THE NEXT 10 YEARS: CREDIT UNIONS 2025

|

|

|

- Ross Carpenter

- 5 years ago

- Views:

Transcription

1 THE NEXT 10 YEARS:

2 INTRODUCTION The ecosystem matters, and the global financial ecosystem is incredibly large and incredibly complex

3 DISRUPTORS Technological disruption, increased regulation, changing consumer behaviors, and asset-growth will be topics of constant discussion for credit union leaders.

4 INTRODUCTION In the next 10 years, areas that will see the most dramatic changes include: Consolidation/Mergers Payments Technology Lending Regulation

5 CREDIT UNION FORECAST 2025

6 DISRUPTORS: WHAT DO THEY LOOK LIKE? CONSOLIDATION PAYMENTS REGULATION TECHNOLOGY LENDING?????

7 FINANCIAL SYSTEM IN : 315 Source:

8 FINANCIAL SYSTEM IN 2025 Since 1998 CUs -158% Assets +242% Prediction: Credit unions will continue to decline by credit unions per year Source: NCUA 5300,

9 FINANCIAL SYSTEM IN 2025 Competing on: Corporate social responsibility Sustainable businesses Environmental impact 55% of global online consumers across 60 countries willing to pay more for products and services provided by companies committed to positive social and environmental impact Source:

Large global businesses are unappealing in developed markets (35%) compared to emerging markets (51%)")

10 FINANCIAL SYSTEM IN 2025 Millennials overwhelmingly believe. Businesses are focused on their own agendas rather than helping to improve society (75%) Large global businesses are unappealing in developed markets (35%) compared to emerging markets (51%) Source: cuments/about-deloitte/gx-wef-2015-millennial-surveyexecutivesummary.pdf

11 FINANCIAL SYSTEM IN 2025 Source: GABV Report March 2012

12 FINANCIAL SYSTEM IN 2025 The most attractive segments: Consumer lending (Prosper, LendingClub) -- Peer to peer loan issuances on the two biggest networks jumped from US$26 million in 2009 to more than US$1.7 billion in 2014 Small business lending (Kabbage, OnDeck) -- Alternative lenders have higher commercial loan approval rates (62%) than small banks (50%), credit unions (43%), and big banks (21%)

13 FINANCIAL SYSTEM IN 2025

14 + NIMBLE STARTUPS THAT MATCH MEMBERS DIGITAL SHIFTS

15

16 FINANCIAL TECHNOLOGY IN Rerouting Networks Mobile phones with instant Internet access don't require a traditional payment network to move money.

17 FINANCIAL TECHNOLOGY IN Those with low household incomes less likely to have home-internet access = smartphone dependency? 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% 1st Quintile 2nd Quintile 3rd Quintile 4th Quintile 5th Quintile Home Computer Internet Use from Home Source: Pew Research Center, 2014

30 25 20 15 10 5 0 First quintile Second quintile Third quintile Fourth quintile Fifth quintile Source: Pew Research")

18 FINANCIAL TECHNOLOGY IN Likely: Income key predictor of smartphone dependency 35 Percentage of Households by Quintile with ONLY a Cellphone (no landline) First quintile Second quintile Third quintile Fourth quintile Fifth quintile Source: Pew Research Center, 2014

19 FINANCIAL TECHNOLOGY IN Goodbye ATMs As mobile rises, ATMs will phase out over the next 10 years, mainly by attrition -- A la carte Pricing Services like remittances, wires, and foreign exchange will start to come with Blockchain technologies that push the wholesale prices close to zero

20 FINANCIAL TECHNOLOGY IN Mobile identity The smartphone won't just be about transactions. Location features and the camera will allow FIs to run credible Know Your Customer screens entirely remotely

21 FINANCIAL TECHNOLOGY IN 2025 Source: 2013 Federal Reserve Payments Study

22 FINANCIAL TECHNOLOGY IN 2025

23 PAYDAY LENDING IN 2025 Every year, up to 2.5 million Canadians use payday loans $2.5 bln in loans = $1000 per person Source: Technology, Media & Telecommunications Predictions, Deloitte.

24 CREDIT UNION ECOSYSTEM IN 2025 Movement? System? Industry?

25 CREDIT UNION ECOSYSTEM IN Consolidation System will consolidate ownership of wealth management, payments, and other system-owned entities. Ownership of system entities may depart from co-operative form.

26 CREDIT UNION ECOSYSTEM IN 2025 Survey of CEOs: Credit Unions in 2025 Were Source: Filene Survey, 2015

27 CREDIT UNION ECOSYSTEM IN 2025 Survey of CEOs: Credit Unions In 2025 Had Source: Filene Survey, 2015

28 CONSUMER BEHAVIOR IN 2025 With their purchasing and borrowing decisions, consumers will lead financial decisions over the next 10 years. Dramatic changes in their spending, their payment behaviors, and their desires to own or simply access expensive assets like homes and cars, will make it harder for credit unions to rely on traditional products for profitability

29 CONSUMER BEHAVIOR IN Sustainability Renewable energy and resource conservation will explode in importance with the changing generations, aiding credit unions that support such initiatives at the product (not just the institutional) level Look for more loans that reward sustainable purchases and underwriting that considers environmental and social benefits

30 CONSUMER BEHAVIOR IN Mobile First (Wearables Too) Situationally aware banking apps will help members make financial/spending decisions

31 CONSUMER BEHAVIOR IN Car Ownership Shifts Millennials are less likely to own 2-3 cars. They won t go straight to Uber, but auto growth will decline

32 CONSUMER BEHAVIOR IN 2025 (3) Owned Autonomy High tech, individually operated Tesla, Mobileye (4) Shared Autonomy Autonomous, PODS Google, Apple, Uber 2.0 Asset Owned Asset Shared (1) Today 100 yr. old model Original equipment manufacturers, Suppliers, Rentals (2) Shared Economy Low tech, shared assets Uber, Lyft, Sidecar Source: Morgan Stanley, 2015

33 CONSUMER BEHAVIOR IN Rise of the Family Account As more families take responsibility for aging relatives and concerns about elder abuse proliferate, look for more robust family accounts. On/Off switches for viewing privileges and control privileges Source: Pew Research Center, 2014

34 CONSUMER BEHAVIOR IN 2025 Source: Pew Research Center, 2014

35 Multi-generational households on the rise here too, especially with indigenous peoples

36 Source: new-homes.lennar.com

37 Source: U_S Annuity_Sales_Improve_Three_Percent_in_201 4.aspx

38 Source: U_S Annuity_Sales_Improve_Three_Percent_in_201 4.aspx

39 CONSUMER BEHAVIOR IN emortgages QuickenLoans and aggregators like LendingTree have proven that a face-to-face transaction is no longer a given. In the United States in 2012: 50% of lenders took more than 25% of their mortgage applications online 61% of applications submitted through third-party underwriting systems were approved online

40 CONSUMER BEHAVIOR IN Algorithmic Banking Saving, spending, and revolving debt will be subjected to informational algorithms for optimized decisionmaking. Startups like Earnest, and Affirm are already exploring alternative underwriting schemes that rely on a mosaic of data beyond a traditional credit score

41 REGULATION IN Rising Leadership Standards As credit unions grow and take on different kinds of risk, regulators expect credit unions to recruit directors with the appropriate skill sets to ensure the institution's soundness. These expectations challenge the credit union s co-operative structure.

")

42 REGULATION IN Regulatory Burden Driven by an increasing political and economically unstable global environment, policymakers impose an increase amount of regulatory requirements around tracking the flow of money (e.g., Common Reporting Standard, AML/ATF, Privacy Legislation)

43 REGULATION IN Social Reporting As consumer protection and addressing pressing social and environmental needs continue to grab the attention of policy makers, by 2025, credit unions will be required to submit at least a few key indicators of social and environmental impact statements along with financial reporting.

44 REGULATION IN Taxation Against a broad-based policy push to simplify the federal income tax act, credit unions successfully advocate for a new tax credit that recognizes their cooperative form.

