Securitization and forfeiting

|

|

|

- Claribel O’Brien’

- 5 years ago

- Views:

Transcription

1 Securitization and forfeiting

2 SECURITIZATION MARKET

3 Securitization Securitization certainly has a black mark against it, but it is far too useful to be banished for good. Almost all financial innovations, from the humble mortgage to the joint-stock company, have had to re-establish their reputations after a bust at some point in their history. Society benefited from their eventual rehabilitation as it most probably will from the revival of securitization. It s Back, The Economist, 11 th Jan 2014

4 Problems of securitization The fundamental conflicts of interest between participants Falling lending standards Achievement of high leverage in sequencing schemes, repeated sequencing (synthetic bonds, CDO s) Use of complex legal, operational, financial structures Insufficient transparency Modeling errors Low investor readiness Lack of attention to proper due diligence

5 Reforms in securitization Increasing quality of lending standards Adaptation of duties of securitization intermediaries Application of simple, transparent, easy-to-use sequencing schemes Creation of secure, transparent and low-cost environmental claims (one of the most important goals) Use of securitization for the needs of the real economy Increasing the transparency of credit rating methodologies, reducing rating shopping, reducing the use of external credit ratings for supervisory purposes Adaptation of supervisory requirements for capital adequacy Development of long-term institutional investors Europe: standardization of documentation, harmonization of loan level data, insolvency procedures and taxation TVF SDN/15/01

6 SIMPLE SST (Simple-Standard-Transparent) Traditional securitization. Synthetic and repeated issues are not suitable. Active asset management is not allowed Whole-portfolio securitization or random selection (no cherry picking); principle of real money transfer; Insolvency Claw Backs Transferable monetary claims, i.e. originated from the usual activity of the originator; legally valid and enforceable; there is no dispute between the debtor and the creditor The overdue claims ration do not exceed 90 days; the sole source of satisfaction of the claim is not the sale of the debtor's property; the debtor is not insolvent, bankrupt or restructured. Derivative financial instruments - only for interest rate and currency risk insurance There has been at least one loan payment (except for credit cards)

7 SST (Simple-Standard-Transparent) STANDARDIZATION The initiator retains a certain risk tranche of [5%]. It is the duty of investors to verify the fulfillment of this requirement ("indirect approach") in addition to the direct requirement Coupon payments associated with well-known indices, internal triggering indices and formulas are not allowed Early redemption provisions for revolving portfolios due to: i) deterioration in the credit quality of the underlying assets, ii) lack of adequate assets, iii) insolvency of the originator or servant; Consecutive redemption is maintained; assets are not liquidated Replacement of administrator or other counterparty (swap, liquidity line) in case of insolvency Investor trustee and investor decision making Requirements for administrators

8 SST (Simple-Standard-Transparent) Transparency Access to the data and documentation required for evaluation The contracts clearly set out procedures for past due, default, insolvency, restructuring, abstentions, redundancies, etc. Clearly defined cash flow allocation (CF watefall) Compulsory verification of transferable claims (representative selection) carried out outside the credit rating agency due diligence scope Track records on similar insolvency indicators, including shocks, or at least 5 years. Loan-by-loan data Not less than a quarterly report on the portfolio status Credit risk Debtor's creditworthiness assessment 2014/17 / EU, 2008/48 / EC Concentration (<1%) The borrower's classification is in accordance with the requirements of the standardized approach according to the types of loans

9 SECURITIZATION

10 Basic principle Last Loss Lowest return Loan Loan Loan Loan Loan Loan Loan Loan Loan Loan Loan Loan Loan Assets Receivables SPV Liabilities Debt Equity AAA/ AA A BBB BB/B Not rated Borrower Bank Market First Loss Highest return Investors

--California Republic Bancorp ( CRB or Company ) (OTCBB: CRPB), a bank holding company for California Republic Bank ( Bank ), announced.")

11 Example of securitization Dec 19, 2014 California Republic Bancorp Announces Completion of $325 Million Prime Auto Loan Securitization Transaction IRVINE, Calif.--(BUSINESS WIRE)--California Republic Bancorp ( CRB or Company ) (OTCBB: CRPB), a bank holding company for California Republic Bank ( Bank ), announced.. The securitization structure included six note classes issued by the securitization trust created by the Bank as follows: Class Amount Coupon Credit Rating (sf) (1) A-1 $ 45,500, % A-1+ /R-1(high) A-2 $ 91,000, % AAA / AAA A-3 $ 78,000, % AAA / AAA A-4 $ 80,760, % AAA / AAA B $ 18,850, % A / A C $ 10,890, % BBB / BBB $ 325,000,000 (1) Credit Ratings from Standard & Poor's and DBRS, respectively

12 What can be securitized? Any monetary claims that can reasonably be predicted from cash flows "Collateral" - means receivables that are transferred to a special purpose entity collateral - do not mix with the traditional notion of this concept! Monetary claims do not necessarily result from financial transactions Nevertheless, loans are usually cash flow claims Housing loans (MBS, RMBS); other real estate loans (CMBS) Car loans (auto ABS), consumer ABSs, credit cards ABS, leasing ABS, loan research Small and medium-sized business loans (SME ABS) Whole business securitization (mining, transport, communications, copyrights, recovery of claims, etc.)

13 Advantages of securitization (I) Financing and Risk Transfer / Sharing Facility Diversifying funding sources, which is an alternative to bank financing domination (85% in Europe) Less risk is concentrated in the banking sector Monetary requirements are transformed into instruments that best fit the business climate and the needs of investors (maturity, interest rates, credit risk) The risk is allocated among investors according to their level of risk tolerance and ability to manage this risk Reduced borrowing costs for entities with lower creditworthiness Increased competition

14 Advantages of securitization (II) Capital mobility is increasing and risk management measures are expanding The credit market available to a wider range of investors increases the transparency of the market The asset class is attractive to investors due to returns, risks and correlations with other asset classes. The securitization of monetary claims increases the amount of financial assets that can be pledged as collateral in other transactions. The push for standardization of market instruments and processes, lower costs, and more efficient financial sector Securitization before the crisis has been successful for 30 years

15 Participants of securitization transaction Borrower Swap counterparty Credit Enhancer Liquidity Provider Rating Agency Originator Arranger Legal Advisor SPV Trustee Auditor Warehouse Lender Servicer Asset Manager Underwriter Master Servicer Custodian Investor

16 Rating agencies insights Many companies in emerging markets, including banks, non-bank lenders, leasing companies and other originators of securitizable assets, do not yet have access to securitization as a financing tool. This is due to a number of factors, including legal and regulatory infrastructures that are not yet conducive and asset pools that are not sufficiently developed However, it is rating agencies opinion that these will not be permanent barriers. Experience in Latin America, Asia and South Africa demonstrates that securitization can become a viable and beneficial financing tool in emerging markets Global experience suggests that the initial securitization can be a difficult process for asset originators Securitization is information intensive and requires a company be able to communicate clearly the nature of its assets and quantify asset performance in very specific ways

17 Due diligence scope (I) Collateral analysis (data on pool of assets): Delinquencies Defaults Recoveries Prepayments Identifying characteristics: diversification of obligors, including creditworthiness as defined by internal or external risk rating systems, geographical location and asset types Structure of receivables, including original amount and term, interest rate, outstanding balance and remaining term

18 Due diligence scope (II) Collateral analysis (data on pool of assets): Originator/Servicer review policies and procedures by which the assets are originated An operational track record and stable ownership structure. Managers with backgrounds and experience that demonstrate an understanding of their business area. A rational organisational structure that demonstrates depth of management skill. A comprehensive set of human resource and employee training practices. A suitable management information system ( MIS ) in key operational areas. A corporate strategy that is ingrained in current corporate practices and forms a basis for future growth. A track record of financial strength and a clear strategy for meeting financing needs. An understandable and realistic motivation for securitisation. Availability of back-up servicer

