HOUSING FINANCE PUBLIC HEARING. 13/14 October 2011

|

|

|

- Juliet Small

- 5 years ago

- Views:

Transcription

1 HOUSING FINANCE PUBLIC HEARING 13/14 October 2011

2 FINANCIAL SECTOR CHARTER (FSC) 2

3 FINANCIAL SECTOR CHARTER 3 The Financial Sector Charter will add a deep social dimension to the functioning of our financial system. It goes to the core of how the financial sector will address the urgent need to make business sense of a more sustainable, inclusive and equitable future. At the same time, measures designed to achieve our empowerment & transformational goals must be implemented in such a way that they do not jeopardise ongoing financial stability (Extract from the Trevor Manuel presentation to Financial Sector Campaign Coalition 2005)

4 FINANCIAL SECTOR CHARTER THE CATALYST 4 Concluded in October 2003 FINANCIAL SECTOR CHARTER First measurement period 1 January 2004 to 31 December 2008 Human Resource Develop ment (22) Procurement (15) Enterprise Development Access To Financial Services (18) Ownership & Control in Financial Sector (14) Corporate Social Investment (3) Empowerment Financing Geographic Access Transacti on & Savings Accounts Mzansi Consumer Education (2) BEE Tranaction Financing (5) Low Income Housing Agricultural Development SMEs Infrastruc ture Empowerment Finance (21)

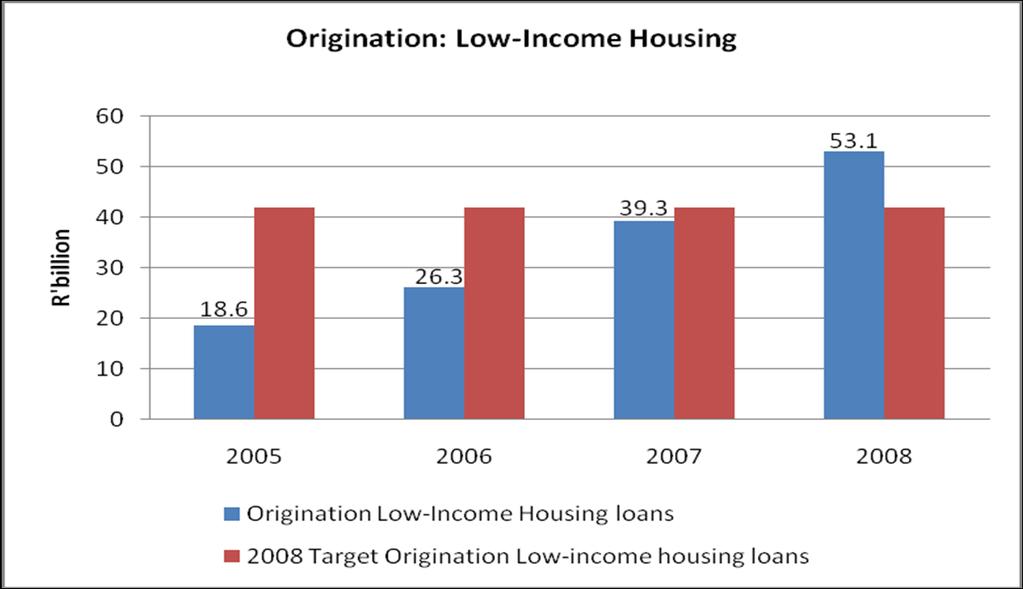

5 FSC EMPOWERMENT FINANCE (HOUSING) COMMITMENTS 5 FSC PERIOD: 1 JANUARY 2004 TO 31 DECEMBER HOUSING FINANCE (MORTGAGES, SECURED/PARTLY SECURED, UNSECURED HOUSING PERSONAL LOANS, RESIDENTIAL DEVELOPMENT LOANS, WHOLESALE LOANS) ORIGINATION TARGET - GROSS SALES TARGETTED INVESTMENTS TARGET - BALANCE OUTSTANDING ON LOANS AS AT 31 DECEMBER 2008 ORIGINATION TARGET 4 MAJOR MORTGAGEES OTHER LENDERS TOTAL R 40 BILLION R 2 BILLION R 42 BILLION TARGETTED INVESTMENTS TARGET (ACTUAL: R31.8 BN) 4 MAJOR MORTGAGEES R 30 BILLION OTHERS R 2 BILLION TOTAL R 32 BILLION TARGET MARKET: HOUSEHOLD GROSS MONTHLY INCOME BETWEEN R1500 AND R7 500 (2004) ADJUSTED ANNUALLY BY CPIX (R1 928-R9 670 IN 2008)

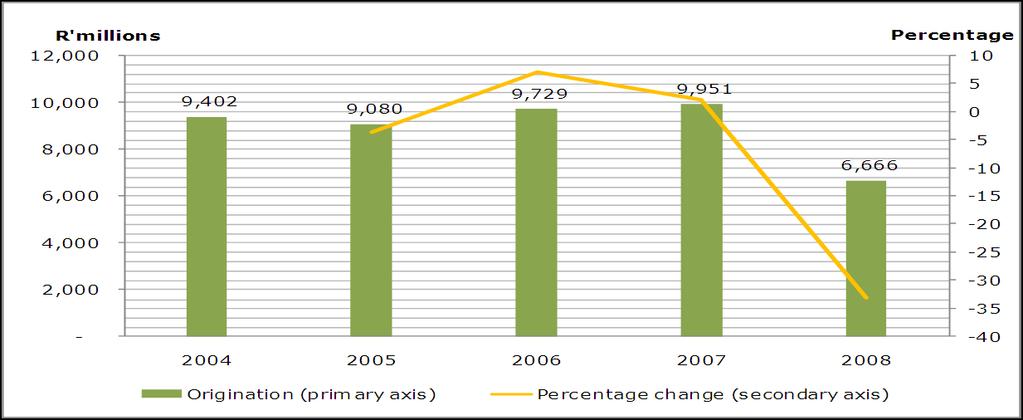

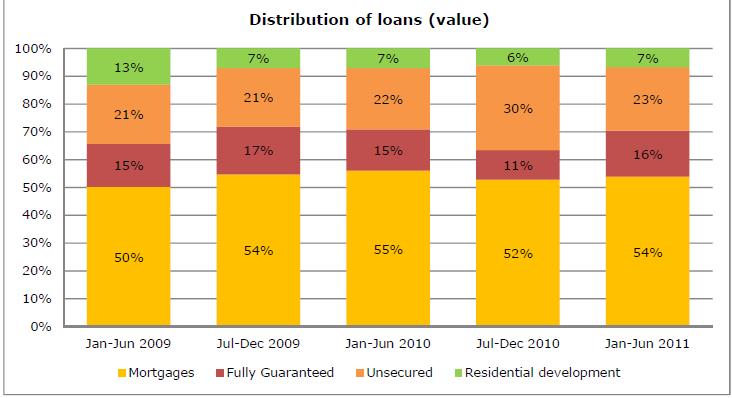

6 ACHIEVEMENTS (VALUE) 6

7 ACHIEVEMENTS (VALUE) 7

8 Figure 12 Low Income Housing INTEREST RATE VOLATILITY 8 AFFORDABILITY IMPACT : AVERAGE MIDDLE INCOME HOUSEHOLD HAD LOST 42% OF THEIR SPENDING POWER IN 2008 (SA PERFECT STORM INTEREST RATE, FUEL, ELECTRICITY, UTILITIES, FOOD, TRANSPORT SPIKES)

9 AFFORDABILITY IMPACT (5% INTEREST RATE INCREASE) 9 Household income Housing affordability prior to interest change Housing affordability after interest change Note: Average minimum entry level price for bonded units is R and so FSC target market for mortgages is now obsolete

11001-16000 8001-11000 6001-8000 4501-6000 3501-4500 2501-3500 1501-2500 6.27% 6.74% 6.82% 7.17% 7.04% 8.96% 11.")