45 LENDING IN Brokers Bust? FinTech will squeeze mortgage brokers out of the equation. Front-end origination will move away from financial institutions to consumer technology innovators

46 LENDING IN Big Auto Shakeup The global auto market is a $2 trillion industry that everyone from Tesla, to Google, to Apple, to all the existing incumbents is dying to dominate. Watch as shared economy bites away first at urban dwellers and then spreads everywhere. And not too much later: autonomous cars that offer access but not ownership.

47 LENDING IN Easier Mortgages Underwriting, appraisals, insurance and many other aspects of the mortgage will be automated. Goldman Sachs: In three years, large non-banks share of mortgage originations has doubled to 42%. In mortgage servicing, non-banks share has more than tripled to 27%.

48 LENDING IN Insatiable P2P P2P lenders are a real risk to credit unions. Prosper and Lending Club are moving to add business lending to their growing consumer portfolios, and they will continue to eat their way up the value chain. -- Business Lending Potentially $178B of small business loans in the banking system is at risk of being disintermediated, with $1.6bn of banking industry profits attached to those loans Source: Goldman Sachs, 2015

49 CREDIT UNIONS IN 2025 Filene asked CEOs from around North America for their predictions for Here are their most compelling guesses

50 Imagine you are a time traveler returning from 2025, what kinds of services or technologies have credit unions abandoned?

51 If you were to start on just one thing right now to prepare credit unions for 2025, what would that one thing be?

52 Imagine you are a time traveler returning from 2025, what kinds of technologies did you see that helped credit unions remain competitive?

53 Imagine you are a time traveler returning from 2025, how were members in the future accessing their accounts and performing transactions?

54 Imagine you are a time traveler returning from 2025, what was the one, most extraordinary thing you noticed about financial institutions? Credit Unions no longer exist. Fees, fees, fees with no family relationships. No physical branches, all in cyberspace. The small financial institutions have disappeared. After major disruption from electronic theft, identity breaches, and government spying, consumers face significant losses of money and trust.

55 10-YEAR FORECASTS We propose four possible economic scenarios and detail what each would mean for Canadian credit unions

56 10-YEAR FORECAST BASELINE The continuation of recent patterns of moderate growth. It assumes no major economic or financial disturbances in coming years.

57 FINANCIAL CRISIS The next ten years will include another financial crisis that will result in credit unions experiencing large declines in ROA.

58 CREDIT BOOM Deficit spending generates economics growth which consumers leverage into more debt-fueled spending, driving a growth pattern similar to what we observed in period, when deficit spending was last in vogue. We also assume that the Bank of Canada will eventually allow interest rates to rise, which will temporarily depress credit union ROA, but the economy will avoid economic and credit crises

59 INFLATION + RECESSION Inflation climbs somewhat quickly (to 5% by 2018); the Bank of Canada targets an overnight rate of 6.5% but then a recession takes place (-1% of GDP). The increases in unemployment will be smaller than in most recessions and loan losses correspondingly small. Following small declines and subsequent increases in interest rates, the economy stabilizes.

60 10-YEAR FORECASTS Credit Union Assets Historical Data and Projections $Billions, inflation-adjusted, Logarithmac Scale Baseline Financial Crisis Credit Boom Inflation + Recession 2014 Assets: $171B $425 Bln $296 Bln $246 Bln $219 Bln

61 10-YEAR FORECASTS 10.0% 8.0% 6.0% Credit Union Capital (Net Worth) Equity/Assets, Baseline Financial Crisis Credit Boom Inflation + Recession 4.0% 2.0%

62 10-YEAR FORECASTS

63 QUESTIONS?

64 CONVENTION WORKSHOPS

65 PRE-CONVENTION SURVEY Survey says.

66 RISE OF ONLINE LENDING: moderate to high urgency; need to move, or know more. 10% of respondents active in this area. Almost a third investigating About a third said low to no threat. Over half said moderate to high, or becoming high soon. Some concerns about members financial well-being. A couple of comments: it s an opportunity to build membership! Most thought players should be regulated like other FIs. Only about half think they will be. Sense of urgency to move on this, or learn more soon.

must take precedence.")

67 UNBUNDLING the DIGITAL WALLET: waiting for the leaders Most critical features: Ease of use, Security, ability to handle both debit and credit. About 70% said they were interested but nothing is planned yet. Many comments indicated that other critical priorities (compliance) must take precedence. Many said waiting for LCUC lead.

68 COMMUNICATING in a DIGITAL NATION: a priority for some, soon for others. Two thirds of respondents say the CU is using Facebook. Just under half said Twitter. LinkedIn: less than 30%, everything else limited. Over 80% of respondents said: prioritizing more highly in coming years. What resources are in place? About 40% were unsure. Of the rest, half said a part time person; 20% said a dedicated person. 40% said they had a budget.

69 RIGHTSIZING BIG DATA: Member data most critical. Need to act together. Member data highest importance, then Financial, then Risk & Sales data. Managing our data moderately well -- member data not so much. Opportunities: Learning together. Getting big picture. Needs: infrastructure/ process/ skills. Some said consistent core banking system. Some said: compliance costs taking precedence. Pain Points: Skills, tools, process. Strategy asking the right questions in the first place. Gathering the data in the first place, and data validity.

70 BRANCH OF THE FUTURE: Advice and Wealth Management. Top Challenges: Personal Devices, Member Engagement, Digital strategy (in branch) Facelift for legacy branch not a priority. Future predictions: Mobile and Online channels most important. ITMs/Branches distant third. Purposes of branches: Advisory, Wealth Mgmt. Loans and Member retention distant third. Predictions: somewhat larger percentage of Flagship and Full Service branches.

71 MILLENNIALS: Happiness. Values. Flexibility. Feedback. Difficult for some to respond to employee demographics questions. Top employment priorities cited: Flexibility and Professional Development. Compensation a late third. Many could not answer. Differences? Loyalty (not much) Adaptability, energy (lots) Impatience with inefficiency Perhaps a bit threatening Care & feeding feedback, support.

72 ALL SET?

The Socialisation of Finance April 2015 Introduction crowd funding, peer to peer lending, socialized payments and automated investing

The Socialisation of Finance April 2015. Introduction An insightful report published in March 2015 by the leading investment bank, Goldman Sachs provides some interesting perspectives on how finance is

The Socialisation of Finance April 2015. Introduction An insightful report published in March 2015 by the leading investment bank, Goldman Sachs provides some interesting perspectives on how finance is

5/5/2018 CREDIT UNIONS IN Who We Are. Our research (THINK) + our innovation (DO) + our action (CHANGE) = the secret formula.

+ our innovation (DO) + our action (CHANGE) = the secret formula.") CREDIT UNIONS IN 2025 Hawaii Credit Union League Convention May 19, 2018 HELLO! Cortney Angeley Impact Director cortneya@filene.org 2 ABOUT FILENE Who We Are Filene Research Institute conducts research,

CREDIT UNIONS IN 2025 Hawaii Credit Union League Convention May 19, 2018 HELLO! Cortney Angeley Impact Director cortneya@filene.org 2 ABOUT FILENE Who We Are Filene Research Institute conducts research,

Small Business Lending Landscape

Small Business Lending Landscape Opportunity Finance Network June 8, 2016 Agenda Small Business Financing Initiative Overview Today s Topic and Presenters Small Business Lending Landscape How can mission-driven

Small Business Lending Landscape Opportunity Finance Network June 8, 2016 Agenda Small Business Financing Initiative Overview Today s Topic and Presenters Small Business Lending Landscape How can mission-driven

Future of Digitalization & Preparing for a New Reality. Najib Choucair Executive Director Banking Department May 2017

Future of Digitalization & Preparing for a New Reality Najib Choucair Executive Director Banking Department May 2017 In 1993, and after the civil war, the Lebanese economy was practically ruined. BDL s

Future of Digitalization & Preparing for a New Reality Najib Choucair Executive Director Banking Department May 2017 In 1993, and after the civil war, the Lebanese economy was practically ruined. BDL s

Digital insurance: How to compete in the new digital economy

Digital insurance: How to compete in the new digital economy The traditional insurance company is set up to best serve a type of customer that, in the very near future, may no longer exist. Demographic

Digital insurance: How to compete in the new digital economy The traditional insurance company is set up to best serve a type of customer that, in the very near future, may no longer exist. Demographic

Overview of the U.S. Payments Industry

0 Overview of the U.S. Payments Industry Southern Financial Exchange Conference May 3, 2017 Today s Discussion Trends in payments volume and value Five forces impacting payments 1 US PAYMENTS INDUSTRY:

0 Overview of the U.S. Payments Industry Southern Financial Exchange Conference May 3, 2017 Today s Discussion Trends in payments volume and value Five forces impacting payments 1 US PAYMENTS INDUSTRY:

Customer Centricity Conference

Customer Centricity Conference New needs, new data Duncan Anderson September 2016 2016 Willis Towers Watson. All rights reserved. New needs and new data 2 New needs New needs and new data New data So?