19 Due diligence scope (III) Legal Structure and Documentation Review transferability of assets; bankruptcy remoteness of the issuer; security interest over the assets; Taxation: transfer tax, stamp duty and withholding tax; Regulatory issues Set-off risk The legal ability to transfer assets and attached security to a third party. The requirement in some jurisdictions to notify underlying obligors in writing of the transfer of assets and to receive confirmation from the obligor The existence and reliability of special purpose vehicle ( SPV ), bankruptcy and foreclosure legislation. The potential impact of consumer and data protection laws. Sovereign Risk Evaluation Cash flow analysis and Financial Structure

20 Due diligence scope (IV) Credit Origination and Monitoring Procedures Clearly documented and implemented credit underwriting and origination policies and procedures and delegated authorities. Clear policies and procedures for valuation of collateral, accurate completion of registration of collateral and on-going monitoring of collateral interests. Standardised and comprehensive legal contracts and accuracy in completion of contract documentation. Comprehensive documentation management, including clear instructions on the documentation needed for a transaction and well organised filing systems. Vigorous monitoring, collection and problem asset policies and procedures. Concise and uniformly implemented provisioning and write-off policies. Comprehensive management information reporting systems that distribute key management information on a timely basis.

21 Due diligence scope (V) Operational Risk Procedures File structure, maintenance, storage methods and access controls structured to reduce operational risks Adequate computer systems to provide information to management on a real time basis Regular back-up and storage of key data. Access controls on key systems Internal and external audit policies, quality control procedures and anti-fraud measures Established and tested disaster recovery and emergency planning

22 Rating agencies stresses Securitization is a unique long-term financing tool that requires real commitment on the part of a company to develop internal capacity to support the process. Rating agencies will look for the originator to demonstrate: a solid performance track record for an asset pool; ability to service the assets concerned; ability in the case of revolving or future flow transactions to continue to originate the assets. Two key areas that in rating agencies experience cause challenges to securitization in emerging markets: credit originating and servicing policies and procedures availability of reliable and standardized data. In rating agencies experience, companies that bring their information systems inline with the data requirements of securitization find that on-going securitizations are more efficient To facilitate this process, rating agencies encourages originators and arrangers to approach the agency early in the development of a transaction. In this way, it may be able to aid the rating process by identifying potential barriers, allowing the originator time to address them.

23 Importance of track record Rating agencies generally looks for a minimum of three to five years of historical data before it can draw meaningful default, recovery and prepayment assumptions Ultimately, it is possible to structure a transaction with less data; however, this comes at a cost to the originator The less data available, the more conservative the agency s default probability and realized loss assumptions, potentially making it more difficult for transactions to achieve their target ratings The better the quality and quantity of performance data available, the better able the agency is to refine the credit enhancement levels, usually to the benefit of the originator

24 Some conclusions Securitization is an effective borrowing and risk transfer / sharing mechanism Securitization is a financial instrument established in mature markets and it is given a special high level political attention (EU Capital Market Union) VIPA projects are potentially very attractive for securitization Lithuania's experience, as in most of Eastern Europe and the Nordic countries, is limited A particularly beneficial environment for financing energy efficiency projects: the low interest rate environment and green initiatives There are background allowing to use of the securitization instrument in Lithuania although Lithuanian legal framework is not fully allow to use securitization in full extent

25 Examples

26 Examples

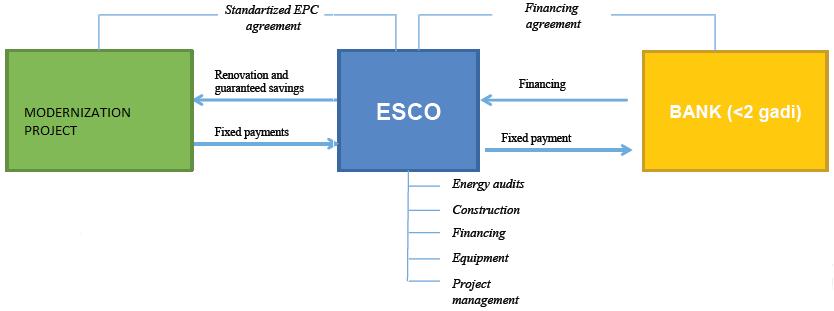

27 VIPA SECURITIZATION INITIATIVE

28 VIPA SECURITIZATION INITIATIVE The financial flows received for renovation of multi-apartment houses are a proper object for securitization VIPA may issue green bonds on the basis of financial lows of the multi-apartment house portfolios DNMF INVESTORS Receivables Reflows SPV Debt securities

29 VIPA SECURITIZATION INITIATIVE In 2015, VIPA considered a possibility to apply and implement with respect to the energy efficiency projects one of the most popular financial instrument securitization. In the beginning of 2016 the Company was continuing the negotiations with th strategic partner EBRD regarding mezzanine and the participation in the securitsation transaction. EBRD submitted a proposal for the transaction (Pre-financing Agreement and Feasibility study Terms of Reference). TRANSFER OF THE LOANS TO INVESTORS USING SECURITIZATION WOULD ALLOW: DECREASE THE return required by investors (discount rate) thus increasing the price of the financial assets being sold ATTRACT larger private capital resources Achieve larger multiplier of the programme Achieve higher leverage indicator Synergy for other programmes Regional leadership, strengthening of the institutional authority, preconditions for more constructive partnership

30 SECURITIZATION INITIATIVE Securitization initiative launched in the end of 2015 Discussion on securitization initiative resulted Extension of EBRD loan to MABR Project (EBRD signed agreement with MoF) on capital market legal framework harmonization VIPA has made assessment of the deal structure, environment, requirements and other conditions is performed VIPA self-assessment is performed (139 actions identified and under implementation) Steps taken to deal with challenges associated with handling personal data and improving administration of the loans

31 FORFEITING FACILITY

32 Forfeiting facility Source: LABEEF

33 THANK YOU FOR ATENTTION! CONTACTS Justinas Bucys Head of investment and development division Tel. (+370) Mobile (+370) j.bucys@vipa.lt Kristina Vaskelienė Deputy Chief Executive Officer Kristina Vaskelienė (8 5) k.vaskeliene@vipa.lt

34

Structured Finance. Securitisation in Emerging Markets: Preparing for the Rating Process. Special Report

Special Report Analysts Europe, Middle East & Africa Nick Eisinger +44 20 7417 4341 nick.eisinger@fitchratings.com Wasif Kazi +44 20 7417 4168 wasif.kazi@fitchratings.com Antonio Corbi +44 20 7417 4113

Special Report Analysts Europe, Middle East & Africa Nick Eisinger +44 20 7417 4341 nick.eisinger@fitchratings.com Wasif Kazi +44 20 7417 4168 wasif.kazi@fitchratings.com Antonio Corbi +44 20 7417 4113

Rating Methodology. Structured Finance. Global Credit-Linked Note and Repackaging Vehicle Rating Criteria. Updated May 2017

Rating Methodology Structured Finance Global Credit-Linked Note and Repackaging Vehicle Rating Criteria Related Research Updated May 2017 Each transaction will be accompanied with a transaction specific

Rating Methodology Structured Finance Global Credit-Linked Note and Repackaging Vehicle Rating Criteria Related Research Updated May 2017 Each transaction will be accompanied with a transaction specific

3 Decree of Národná banka Slovenska of 26 April 2011

3 Decree of Národná banka Slovenska of 26 April 2011 amending Decree No 4/2007 of Národná banka Slovenska on banks' own funds of financing and banks' capital requirements and on investment firms' own funds

3 Decree of Národná banka Slovenska of 26 April 2011 amending Decree No 4/2007 of Národná banka Slovenska on banks' own funds of financing and banks' capital requirements and on investment firms' own funds

CRR IV - Article 194 CRR IV Principles governing the eligibility of credit risk mitigation techniques legal opinion

CRR IV - Article 194 https://www.eba.europa.eu/regulation-and-policy/single-rulebook/interactive-single-rulebook/- /interactive-single-rulebook/article-id/1616 Must lending institutions always obtain a

CRR IV - Article 194 https://www.eba.europa.eu/regulation-and-policy/single-rulebook/interactive-single-rulebook/- /interactive-single-rulebook/article-id/1616 Must lending institutions always obtain a

In various tables, use of - indicates not meaningful or not applicable.