10 INCOME PROFILE 10 Households (%) by Household Income Category % 5.66% FSC Target Market Income Category (Monthly) % 6.74% 6.82% 7.17% 7.04% 8.96% 11.64% Primary 5% Resale 13% Extensions 19% Home Improvements 33% % 8.54% 7.40% 4.84% 5% INCREASE IN INTEREST RATES = R356 EXTRA p.m. PER R BOND OR 26% DECREASE IN AFFORDABILITY 0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00% Number of Households (as %) Source: Global Insight

11 ARREARS 11

12 ARREARS PER SEGMENT 12

VALUE 13")

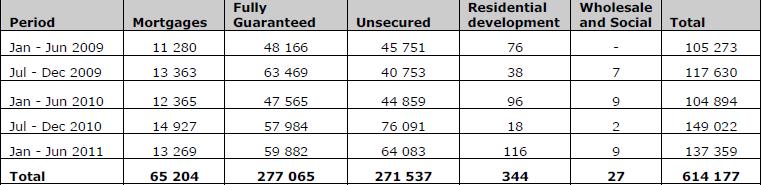

13 PRODUCT MIX (4 MAJOR MORTGAGEES) VALUE 13

")

14 TARGETTED INVESTMENT (4 MAJOR MORTGAGEES) 14

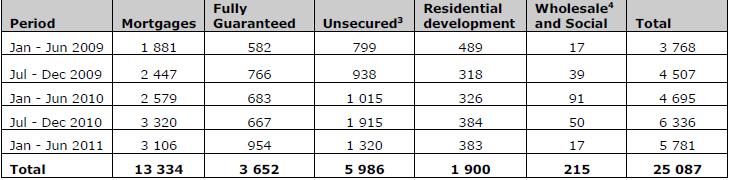

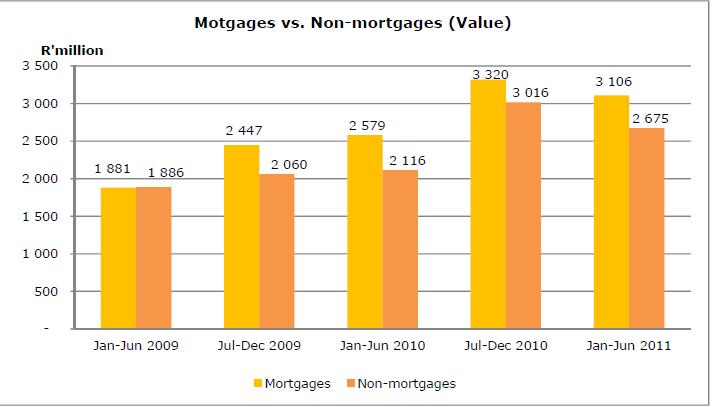

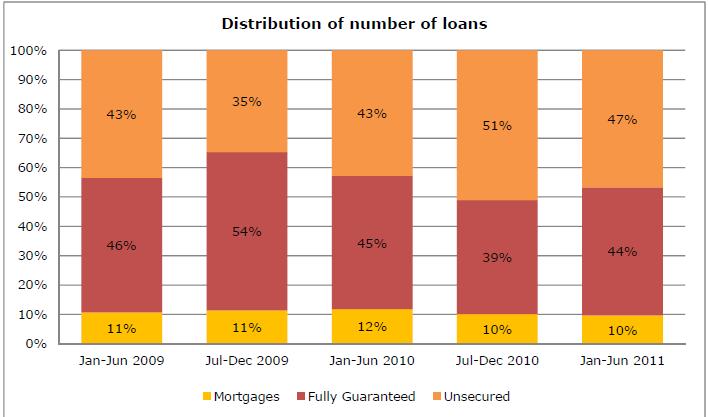

15 ACHIEVEMENTS (NUMBER) 15 Fully Residential Wholesale & Period Mortgage Guaranteed Unsecured Development Social Total Total

16 TARGET MARKET ADJUSTMENT 16 Entry housing from R upwards Alignment to draft DHS Inclusionary Housing definition (FSC +40%) 2011: Gross household income ceiling R adjusted annually by the midpoint between CPI and BCI (equates to a mortgage bond of +- R )

17 ACHIEVEMENTS (VALUE) 17

18 ACHIEVEMENTS (VALUE) 18

19 ACHIEVEMENTS (VALUE) 19

20 ACHIEVEMENTS (NUMBER) 20

21 ACHIEVEMENTS (NUMBER) 21

22 LESSONS LEARNT 22 HOUSING SUPPLY, NOT FINANCE IS THE ISSUE DESPERATE NEED FOR AFFORDABLE NEW BUILDS WITHIN TARGET MARKET NEED FOR KEY PLAYER PARTNERSHIPS INCLUDING COMMITMENTS FSC TARGET MARKET IS COMMERCIALLY VIABLE (HAS BECOME INSTITUTIONALISED WITHIN MEMBER BANK STRUCTURES) DIFFERENTIATED SEGMENTATION APPROACH NEEDED (INCLUDES OPERATING MODEL) AFFORDABILITY AND CREDIT TRACK-RECORDS ARE KEY BORROWER EDUCATION IS ALSO KEY HUMAN SETTLEMENT APPROACH NEEDED (INFRASTRUCTURE BLOCKAGE) AVOID SUB PRIME TRAP AFFORDABLE LONG TERM FIXED INTEREST RATE ESSENTIAL REGULATORY AND THINNESS OF MARKET IMPEDIMENTS CREDIBLE MARKET MAKER

23 UNDERSTANDING THE MARKET 23 R3.5/R12k: Backlog: 1 million units 20% of workers (was in 2004) BNG (subsidy): Backlog: 2.3 million units was 1.2 million in 1994 Informal settlements: were 300 in 1994 now Source: Finmark Trust

24 AFFORDABILITY GAP GAUTENG 24 Source: South African Institute for Race Relations

25 GROWTH IN BUILDING COSTS m 2 FOR AFFORDABLE HOUSING UNITS Average increase of 28% 1700 R/m Jan 2007 Jan 2008 Jan 40m 2 unit 50m 2 unit 60m 2 unit 70m 2 unit 80m 2 unit Source Viruly Consulting

26 DEVELOPER PROFITABILITY (2008) 26

27")

27 INFRASTRUCTURE COST INCREASES (2008) 27

28 COST/SUBSIDY SHORTFALL BNG UNIT Item Actual cost Subsidy limits Variance Raw land assembly R (R24,4m2) R R100 Township Proclamation R R Land servicing* R A-grade services R B-Grade services -R Professional fees R R R1 069 Statutory Approvals/ Enrolment R R R4 082 Top structure R R R5 527 Profit R24 100(17%) R 1 833(2%) -R Total Cost Unit R144,800 R R55,683

29 29 LOANS, SUBSIDY & SUBSIDY SHORTFALL 2008 Loans, Subsidy & Subsidy Shortfall 200, , , , ,000 Shortfall in govt subsidy 75,000 50,000 25,000 +HH affordability - Loan Subsidy Cost of Marketable top structure what paying hhs will accept- 0 1,500 2,000 2,500 3,000 3,500 4,000 4,500 5,000 5,500 6,000 6,500 7,000 7,500 8,000 8,500 9,000 9,500 10,000 Income per household

100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Households per Incom e Band 992,697 9% 637,311 5% 522,121 4% 2,296,955")

30 WHERE ARE WE? 30 Chart A Monthly Household Income Distribution (Source: Adapted from Rust, 2009) 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Households per Incom e Band 992,697 9% 637,311 5% 522,121 4% 2,296,955 18% 3,539, % 4,469,158 36% 7% of South African adults are mortgage holders 45% have formal property title but no mortgage 24% only have informal title 24% rent 18% of households can only afford to buy a new home R R12001 R18000 R9001 R12000 R3501 R9000 R1501 R3500 <R1500

31 UNDERSTANDING THE MARKET 31

32 HOUSEHOLD DEBT TO DISPOSABLE INCOME 32

33 UNDERSTANDING THE MARKET 33 SOURCE: ABSA SOURCE: SARB

34 AFFORDABILITY GAP 34

35 WHERE ARE WE? 35

?")

36 WHERE ARE WE (CONT)? 36

37 WHERE ARE WE (CONT)? 37 Source: World bank

38 CAN BANKS DO MORE? ABSOLUTELY (COMPETITION, INNOVATION, PARTNERSHIPS, CHANGE SUBSIDY MODEL TEMPORARY BENEFICIARIES, REDUCE MINIMUM STANDARDS FOR SUBSIDY HOUSING, LENDERS TO FINANCE BNG SPEC UNITS?) BUT NOT SUB PRIME (USA LESSON). BANKS HAVE FIDUCIARY RESPONSIBILITY (DEPOSITORS, INVESTORS MONEY AT RISK) MEANINGFUL HONEST PARTNERSHIP (GOVT. (3 TIERS), DEVELOPERS, SELECTIVE EMPLOYERS, LENDERS, MATERIAL SUPPLIERS) INFRASTRUCTURE RETHINK? DELIVERY MODEL DENSIFICATION (SPRAWL COSTS PLUS PROMOTES INCOME APARTHEID) INFORMAL SETTLEMENTS SOLVENCY OF MUNICIPALITIES (9% PROPENSITY TO BORROW) DFIS/TREASURY REGULATORY REFORM 5 YEARS RAW LAND TO HOME (REDUCE COST OF HOME 16% IF HALVE TIME) CONSUMER CHOICE (PRE-OCCUPATION WITH OWNERSHIP SHIFT TOWARDS RENTAL, INFORMAL SETTLEMENT TENURE SECURITY, HOUSING MICRO FINANCE INCREMENTAL APPROACH WIDTH OVER DEPTH ) PUT CONSUMER BACK INTO DRIVING SEAT (HUMAN SETTLEMENT APPROACH BRAZILIAN TYPE MODEL?) 38