Customer Centricity Conference New needs, new data Duncan Anderson September 2016 2016 Willis Towers Watson. All rights reserved. New needs and new data 2 New needs New needs and new data New data So?

Insurtech the revolution in insurance. 11 th October 2017

Insurtech the revolution in insurance 11 th October 2017 Presentation Agenda 1 Introduction into Insurtech 2 Current Landscape 3 Impact on Middle Eastern Market 4 Benefit of Insurtech the auto example

Insurtech the revolution in insurance 11 th October 2017 Presentation Agenda 1 Introduction into Insurtech 2 Current Landscape 3 Impact on Middle Eastern Market 4 Benefit of Insurtech the auto example

The Peer-to-Peer Landscape

The Peer-to-Peer Landscape Presented by: SimplyCredit Inc Karthik Sethuraman, CEO Alan Bahr SVP, Business Development September 15, 2016 Agenda Peer-to-Peer (P2P) Lending Defined Performance of Key P2P

The Peer-to-Peer Landscape Presented by: SimplyCredit Inc Karthik Sethuraman, CEO Alan Bahr SVP, Business Development September 15, 2016 Agenda Peer-to-Peer (P2P) Lending Defined Performance of Key P2P

Lending Strategies 2.0. Carolinas Credit Union League 2015 Leadership Conference October 22, 2015

Lending Strategies 2.0 Carolinas Credit Union League 2015 Leadership Conference October 22, 2015 WHAT DOES THE FUTURE HOLD? CUES - Scenarios for Credit Unions through 2020 Two Uncertainties/Four Scenarios

Lending Strategies 2.0 Carolinas Credit Union League 2015 Leadership Conference October 22, 2015 WHAT DOES THE FUTURE HOLD? CUES - Scenarios for Credit Unions through 2020 Two Uncertainties/Four Scenarios

DUST OFF YOUR DEPOSIT ACQUISITION STRATEGY PRESENTED BY:

DUST OFF YOUR DEPOSIT ACQUISITION STRATEGY PRESENTED BY: Rob Johnson Executive Vice President/Principal c. myers corporation KEY TAKEAWAYS Questions that should be addressed to help ensure a strong deposit

DUST OFF YOUR DEPOSIT ACQUISITION STRATEGY PRESENTED BY: Rob Johnson Executive Vice President/Principal c. myers corporation KEY TAKEAWAYS Questions that should be addressed to help ensure a strong deposit

SVB Analytics Asia Tour 2015 SSVB Frontier Technology Forum Fintech Forum

SVB Analytics Asia Tour 2015 SSVB Frontier Technology Forum Fintech Forum Steve Allan, SVB Analytics Dec 18, 2015 1 SOURCES Utilities of a Bank Functions Intermediary Risk Mgmt. Enforcement Custody Transit

SVB Analytics Asia Tour 2015 SSVB Frontier Technology Forum Fintech Forum Steve Allan, SVB Analytics Dec 18, 2015 1 SOURCES Utilities of a Bank Functions Intermediary Risk Mgmt. Enforcement Custody Transit

Globalization is real and is just as real for

Closing Panel: Improving Rural Capital Markets Gary Warren Globalization is real and is just as real for the banking industry, if not more so, than most industries. Information technology advancements

Closing Panel: Improving Rural Capital Markets Gary Warren Globalization is real and is just as real for the banking industry, if not more so, than most industries. Information technology advancements

Whatever happened to crowdfunding?

FCA Future Scenarios ++++++++++++++++++++++++++++ All views expressed in this article are those of the author and do not necessarily represent the views of the Dubai Financial Services Authority or of

FCA Future Scenarios ++++++++++++++++++++++++++++ All views expressed in this article are those of the author and do not necessarily represent the views of the Dubai Financial Services Authority or of

Account aggregation and the lending experience

Account aggregation and the lending experience Introducing: Steve Smith Finicity Laura DeSoto Experian Today s digital age 3 Experian The culture of immediacy Customers expect instant mobile service and

Account aggregation and the lending experience Introducing: Steve Smith Finicity Laura DeSoto Experian Today s digital age 3 Experian The culture of immediacy Customers expect instant mobile service and

2 INTEREST RATE OVERNIGHT AVERAGES

TABLE OF CONTENTS April 2016 2 INTEREST RATE OVERNIGHT AVERAGES 2 GENERAL INDUSTRY Banks Look to Enter the Lucrative Business of Check-Cashing 2 TECHNOLOGY & INNOVATION Banks Fintech Fight With Apps Heats

TABLE OF CONTENTS April 2016 2 INTEREST RATE OVERNIGHT AVERAGES 2 GENERAL INDUSTRY Banks Look to Enter the Lucrative Business of Check-Cashing 2 TECHNOLOGY & INNOVATION Banks Fintech Fight With Apps Heats

HOW TO BUY A CAR WITH BAD CREDIT

Your credit score is not the only way to prove your credit worthiness. It does do a good job of indicating what type of credit customer you might be; however, today the credit system is being used to exploit

Your credit score is not the only way to prove your credit worthiness. It does do a good job of indicating what type of credit customer you might be; however, today the credit system is being used to exploit

Now+NEXT 2018 FIS PACE FINDINGS WHAT S. for Small-to-midsize Business Banking in the United States. fisglobal.com/pace

2018 FIS PACE FINDINGS Performance Against Customer Expectations (PACE) WHAT S Now+NEXT for Small-to-midsize Business Banking in the United States fisglobal.com/pace Small-to-midsize Business Banking in

2018 FIS PACE FINDINGS Performance Against Customer Expectations (PACE) WHAT S Now+NEXT for Small-to-midsize Business Banking in the United States fisglobal.com/pace Small-to-midsize Business Banking in

A digital financial brand for the next generation of Canadians

A digital financial brand for the next generation of Canadians Mogo Finance Technology Inc. NOVEMBER 2015 Forward-Looking Statements Forward-Looking Information: This document contains forward looking

A digital financial brand for the next generation of Canadians Mogo Finance Technology Inc. NOVEMBER 2015 Forward-Looking Statements Forward-Looking Information: This document contains forward looking

Industry Perspective. Four factors creating a perfect storm in the insurance industry

Industry Perspective Four factors creating a perfect storm in the insurance industry The storm is brewing By Phil Ratcliff Industry General Manager, Insurance, DXC Technology As they retire, they are taking

Industry Perspective Four factors creating a perfect storm in the insurance industry The storm is brewing By Phil Ratcliff Industry General Manager, Insurance, DXC Technology As they retire, they are taking

Robinson Digital Marketing & Data Analytics. United States 2018 Economic Forecast Report

Robinson Digital Marketing & Data Analytics United States 2018 Economic Forecast Report December 12, 2017 Edition Robinson Digital Marketing & Data Analytics Amos B Robinson, Principal, Digital Marketing

Robinson Digital Marketing & Data Analytics United States 2018 Economic Forecast Report December 12, 2017 Edition Robinson Digital Marketing & Data Analytics Amos B Robinson, Principal, Digital Marketing

