Reykjavík, 19. december Recommendation on countercyclical capital buffer

|

|

|

- Marjory Floyd

- 5 years ago

- Views:

Transcription

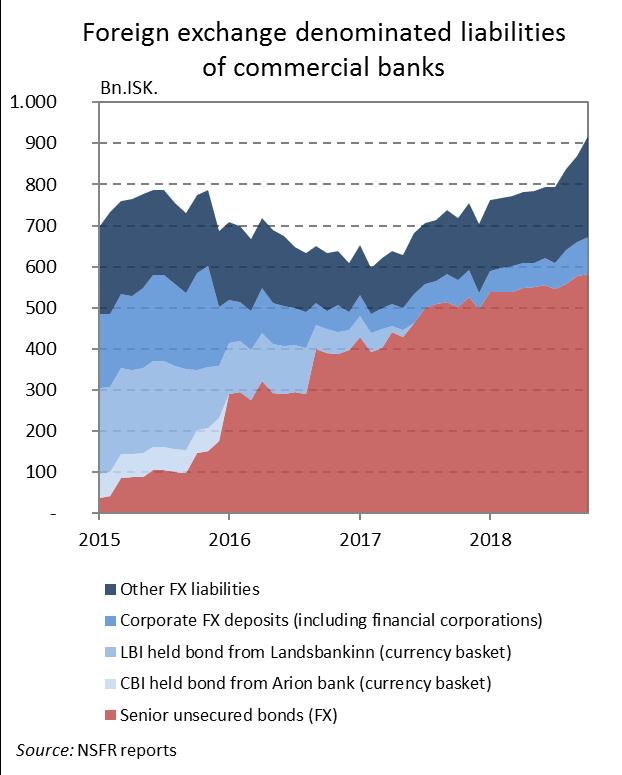

1 Reykjavík, 19. december 2018 Recommendation on countercyclical capital buffer On a quarterly basis, the Financial Stability Council shall submit recommendations to the Financial Supervisory Authority concerning the value of the countercyclical capital buffer pursuant to Article 86(d), Paragraph 1 of the Act on Financial Undertakings, no. 161/2002. In particular, the Council bases its recommendations on recommendations and analysis from the Systemic Risk Committee in determining the value of the countercyclical capital buffer; cf. the Act on a Financial Stability Council, no. 66/2014. The main purpose of the countercyclical capital buffer is to enhance financial system resilience against potential losses following excessive debt collection and accumulation of cyclical systemic risk. The buffer may be built up concurrent with the accumulation of imbalances in the financial system. The buffer requirement is reduced or lifted during a concurrent downward financial and business cycle so as to enhance financial institutions ability to maintain a sustainable supply of credit. The countercyclical capital buffer therefore changes with developments in cyclical systemic risk. With reference to the analysis conducted by the Systemic Risk Committee, the Financial Stability Council recommends to the Financial Supervisory Authority that the countercyclical capital buffer be raised by 25 basis points, to 2%, for all financial undertakings each institution individually and at the group level. Systemic Risk Committee analysis The decision to recommend a countercyclical capital buffer in Iceland takes account, among other things, of four core indicators that the Financial Stability Council has defined for the first intermediate objective of financial stability: growth in the credit-to-gdp ratio, real credit growth to households and businesses, real increases in residential and commercial real estate prices, and the credit-to-gdp gap. A number of other indicators are considered as well, so as to obtain a clear overview of cyclical systemic risk. 1 The financial cycle is according to all underlying indicators currently in an upswing stage. Due to persisting positive credit growth, increases in property prices and favorable economic conditions it is the view of the Financial Stability Council that the build-up of the countercyclical capital buffer should be continued. Credit growth and private sector debt The twelve-month growth in total private sector debt during Q3/2018 was 6.9% in real terms. Household debt increased by 4.6% in real terms and corporate debt by 9%. Private sector debt growth adjusted for inflation and exchange rate movements has been positive since the beginning of Most of the growth has been sustained by deposit institutions, their net private credit growth having been positive since the second half of The credit-to-gdp ratio rose by 4.4 percentage points between Q3/2017 and Q3/2018 and by 2.6% between April 2018, when the countercyclical captal buffer was last raised, and Q3/ The European Systemic Risk Board (ESRB/2014/1) recommends that when assessing quantitive information in regards to decisions on the appropriate countercyclical capital buffer that designated authorities should monitor a set of variables that indicate the build-up of cyclical systemic risk. This set should include the following: Measures of potential overvaluation of property prices, measures of credit developments, measures of external imbalances, measures of the strength of bank balance sheets, measures of private sector debt burden, measures of potential mispricing of risk as well as measures of derived from models that combine the gredit-to-gdp gap and a selection of the above measures.

2 The private sector credit-to-gdp ratio has been decreasing during the last several years and is now comparable to its value at the turn of the century. Should households start to take advantage of their increased overall crediworthiness in order to increase their debt levels this could lead to further debt imbalances. Corporate debt has risen notably more than other debt during the last few years and at the end of October 2018 the twelve-month growth of deposit instution s credit to firm was 12.8% in real terms. It s therefore important that the resilience of credit institutions should continue to be closely monitored. Real estate markets Despite the fact that increases in housing prices in the capital area have slowed down during 2018, the real price of housing is still high from a historical perspective. Housing prices have grown at a similar rate as the spending power of households, but when viewed in terms of other fundamentals prices appear overvalued. Historically, periods of rapid increases in housing prices accompanied by more lenient lending policies have routinely led to periods of rapid debt growth. 2 Thus, that debt growth was up until recently relatively low compared to the rapid growth of housing prices and the fact that at the same time lending policies were lossened somewhat, may indicate that private sector debt will continue to rise during the coming months. Experience has also shown that such periods as described can stimluate an increase in debt driven consumption. 3 Should housing prices and debt continue to grow at positive rates this might lead to housholds becoming more sensitive to sharp downswings in property prices, especially if households have taken out adjustable rate mortages and most of their net worth is tied up in homes. 4 This is the case with a sizable number of Icelandic households. Therefore, it is important to continue to monitor lender resilience in regards to both the impairment of housing loans as well as any possible indirect losses when widespread household financial difficulties lead to reduced demand and economic activity. During crises commercial real estate prices have a tendancy to fall much more rapidly than other real estate prices and historically credit institutions have experienced significant impairment losses on commercial real estate loans. 5 Thus, credit institutions face higher credit risk during periods when commercial real estate prices increase rapidly accompanied by increased commercial real estate lending. There are some indications that the overall returns of Icelandic firms are decreasing. Should prices of commercial real estate keep increasing while firm profits continue to deteriate it is possible that credit institution resilience would be negatively effected as loan portfolious become riskier. Financial market equity and funding The capital adequacy ratios of the three largest banks have decreased during the last several years. The banks funding has also recently become more risky, with tier 2 capital having increased at the expanse of Common Equity Tier 1 (CET 1) ratios. Raising the countercyclical capital buffer is thus expected to increase the quality of equity since the buffer requirement must be fufilled exclusively with CET 1 captial. The inflow of foreign capital can intensify the credit cycle and lead to current account imbalances. Private sector resilience to shocks is also reduced as the ratio of foreign denominated debt is increased. 6 The three largest banks have increasingly been seeking funding from foreign credit markets. Furthermore, recently there has been an increase in the banks foreign denominated lending to firms. Whether the banks increased dependancy on foreign denominated funding is further stimulating debt growth remains to be seen. 2 Roy & Kemme (2012). Causes of banking crises: deregluation, credit booms and asset bubbles, then and now. International Review of Economics & Finance. 24. pp Aoki et al. (2004). Housing prices, consumption, and monetary policy: A financial accelerator approach. Journal of Financial Intermediation. 13(4). pp IMF (2017). Household debt and financial Stability. Global Financial Stability Report and Zabai (2017). Household debt: recent development and challenges. BIS Quarterly Review, December pp Norges Bank (2018). Financial stability report 2018: Vulnerabilities and risks. and Kragh-Sorensen & Solheim (2014). What do banks lose money on during crises?. Norges Bank staff memo no.3/ Giese et al. (2014). The credit-to-gdp gap and complementary indicators for macroprudential policy: Evidence from the UK. International Journal of Fiance & Economics, 19(1), pp and Hahm, Shin & Shin (2013). Noncore bank liabilities and financial vulnerability. Journal of Money, Credit and Banking. 45(s1). pp