39 CAN BANKS DO MORE? (CONTINUED) 39 CONSTRAINTS AFFORDABILITY Need to holistically address affordability gap Home-ownership subsidy programmes including FLISP review R1 billion guarantee fund will only partly address affordability shortfall (need for a bouquet of interventions) Over-indebted consumers with blemished credit track-records Affordable long term fixed interest rate DISPROPORTIONATE INCREASES IN ADMINISTRATIVE COSTS STRIPPING DISPOSABLE INCOMES, SLOWING GDP AND STARTING TO EVEN THREATEN HOME-OWNERSHIP AS AN ACHIEVABLE PRIORITY WORLD ECONOMIC TURMOIL IMPACT ON LENDER AND CONSUMER CERTAINTY AND HENCE INVESTOR CONFIDENCE BASEL III (2017) : MATCH LONG TERM ASSETS WITH QUALITY LONG TERM DEPOSITS TO DISINCENTIVISE MORTGAGEES (COST OF FUNDS, LIQUIDITY) SUPPLY, SUPPLY, SUPPLY

40 40

Housing Microfinance in South Africa: Status, Problems and Prospects. Based on literature review, interviews, workshop inputs & peer inputs

A Mouse That Roared? Housing Microfinance in South Africa: Status, Problems and Prospects FinMark Forum Sandton David Gardner 18 September, 2008 Study Background Finmark Trust & HIVOS-funded Based on literature

A Mouse That Roared? Housing Microfinance in South Africa: Status, Problems and Prospects FinMark Forum Sandton David Gardner 18 September, 2008 Study Background Finmark Trust & HIVOS-funded Based on literature

The IDB and Housing. Reforming Housing Policies in Latin America Learning from Experience

Reforming Housing Policies in Latin America Learning from Experience Michael Jacobs Inter-American Development Bank November 2003 1 A Summary The Lessons of Experience (1950s 1980s) 1st Generation: Public

Reforming Housing Policies in Latin America Learning from Experience Michael Jacobs Inter-American Development Bank November 2003 1 A Summary The Lessons of Experience (1950s 1980s) 1st Generation: Public

PRESENTATION TO PORTFOLIO COMMITTEE ON HUMAN SETTLEMENTS OCTOBER 2017 INTEGRATED ANNUAL REPORT 2017

PRESENTATION TO PORTFOLIO COMMITTEE ON HUMAN SETTLEMENTS OCTOBER 2017 INTEGRATED ANNUAL REPORT 2017 2 0 CONTENTS NHFC Overview Business Model Corporate Governance & Risk Management Business Performance

PRESENTATION TO PORTFOLIO COMMITTEE ON HUMAN SETTLEMENTS OCTOBER 2017 INTEGRATED ANNUAL REPORT 2017 2 0 CONTENTS NHFC Overview Business Model Corporate Governance & Risk Management Business Performance

REPORT EMANATING FROM THE STRATEGIC FLISP WORKSHOP HELD ON 15 AUGUST 2013 AT FOUNTAINS HOTEL, ST GEORGES MALL, CAPE TOWN

Kahmiela August Director-Affordable Housing Email: Kahmiela.August@westerncape.gov.za Tel: +27 021 483 8412 Fax: +27 021 483 6617 Reference: 13/1/1 Strategic FLISP Workshop REPORT EMANATING FROM THE STRATEGIC

Kahmiela August Director-Affordable Housing Email: Kahmiela.August@westerncape.gov.za Tel: +27 021 483 8412 Fax: +27 021 483 6617 Reference: 13/1/1 Strategic FLISP Workshop REPORT EMANATING FROM THE STRATEGIC

FINANCIAL SECTOR CODE

FINANCIAL SECTOR CODE Agenda Introductions Gazetting and implementation Who does it apply to? Transitional Period What is different FSC Overview Introduction The Financial Sector Charter (the Charter)

FINANCIAL SECTOR CODE Agenda Introductions Gazetting and implementation Who does it apply to? Transitional Period What is different FSC Overview Introduction The Financial Sector Charter (the Charter)

SOUTH AFRICAN BANKING SECTOR OVERVIEW

1 SOUTH AFRICAN BANKING SECTOR OVERVIEW TABLE OF CONTENTS Sections Page 1 Background 1 2. Total Assets 1 3. Total liabilities 3 4. Credit extension 4 5. Branches and ATMs 5 6. Usage of payment systems

1 SOUTH AFRICAN BANKING SECTOR OVERVIEW TABLE OF CONTENTS Sections Page 1 Background 1 2. Total Assets 1 3. Total liabilities 3 4. Credit extension 4 5. Branches and ATMs 5 6. Usage of payment systems

Lessons Learnt & Policy recommendations

Lessons Learnt & Policy recommendations FINAL DISSEMINATION EVENT, Brussels, Feb. 21 st, 2017 Athanassios (Nassos) Petsopoulos Bulgaria: Lessons learnt - BCC & EAP (1) Most sports hall owners haven t heard

Lessons Learnt & Policy recommendations FINAL DISSEMINATION EVENT, Brussels, Feb. 21 st, 2017 Athanassios (Nassos) Petsopoulos Bulgaria: Lessons learnt - BCC & EAP (1) Most sports hall owners haven t heard

BROAD-BASED BLACK ECONOMIC EMPOWERMENT TRANSACTION 18 December 2018

KHULA SIZWE BROAD-BASED BLACK ECONOMIC EMPOWERMENT TRANSACTION 18 December 2018 The Circular published on 18 December 2018 is the main source of detailed information on the proposed B-BBEE transaction,

KHULA SIZWE BROAD-BASED BLACK ECONOMIC EMPOWERMENT TRANSACTION 18 December 2018 The Circular published on 18 December 2018 is the main source of detailed information on the proposed B-BBEE transaction,

NLA membership helps landlords achieve business success by providing a wide range of information, advice and services.

NLA 2016 Autumn Statement Submission October 2016 About the NLA The National Landlords Association (NLA) is the UK s leading organisation for private-residential landlords. We work with 70,000 landlords

NLA 2016 Autumn Statement Submission October 2016 About the NLA The National Landlords Association (NLA) is the UK s leading organisation for private-residential landlords. We work with 70,000 landlords

South Africa s Financial Sector Charter: Where From, Where To?

South Africa s Financial Sector Charter: Where From, Where To? By Mary R. Tomlinson Visiting Research Fellow, University of the Witwatersrand Graduate School of Public and Development Management INTRODUCTION

South Africa s Financial Sector Charter: Where From, Where To? By Mary R. Tomlinson Visiting Research Fellow, University of the Witwatersrand Graduate School of Public and Development Management INTRODUCTION

Scoping study: Overview of the housing 6inance sector in Zambia

Scoping study: Overview of the housing 6inance sector in Zambia Study commissioned by FINMARK TRUST May 2013, Lusaka Section I - Introduction Section II Context Section III Housing Finance Value Chain

Scoping study: Overview of the housing 6inance sector in Zambia Study commissioned by FINMARK TRUST May 2013, Lusaka Section I - Introduction Section II Context Section III Housing Finance Value Chain

A Ten-Year Capital Financing Plan for Toronto Community Housing

STAFF REPORT ACTION REQUIRED A Ten-Year Capital Financing Plan for Toronto Community Housing Date: October 16, 2013 To: From: Wards: Executive Committee City Manager All Reference Number: SUMMARY At its

STAFF REPORT ACTION REQUIRED A Ten-Year Capital Financing Plan for Toronto Community Housing Date: October 16, 2013 To: From: Wards: Executive Committee City Manager All Reference Number: SUMMARY At its

THE FSC JOURNEY SUMMARY OF THE NEW FSC CODES. 31 January 2017 Sandton, Jhb. Copyright Alternative Prosperity Advisory and Products (Pty) Ltd, 2015

Ltd, 2015") THE FSC JOURNEY SUMMARY OF THE NEW FSC CODES 31 January 2017 Sandton, Jhb Copyright Alternative Prosperity Advisory and Products (Pty) Ltd, 2015 Status of the Revised FSC Codes The amended codes has gone

THE FSC JOURNEY SUMMARY OF THE NEW FSC CODES 31 January 2017 Sandton, Jhb Copyright Alternative Prosperity Advisory and Products (Pty) Ltd, 2015 Status of the Revised FSC Codes The amended codes has gone

Redesigning Financial Services: Inclusive Credit Scoring. Nick Henry Professor/Co-Director, Centre for Business in Society Coventry University

Redesigning Financial Services: Inclusive Credit Scoring Nick Henry Professor/Co-Director, Centre for Business in Society Coventry University CfRC 2018, London, 25 April The Presentation Henry, N. and

Redesigning Financial Services: Inclusive Credit Scoring Nick Henry Professor/Co-Director, Centre for Business in Society Coventry University CfRC 2018, London, 25 April The Presentation Henry, N. and

STANDING TITLE OF COMMITTEE ON HEARINGS PRESENTATION TRANSFORMATION

STANDING TITLE OF COMMITTEE ON FINANCE PRESENTATION HEARINGS PRESENTATION TRANSFORMATION SUBTITLE 13 14 OCTOBER MARCH 2017 2015 1 WHO IS ASISA? An industry association representing the majority of South