Startups And The Un-Banking Of America

Startups And The Un-Banking Of America Posted yesterday by Rebecca Lynn (@VCRebecca) Editor s note: Rebecca Lynn is a general partner at Canvas Venture Fund, an earlystage venture capital firm. She has

Startups And The Un-Banking Of America Posted yesterday by Rebecca Lynn (@VCRebecca) Editor s note: Rebecca Lynn is a general partner at Canvas Venture Fund, an earlystage venture capital firm. She has

AIB Finance & Leasing: Leasing Life Conference, Paris

AIB Finance & Leasing: Leasing Life Conference, Paris 24 th November 2016 Presented by: Kieran Marshall Managing Director AIB Finance & Leasing Agenda 1. Ireland's Market Ireland in Numbers Impact of FDI

AIB Finance & Leasing: Leasing Life Conference, Paris 24 th November 2016 Presented by: Kieran Marshall Managing Director AIB Finance & Leasing Agenda 1. Ireland's Market Ireland in Numbers Impact of FDI

Factoring Market Research& Asia Market Overview

Factoring Market Research& Asia Market Overview May 2018 Factoring is a range of services rendered to suppliers of goods trading on credit terms and based on financing them against assignment of the underlying

Factoring Market Research& Asia Market Overview May 2018 Factoring is a range of services rendered to suppliers of goods trading on credit terms and based on financing them against assignment of the underlying

Financial Inclusion and Fintech

Financial Inclusion and Fintech The views expressed in this presentation are those of the author and do not necessarily represent the views of the NBC. 2 Agenda Financial Inclusion Landscape Regulatory

Financial Inclusion and Fintech The views expressed in this presentation are those of the author and do not necessarily represent the views of the NBC. 2 Agenda Financial Inclusion Landscape Regulatory

PIERRE CARDENAS NCCO,MBA INNOVATORS OF CHANGE PRESIDENT/CEO

PIERRE CARDENAS NCCO,MBA INNOVATORS OF CHANGE PRESIDENT/CEO Let s Take a look at what is TAKING PLACE TODAY! Key Fact: In 2012, the number of credit union branches declined for the first time

PIERRE CARDENAS NCCO,MBA INNOVATORS OF CHANGE PRESIDENT/CEO Let s Take a look at what is TAKING PLACE TODAY! Key Fact: In 2012, the number of credit union branches declined for the first time

Insurance Technology and Longevity Risk. Jennifer Li-Ling Wang Vice President of National Chenghgchi University Chairman of Fintech Research Center

Insurance Technology and Longevity Risk Jennifer Li-Ling Wang Vice President of National Chenghgchi University Chairman of Fintech Research Center The Impact of InsurTech WEF FinTech report in 2015 state

Insurance Technology and Longevity Risk Jennifer Li-Ling Wang Vice President of National Chenghgchi University Chairman of Fintech Research Center The Impact of InsurTech WEF FinTech report in 2015 state

Future Trends 2017: The Shift Gains Momentum

Future Trends 2017: The Shift Gains Momentum IASA Spring Meeting April 2017 1 People Market Trend: Pressure on insurance industry driving new expectations, innovations and competition Changing customer

Future Trends 2017: The Shift Gains Momentum IASA Spring Meeting April 2017 1 People Market Trend: Pressure on insurance industry driving new expectations, innovations and competition Changing customer

Extracting tax value from the Internet-of- Things

www.pwc.com/communications Extracting tax value from the Internet-of- Things Why companies must consider tax up front when deciding on investments in IoT capabilities and services Tax: the missing component

www.pwc.com/communications Extracting tax value from the Internet-of- Things Why companies must consider tax up front when deciding on investments in IoT capabilities and services Tax: the missing component

BOFI HOLDING, INC. Investor Presentation September 2017

BOFI HOLDING, INC. Investor Presentation September 2017 NASDAQ: BOFI0 Safe Harbor This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act

BOFI HOLDING, INC. Investor Presentation September 2017 NASDAQ: BOFI0 Safe Harbor This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act

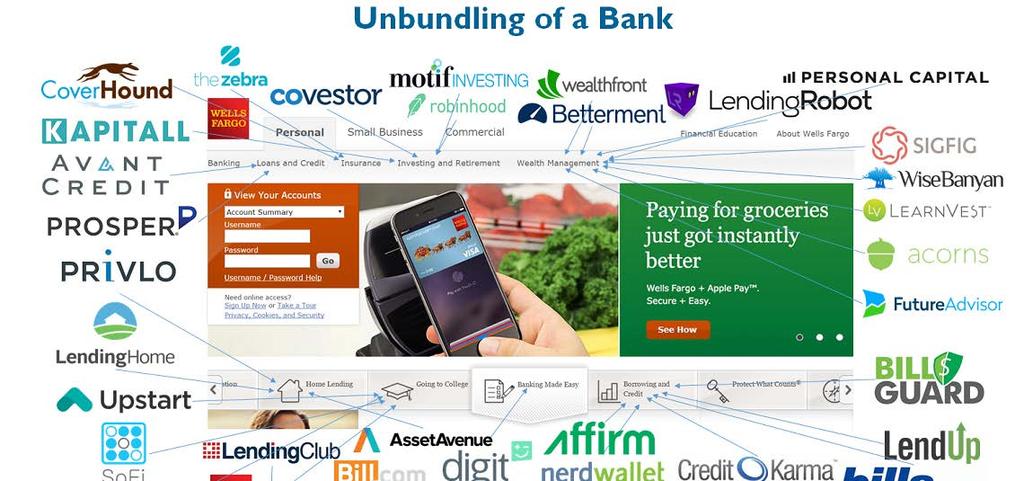

The Decoupling of Banks

The Decoupling of Banks How Non-Bank Entities will Dictate the Future of Consumer Financial Services Dan Ballen Vice President at Pine Brook Partners About Pine Brook Partners. Founded in 2006, Pine Brook

The Decoupling of Banks How Non-Bank Entities will Dictate the Future of Consumer Financial Services Dan Ballen Vice President at Pine Brook Partners About Pine Brook Partners. Founded in 2006, Pine Brook

FROM 12 TO 21: OUR WAY FORWARD

FROM 12 TO 21: OUR WAY FORWARD MESSAGE FROM THE BOARD Weldon Cowan, chair of the board of directors The board of directors shares the corporation s excitement about the next phase of the From 12 to 21

FROM 12 TO 21: OUR WAY FORWARD MESSAGE FROM THE BOARD Weldon Cowan, chair of the board of directors The board of directors shares the corporation s excitement about the next phase of the From 12 to 21

In-Focus FEATURING THE STATE OF DIGITAL MORTGAGE AN EXCERPT FROM MOVING FORWARD IN REVERSE

In-Focus FEATURING THE STATE OF DIGITAL MORTGAGE AN EXCERPT FROM Volume 3, 1, Issue 2 1 2018 2016 Strategic Mortgage Finance Group, LLC. All Rights Reserved. February, July, 2016 2018 By Jim Cameron A

In-Focus FEATURING THE STATE OF DIGITAL MORTGAGE AN EXCERPT FROM Volume 3, 1, Issue 2 1 2018 2016 Strategic Mortgage Finance Group, LLC. All Rights Reserved. February, July, 2016 2018 By Jim Cameron A

WHITE PAPER. Tech Trends in Debt Collection Software that are Personalizing the Debt Collection Process and Helping Enterprises Protect Their Brands

WHITE PAPER Tech Trends in Debt Collection Software that are Personalizing the Debt Collection Process and Helping Enterprises Protect Their Brands DIGITAL TECHNOLOGY AND CHANGE IN DEBT COLLECTION The

WHITE PAPER Tech Trends in Debt Collection Software that are Personalizing the Debt Collection Process and Helping Enterprises Protect Their Brands DIGITAL TECHNOLOGY AND CHANGE IN DEBT COLLECTION The

INSURANCE INNOVATION EXECUTIVE BOARD

INSURANCE INNOVATION EXECUTIVE BOARD STATE OF INSURTECH Tim Hoying October 26, 2017 UPDATE ON INSURTECH INVESTMENT $USD, in millions THE INSURTECH LANDSCAPE IS GROWING WITH CLOSE TO $7.1 BILLION INVESTED

INSURANCE INNOVATION EXECUTIVE BOARD STATE OF INSURTECH Tim Hoying October 26, 2017 UPDATE ON INSURTECH INVESTMENT $USD, in millions THE INSURTECH LANDSCAPE IS GROWING WITH CLOSE TO $7.1 BILLION INVESTED

Millennial Money Mindset Report

Millennial Money Mindset Report 2017 In Partnership with: Data Analysis support by Executive Summary 2017 Millennial Money Mindset Report Previous studies have shown that the expectations of Millennials

Millennial Money Mindset Report 2017 In Partnership with: Data Analysis support by Executive Summary 2017 Millennial Money Mindset Report Previous studies have shown that the expectations of Millennials

Health consumers see the healthcare world around them changing, but INSURERS AND HEALTHCARE PROVIDERS DON T NEED TO COPY AMAZON

HEALTH INNOVATION JOURNAL INSURERS AND HEALTHCARE PROVIDERS DON T NEED TO COPY AMAZON THEY JUST HAVE TO PERSUADE CONSUMERS TO LIKE THEM John Rudoy Principal, Health & Life Sciences, Oliver Wyman Helen

HEALTH INNOVATION JOURNAL INSURERS AND HEALTHCARE PROVIDERS DON T NEED TO COPY AMAZON THEY JUST HAVE TO PERSUADE CONSUMERS TO LIKE THEM John Rudoy Principal, Health & Life Sciences, Oliver Wyman Helen

What economic, industry and demographic forces do we face?

What economic, industry and demographic forces do we face? April 24, 2013 Fabio Biasella VP, Client Advisory Services A Data Driven Approach for Fact Based Decision Making 2 1 How Do Our Customers Work

What economic, industry and demographic forces do we face? April 24, 2013 Fabio Biasella VP, Client Advisory Services A Data Driven Approach for Fact Based Decision Making 2 1 How Do Our Customers Work

2015 Growth Strategy Survey

Strong Board. Strong Bank. 2015 Growth Strategy Survey AUG 2015 RESEARCH Sponsored by: 2 2015 GROWTH STRATEGY SURVEY TABLE OF CONTENTS Executive Summary 3 Growth & Profitability 4 Connecting With Consumers

Strong Board. Strong Bank. 2015 Growth Strategy Survey AUG 2015 RESEARCH Sponsored by: 2 2015 GROWTH STRATEGY SURVEY TABLE OF CONTENTS Executive Summary 3 Growth & Profitability 4 Connecting With Consumers

Consumer Survey 2017 presented by The Telegraph. What consumers really think

Consumer Survey 2017 presented by The Telegraph What consumers really think Introduction The Telegraph are delighted to present our first fintech-focused consumer survey, aimed at placing a spotlight on

Consumer Survey 2017 presented by The Telegraph What consumers really think Introduction The Telegraph are delighted to present our first fintech-focused consumer survey, aimed at placing a spotlight on

PayStand s Guide to Understanding ACH and echeck. How to Receive Direct Bank Payments Online

PayStand s Guide to Understanding ACH and echeck How to Receive Direct Bank Payments Online Table of Contents Do direct bank payments make sense for your business? What s the difference between ACH and

PayStand s Guide to Understanding ACH and echeck How to Receive Direct Bank Payments Online Table of Contents Do direct bank payments make sense for your business? What s the difference between ACH and

LEVERAGING TECHNOLOGY TO IMPROVE PARTICIPATION AND PARTICIPANT OUTCOMES

LEVERAGING TECHNOLOGY TO IMPROVE PARTICIPATION AND PARTICIPANT OUTCOMES JESSICA MALDONADO, AIFA, GFS, C(K)P, PPC Vice President of Searcy Financial Services, Inc. LEARNING OBJECTIVES Factors that impact

LEVERAGING TECHNOLOGY TO IMPROVE PARTICIPATION AND PARTICIPANT OUTCOMES JESSICA MALDONADO, AIFA, GFS, C(K)P, PPC Vice President of Searcy Financial Services, Inc. LEARNING OBJECTIVES Factors that impact

The State of Consumer Finance: Why the Time is Now for Marketplace Lending AL GOLDSTEIN, CEO AVANT

The State of Consumer Finance: Why the Time is Now for Marketplace Lending AL GOLDSTEIN, CEO AVANT The lending industry is overdue for disruption Potential for Disruption Low High Mortgage SMB Loans International

The State of Consumer Finance: Why the Time is Now for Marketplace Lending AL GOLDSTEIN, CEO AVANT The lending industry is overdue for disruption Potential for Disruption Low High Mortgage SMB Loans International

Are you ready to be an Insurer of Things? How the Internet of Things is changing the rules of the game for insurers

Are you ready to be an Insurer of Things? How the Internet of Things is changing the rules of the game for insurers The traditional business model for insurance, though still a solid source of revenue,

Are you ready to be an Insurer of Things? How the Internet of Things is changing the rules of the game for insurers The traditional business model for insurance, though still a solid source of revenue,

Disruption and Insurance. Challenges and Opportunities All Along the Value Chain

Disruption and Insurance Challenges and Opportunities All Along the Value Chain Greatest Threats, Opportunities Whither Silicon Valley? Greatest Opportunity Greatest Threat Advanced Analytics 32% Insurtech

Disruption and Insurance Challenges and Opportunities All Along the Value Chain Greatest Threats, Opportunities Whither Silicon Valley? Greatest Opportunity Greatest Threat Advanced Analytics 32% Insurtech

Finnovation Bye Bye Banks?

Finnovation Bye Bye Banks? Prof Dr. Bjorn Cumps Vlerick Business School HOW FAST IS IT GOING? FAST! 2 REMEMBER? 41% market share 3 HOW FAST IS IT GOING? FAST! 6 million units sold in 15 months 10 million

Finnovation Bye Bye Banks? Prof Dr. Bjorn Cumps Vlerick Business School HOW FAST IS IT GOING? FAST! 2 REMEMBER? 41% market share 3 HOW FAST IS IT GOING? FAST! 6 million units sold in 15 months 10 million

Insurance 2020 & Beyond

Insurance 2020 & Beyond México November, 2015 By. Stephen T. O Hearn Leader of the Global Insurance Practice Transformación del Sector Asegurador, más allá de la Regulación Research assessed 32 distinct

Insurance 2020 & Beyond México November, 2015 By. Stephen T. O Hearn Leader of the Global Insurance Practice Transformación del Sector Asegurador, más allá de la Regulación Research assessed 32 distinct

AUTOMATE MORTGAGE BROKER COMPENSATION

HOW SALES COMMISSION SOFTWARE HELPS AUTOMATE MORTGAGE BROKER COMPENSATION Automate Mortgage Broker Compensation 01 Contents 02 03 06 07 08 Introduction Incentive Software Eliminates Spreadsheet Complexity

HOW SALES COMMISSION SOFTWARE HELPS AUTOMATE MORTGAGE BROKER COMPENSATION Automate Mortgage Broker Compensation 01 Contents 02 03 06 07 08 Introduction Incentive Software Eliminates Spreadsheet Complexity

Trends in Auto Purchasing

Trends in Auto Purchasing Ben Klepzig May 8, 2015 LLAA,LLSP-1149422.1-0315-0417 CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited 2015 CUNA Mutual Group, All Rights Reserved.

Trends in Auto Purchasing Ben Klepzig May 8, 2015 LLAA,LLSP-1149422.1-0315-0417 CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited 2015 CUNA Mutual Group, All Rights Reserved.