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

March 2017 For intermediaries and professional investors only. Not for further distribution.

Understanding Structured Credit March 2017 For intermediaries and professional investors only. Not for further distribution. Contents Investing in a rising interest rate environment 3 Understanding Structured

Understanding Structured Credit March 2017 For intermediaries and professional investors only. Not for further distribution. Contents Investing in a rising interest rate environment 3 Understanding Structured

Installment Receivables and Card Shopping Receivables

Last updated: June 2, 2014 Installment Receivables and Card Shopping Receivables 1. Outline of Underlying Assets Installment sales are defined under Installment Sales Act as payments over a period of not

Last updated: June 2, 2014 Installment Receivables and Card Shopping Receivables 1. Outline of Underlying Assets Installment sales are defined under Installment Sales Act as payments over a period of not

Information page Alternative Investment Fund Managers Directive Operating conditions Investment in securitisation positions

Information page Alternative Investment Fund Managers Directive Operating conditions Investment in securitisation positions Issued : 19 March 2013 Table of Contents 1. Introduction... 3 2. Definitions...

Information page Alternative Investment Fund Managers Directive Operating conditions Investment in securitisation positions Issued : 19 March 2013 Table of Contents 1. Introduction... 3 2. Definitions...

P2.T6. Credit Risk Measurement & Management. Moorad Choudhry, Structured Credit Products: Credit Derivatives & Synthetic Sercuritization, 2nd Edition

P2.T6. Credit Risk Measurement & Management Moorad Choudhry, Structured Credit Products: Credit Derivatives & Synthetic Sercuritization, 2nd Edition Bionic Turtle FRM Study Notes By Nicole Seaman and David

P2.T6. Credit Risk Measurement & Management Moorad Choudhry, Structured Credit Products: Credit Derivatives & Synthetic Sercuritization, 2nd Edition Bionic Turtle FRM Study Notes By Nicole Seaman and David

Basel II Pillar 3 disclosures 6M 09

Basel II Pillar 3 disclosures 6M 09 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group

Basel II Pillar 3 disclosures 6M 09 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group

P2.T6. Credit Risk Measurement & Management. Ashcroft & Schuermann, Understanding the Securitization of Subprime Mortgage Credit

P2.T6. Credit Risk Measurement & Management Ashcroft & Schuermann, Understanding the Securitization of Subprime Mortgage Credit Bionic Turtle FRM Study Notes Reading 48 By David Harper, CFA FRM CIPM www.bionicturtle.com

P2.T6. Credit Risk Measurement & Management Ashcroft & Schuermann, Understanding the Securitization of Subprime Mortgage Credit Bionic Turtle FRM Study Notes Reading 48 By David Harper, CFA FRM CIPM www.bionicturtle.com

GLOBAL CREDIT RATING CO. Rating Methodology. Structured Finance. Global Consumer ABS Rating Criteria Updated April 2014

GCR GLOBAL CREDIT RATING CO. Local Expertise Global Presence Rating Methodology Structured Finance Global Consumer ABS Rating Criteria Updated April 2014 Introduction GCR s Global Consumer ABS Rating Criteria

GCR GLOBAL CREDIT RATING CO. Local Expertise Global Presence Rating Methodology Structured Finance Global Consumer ABS Rating Criteria Updated April 2014 Introduction GCR s Global Consumer ABS Rating Criteria

COPYRIGHTED MATERIAL. Structured finance is a generic term referring to financings more complicated. Securitization Terminology CHAPTER 1

CHAPTER 1 Securitization Terminology Structured finance is a generic term referring to financings more complicated than traditional loans, generic bonds, and common equity. Relatively simple transactions

CHAPTER 1 Securitization Terminology Structured finance is a generic term referring to financings more complicated than traditional loans, generic bonds, and common equity. Relatively simple transactions

BANK OF ENGLAND MARKET NOTICE: EXTENDED COLLATERAL LONG-TERM REPO OPERATIONS

BANK OF ENGLAND MARKET NOTICE: EXTENDED COLLATERAL LONG-TERM REPO OPERATIONS 1 The Bank will continue to hold extended collateral three-month long-term repo open market operations (OMOs) weekly up to and

BANK OF ENGLAND MARKET NOTICE: EXTENDED COLLATERAL LONG-TERM REPO OPERATIONS 1 The Bank will continue to hold extended collateral three-month long-term repo open market operations (OMOs) weekly up to and

P2.T6. Credit Risk Measurement & Management. Ashcraft & Schuermann, Understanding the Securitization of Subprime Mortgage Credit

P2.T6. Credit Risk Measurement & Management Ashcraft & Schuermann, Understanding the Securitization of Subprime Mortgage Credit Bionic Turtle FRM Study Notes Sample By David Harper, CFA FRM CIPM and Deepa

P2.T6. Credit Risk Measurement & Management Ashcraft & Schuermann, Understanding the Securitization of Subprime Mortgage Credit Bionic Turtle FRM Study Notes Sample By David Harper, CFA FRM CIPM and Deepa

Basel Committee Proposes Simple, Transparent and Comparable Securitisation Framework for Short-Term Securitisations

July 27, 2017 Current Issues Relevant to Our Clients Basel Committee Proposes Simple, Transparent and Comparable Securitisation Framework for Short-Term Securitisations On July 6, 2017, the Basel Committee

July 27, 2017 Current Issues Relevant to Our Clients Basel Committee Proposes Simple, Transparent and Comparable Securitisation Framework for Short-Term Securitisations On July 6, 2017, the Basel Committee

Investment Insights What are asset-backed securities?

Investment Insights What are asset-backed securities? Asset-backed securities (ABS) are bonds secured by diversified pools of receivables across a variety of consumer or commercial assets. These assets

Investment Insights What are asset-backed securities? Asset-backed securities (ABS) are bonds secured by diversified pools of receivables across a variety of consumer or commercial assets. These assets

The South African Bank of Athens Limited. PILLAR 3 REGULATORY REPORT December 2016

The South African Bank of Athens Limited PILLAR 3 REGULATORY REPORT December 2016 CONTENTS Page Introduction 2 Capital management 3 Risk Management 7 Credit Risk 9 Market Risk 18 Interest Rate Risk 19

The South African Bank of Athens Limited PILLAR 3 REGULATORY REPORT December 2016 CONTENTS Page Introduction 2 Capital management 3 Risk Management 7 Credit Risk 9 Market Risk 18 Interest Rate Risk 19

Disclosure of Service Descriptions

Disclosure of Ancillary and business operations in the Kingdom of Saudi Arabia are principally conducted through Standard & Poor s Credit Market Services Europe Limited ( SPCMSE ). In accordance with the

Disclosure of Ancillary and business operations in the Kingdom of Saudi Arabia are principally conducted through Standard & Poor s Credit Market Services Europe Limited ( SPCMSE ). In accordance with the