STANDING TITLE OF COMMITTEE ON FINANCE PRESENTATION HEARINGS PRESENTATION TRANSFORMATION SUBTITLE 13 14 OCTOBER MARCH 2017 2015 1 WHO IS ASISA? An industry association representing the majority of South

MID-TERM REVIEW OF MONETARY POLICY STATEMENT 2006

MID-TERM REVIEW OF MONETARY POLICY STATEMENT 1. Introduction 1.1 There are three objectives to undertake a mid-term review of the Monetary Policy Statement (MPS). First, it is intended to review progress

MID-TERM REVIEW OF MONETARY POLICY STATEMENT 1. Introduction 1.1 There are three objectives to undertake a mid-term review of the Monetary Policy Statement (MPS). First, it is intended to review progress

BUILDING CAPACITY FOR SUSTAINABLE DELIVERY PRESENTATION BY: MS ANNAH MOKGADINYANE CHIEF PLANNER: NATIONAL DEPARTMENT OF HUMAN SETTLEMENTS

REVISITING THE INCREMENTAL HOUSING PROCESS AS A POLICY IMPLEMENTATION TOOL FOR ACCELERATING HOUSING SERVICE DELIVERY: A STUDY OF SELECTED RURAL AREAS IN SOUTH AFRICA PRESENTATION BY: MS ANNAH MOKGADINYANE

REVISITING THE INCREMENTAL HOUSING PROCESS AS A POLICY IMPLEMENTATION TOOL FOR ACCELERATING HOUSING SERVICE DELIVERY: A STUDY OF SELECTED RURAL AREAS IN SOUTH AFRICA PRESENTATION BY: MS ANNAH MOKGADINYANE

I look forward to an informative panel discussion and hear your views around this topic. Thank you

Remarks by Daniel Mminele, Deputy Governor, South African Reserve Bank, at the Institute of International Finance (IIF) High Level Public-Private Sector Conference, The G20 Agenda under the Australian

Remarks by Daniel Mminele, Deputy Governor, South African Reserve Bank, at the Institute of International Finance (IIF) High Level Public-Private Sector Conference, The G20 Agenda under the Australian

GUIDANCE NOTE GN100 on CODE SERIES FS100, STATEMENT 100 RULES GOVERNING THE PROVISION OF BLACK BUSINESS GROWTH FUNDING: OWNERSHIP

GUIDANCE NOTE GN100 on CODE SERIES FS100, STATEMENT 100 RULES GOVERNING THE PROVISION OF BLACK BUSINESS GROWTH FUNDING: OWNERSHIP The provision of risk capital to support black business was negotiated

GUIDANCE NOTE GN100 on CODE SERIES FS100, STATEMENT 100 RULES GOVERNING THE PROVISION OF BLACK BUSINESS GROWTH FUNDING: OWNERSHIP The provision of risk capital to support black business was negotiated

Bank of Ireland Presentation October As at 1 Oct 2014

Bank of Ireland Presentation October 2014 As at 1 Oct 2014 1 Forward-Looking statement This document contains certain forward-looking statements within the meaning of Section 21E of the US Securities Exchange

Bank of Ireland Presentation October 2014 As at 1 Oct 2014 1 Forward-Looking statement This document contains certain forward-looking statements within the meaning of Section 21E of the US Securities Exchange

POWER SECTOR REFORM AND SUBSIDIES. Budak Dilli ESMAP KNOWLEDGE EXCHANGE FORUM GENEVA October 2018

POWER SECTOR REFORM AND SUBSIDIES Budak Dilli ESMAP KNOWLEDGE EXCHANGE FORUM GENEVA October 2018 OVERVIEW OF TURKISH POWER SECTOR Population :80 Million, Geographic Area :780,500 km 2 Rapid demand growth:

POWER SECTOR REFORM AND SUBSIDIES Budak Dilli ESMAP KNOWLEDGE EXCHANGE FORUM GENEVA October 2018 OVERVIEW OF TURKISH POWER SECTOR Population :80 Million, Geographic Area :780,500 km 2 Rapid demand growth:

Poverty and Income Inequality in Scotland: 2013/14 A National Statistics publication for Scotland

Poverty and Income Inequality in Scotland: 2013/14 A National Statistics publication for Scotland EQUALITY, POVERTY AND SOCIAL SECURITY This publication presents annual estimates of the percentage and

Poverty and Income Inequality in Scotland: 2013/14 A National Statistics publication for Scotland EQUALITY, POVERTY AND SOCIAL SECURITY This publication presents annual estimates of the percentage and

PORTFOLIO COMMITTEE ON TRADE AND INDUSTRY. Mr. Sithembele Mase. CHIEF EXECUTIVE OFFICER: samaf. CONTACT : (Marketing Manager)

") PORTFOLIO COMMITTEE ON TRADE AND INDUSTRY Mr. Sithembele Mase CHIEF EXECUTIVE OFFICER: samaf CONTACT : 012 394 1805 (Marketing Manager) 012 394 1722 (PA Line) 012 394 1116 (Direct Line) 1 CONTENT 1. Rationale

PORTFOLIO COMMITTEE ON TRADE AND INDUSTRY Mr. Sithembele Mase CHIEF EXECUTIVE OFFICER: samaf CONTACT : 012 394 1805 (Marketing Manager) 012 394 1722 (PA Line) 012 394 1116 (Direct Line) 1 CONTENT 1. Rationale

Financial Inclusion: A Pathway to Financial Stability? Understanding the Linkages

1 st Annual GPFI Conference on Standard- Setting Bodies and Financial Inclusion October 29, 2012 Basel, Switzerland Financial Inclusion: A Pathway to Financial Stability? Understanding the Linkages Hosted

1 st Annual GPFI Conference on Standard- Setting Bodies and Financial Inclusion October 29, 2012 Basel, Switzerland Financial Inclusion: A Pathway to Financial Stability? Understanding the Linkages Hosted

Composition of the intergovernmental system Alignment between functional and fiscal assignments

. Disaster Management Amendment Bill: National Treasury inputs National Assembly: Portfolio Committee on Cooperative Governance and Traditional Affairs (CoGTA) x 20 May 2015 Outline Composition of the

. Disaster Management Amendment Bill: National Treasury inputs National Assembly: Portfolio Committee on Cooperative Governance and Traditional Affairs (CoGTA) x 20 May 2015 Outline Composition of the

Plenary Session 3: Financial Inclusion A Pathway to Financial Stability? Understanding the Linkages. Issues Paper. Introduction

GPFI 1 st Annual Conference on Standard- Setting Bodies and Financial Inclusion: Promoting Financial Inclusion through Proportionate Standards and Guidance Basel, October 29, 2012 Plenary Session 3: Financial

GPFI 1 st Annual Conference on Standard- Setting Bodies and Financial Inclusion: Promoting Financial Inclusion through Proportionate Standards and Guidance Basel, October 29, 2012 Plenary Session 3: Financial

An EMPOWERDEX Guide. The Codes of Good Practice. Codes Definitions

An EMPOWERDEX Guide The Codes of Good Practice Codes Definitions ABET: Means Adult Basic Education and Training as determined by the National Qualifications Authority Accreditation Body: Means the South

An EMPOWERDEX Guide The Codes of Good Practice Codes Definitions ABET: Means Adult Basic Education and Training as determined by the National Qualifications Authority Accreditation Body: Means the South

A Perspective of ASEAN Financial Sector under the Global Financial Crisis: Assisting SMEs Through Financial Sector Intervention in Asia

International Conference on A Perspective of Asian Financial Sector under the Global Financial Crisis January 21, 2010 A Perspective of ASEAN Financial Sector under the Global Financial Crisis: Assisting

International Conference on A Perspective of Asian Financial Sector under the Global Financial Crisis January 21, 2010 A Perspective of ASEAN Financial Sector under the Global Financial Crisis: Assisting

Challenges for Revenue Growth and Profitability in a Declining Interest Rate and Low Inflation Environment

Challenges for Revenue Growth and Profitability in a Declining Interest Rate and Low Inflation Environment October 2003 Agenda General results Business Environment Issues Addressed Strategic Focus Cost

Challenges for Revenue Growth and Profitability in a Declining Interest Rate and Low Inflation Environment October 2003 Agenda General results Business Environment Issues Addressed Strategic Focus Cost

SA Consumer Credit Index Q3 2018

SA Consumer Credit Index Q3 2018 Executive Summary Credit index remains above 50 in Q3 51 Q3 2018 52 Q2 2018 54 Q3 2017 Index: 50.0 = breakeven The TransUnion SA Consumer Credit Index (CCI) declined marginally

SA Consumer Credit Index Q3 2018 Executive Summary Credit index remains above 50 in Q3 51 Q3 2018 52 Q2 2018 54 Q3 2017 Index: 50.0 = breakeven The TransUnion SA Consumer Credit Index (CCI) declined marginally

Sasol Limited BEE Transaction Media Briefing

Sasol Limited BEE Transaction Media Briefing 25 March 2008 forward-looking statements We may in this document make statements that are not historical facts and relate to analyses and other information