3 Economic outlook The output gap has continued to narrow and during the next couple of years economic growth is likely to be in line with the equilibrium growth of potential ouput. While private consumption has grown considerably there is still a sizable trade surplus. The Króna has depreciated during the last few months, which improves the terms of trade and the position of exporters. The economic outlook therefore does not indicate any reason for slowing down the build-up of the countercyclical capital buffer. The duration and magnitude of financial cycles are generally longer and higher than those of business cycles. Authorities should take this into account when making decisions on appropriate macroprudential policies in order to mitigate systemic risk. Conclusion Developments in cyclical systemic risk since the last increase in the countercyclical capital buffer are considered to warrant continued build-up of the countercyclical capital buffer, as previous instructions from the Financial Stability Council have indicated that the countercyclical capital buffer is in an upward phase. With reference to the analysis conducted by the Systemic Risk Committee, the Financial Stability Council recommends to the Financial Supervisory Authority that the countercyclical capital buffer be raised by 25 basis points, to 2%, for all financial undertakings each institution individually and at the group level apart from those institutions that are exempt from capital buffers pursuant to Article 84, Paragraph 4 of the Act on Financial Undertakings, no. 161/2002, and that the buffer take effect twelve (12) months after the date of the Financial Supervisory Authority decision. The Financial Stability Council can therefore be expected to recommend that the build-up of the countercyclical capital buffer continue in line with increased risk in the financial system.

4 Appendix to recommendation concerning countercyclical capital buffer In accordance with offical financial stability policy, the Financial Stability Council shall regularily disclose which indicators it takes into particular consideration in analysing systemic risk. Below are the indicators considered most important in the assessment of the countercyclical capital buffer at the Financial Stability Concil meeting of 19. december 2018.

5

6

Note on Countercyclical Capital Buffer Methodology

Note on Countercyclical Capital Buffer Methodology Prepared by Financial Stability Department December 2018 1 1. Background and Legal Basis Following the recent financial crisis, the Basel Committee on

Note on Countercyclical Capital Buffer Methodology Prepared by Financial Stability Department December 2018 1 1. Background and Legal Basis Following the recent financial crisis, the Basel Committee on

14. What Use Can Be Made of the Specific FSIs?

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers

The countercyclical capital buffer

The countercyclical capital buffer 17 November 217 The Systemic Risk Council, the Council, may recommend initiatives in the financial area to reduce or prevent the build-up of risks in the financial system.

The countercyclical capital buffer 17 November 217 The Systemic Risk Council, the Council, may recommend initiatives in the financial area to reduce or prevent the build-up of risks in the financial system.

EXECUTIVE COMMITTEE ACT 53/ Subject: Definition of a policy strategy for the exercise of the macro-prudential tasks of the Bank of Greece

EXECUTIVE COMMITTEE ACT 53/14.12.2015 Subject: Definition of a policy strategy for the exercise of the macro-prudential tasks of the Bank of Greece THE EXECUTIVE COMMITTEE OF THE BANK OF GREECE, having

EXECUTIVE COMMITTEE ACT 53/14.12.2015 Subject: Definition of a policy strategy for the exercise of the macro-prudential tasks of the Bank of Greece THE EXECUTIVE COMMITTEE OF THE BANK OF GREECE, having

EUROPEAN SYSTEMIC RISK BOARD

2.9.2014 EN Official Journal of the European Union C 293/1 I (Resolutions, recommendations and opinions) RECOMMENDATIONS EUROPEAN SYSTEMIC RISK BOARD RECOMMENDATION OF THE EUROPEAN SYSTEMIC RISK BOARD

2.9.2014 EN Official Journal of the European Union C 293/1 I (Resolutions, recommendations and opinions) RECOMMENDATIONS EUROPEAN SYSTEMIC RISK BOARD RECOMMENDATION OF THE EUROPEAN SYSTEMIC RISK BOARD

CNB press conference

Financial Stability Report 217/218 CNB press conference Jiří Rusnok, Governor Jan Frait, Executive Director, Financial Stability Department Prague, 12 June 218 I. Aggregate assessment of risks and overview

Financial Stability Report 217/218 CNB press conference Jiří Rusnok, Governor Jan Frait, Executive Director, Financial Stability Department Prague, 12 June 218 I. Aggregate assessment of risks and overview

1 DIRECTIVE 2013/36/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 26 June 2013 on access to the

Methodology underlying the determination of the benchmark countercyclical capital buffer rate and supplementary indicators signalling the build-up of cyclical systemic financial risk The application of

Methodology underlying the determination of the benchmark countercyclical capital buffer rate and supplementary indicators signalling the build-up of cyclical systemic financial risk The application of

Increase of the countercyclical capital buffer rate

Recommendation 25 September 218 Increase of the countercyclical capital buffer rate The Systemic Risk Council, the Council, recommends that the Minister for Industry, Business and Financial Affairs increase

Recommendation 25 September 218 Increase of the countercyclical capital buffer rate The Systemic Risk Council, the Council, recommends that the Minister for Industry, Business and Financial Affairs increase

Activation of the countercyclical capital buffer

Recommendation December 17 Activation of the countercyclical capital buffer The Systemic Risk Council, the Council, recommends that the Minister for Industry, Business and Financial Affairs set a countercyclical

Recommendation December 17 Activation of the countercyclical capital buffer The Systemic Risk Council, the Council, recommends that the Minister for Industry, Business and Financial Affairs set a countercyclical

Asia s Debt Risks The risk of financial crises is limited, but attention should be paid to slowing domestic demand.