Goldman Sachs Group UK (GSGUK) Pillar 3 Disclosures

Pillar 3 Disclosures") Goldman Sachs Group UK (GSGUK) Pillar 3 Disclosures For the year ended December 31, 2013 TABLE OF CONTENTS Page No. Introduction... 3 Regulatory Capital... 6 Risk-Weighted Assets... 7 Credit Risk... 7

Goldman Sachs Group UK (GSGUK) Pillar 3 Disclosures For the year ended December 31, 2013 TABLE OF CONTENTS Page No. Introduction... 3 Regulatory Capital... 6 Risk-Weighted Assets... 7 Credit Risk... 7

Future Flow Securitization

Last Updated: June 20, 2016 Future Flow Securitization 1. Future Flow Securitization In a future flow securitization, a company issues a debt instrument 1 whose repayment of principal and interest is secured

Last Updated: June 20, 2016 Future Flow Securitization 1. Future Flow Securitization In a future flow securitization, a company issues a debt instrument 1 whose repayment of principal and interest is secured

FBF RESPONSE TO EBA/DP/2014/02 DISCUSSION PAPER RELATIVE TO SIMPLE STANDARD AND TRANSPARENT SECURITISATIONS

20150114 FBF RESPONSE TO EBA/DP/2014/02 DISCUSSION PAPER RELATIVE TO SIMPLE STANDARD AND TRANSPARENT SECURITISATIONS The French Banking Federation (FBF) represents the interests of the banking industry

20150114 FBF RESPONSE TO EBA/DP/2014/02 DISCUSSION PAPER RELATIVE TO SIMPLE STANDARD AND TRANSPARENT SECURITISATIONS The French Banking Federation (FBF) represents the interests of the banking industry

Standard and Poor's RMBS Presale Report Paragon Mortgages (No. 4) PLC

PLC") Page 1 of 9 Publication Date: March 15, 2002 RMBS Presale Report Paragon Mortgages (No. 4) PLC 500 million mortgage-backed floating-rate notes James Cuby, London (44) 20-7826-3625 and Brian Kane, London

Page 1 of 9 Publication Date: March 15, 2002 RMBS Presale Report Paragon Mortgages (No. 4) PLC 500 million mortgage-backed floating-rate notes James Cuby, London (44) 20-7826-3625 and Brian Kane, London

EBA technical advice on Qualifying Securitisations. Public Hearing Event - London 26 June 2015

EBA technical advice on Qualifying Securitisations Public Hearing Event - London 26 June 2015 Mandate European Commission Call for Advice (Jan 2014): [ ] promoting the development of safe and stable securitisation

EBA technical advice on Qualifying Securitisations Public Hearing Event - London 26 June 2015 Mandate European Commission Call for Advice (Jan 2014): [ ] promoting the development of safe and stable securitisation

Guideline. Capital Adequacy Requirements (CAR) Structured Credit Products. Effective Date: November 2017 / January

Structured Credit Products. Effective Date: November 2017 / January") Guideline Subject: Capital Adequacy Requirements (CAR) Chapter 7 Effective Date: November 2017 / January 2018 1 The Capital Adequacy Requirements (CAR) for banks (including federal credit unions), bank

Guideline Subject: Capital Adequacy Requirements (CAR) Chapter 7 Effective Date: November 2017 / January 2018 1 The Capital Adequacy Requirements (CAR) for banks (including federal credit unions), bank

THE NAME IS BOND COVERED BOND

THE NAME IS BOND COVERED BOND Covered Bonds An Alternative Source of Financing Mortgage Lending December 4, 2012 Mira Tamboli Presentation Outline Introduction Covered Bond Basics Product Overview Issuer

THE NAME IS BOND COVERED BOND Covered Bonds An Alternative Source of Financing Mortgage Lending December 4, 2012 Mira Tamboli Presentation Outline Introduction Covered Bond Basics Product Overview Issuer

EUROPEAN COMMISSION SECURITISATION PROPOSALS

EUROPEAN COMMISSION SECURITISATION PROPOSALS THE COMMISSION'S OVERALL APPROACH Securitisation is an important channel for diversifying funding sources and allocating risk more efficiently within the EU

EUROPEAN COMMISSION SECURITISATION PROPOSALS THE COMMISSION'S OVERALL APPROACH Securitisation is an important channel for diversifying funding sources and allocating risk more efficiently within the EU

Margin Requirements for Non-Centrally Cleared Derivatives

Guideline Subject: Category: Sound Business and Financial Practices No: E-22 Effective Date: September 2016 Canada, as a member of the Basel Committee on Banking Supervision (BCBS), participated in the

Guideline Subject: Category: Sound Business and Financial Practices No: E-22 Effective Date: September 2016 Canada, as a member of the Basel Committee on Banking Supervision (BCBS), participated in the

Pierpont Securities LLC. pierpontsecurities.com 2012 Pierpont Securities, a member of FINRA and SIPC

Pierpont Securities LLC SECURITIZATION OVERVIEW SECURITIZATION Section I: Section II: Section III: Appendix: Definition Process Analysis Market Defined Terms P R O P R I E T A R Y A N D C O N F I D E N

Pierpont Securities LLC SECURITIZATION OVERVIEW SECURITIZATION Section I: Section II: Section III: Appendix: Definition Process Analysis Market Defined Terms P R O P R I E T A R Y A N D C O N F I D E N

Basel II Pillar 3 Disclosures Year ended 31 December 2009

DBS Group Holdings Ltd and its subsidiaries (the Group) have adopted Basel II as set out in the revised Monetary Authority of Singapore Notice to Banks No. 637 (Notice on Risk Based Capital Adequacy Requirements

DBS Group Holdings Ltd and its subsidiaries (the Group) have adopted Basel II as set out in the revised Monetary Authority of Singapore Notice to Banks No. 637 (Notice on Risk Based Capital Adequacy Requirements

M E M O R A N D U M. To: EBA Re: Comment on EBA proposed measurement of exposures to securitised assets By: Gordian Knot Date: August 2013

M E M O R A N D U M To: EBA Re: Comment on EBA proposed measurement of exposures to securitised assets By: Gordian Knot Date: August 2013 1 Purpose The EBA issued a paper in May 2013 proposing new ways

M E M O R A N D U M To: EBA Re: Comment on EBA proposed measurement of exposures to securitised assets By: Gordian Knot Date: August 2013 1 Purpose The EBA issued a paper in May 2013 proposing new ways

European Mortgage Securitisation: A Valuer s Guide

European Mortgage Securitisation: A Valuer s Guide November 2002 This guide is published by TEGoVA with the kind assistance of the Verband Deutscher Hypothekenbanken (Association of German Mortgage Banks).

European Mortgage Securitisation: A Valuer s Guide November 2002 This guide is published by TEGoVA with the kind assistance of the Verband Deutscher Hypothekenbanken (Association of German Mortgage Banks).

Asset Securitization. From Moody s Perspective. Presented by: Li Ma, VP Senior Analyst, Structured Finance Group Hong Kong. November 7, 2005 Shanghai

Asset Securitization From Moody s Perspective Presented by: Li Ma, VP Senior Analyst, Structured Finance Group Hong Kong November 7, 2005 Shanghai Agenda What is Securitization? What Can be Securitized?

Asset Securitization From Moody s Perspective Presented by: Li Ma, VP Senior Analyst, Structured Finance Group Hong Kong November 7, 2005 Shanghai Agenda What is Securitization? What Can be Securitized?

Taiwan Ratings. An Introduction to CDOs and Standard & Poor's Global CDO Ratings. Analysis. 1. What is a CDO? 2. Are CDOs similar to mutual funds?

An Introduction to CDOs and Standard & Poor's Global CDO Ratings Analysts: Thomas Upton, New York Standard & Poor's Ratings Services has been rating collateralized debt obligation (CDO) transactions since

An Introduction to CDOs and Standard & Poor's Global CDO Ratings Analysts: Thomas Upton, New York Standard & Poor's Ratings Services has been rating collateralized debt obligation (CDO) transactions since

Basel Committee on Banking Supervision

Basel Committee on Banking Supervision Standard Capital treatment for short-term simple, transparent and comparable securitisations May 2018 This publication is available on the BIS website (www.bis.org).

Basel Committee on Banking Supervision Standard Capital treatment for short-term simple, transparent and comparable securitisations May 2018 This publication is available on the BIS website (www.bis.org).

PRODUCT KEY FACTS Value Partners Greater China High Yield Income Fund

PRODUCT KEY FACTS Value Partners Greater China High Yield Income Fund Issuer: Value Partners Hong Kong Limited April 2017 This statement provides you with key information about the Value Partners Greater

PRODUCT KEY FACTS Value Partners Greater China High Yield Income Fund Issuer: Value Partners Hong Kong Limited April 2017 This statement provides you with key information about the Value Partners Greater

Funding Housing in the Bond Market. September 2016

Funding Housing in the Bond Market September 2016 Overview: ALCB Fund PART 1 Overview of ALCB Fund Target Impact: Capital Market Development Increased primary issuance and capacity Issuer Balance Sheet

Funding Housing in the Bond Market September 2016 Overview: ALCB Fund PART 1 Overview of ALCB Fund Target Impact: Capital Market Development Increased primary issuance and capacity Issuer Balance Sheet

Regulatory Capital Pillar 3 Disclosures

Regulatory Capital Pillar 3 Disclosures December 31, 2016 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply

Regulatory Capital Pillar 3 Disclosures December 31, 2016 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply

2016 RISK AND PILLAR III REPORT SECOND UPDATE AS OF JUNE 30, 2017

2016 RISK AND PILLAR III REPORT SECOND UPDATE AS OF JUNE 30, 2017 NATIXIS - 2016 Risk & Pillar III Report second update as of June 30, 2017 2 TABLE OF CONTENTS Update by chapter of the Risk and Pillar

2016 RISK AND PILLAR III REPORT SECOND UPDATE AS OF JUNE 30, 2017 NATIXIS - 2016 Risk & Pillar III Report second update as of June 30, 2017 2 TABLE OF CONTENTS Update by chapter of the Risk and Pillar

Margin Requirements for Non-Centrally Cleared Derivatives

Guideline Subject: Category: Sound Business and Financial Practices No: E-22 Effective Date: June 2017 Canada, as a member of the Basel Committee on Banking Supervision (BCBS), participated in the development

Guideline Subject: Category: Sound Business and Financial Practices No: E-22 Effective Date: June 2017 Canada, as a member of the Basel Committee on Banking Supervision (BCBS), participated in the development

Assessing Capital Markets Union

6 Assessing Capital Markets Union Quarterly Assessment by Paul Richards Summary It is too early to make an assessment of Capital Markets Union, but not too early to give a market view of the tests by which

6 Assessing Capital Markets Union Quarterly Assessment by Paul Richards Summary It is too early to make an assessment of Capital Markets Union, but not too early to give a market view of the tests by which

IFMR CAPITAL CONNECTING MICROFINANCE INSTITUTIONS TO CAPITAL MARKETS

Introduction to Securitisation for MFIs IFMR CAPITAL CONNECTING MICROFINANCE INSTITUTIONS TO CAPITAL MARKETS About IFMR Capital IFMR Capital is a non-banking finance company based in Chennai, whose mission

Introduction to Securitisation for MFIs IFMR CAPITAL CONNECTING MICROFINANCE INSTITUTIONS TO CAPITAL MARKETS About IFMR Capital IFMR Capital is a non-banking finance company based in Chennai, whose mission

Basel II Pillar 3 disclosures

Basel II Pillar 3 disclosures 6M10 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG and its consolidated

Basel II Pillar 3 disclosures 6M10 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG and its consolidated

Securitisation: Current concerns and long-term value

Securitisation: Current Concerns and Long-term Value Securitisation: Current concerns and long-term value Paul Lejot, Douglas Arner & Lotte Schou-Zibell Manila, 1 February 2008 Asian Institute of International

Securitisation: Current Concerns and Long-term Value Securitisation: Current concerns and long-term value Paul Lejot, Douglas Arner & Lotte Schou-Zibell Manila, 1 February 2008 Asian Institute of International

Regulatory Capital Pillar 3 Disclosures

Regulatory Capital Pillar 3 Disclosures June 30, 2014 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply 3 Capital

Regulatory Capital Pillar 3 Disclosures June 30, 2014 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply 3 Capital

Repackaged Financial Instruments

Last Updated: December 3, 2012 Repackaged Financial Instruments 1. Repackaged Financial Instruments A repackaged note means the note newly repackaged using derivatives such as currency and interest rate

Last Updated: December 3, 2012 Repackaged Financial Instruments 1. Repackaged Financial Instruments A repackaged note means the note newly repackaged using derivatives such as currency and interest rate

Publication Date: Jan. 29, 2005 CLO Postsale Report

Publication Date: Jan. 29, 2005 CLO Postsale Report GC FTPYME PASTOR 1, Fondo de Titulización de Activos 225 million floating-rate notes Analysts: Patricia Pérez Arias, London (44) 20-7826-3840 and José

Publication Date: Jan. 29, 2005 CLO Postsale Report GC FTPYME PASTOR 1, Fondo de Titulización de Activos 225 million floating-rate notes Analysts: Patricia Pérez Arias, London (44) 20-7826-3840 and José

PRIME COLLATERALISED SECURITIES

PRIME COLLATERALISED SECURITIES RISK TRANSFER SECURITISATION ELIGIBILITY CRITERIA Version 2 July 2018 July 2018 CONTENTS ELIGIBILITY CRITERIA Clause Page Common Eligibility Criteria 1 (a) Balance Sheet

PRIME COLLATERALISED SECURITIES RISK TRANSFER SECURITISATION ELIGIBILITY CRITERIA Version 2 July 2018 July 2018 CONTENTS ELIGIBILITY CRITERIA Clause Page Common Eligibility Criteria 1 (a) Balance Sheet

Securitized Products. Standardized Information Reporting Package (SIRP) Guidebook

Guidebook") Securitized Products Standardized Information Reporting Package (SIRP) Guidebook Prepared: July 2012 Revised: September 2015 Japan Securities Dealers Association Working Group on Securitized Products 1

Securitized Products Standardized Information Reporting Package (SIRP) Guidebook Prepared: July 2012 Revised: September 2015 Japan Securities Dealers Association Working Group on Securitized Products 1

PRODUCT KEY FACTS Value Partners Greater China High Yield Income Fund

PRODUCT KEY FACTS Value Partners Greater China High Yield Income Fund Issuer: Value Partners Hong Kong Limited 15 November 2013 This statement provides you with key information about the Value Partners

PRODUCT KEY FACTS Value Partners Greater China High Yield Income Fund Issuer: Value Partners Hong Kong Limited 15 November 2013 This statement provides you with key information about the Value Partners

Securitisation Framework

Securitisation Framework Recent regulatory changes and market trend Zeshan Choudhry June 2011 Contents 1 Introduction and Background 2 Overview of Common Practice 3 Review of Securitisation Framework under

Securitisation Framework Recent regulatory changes and market trend Zeshan Choudhry June 2011 Contents 1 Introduction and Background 2 Overview of Common Practice 3 Review of Securitisation Framework under

Term Asset-Backed Securities Loan Facility: Terms and Conditions 1. Printer version Changes from October November 130 Terms and Conditions

Term Asset-Backed Securities Loan Facility: Terms and Conditions 1 Effective November July 21, 201013, 2009 Printer version Changes from October November 130 Terms and Conditions General Terms and Conditions

Term Asset-Backed Securities Loan Facility: Terms and Conditions 1 Effective November July 21, 201013, 2009 Printer version Changes from October November 130 Terms and Conditions General Terms and Conditions

Basel III Pillar 3 Disclosures Report. For the Quarterly Period Ended December 31, 2015

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended December 31, 2015 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy...

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended December 31, 2015 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy...

Regulatory Capital Pillar 3 Disclosures

Regulatory Capital Pillar 3 Disclosures June 30, 2015 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply 3 Capital

Regulatory Capital Pillar 3 Disclosures June 30, 2015 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply 3 Capital

Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One Is Right for You?

The following information and opinions are provided courtesy of Wells Fargo Bank, N.A. Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One Is Right for You? 1 2 2 3 3 4 Commercial real

The following information and opinions are provided courtesy of Wells Fargo Bank, N.A. Recourse vs. Nonrecourse: Commercial Real Estate Financing Which One Is Right for You? 1 2 2 3 3 4 Commercial real

Erste Bank der oesterreichischen Sparkassen AG

International Structured Finance Europe, Middle East, Africa Pre-Sale Report Erste Bank der oesterreichischen Sparkassen AG Covered Bonds / Austria This pre-sale report addresses the structure and characteristics

International Structured Finance Europe, Middle East, Africa Pre-Sale Report Erste Bank der oesterreichischen Sparkassen AG Covered Bonds / Austria This pre-sale report addresses the structure and characteristics

PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. December 2012 PILLAR 3 DISCLOSURES For the period ended June 30, 2014 TABLE OF CONTENTS Page No. Index of Tables 2 Introduction 3 Regulatory Capital 7 Capital Structure 8

The Goldman Sachs Group, Inc. December 2012 PILLAR 3 DISCLOSURES For the period ended June 30, 2014 TABLE OF CONTENTS Page No. Index of Tables 2 Introduction 3 Regulatory Capital 7 Capital Structure 8

Rating Methodology. Structured Finance and Securitisation. Global Master Structured Finance Rating Criteria Updated February 2016

GLOBAL CREDIT RATING CO. Rating Methodology Structured Finance and Securitisation Global Master Structured Finance Rating Criteria Updated February 2016 Related Methodologies Global Asset Backed Commercial

GLOBAL CREDIT RATING CO. Rating Methodology Structured Finance and Securitisation Global Master Structured Finance Rating Criteria Updated February 2016 Related Methodologies Global Asset Backed Commercial

Having regard to the Treaty on the Functioning of the European Union, and in particular Article 114 thereof,

28.12.2017 Official Journal of the European Union L 347/35 REGULATION (EU) 2017/2402 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 12 December 2017 laying down a general framework for securitisation

28.12.2017 Official Journal of the European Union L 347/35 REGULATION (EU) 2017/2402 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 12 December 2017 laying down a general framework for securitisation

EBF response to EBA consultation on homogeneity of underlying assets

15/03/2018 EBF response to EBA consultation on homogeneity of underlying assets Key points: Well established securitisations considered as high-quality under current market practices must be preserved

15/03/2018 EBF response to EBA consultation on homogeneity of underlying assets Key points: Well established securitisations considered as high-quality under current market practices must be preserved

Structured Finance. South Africa/ABCP Special Report

South Africa/ABCP Special Report Analysts David Kubayi, Johannesburg +27 11 380 0905 david.kubayi@fitchratings.com Joshua Cohen, Johannesburg +27 11 380 0907 joshua.cohen@fitchratings.com Rabia Parker,

South Africa/ABCP Special Report Analysts David Kubayi, Johannesburg +27 11 380 0905 david.kubayi@fitchratings.com Joshua Cohen, Johannesburg +27 11 380 0907 joshua.cohen@fitchratings.com Rabia Parker,

PILLAR 3 DISCLOSURES

. The Goldman Sachs Group, Inc. December 2012 PILLAR 3 DISCLOSURES For the period ended December 31, 2014 TABLE OF CONTENTS Page No. Index of Tables 2 Introduction 3 Regulatory Capital 7 Capital Structure

. The Goldman Sachs Group, Inc. December 2012 PILLAR 3 DISCLOSURES For the period ended December 31, 2014 TABLE OF CONTENTS Page No. Index of Tables 2 Introduction 3 Regulatory Capital 7 Capital Structure

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD ( D)

BERHAD ( D)") Company No. 911666-D INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (Incorporated in Malaysia) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) PILLAR 3 DISCLOSURE

Company No. 911666-D INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (Incorporated in Malaysia) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) PILLAR 3 DISCLOSURE

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD ( D)

BERHAD ( D)") Company No. 911666 D INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (Incorporated in Malaysia) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) PILLAR 3 DISCLOSURE

Company No. 911666 D INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (Incorporated in Malaysia) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) PILLAR 3 DISCLOSURE

The Securitization Process/1

The Securitization Process/1 Asset-Backed Securities The Securitization Process Prof. Ian Giddy Stern School of Business New York University Asset-Backed Securities The basic idea What s needed? The technique

The Securitization Process/1 Asset-Backed Securities The Securitization Process Prof. Ian Giddy Stern School of Business New York University Asset-Backed Securities The basic idea What s needed? The technique

Structured Finance.. Rating Methodology..

Structured Finance.. Rating Methodology.. www.arcratings.com GLOBAL CRITERIA FOR RATING TRADE RECEIVABLES ECEIVABLES-BACKED ACKED SECURITISATIONS February 6, 2015 I. INTRODUCTION This Criteria (the Criteria

Structured Finance.. Rating Methodology.. www.arcratings.com GLOBAL CRITERIA FOR RATING TRADE RECEIVABLES ECEIVABLES-BACKED ACKED SECURITISATIONS February 6, 2015 I. INTRODUCTION This Criteria (the Criteria

Transaction Update: BRFkredit A/S (Capital Center E Mortgage Covered Bonds)

") Transaction Update: BRFkredit A/S (Capital Center E Mortgage Covered Bonds) SDOs (Særligt Dækkede Obligationer) Primary Credit Analyst: Ioan Isopel, Frankfurt (49) 69-33-999-306; ioan.isopel@standardandpoors.com

Transaction Update: BRFkredit A/S (Capital Center E Mortgage Covered Bonds) SDOs (Særligt Dækkede Obligationer) Primary Credit Analyst: Ioan Isopel, Frankfurt (49) 69-33-999-306; ioan.isopel@standardandpoors.com

Maiden Lane LLC (A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York)

") (A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York) Consolidated Financial Statements for the Period March 14, 2008 to December 31, 2008, and Independent Auditors Report MAIDEN

(A Special Purpose Vehicle Consolidated by the Federal Reserve Bank of New York) Consolidated Financial Statements for the Period March 14, 2008 to December 31, 2008, and Independent Auditors Report MAIDEN

MANAGING RISK IN EMERGING MARKETS OUR CORE BUSINESS FISCAL YEAR 2013

MANAGING RISK IN EMERGING MARKETS OUR CORE BUSINESS FISCAL YEAR 2013 PROVEN TRACK RECORD 2 IFC IN NUMBERS 57 $63.2bn $49.6bn $13.6bn $24.9bn $18.3bn $6.5bn $1bn Years of profitable investments in emerging

MANAGING RISK IN EMERGING MARKETS OUR CORE BUSINESS FISCAL YEAR 2013 PROVEN TRACK RECORD 2 IFC IN NUMBERS 57 $63.2bn $49.6bn $13.6bn $24.9bn $18.3bn $6.5bn $1bn Years of profitable investments in emerging

Credit Risk Retention Under the Dodd-Frank Act what do EU firms need to know?