Sasol Limited BEE Transaction Media Briefing 25 March 2008 forward-looking statements We may in this document make statements that are not historical facts and relate to analyses and other information

BROAD BASED BLACK ECONOMIC EMPOWERMENT ACT SECTION 9 (1) CODES OF GOOD PRACTICE AS AMENDED SCHEDULE 2

CODES OF GOOD PRACTICE AS AMENDED SCHEDULE 2") STAATSKOERANT, 1 DESEMBER 2017 No. 41287 323 BROAD BASED BLACK ECONOMIC EMPOWERMENT ACT SECTION 9 (1) CODES OF GOOD PRACTICE AS AMENDED SCHEDULE 2 INTERPRETATION AND DEFINITIONS Part 1: Interpretation

STAATSKOERANT, 1 DESEMBER 2017 No. 41287 323 BROAD BASED BLACK ECONOMIC EMPOWERMENT ACT SECTION 9 (1) CODES OF GOOD PRACTICE AS AMENDED SCHEDULE 2 INTERPRETATION AND DEFINITIONS Part 1: Interpretation

Public Private Partnerships. The South African Experience

Public Private Partnerships The South African Experience Geneva UNECE 18 November 2003 1 Uven Bunsee PPP Unit, South African National Treasury 1 2 General Demographics Population: 44 m Credit rating S&P:

Public Private Partnerships The South African Experience Geneva UNECE 18 November 2003 1 Uven Bunsee PPP Unit, South African National Treasury 1 2 General Demographics Population: 44 m Credit rating S&P:

Annual Report Presentation to the Human Settlements Portfolio Committee. Mr. Samson Moraba CEO 02 September 2011

Annual Report Presentation to the Human Settlements Portfolio Committee Mr. Samson Moraba CEO 02 September 2011 Mandate, Vision, Mission Strategic Objectives NHFC Values NHFC Outcomes NHFC Past Performance

Annual Report Presentation to the Human Settlements Portfolio Committee Mr. Samson Moraba CEO 02 September 2011 Mandate, Vision, Mission Strategic Objectives NHFC Values NHFC Outcomes NHFC Past Performance

Table of Contents. For further information contact: Investor Relations Warwick Bryan Phone: Facsimile: com.

Basel II Pillar 3 Capital Adequacy and Risk Disclosures as at 31 December 2008 Table of Contents 1. Introduction... 3 2. Scope of application... 4 3. Capital and Risk Summary... 5 3.1 Capital... 6 3.2

Basel II Pillar 3 Capital Adequacy and Risk Disclosures as at 31 December 2008 Table of Contents 1. Introduction... 3 2. Scope of application... 4 3. Capital and Risk Summary... 5 3.1 Capital... 6 3.2

Monitoring the Performance of the South African Labour Market

Monitoring the Performance of the South African Labour Market An overview of the South African labour market from 1 of 2009 to of 2010 August 2010 Contents Recent labour market trends... 2 A brief labour

Monitoring the Performance of the South African Labour Market An overview of the South African labour market from 1 of 2009 to of 2010 August 2010 Contents Recent labour market trends... 2 A brief labour

BUILDING SUSTAINABLE FUNDING PARTNERSHIPS towards an all inclusive housing funding model for South Africa

BUILDING SUSTAINABLE FUNDING PARTNERSHIPS towards an all inclusive housing funding model for South Africa Presented by Kutoane Kutoane CEO Gauteng Partnership Fund Date: 17 th September 2012 BACKGROUND

BUILDING SUSTAINABLE FUNDING PARTNERSHIPS towards an all inclusive housing funding model for South Africa Presented by Kutoane Kutoane CEO Gauteng Partnership Fund Date: 17 th September 2012 BACKGROUND

ACCESSING HOUSING FINANCE IN THE COUNTRY SOUTH AFRICA DIRECTOR : OFFICE OF DISCLOSURE DEPARTMENT OF HUMAN SETTLEMENTS

ELIMINATING DISCRIMINATION IN ACCESSING HOUSING FINANCE IN THE COUNTRY SOUTH AFRICA PRESENTER : MR. G. PHOKU DIRECTOR : OFFICE OF DISCLOSURE DEPARTMENT OF HUMAN SETTLEMENTS 1 TABLE OF CONTENTS 1. BACKGROUND

ELIMINATING DISCRIMINATION IN ACCESSING HOUSING FINANCE IN THE COUNTRY SOUTH AFRICA PRESENTER : MR. G. PHOKU DIRECTOR : OFFICE OF DISCLOSURE DEPARTMENT OF HUMAN SETTLEMENTS 1 TABLE OF CONTENTS 1. BACKGROUND

Shelter response to DWP consultation on Discretionary Housing Payments good practice manual

Consultation response Shelter response to DWP consultation on Discretionary Housing Payments good practice manual August 2012 /policylibrary 2012 Shelter. All rights reserved. This document is only for

Consultation response Shelter response to DWP consultation on Discretionary Housing Payments good practice manual August 2012 /policylibrary 2012 Shelter. All rights reserved. This document is only for

Incremental housing: An analysis of the market, and opportunities for housing micro lenders

1 Incremental housing: An analysis of the market, and opportunities for housing micro lenders Presentation to the RHLF 11 th Annual Workshop How Can Incremental Finance Accelerate Housing Delivery? 6 September

1 Incremental housing: An analysis of the market, and opportunities for housing micro lenders Presentation to the RHLF 11 th Annual Workshop How Can Incremental Finance Accelerate Housing Delivery? 6 September

BANK OF BOTSWANA MONETARY POLICY STATEMENT Mid-Year Review

BANK OF BOTSWANA MONETARY POLICY STATEMENT 00 Mid-Year Review 1. INTRODUCTION 1.1 The Monetary Policy Statement (MPS) released in February 00 specified several objectives that the Bank of Botswana intended

BANK OF BOTSWANA MONETARY POLICY STATEMENT 00 Mid-Year Review 1. INTRODUCTION 1.1 The Monetary Policy Statement (MPS) released in February 00 specified several objectives that the Bank of Botswana intended

Infrastructure Investment in Asia

Economy Insight: A Synopsis of ADB Paper Infrastructure Investment in Asia Infrastructure Investment in Asia FICCI Research May 27, 2016 Good infrastructure plays a crucial role towards the growth of an

Economy Insight: A Synopsis of ADB Paper Infrastructure Investment in Asia Infrastructure Investment in Asia FICCI Research May 27, 2016 Good infrastructure plays a crucial role towards the growth of an

Policies and Procedures for the Initial Allocation of Fund Resources

Policies and Procedures for the Initial Allocation of Fund Resources GCF/B.06/05 7 February 2014 Meeting of the Board 19 21 February 2014 Bali, Indonesia Agenda item 9 Page b Recommended action by the

Policies and Procedures for the Initial Allocation of Fund Resources GCF/B.06/05 7 February 2014 Meeting of the Board 19 21 February 2014 Bali, Indonesia Agenda item 9 Page b Recommended action by the

Budget Hearing. May 3, 2011

2011-2012 Budget Hearing May 3, 2011 The purpose of tonight s meeting is to present budgeting options that are being considered to balance the 2011-2012 budget and to solicit input from the community regarding

2011-2012 Budget Hearing May 3, 2011 The purpose of tonight s meeting is to present budgeting options that are being considered to balance the 2011-2012 budget and to solicit input from the community regarding

Credit Crunch: Causes, Effects & Implications. Ian Clarke, 29 th May 2008

: Causes, Effects & Implications Ian Clarke, 29 th May 2008 : Causes, Effects and Implications A review of the causal process Impact of the Longer term implications? 2 The : Causal Process Background Sustained

: Causes, Effects & Implications Ian Clarke, 29 th May 2008 : Causes, Effects and Implications A review of the causal process Impact of the Longer term implications? 2 The : Causal Process Background Sustained

MYPD3 Application Gauteng January 2013

MYPD3 Application 2014-2018 Gauteng January 2013 Disclaimer This presentation does not constitute or form part of and should not be construed as, an offer to sell, or the solicitation or invitation of

MYPD3 Application 2014-2018 Gauteng January 2013 Disclaimer This presentation does not constitute or form part of and should not be construed as, an offer to sell, or the solicitation or invitation of

Portfolio Committee on Energy

Portfolio Committee on Energy Briefing Integrated National Electrification Programme (INEP) 26 August 2014 Context & Purpose Previous briefings to PC on INEP DoE in September 2013 Salga and DoE in February

Portfolio Committee on Energy Briefing Integrated National Electrification Programme (INEP) 26 August 2014 Context & Purpose Previous briefings to PC on INEP DoE in September 2013 Salga and DoE in February

Monetary Policy Report 3/12. Charts

Monetary Policy Report / Charts Chart. Key rates and estimated forward rates as at June and October.¹) Percent. January December ²) US Euro area³) UK 9 ) Broken lines show estimated forward rates as at

Monetary Policy Report / Charts Chart. Key rates and estimated forward rates as at June and October.¹) Percent. January December ²) US Euro area³) UK 9 ) Broken lines show estimated forward rates as at

