Financial Education. Debt Repayment of Young Adults

|

|

|

- Cori Small

- 6 years ago

- Views:

Transcription

1 Introduction and Debt Repayment of Young Adults Alexandra Brown 1 J. Michael Collins 2 Maximilian Schmeiser 1 Carly Urban 3 1 Federal Reserve Board 2 University of Wisconsin-Madison 3 Department of Agricultural Economics and Economics Montana State University March 6, 2015

2 Introduction Financial Literacy in the U.S. Financial literacy in the U.S. is generally low, but financial knowledge amongst young adults is particularly weak: Less than 1 3 of Americans ages 23 to 28 possess basic knowledge of interest rates, inflation and risk diversification. Low levels of financial literacy have been associated with: lower rate of asset accumulation lower stock market participation higher levels of debt

3 Introduction Financial Literacy in the U.S. Financial literacy in the U.S. is generally low, but financial knowledge amongst young adults is particularly weak: Less than 1 3 of Americans ages 23 to 28 possess basic knowledge of interest rates, inflation and risk diversification. Low levels of financial literacy have been associated with: lower rate of asset accumulation lower stock market participation higher levels of debt

4 Introduction Financial Literacy in the U.S. Financial literacy in the U.S. is generally low, but financial knowledge amongst young adults is particularly weak: Less than 1 3 of Americans ages 23 to 28 possess basic knowledge of interest rates, inflation and risk diversification. Low levels of financial literacy have been associated with: lower rate of asset accumulation lower stock market participation higher levels of debt

5 Introduction Financial Literacy in the U.S. Financial literacy in the U.S. is generally low, but financial knowledge amongst young adults is particularly weak: Less than 1 3 of Americans ages 23 to 28 possess basic knowledge of interest rates, inflation and risk diversification. Low levels of financial literacy have been associated with: lower rate of asset accumulation lower stock market participation higher levels of debt

6 Introduction Policymakers calls for increasing financial literacy in the U.S. One response: Expand K-12 personal finance and economic education requirements. Existing body of research on the effectiveness of personal finance education yields conflicting findings at best. This paper: examine the effect of state financial education mandates

7 Introduction Policymakers calls for increasing financial literacy in the U.S. One response: Expand K-12 personal finance and economic education requirements. Existing body of research on the effectiveness of personal finance education yields conflicting findings at best. This paper: examine the effect of state financial education mandates

8 Introduction Policymakers calls for increasing financial literacy in the U.S. One response: Expand K-12 personal finance and economic education requirements. Existing body of research on the effectiveness of personal finance education yields conflicting findings at best. This paper: examine the effect of state financial education mandates

9 Introduction Policymakers calls for increasing financial literacy in the U.S. One response: Expand K-12 personal finance and economic education requirements. Existing body of research on the effectiveness of personal finance education yields conflicting findings at best. This paper: examine the effect of state financial education mandates

10 Mechanisms Introduction Borrowers can behave counter to their own long-run preferences Consumption in the current period that results in missing loan payments Could fail to fully appreciate future costs of this in the present Problem may be even worse for relatively naive young adults Education may focus limited cognitive attention to financial issues

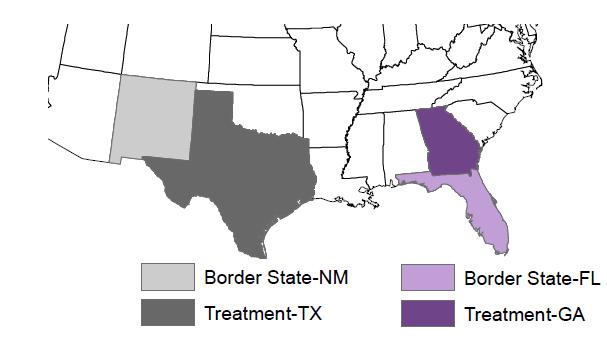

11 This Paper Introduction Question: What are the effects of personal finance education mandates in high school on credit behavior in early adulthood? Georgia and Texas implemented personal finance competency requirements in 2007 did not implement other curriculum changes at the same time Nearby state(s) had no comparable education policy shifts Using border-state, compare areas using difference-in-differences in loan repayment rates for students exposed to financial education competency mandates Across state; before and after implementation to the change

12 Policy Begins Last year of Policy Estimated Grad Year 2000 Sample: yr olds Grad year 2001 Sample Grad year 2007 Post1" Sample Grad year 2002 Sample Grad year 2008 Post2" Sample Grad year 2003 Sample Grad year 2009 Post3" Sample Grad year 2004 Sample Grad year 2005 Sample Grad year 2006 Sample

13 Approach Introduction Researched each mandate: standardized curricula, graduation requirements, testing requirements, teacher training, etc. Begin treatment with first class affected by mandate, not following passage of mandate. Use panel from the Consumer Credit Panel (CCP) to determine if young adults (18-22) have better financial outcomes after exposure to financial education.

14 Introduction : Behavioral Response Adding mandate for financial education makes financial management more salient. Reminder to avoid missing payments (a common behavior for young people) Attention to importance of on-time payments results in fewer delinquencies/defaults.

15 Data Sources Introduction Mandates Consumer Credit Panel Collect data on financial education mandates from 2000 to present from: Jump$tart Coalition for Personal Financial Literacy Council for Economic Education (CEE) Survey of the States Champlain College Center for Financial Literacy In many cases, Jump$tart and CEE conflict. Heterogeneity in actual implementation (vs. mandate) matters. Direct contact with states, graduation requirement documents, standardized curriculum

16

17 Introduction Consumer Credit Panel Data Mandates Consumer Credit Panel Credit bureau data from the FRBNY/Equifax Consumer Credit Panel 5% household sample of Equifax records (includes all household members with credit files) Quarterly panel data observe when first have data reported Assume age 18 = graduation year. Assume went to high school in current state in credit report address. Restrict the sample to those (1stQ) years of age. Dependent variables: Credit score (Equifax risk score) Delinquency: Any account 30, or 90+ days delinquent

18 Introduction Empirical Method Empirical Strategy: Difference-in-Differences Y ist = α 0 + β 1 (T s P1 it ) + β 2 (T s P2 it ) + β 3 (T s P3 it ) + γ 1 u it + δ s + κx it + η t + ɛ ist Y ist = credit score, any trade delinquency, and auto trade delinquency T s = 1 if state was treated T s P1, 2, 3 it = 1 if received education 2008, 2009, or 2010 u it = unemployment rate in the county n i = number of quarters of individual s credit file δ s = state fixed effects X it = number of credit accounts for individual i η t = quarter by year fixed effects

19 Introduction Empirical Method GA Border (FL) TX Border (NM) Credit Score (89.40) (88.10) (88.50) (87.20) Number of Accounts (2.20) (2.60) (2.50) (2.20) Account 30 Days Delinquent (0.36) (0.36) (0.36) (0.34) Account 90 + Days Delinquent (0.39) (0.38) (0.38) (0.37) Auto 30 Days Delinquent (0.19) (0.17) (0.18) (0.17) Auto 90 + Days Delinquent (0.11) (0.10) (0.09) (0.10) County Unemployment Rate (1.70) (1.76) (1.57) (1.58) State Level % Some College (4.58) (3.07) (3.86) (3.11) Number of Individuals 55, , ,807 12,625

20 Introduction Empirical Method Treatment Effect: Difference in Difference by Graduation Year: Georgia vs. Florida (1) (2) (3) (4) (5) Credit Auto 30 Auto 90 + Score Days Del Days Del Days Del Days Del 08 Grad * *** (0.407) (0.001) (0.001) (0.002) (0.001) 09 Grad 6.293*** *** ** (0.410) (0.001) (0.001) (0.002) (0.001) 10 Grad 10.89*** *** *** *** (0.486) (0.001) (0.002) (0.002) (0.002) N 1,632,241 1,407,663 1,407, , ,800 Notes: Robust standard errors clustered at the individual level in parentheses. * p < 0.10, ** p < 0.05, *** p < was first graduating class affected by the requirement. Models include state-level and quarter by year fixed effects, unemployment rate in the state and year of graduation, and number of accounts.

21 Introduction Empirical Method Treatment Effect: Difference in Difference by Graduation Year: Texas vs. New Mexico (1) (2) (3) (4) (5) Credit Auto 30 Auto 90 + Score Days Del Days Del Days Del Days Del *** *** *** * (0.299) (0.0007) (0.0009) (0.0010) (0.0008) *** ** *** *** *** (0.324) (0.0007) (0.001) (0.001) (0.001) *** *** *** *** *** (0.388) (0.0009) (0.0012) (0.0019) (0.001) N 1,585,593 1,669,260 1,669,260 1,669,260 1,669,260 Notes: Robust standard errors clustered at the individual level in parentheses. * p < 0.10, ** p < 0.05, *** p < was the first graduating class affected by the requirement. Models include state-level and quarter by year fixed effects, unemployment rate in the state and year of graduation, and number of accounts.

22 Summary Introduction Empirical Method Georgia grads after policy have credit scores 11 points higher 30 day delinquency lower by 4.2 percent (marginal effect from mean) 90 plus days delinquency about 10 percent Texas grads credit scores are over 31.7 points larger 90 plus days delinquent is much larger almost 5.8 percentage points translates into 1/3rd fewer severe delinquencies

23 Implications Introduction Younger people have lower credit scores learning by experience Nearly a quarter are 30 or more behind on at least one account Payments have big effect on the credit score of someone with a brief credit history. However, many cautions... Longer-run persistence into later adulthood unknown may just jump start trial and error learning Displacement of other curricula could have offsetting effects Time period specific issues during recession

Grand Challenge in Social Work. Fern Martine - Kiera Gardner - Brandi Stoneman - Aubree Payne University of Utah

Grand Challenge in Social Work Fern Martine - Kiera Gardner - Brandi Stoneman - Aubree Payne University of Utah Background Grand Challenge: Create a Social Response to a Changing Environment Our Challenge:

Grand Challenge in Social Work Fern Martine - Kiera Gardner - Brandi Stoneman - Aubree Payne University of Utah Background Grand Challenge: Create a Social Response to a Changing Environment Our Challenge:

Student Loan Borrowing and Repayment Trends, 2015 Cleveland Fed 2015 Policy Summit

Student Loan Borrowing and Repayment Trends, 2015 Cleveland Fed 2015 Policy Summit June 18, 2015 Andrew Haughwout, Research Group The views presented here are those of the authors and do not necessarily

Student Loan Borrowing and Repayment Trends, 2015 Cleveland Fed 2015 Policy Summit June 18, 2015 Andrew Haughwout, Research Group The views presented here are those of the authors and do not necessarily

Import Competition and Household Debt

Import Competition and Household Debt Barrot (MIT) Plosser (NY Fed) Loualiche (MIT) Sauvagnat (Bocconi) USC Spring 2017 The views expressed in this paper are those of the authors and do not necessarily

Import Competition and Household Debt Barrot (MIT) Plosser (NY Fed) Loualiche (MIT) Sauvagnat (Bocconi) USC Spring 2017 The views expressed in this paper are those of the authors and do not necessarily

The Impact of Credit Counseling on Consumer Outcomes: Evidence from a National Demonstration Program

The Impact of Credit Counseling on Consumer Outcomes: Evidence from a National Demonstration Program Stephen Roll Stephanie Moulton, PhD Credit Counseling Overview Reaches two million clients a year Provides

The Impact of Credit Counseling on Consumer Outcomes: Evidence from a National Demonstration Program Stephen Roll Stephanie Moulton, PhD Credit Counseling Overview Reaches two million clients a year Provides

Personal finance literacy formal preparation prior to college, what is sought in the university-level course, and student performance

Personal finance literacy formal preparation prior to college, what is sought in the university-level course, and student performance ABSTRACT Charles Corcoran University of Wisconsin River Falls A review

Personal finance literacy formal preparation prior to college, what is sought in the university-level course, and student performance ABSTRACT Charles Corcoran University of Wisconsin River Falls A review

Do Student Loan Borrowers Opportunistically Default? Evidence from Bankruptcy Reform

Do Student Loan Borrowers Opportunistically Default? Evidence from Bankruptcy Reform Rajeev Darolia, University of Missouri Dubravka Ritter, Federal Reserve Bank of Philadelphia 2015 Policy Summit on Housing,

Do Student Loan Borrowers Opportunistically Default? Evidence from Bankruptcy Reform Rajeev Darolia, University of Missouri Dubravka Ritter, Federal Reserve Bank of Philadelphia 2015 Policy Summit on Housing,

Summary. The importance of accessing formal credit markets

Policy Brief: The Effect of the Community Reinvestment Act on Consumers Contact with Formal Credit Markets by Ana Patricia Muñoz and Kristin F. Butcher* 1 3, 2013 November 2013 Summary Data on consumer

Policy Brief: The Effect of the Community Reinvestment Act on Consumers Contact with Formal Credit Markets by Ana Patricia Muñoz and Kristin F. Butcher* 1 3, 2013 November 2013 Summary Data on consumer

Credit Constraints and Search Frictions in Consumer Credit Markets

in Consumer Credit Markets Bronson Argyle Taylor Nadauld Christopher Palmer BYU BYU Berkeley-Haas CFPB 2016 1 / 20 What we ask in this paper: Introduction 1. Do credit constraints exist in the auto loan

in Consumer Credit Markets Bronson Argyle Taylor Nadauld Christopher Palmer BYU BYU Berkeley-Haas CFPB 2016 1 / 20 What we ask in this paper: Introduction 1. Do credit constraints exist in the auto loan

Interest Rate Pass-Through: Mortgage Rates, Household Consumption, and Voluntary Deleveraging. Online Appendix

Interest Rate Pass-Through: Mortgage Rates, Household Consumption, and Voluntary Deleveraging Marco Di Maggio, Amir Kermani, Benjamin J. Keys, Tomasz Piskorski, Rodney Ramcharan, Amit Seru, Vincent Yao

Interest Rate Pass-Through: Mortgage Rates, Household Consumption, and Voluntary Deleveraging Marco Di Maggio, Amir Kermani, Benjamin J. Keys, Tomasz Piskorski, Rodney Ramcharan, Amit Seru, Vincent Yao

Student Loans: Painting a Clear Picture

Student Loans: Painting a Clear Picture University of Kansas April 22, 2014 Kelly D. Edmiston Senior Economist Federal Reserve Bank of Kansas City Outline Outstanding Student Loan Debt Capacity to Repay

Student Loans: Painting a Clear Picture University of Kansas April 22, 2014 Kelly D. Edmiston Senior Economist Federal Reserve Bank of Kansas City Outline Outstanding Student Loan Debt Capacity to Repay

Compendium of Financial Literacy Resources & Identity Theft Data

Compendium of Financial Literacy Resources & Identity Theft Data Featuring Financial Literacy Resources Consumer Complaint Data 50 States and the District of Columbia William R. Slap Wesleyan University

Compendium of Financial Literacy Resources & Identity Theft Data Featuring Financial Literacy Resources Consumer Complaint Data 50 States and the District of Columbia William R. Slap Wesleyan University

Household Debt in America: A Look Across Generations Over Time

Household Debt in America: A Look Across Generations Over Time Carlos Garriga Bryan Noeth Don E. Schlagenhauf Federal Reserve Bank of St. Louis The Center for Household Financial Stability and Research

Household Debt in America: A Look Across Generations Over Time Carlos Garriga Bryan Noeth Don E. Schlagenhauf Federal Reserve Bank of St. Louis The Center for Household Financial Stability and Research

IMPACT OF FINANCIAL COUNSELING ON FINANCIAL STABILITY ANALYSIS OF THE NEW YORK CITY MODEL

CFS Research Brief (FLRC 11-9) October 2011 IMPACT OF FINANCIAL COUNSELING ON FINANCIAL STABILITY ANALYSIS OF THE NEW YORK CITY MODEL By J. Michael Collins, Cathie Mahon, Monica Martinez, & Karen Walsh

CFS Research Brief (FLRC 11-9) October 2011 IMPACT OF FINANCIAL COUNSELING ON FINANCIAL STABILITY ANALYSIS OF THE NEW YORK CITY MODEL By J. Michael Collins, Cathie Mahon, Monica Martinez, & Karen Walsh

Student Loan Debt Statistics In 2018: A $1.5 Trillion Crisis

36,777 views Jun 13, 2018, 08:32am Student Loan Debt Statistics In 2018: A $1.5 Trillion Crisis Zack Friedman Senior Contributor i Shutterstock Student loan debt is now the second highest consumer debt

36,777 views Jun 13, 2018, 08:32am Student Loan Debt Statistics In 2018: A $1.5 Trillion Crisis Zack Friedman Senior Contributor i Shutterstock Student loan debt is now the second highest consumer debt

Online Appendix for: Minimum Wages and Consumer Credit: Lisa J. Dettling and Joanne W. Hsu

Online Appendix for: Minimum Wages and Consumer Credit: Impacts on Access to Credit and Traditional and High-Cost Borrowing Lisa J. Dettling and Joanne W. Hsu A1 Appendix Figure 1: Regional Representation

Online Appendix for: Minimum Wages and Consumer Credit: Impacts on Access to Credit and Traditional and High-Cost Borrowing Lisa J. Dettling and Joanne W. Hsu A1 Appendix Figure 1: Regional Representation

Impact of Financial Education Mandates on Younger Consumers Use of Alternative Financial Services

Impact of Financial Education Mandates on Younger Consumers Use of Alternative Financial Services Melody Harvey 1 Pardee RAND Graduate School ABSTRACT Financial literacy in the United States remains alarmingly

Impact of Financial Education Mandates on Younger Consumers Use of Alternative Financial Services Melody Harvey 1 Pardee RAND Graduate School ABSTRACT Financial literacy in the United States remains alarmingly

Florida: An Economic Overview

Florida: An Economic Overview December 26, 2018 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Shifting in Key Economic Variables

Florida: An Economic Overview December 26, 2018 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Shifting in Key Economic Variables

HOW THE H&R BLOCK BUDGET CHALLENGE

HOW THE MEETS THE COUNCIL FOR ECONOMIC EDUCATION (CEE) NATIONAL STANDARDS FOR FINANCIAL LITERACY WHAT ARE THE CEE STANDARDS FOR FINANCIAL LITERACY FOR PERSONAL FINANCE? The CEE Standards for Financial

HOW THE MEETS THE COUNCIL FOR ECONOMIC EDUCATION (CEE) NATIONAL STANDARDS FOR FINANCIAL LITERACY WHAT ARE THE CEE STANDARDS FOR FINANCIAL LITERACY FOR PERSONAL FINANCE? The CEE Standards for Financial

CFPB Data Point: Becoming Credit Visible

June 2017 CFPB Data Point: Becoming Credit Visible The CFPB Office of Research p Kenneth P. Brevoort p Michelle Kambara This is another in an occasional series of publications from the Consumer Financial

June 2017 CFPB Data Point: Becoming Credit Visible The CFPB Office of Research p Kenneth P. Brevoort p Michelle Kambara This is another in an occasional series of publications from the Consumer Financial

Financial Education and the Debt Behavior of the Young

Federal Reserve Bank of New York Staff Reports Financial Education and the Debt Behavior of the Young Meta Brown Wilbert van der Klaauw Jaya Wen Basit Zafar Staff Report No. 634 September 2013 This paper

Federal Reserve Bank of New York Staff Reports Financial Education and the Debt Behavior of the Young Meta Brown Wilbert van der Klaauw Jaya Wen Basit Zafar Staff Report No. 634 September 2013 This paper

TRENDS IN HEALTH INSURANCE COVERAGE IN GEORGIA

TRENDS IN HEALTH INSURANCE COVERAGE IN GEORGIA Georgia Health Policy Center, Andrew Young School of Policy Studies and Center for Health Services Research, Institute of Health Administration J. Mack Robinson

TRENDS IN HEALTH INSURANCE COVERAGE IN GEORGIA Georgia Health Policy Center, Andrew Young School of Policy Studies and Center for Health Services Research, Institute of Health Administration J. Mack Robinson

NYFed s Center for Microeconomic Data currently houses two major data collection efforts:

Presentation Outline NYFed s Center for Microeconomic Data currently houses two major data collection efforts: Survey of Consumer Expectations (SCE) NYFed Consumer Credit Panel (CCP) For each: Brief description

Presentation Outline NYFed s Center for Microeconomic Data currently houses two major data collection efforts: Survey of Consumer Expectations (SCE) NYFed Consumer Credit Panel (CCP) For each: Brief description

PAGE ONE Economics TEACHER EDITION. Education, Income, and Wealth

TEACHER EDITION Page One Economics is an informative accessible essay on timely economic issues. The Teacher Edition provides the essay; student questions with answers; and additional lesson ideas for

TEACHER EDITION Page One Economics is an informative accessible essay on timely economic issues. The Teacher Edition provides the essay; student questions with answers; and additional lesson ideas for

STATE OF WORKING ARIZONA

Fall, 2008 STATE OF WORKING ARIZONA Public Policy Helps Arizona Families Move Ahead with Education, Child Care and Health Care In 2008, the mortgage crisis toppled Arizona s housing market, dramatically

Fall, 2008 STATE OF WORKING ARIZONA Public Policy Helps Arizona Families Move Ahead with Education, Child Care and Health Care In 2008, the mortgage crisis toppled Arizona s housing market, dramatically

National Conference of State Legislatures. Women s Legislative Network

National Conference of State Legislatures Women s Legislative Network July 24, 2008 1 Marsha A. Goetting Ph.D., CFP, CFCS Professor & Extension Family Economics Specialist Department of Agricultural Economics

National Conference of State Legislatures Women s Legislative Network July 24, 2008 1 Marsha A. Goetting Ph.D., CFP, CFCS Professor & Extension Family Economics Specialist Department of Agricultural Economics

Teacher's Guide. Lesson Five. Buying a Home 04/09

Teacher's Guide $ Lesson Five Buying a Home 04/09 buying a home websites Buying a Home is a major life milestone that requires some thoughtful planning and know-how. Students need to understand all aspects

Teacher's Guide $ Lesson Five Buying a Home 04/09 buying a home websites Buying a Home is a major life milestone that requires some thoughtful planning and know-how. Students need to understand all aspects

EverFi - Financial Literacy

EverFi - Financial Literacy EverFi - Financial Literacy teaches, assesses and certifies students in critical financial concepts through the latest online, interactive curriculum including 3D gaming, animations,

EverFi - Financial Literacy EverFi - Financial Literacy teaches, assesses and certifies students in critical financial concepts through the latest online, interactive curriculum including 3D gaming, animations,

Student Loan Debt Worries May Be Overstated

WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS June 12, 2018 Michael Taylor, CFA Investment Strategy Analyst Student Loan Debt Worries May Be Overstated Key takeaways» Today, U.S. student loan debt

WEEKLY GUIDANCE ON ECONOMIC AND GEOPOLITICAL EVENTS June 12, 2018 Michael Taylor, CFA Investment Strategy Analyst Student Loan Debt Worries May Be Overstated Key takeaways» Today, U.S. student loan debt

Does providing FICO Scores influence financial behavior?

Power of Our Past Force of Our Future Does providing FICO Scores influence financial behavior? October 2018 Jeff Johnston, MBA Sallie Mae Ohio Association of Student Financial Aid Administrators 50th Anniversary

Power of Our Past Force of Our Future Does providing FICO Scores influence financial behavior? October 2018 Jeff Johnston, MBA Sallie Mae Ohio Association of Student Financial Aid Administrators 50th Anniversary

Empirical Tools of Public Economics. Part-2

Empirical Tools of Public Economics Part-2 Outline 3.1. Correlation vs. Causality 3.2. Ideal case: Randomized Trials 3.3. Reality: Observational Data Observational data: Data generated by individual behavior

Empirical Tools of Public Economics Part-2 Outline 3.1. Correlation vs. Causality 3.2. Ideal case: Randomized Trials 3.3. Reality: Observational Data Observational data: Data generated by individual behavior

Money Management Curriculum Overview

Teaching Notes: The money management curriculum will help students understand their financial standing and create a plan that will help them succeed in improving their financial future. There are eight

Teaching Notes: The money management curriculum will help students understand their financial standing and create a plan that will help them succeed in improving their financial future. There are eight

Trends Report Alternative Financial Services Lending Trends Insights into the Industry and Its Consumers

Trends Report 2018 Alternative Financial Services Lending Trends Insights into the Industry and Its Consumers 2018 Alternative Financial Services Lending Trends Overview How subprime borrower behavior

Trends Report 2018 Alternative Financial Services Lending Trends Insights into the Industry and Its Consumers 2018 Alternative Financial Services Lending Trends Overview How subprime borrower behavior

THE FINANCIAL PLANNER S GUIDE TO STUDENT LOAN REFINANCING

THE FINANCIAL PLANNER S GUIDE TO STUDENT LOAN REFINANCING ADVISING CLIENTS WITH STUDENT LOANS Financial planners today have more clients dealing with student loans than ever before. Outstanding student

THE FINANCIAL PLANNER S GUIDE TO STUDENT LOAN REFINANCING ADVISING CLIENTS WITH STUDENT LOANS Financial planners today have more clients dealing with student loans than ever before. Outstanding student

Marketplaces Investing Basics

Marketplaces Investing Basics Curriculum Guide Recommended Grade Level 9-12 Subject Fit Business, Economics, Social Studies, and CTE Total Time 5 modules, 10-20 minutes each Standards Alignment Jump$tart

Marketplaces Investing Basics Curriculum Guide Recommended Grade Level 9-12 Subject Fit Business, Economics, Social Studies, and CTE Total Time 5 modules, 10-20 minutes each Standards Alignment Jump$tart

Uninsured Children : Charting the Nation s Progress

Uninsured Children 2009-2011: Charting the Nation s Progress by Joan Alker, Tara Mancini, and Martha Heberlein Key Findings 1. 2. 3. While nationally children s coverage rates continued to improve, more

Uninsured Children 2009-2011: Charting the Nation s Progress by Joan Alker, Tara Mancini, and Martha Heberlein Key Findings 1. 2. 3. While nationally children s coverage rates continued to improve, more

EverFi Financial Literacy Cumulative Exam

EverFi Financial Literacy Cumulative Exam Module 1: Savings 1. Use the Rule of 72 to calculate how long it will take for your money to double if it s earning 6% in interest: a. 12yrs b. 16yrs c. 36yrs

EverFi Financial Literacy Cumulative Exam Module 1: Savings 1. Use the Rule of 72 to calculate how long it will take for your money to double if it s earning 6% in interest: a. 12yrs b. 16yrs c. 36yrs

February 12, 2009 SHARE Annual Meeting Philadelphia, PA. Joel Cantor*,Alan Monheit*,^, Dina Belloff*, Derek DeLia* and Margaret Koller*

Evaluating State Policies to Extend Adult Dependent Coverage to Young Adults February 12, 2009 SHARE Annual Meeting Philadelphia, PA Joel Cantor*,Alan Monheit*,^, Dina Belloff*, Derek DeLia* and Margaret

Evaluating State Policies to Extend Adult Dependent Coverage to Young Adults February 12, 2009 SHARE Annual Meeting Philadelphia, PA Joel Cantor*,Alan Monheit*,^, Dina Belloff*, Derek DeLia* and Margaret

The Impacts of State Tax Structure: A Panel Analysis

The Impacts of State Tax Structure: A Panel Analysis Jacob Goss and Chang Liu0F* University of Wisconsin-Madison August 29, 2018 Abstract From a panel study of states across the U.S., we find that the

The Impacts of State Tax Structure: A Panel Analysis Jacob Goss and Chang Liu0F* University of Wisconsin-Madison August 29, 2018 Abstract From a panel study of states across the U.S., we find that the

Health Insurance Coverage in 2014: Significant Progress, but Gaps Remain

ACA Implementation Monitoring and Tracking Health Insurance Coverage in 2014: Significant Progress, but Gaps Remain September 2016 By Laura Skopec, John Holahan, and Patricia Solleveld With support from

ACA Implementation Monitoring and Tracking Health Insurance Coverage in 2014: Significant Progress, but Gaps Remain September 2016 By Laura Skopec, John Holahan, and Patricia Solleveld With support from

DO INCOME PROJECTIONS AFFECT RETIREMENT SAVING?

April 2013, Number 13-4 RETIREMENT RESEARCH DO INCOME PROJECTIONS AFFECT RETIREMENT SAVING? By Gopi Shah Goda, Colleen Flaherty Manchester, and Aaron Sojourner* Introduction Americans retirement security

April 2013, Number 13-4 RETIREMENT RESEARCH DO INCOME PROJECTIONS AFFECT RETIREMENT SAVING? By Gopi Shah Goda, Colleen Flaherty Manchester, and Aaron Sojourner* Introduction Americans retirement security

Do School District Bond Guarantee Programs Matter?

Providence College DigitalCommons@Providence Economics Student Papers Economics 12-2013 Do School District Bond Guarantee Programs Matter? Michael Cirrotti Providence College Follow this and additional

Providence College DigitalCommons@Providence Economics Student Papers Economics 12-2013 Do School District Bond Guarantee Programs Matter? Michael Cirrotti Providence College Follow this and additional

While one in five Californians overall is uninsured, the rate among those who work is even higher: one in four.

: By the Numbers December 2013 Introduction California had the greatest number of uninsured residents of any state, 7 million, and the seventh largest percentage of uninsured residents under 65 in the

: By the Numbers December 2013 Introduction California had the greatest number of uninsured residents of any state, 7 million, and the seventh largest percentage of uninsured residents under 65 in the

Student Loans Is There a Crisis?

Student Loans Is There a Crisis? Economic Education Advisory Council of the Federal Reserve Bank of Kansas City September 27, 2012 Kelly D. Edmiston Federal Reserve Bank of Kansas City Access to full report

Student Loans Is There a Crisis? Economic Education Advisory Council of the Federal Reserve Bank of Kansas City September 27, 2012 Kelly D. Edmiston Federal Reserve Bank of Kansas City Access to full report

MANAGING PERSONAL FINANCES

MANAGING PERSONAL FINANCES FACILITATOR: PATRICK WAMEYO ACIB (UK), MBA FINANCIAL LITERACY EDUCATOR & COACH +254 723 786 362 +254 732 786 362 #pwameyo A LIFE TIME APPROACH Theme PAY CHEQUE TO ME INCORPORATION

MANAGING PERSONAL FINANCES FACILITATOR: PATRICK WAMEYO ACIB (UK), MBA FINANCIAL LITERACY EDUCATOR & COACH +254 723 786 362 +254 732 786 362 #pwameyo A LIFE TIME APPROACH Theme PAY CHEQUE TO ME INCORPORATION

NASRA ISSUE BRIEF: Cost-of-Living Adjustments

NASRA ISSUE BRIEF: Cost-of-Living Adjustments February 2014 Cost-of-living adjustments (COLAs) in some form are provided on most state and local government pensions. The purpose of a COLA is to offset

NASRA ISSUE BRIEF: Cost-of-Living Adjustments February 2014 Cost-of-living adjustments (COLAs) in some form are provided on most state and local government pensions. The purpose of a COLA is to offset

Policy lessons from Illinois exodus of people and money By J. Scott Moody and Wendy P. Warcholik Illinois Policy Institute Senior Fellows

ILLINOIS POLICY INSTITUTE SPECIAL REPORT JULY 2014 Policy lessons from Illinois exodus of people and money By J. Scott Moody and Wendy P. Warcholik Illinois Policy Institute Senior Fellows Executive summary

ILLINOIS POLICY INSTITUTE SPECIAL REPORT JULY 2014 Policy lessons from Illinois exodus of people and money By J. Scott Moody and Wendy P. Warcholik Illinois Policy Institute Senior Fellows Executive summary

Debt. In the third quarter of 2016, the upward. Consumer Debt Growth Stalls Despite Strong Sectors. Executive Summary

VOL., ISSUE 3, COVERING 6:Q3 Debt Consumer Debt Growth Stalls Despite Strong Sectors By Lowell R. Ricketts and Don E. Schlagenhauf In the third quarter of 6, the upward trend in per capita consumer debt

VOL., ISSUE 3, COVERING 6:Q3 Debt Consumer Debt Growth Stalls Despite Strong Sectors By Lowell R. Ricketts and Don E. Schlagenhauf In the third quarter of 6, the upward trend in per capita consumer debt

David Newhouse Daniel Suryadarma

David Newhouse Daniel Suryadarma Outline of presentation 1. Motivation Vocational education expansion 2. Data 3. Determinants of choice of type 4. Effects of high school type Entire sample Cohort vs. age

David Newhouse Daniel Suryadarma Outline of presentation 1. Motivation Vocational education expansion 2. Data 3. Determinants of choice of type 4. Effects of high school type Entire sample Cohort vs. age

Labor Regulation, Enforcement, and Employment: Lessons from China. Albert Park Hong Kong University of Science and Technology

Labor Regulation, Enforcement, and Employment: Lessons from China Albert Park Hong Kong University of Science and Technology Motivations Debates over optimal labor regulation Concerns about enforcement

Labor Regulation, Enforcement, and Employment: Lessons from China Albert Park Hong Kong University of Science and Technology Motivations Debates over optimal labor regulation Concerns about enforcement

Update: Obamacare s Impact on Small Business Wages and Employment Sam Batkins, Ben Gitis

Update: Obamacare s Impact on Small Business Wages and Employment Sam Batkins, Ben Gitis Executive Summary Research from the American Action Forum (AAF) finds regulations from the Affordable Care Act (ACA)

Update: Obamacare s Impact on Small Business Wages and Employment Sam Batkins, Ben Gitis Executive Summary Research from the American Action Forum (AAF) finds regulations from the Affordable Care Act (ACA)

Working Papers WP January 2018

Working Papers WP 18-03 January 2018 https://doi.org/10.21799/frbp.wp.2018.03 Did the ACA s Dependent Coverage Mandate Reduce Financial Distress for Young Adults? Nathan Blascak Federal Reserve Bank of

Working Papers WP 18-03 January 2018 https://doi.org/10.21799/frbp.wp.2018.03 Did the ACA s Dependent Coverage Mandate Reduce Financial Distress for Young Adults? Nathan Blascak Federal Reserve Bank of

Ken Goodgames Chief Executive Officer Transformance

Ken Goodgames Chief Executive Officer Transformance Cornerstone Credit Union Foundation FOCUS Summit MARCH 3, 2016 ABOUT TRANSFORMANCE Learning & Development Solutions: From crisis counseling & community

Ken Goodgames Chief Executive Officer Transformance Cornerstone Credit Union Foundation FOCUS Summit MARCH 3, 2016 ABOUT TRANSFORMANCE Learning & Development Solutions: From crisis counseling & community

2/3 81% 67% Millennials and money. Key insights. Millennials are optimistic despite a challenging start to adulthood

2/3 Proportion of Millennials who believe they will achieve a greater standard of living than their parents 81% Percentage of Millennials who believe they need to pay off their debts before they can begin

2/3 Proportion of Millennials who believe they will achieve a greater standard of living than their parents 81% Percentage of Millennials who believe they need to pay off their debts before they can begin

Nearly Half of All Americans Don t Pay Income Taxes

Nearly Half of All Americans Don t Pay Income Taxes Percentage of U.S. Population Not Represented on a Taxable Return 50% 49.5% 40% 34.1% 30% 23.7% 20% 10% 12% 0% 1962 1970 1980 1990 2000 2009 Note: Figures

Nearly Half of All Americans Don t Pay Income Taxes Percentage of U.S. Population Not Represented on a Taxable Return 50% 49.5% 40% 34.1% 30% 23.7% 20% 10% 12% 0% 1962 1970 1980 1990 2000 2009 Note: Figures

Economic Vulnerability and Financial Fragility

USRT Conference: Underserved Roundtable Economic Vulnerability and Financial Fragility March 18, 2014 William R. Emmons Center for Household Financial Stability Federal Reserve Bank of St. Louis William.R.Emmons@stls.frb.org

USRT Conference: Underserved Roundtable Economic Vulnerability and Financial Fragility March 18, 2014 William R. Emmons Center for Household Financial Stability Federal Reserve Bank of St. Louis William.R.Emmons@stls.frb.org

Depositor Runs and Financial Literacy by Kim

Depositor Runs and Financial Literacy by Kim Discussant: Andres Liberman (NYU) FRS 2016 June 3, 2016 Summary of the paper Question: does depositor behavior during a bank run vary with financial literacy?

Depositor Runs and Financial Literacy by Kim Discussant: Andres Liberman (NYU) FRS 2016 June 3, 2016 Summary of the paper Question: does depositor behavior during a bank run vary with financial literacy?

Credit Market Consequences of Credit Flag Removals *

Credit Market Consequences of Credit Flag Removals * Will Dobbie Benjamin J. Keys Neale Mahoney July 7, 2017 Abstract This paper estimates the impact of a credit report with derogatory marks on financial

Credit Market Consequences of Credit Flag Removals * Will Dobbie Benjamin J. Keys Neale Mahoney July 7, 2017 Abstract This paper estimates the impact of a credit report with derogatory marks on financial

TASK: What is the True Cost of Purchasing an Automobile?

This task was developed by secondary mathematics and CTE teachers across Washington State from urban and rural areas. These teachers have incorporated financial literacy in their classroom and have received

This task was developed by secondary mathematics and CTE teachers across Washington State from urban and rural areas. These teachers have incorporated financial literacy in their classroom and have received

HOW THE H&R BLOCK BUDGET CHALLENGE

HOW THE MEETS THE JUMP$TART NATIONAL STANDARDS IN K-12 PERSONAL FINANCE EDUCATION WHAT ARE THE JUMP$TART NATIONAL STANDARDS FOR PERSONAL FINANCE? The National Standards in K-12 Personal Finance Education,

HOW THE MEETS THE JUMP$TART NATIONAL STANDARDS IN K-12 PERSONAL FINANCE EDUCATION WHAT ARE THE JUMP$TART NATIONAL STANDARDS FOR PERSONAL FINANCE? The National Standards in K-12 Personal Finance Education,

Online Appendix for: Consumption Reponses to In-Kind Transfers: Evidence from the Introduction of the Food Stamp Program

Online Appendix for: Consumption Reponses to In-Kind Transfers: Evidence from the Introduction of the Food Stamp Program Hilary W. Hoynes University of California, Davis and NBER hwhoynes@ucdavis.edu and

Online Appendix for: Consumption Reponses to In-Kind Transfers: Evidence from the Introduction of the Food Stamp Program Hilary W. Hoynes University of California, Davis and NBER hwhoynes@ucdavis.edu and

Peer Effects and Retirement Decisions: Evidence from Pension Reform in Germany

Peer Effects and Retirement Decisions: Evidence from Pension Reform in Germany Mary K. Hamman, University of Wisconsin-La Crosse Daniela Hochfellner, New York University David A. Jaeger, CUNY Graduate

Peer Effects and Retirement Decisions: Evidence from Pension Reform in Germany Mary K. Hamman, University of Wisconsin-La Crosse Daniela Hochfellner, New York University David A. Jaeger, CUNY Graduate

Is Financial Knowledge Associated with Past-Due Medical Debt?

H E A L T H P O L I C Y C E N T E R A N D O P P O R T U N I T Y A N D O W N E R S H I P I N I T I A T I V E Is Financial Knowledge Associated with Past-Due Medical Debt? Breno Braga, Signe-Mary McKernan,

H E A L T H P O L I C Y C E N T E R A N D O P P O R T U N I T Y A N D O W N E R S H I P I N I T I A T I V E Is Financial Knowledge Associated with Past-Due Medical Debt? Breno Braga, Signe-Mary McKernan,

Developing Financial Capability Over the Life Course

1 / 51 Developing Financial Capability Over the Life Course J. Michael Collins University of Wisconsin-Madison June 3, 2 / 51 Table of Contents 1 2 3 4 5 6 7 3 / 51 Financial Capability Over the Life Course

1 / 51 Developing Financial Capability Over the Life Course J. Michael Collins University of Wisconsin-Madison June 3, 2 / 51 Table of Contents 1 2 3 4 5 6 7 3 / 51 Financial Capability Over the Life Course

Appendix (for online publication)

") Appendix (for online publication) Figure A1: Log GDP per Capita and Agricultural Share Notes: Table source data is from Gollin, Lagakos, and Waugh (2014), Online Appendix Table 4. Kenya (KEN) and Indonesia

Appendix (for online publication) Figure A1: Log GDP per Capita and Agricultural Share Notes: Table source data is from Gollin, Lagakos, and Waugh (2014), Online Appendix Table 4. Kenya (KEN) and Indonesia

How House Price Dynamics and Credit Constraints affect the Equity Extraction of Senior Homeowners

How House Price Dynamics and Credit Constraints affect the Equity Extraction of Senior Homeowners Stephanie Moulton, John Glenn College of Public Affairs, The Ohio State University Donald Haurin, Department

How House Price Dynamics and Credit Constraints affect the Equity Extraction of Senior Homeowners Stephanie Moulton, John Glenn College of Public Affairs, The Ohio State University Donald Haurin, Department

EVERFI Financial Literacy

EVERFI Financial Literacy EVERFI - Financial Literacy builds the foundation for students future financial well being. Covering everything from common account types to the basics of investing, each module

EVERFI Financial Literacy EVERFI - Financial Literacy builds the foundation for students future financial well being. Covering everything from common account types to the basics of investing, each module

Underwater on Student Debt

E D U C A T I O N P O L I C Y P R O G R A M RE S E ARCH RE P O R T Underwater on Student Debt Understanding Consumer Credit and Student Loan Default Kristin Blagg August 2018 AB O U T T H E U R BA N I

E D U C A T I O N P O L I C Y P R O G R A M RE S E ARCH RE P O R T Underwater on Student Debt Understanding Consumer Credit and Student Loan Default Kristin Blagg August 2018 AB O U T T H E U R BA N I

State Dependency of Monetary Policy: The Refinancing Channel

State Dependency of Monetary Policy: The Refinancing Channel Martin Eichenbaum, Sergio Rebelo, and Arlene Wong May 2018 Motivation In the US, bulk of household borrowing is in fixed rate mortgages with

State Dependency of Monetary Policy: The Refinancing Channel Martin Eichenbaum, Sergio Rebelo, and Arlene Wong May 2018 Motivation In the US, bulk of household borrowing is in fixed rate mortgages with

Mortgage Rates, Household Balance Sheets, and the Real Economy

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

Effects of working part-time and full-time on physical and mental health in old age in Europe

Effects of working part-time and full-time on physical and mental health in old age in Europe Tunga Kantarcı Ingo Kolodziej Tilburg University and Netspar RWI - Leibniz Institute for Economic Research

Effects of working part-time and full-time on physical and mental health in old age in Europe Tunga Kantarcı Ingo Kolodziej Tilburg University and Netspar RWI - Leibniz Institute for Economic Research

Policy Evaluation: Methods for Testing Household Programs & Interventions

Policy Evaluation: Methods for Testing Household Programs & Interventions Adair Morse University of Chicago Federal Reserve Forum on Consumer Research & Testing: Tools for Evidence-based Policymaking in

Policy Evaluation: Methods for Testing Household Programs & Interventions Adair Morse University of Chicago Federal Reserve Forum on Consumer Research & Testing: Tools for Evidence-based Policymaking in

Information Use and Attention Deferment in College Student Loan Decisions

Information Use and Attention Deferment in College Student Loan Decisions Rajeev Darolia University of Missouri New York Federal Reserve Bank April 27, 2017 1 Motivation Increasing focus on risk in higher

Information Use and Attention Deferment in College Student Loan Decisions Rajeev Darolia University of Missouri New York Federal Reserve Bank April 27, 2017 1 Motivation Increasing focus on risk in higher

Why is voluntary financial education so unpopular? Experimental evidence from Mexico

Why is voluntary financial education so unpopular? Experimental evidence from Mexico Miriam Bruhn, World Bank Gabriel Lara Ibarra, World Bank David McKenzie, World Bank Understanding Banks in Emerging

Why is voluntary financial education so unpopular? Experimental evidence from Mexico Miriam Bruhn, World Bank Gabriel Lara Ibarra, World Bank David McKenzie, World Bank Understanding Banks in Emerging

BTC Reports WHAT S THE HARM? PLENTY. Unemployment Insurance Changes Threaten the State s Economy and Hurt the Unemployed

BTC Reports BUDGET & TAX CENTER VOLUME 20 NUMBER 5 July 2014 ENJOY READING THESE REPORTS? Please consider making a donation to support the Budget & tax Center at www.ncjustice.org WHAT S THE HARM? PLENTY.

BTC Reports BUDGET & TAX CENTER VOLUME 20 NUMBER 5 July 2014 ENJOY READING THESE REPORTS? Please consider making a donation to support the Budget & tax Center at www.ncjustice.org WHAT S THE HARM? PLENTY.

Session III Differences in Differences (Dif- and Panel Data

Session III Differences in Differences (Dif- in-dif) and Panel Data Christel Vermeersch March 2007 Human Development Network Middle East and North Africa Region Spanish Impact Evaluation Fund Structure

Session III Differences in Differences (Dif- in-dif) and Panel Data Christel Vermeersch March 2007 Human Development Network Middle East and North Africa Region Spanish Impact Evaluation Fund Structure

Personalized Information as a Tool to Improve Pension Savings

Personalized Information as a Tool to Improve Pension Savings Results from a Randomized Control Trial in Chile Olga Fuentes (SP) Jeanne Lafortune (PUC) Julio Riutort (UAI) José Tessada (PUC) Félix Villatoro

Personalized Information as a Tool to Improve Pension Savings Results from a Randomized Control Trial in Chile Olga Fuentes (SP) Jeanne Lafortune (PUC) Julio Riutort (UAI) José Tessada (PUC) Félix Villatoro

The U.S. Housing Market: Where Is It Heading?

The U.S. Housing Market: Where Is It Heading? Anthony Murphy Federal Reserve Bank of Dallas Sul Ross State University, Alpine TX 29 October 2014 The views expressed are those of the author and do not reflect

The U.S. Housing Market: Where Is It Heading? Anthony Murphy Federal Reserve Bank of Dallas Sul Ross State University, Alpine TX 29 October 2014 The views expressed are those of the author and do not reflect

EDA Redevelopment Area Analysis. Lawrence Wood Amy Glasmeier Fall 2003 One Nation, Pulling Apart

EDA Redevelopment Area Analysis Lawrence Wood Amy Glasmeier Fall 2003 One Nation, Pulling Apart I. Introduction In accordance with the Area Redevelopment Act (Public Law 87-27), in 1965 the EDA designated

EDA Redevelopment Area Analysis Lawrence Wood Amy Glasmeier Fall 2003 One Nation, Pulling Apart I. Introduction In accordance with the Area Redevelopment Act (Public Law 87-27), in 1965 the EDA designated

Electronic Supplementary Material for the Article: The Impact of Internet Diffusion on Marriage Rates: Evidence from the Broadband Market

Electronic Supplementary Material for the Article: The Impact of Internet Diffusion on Marriage Rates: Evidence from the Broadband Market By Andriana Bellou 1 Appendix A. Data Definitions and Sources This

Electronic Supplementary Material for the Article: The Impact of Internet Diffusion on Marriage Rates: Evidence from the Broadband Market By Andriana Bellou 1 Appendix A. Data Definitions and Sources This

Investor Testing of Target Date Retirement Fund (TDF) Comprehension and Communications

Comprehension and Communications") Investor Testing of Target Date Retirement Fund (TDF) Comprehension and Communications Submitted to: The U.S. Securities and Exchange Commission February 15, 2012 This study presents the findings of Siegel

Investor Testing of Target Date Retirement Fund (TDF) Comprehension and Communications Submitted to: The U.S. Securities and Exchange Commission February 15, 2012 This study presents the findings of Siegel

Shale Gas Development and Housing Values Over a Decade: Evidence from the Barnett Shale

Shale Gas Development and Housing Values Over a Decade: Evidence from the Barnett Shale Jeremy G. Weber (USDA/Economic Research Service) Wesley Burnett (West Virginia University) Irene M. Xiarchos (USDA/Office

Shale Gas Development and Housing Values Over a Decade: Evidence from the Barnett Shale Jeremy G. Weber (USDA/Economic Research Service) Wesley Burnett (West Virginia University) Irene M. Xiarchos (USDA/Office

The Effects of the Dependent Coverage Mandates on Fathers Job Mobility and Compensation

1/44 The Effects of the Dependent Coverage Mandates on Fathers Job Mobility and Compensation Dajung Jun Michigan State University October 31, 2018 The research in this paper was conducted while the author

1/44 The Effects of the Dependent Coverage Mandates on Fathers Job Mobility and Compensation Dajung Jun Michigan State University October 31, 2018 The research in this paper was conducted while the author

The Evolution of Household Leverage During the Recovery

ECONOMIC COMMENTARY Number 2014-17 September 2, 2014 The Evolution of Household Leverage During the Recovery Stephan Whitaker Recent research has shown that geographic areas that experienced greater household

ECONOMIC COMMENTARY Number 2014-17 September 2, 2014 The Evolution of Household Leverage During the Recovery Stephan Whitaker Recent research has shown that geographic areas that experienced greater household

TASK: Interest Comparison

This task was developed by secondary mathematics and CTE teachers across Washington State from urban and rural areas. These teachers have incorporated financial literacy in their classroom and have received

This task was developed by secondary mathematics and CTE teachers across Washington State from urban and rural areas. These teachers have incorporated financial literacy in their classroom and have received

Course Outcome Summary

SSECON ECONOMICS Course Information: Description: Economics is the study of how individuals and nations make choices about how to use scarce resources to fulfill their wants. This course will examine economics

SSECON ECONOMICS Course Information: Description: Economics is the study of how individuals and nations make choices about how to use scarce resources to fulfill their wants. This course will examine economics

Early Impact of the Affordable Care Act on Health Insurance Coverage of Young Adults

Early Impact of the Affordable Care Act on Health Insurance Coverage of Young Adults AcademyHealth State Health Research and Policy Interest Group Meeting June 23, 2012 Orlando, FL Joel C. Cantor, ScD;

Early Impact of the Affordable Care Act on Health Insurance Coverage of Young Adults AcademyHealth State Health Research and Policy Interest Group Meeting June 23, 2012 Orlando, FL Joel C. Cantor, ScD;

Florida: An Economic Overview

Florida: An Economic Overview February 7, 2018 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Residential Credit Still Difficult to

Florida: An Economic Overview February 7, 2018 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Residential Credit Still Difficult to

Brookings Papers on Economic Activity

Brookings Papers on Economic Activity Brookings Papers on Economic Activity Fall 2015 Conference A crisis in student loans? How changes in the characteristics of borrowers and in the institutions they

Brookings Papers on Economic Activity Brookings Papers on Economic Activity Fall 2015 Conference A crisis in student loans? How changes in the characteristics of borrowers and in the institutions they

U.S. and Regional Economic Conditions and Outlook

U.S. and Regional Economic Conditions and Outlook CFA Society of Nebraska Omaha, NE January 14, 215 Kelly D. Edmiston Federal Reserve Bank of Kansas City Outline Structure and Role of the Federal Reserve

U.S. and Regional Economic Conditions and Outlook CFA Society of Nebraska Omaha, NE January 14, 215 Kelly D. Edmiston Federal Reserve Bank of Kansas City Outline Structure and Role of the Federal Reserve

The State of Young Adult s Balance Sheets: Evidence from the Survey of Consumer Finances

The State of Young Adult s Balance Sheets: Evidence from the Survey of Consumer Finances Lisa J. Dettling Federal Reserve Board Joanne W. Hsu Federal Reserve Board May 2014 Abstract In this paper, we investigate

The State of Young Adult s Balance Sheets: Evidence from the Survey of Consumer Finances Lisa J. Dettling Federal Reserve Board Joanne W. Hsu Federal Reserve Board May 2014 Abstract In this paper, we investigate

State Budget Update: March 2011

April 19, 2011 Nearly two years into the US economic recovery, following the end of the Great Recession, state finances are showing encouraging signs of revenue stability. At the same time, budget gaps

April 19, 2011 Nearly two years into the US economic recovery, following the end of the Great Recession, state finances are showing encouraging signs of revenue stability. At the same time, budget gaps

Special Report. Sources of Health Insurance and Characteristics of the Uninsured EBRI EMPLOYEE BENEFIT RESEARCH INSTITUTE

January 1993 Jan. Feb. Sources of Health Insurance and Characteristics of the Uninsured Analysis of the March 1992 Current Population Survey Mar. Apr. May Jun. Jul. Aug. EBRI EMPLOYEE BENEFIT RESEARCH

January 1993 Jan. Feb. Sources of Health Insurance and Characteristics of the Uninsured Analysis of the March 1992 Current Population Survey Mar. Apr. May Jun. Jul. Aug. EBRI EMPLOYEE BENEFIT RESEARCH

The Impact of the Student Debt Crisis on Housing: Five Takeaways for the U.S. Real Estate Industry

The Impact of the Student Debt Crisis on Housing: Five Takeaways for the U.S. Real Estate Industry By Cari Smith, Vice President, and Steven Wang, Senior Associate Between 2000 and 2014, the total volume

The Impact of the Student Debt Crisis on Housing: Five Takeaways for the U.S. Real Estate Industry By Cari Smith, Vice President, and Steven Wang, Senior Associate Between 2000 and 2014, the total volume

ONLINE APPENDIX (NOT FOR PUBLICATION) Appendix A: Appendix Figures and Tables

Appendix A: Appendix Figures and Tables") ONLINE APPENDIX (NOT FOR PUBLICATION) Appendix A: Appendix Figures and Tables 34 Figure A.1: First Page of the Standard Layout 35 Figure A.2: Second Page of the Credit Card Statement 36 Figure A.3: First

ONLINE APPENDIX (NOT FOR PUBLICATION) Appendix A: Appendix Figures and Tables 34 Figure A.1: First Page of the Standard Layout 35 Figure A.2: Second Page of the Credit Card Statement 36 Figure A.3: First

Florida: An Economic Overview

Florida: An Economic Overview January 26, 2016 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

Florida: An Economic Overview January 26, 2016 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

Slow and Low: The Economic and Financial Outlook

Southern Legislative Conference 7th Annual Meeting Slow and Low: The Economic and Financial Outlook July, William R. Emmons Federal Reserve Bank of St. Louis William.R.Emmons@stls.frb.org These comments

Southern Legislative Conference 7th Annual Meeting Slow and Low: The Economic and Financial Outlook July, William R. Emmons Federal Reserve Bank of St. Louis William.R.Emmons@stls.frb.org These comments

Deteriorating Health Insurance Coverage from 2000 to 2010: Coverage Takes the Biggest Hit in the South and Midwest

ACA Implementation Monitoring and Tracking Deteriorating Health Insurance Coverage from 2000 to 2010: Coverage Takes the Biggest Hit in the South and Midwest August 2012 Fredric Blavin, John Holahan, Genevieve

ACA Implementation Monitoring and Tracking Deteriorating Health Insurance Coverage from 2000 to 2010: Coverage Takes the Biggest Hit in the South and Midwest August 2012 Fredric Blavin, John Holahan, Genevieve

Effects of Increased Elderly Employment on Other Workers Employment and Elderly s Earnings in Japan. Ayako Kondo Yokohama National University

Effects of Increased Elderly Employment on Other Workers Employment and Elderly s Earnings in Japan Ayako Kondo Yokohama National University Overview Starting from April 2006, employers in Japan have to

Effects of Increased Elderly Employment on Other Workers Employment and Elderly s Earnings in Japan Ayako Kondo Yokohama National University Overview Starting from April 2006, employers in Japan have to

Providing Subprime Consumers with Access to Credit: Helpful or Harmful? James R. Barth Auburn University

Providing Subprime Consumers with Access to Credit: Helpful or Harmful? James R. Barth Auburn University FICO Scores: Identifying Subprime Consumers Category FICO Score Range Super-prime 740 and Higher

Providing Subprime Consumers with Access to Credit: Helpful or Harmful? James R. Barth Auburn University FICO Scores: Identifying Subprime Consumers Category FICO Score Range Super-prime 740 and Higher

Issue Brief No Sources of Health Insurance and Characteristics of the Uninsured: Analysis of the March 2005 Current Population Survey

Issue Brief No. 287 Sources of Health Insurance and Characteristics of the Uninsured: Analysis of the March 2005 Current Population Survey by Paul Fronstin, EBRI November 2005 This Issue Brief provides

Issue Brief No. 287 Sources of Health Insurance and Characteristics of the Uninsured: Analysis of the March 2005 Current Population Survey by Paul Fronstin, EBRI November 2005 This Issue Brief provides