CLIENT BRIEFING Credit Risk Retention in the U.S. Credit Risk Retention Under the Dodd-Frank Act what do EU firms need to know? This client briefing gives an overview of the proposed U.S. risk retention

CLIENT BRIEFING Credit Risk Retention in the U.S. Credit Risk Retention Under the Dodd-Frank Act what do EU firms need to know? This client briefing gives an overview of the proposed U.S. risk retention

Credit Rating Agencies ESMA s investigation into structured finance ratings

Credit Rating Agencies ESMA s investigation into structured finance ratings 16 December 2014 ESMA/2014/1524 Date: 16 December 2014 ESMA/2014/1524 Table of Contents 1 Executive Summary... 4 2 Who should

Credit Rating Agencies ESMA s investigation into structured finance ratings 16 December 2014 ESMA/2014/1524 Date: 16 December 2014 ESMA/2014/1524 Table of Contents 1 Executive Summary... 4 2 Who should

ABS Eligibility Assessment Form

ABS Eligibility Assessment Form To start the process of the eligibility assessment of an asset-backed security (ABS), a completed application form and all related documents must be submitted to De Nederlandsche

ABS Eligibility Assessment Form To start the process of the eligibility assessment of an asset-backed security (ABS), a completed application form and all related documents must be submitted to De Nederlandsche

Mechanics and Benefits of Securitization

Mechanics and Benefits of Securitization Executive Summary Securitization is not a new concept. In its most basic form, securitization dates back to the late 18th century. The first modern residential

Mechanics and Benefits of Securitization Executive Summary Securitization is not a new concept. In its most basic form, securitization dates back to the late 18th century. The first modern residential

Puerto Rico GNMA & U.S. Government Target Maturity Fund, Inc.

OFFERING CIRCULAR Puerto Rico GNMA & U.S. Government Target Maturity Fund, Inc. Tax-Free Secured Obligations The Tax-Free Secured Obligations (the "Notes") are offered by Puerto Rico GNMA & U.S. Government

OFFERING CIRCULAR Puerto Rico GNMA & U.S. Government Target Maturity Fund, Inc. Tax-Free Secured Obligations The Tax-Free Secured Obligations (the "Notes") are offered by Puerto Rico GNMA & U.S. Government

PRODUCT KEY FACTS. BlackRock Global Funds US Government Mortgage Fund. April 2018

PRODUCT KEY FACTS BlackRock Global Funds US Government Mortgage Fund April 2018 BlackRock Asset Management North Asia Limited Quick facts Fund Manager: Investment Adviser: Depositary: Ongoing charges over

PRODUCT KEY FACTS BlackRock Global Funds US Government Mortgage Fund April 2018 BlackRock Asset Management North Asia Limited Quick facts Fund Manager: Investment Adviser: Depositary: Ongoing charges over

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD ( D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II)

BERHAD ( D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II)") INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) Pillar 3 Disclosure for Financial Year Ended 31 December 2015 Table of Contents 1.0 OVERVIEW... 1 2.0 CAPITAL

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) Pillar 3 Disclosure for Financial Year Ended 31 December 2015 Table of Contents 1.0 OVERVIEW... 1 2.0 CAPITAL

Hypo Real Estate Bank International AG Million Floating-Rate Amortizing Credit-Linked Notes (ESTATE UK-3)

") Publication Date: Feb. 8, 2007 CMBS Presale Report Hypo Real Estate Bank International AG 113.68 Million Floating-Rate Amortizing Credit-Linked Notes (ESTATE UK-3) Analyst: Jason Sunderland, London (44)

Publication Date: Feb. 8, 2007 CMBS Presale Report Hypo Real Estate Bank International AG 113.68 Million Floating-Rate Amortizing Credit-Linked Notes (ESTATE UK-3) Analyst: Jason Sunderland, London (44)

Methodology. Derivative Criteria for European Structured Finance Transactions

Methodology Derivative Criteria for European Structured Finance Transactions october 2014 CONTACT INFORMATION Claire J. Mezzanotte Group Managing Director Head of Global Structured Finance Tel. +44 207

Methodology Derivative Criteria for European Structured Finance Transactions october 2014 CONTACT INFORMATION Claire J. Mezzanotte Group Managing Director Head of Global Structured Finance Tel. +44 207

Basel II Pillar 3 Disclosures

DBS GROUP HOLDINGS LTD & ITS SUBSIDIARIES DBS Annual Report 2008 123 DBS Group Holdings Ltd and its subsidiaries (the Group) have adopted Basel II as set out in the revised Monetary Authority of Singapore

DBS GROUP HOLDINGS LTD & ITS SUBSIDIARIES DBS Annual Report 2008 123 DBS Group Holdings Ltd and its subsidiaries (the Group) have adopted Basel II as set out in the revised Monetary Authority of Singapore

Prime Trust Conduit Overview Report, November 2016

Prime Trust Conduit Overview Report, November 2016 This report was produced on November 14, 2016 and, unless stated otherwise herein, the information in this report is current as of that date. For a copy

Prime Trust Conduit Overview Report, November 2016 This report was produced on November 14, 2016 and, unless stated otherwise herein, the information in this report is current as of that date. For a copy

Item Level Explanation Comments Notes. expression acceptable. Include condition precedent for calculation

Common Information Item List Appendix RMBS (Securitized Products Backed by Japanese Housing Loans) June 5, 2008 Item Level Explanation Comments Notes I Information on Specification of the Product and Outline

Common Information Item List Appendix RMBS (Securitized Products Backed by Japanese Housing Loans) June 5, 2008 Item Level Explanation Comments Notes I Information on Specification of the Product and Outline

Technical Cooperation s Contribution to Transition in Early Transition Countries: Evidence from Micro, Small and Medium Enterprises Lending 1

WORKING DRAFT Technical Cooperation s Contribution to Transition in Early Transition Countries: Evidence from Micro, Small and Medium Enterprises Lending 1 Office of Chief Economist, the European Bank

WORKING DRAFT Technical Cooperation s Contribution to Transition in Early Transition Countries: Evidence from Micro, Small and Medium Enterprises Lending 1 Office of Chief Economist, the European Bank

Asset Securitisation in East Asia

East Asian Finance-Road to Robust Markets Asset Securitisation in East Asia Ismail Dalla Hong Kong June 22-23, 06 Views expressed in this presentation do not represent official views of the World Bank

East Asian Finance-Road to Robust Markets Asset Securitisation in East Asia Ismail Dalla Hong Kong June 22-23, 06 Views expressed in this presentation do not represent official views of the World Bank

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD ( D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II)

BERHAD ( D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II)") INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) Pillar 3 Disclosure for the Half-Year Ended 30 June 2016 Table of Contents 1.0 OVERVIEW... 1 2.0 CAPITAL

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) Pillar 3 Disclosure for the Half-Year Ended 30 June 2016 Table of Contents 1.0 OVERVIEW... 1 2.0 CAPITAL

CDOs October 19, 2006

2006 Annual Meeting & Education Conference New York, NY CDOs Ozgur K. Bayazitoglu AIG Global Investment Group Keith M. Ashton TIAA-CREF Michael Lamont Deutsche Bank Securities Inc. Vicki E. Marmorstein

2006 Annual Meeting & Education Conference New York, NY CDOs Ozgur K. Bayazitoglu AIG Global Investment Group Keith M. Ashton TIAA-CREF Michael Lamont Deutsche Bank Securities Inc. Vicki E. Marmorstein