Employment & Poverty

Employment & Poverty Presentation to Jobs & Poverty Campaign Workshop Johannesburg June 18, 2007 Dr. Miriam Altman Executive Director Employment, Growth & Development Initiative maltman@hsrc.ac.za This

Employment & Poverty Presentation to Jobs & Poverty Campaign Workshop Johannesburg June 18, 2007 Dr. Miriam Altman Executive Director Employment, Growth & Development Initiative maltman@hsrc.ac.za This

FIRST OECD FORUM ON PUBLIC DEBT MANAGEMENT 7 TO 8 DECEMBER 2006, AMSTERDAM

FIRST OECD FORUM ON PUBLIC DEBT MANAGEMENT 7 TO 8 DECEMBER 2006, AMSTERDAM PRESENTATION BY JOHAN KRYNAUW ASSET AND LIABILITY MANAGEMENT DIVISION NATIONAL TREASURY: SOUTH AFRICA (Johan.Krynauw@treasury.gov.za)

FIRST OECD FORUM ON PUBLIC DEBT MANAGEMENT 7 TO 8 DECEMBER 2006, AMSTERDAM PRESENTATION BY JOHAN KRYNAUW ASSET AND LIABILITY MANAGEMENT DIVISION NATIONAL TREASURY: SOUTH AFRICA (Johan.Krynauw@treasury.gov.za)

T H E NA I RO B I C A L L TO A C T I O N F O R C L O S I N G T H E I M P L E M E N TA T I O N G A P I N H E A LT H P RO M O T I O N

T H E NA I RO B I C A L L TO A C T I O N F O R C L O S I N G T H E I M P L E M E N TA T I O N G A P I N H E A LT H P RO M O T I O N 1. INTRODUCTION PURPOSE The Nairobi Call to Action identifies key strategies

T H E NA I RO B I C A L L TO A C T I O N F O R C L O S I N G T H E I M P L E M E N TA T I O N G A P I N H E A LT H P RO M O T I O N 1. INTRODUCTION PURPOSE The Nairobi Call to Action identifies key strategies

Carnegie Nordic Large Cap Seminar Stockholm 4 March 2008 Mikael Inglander, CFO

Carnegie Nordic Large Cap Seminar Stockholm 4 March 28 Mikael Inglander, CFO The leading bank in four small countries Sweden Total population: 9.2m Employees: 8,75 Private customers: 4.1m Corp. customers:

Carnegie Nordic Large Cap Seminar Stockholm 4 March 28 Mikael Inglander, CFO The leading bank in four small countries Sweden Total population: 9.2m Employees: 8,75 Private customers: 4.1m Corp. customers:

FINANCIAL INCLUSION million vouchers in 2017 INNOVATION TO IMPROVE ACCESS AND AFFORDABILITY FIVE

FIVE FINANCIAL INCLUSION Many Africans remain excluded from formal financial systems. They are limited to transacting in cash, rely on family and friends for credit, and have no personal or business insurance.

FIVE FINANCIAL INCLUSION Many Africans remain excluded from formal financial systems. They are limited to transacting in cash, rely on family and friends for credit, and have no personal or business insurance.

Indicator Watch for the South African Commercial Property Market Cycle

Indicator Watch for the South African Commercial Property Market Cycle April 2017 Cycle Position Summary Recent political events and the downgrading of South Africa s international credit rating have led

Indicator Watch for the South African Commercial Property Market Cycle April 2017 Cycle Position Summary Recent political events and the downgrading of South Africa s international credit rating have led

DCLG consultation Increasing the borrowing capacity of stock transfer housing associations

DCLG consultation Increasing the borrowing capacity of stock transfer housing associations CIH response May 2015 Emailed to: lsvt.valuation@communities.gsi.gov.uk 1 Introduction 1. The Chartered Institute

DCLG consultation Increasing the borrowing capacity of stock transfer housing associations CIH response May 2015 Emailed to: lsvt.valuation@communities.gsi.gov.uk 1 Introduction 1. The Chartered Institute

The Money Statistics. December.

The Money Statistics December 2018 Welcome to the December 2018 edition of The Money Statistics, The Money Charity s monthly roundup of statistics about how we use money in the UK. If you have any questions,

The Money Statistics December 2018 Welcome to the December 2018 edition of The Money Statistics, The Money Charity s monthly roundup of statistics about how we use money in the UK. If you have any questions,

Strategic planning interventions in the post recession period A London case study Duncan Bowie University of Westminster

Strategic planning interventions in the post recession period A London case study Duncan Bowie University of Westminster RSA Winter Conference 23 November 2012 Subject of Research To analyse: Impact of

Strategic planning interventions in the post recession period A London case study Duncan Bowie University of Westminster RSA Winter Conference 23 November 2012 Subject of Research To analyse: Impact of

Testimony Submission for the Record. House Ways and Means Committee

Testimony Submission for the Record House Ways and Means Committee Hearing on: Economic Challenges Facing Middle Class Families Jan. 31, 2007, 2 p.m. 1100 Longworth HOB Submitted by: Dallas Salisbury,CEO

Testimony Submission for the Record House Ways and Means Committee Hearing on: Economic Challenges Facing Middle Class Families Jan. 31, 2007, 2 p.m. 1100 Longworth HOB Submitted by: Dallas Salisbury,CEO

MYPD3 Application January 2013

MYPD3 Application 2014-2018 January 2013 Disclaimer This presentation does not constitute or form part of and should not be construed as, an offer to sell, or the solicitation or invitation of any offer

MYPD3 Application 2014-2018 January 2013 Disclaimer This presentation does not constitute or form part of and should not be construed as, an offer to sell, or the solicitation or invitation of any offer

Economic Policy in the Crisis. Lars Calmfors Jönköping International Business School, 2 November 2009

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

Strategic Risk Management and Balance Sheet Management under the new regulatory environment

Strategic Risk Management and Balance Sheet Management under the new regulatory environment Vishal Kapoor Regional Practice Lead (APAC) Balance Sheet Management, Moody s Analytics 1 Introduction to Moody

Strategic Risk Management and Balance Sheet Management under the new regulatory environment Vishal Kapoor Regional Practice Lead (APAC) Balance Sheet Management, Moody s Analytics 1 Introduction to Moody

CAN A SOUTH AFRICAN EXPORT CREDIT AGENCY NAVIGATE DOMESTIC AND GLOBAL HEADWINDS?

CAN A SOUTH AFRICAN EXPORT CREDIT AGENCY NAVIGATE DOMESTIC AND GLOBAL HEADWINDS? 6 JUNE 2018 CYRIL PRINSLOO AND PALESA SHIPALANA OVERVIEW 1. Context Working Paper - Can a South African Export Credit Agency

CAN A SOUTH AFRICAN EXPORT CREDIT AGENCY NAVIGATE DOMESTIC AND GLOBAL HEADWINDS? 6 JUNE 2018 CYRIL PRINSLOO AND PALESA SHIPALANA OVERVIEW 1. Context Working Paper - Can a South African Export Credit Agency

Liberty Holdings Ltd. Thabo Dloti Group Chief Executive 16 October 2014

Liberty Holdings Ltd Thabo Dloti Group Chief Executive 16 October 2014 Liberty Holdings Limited - today A leading financial services holding company in sub-sahara Africa that provides wealth creation and

Liberty Holdings Ltd Thabo Dloti Group Chief Executive 16 October 2014 Liberty Holdings Limited - today A leading financial services holding company in sub-sahara Africa that provides wealth creation and

ACCESS MORE ALTERNATIVE INVESTING - THE NEW DIVERSIFICATION. A part of the FirstRand Group

ACCESS MORE ALTERNATIVE INVESTING - THE NEW DIVERSIFICATION A part of the FirstRand Group A B Today s global investment climate of prolonged uncertainty calls for a shift beyond the traditional understanding

ACCESS MORE ALTERNATIVE INVESTING - THE NEW DIVERSIFICATION A part of the FirstRand Group A B Today s global investment climate of prolonged uncertainty calls for a shift beyond the traditional understanding

Central Bank Macro-Prudential Policy Proposals Submission December 2014

Central Bank Macro-Prudential Policy Proposals Submission December 2014 Policy@scsi.ie SCSI RED C Poll and Member Surveys SCSI commissioned a RED C Poll of prospective purchasers to inform our recommendations

Central Bank Macro-Prudential Policy Proposals Submission December 2014 Policy@scsi.ie SCSI RED C Poll and Member Surveys SCSI commissioned a RED C Poll of prospective purchasers to inform our recommendations

TRANSLATING REGULATORY CHANGE TO BALANCE SHEET ACTION

TRANSLATING REGULATORY CHANGE TO BALANCE SHEET ACTION ACTUARIES INSTITUTE CONFERENCE PLENARY 1 August 2016 Shaun Dooley, Group Treasurer CONTENTS Dimensions of regulatory change Net Stable Funding Ratio

TRANSLATING REGULATORY CHANGE TO BALANCE SHEET ACTION ACTUARIES INSTITUTE CONFERENCE PLENARY 1 August 2016 Shaun Dooley, Group Treasurer CONTENTS Dimensions of regulatory change Net Stable Funding Ratio