September TD Bank Checking Experience Index 2015

September 2015 TD Bank Checking Experience Index 2015 Overview TD Bank s 3 rd Checking Experience Index - better understanding consumers checking account experiences, behaviors and attitudes. Methodology

September 2015 TD Bank Checking Experience Index 2015 Overview TD Bank s 3 rd Checking Experience Index - better understanding consumers checking account experiences, behaviors and attitudes. Methodology

Mortgage Lender Sentiment Survey

Mortgage Lender Sentiment Survey How Will Artificial Intelligence Shape Mortgage Lending? Q3 2018 Topic Analysis Published October 4, 2018 2018 Fannie Mae. Trademarks of Fannie Mae. 1 Table of Contents

Mortgage Lender Sentiment Survey How Will Artificial Intelligence Shape Mortgage Lending? Q3 2018 Topic Analysis Published October 4, 2018 2018 Fannie Mae. Trademarks of Fannie Mae. 1 Table of Contents

2018 National Survey of Community Banks

2018 National Survey of Community Banks Thank you for agreeing to participate in a brief survey being conducted by the Survey Research Institute (SRI) at Cornell University on behalf of the state banking

2018 National Survey of Community Banks Thank you for agreeing to participate in a brief survey being conducted by the Survey Research Institute (SRI) at Cornell University on behalf of the state banking

Blockchain: A true disruptor for the energy industry Use cases and strategic questions

Blockchain: A true disruptor for the energy industry Use cases and strategic questions Phoenix rising The oilfield services sector transforms again In its ongoing journey to power and move the world, the

Blockchain: A true disruptor for the energy industry Use cases and strategic questions Phoenix rising The oilfield services sector transforms again In its ongoing journey to power and move the world, the

DIGITAL FINANCIAL SERVICES CHALLENGES AND OPPORTUNITIES FOR BANKS

DIGITAL FINANCIAL SERVICES CHALLENGES AND OPPORTUNITIES FOR BANKS MARTIN HOLTMANN MANAGER, DIGITAL FINANCE AND MICROFINANCE FINANCIAL INSTITUTIONS GROUP Digital Financial Services (DFS) Financial Services

DIGITAL FINANCIAL SERVICES CHALLENGES AND OPPORTUNITIES FOR BANKS MARTIN HOLTMANN MANAGER, DIGITAL FINANCE AND MICROFINANCE FINANCIAL INSTITUTIONS GROUP Digital Financial Services (DFS) Financial Services

Defining your digital strategy in a disruptive world

REPORT Defining your digital strategy in a disruptive world UK Insurance Underwriting Digitisation Study 2017 MAY 2017 Introduction In January 2017, LexisNexis Risk Solutions released a comprehensive study

REPORT Defining your digital strategy in a disruptive world UK Insurance Underwriting Digitisation Study 2017 MAY 2017 Introduction In January 2017, LexisNexis Risk Solutions released a comprehensive study

Edmonton Real Estate Forum. Ron Gilbertson President and CEO Edmonton Economic Development Corporation

Edmonton Real Estate Forum Ron Gilbertson President and CEO Edmonton Economic Development Corporation The Latest Economic News Depression Economic Downturn The Economy What s Going On? Edmonton and Alberta

Edmonton Real Estate Forum Ron Gilbertson President and CEO Edmonton Economic Development Corporation The Latest Economic News Depression Economic Downturn The Economy What s Going On? Edmonton and Alberta

PROMISE & PERIL. PROMISE & PERIL Managing the Uncertainty of Rapid Innovation and a Changing Economy

PROMISE & PERIL Managing the Uncertainty of Rapid Innovation and a Changing Economy PROMISE & PERIL Managing the Uncertainty of Rapid Innovation and a Changing Economy PROMISE & PERIL Managing the Uncertainty

PROMISE & PERIL Managing the Uncertainty of Rapid Innovation and a Changing Economy PROMISE & PERIL Managing the Uncertainty of Rapid Innovation and a Changing Economy PROMISE & PERIL Managing the Uncertainty

The Digital-First Mortgage MAKING BORROWERS, LOAN OFFICERS, AND PARTNERS FEEL RIGHT AT HOME

The Digital-First Mortgage MAKING BORROWERS, LOAN OFFICERS, AND PARTNERS FEEL RIGHT AT HOME Contents Introduction 1 Mortgage Providers Are Missing Expectations 3 Discover the Digital-First Mortgage 4 Borrower

The Digital-First Mortgage MAKING BORROWERS, LOAN OFFICERS, AND PARTNERS FEEL RIGHT AT HOME Contents Introduction 1 Mortgage Providers Are Missing Expectations 3 Discover the Digital-First Mortgage 4 Borrower

Credit Unions and Millennials: Divided or United?

Credit Unions and Millennials: Divided or United? Summary Credit unions face a unique set of challenges in a world of ever-changing technology, increasing expectations and fast-paced innovation. We live

Credit Unions and Millennials: Divided or United? Summary Credit unions face a unique set of challenges in a world of ever-changing technology, increasing expectations and fast-paced innovation. We live

MORGAN STANLEY FINANCIALS

MORGAN STANLEY FINANCIALS CONFERENCE 19 March 2013 António Horta-Osório Group Chief Executive 2012 HIGHLIGHTS Significantly improved performance and balance sheet further strengthened and de-risked d Balance

MORGAN STANLEY FINANCIALS CONFERENCE 19 March 2013 António Horta-Osório Group Chief Executive 2012 HIGHLIGHTS Significantly improved performance and balance sheet further strengthened and de-risked d Balance

Brazil s Agenda 2018 The companies perspectives and strategies for a decisive year full of transformations. December 2017

Brazil s The companies perspectives and strategies for a decisive year full of transformations December 2017 1 Contents Brazil s 3 Key findings 4 Survey sample 5 7 Results expectations 8 Sectors and regions

Brazil s The companies perspectives and strategies for a decisive year full of transformations December 2017 1 Contents Brazil s 3 Key findings 4 Survey sample 5 7 Results expectations 8 Sectors and regions

DIGITAL MONEY TRENDS REPORT PRESENTED BY

DIGITAL MONEY TRENDS REPORT PRESENTED BY INTRODUCTION Canadians continue to look beyond traditional sources when learning about and applying for personal finance products. Sites like RateHub.ca, which

DIGITAL MONEY TRENDS REPORT PRESENTED BY INTRODUCTION Canadians continue to look beyond traditional sources when learning about and applying for personal finance products. Sites like RateHub.ca, which

at the center of banking since 1853 SM

at the center of banking since 1853 SM The Clearing House: The oldest banking association and payments company in the United States. Originally established in 1853 to bring order to clearing and settling

at the center of banking since 1853 SM The Clearing House: The oldest banking association and payments company in the United States. Originally established in 1853 to bring order to clearing and settling

Federally Insured by NCUA. Business Banking

Federally Insured by NCUA Business Banking It s important you have someone you can trust when it comes to your business needs. Helping you achieve your financial goals is our top priority, and our experienced

Federally Insured by NCUA Business Banking It s important you have someone you can trust when it comes to your business needs. Helping you achieve your financial goals is our top priority, and our experienced

people and culture are key to our success

april 2018 dear fellow shareholders, 2017 capped Morgan Stanley s journey through a multi-decade period of challenges and recovery. By transforming our business mix and risk profile, and embracing the

april 2018 dear fellow shareholders, 2017 capped Morgan Stanley s journey through a multi-decade period of challenges and recovery. By transforming our business mix and risk profile, and embracing the

2020 STRATEGIC AND FINANCIAL PLAN TRANSFORM TO GROW

2020 STRATEGIC AND FINANCIAL PLAN TRANSFORM TO GROW Paris, 27 November 2017 Societe Generale will present tomorrow its 2020 Strategic and Financial Plan at an Investor Day in Paris. Commenting on the plan,

2020 STRATEGIC AND FINANCIAL PLAN TRANSFORM TO GROW Paris, 27 November 2017 Societe Generale will present tomorrow its 2020 Strategic and Financial Plan at an Investor Day in Paris. Commenting on the plan,

INSURTECH OUTLOOK. Executive Summary september 2016

INSURTECH OUTLOOK Executive Summary september 2016 BRUNO ABRIL Global Head, Insurance The Insurance Industry is gradually reinventing itself to respond to the digital transformation challenge, incorporating

INSURTECH OUTLOOK Executive Summary september 2016 BRUNO ABRIL Global Head, Insurance The Insurance Industry is gradually reinventing itself to respond to the digital transformation challenge, incorporating

2018 Edelman Trust Barometer

2018 Edelman Trust Barometer Global Trust in Technology #TrustBarometer 1 2018 Edelman Trust Barometer Methodology Online Survey in 28 Countries 18 years of data 33,000+ respondents total All fieldwork

2018 Edelman Trust Barometer Global Trust in Technology #TrustBarometer 1 2018 Edelman Trust Barometer Methodology Online Survey in 28 Countries 18 years of data 33,000+ respondents total All fieldwork

YOUBIQUITY FINANCE GENERAL INSURANCE SUMMARY.