Mizuho Economic Outlook & Analysis November 15, 218 Asia s Debt Risks The risk of financial crises is limited, but attention should be paid to slowing domestic demand. < Summary > Expanding private debt

Mizuho Economic Outlook & Analysis November 15, 218 Asia s Debt Risks The risk of financial crises is limited, but attention should be paid to slowing domestic demand. < Summary > Expanding private debt

Decision regarding the countercyclical buffer rate

2015-03-16 DECISION FI Ref. 15-3226 Finansinspektionen Box 7821 SE-103 97 Stockholm [Brunnsgatan 3] Tel +46 8 787 80 00 Fax +46 8 24 13 35 finansinspektionen@fi.se www.fi.se Decision regarding the countercyclical

2015-03-16 DECISION FI Ref. 15-3226 Finansinspektionen Box 7821 SE-103 97 Stockholm [Brunnsgatan 3] Tel +46 8 787 80 00 Fax +46 8 24 13 35 finansinspektionen@fi.se www.fi.se Decision regarding the countercyclical

SYSTEMIC RISK BUFFER. Background analysis for the implementation of the Systemic Risk Buffer as a macro-prudential measure in Estonia

SYSTEMIC RISK BUFFER Background analysis for the implementation of the as a macro-prudential measure in Estonia May 214 SUMMARY Starting from 1 January 214 the revised prudential requirements for credit

SYSTEMIC RISK BUFFER Background analysis for the implementation of the as a macro-prudential measure in Estonia May 214 SUMMARY Starting from 1 January 214 the revised prudential requirements for credit

INCREASING THE RATE OF CAPITAL FORMATION (Investment Policy Report)

") policies can increase our supply of goods and services, improve our efficiency in using the Nation's human resources, and help people lead more satisfying lives. INCREASING THE RATE OF CAPITAL FORMATION

policies can increase our supply of goods and services, improve our efficiency in using the Nation's human resources, and help people lead more satisfying lives. INCREASING THE RATE OF CAPITAL FORMATION

DEVELOPMENTS IN 2017 AND 2018 Q1

10 1 SUMMARY OVERALL ASSESSMENT Financial sector resiliance Cyclical risks Structural risks FSR 2015/2016 FSR 2016/2017 FSR 2017/2018 The Czech financial sector has developed highly favourably since spring

10 1 SUMMARY OVERALL ASSESSMENT Financial sector resiliance Cyclical risks Structural risks FSR 2015/2016 FSR 2016/2017 FSR 2017/2018 The Czech financial sector has developed highly favourably since spring

Is Something Rotten in the State of Iceland?

Is Something Rotten in the State of Iceland? Insight Is Something Rotten in the State of Iceland? 22 March 2006 2005: Report authors: Björn R. Guðmundsson +354 410 7382 bjornr@landsbanki.is Edda Rós Karlsdóttir

Is Something Rotten in the State of Iceland? Insight Is Something Rotten in the State of Iceland? 22 March 2006 2005: Report authors: Björn R. Guðmundsson +354 410 7382 bjornr@landsbanki.is Edda Rós Karlsdóttir

2018 Article IV Consultation with Norway Concluding Statement of the IMF Mission

2018 Article IV Consultation with Norway Concluding Statement of the IMF Mission June 7, 2018 A Concluding Statement describes the preliminary findings of IMF staff at the end of an official staff visit

2018 Article IV Consultation with Norway Concluding Statement of the IMF Mission June 7, 2018 A Concluding Statement describes the preliminary findings of IMF staff at the end of an official staff visit

Loan losses of banks and assessments of capital adequacy in the economic decline stage Flash report, 22 July 2009

Eesti Pank Bank of Estonia Loan losses of banks and assessments of capital adequacy in the economic decline stage Flash report, July 9 The banks operating in Estonia have used their earlier years profits

Eesti Pank Bank of Estonia Loan losses of banks and assessments of capital adequacy in the economic decline stage Flash report, July 9 The banks operating in Estonia have used their earlier years profits

Financial Stability Report 2012/2013

Financial Stability Report 2012/2013 Press Conference Presentation Miroslav Singer Governor Prague, 18 June 2013 Structure of presentation I. Initial state of real economy and financial sector and alternative

Financial Stability Report 2012/2013 Press Conference Presentation Miroslav Singer Governor Prague, 18 June 2013 Structure of presentation I. Initial state of real economy and financial sector and alternative

Information Note: The application of the countercyclical capital buffer in Ireland

2016 Information Note: The application of the countercyclical capital buffer in Ireland TABLE OF CONTENTS 1 Section 1: Background... 1 Section 2: The Central Bank as designated authority... 1 Decision

2016 Information Note: The application of the countercyclical capital buffer in Ireland TABLE OF CONTENTS 1 Section 1: Background... 1 Section 2: The Central Bank as designated authority... 1 Decision

Operationalizing the Selection and Application of Macroprudential Instruments

Operationalizing the Selection and Application of Macroprudential Instruments Presented by Tobias Adrian, Federal Reserve Bank of New York Based on Committee for Global Financial Stability Report 48 The

Operationalizing the Selection and Application of Macroprudential Instruments Presented by Tobias Adrian, Federal Reserve Bank of New York Based on Committee for Global Financial Stability Report 48 The

Normalizing Monetary Policy

Normalizing Monetary Policy Martin Feldstein The current focus of Federal Reserve policy is on normalization of monetary policy that is, on increasing short-term interest rates and shrinking the size of

Normalizing Monetary Policy Martin Feldstein The current focus of Federal Reserve policy is on normalization of monetary policy that is, on increasing short-term interest rates and shrinking the size of

Ric Battellino: Recent financial developments

Ric Battellino: Recent financial developments Address by Mr Ric Battellino, Deputy Governor of the Reserve Bank of Australia, at the Annual Stockbrokers Conference, Sydney, 26 May 2011. * * * Introduction

Ric Battellino: Recent financial developments Address by Mr Ric Battellino, Deputy Governor of the Reserve Bank of Australia, at the Annual Stockbrokers Conference, Sydney, 26 May 2011. * * * Introduction

FINNISH BANKING IN Financial overview of Finnish banks

FINNISH BANKING IN 2017 Financial overview of Finnish banks 1 FINNISH BANKING IN 2017 Contents 1 Economic environment... 2 1.1 Economic development... 2 1.2 Regulatory environment... 2 1.3 Housing market...