SABOA 2013 NATIONAL CONFERENCE 28 FEBRUARY 2013 CSIR CONFERENCE CENTRE

SABOA 2013 NATIONAL CONFERENCE 28 FEBRUARY 2013 CSIR CONFERENCE CENTRE Don Mashele Head of Regions Overview and Background Challenges that led to the establishment of sefa Limited success in fostering

SABOA 2013 NATIONAL CONFERENCE 28 FEBRUARY 2013 CSIR CONFERENCE CENTRE Don Mashele Head of Regions Overview and Background Challenges that led to the establishment of sefa Limited success in fostering

Strategic Corporate Plan

Strategic Corporate Plan 2012-2017 Dr. Jeffrey Mahachi Acting chief Executive Officer Jeffreym@nhbrc.org.za Click to edit Master subtitle style 13 March 2012 Vision A world class home builders warranty

Strategic Corporate Plan 2012-2017 Dr. Jeffrey Mahachi Acting chief Executive Officer Jeffreym@nhbrc.org.za Click to edit Master subtitle style 13 March 2012 Vision A world class home builders warranty

Housing Development Agency. Business Case Activating the Development Agency Role. Board Approved 11 March 2016

Housing Development Agency Business Case Activating the Development Agency Role Board Approved Final Version 5.0 Table of Contents Executive Summary 4 1 Introduction 9 2 Background 10 2.1 Establishment

Housing Development Agency Business Case Activating the Development Agency Role Board Approved Final Version 5.0 Table of Contents Executive Summary 4 1 Introduction 9 2 Background 10 2.1 Establishment

Economic Projections :1

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

THE HOUSING CRISIS CAN BE SOLVED

THE HOUSING CRISIS CAN BE SOLVED Sinn Féin Alternative Budget 2019 SINN FÉIN ALTERNATIVE BUDGET 2019 THE HOUSING CRISIS CAN BE SOLVED 1 Contents Public Housing... 2 Private Rental... 4 Homelessness...

THE HOUSING CRISIS CAN BE SOLVED Sinn Féin Alternative Budget 2019 SINN FÉIN ALTERNATIVE BUDGET 2019 THE HOUSING CRISIS CAN BE SOLVED 1 Contents Public Housing... 2 Private Rental... 4 Homelessness...

Quarterly Financial Report

Quarterly Financial Report SECOND QUARTER June 30, 207 (Unaudited) Management s Discussion and Analysis Table of Contents MANAGEMENT S DISCUSSION AND ANALYSIS... 3 THE OPERATING ENVIRONMENT AND OUTLOOK

Quarterly Financial Report SECOND QUARTER June 30, 207 (Unaudited) Management s Discussion and Analysis Table of Contents MANAGEMENT S DISCUSSION AND ANALYSIS... 3 THE OPERATING ENVIRONMENT AND OUTLOOK

RURAL HOUSING LOAN FUND

RURAL HOUSING LOAN FUND Presentation at the : ANNUAL WORKSHOP 23 MARCH 2017 JABULANI FAKAZI, CEO 1 Outline 2 RHLF mandate Howe we create value for people in our mandate Business model RHLF Pricing Policy

RURAL HOUSING LOAN FUND Presentation at the : ANNUAL WORKSHOP 23 MARCH 2017 JABULANI FAKAZI, CEO 1 Outline 2 RHLF mandate Howe we create value for people in our mandate Business model RHLF Pricing Policy

High-cost credit review: Feedback from roundtables

Financial Conduct Authority High-cost credit review: Feedback from roundtables Introduction 1. This paper summarises the issues and ideas raised by participants in our roundtables. These points do not

Financial Conduct Authority High-cost credit review: Feedback from roundtables Introduction 1. This paper summarises the issues and ideas raised by participants in our roundtables. These points do not

General Election What does it mean for housing in Wales? Specialist Briefing

General Election 2015 What does it mean for housing in Wales? Specialist Briefing Introduction The 2015 UK General Election results gave the Conservative party a majority of 12 seats in the UK parliament.

General Election 2015 What does it mean for housing in Wales? Specialist Briefing Introduction The 2015 UK General Election results gave the Conservative party a majority of 12 seats in the UK parliament.

Tariffs and Tariff Design Promoting Access to the Poor

Regulation for Practitioners Building Capacity through Participation Tariffs and Tariff Design Promoting Access to the Poor Gloria Magombo Energy Advisor gmagombo@satradehub.org July 27-31, Eskom Convention

Regulation for Practitioners Building Capacity through Participation Tariffs and Tariff Design Promoting Access to the Poor Gloria Magombo Energy Advisor gmagombo@satradehub.org July 27-31, Eskom Convention

CRD 5: The new Large Exposures Framework February 2017

CRD 5: The new Large Exposures Framework February 2017 1 - Overview of Key Messages 1. Significance and potential impacts The Large Exposures framework is a key component of the prudential rules It is

CRD 5: The new Large Exposures Framework February 2017 1 - Overview of Key Messages 1. Significance and potential impacts The Large Exposures framework is a key component of the prudential rules It is

Chart 1.1 Unemployment rate. Percent of labour force. Seasonally adjusted. January 2008 May 2013

Chart. Unemployment rate. Percent of labour force. Seasonally adjusted. January 8 May Euro area US 8 8 8 9 Source: Thomson Reuters Chart. GDP for trading partners in MPR / ) and MPR /. Four quarter change.

Chart. Unemployment rate. Percent of labour force. Seasonally adjusted. January 8 May Euro area US 8 8 8 9 Source: Thomson Reuters Chart. GDP for trading partners in MPR / ) and MPR /. Four quarter change.

By Mathias Katamba, M.D, Housing Finance Bank Rotary Club of Kampala South, Hotel Africana 5 th September, 2016

By Mathias Katamba, M.D, Housing Finance Bank Rotary Club of Kampala South, Hotel Africana 5 th September, 2016 Quick Facts & Figures Only 28% of Ugandan adults above 15 years have a bank account 17% used

By Mathias Katamba, M.D, Housing Finance Bank Rotary Club of Kampala South, Hotel Africana 5 th September, 2016 Quick Facts & Figures Only 28% of Ugandan adults above 15 years have a bank account 17% used

Private Participation in Infrastructure: Lessons Learned. Mobilizing Private Capital and Management into Infrastructure Development

Private Participation in Infrastructure: Lessons Learned Mobilizing Private Capital and Management into Infrastructure Development Enhancing the Investment Climate: The Case for Infrastructure OECD Global

Private Participation in Infrastructure: Lessons Learned Mobilizing Private Capital and Management into Infrastructure Development Enhancing the Investment Climate: The Case for Infrastructure OECD Global

Presentation to the Egyptian Ministry of Planning, Monitoring, and Administrative Reform (MPMAR) Study Tour: South Africa.

Study Tour: South Africa.") Presentation to the Egyptian Ministry of Planning, Monitoring, and Administrative Reform (MPMAR) Study Tour: South Africa April 13 2016 STRUCTURE OF THE PRESENTATION 1. Background to South Africa s Intergovernmental

Presentation to the Egyptian Ministry of Planning, Monitoring, and Administrative Reform (MPMAR) Study Tour: South Africa April 13 2016 STRUCTURE OF THE PRESENTATION 1. Background to South Africa s Intergovernmental

A new national consensus and a new commitment to deliver were necessary to address the triple challenges of poverty, unemployment and inequality.

Budget 2017 Introduction In delivering Budget 2017 in parliament, the finance minister, Pravin Gordhan, emphasised that South Africa was at a conjuncture which requires the wisdom of our elders to help

Budget 2017 Introduction In delivering Budget 2017 in parliament, the finance minister, Pravin Gordhan, emphasised that South Africa was at a conjuncture which requires the wisdom of our elders to help

Old Mutual SME Employee Benefits Monitor for 2015

Our ability to see the bigger picture fully supports your entrepreneurial thinking, because the more meaningful a business becomes to its employees, the more effort employees make to bring about success.

Our ability to see the bigger picture fully supports your entrepreneurial thinking, because the more meaningful a business becomes to its employees, the more effort employees make to bring about success.