YOUBIQUITY FINANCE 2016 - GENERAL INSURANCE SUMMARY. Consumers want insurance providers to make digital self-service easier, using support technologies that build customer confidence and better relationships.

YOUBIQUITY FINANCE 2016 - GENERAL INSURANCE SUMMARY. Consumers want insurance providers to make digital self-service easier, using support technologies that build customer confidence and better relationships.

Goldman Sachs U.S. Financial Services Conference 2017

Goldman Sachs U.S. Financial Services Conference 2017 Tim Sloan Chief Executive Officer and President December 5, 2017 2017 Wells Fargo & Company. All rights reserved. Wells Fargo Vision We want to satisfy

Goldman Sachs U.S. Financial Services Conference 2017 Tim Sloan Chief Executive Officer and President December 5, 2017 2017 Wells Fargo & Company. All rights reserved. Wells Fargo Vision We want to satisfy

I would now like to turn over to your host, Maureen Davenport, Fannie Mae's Senior Vice President and Chief Communications Officer.

Fannie Mae First Quarter 2017 Earnings Media Call Remarks Adapted from Comments Delivered by Timothy J. Mayopoulos, President and CEO, Fannie Mae, Washington, DC Operator: Welcome and thank you for standing

Fannie Mae First Quarter 2017 Earnings Media Call Remarks Adapted from Comments Delivered by Timothy J. Mayopoulos, President and CEO, Fannie Mae, Washington, DC Operator: Welcome and thank you for standing

The Young-at-Heart Economy

ECONOMIC COMMENTARY SPRING 2018 The Young-at-Heart Economy 5 REASONS WE DON T EXPECT AN ECONOMIC DOWNTURN SOON SUMMARY ANTHONY CHAN, PhD CHIEF ECONOMIST FOR CHASE Anthony is a member of the J.P. Morgan

ECONOMIC COMMENTARY SPRING 2018 The Young-at-Heart Economy 5 REASONS WE DON T EXPECT AN ECONOMIC DOWNTURN SOON SUMMARY ANTHONY CHAN, PhD CHIEF ECONOMIST FOR CHASE Anthony is a member of the J.P. Morgan

Global Stock Plan Services

Global Stock Plan Services Understanding Your Equity Compensation Needs Company-sponsored equity plans not only represent a significant investment in your employees and your company, but also may be challenging

Global Stock Plan Services Understanding Your Equity Compensation Needs Company-sponsored equity plans not only represent a significant investment in your employees and your company, but also may be challenging

SHARETHIS FINANCE STUDY

SHARETHIS FINANCE STUDY EVERY MONTH, 32 MILLION USERS GENERATE 68 MILLION SOCIAL ACTIONS RELATED TO FINANCE. 32 Million Finance Sharers SHARETHIS SOCIAL INTELLIGENCE PLATFORM 53 Billion Webpage Views 3.1

SHARETHIS FINANCE STUDY EVERY MONTH, 32 MILLION USERS GENERATE 68 MILLION SOCIAL ACTIONS RELATED TO FINANCE. 32 Million Finance Sharers SHARETHIS SOCIAL INTELLIGENCE PLATFORM 53 Billion Webpage Views 3.1

These financial impacts are considerable in terms of the scale of credit union operations. $1.1 BILLION. Total Financial Impact of Regulation .

Credit Unions Strongest Advocate Regulatory Burden Financial Impact Study EXECUTIVE SUMMARY Credit unions recognize that they operate in a regulated industry and must bear reasonable costs of regulation.

Credit Unions Strongest Advocate Regulatory Burden Financial Impact Study EXECUTIVE SUMMARY Credit unions recognize that they operate in a regulated industry and must bear reasonable costs of regulation.

Blockchain and Trucking: The Promise and Potential

Blockchain, sometimes referred to as distributed ledger technology (DLT), has been making a lot of headlines lately in business news. The general public might associate blockchain with Bitcoin. However,

Blockchain, sometimes referred to as distributed ledger technology (DLT), has been making a lot of headlines lately in business news. The general public might associate blockchain with Bitcoin. However,

Will Mortgage Tech Power 2018?

Will Mortgage Tech Power 2018? Mortgage Efficiency Survey 2017 www.iress.com September 2017 1 Will Mortgage Tech Power 2018? Mortgage Efficiency Survey 2017 Contents Findings at a glance 3 Buyer types

Will Mortgage Tech Power 2018? Mortgage Efficiency Survey 2017 www.iress.com September 2017 1 Will Mortgage Tech Power 2018? Mortgage Efficiency Survey 2017 Contents Findings at a glance 3 Buyer types

Released: September 7, 2010

Released: September 7, 2010 Commentary 2 The Numbers That Drive Real Estate 3 Recent Government Action 10 Topics for Home Buyers, Sellers, and Owners 13 Brought to you by: KW Research Commentary The housing

Released: September 7, 2010 Commentary 2 The Numbers That Drive Real Estate 3 Recent Government Action 10 Topics for Home Buyers, Sellers, and Owners 13 Brought to you by: KW Research Commentary The housing

The Time is now EPOS. Everything is Possible A new era has started. Don t pass it. It s your chance to make a change!

The Time is now EPOS Everything is Possible A new era has started. Don t pass it. It s your chance to make a change! Blockchain technology will revolutionize payments and much more. So look for a way how

The Time is now EPOS Everything is Possible A new era has started. Don t pass it. It s your chance to make a change! Blockchain technology will revolutionize payments and much more. So look for a way how

AICPA Business and Industry Economic Outlook Survey. Detailed Survey Results: 4Q 2018

AICPA Business and Industry Economic Outlook Survey Detailed Survey Results: 4Q 2018 Survey Background Conducted between November 7-28, 2018 Quarterly Survey CPA decision makers (primarily CFO s, CEOs

AICPA Business and Industry Economic Outlook Survey Detailed Survey Results: 4Q 2018 Survey Background Conducted between November 7-28, 2018 Quarterly Survey CPA decision makers (primarily CFO s, CEOs

SMART HOMES: POWERING NEW P&C INSURANCE September 2018

SMART HOMES: POWERING NEW P&C INSURANCE September 2018 1 SMART HOMES: POWERING THE NEW P&C INSURANCE Smart home technology is not only revolutionizing Property and Casualty policy writing - it s revolutionizing

SMART HOMES: POWERING NEW P&C INSURANCE September 2018 1 SMART HOMES: POWERING THE NEW P&C INSURANCE Smart home technology is not only revolutionizing Property and Casualty policy writing - it s revolutionizing

BANK EXECUTIVE BUSINESS OUTLOOK SURVEY 2015, Q3

BANKS SHOWING SIGNS OF OPTIMISM As banks enter year seven of economic recovery. BANK EXECUTIVE BUSINESS OUTLOOK SURVEY 2015, Q3 1 INTRODUCTION BANKS SHOWING SIGNS OF OPTIMISM As banks enter year seven

BANKS SHOWING SIGNS OF OPTIMISM As banks enter year seven of economic recovery. BANK EXECUTIVE BUSINESS OUTLOOK SURVEY 2015, Q3 1 INTRODUCTION BANKS SHOWING SIGNS OF OPTIMISM As banks enter year seven

#$%&#%'##( ) *+,) -"

*+,) -") Page 1 of 10!"!" #$%" &' ('( $)" $*% ( %+,,-%+.+$#(. +/01230244 Market Musings #$%&#%'##( ) *+,) -" Lousy economic moved the market lower as the pork in Obama's stimulus package began to also surface.

Page 1 of 10!"!" #$%" &' ('( $)" $*% ( %+,,-%+.+$#(. +/01230244 Market Musings #$%&#%'##( ) *+,) -" Lousy economic moved the market lower as the pork in Obama's stimulus package began to also surface.

Based on the audacious premise that a lot more can be done with a lot less.

A lot less of IT involvement, minimal processes, greater attention to high-value tasks, enhanced decision-making all resulting in better underwriting. Based on the audacious premise that a lot more can

A lot less of IT involvement, minimal processes, greater attention to high-value tasks, enhanced decision-making all resulting in better underwriting. Based on the audacious premise that a lot more can

A HISTORIC TRANSFER OF WEALTH IS IMMINENT

A HISTORIC TRANSFER OF WEALTH IS IMMINENT Connect With The Millennial Investors Who Will Control It. A new generation is edging into the workforce and slowly taking over leadership positions. At the same

A HISTORIC TRANSFER OF WEALTH IS IMMINENT Connect With The Millennial Investors Who Will Control It. A new generation is edging into the workforce and slowly taking over leadership positions. At the same

WELCOME TO BETHPAGE. Extraordinary value and service, anytime, anywhere.

WELCOME TO BETHPAGE Dear Member: Welcome and Congratulations! You are now a member of Long Island s premier community financial institution. At Bethpage, we re built to give you more because we re a credit

WELCOME TO BETHPAGE Dear Member: Welcome and Congratulations! You are now a member of Long Island s premier community financial institution. At Bethpage, we re built to give you more because we re a credit

I. Content of business

I. Content of business (I) Business activities Jih Sun Financial Holding Co., Ltd. 1. Principal business activities The Company is a financial holding company; its business activities are confined to those

I. Content of business (I) Business activities Jih Sun Financial Holding Co., Ltd. 1. Principal business activities The Company is a financial holding company; its business activities are confined to those

INNOVATIONS IN IDENTITY IN FINANCIAL SERVICES

In financial services, identity defines and permits the relationship between providers and clients. Financial institutions need to know they are lending to genuine, legal and reliable customers, and customers

In financial services, identity defines and permits the relationship between providers and clients. Financial institutions need to know they are lending to genuine, legal and reliable customers, and customers

Cash, electronic or online: How do Germans pay?

Monitor Household finance December, 18 Authors Heike Mai +9 9 91-31 heike.mai@db.com Orçun Kaya +9 9 91-3173 orcun.kaya@db.com Editor Jan Schildbach Deutsche Bank AG Deutsche Bank Research Frankfurt am

Monitor Household finance December, 18 Authors Heike Mai +9 9 91-31 heike.mai@db.com Orçun Kaya +9 9 91-3173 orcun.kaya@db.com Editor Jan Schildbach Deutsche Bank AG Deutsche Bank Research Frankfurt am

Bank of America Morgan Stanley Financials Conference

Bank of America Morgan Stanley Financials Conference Dean Athanasia Co-head of Consumer & Small Business June 12, 2018 Consumer Banking key takeaways 1. Powerful, industry-leading U.S. consumer franchise

Bank of America Morgan Stanley Financials Conference Dean Athanasia Co-head of Consumer & Small Business June 12, 2018 Consumer Banking key takeaways 1. Powerful, industry-leading U.S. consumer franchise

Advertising Compliance

Advertising Compliance John Zasada Principal 218 790 1086 1 1 Credit Union Compliance Practice Review websites and social media for compliance before CU release Ongoing Regulatory Compliance Assistance

Advertising Compliance John Zasada Principal 218 790 1086 1 1 Credit Union Compliance Practice Review websites and social media for compliance before CU release Ongoing Regulatory Compliance Assistance

Augmenting the Retail Deposit Franchise in Today's Environment. Kevin Kirksey

Augmenting the Retail Deposit Franchise in Today's Environment Kevin Kirksey Agenda Trends in non-maturity deposits Critical non-maturity deposit variables RATE CHANGE COEFFICIENT (BETA) NON-INTEREST COST

Augmenting the Retail Deposit Franchise in Today's Environment Kevin Kirksey Agenda Trends in non-maturity deposits Critical non-maturity deposit variables RATE CHANGE COEFFICIENT (BETA) NON-INTEREST COST

Global Financial Crisis and China s Countermeasures

Global Financial Crisis and China s Countermeasures Qin Xiao The year 2008 will go down in history as a once-in-a-century financial tsunami. This year, as the crisis spreads globally, the impact has been

Global Financial Crisis and China s Countermeasures Qin Xiao The year 2008 will go down in history as a once-in-a-century financial tsunami. This year, as the crisis spreads globally, the impact has been

Harnessing the 'Bang': from Digital Disruption to Digital Transformation

Harnessing the 'Bang': from Digital Disruption to Digital Transformation Stephen Huppert Deloitte Touche Tohmatsu This presentation has been prepared for the Actuaries Institute 2015 Actuaries Summit.

Harnessing the 'Bang': from Digital Disruption to Digital Transformation Stephen Huppert Deloitte Touche Tohmatsu This presentation has been prepared for the Actuaries Institute 2015 Actuaries Summit.

ICICI Group. Performance and Strategy. February 2016

ICICI Group Performance and Strategy February 2016 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to

ICICI Group Performance and Strategy February 2016 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to

We are a Nonpartisan Organization Working to: RAISE PUBLIC AWARENESS CONVENE LEADERS AND STAKEHOLDERS DRIVE GROUNDBREAKING RESEARCH

MEDIA KIT We are a Nonpartisan Organization Working to: RAISE PUBLIC AWARENESS about fiscal challenges threatening America s economy CONVENE LEADERS AND STAKEHOLDERS from across the political and ideological

MEDIA KIT We are a Nonpartisan Organization Working to: RAISE PUBLIC AWARENESS about fiscal challenges threatening America s economy CONVENE LEADERS AND STAKEHOLDERS from across the political and ideological

2010 National Auto Insurance Study SM

Keeping Millennials for Life: Tailoring Service to Meet the Unique Needs of Generation Y Customers July 2010 Insurance Practice A Global Marketing Information Company businesscenter.jdpower.com 37309844358/080210

Keeping Millennials for Life: Tailoring Service to Meet the Unique Needs of Generation Y Customers July 2010 Insurance Practice A Global Marketing Information Company businesscenter.jdpower.com 37309844358/080210

MARKETPLACE LENDING FOR INSTITUTIONAL INVESTORS AND WEALTH MANAGERS

MARKETPLACE LENDING FOR INSTITUTIONAL INVESTORS AND WEALTH MANAGERS An Overview 2017 MARK SHORE Chief Research Officer, Shore Capital Research, LLC Adjunct Professor, DePaul University Since 2014 when

MARKETPLACE LENDING FOR INSTITUTIONAL INVESTORS AND WEALTH MANAGERS An Overview 2017 MARK SHORE Chief Research Officer, Shore Capital Research, LLC Adjunct Professor, DePaul University Since 2014 when

Operational Excellence / Transformative Strategies for Insurers

5 Operational Excellence / Transformative Strategies for Insurers The insurance market has been under pressure to transform for many years now. PWC identify five distinct pressure points: social, technological,

5 Operational Excellence / Transformative Strategies for Insurers The insurance market has been under pressure to transform for many years now. PWC identify five distinct pressure points: social, technological,

BANK OF AMERICA MERRILL LYNCH 17 th Annual Banking & Insurance CEO Conference. 25 September António Horta-Osório

BANK OF AMERICA MERRILL LYNCH 17 th Annual Banking & Insurance CEO Conference 25 September 2012 António Horta-Osório Group Chief Executive AGENDA STRONG CORE FRANCHISE REDUCING RISK & INCREASING EFFICIENCY

BANK OF AMERICA MERRILL LYNCH 17 th Annual Banking & Insurance CEO Conference 25 September 2012 António Horta-Osório Group Chief Executive AGENDA STRONG CORE FRANCHISE REDUCING RISK & INCREASING EFFICIENCY