FINNISH BANKING IN 2017 Financial overview of Finnish banks 1 FINNISH BANKING IN 2017 Contents 1 Economic environment... 2 1.1 Economic development... 2 1.2 Regulatory environment... 2 1.3 Housing market...

Grant Spencer: Reserve Bank of New Zealand s perspective on housing

Grant Spencer: Reserve Bank of New Zealand s perspective on housing Speech by Mr Grant Spencer, Deputy Governor and Head of Financial Stability of the Reserve Bank of New Zealand, to Employers and Manufacturers

Grant Spencer: Reserve Bank of New Zealand s perspective on housing Speech by Mr Grant Spencer, Deputy Governor and Head of Financial Stability of the Reserve Bank of New Zealand, to Employers and Manufacturers

Activation of the systemic risk buffer in the Faroe Islands

Recommendation 3 March 217 Activation of the systemic risk buffer in the Faroe Islands The Systemic Risk Council recommends that the Minister for Industry, Business and Financial Affairs set a general

Recommendation 3 March 217 Activation of the systemic risk buffer in the Faroe Islands The Systemic Risk Council recommends that the Minister for Industry, Business and Financial Affairs set a general

Commercial real estate and financial stability

S P E E C H Date: 10/05/2017 Speaker: Erik Thedéen Meeting: DI Bank FI Ref.17-590 Finansinspektionen Box 7821 SE-103 97 Stockholm [Brunnsgatan 3] Tel +46 8 408 980 00 Fax +46 8 24 13 35 finansinspektionen@fi.se

S P E E C H Date: 10/05/2017 Speaker: Erik Thedéen Meeting: DI Bank FI Ref.17-590 Finansinspektionen Box 7821 SE-103 97 Stockholm [Brunnsgatan 3] Tel +46 8 408 980 00 Fax +46 8 24 13 35 finansinspektionen@fi.se

Embargo until 12:30 pm CET (6:30 am Washington, DC time) on May 15, Germany: Staff Concluding Statement of the 2017 Article IV Mission

on May 15, Germany: Staff Concluding Statement of the 2017 Article IV Mission") Embargo until 12:30 pm CET (6:30 am Washington, DC time) on May 15, 2017 May 15, 2016 Germany: Staff Concluding Statement of the 2017 Article IV Mission A Concluding Statement describes the preliminary

Embargo until 12:30 pm CET (6:30 am Washington, DC time) on May 15, 2017 May 15, 2016 Germany: Staff Concluding Statement of the 2017 Article IV Mission A Concluding Statement describes the preliminary

1. Residential property

A. Macroprudential policy The purpose of the Bank s activities in performing its macroprudential mandate is to safeguard overall financial stability. The Bank fulfils part of that responsibility jointly

A. Macroprudential policy The purpose of the Bank s activities in performing its macroprudential mandate is to safeguard overall financial stability. The Bank fulfils part of that responsibility jointly

Limits on debt-to-income as a macro-prudential tool

Date: 19 August 2016 To: Minister of Finance Limits on debt-to-income as a macro-prudential tool 1. The purpose of this memorandum is to seek your agreement to add an additional class of policy tool to

Date: 19 August 2016 To: Minister of Finance Limits on debt-to-income as a macro-prudential tool 1. The purpose of this memorandum is to seek your agreement to add an additional class of policy tool to

OF HOUSEHOLDS COUNTERCYCLICAL CAPITAL BUFFER. June BACKGROUND MATERIAL FOR DECISION

REVIEW OF THE SURVEY OF THE FINANCIAL BEHAVIOUR COUNTERCYCLICAL CAPITAL BUFFER BACKGROUND MATERIAL FOR DECISION 13 17 OF HOUSEHOLDS Q1 June 13 Abbreviations ISSN 2424-371 CCB ECB EEA ESRB GDP MFI RE countercyclical

REVIEW OF THE SURVEY OF THE FINANCIAL BEHAVIOUR COUNTERCYCLICAL CAPITAL BUFFER BACKGROUND MATERIAL FOR DECISION 13 17 OF HOUSEHOLDS Q1 June 13 Abbreviations ISSN 2424-371 CCB ECB EEA ESRB GDP MFI RE countercyclical

FIGURE EAP: Recent developments

Growth in the East Asia and Pacific region is expected to remain solid, slowing marginally to 6.3 percent in 2018 and to an average of 6.1 percent in 2019-20, broadly as previously projected. This modest

Growth in the East Asia and Pacific region is expected to remain solid, slowing marginally to 6.3 percent in 2018 and to an average of 6.1 percent in 2019-20, broadly as previously projected. This modest

made available a few days after the next regularly scheduled and the Board's Annual Report. The summary descriptions of

FEDERAL RESERVE press release For Use at 4:00 p.m. October 20, 1978 The Board of Governors of the Federal Reserve System and the Federal Open Market Committee today released the attached record of policy

FEDERAL RESERVE press release For Use at 4:00 p.m. October 20, 1978 The Board of Governors of the Federal Reserve System and the Federal Open Market Committee today released the attached record of policy

A new macro-prudential policy framework for New Zealand final policy position

A new macro-prudential policy framework for New Zealand final policy position May 2013 2 1.0 Background 1. During March and April, the Reserve Bank undertook a public consultation on its proposed framework

A new macro-prudential policy framework for New Zealand final policy position May 2013 2 1.0 Background 1. During March and April, the Reserve Bank undertook a public consultation on its proposed framework

FISCAL COUNCIL OPINION ON THE SUMMER FORECAST 2018 OF THE MINISTRY OF FINANCE

FISCAL COUNCIL OPINION ON THE SUMMER FORECAST 2018 OF THE MINISTRY OF FINANCE September 2018 Contents Opinion... 3 Explanatory Report... 4 Opinion on the summer forecast 2018 of the Ministry of Finance...

FISCAL COUNCIL OPINION ON THE SUMMER FORECAST 2018 OF THE MINISTRY OF FINANCE September 2018 Contents Opinion... 3 Explanatory Report... 4 Opinion on the summer forecast 2018 of the Ministry of Finance...