Chief financial officer s report

26 FNB NAMIBIA GROUP ANNUAL REPORT 28 Outgoing CFO Gideon Cornelissen. Newly appointed CFO Erwin Tjipuka. Chief financial officer s report Once-off and exceptional transactions in this financial year mean

26 FNB NAMIBIA GROUP ANNUAL REPORT 28 Outgoing CFO Gideon Cornelissen. Newly appointed CFO Erwin Tjipuka. Chief financial officer s report Once-off and exceptional transactions in this financial year mean

October Copyright 2012 Eighty20. This presentation is incomplete without the accompanying oral commentary

Bubbles October 2012 Copyright 2012 Eighty20 This presentation is incomplete without the accompanying oral commentary 2 What is a bubble? Why do we care? Asset bubble Prices of specific asset classes are

Bubbles October 2012 Copyright 2012 Eighty20 This presentation is incomplete without the accompanying oral commentary 2 What is a bubble? Why do we care? Asset bubble Prices of specific asset classes are

Standard Bank Group (SBG) Financial results presentation For the year ended 31 December 2009

Financial results presentation For the year ended 31 December 2009") Standard Bank Group (SBG) Financial results presentation For the year ended 31 December 2009 Financial highlights FY09 change FY08 Headline earnings (Rm) 11 718 (17) 14 150 Headline EPS (HEPS) (cents)

Standard Bank Group (SBG) Financial results presentation For the year ended 31 December 2009 Financial highlights FY09 change FY08 Headline earnings (Rm) 11 718 (17) 14 150 Headline EPS (HEPS) (cents)

EX26.2. Financial Sustainability of Toronto Community Housing Corporation Prepared for the City of Toronto. Appendix 4. Summary Report.

EX26.2 Appendix 4 Financial Sustainability of Toronto Community Housing Corporation Prepared for the City of Toronto 6 June 2017 Summary Report Prepared for the exclusive use of the City of Toronto under

EX26.2 Appendix 4 Financial Sustainability of Toronto Community Housing Corporation Prepared for the City of Toronto 6 June 2017 Summary Report Prepared for the exclusive use of the City of Toronto under

SETTING THE CONTEXT: SOUTH AFRICA

SETTING THE CONTEXT: SOUTH AFRICA MORE THAN SHELTER: HOUSING AS AN INSTRUMENT OF ECONOMIC AND SOCIAL DEVELOPMENT A Harvard Joint Center for Housing Studies International Housing Conference Supported by

SETTING THE CONTEXT: SOUTH AFRICA MORE THAN SHELTER: HOUSING AS AN INSTRUMENT OF ECONOMIC AND SOCIAL DEVELOPMENT A Harvard Joint Center for Housing Studies International Housing Conference Supported by

Credit Opinion: Sydbank A/S - DRAFT - In Progress or Approved Version. Global Credit Research. Ratings. Contacts. Key Indicators

Credit Opinion: Sydbank A/S - DRAFT - In Progress or Approved Version Global Credit Research Aabenraa, Denmark Ratings Category Outlook Bank Deposits Baseline Credit Assessment Adjusted Baseline Credit

Credit Opinion: Sydbank A/S - DRAFT - In Progress or Approved Version Global Credit Research Aabenraa, Denmark Ratings Category Outlook Bank Deposits Baseline Credit Assessment Adjusted Baseline Credit

E Distribution: GENERAL RESOURCE, FINANCIAL AND BUDGETARY MATTERS. Agenda item 6 FORWARD PURCHASE FACILITY. For approval

Executive Board Annual Session Rome, 4 8 June 2012 RESOURCE, FINANCIAL AND BUDGETARY MATTERS Agenda item 6 For approval FORWARD PURCHASE FACILITY E Distribution: GENERAL WFP/EB.A/2012/6-B/1 4 May 2012

Executive Board Annual Session Rome, 4 8 June 2012 RESOURCE, FINANCIAL AND BUDGETARY MATTERS Agenda item 6 For approval FORWARD PURCHASE FACILITY E Distribution: GENERAL WFP/EB.A/2012/6-B/1 4 May 2012

Interim Report For the six months ended 30 June 2015

Interim Report For the six months ended 30 June 2015 Interim Report for the six months ended 30 June 2015 Forward-Looking statement This document contains certain forward-looking statements within the

Interim Report For the six months ended 30 June 2015 Interim Report for the six months ended 30 June 2015 Forward-Looking statement This document contains certain forward-looking statements within the

FINANCE FOR ALL? POLICIES AND PITFALLS IN EXPANDING ACCESS A WORLD BANK POLICY RESEARCH REPORT

FINANCE FOR ALL? POLICIES AND PITFALLS IN EXPANDING ACCESS A WORLD BANK POLICY RESEARCH REPORT Summary A new World Bank policy research report (PRR) from the Finance and Private Sector Research team reviews

FINANCE FOR ALL? POLICIES AND PITFALLS IN EXPANDING ACCESS A WORLD BANK POLICY RESEARCH REPORT Summary A new World Bank policy research report (PRR) from the Finance and Private Sector Research team reviews

BOP Housing Finance Conference Miami, June Bridging the Gap MFH -- Mortgage Lending:

BOP Housing Finance Conference Miami, June 2011 Bridging the Gap MFH -- Mortgage Lending: The Future of Low Income Housing Finance? Some international experiences The World Bank FPD /GCMNB Olivier Hassler

BOP Housing Finance Conference Miami, June 2011 Bridging the Gap MFH -- Mortgage Lending: The Future of Low Income Housing Finance? Some international experiences The World Bank FPD /GCMNB Olivier Hassler

Codes of Good Practice on Broad-Based Black Economic Empowerment: Amended Financial Sector Code 2017

Codes of Good Practice on Broad-Based Black Economic Empowerment: Amended Financial Sector Code 2017 Published under GN 1325 in GG 41287 of 1 December 2017 I, Dr Rob Davies, Minister of Trade and Industry,

Codes of Good Practice on Broad-Based Black Economic Empowerment: Amended Financial Sector Code 2017 Published under GN 1325 in GG 41287 of 1 December 2017 I, Dr Rob Davies, Minister of Trade and Industry,

3rd Annual Affordable Housing Africa

3rd Annual Affordable Housing Africa Bridging the Gap: Housing Finance & Policy Developing Primary and Secondary Mortgage Markets to Provide Accessible and Affordable Housing in Nigeria Charles Inyangete,

3rd Annual Affordable Housing Africa Bridging the Gap: Housing Finance & Policy Developing Primary and Secondary Mortgage Markets to Provide Accessible and Affordable Housing in Nigeria Charles Inyangete,

RETAIL DISTRIBUTION REVIEW (RDR): STATUS UPDATE ON PROPOSAL TT - SPECIAL REMUNERATION DISPENSATION FOR THE LOW- INCOME MARKET.

: STATUS UPDATE ON PROPOSAL TT - SPECIAL REMUNERATION DISPENSATION FOR THE LOW- INCOME MARKET.") RETAIL DISTRIBUTION REVIEW (RDR): STATUS UPDATE ON PROPOSAL TT - SPECIAL REMUNERATION DISPENSATION FOR THE LOW- INCOME MARKET December 2018 1 BACKGROUND The former Financial Services Board ( FSB ) s Retail

RETAIL DISTRIBUTION REVIEW (RDR): STATUS UPDATE ON PROPOSAL TT - SPECIAL REMUNERATION DISPENSATION FOR THE LOW- INCOME MARKET December 2018 1 BACKGROUND The former Financial Services Board ( FSB ) s Retail

Mainstreaming Incremental Housing The Case of Zambian Home Loans

Mainstreaming Incremental Housing The Case of Zambian Home Loans putting it in perspective Informal Settlement growth Circ. 65% of working Adults own land Informal Construction workers Most civil servants

Mainstreaming Incremental Housing The Case of Zambian Home Loans putting it in perspective Informal Settlement growth Circ. 65% of working Adults own land Informal Construction workers Most civil servants

AGSA Strategic plan and budget SCoAG engagement 17 November 2017

AGSA Strategic plan and budget 2018-2021 SCoAG engagement 17 November 2017 Reputation promise The Auditor-General of South Africa has a constitutional mandate and, as the Supreme Audit Institution (SAI)

AGSA Strategic plan and budget 2018-2021 SCoAG engagement 17 November 2017 Reputation promise The Auditor-General of South Africa has a constitutional mandate and, as the Supreme Audit Institution (SAI)

Selected Statistics about the Saskatchewan Construction Industry

Selected Statistics about the Saskatchewan Construction Industry Presented to the: Saskatchewan Construction Association June 2015 Presented by: Mark Cooper, President & CEO Doug Elliott Saskatchewan Construction

Selected Statistics about the Saskatchewan Construction Industry Presented to the: Saskatchewan Construction Association June 2015 Presented by: Mark Cooper, President & CEO Doug Elliott Saskatchewan Construction

ADDRESS BY MINISTER OF MINERAL RESOURCES, MOSEBENZI ZWANE (MP) AT THE BLACK BUSINESS COUNCIL (BBC) BUSINESS BREAKFAST, 18 TH AUGUST 2017

AT THE BLACK BUSINESS COUNCIL (BBC) BUSINESS BREAKFAST, 18 TH AUGUST 2017") ADDRESS BY MINISTER OF MINERAL RESOURCES, MOSEBENZI ZWANE (MP) AT THE BLACK BUSINESS COUNCIL (BBC) BUSINESS BREAKFAST, 18 TH AUGUST 2017 President of the Black Business Council, Dr Danisa Baloyi All the

ADDRESS BY MINISTER OF MINERAL RESOURCES, MOSEBENZI ZWANE (MP) AT THE BLACK BUSINESS COUNCIL (BBC) BUSINESS BREAKFAST, 18 TH AUGUST 2017 President of the Black Business Council, Dr Danisa Baloyi All the