Information Memorandum. Westpac Securitisation Trust Series WST Trust. Mortgage Backed Floating Rate Notes. A$2,300,000,000 Class A Notes

Westpac Securitisation Trust Series 2014-1 WST Trust Mortgage Backed Floating Rate Notes A$2,300,000,000 Class A Notes rated AAAsf by Standard and Poor's (Australia) Pty Limited and Aaa(sf) by Moody's

Westpac Securitisation Trust Series 2014-1 WST Trust Mortgage Backed Floating Rate Notes A$2,300,000,000 Class A Notes rated AAAsf by Standard and Poor's (Australia) Pty Limited and Aaa(sf) by Moody's

First Synthetic Securitization of. SME Loans in CEE. Lessons Learned. Worldbank Conference. Bratislava, May

Bratislava, May 16 2008 Worldbank Conference Page 1 First Synthetic Securitization of SME Loans in CEE Lessons Learned May 2008 Why securitisation? The profitability of CEE banking business frequently

Bratislava, May 16 2008 Worldbank Conference Page 1 First Synthetic Securitization of SME Loans in CEE Lessons Learned May 2008 Why securitisation? The profitability of CEE banking business frequently

General Inspectorate of Banking Supervision

NATIONAL BANK OF POLAND COMMISSION FOR BANKING SUPERVISION General Inspectorate of Banking Supervision Resolution no. 6/2007 of the Commission for Banking Supervision of 13 March 2007 on detailed principles

NATIONAL BANK OF POLAND COMMISSION FOR BANKING SUPERVISION General Inspectorate of Banking Supervision Resolution no. 6/2007 of the Commission for Banking Supervision of 13 March 2007 on detailed principles

Finland. Country Q&A Finland. Antti Niemi and Kimmo Mettälä, LMR Attorneys Ltd. Country Q&A MARKET AND LEGAL REGIME REASONS FOR DOING A SECURITISATION

Finland Finland Antti Niemi and Kimmo Mettälä, LMR Attorneys Ltd www.practicallaw.com/ 9-380-9565 MARKET AND LEGAL REGIME 1. Please give a brief overview of the securitisation market in your jurisdiction.

Finland Finland Antti Niemi and Kimmo Mettälä, LMR Attorneys Ltd www.practicallaw.com/ 9-380-9565 MARKET AND LEGAL REGIME 1. Please give a brief overview of the securitisation market in your jurisdiction.

Explanatory notes to the Registration form for securitisation-spvs (Special Purpose Vehicles)

") Explanatory notes to the Registration form for securitisation-spvs (Special Purpose Vehicles) Version 3.0 1 December 2014 De Nederlandsche Bank NV, 2014 Contents INTRODUCTION... 2 CONCEPTS AND DEFINITIONS...

Explanatory notes to the Registration form for securitisation-spvs (Special Purpose Vehicles) Version 3.0 1 December 2014 De Nederlandsche Bank NV, 2014 Contents INTRODUCTION... 2 CONCEPTS AND DEFINITIONS...

Housing Finance in South Asia, Jakarta May 27 29, 2009 R V VERMA NATIONAL HOUSING BANK INDIA

Liquidity and Funding Issues including Secondary Mortgage gg Facilities Housing Finance in South Asia, Jakarta May 27 29, 2009 R V VERMA NATIONAL HOUSING BANK INDIA Contents I. Goba Global Developments

Liquidity and Funding Issues including Secondary Mortgage gg Facilities Housing Finance in South Asia, Jakarta May 27 29, 2009 R V VERMA NATIONAL HOUSING BANK INDIA Contents I. Goba Global Developments

Assets Eligible as Collateral under the Bank of Canada s Standing Liquidity Facility

Assets Eligible as Collateral under the Bank of Canada s Standing Liquidity Facility The Bank of Canada, through its Standing Liquidity Facility (SLF), provides access to liquidity to those institutions

Assets Eligible as Collateral under the Bank of Canada s Standing Liquidity Facility The Bank of Canada, through its Standing Liquidity Facility (SLF), provides access to liquidity to those institutions

Lease Receivables. 1. The Outline of the General Scheme (in case of the Entrustment Method)

") Lease Receivables Last Updated: May 11, 2007 1. The Outline of the General Scheme (in case of the Entrustment Method) (1) A lease company being the originator assigns its leasing receivables from many

Lease Receivables Last Updated: May 11, 2007 1. The Outline of the General Scheme (in case of the Entrustment Method) (1) A lease company being the originator assigns its leasing receivables from many

Quantitative and Qualitative Disclosures about Market Risk.

Item 7A. Quantitative and Qualitative Disclosures about Market Risk. Risk Management. Risk Management Policy and Control Structure. Risk is an inherent part of the Company s business and activities. The

Item 7A. Quantitative and Qualitative Disclosures about Market Risk. Risk Management. Risk Management Policy and Control Structure. Risk is an inherent part of the Company s business and activities. The

PILLAR 3 DISCLOSURE CITIBANK BERHAD

CITIBANK BERHAD PILLAR 3 DISCLOSURE CONTENTS Introduction Capital Adequacy Capital Structure Risk Management Credit Risk Securitization Market Risk Operational Risk Equities Interest Rate Risk/ Rate of

CITIBANK BERHAD PILLAR 3 DISCLOSURE CONTENTS Introduction Capital Adequacy Capital Structure Risk Management Credit Risk Securitization Market Risk Operational Risk Equities Interest Rate Risk/ Rate of

Assessing Credit Risk

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

Rating Methodology. Structured Finance. Global Trade Receivables Securitisation Rating Criteria. Updated May 2017

Rating Methodology Structured Finance Global Trade Receivables Securitisation Rating Criteria Updated May 2017 Related Methodology The Criteria should be read in conjunction with GCR s Global Structured

Rating Methodology Structured Finance Global Trade Receivables Securitisation Rating Criteria Updated May 2017 Related Methodology The Criteria should be read in conjunction with GCR s Global Structured

Rating Methodology. Structured Finance and Securitisation. Global Master Structured Finance Rating Criteria Updated June 2018

GLOBAL CREDIT RATING CO. Methodology Structured Finance and Securitisation Global Master Structured Finance Criteria Updated June 2018 Related Methodologies Global Asset Backed Commercial Paper Criteria,

GLOBAL CREDIT RATING CO. Methodology Structured Finance and Securitisation Global Master Structured Finance Criteria Updated June 2018 Related Methodologies Global Asset Backed Commercial Paper Criteria,

Community Trust Company Basel III Pillar 3 Disclosures December 31, 2017

Community Trust Company Basel III Pillar 3 Disclosures December 31, 2017 Basel III Pillar 3 Disclosures Page 1 of 18 Contents Part 1 - Scope of Application... 3 Basis of preparation... 3 Significant subsidiaries...

Community Trust Company Basel III Pillar 3 Disclosures December 31, 2017 Basel III Pillar 3 Disclosures Page 1 of 18 Contents Part 1 - Scope of Application... 3 Basis of preparation... 3 Significant subsidiaries...

Nissan Auto Lease Trust 2007-A

Prospectus Supplement NALT 2007-A (To Prospectus Dated July 24, 2007) Prospectus Supplement $1,090,079,000 Nissan Auto Lease Trust 2007-A Issuing Entity Nissan Auto Leasing LLC II Depositor Nissan Motor

Prospectus Supplement NALT 2007-A (To Prospectus Dated July 24, 2007) Prospectus Supplement $1,090,079,000 Nissan Auto Lease Trust 2007-A Issuing Entity Nissan Auto Leasing LLC II Depositor Nissan Motor