Designing Scenarios for Macro Stress Testing (Financial System Report, April 2016)

") Financial System Report Annex Series inancial ystem eport nnex A Designing Scenarios for Macro Stress Testing (Financial System Report, April 1) FINANCIAL SYSTEM AND BANK EXAMINATION DEPARTMENT BANK OF

Financial System Report Annex Series inancial ystem eport nnex A Designing Scenarios for Macro Stress Testing (Financial System Report, April 1) FINANCIAL SYSTEM AND BANK EXAMINATION DEPARTMENT BANK OF

Finland falling further behind euro area growth

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

The Belgian Mortgage Market: Recent Developments and Prudential Measures

Thomas Schepens Nationale Bank van Belgiё 1 Introduction The presentation at the workshop was based on two articles that appeared in the Financial Stability Review 2014 of the Nationale Bank van Belgiё

Thomas Schepens Nationale Bank van Belgiё 1 Introduction The presentation at the workshop was based on two articles that appeared in the Financial Stability Review 2014 of the Nationale Bank van Belgiё

Minutes of the Monetary Policy Committee meeting, August 2016

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting, August 2016 Published 7 September 2016 The Act on the Central Bank of Iceland stipulates that

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting, August 2016 Published 7 September 2016 The Act on the Central Bank of Iceland stipulates that

Increase of the systemic risk buffer rate in the Faroe Islands

Recommendation 9 April 218 Increase of the systemic risk buffer rate in the Faroe Islands The Systemic Risk Council recommends that the Minister for Industry, Business and Financial Affairs raise the general

Recommendation 9 April 218 Increase of the systemic risk buffer rate in the Faroe Islands The Systemic Risk Council recommends that the Minister for Industry, Business and Financial Affairs raise the general

Economic Outlook, January 2016 Jeffrey M. Lacker President, Federal Reserve Bank of Richmond

Economic Outlook, January 2016 Jeffrey M. Lacker President, Federal Reserve Bank of Richmond Annual Meeting of the South Carolina Business & Industry Political Education Committee Columbia, South Carolina

Economic Outlook, January 2016 Jeffrey M. Lacker President, Federal Reserve Bank of Richmond Annual Meeting of the South Carolina Business & Industry Political Education Committee Columbia, South Carolina

Macro-prudential policy in the New Zealand context

Macro-prudential policy in the New Zealand context MONETARY POLICY WORKSHOP ON STRENGTHENING MACRO-PRUDENTIAL FRAMEWORKS TOKYO, JAPAN MARCH 22-23 212 Chris Hunt Reserve Bank of New Zealand Outline 1. Broader

Macro-prudential policy in the New Zealand context MONETARY POLICY WORKSHOP ON STRENGTHENING MACRO-PRUDENTIAL FRAMEWORKS TOKYO, JAPAN MARCH 22-23 212 Chris Hunt Reserve Bank of New Zealand Outline 1. Broader

Economic Survey December 2006 English Summary

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

Developments in inflation and its determinants

INFLATION REPORT February 2018 Summary Developments in inflation and its determinants The annual CPI inflation rate strengthened its upward trend in the course of 2017 Q4, standing at 3.32 percent in December,

INFLATION REPORT February 2018 Summary Developments in inflation and its determinants The annual CPI inflation rate strengthened its upward trend in the course of 2017 Q4, standing at 3.32 percent in December,

Investment and its Financing: A Macro Perspective

G R O U P O F T W E N T Y Investment and its Financing: A Macro Perspective Annex to the G Surveillance Note Meetings of G Finance Ministers and Central Bank Governors February, 3 Prepared by Staff of

G R O U P O F T W E N T Y Investment and its Financing: A Macro Perspective Annex to the G Surveillance Note Meetings of G Finance Ministers and Central Bank Governors February, 3 Prepared by Staff of

Financial Stability: The Role of Real Estate Values

EMBARGOED UNTIL 9:45 P.M. on Tuesday, March 21, 2017 U.S. Eastern Time which is 9:45 A.M. on Wednesday, March 22, 2017 in Bali, Indonesia OR UPON DELIVERY Financial Stability: The Role of Real Estate Values

EMBARGOED UNTIL 9:45 P.M. on Tuesday, March 21, 2017 U.S. Eastern Time which is 9:45 A.M. on Wednesday, March 22, 2017 in Bali, Indonesia OR UPON DELIVERY Financial Stability: The Role of Real Estate Values

Use the following to answer question 15: AE0 AE1. Real expenditures. Real income. Page 3

Chapter 10 1. An example of an autonomous consumption policy is a policy that A) lowers tax rates to stimulate additional consumer spending. B) makes credit more widely available to consumers in order

Chapter 10 1. An example of an autonomous consumption policy is a policy that A) lowers tax rates to stimulate additional consumer spending. B) makes credit more widely available to consumers in order

REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL. Market developments potentially requiring the use of Article 459 CRR

EUROPEAN COMMISSION Brussels, 8.3.2017 COM(2017) 121 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Market developments potentially requiring the use of Article 459 CRR EN

EUROPEAN COMMISSION Brussels, 8.3.2017 COM(2017) 121 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Market developments potentially requiring the use of Article 459 CRR EN

Macroprudential Policies

Macroprudential Policies Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges and Policies Jakarta, 9-13 April 2018 Yoke Wang Tok The views expressed herein are

Macroprudential Policies Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges and Policies Jakarta, 9-13 April 2018 Yoke Wang Tok The views expressed herein are

Macro-prudential Policy Strategy July 2016 Financial Stability Department

Macro-prudential Policy Strategy July 2016 Fátima Silva Outline 1. Macro-prudential Policy Strategy 2. Macro-prudential Toolkit: Policy Actions in 2015/2016 2.1. Countercyclical Capital Buffer 2.2. O-SIIs

Macro-prudential Policy Strategy July 2016 Fátima Silva Outline 1. Macro-prudential Policy Strategy 2. Macro-prudential Toolkit: Policy Actions in 2015/2016 2.1. Countercyclical Capital Buffer 2.2. O-SIIs

SOUTH ASIA. Chapter 2. Recent developments

SOUTH ASIA GLOBAL ECONOMIC PROSPECTS January 2014 Chapter 2 s GDP growth rose to an estimated 4.6 percent in 2013 from 4.2 percent in 2012, but was well below its average in the past decade, reflecting

SOUTH ASIA GLOBAL ECONOMIC PROSPECTS January 2014 Chapter 2 s GDP growth rose to an estimated 4.6 percent in 2013 from 4.2 percent in 2012, but was well below its average in the past decade, reflecting

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL

EUROPEAN COMMISSION Brussels, 9.4.2018 COM(2018) 172 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL on Effects of Regulation (EU) 575/2013 and Directive 2013/36/EU on the Economic

EUROPEAN COMMISSION Brussels, 9.4.2018 COM(2018) 172 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL on Effects of Regulation (EU) 575/2013 and Directive 2013/36/EU on the Economic

Ryuzo Miyao: Economic activity and prices in Japan and monetary policy

Ryuzo Miyao: Economic activity and prices in Japan and monetary policy Summary of a speech by Mr Ryuzo Miyao, Member of the Policy Board of the Bank of Japan, at a meeting with business leaders, Tokushima,

Ryuzo Miyao: Economic activity and prices in Japan and monetary policy Summary of a speech by Mr Ryuzo Miyao, Member of the Policy Board of the Bank of Japan, at a meeting with business leaders, Tokushima,

Household Balance Sheets and Debt an International Country Study

47 Household Balance Sheets and Debt an International Country Study Jacob Isaksen, Paul Lassenius Kramp, Louise Funch Sørensen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY What are the

47 Household Balance Sheets and Debt an International Country Study Jacob Isaksen, Paul Lassenius Kramp, Louise Funch Sørensen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY What are the

The Icelandic Economy

The Icelandic Economy Spring 2006 Macroeconomic forecast 2006 2010 Summary edition on April 25th 2006 M inistry of Finance The Icelandic Economy Spring 2006 25 April, 2006 This issue is published on the

The Icelandic Economy Spring 2006 Macroeconomic forecast 2006 2010 Summary edition on April 25th 2006 M inistry of Finance The Icelandic Economy Spring 2006 25 April, 2006 This issue is published on the

Economic Survey August 2006 English Summary

Economic Survey August English Summary. Short term outlook In several respects, the upswing in the Danish economy is stronger than expected in the May survey: private sector employment has increased strongly,

Economic Survey August English Summary. Short term outlook In several respects, the upswing in the Danish economy is stronger than expected in the May survey: private sector employment has increased strongly,

Economic Letter. Using the Countercyclical Capital Buffer: Insights from a structural model. Matija Lozej & Martin O Brien Vol. 2018, No.

Economic Letter Using the Countercyclical Capital Buffer: Insights from a structural model Matija Lozej & Martin O Brien Vol. 8, No. 7 Using the Countercyclical Capital Buffer Central Bank of Ireland Page

Economic Letter Using the Countercyclical Capital Buffer: Insights from a structural model Matija Lozej & Martin O Brien Vol. 8, No. 7 Using the Countercyclical Capital Buffer Central Bank of Ireland Page

The Role of Foreign Financial Institutions in Japan's Financial System

September 29, 2014 Bank of Japan The Role of Foreign Financial Institutions in Japan's Financial System Speech at a Meeting Held by the International Bankers Association of Japan Haruhiko Kuroda Governor

September 29, 2014 Bank of Japan The Role of Foreign Financial Institutions in Japan's Financial System Speech at a Meeting Held by the International Bankers Association of Japan Haruhiko Kuroda Governor

Executive Directors welcomed the continued

ANNEX IMF EXECUTIVE BOARD DISCUSSION OF THE OUTLOOK, AUGUST 2006 The following remarks by the Acting Chair were made at the conclusion of the Executive Board s discussion of the World Economic Outlook

ANNEX IMF EXECUTIVE BOARD DISCUSSION OF THE OUTLOOK, AUGUST 2006 The following remarks by the Acting Chair were made at the conclusion of the Executive Board s discussion of the World Economic Outlook

Svein Gjedrem: The central bank s instruments

Svein Gjedrem: The central bank s instruments Lecture by Mr Svein Gjedrem, Governor of the Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME)/BI Norwegian School of Management,

Svein Gjedrem: The central bank s instruments Lecture by Mr Svein Gjedrem, Governor of the Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME)/BI Norwegian School of Management,

CRS Report for Congress

CRS Report for Congress Received through the CRS Web Order Code RS21951 October 12, 2004 Changing Causes of the U.S. Trade Deficit Summary Marc Labonte and Gail Makinen Government and Finance Division

CRS Report for Congress Received through the CRS Web Order Code RS21951 October 12, 2004 Changing Causes of the U.S. Trade Deficit Summary Marc Labonte and Gail Makinen Government and Finance Division

8. Foreign debt. Chart 8.2

8. Foreign debt External debt Iceland s external indebtedness is high by international comparison and has risen sharply since the mid-1990s. As can be seen from Chart 8.1 only two other developed countries,

8. Foreign debt External debt Iceland s external indebtedness is high by international comparison and has risen sharply since the mid-1990s. As can be seen from Chart 8.1 only two other developed countries,

Lars Nyberg: Developments in the property market

Lars Nyberg: Developments in the property market Speech by Mr Lars Nyberg, Deputy Governor of the Sveriges Riksbank, at Fastighetsvärlden (Swedish newspaper), Stockholm, 30 May 2007. * * * I would like

Lars Nyberg: Developments in the property market Speech by Mr Lars Nyberg, Deputy Governor of the Sveriges Riksbank, at Fastighetsvärlden (Swedish newspaper), Stockholm, 30 May 2007. * * * I would like

Template for notifying intended measures to be taken under Article 458 of the Capital Requirements Regulation (CRR)

") Template for notifying intended measures to be taken under Article 458 of the Capital Requirements Regulation (CRR) Please send this template to notifications@esrb.europa.eu when notifying the ESRB; macropru.notifications@ecb.europa.eu

Template for notifying intended measures to be taken under Article 458 of the Capital Requirements Regulation (CRR) Please send this template to notifications@esrb.europa.eu when notifying the ESRB; macropru.notifications@ecb.europa.eu

SPEECH. Monetary policy and the current economic situation. Well-balanced monetary policy in July

SPEECH DATE: 22 August 2013 SPEAKER: First Deputy Governor Kerstin af Jochnick LOCATION: County Administrative Board in Kalmar SVERIGES RIKSBANK SE-103 37 Stockholm (Brunkebergstorg 11) Tel +46 8 787 00

SPEECH DATE: 22 August 2013 SPEAKER: First Deputy Governor Kerstin af Jochnick LOCATION: County Administrative Board in Kalmar SVERIGES RIKSBANK SE-103 37 Stockholm (Brunkebergstorg 11) Tel +46 8 787 00

Angola - Economic Report

Angola - Economic Report Index I. Assumptions on National Policy and External Environment... 2 II. Recent Trends... 3 A. Real Sector Developments... 3 B. Monetary and Financial sector developments... 5

Angola - Economic Report Index I. Assumptions on National Policy and External Environment... 2 II. Recent Trends... 3 A. Real Sector Developments... 3 B. Monetary and Financial sector developments... 5

Advanced Market Analysis for Commercial Real Estate

Ward Center for Real Estate Studies www.ccim.com Advanced Market Analysis for Commercial Real Estate PPT Handout EXCELLENCE SUCCESS SKILL LEADERSHIP CHALLENGE STRENGTH Copyright 2012 by the CCIM Institute

Ward Center for Real Estate Studies www.ccim.com Advanced Market Analysis for Commercial Real Estate PPT Handout EXCELLENCE SUCCESS SKILL LEADERSHIP CHALLENGE STRENGTH Copyright 2012 by the CCIM Institute

Part IV Dissemination and Data Analysis

- 268 - Part IV Dissemination and Data Analysis - 269 - Chapter Twelve Dissemination of FSI ratios and related data Introduction 12.1 To enhance the transparency of their financial system, countries are

- 268 - Part IV Dissemination and Data Analysis - 269 - Chapter Twelve Dissemination of FSI ratios and related data Introduction 12.1 To enhance the transparency of their financial system, countries are

FINANCIAL STABILITY IN THE REPUBLIC OF BELARUS

NATIONAL BANK OF 1 THE REPUBLIC OF BELARUS FINANCIAL STABILITY IN THE REPUBLIC OF BELARUS 2010 MINSK, 2011 2 This publication has been prepared by the Banking Supervision Directorate in concert with the

NATIONAL BANK OF 1 THE REPUBLIC OF BELARUS FINANCIAL STABILITY IN THE REPUBLIC OF BELARUS 2010 MINSK, 2011 2 This publication has been prepared by the Banking Supervision Directorate in concert with the

Exploring the Economy s Progress and Outlook

EMBARGOED UNTIL Friday, September 9, 2016 at 8:15 A.M. U.S. Eastern Time OR UPON DELIVERY Exploring the Economy s Progress and Outlook Eric S. Rosengren President & Chief Executive Officer Federal Reserve

EMBARGOED UNTIL Friday, September 9, 2016 at 8:15 A.M. U.S. Eastern Time OR UPON DELIVERY Exploring the Economy s Progress and Outlook Eric S. Rosengren President & Chief Executive Officer Federal Reserve

APPLICATION OF THE COUNTERCYCLICAL CAPITAL BUFFER IN LITHUANIA

TEMINIŲ STRAIPSNIŲ SERIJA No 5 / 215 TRANSLATION APPLICATION OF THE COUNTERCYCLICAL CAPITAL BUFFER IN LITHUANIA Bank of Lithuania, 215 Reproduction for educational and non-commercial purposes is permitted

TEMINIŲ STRAIPSNIŲ SERIJA No 5 / 215 TRANSLATION APPLICATION OF THE COUNTERCYCLICAL CAPITAL BUFFER IN LITHUANIA Bank of Lithuania, 215 Reproduction for educational and non-commercial purposes is permitted

Grant Spencer: Update on the New Zealand housing market

Grant Spencer: Update on the New Zealand housing market Speech by Mr Grant Spencer, Deputy Governor and Head of Financial Stability of the Reserve Bank of New Zealand, to Admirals Breakfast Club, Auckland,

Grant Spencer: Update on the New Zealand housing market Speech by Mr Grant Spencer, Deputy Governor and Head of Financial Stability of the Reserve Bank of New Zealand, to Admirals Breakfast Club, Auckland,

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-Second Meeting October 9 10, 2015 Statement by José Darío Uribe, Governor, Banco de la República, Colombia On behalf of Colombia, Costa Rica, El Salvador,

International Monetary and Financial Committee Thirty-Second Meeting October 9 10, 2015 Statement by José Darío Uribe, Governor, Banco de la República, Colombia On behalf of Colombia, Costa Rica, El Salvador,

ANNUAL REPORT 2015 CHAPTER 2 COMPETITIVE ADJUSTMENT AND RECOVERY IN THE SPANISH ECONOMY DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

ANNUAL REPORT 215 CHAPTER 2 COMPETITIVE ADJUSTMENT AND RECOVERY IN THE SPANISH ECONOMY THE RECOVERY IN COMPETITIVENESS There has been a significant improvement in price/cost competitiveness since 28, although

ANNUAL REPORT 215 CHAPTER 2 COMPETITIVE ADJUSTMENT AND RECOVERY IN THE SPANISH ECONOMY THE RECOVERY IN COMPETITIVENESS There has been a significant improvement in price/cost competitiveness since 28, although

Press release 557 th Meeting of the Governing Board of the Bank of Slovenia Ljubljana, 7 June 2016

Press release 557 th Meeting of the Governing Board of the Bank of Slovenia Ljubljana, 7 June 2016 The Governing Board of the Bank of Slovenia discussed the June 2016 Macroeconomic Forecast for Slovenia*

Press release 557 th Meeting of the Governing Board of the Bank of Slovenia Ljubljana, 7 June 2016 The Governing Board of the Bank of Slovenia discussed the June 2016 Macroeconomic Forecast for Slovenia*

Turkey s Experience with Macroprudential Policy

Turkey s Experience with Macroprudential Policy Hakan Kara* Central Bank of Turkey Macroprudential Policy: Effectiveness and Implementation Challenges CBRT-IMF-BIS Joint Conference October 26-27, 2015

Turkey s Experience with Macroprudential Policy Hakan Kara* Central Bank of Turkey Macroprudential Policy: Effectiveness and Implementation Challenges CBRT-IMF-BIS Joint Conference October 26-27, 2015

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy Perry Warjiyo 1 Abstract As a bank-based economy, global factors affect financial intermediation

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy Perry Warjiyo 1 Abstract As a bank-based economy, global factors affect financial intermediation

5. Bulgarian National Bank Forecast of Key

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2018 2020 This issue of Economic Review includes the of key macroeconomic indicators for the 2018 2020 period. It is based on information

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2018 2020 This issue of Economic Review includes the of key macroeconomic indicators for the 2018 2020 period. It is based on information

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016 At the meeting, members of the Monetary Policy Council discussed monetary policy against the background of macroeconomic

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016 At the meeting, members of the Monetary Policy Council discussed monetary policy against the background of macroeconomic

Changes in financial intermediation structure

Changes in financial intermediation structure Their implications for central bank policies: Korea s experience Huh Jinho 1 Abstract Korea s financial intermediation structure has changed significantly

Changes in financial intermediation structure Their implications for central bank policies: Korea s experience Huh Jinho 1 Abstract Korea s financial intermediation structure has changed significantly

Grant Spencer: Trends in the New Zealand housing market

Grant Spencer: Trends in the New Zealand housing market Speech by Mr Grant Spencer, Deputy Governor and Head of Financial Stability of the Reserve Bank of New Zealand, to the Property Council of New Zealand,

Grant Spencer: Trends in the New Zealand housing market Speech by Mr Grant Spencer, Deputy Governor and Head of Financial Stability of the Reserve Bank of New Zealand, to the Property Council of New Zealand,

Iceland Economic Outlook

Iceland Economic Outlook Fridrik M. Baldursson IACC Conference New York, April 14 2011 What happened in Iceland? Banking sector grew to 10 x GDP in 2008 GDP on order of 10 bn Banks were allowed to collapse

