 4 - Completing the Closing Disclosure Presented by the Consumer Financial Protection Bureau The content of this webinar is

Outlook Live Webinar- November 18, 2014 TILA-RESPA Integrated Disclosures, Part 4 - Completing the Closing Disclosure Presented by the Consumer Financial Protection Bureau The content of this webinar is

REGULATION OF NON-DEPOSITORY COVERED PERSONS UNDER THE DODD-FRANK ACT

Vol. 28 No. 1 January 2012 REGULATION OF NON-DEPOSITORY COVERED PERSONS UNDER THE DODD-FRANK ACT The jurisdiction and rulemaking authority of the Consumer Financial Protection Bureau under Title X of the

Vol. 28 No. 1 January 2012 REGULATION OF NON-DEPOSITORY COVERED PERSONS UNDER THE DODD-FRANK ACT The jurisdiction and rulemaking authority of the Consumer Financial Protection Bureau under Title X of the

Summary of Mortgage Related Provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act. August 6, 2010

Summary of Mortgage Related Provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act August 6, 2010 BACKGROUND This summary describes key points in the Dodd-Frank Wall Street Reform

Summary of Mortgage Related Provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act August 6, 2010 BACKGROUND This summary describes key points in the Dodd-Frank Wall Street Reform

Credit Union Advisory Council

September 2017 Credit Union Advisory Council September 7, 2017 Meeting of the Credit Union Advisory Council The Credit Union Advisory Council (CUAC) of the Consumer Financial Protection Bureau (CFPB) met

September 2017 Credit Union Advisory Council September 7, 2017 Meeting of the Credit Union Advisory Council The Credit Union Advisory Council (CUAC) of the Consumer Financial Protection Bureau (CFPB) met

About this report. Confidential and proprietary information 2018 Navient Solutions, LLC. All rights reserved.

CFPB Consumer Response Portal Summary of Navient Customer Submissions Through the CFPB Student Loan Complaint Portal October 1, 2016 - September 30, 2017 March 2018 About this report This report is Navient

CFPB Consumer Response Portal Summary of Navient Customer Submissions Through the CFPB Student Loan Complaint Portal October 1, 2016 - September 30, 2017 March 2018 About this report This report is Navient

Request for Information Regarding Ability-to-Repay/Qualified Mortgage Rule Assessment

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION [Docket No. CFPB-2017-0014] Request for Information Regarding Ability-to-Repay/Qualified Mortgage Rule Assessment AGENCY: Bureau of Consumer

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION [Docket No. CFPB-2017-0014] Request for Information Regarding Ability-to-Repay/Qualified Mortgage Rule Assessment AGENCY: Bureau of Consumer

Lending Audit. Chapter 8. Introduction. Laws and Regulations Covered by the Audit

Chapter 8 Introduction Auditing the lending functions of the bank for compliance with federal regulations can be an intimidating job. In general, the laws and regulations that deal with the lending function

Chapter 8 Introduction Auditing the lending functions of the bank for compliance with federal regulations can be an intimidating job. In general, the laws and regulations that deal with the lending function

Bureau Update: Debt Collection

Bureau Update: Debt Collection NACARA October 16, 2018 Charleston, SC This presentation is being made by representatives of the Bureau of Consumer Financial Protection on behalf of the Bureau. It does

Bureau Update: Debt Collection NACARA October 16, 2018 Charleston, SC This presentation is being made by representatives of the Bureau of Consumer Financial Protection on behalf of the Bureau. It does

Bureau Update: Debt Collection. Sep 2018

Bureau Update: Debt Collection Sep 2018 This presentation is being made by representatives of the Bureau of Consumer Financial Protection on behalf of the Bureau. It does not constitute legal interpretation,

Bureau Update: Debt Collection Sep 2018 This presentation is being made by representatives of the Bureau of Consumer Financial Protection on behalf of the Bureau. It does not constitute legal interpretation,

Initial Analysis of CFPB s Final Rule to Address Payday & Car Title Loans

Initial Analysis of CFPB s Final Rule to Address Payday & Car Title Loans Policy Brief October 18, 2017 The following provides an overview of CFPB s final rule addressing payday and car title lending and

Initial Analysis of CFPB s Final Rule to Address Payday & Car Title Loans Policy Brief October 18, 2017 The following provides an overview of CFPB s final rule addressing payday and car title lending and

Second Summary of Mortgage Related Provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173) July 13, 2010

July 13, 2010") Second Summary of Mortgage Related Provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173) July 13, 2010 As signed by the Conference of the House and Senate on June 29,

Second Summary of Mortgage Related Provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173) July 13, 2010 As signed by the Conference of the House and Senate on June 29,

Fair lending report of the Consumer Financial Protection Bureau

Fair lending report of the Consumer Financial Protection Bureau April 2014 Message from Richard Cordray Director of the CFPB From the moment we first opened our doors, the Consumer Financial Protection

Fair lending report of the Consumer Financial Protection Bureau April 2014 Message from Richard Cordray Director of the CFPB From the moment we first opened our doors, the Consumer Financial Protection

CFPB Consumer Laws and Regulations

Fair Debt Collection Practices Act 1 The Fair Debt Collection Practices Act ()(15 U.S.C. 1692 et seq.), which became effective March 20, 1978, was designed to eliminate abusive, deceptive, and unfair debt

Fair Debt Collection Practices Act 1 The Fair Debt Collection Practices Act ()(15 U.S.C. 1692 et seq.), which became effective March 20, 1978, was designed to eliminate abusive, deceptive, and unfair debt

SUBSTITUTE AMENDMENT CHANGES

Title I Improving Consumer Access to Mortgage Credit 103 Tailored exemption from appraisal requirements Adds definition of transaction value and provides additional detail on criteria for efforts to contact

Title I Improving Consumer Access to Mortgage Credit 103 Tailored exemption from appraisal requirements Adds definition of transaction value and provides additional detail on criteria for efforts to contact

Reverse Mortgage. Examination Procedures

Examination Procedures Reverse Mortgage Servicing Exam Date: Exam ID No. These examination procedures apply to reverse mortgage Prepared By: servicing and are a stand-alone resource to complete a reverse

Examination Procedures Reverse Mortgage Servicing Exam Date: Exam ID No. These examination procedures apply to reverse mortgage Prepared By: servicing and are a stand-alone resource to complete a reverse

CFPB Integrated Mortgage Disclosure Final Rule

CFPB Integrated Mortgage Disclosure Final Rule Current Status of the New Rule Mary Schuster Chief Product Officer - RamQuest The Regulatory Reform Ecosystem Meet the CFPB Mission Statement o To make markets

CFPB Integrated Mortgage Disclosure Final Rule Current Status of the New Rule Mary Schuster Chief Product Officer - RamQuest The Regulatory Reform Ecosystem Meet the CFPB Mission Statement o To make markets

Consumer Regulatory Changes

Consumer Regulatory Changes Federal Reserve Board Division of Consumer and Community Affairs August 19, 2010 Visit us at www.consumercomplianceoutlook.org The The opinions expressed in in this this presentation

Consumer Regulatory Changes Federal Reserve Board Division of Consumer and Community Affairs August 19, 2010 Visit us at www.consumercomplianceoutlook.org The The opinions expressed in in this this presentation

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended