1. Draw a timeline to determine the number of periods for which each cash flow will earn the rate-of-return 2. Calculate the future value of each

|

|

|

- Preston Phillips

- 5 years ago

- Views:

Transcription

1

2

3

4

5 1. Draw a timeline to determine the number of periods for which each cash flow will earn the rate-of-return 2. Calculate the future value of each cash flow using Equation Add the future values

6

7

8

9 A series of equally-spaced and level cash flows extending over a finite number of periods A series of equally-spaced and level cash flows that continue forever

10 cash flows occur at the end of a period cash flows occur at the beginning of a period

11

12 To calculate a future value or a present value is to calculate an equivalent amount The amount reflects an adjustment to account for the effect of compounding

13 Present value of an annuity

14 A contract will pay $2,000 at the end of each year for three years and the appropriate discount rate is 8%. What is a fair price for the contract?

15 Present Value of Annuity

16 You borrow $400,000 to buy a home. The 30- year mortgage requires 360 monthly payments at a monthly rate of 6.15%/12 or.51042%. How much is the monthly payment?

17

18 How borrowed funds are repaid over the life of a loan Each payment includes less interest and more principal; the loan is paid off with the last payment Amortization schedule shows interest and principal in each payment, and amount of principal still owed after each payment

19

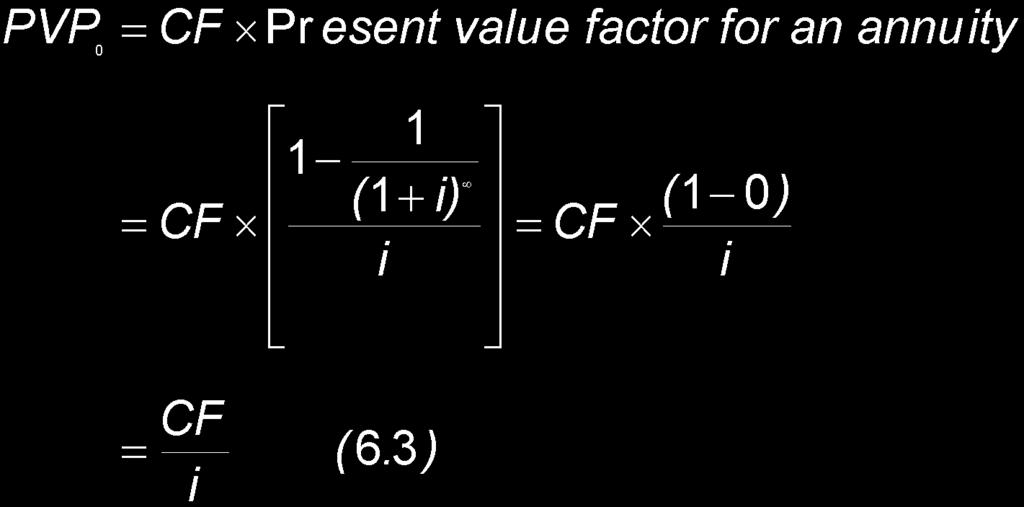

20

21

22 The present value of an annuity equation can be used to find the interest rate or discount rate for an annuity To determine the rate-of-return for an annuity, solve the equation for i Using a calculator is easier than a trial-and-error approach

23 Finding the Interest Rate

24 The future value of an annuity equation is derived from Equation 6.1

25

26 Future Value of an Annuity

27 A stream of equal cash flows that goes on forever Preferred stock and some bonds are perpetuities Equation for the present value of a perpetuity can be derived from the present value of an annuity equation

28

29 Suppose you decide to endow a chair in finance. The goal of the endowment is to provide $100,000 of financial support per year forever. If the endowment earns a rate of 8%, how much money will you have to donate to provide the desired level of support?

30 Present Value of Annuity Due Future Value of Annuity Due

31 The present value or future value of an annuity due is always higher than that of an ordinary annuity that is otherwise identical.

32

33 equally-spaced cash flows that increase in size at a constant rate for a finite number of periods equally-spaced cash flows that increase in size at a constant rate forever

34 Multiyear product or service contract with periodic cash flows that increase at a constant rate for a finite number of years Common stock whose dividend is expected to increase at a constant rate forever

35 Calculate the present value of growing annuity (only) when the growth rate is less than the discount rate.

36 A coffee shop will operate for fifty more years. Cash flow was $300,000 last year and increases by 2.5% each year. The discount rate for similar firms is 15%. Estimate the value of the firm.

when the growth rate is less than")

37 Use Equation 6.6 to calculate the present value of growing perpetuity (only) when the growth rate is less than discount rate. It is derived from equation 6.5 when the number of periods approaches infinity

38 A firm s cash flow was $450,000 last year. You expect the cash flow to increase by 5% per year forever. If you use a discount rate of 18%, what is the value of the firm?

39 The most common way to quote interest rates is in terms of annual percentage rate (APR). It does not incorporate the effects of compounding. The most appropriate way to quote interest rates is in terms of effective annual rate (EAR). It incorporates the effects of compounding.

40 APR = (periodic rate) x m APR does not account for the number of compounding periods or adjust the annualized interest rate for the time value of money APR is not a precise measure of the rates involved in borrowing and investing

41 Anna is charged 1% interest when she borrows $2000 for one week. What is the annual percentage interest rate (APR) on the loan?

42 EAR accounts for the number of compounding periods and adjusts the annualized interest rate for the time value of money EAR is a more accurate measure of the rates involved in lending and investing

43 Anna is charged 1% interest when she borrows $2000 for one week. What is the effective annual interest rate (EAR)?

. What is the EAR?")

44 Your credit card has an APR of 12 % (1% per month). What is the EAR?

45 Truth-in-Lending Act (1968) requires that borrowers be told the actual cost of credit Truth-in-Savings Act (1991) requires that the actual return on savings be disclosed to consumers Credit Card Act (2009) limits credit card fees and interest rate increases, and requires better disclosure of contract details

CHAPTER 4 TIME VALUE OF MONEY

CHAPTER 4 TIME VALUE OF MONEY 1 Learning Outcomes LO.1 Identify various types of cash flow patterns (streams) seen in business. LO.2 Compute the future value of different cash flow streams. Explain the

CHAPTER 4 TIME VALUE OF MONEY 1 Learning Outcomes LO.1 Identify various types of cash flow patterns (streams) seen in business. LO.2 Compute the future value of different cash flow streams. Explain the

Future Value of Multiple Cash Flows

Future Value of Multiple Cash Flows FV t CF 0 t t r CF r... CF t You open a bank account today with $500. You expect to deposit $,000 at the end of each of the next three years. Interest rates are 5%,

Future Value of Multiple Cash Flows FV t CF 0 t t r CF r... CF t You open a bank account today with $500. You expect to deposit $,000 at the end of each of the next three years. Interest rates are 5%,

Time Value of Money. Part III. Outline of the Lecture. September Growing Annuities. The Effect of Compounding. Loan Type and Loan Amortization

Time Value of Money Part III September 2003 Outline of the Lecture Growing Annuities The Effect of Compounding Loan Type and Loan Amortization 2 Growing Annuities The present value of an annuity in which

Time Value of Money Part III September 2003 Outline of the Lecture Growing Annuities The Effect of Compounding Loan Type and Loan Amortization 2 Growing Annuities The present value of an annuity in which

3. Time value of money. We will review some tools for discounting cash flows.

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

3. Time value of money

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

Lecture 3. Chapter 4: Allocating Resources Over Time

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Principles of Corporate Finance

Principles of Corporate Finance Professor James J. Barkocy Time is money really McGraw-Hill/Irwin Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Time Value of Money Money has a

Principles of Corporate Finance Professor James J. Barkocy Time is money really McGraw-Hill/Irwin Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Time Value of Money Money has a

Time Value of Money. All time value of money problems involve comparisons of cash flows at different dates.

Time Value of Money The time value of money is a very important concept in Finance. This section is aimed at giving you intuitive and hands-on training on how to price securities (e.g., stocks and bonds),

Time Value of Money The time value of money is a very important concept in Finance. This section is aimed at giving you intuitive and hands-on training on how to price securities (e.g., stocks and bonds),

Time Value of Money. Lakehead University. Outline of the Lecture. Fall Future Value and Compounding. Present Value and Discounting

Time Value of Money Lakehead University Fall 2004 Outline of the Lecture Future Value and Compounding Present Value and Discounting More on Present and Future Values 2 Future Value and Compounding Future

Time Value of Money Lakehead University Fall 2004 Outline of the Lecture Future Value and Compounding Present Value and Discounting More on Present and Future Values 2 Future Value and Compounding Future

Solution Set 1 Foundations of Finance. Problem Set 1 Solution: Time Value of Money and Equity Markets

Problem Set 1 Solution: Time Value of Money Equity Markets I. Present Value with Multiple Cash Flows: 0 1 2 3 A: 40000 40000 B: 30000 20000 20000 APR is 16% compounded quarterly; Periodic Rate (with quarterly

Problem Set 1 Solution: Time Value of Money Equity Markets I. Present Value with Multiple Cash Flows: 0 1 2 3 A: 40000 40000 B: 30000 20000 20000 APR is 16% compounded quarterly; Periodic Rate (with quarterly

1. Assume that monthly payments begin in one month. What will each payment be? A) $ B) $1, C) $1, D) $1, E) $1,722.

$ B) $1, C) $1, D) $1, E) $1,722.") Name: Date: You and your spouse have found your dream home. The selling price is $220,000; you will put $50,000 down and obtain a 30-year fixed-rate mortgage at 7.5% APR for the balance. 1. Assume that

Name: Date: You and your spouse have found your dream home. The selling price is $220,000; you will put $50,000 down and obtain a 30-year fixed-rate mortgage at 7.5% APR for the balance. 1. Assume that

Chapter 6. Learning Objectives. Principals Applies in this Chapter. Time Value of Money

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

Chapter 02 Test Bank - Static KEY

Chapter 02 Test Bank - Static KEY 1. The present value of $100 expected two years from today at a discount rate of 6 percent is A. $112.36. B. $106.00. C. $100.00. D. $89.00. 2. Present value is defined

Chapter 02 Test Bank - Static KEY 1. The present value of $100 expected two years from today at a discount rate of 6 percent is A. $112.36. B. $106.00. C. $100.00. D. $89.00. 2. Present value is defined

Chapter 5 Time Value of Money

Chapter 5 Time Value of Money Answers to End-of-Chapter 5 Questions 5-1 The opportunity cost is the rate of interest one could earn on an alternative investment with a risk equal to the risk of the investment

Chapter 5 Time Value of Money Answers to End-of-Chapter 5 Questions 5-1 The opportunity cost is the rate of interest one could earn on an alternative investment with a risk equal to the risk of the investment

Midterm Review Package Tutor: Chanwoo Yim

COMMERCE 298 Intro to Finance Midterm Review Package Tutor: Chanwoo Yim BCom 2016, Finance 1. Time Value 2. DCF (Discounted Cash Flow) 2.1 Constant Annuity 2.2 Constant Perpetuity 2.3 Growing Annuity 2.4

COMMERCE 298 Intro to Finance Midterm Review Package Tutor: Chanwoo Yim BCom 2016, Finance 1. Time Value 2. DCF (Discounted Cash Flow) 2.1 Constant Annuity 2.2 Constant Perpetuity 2.3 Growing Annuity 2.4

CHAPTER 4. The Time Value of Money. Chapter Synopsis

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

Chapter 4 The Time Value of Money

Chapter 4 The Time Value of Money Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 4.1 The Timeline 4.2 The Three Rules of Time Travel 4.3 Valuing a Stream of Cash Flows 4.4 Calculating

Chapter 4 The Time Value of Money Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 4.1 The Timeline 4.2 The Three Rules of Time Travel 4.3 Valuing a Stream of Cash Flows 4.4 Calculating

Chapter 2 Time Value of Money

1. Future Value of a Lump Sum 2. Present Value of a Lump Sum 3. Future Value of Cash Flow Streams 4. Present Value of Cash Flow Streams 5. Perpetuities 6. Uneven Series of Cash Flows 7. Other Compounding

1. Future Value of a Lump Sum 2. Present Value of a Lump Sum 3. Future Value of Cash Flow Streams 4. Present Value of Cash Flow Streams 5. Perpetuities 6. Uneven Series of Cash Flows 7. Other Compounding

Financial Management I

Financial Management I Workshop on Time Value of Money MBA 2016 2017 Slide 2 Finance & Valuation Capital Budgeting Decisions Long-term Investment decisions Investments in Net Working Capital Financing

Financial Management I Workshop on Time Value of Money MBA 2016 2017 Slide 2 Finance & Valuation Capital Budgeting Decisions Long-term Investment decisions Investments in Net Working Capital Financing

บทท 3 ม ลค าของเง นตามเวลา (Time Value of Money)

") บทท 3 ม ลค าของเง นตามเวลา (Time Value of Money) Topic Coverage: The Interest Rate Simple Interest Rate Compound Interest Rate Amortizing a Loan Compounding Interest More Than Once per Year The Time Value

บทท 3 ม ลค าของเง นตามเวลา (Time Value of Money) Topic Coverage: The Interest Rate Simple Interest Rate Compound Interest Rate Amortizing a Loan Compounding Interest More Than Once per Year The Time Value

SOLUTION METHODS FOR SELECTED BASIC FINANCIAL RELATIONSHIPS

SVEN THOMMESEN FINANCE 2400/3200/3700 Spring 2018 [Updated 8/31/16] SOLUTION METHODS FOR SELECTED BASIC FINANCIAL RELATIONSHIPS VARIABLES USED IN THE FOLLOWING PAGES: N = the number of periods (months,

SVEN THOMMESEN FINANCE 2400/3200/3700 Spring 2018 [Updated 8/31/16] SOLUTION METHODS FOR SELECTED BASIC FINANCIAL RELATIONSHIPS VARIABLES USED IN THE FOLLOWING PAGES: N = the number of periods (months,

Review for Exam #2. Review for Exam #2. Exam #2. Don t Forget: Scan Sheet Calculator Pencil Picture ID Cheat Sheet.

Review for Exam #2 Exam #2 Don t Forget: Scan Sheet Calculator Pencil Picture ID Cheat Sheet Things To Do Study both the notes and the book. Do suggested problems. Do more problems! Be comfortable with

Review for Exam #2 Exam #2 Don t Forget: Scan Sheet Calculator Pencil Picture ID Cheat Sheet Things To Do Study both the notes and the book. Do suggested problems. Do more problems! Be comfortable with

Chapter 5. Learning Objectives. Principals Applied in this Chapter. Time Value of Money. Principle 1: Money Has a Time Value.

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5. Time Value of Money

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

FinQuiz Notes

Reading 6 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 6 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

A central precept of financial analysis is money s time value. This essentially means that every dollar (or

INTRODUCTION TO THE TIME VALUE OF MONEY 1. INTRODUCTION A central precept of financial analysis is money s time value. This essentially means that every dollar (or a unit of any other currency) received

INTRODUCTION TO THE TIME VALUE OF MONEY 1. INTRODUCTION A central precept of financial analysis is money s time value. This essentially means that every dollar (or a unit of any other currency) received

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value

CHAPTER 2 How to Calculate Present Values

CHAPTER How to Calculate Present Values Answers to Problem Sets. If the discount factor is.507, then.507 x. 6 = $. Est time: 0-05. DF x 39 = 5. Therefore, DF =5/39 =.899. Est time: 0-05 3. PV = 374/(.09)

CHAPTER How to Calculate Present Values Answers to Problem Sets. If the discount factor is.507, then.507 x. 6 = $. Est time: 0-05. DF x 39 = 5. Therefore, DF =5/39 =.899. Est time: 0-05 3. PV = 374/(.09)

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concept Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value decreases. 2. Assuming positive

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concept Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value decreases. 2. Assuming positive

Format: True/False. Learning Objective: LO 3

Parrino/Fundamentals of Corporate Finance, Test Bank, Chapter 6 1.Calculating the present and future values of multiple cash flows is relevant only for individual investors. 2.Calculating the present and

Parrino/Fundamentals of Corporate Finance, Test Bank, Chapter 6 1.Calculating the present and future values of multiple cash flows is relevant only for individual investors. 2.Calculating the present and

FINAN303 Principles of Finance Spring Time Value of Money Part B

Time Value of Money Part B 1. Examples of multiple cash flows - PV Mult = a. Present value of a perpetuity b. Present value of an annuity c. Uneven cash flows T CF t t=0 (1+i) t 2. Annuity vs. Perpetuity

Time Value of Money Part B 1. Examples of multiple cash flows - PV Mult = a. Present value of a perpetuity b. Present value of an annuity c. Uneven cash flows T CF t t=0 (1+i) t 2. Annuity vs. Perpetuity

5-1 FUTURE VALUE If you deposit $10,000 in a bank account that pays 10% interest ann~ally, how much will be in your account after 5 years?

174 Part 2 Fundamental Concepts in Financial Management QuESTIONS 5-1 What is an opportunity cost? How is this concept used in TVM analysis, and where is it shown on a time line? Is a single number used

174 Part 2 Fundamental Concepts in Financial Management QuESTIONS 5-1 What is an opportunity cost? How is this concept used in TVM analysis, and where is it shown on a time line? Is a single number used

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concept Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value decreases. 2. Assuming positive

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concept Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value decreases. 2. Assuming positive

Disclaimer: This resource package is for studying purposes only EDUCATION

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 1: The Corporation The Three Types of Firms -Sole Proprietorships -Owned and ran by one person -Owner has unlimited liability

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 1: The Corporation The Three Types of Firms -Sole Proprietorships -Owned and ran by one person -Owner has unlimited liability

Chapter 4. Discounted Cash Flow Valuation

Chapter 4 Discounted Cash Flow Valuation Appreciate the significance of compound vs. simple interest Describe and compute the future value and/or present value of a single cash flow or series of cash flows

Chapter 4 Discounted Cash Flow Valuation Appreciate the significance of compound vs. simple interest Describe and compute the future value and/or present value of a single cash flow or series of cash flows

Fahmi Ben Abdelkader HEC, Paris Fall Students version 9/11/2012 7:50 PM 1

Financial Economics Time Value of Money Fahmi Ben Abdelkader HEC, Paris Fall 2012 Students version 9/11/2012 7:50 PM 1 Chapter Outline Time Value of Money: introduction Time Value of money Financial Decision

Financial Economics Time Value of Money Fahmi Ben Abdelkader HEC, Paris Fall 2012 Students version 9/11/2012 7:50 PM 1 Chapter Outline Time Value of Money: introduction Time Value of money Financial Decision

Chapter 03 - Basic Annuities

3-1 Chapter 03 - Basic Annuities Section 3.0 - Sum of a Geometric Sequence The form for the sum of a geometric sequence is: Sum(n) a + ar + ar 2 + ar 3 + + ar n 1 Here a = (the first term) n = (the number

3-1 Chapter 03 - Basic Annuities Section 3.0 - Sum of a Geometric Sequence The form for the sum of a geometric sequence is: Sum(n) a + ar + ar 2 + ar 3 + + ar n 1 Here a = (the first term) n = (the number

Chapter 4. Discounted Cash Flow Valuation

Chapter 4 Discounted Cash Flow Valuation 1 Acknowledgement This work is reproduced, based on the book [Ross, Westerfield, Jaffe and Jordan Core Principles and Applications of Corporate Finance ]. This

Chapter 4 Discounted Cash Flow Valuation 1 Acknowledgement This work is reproduced, based on the book [Ross, Westerfield, Jaffe and Jordan Core Principles and Applications of Corporate Finance ]. This

Chapter 5. Interest Rates ( ) 6. % per month then you will have ( 1.005) = of 2 years, using our rule ( ) = 1.

6. % per month then you will have ( 1.005) = of 2 years, using our rule ( ) = 1.") Chapter 5 Interest Rates 5-. 6 a. Since 6 months is 24 4 So the equivalent 6 month rate is 4.66% = of 2 years, using our rule ( ) 4 b. Since one year is half of 2 years ( ).2 2 =.0954 So the equivalent

Chapter 5 Interest Rates 5-. 6 a. Since 6 months is 24 4 So the equivalent 6 month rate is 4.66% = of 2 years, using our rule ( ) 4 b. Since one year is half of 2 years ( ).2 2 =.0954 So the equivalent

Perpetuity It is a type of annuity whose payments continue forever.

Perpetuity It is a type of annuity whose payments continue forever. Something to think about... How does an equal payment at an equal interval continue forever? Example: An individual might, for example

Perpetuity It is a type of annuity whose payments continue forever. Something to think about... How does an equal payment at an equal interval continue forever? Example: An individual might, for example

Mathematics of Finance

CHAPTER 55 Mathematics of Finance PAMELA P. DRAKE, PhD, CFA J. Gray Ferguson Professor of Finance and Department Head of Finance and Business Law, James Madison University FRANK J. FABOZZI, PhD, CFA, CPA

CHAPTER 55 Mathematics of Finance PAMELA P. DRAKE, PhD, CFA J. Gray Ferguson Professor of Finance and Department Head of Finance and Business Law, James Madison University FRANK J. FABOZZI, PhD, CFA, CPA

I. Warnings for annuities and

Outline I. More on the use of the financial calculator and warnings II. Dealing with periods other than years III. Understanding interest rate quotes and conversions IV. Applications mortgages, etc. 0

Outline I. More on the use of the financial calculator and warnings II. Dealing with periods other than years III. Understanding interest rate quotes and conversions IV. Applications mortgages, etc. 0

The three formulas we use most commonly involving compounding interest n times a year are

Section 6.6 and 6.7 with finance review questions are included in this document for your convenience for studying for quizzes and exams for Finance Calculations for Math 11. Section 6.6 focuses on identifying

Section 6.6 and 6.7 with finance review questions are included in this document for your convenience for studying for quizzes and exams for Finance Calculations for Math 11. Section 6.6 focuses on identifying

CHAPTER 2 TIME VALUE OF MONEY

CHAPTER 2 TIME VALUE OF MONEY True/False Easy: (2.2) Compounding Answer: a EASY 1. One potential benefit from starting to invest early for retirement is that the investor can expect greater benefits from

CHAPTER 2 TIME VALUE OF MONEY True/False Easy: (2.2) Compounding Answer: a EASY 1. One potential benefit from starting to invest early for retirement is that the investor can expect greater benefits from

Lecture 2 Time Value of Money FINA 614

Lecture 2 Time Value of Money FINA 614 Basic Defini?ons Present Value earlier money on a?me line Future Value later money on a?me line Interest rate exchange rate between earlier money and later money

Lecture 2 Time Value of Money FINA 614 Basic Defini?ons Present Value earlier money on a?me line Future Value later money on a?me line Interest rate exchange rate between earlier money and later money

JEM034 Corporate Finance Winter Semester 2017/2018

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #1 Olga Bychkova Topics Covered Today Review of key finance concepts Present value (chapter 2 in BMA) Valuation of bonds (chapter 3 in BMA) Present

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #1 Olga Bychkova Topics Covered Today Review of key finance concepts Present value (chapter 2 in BMA) Valuation of bonds (chapter 3 in BMA) Present

Course FM 4 May 2005

1. Which of the following expressions does NOT represent a definition for a? n (A) (B) (C) (D) (E) v n 1 v i n 1i 1 i n vv v 2 n n 1 v v 1 v s n n 1 i 1 Course FM 4 May 2005 2. Lori borrows 10,000 for

1. Which of the following expressions does NOT represent a definition for a? n (A) (B) (C) (D) (E) v n 1 v i n 1i 1 i n vv v 2 n n 1 v v 1 v s n n 1 i 1 Course FM 4 May 2005 2. Lori borrows 10,000 for

Quantitative Literacy: Thinking Between the Lines

Quantitative Literacy: Thinking Between the Lines Crauder, Evans, Johnson, Noell Chapter 4: Personal Finance 2011 W. H. Freeman and Company 1 Chapter 4: Personal Finance Lesson Plan Saving money: The power

Quantitative Literacy: Thinking Between the Lines Crauder, Evans, Johnson, Noell Chapter 4: Personal Finance 2011 W. H. Freeman and Company 1 Chapter 4: Personal Finance Lesson Plan Saving money: The power

ADMS Finance Midterm Exam Winter 2012 Saturday Feb. 11, Type A Exam

Name Section ID # Prof. Sam Alagurajah Section M Thursdays 4:00 7:00 PM Prof. Lois King Section N Tuesdays, 7:00 10:00 PM Prof. Lois King Section O Internet Prof. Lois King Section P Mondays 11:30 2:30

Name Section ID # Prof. Sam Alagurajah Section M Thursdays 4:00 7:00 PM Prof. Lois King Section N Tuesdays, 7:00 10:00 PM Prof. Lois King Section O Internet Prof. Lois King Section P Mondays 11:30 2:30

Quantitative Literacy: Thinking Between the Lines

Quantitative Literacy: Thinking Between the Lines Crauder, Noell, Evans, Johnson Chapter 4: Personal Finance 2013 W. H. Freeman and Company 1 Chapter 4: Personal Finance Lesson Plan Saving money: The power

Quantitative Literacy: Thinking Between the Lines Crauder, Noell, Evans, Johnson Chapter 4: Personal Finance 2013 W. H. Freeman and Company 1 Chapter 4: Personal Finance Lesson Plan Saving money: The power

TIME VALUE OF MONEY. (Difficulty: E = Easy, M = Medium, and T = Tough) Multiple Choice: Conceptual. Easy:

Multiple Choice: Conceptual. Easy:") TIME VALUE OF MONEY (Difficulty: E = Easy, M = Medium, and T = Tough) Multiple Choice: Conceptual Easy: PV and discount rate Answer: a Diff: E. You have determined the profitability of a planned project

TIME VALUE OF MONEY (Difficulty: E = Easy, M = Medium, and T = Tough) Multiple Choice: Conceptual Easy: PV and discount rate Answer: a Diff: E. You have determined the profitability of a planned project

The time value of money and cash-flow valuation

The time value of money and cash-flow valuation Readings: Ross, Westerfield and Jordan, Essentials of Corporate Finance, Chs. 4 & 5 Ch. 4 problems: 13, 16, 19, 20, 22, 25. Ch. 5 problems: 14, 15, 31, 32,

The time value of money and cash-flow valuation Readings: Ross, Westerfield and Jordan, Essentials of Corporate Finance, Chs. 4 & 5 Ch. 4 problems: 13, 16, 19, 20, 22, 25. Ch. 5 problems: 14, 15, 31, 32,

Understanding Interest Rates

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

Foundations of Finance. Prof. Alex Shapiro

Foundations of Finance Prof. Alex Shapiro Due in class: B01.2311.10 on or before Tuesday, October 7, B01.2311.11 on or before Wednesday, October 8, B01.2311.12 on or before Thursday, October 9. 1. BKM

Foundations of Finance Prof. Alex Shapiro Due in class: B01.2311.10 on or before Tuesday, October 7, B01.2311.11 on or before Wednesday, October 8, B01.2311.12 on or before Thursday, October 9. 1. BKM

SECTION HANDOUT #1 : Review of Topics

SETION HANDOUT # : Review of Topics MBA 0 October, 008 This handout contains some of the topics we have covered so far. You are not required to read it, but you may find some parts of it helpful when you

SETION HANDOUT # : Review of Topics MBA 0 October, 008 This handout contains some of the topics we have covered so far. You are not required to read it, but you may find some parts of it helpful when you

Discounting. Capital Budgeting and Corporate Objectives. Professor Ron Kaniel. Simon School of Business University of Rochester.

Discounting Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Topic Overview The Timeline Compounding & Future Value Discounting & Present

Discounting Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Topic Overview The Timeline Compounding & Future Value Discounting & Present

The Time Value of Money

Chapter 2 The Time Value of Money Time Discounting One of the basic concepts of business economics and managerial decision making is that the value of an amount of money to be received in the future depends

Chapter 2 The Time Value of Money Time Discounting One of the basic concepts of business economics and managerial decision making is that the value of an amount of money to be received in the future depends

Finance Notes AMORTIZED LOANS

Amortized Loans Page 1 of 10 AMORTIZED LOANS Objectives: After completing this section, you should be able to do the following: Calculate the monthly payment for a simple interest amortized loan. Calculate

Amortized Loans Page 1 of 10 AMORTIZED LOANS Objectives: After completing this section, you should be able to do the following: Calculate the monthly payment for a simple interest amortized loan. Calculate

HOW TO CALCULATE PRESENT VALUES

HOW TO CALCULATE PRESENT VALUES Chapter 2 Brealey, Myers, and Allen Principles of Corporate Finance 11 th Global Edition Basics of this chapter Cash Flows (and Free Cash Flows) Definition and why is it

HOW TO CALCULATE PRESENT VALUES Chapter 2 Brealey, Myers, and Allen Principles of Corporate Finance 11 th Global Edition Basics of this chapter Cash Flows (and Free Cash Flows) Definition and why is it

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 01 Introduction Welcome to the course Time value

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 01 Introduction Welcome to the course Time value

5.3 Amortization and Sinking Funds

5.3 Amortization and Sinking Funds Sinking Funds A sinking fund is an account that is set up for a specific purpose at some future date. Typical examples of this are retirement plans, saving money for

5.3 Amortization and Sinking Funds Sinking Funds A sinking fund is an account that is set up for a specific purpose at some future date. Typical examples of this are retirement plans, saving money for

January 29. Annuities

January 29 Annuities An annuity is a repeating payment, typically of a fixed amount, over a period of time. An annuity is like a loan in reverse; rather than paying a loan company, a bank or investment

January 29 Annuities An annuity is a repeating payment, typically of a fixed amount, over a period of time. An annuity is like a loan in reverse; rather than paying a loan company, a bank or investment

4: Single Cash Flows and Equivalence

4.1 Single Cash Flows and Equivalence Basic Concepts 28 4: Single Cash Flows and Equivalence This chapter explains basic concepts of project economics by examining single cash flows. This means that each

4.1 Single Cash Flows and Equivalence Basic Concepts 28 4: Single Cash Flows and Equivalence This chapter explains basic concepts of project economics by examining single cash flows. This means that each

KNGX NOTES FINS1613 [FINS1613] Comprehensive Notes

![KNGX NOTES FINS1613 [FINS1613] Comprehensive Notes](/thumbs/89/99612905.jpg "KNGX NOTES FINS1613 [FINS1613] Comprehensive Notes") 1 [] Comprehensive Notes 1 2 TABLE OF CONTENTS Table of Contents... 2 1. Introduction & Time Value of Money... 3 2. Net Present Value & Interest Rates... 8 3. Valuation of Securities I... 19 4. Valuation

1 [] Comprehensive Notes 1 2 TABLE OF CONTENTS Table of Contents... 2 1. Introduction & Time Value of Money... 3 2. Net Present Value & Interest Rates... 8 3. Valuation of Securities I... 19 4. Valuation

Debt. Last modified KW

Debt The debt markets are far more complicated and filled with jargon than the equity markets. Fixed coupon bonds, loans and bills will be our focus in this course. It's important to be aware of all of

Debt The debt markets are far more complicated and filled with jargon than the equity markets. Fixed coupon bonds, loans and bills will be our focus in this course. It's important to be aware of all of

Part 2. Finite Mathematics. Chapter 3 Mathematics of Finance Chapter 4 System of Linear Equations; Matrices

Part 2 Finite Mathematics Chapter 3 Mathematics of Finance Chapter 4 System of Linear Equations; Matrices Chapter 3 Mathematics of Finance Section 1 Simple Interest Section 2 Compound and Continuous Compound

Part 2 Finite Mathematics Chapter 3 Mathematics of Finance Chapter 4 System of Linear Equations; Matrices Chapter 3 Mathematics of Finance Section 1 Simple Interest Section 2 Compound and Continuous Compound

Chapter 2 Time Value of Money

Chapter 2 Time Value of Money Learning Objectives After reading this chapter, students should be able to: Convert time value of money (TVM) problems from words to time lines. Explain the relationship between

Chapter 2 Time Value of Money Learning Objectives After reading this chapter, students should be able to: Convert time value of money (TVM) problems from words to time lines. Explain the relationship between

Lectures 2-3 Foundations of Finance

Lecture 2-3: Time Value of Money I. Reading II. Time Line III. Interest Rate: Discrete Compounding IV. Single Sums: Multiple Periods and Future Values V. Single Sums: Multiple Periods and Present Values

Lecture 2-3: Time Value of Money I. Reading II. Time Line III. Interest Rate: Discrete Compounding IV. Single Sums: Multiple Periods and Future Values V. Single Sums: Multiple Periods and Present Values

Fin 5413: Chapter 04 - Fixed Interest Rate Mortgage Loans Page 1 Solutions to Problems - Chapter 4 Fixed Interest Rate Mortgage Loans

Fin 5413: Chapter 04 - Fixed Interest Rate Mortgage Loans Page 1 Solutions to Problems - Chapter 4 Fixed Interest Rate Mortgage Loans Problem 4-1 A borrower makes a fully amortizing CPM mortgage loan.

Fin 5413: Chapter 04 - Fixed Interest Rate Mortgage Loans Page 1 Solutions to Problems - Chapter 4 Fixed Interest Rate Mortgage Loans Problem 4-1 A borrower makes a fully amortizing CPM mortgage loan.

SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT. 2) A bond is a security which typically offers a combination of two forms of payments:

A bond is a security which typically offers a combination of two forms of payments:") Solutions to Problem Set #: ) r =.06 or r =.8 SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT PVA[T 0, r.06] j 0 $8000 $8000 { {.06} t.06 &.06 (.06) 0} $8000(7.36009) $58,880.70 > $50,000 PVA[T 0, r.8] $8000(4.49409)

Solutions to Problem Set #: ) r =.06 or r =.8 SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT PVA[T 0, r.06] j 0 $8000 $8000 { {.06} t.06 &.06 (.06) 0} $8000(7.36009) $58,880.70 > $50,000 PVA[T 0, r.8] $8000(4.49409)

Lectures 1-2 Foundations of Finance

Lectures 1-2: Time Value of Money I. Reading A. RWJ Chapter 5. II. Time Line A. $1 received today is not the same as a $1 received in one period's time; the timing of a cash flow affects its value. B.

Lectures 1-2: Time Value of Money I. Reading A. RWJ Chapter 5. II. Time Line A. $1 received today is not the same as a $1 received in one period's time; the timing of a cash flow affects its value. B.

Lecture Notes 2. XII. Appendix & Additional Readings

Foundations of Finance: Concepts and Tools for Portfolio, Equity Valuation, Fixed Income, and Derivative Analyses Professor Alex Shapiro Lecture Notes 2 Concepts and Tools for Portfolio, Equity Valuation,

Foundations of Finance: Concepts and Tools for Portfolio, Equity Valuation, Fixed Income, and Derivative Analyses Professor Alex Shapiro Lecture Notes 2 Concepts and Tools for Portfolio, Equity Valuation,

MATH/STAT 2600, Theory of Interest FALL 2014 Toby Kenney

MATH/STAT 2600, Theory of Interest FALL 2014 Toby Kenney In Class Examples () September 11, 2014 1 / 75 Compound Interest Question 1 (a) Calculate the accumulated value on maturity of $5,000 invested for

MATH/STAT 2600, Theory of Interest FALL 2014 Toby Kenney In Class Examples () September 11, 2014 1 / 75 Compound Interest Question 1 (a) Calculate the accumulated value on maturity of $5,000 invested for

Our Own Problem & Solution Set-Up to Accompany Topic 6. Consider the five $200,000, 30-year amortization period mortgage loans described below.

Our Own Problem & Solution Set-Up to Accompany Topic 6 Notice the nature of the tradeoffs in this exercise: the borrower can buy down the interest rate, and thus make lower monthly payments, by giving

Our Own Problem & Solution Set-Up to Accompany Topic 6 Notice the nature of the tradeoffs in this exercise: the borrower can buy down the interest rate, and thus make lower monthly payments, by giving

Time Value of Money. PV of Multiple Cash Flows. Present Value & Discounting. Future Value & Compounding. PV of Multiple Cash Flows

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting. Konan Chan Financial Management, Time Value of Money

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 9, Mathematics of Finance from Applied Finite Mathematics by Rupinder Sekhon was developed by OpenStax College, licensed by Rice University,

Chapter 9, Mathematics of Finance from Applied Finite Mathematics by Rupinder Sekhon was developed by OpenStax College, licensed by Rice University, and is available on the Connexions website. It is used

Chapter 9, Mathematics of Finance from Applied Finite Mathematics by Rupinder Sekhon was developed by OpenStax College, licensed by Rice University, and is available on the Connexions website. It is used

Sequences, Series, and Limits; the Economics of Finance

CHAPTER 3 Sequences, Series, and Limits; the Economics of Finance If you have done A-level maths you will have studied Sequences and Series in particular Arithmetic and Geometric ones) before; if not you

CHAPTER 3 Sequences, Series, and Limits; the Economics of Finance If you have done A-level maths you will have studied Sequences and Series in particular Arithmetic and Geometric ones) before; if not you

Introduction to Corporate Finance, Fourth Edition. Chapter 5: Time Value of Money

Multiple Choice Questions 11. Section: 5.4 Annuities and Perpetuities B. Chapter 5: Time Value of Money 1 1 n (1 + k) 1 (1.15) PMT $,,(6.5933) $1, 519 k.15 N, I/Y15, PMT,, FV, CPT 1,519 14. Section: 5.7

Multiple Choice Questions 11. Section: 5.4 Annuities and Perpetuities B. Chapter 5: Time Value of Money 1 1 n (1 + k) 1 (1.15) PMT $,,(6.5933) $1, 519 k.15 N, I/Y15, PMT,, FV, CPT 1,519 14. Section: 5.7

Chapter 4: Managing Your Money Lecture notes Math 1030 Section D

Section D.1: Loan Basics Definition of loan principal For any loan, the principal is the amount of money owed at any particular time. Interest is charged on the loan principal. To pay off a loan, you must

Section D.1: Loan Basics Definition of loan principal For any loan, the principal is the amount of money owed at any particular time. Interest is charged on the loan principal. To pay off a loan, you must

Our Own Problems and Solutions to Accompany Topic 11

Our Own Problems and Solutions to Accompany Topic. A home buyer wants to borrow $240,000, and to repay the loan with monthly payments over 30 years. A. Compute the unchanging monthly payments for a standard

Our Own Problems and Solutions to Accompany Topic. A home buyer wants to borrow $240,000, and to repay the loan with monthly payments over 30 years. A. Compute the unchanging monthly payments for a standard

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 09 Future Value Welcome to the lecture series on Time

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 09 Future Value Welcome to the lecture series on Time

Chapter 2 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 2 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 2-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

Chapter 2 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 2-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

APPENDIX 3 TIME VALUE OF MONEY. Time Lines and Notation

1 APPENDIX 3 TIME VALUE OF MONEY The simplest tools in finance are often the most powerful. Present value is a concept that is intuitively appealing, simple to compute, and has a wide range of applications.

1 APPENDIX 3 TIME VALUE OF MONEY The simplest tools in finance are often the most powerful. Present value is a concept that is intuitively appealing, simple to compute, and has a wide range of applications.

FINA 1082 Financial Management

FINA 1082 Financial Management Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA257 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Lecture 1 Introduction

FINA 1082 Financial Management Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA257 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Lecture 1 Introduction

Math 1324 Finite Mathematics Chapter 4 Finance

Math 1324 Finite Mathematics Chapter 4 Finance Simple Interest: Situation where interest is calculated on the original principal only. A = P(1 + rt) where A is I = Prt Ex: A bank pays simple interest at

Math 1324 Finite Mathematics Chapter 4 Finance Simple Interest: Situation where interest is calculated on the original principal only. A = P(1 + rt) where A is I = Prt Ex: A bank pays simple interest at

Worksheet-2 Present Value Math I

What you will learn: Worksheet-2 Present Value Math I How to compute present and future values of single and annuity cash flows How to handle cash flow delays and combinations of cash flow streams How

What you will learn: Worksheet-2 Present Value Math I How to compute present and future values of single and annuity cash flows How to handle cash flow delays and combinations of cash flow streams How

NAME: CLASS PERIOD: Everything You Wanted to Know About Figuring Interest

NAME: CLASS PERIOD: Everything You Wanted to Know About Figuring Interest Credit isn t free. The price of credit is called the interest rate, and total interest paid is known as the finance charge. The

NAME: CLASS PERIOD: Everything You Wanted to Know About Figuring Interest Credit isn t free. The price of credit is called the interest rate, and total interest paid is known as the finance charge. The

The Time Value. The importance of money flows from it being a link between the present and the future. John Maynard Keynes

The Time Value of Money The importance of money flows from it being a link between the present and the future. John Maynard Keynes Get a Free $,000 Bond with Every Car Bought This Week! There is a car

The Time Value of Money The importance of money flows from it being a link between the present and the future. John Maynard Keynes Get a Free $,000 Bond with Every Car Bought This Week! There is a car

ENG120 MIDTERM Spring 2018

ENG120 MIDTERM Spring 2018 Name: (2pts) SID: (2pts) A. Any communication with other students during the exam (including showing, viewing or sharing any writing) is strictly prohibited. Any violation will

ENG120 MIDTERM Spring 2018 Name: (2pts) SID: (2pts) A. Any communication with other students during the exam (including showing, viewing or sharing any writing) is strictly prohibited. Any violation will

Math 1130 Exam 2 Review SHORT ANSWER. Write the word or phrase that best completes each statement or answers the question.

Math 1130 Exam 2 Review Provide an appropriate response. 1) Write the following in terms of ln x, ln(x - 3), and ln(x + 1): ln x 3 (x - 3)(x + 1) 2 1) 2) Write the following in terms of ln x, ln(x - 3),

Math 1130 Exam 2 Review Provide an appropriate response. 1) Write the following in terms of ln x, ln(x - 3), and ln(x + 1): ln x 3 (x - 3)(x + 1) 2 1) 2) Write the following in terms of ln x, ln(x - 3),

Nominal and Effective Interest Rates

Nominal and Effective Interest Rates 4.1 Introduction In all engineering economy relations developed thus far, the interest rate has been a constant, annual value. For a substantial percentage of the projects

Nominal and Effective Interest Rates 4.1 Introduction In all engineering economy relations developed thus far, the interest rate has been a constant, annual value. For a substantial percentage of the projects

CHAPTER 4. Suppose that you are walking through the student union one day and find yourself listening to some credit-card

CHAPTER 4 Banana Stock/Jupiter Images Present Value Suppose that you are walking through the student union one day and find yourself listening to some credit-card salesperson s pitch about how our card

CHAPTER 4 Banana Stock/Jupiter Images Present Value Suppose that you are walking through the student union one day and find yourself listening to some credit-card salesperson s pitch about how our card

ANNUITIES AND AMORTISATION WORKSHOP

OBJECTIVE: 1. Able to calculate the present value of annuities 2. Able to calculate the future value of annuities 3. Able to complete an amortisation schedule TARGET: QMI1500 and BNU1501, any other modules

OBJECTIVE: 1. Able to calculate the present value of annuities 2. Able to calculate the future value of annuities 3. Able to complete an amortisation schedule TARGET: QMI1500 and BNU1501, any other modules

ANSWERS TO CHAPTER QUESTIONS. The Time Value of Money. 1) Compounding is interest paid on principal and interest accumulated.

Compounding is interest paid on principal and interest accumulated.") ANSWERS TO CHAPTER QUESTIONS Chapter 2 The Time Value of Money 1) Compounding is interest paid on principal and interest accumulated. It is important because normal compounding over many years can result

ANSWERS TO CHAPTER QUESTIONS Chapter 2 The Time Value of Money 1) Compounding is interest paid on principal and interest accumulated. It is important because normal compounding over many years can result

FOUNDATIONS OF CORPORATE FINANCE

edition 2 FOUNDATIONS OF CORPORATE FINANCE Kent A. Hickman Gonzaga University Hugh O. Hunter San Diego State University John W. Byrd Fort Lewis College chapter 4 Time Is Money 00 After learning from his

edition 2 FOUNDATIONS OF CORPORATE FINANCE Kent A. Hickman Gonzaga University Hugh O. Hunter San Diego State University John W. Byrd Fort Lewis College chapter 4 Time Is Money 00 After learning from his

5.1 Simple and Compound Interest

5.1 Simple and Compound Interest Simple Interest Principal Rate Time Ex 1) Simple Interest Future Value Ex 2) Maturity Values Find the maturity value for each loan at simple interest. a. A loan of $2500

5.1 Simple and Compound Interest Simple Interest Principal Rate Time Ex 1) Simple Interest Future Value Ex 2) Maturity Values Find the maturity value for each loan at simple interest. a. A loan of $2500

MA 162: Finite Mathematics

MA 162: Finite Mathematics Fall 2014 Ray Kremer University of Kentucky December 1, 2014 Announcements: First financial math homework due tomorrow at 6pm. Exam scores are posted. More about this on Wednesday.

MA 162: Finite Mathematics Fall 2014 Ray Kremer University of Kentucky December 1, 2014 Announcements: First financial math homework due tomorrow at 6pm. Exam scores are posted. More about this on Wednesday.

CHAPTER 4 SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY APPLICATIONS. Copyright -The Institute of Chartered Accountants of India

CHAPTER 4 SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY APPLICATIONS SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY- APPLICATIONS LEARNING OBJECTIVES After studying this chapter students will be able

CHAPTER 4 SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY APPLICATIONS SIMPLE AND COMPOUND INTEREST INCLUDING ANNUITY- APPLICATIONS LEARNING OBJECTIVES After studying this chapter students will be able

Math 134 Tutorial 7, 2011: Financial Maths

Math 134 Tutorial 7, 2011: Financial Maths For each question, identify which of the formulae a to g applies. what you are asked to find, and what information you have been given. Final answers can be worked

Math 134 Tutorial 7, 2011: Financial Maths For each question, identify which of the formulae a to g applies. what you are asked to find, and what information you have been given. Final answers can be worked