Iceland Economic Outlook Fridrik M. Baldursson IACC Conference New York, April 14 2011 What happened in Iceland? Banking sector grew to 10 x GDP in 2008 GDP on order of 10 bn Banks were allowed to collapse

Implementation of the EU fiscal governance framework: Assessment of the fiscal stance appropriate for the euro area

European Fiscal Board Implementation of the EU fiscal governance framework: Assessment of the fiscal stance appropriate for the euro area Prof. Niels THYGESEN Chair of the European Fiscal Board Interparliamentary

European Fiscal Board Implementation of the EU fiscal governance framework: Assessment of the fiscal stance appropriate for the euro area Prof. Niels THYGESEN Chair of the European Fiscal Board Interparliamentary

F I N A N C I A L S T A B I L I T Y R E P O R T

BANK OF ISRAEL F I N A N C I A L S T A B I L I T Y R E P O R T Jerusalem, June 217 Tammuz 5777 This report was written by Meital Graham, Barak Ettinger, Matan Weinberg, Leah Levin-Goldstein, Noam Michelson,

BANK OF ISRAEL F I N A N C I A L S T A B I L I T Y R E P O R T Jerusalem, June 217 Tammuz 5777 This report was written by Meital Graham, Barak Ettinger, Matan Weinberg, Leah Levin-Goldstein, Noam Michelson,

Bubble, Bubble Toil and Trouble:

Client Alert December 22, 2015 Bubble, Bubble Toil and Trouble: The Fed Breathes Life into the Countercyclical Capital Buffer Widespread problems in the banking system are often associated with sharp declines

Client Alert December 22, 2015 Bubble, Bubble Toil and Trouble: The Fed Breathes Life into the Countercyclical Capital Buffer Widespread problems in the banking system are often associated with sharp declines

The Argentine Economy in the year 2006

The Argentine Economy in the year 2006 ECONOMIC REPORT Year 2006 1. The Current Recovery from a Historical Perspective The Argentine economy has completed another year of significant growth with an 8.5%

The Argentine Economy in the year 2006 ECONOMIC REPORT Year 2006 1. The Current Recovery from a Historical Perspective The Argentine economy has completed another year of significant growth with an 8.5%

REPORT. vulnerabilities AND RISKS

217 FinANCIAL STABILITY REPORT vulnerabilities AND RISKS Norges Bank Oslo 217 Address: Bankplassen 2 Postal address: P.O.Box 1179 Sentrum, N-17 Oslo Phone: +47 22316 E-mail: central.bank@norges-bank.no

217 FinANCIAL STABILITY REPORT vulnerabilities AND RISKS Norges Bank Oslo 217 Address: Bankplassen 2 Postal address: P.O.Box 1179 Sentrum, N-17 Oslo Phone: +47 22316 E-mail: central.bank@norges-bank.no

Pohjola Bank plc Financial Statements Bulletin for 1 January 31 December 2015

Pohjola Bank plc Stock Exchange Release, 4 February 2016 at 09.00 am EET Financial Statements Bulletin Pohjola Bank plc Financial Statements Bulletin for 1 January 31 December 2015 Consolidated earnings

Pohjola Bank plc Stock Exchange Release, 4 February 2016 at 09.00 am EET Financial Statements Bulletin Pohjola Bank plc Financial Statements Bulletin for 1 January 31 December 2015 Consolidated earnings

CAPITAL FLOWS TO LATIN AMERICA: CHALLENGES AND POLICY RESPONSES. Javier Guzmán Calafell 1

CAPITAL FLOWS TO LATIN AMERICA: CHALLENGES AND POLICY RESPONSES Javier Guzmán Calafell 1 1. Introduction Capital flows to Latin America and other emerging market regions fell sharply after the collapse

CAPITAL FLOWS TO LATIN AMERICA: CHALLENGES AND POLICY RESPONSES Javier Guzmán Calafell 1 1. Introduction Capital flows to Latin America and other emerging market regions fell sharply after the collapse

China s macroeconomic imbalances: causes and consequences. John Knight and Wang Wei

China s macroeconomic imbalances: causes and consequences John Knight and Wang Wei 1. Introduction This paper is different from the specialist papers at this conference It is more general, and is more

China s macroeconomic imbalances: causes and consequences John Knight and Wang Wei 1. Introduction This paper is different from the specialist papers at this conference It is more general, and is more

Advanced Market Analysis for Commercial Real Estate

Ward Center for Real Estate Studies www.ccim.com Advanced Market Analysis for Commercial Real Estate PPT Handout EXCELLENCE SUCCESS SKILL LEADERSHIP CHALLENGE STRENGTH Copyright 2012 by the CCIM Institute

Ward Center for Real Estate Studies www.ccim.com Advanced Market Analysis for Commercial Real Estate PPT Handout EXCELLENCE SUCCESS SKILL LEADERSHIP CHALLENGE STRENGTH Copyright 2012 by the CCIM Institute

Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead

January 21 Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead Systemic risks have continued to subside as economic fundamentals have improved and substantial public support

January 21 Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead Systemic risks have continued to subside as economic fundamentals have improved and substantial public support

Minutes of the Monetary Policy Committee meeting November 2010

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting November 2010 Published: 17 November 2010 The Act on the Central Bank of Iceland stipulates

The Monetary Policy Committee of the Central Bank of Iceland Minutes of the Monetary Policy Committee meeting November 2010 Published: 17 November 2010 The Act on the Central Bank of Iceland stipulates

1. When the Federal government uses taxation and spending actions to stimulate the economy it is conducting:

1. When the Federal government uses taxation and spending actions to stimulate the economy it is conducting: A. Fiscal policy B. Incomes policy C. Monetary policy D. Employment policy 2. When the Federal

1. When the Federal government uses taxation and spending actions to stimulate the economy it is conducting: A. Fiscal policy B. Incomes policy C. Monetary policy D. Employment policy 2. When the Federal

Class Notes. Chapter 5 Saving and Investment in the Open Economy Learning Objectives

1 Chapter 5 Saving and Investment in the Open Economy Learning Objectives A. Explain how the balance of payments is calculated (Sec. 5.1) B. Discuss goods market equilibrium in an open economy (Sec. 5.2)

1 Chapter 5 Saving and Investment in the Open Economy Learning Objectives A. Explain how the balance of payments is calculated (Sec. 5.1) B. Discuss goods market equilibrium in an open economy (Sec. 5.2)

Demographic Changes and Challenges for Financial Sector

November 19, 2018 Bank of Japan Demographic Changes and Challenges for Financial Sector Remarks at the Paris EUROPLACE Financial Forum in Tokyo Haruhiko Kuroda Governor of the Bank of Japan Introduction

November 19, 2018 Bank of Japan Demographic Changes and Challenges for Financial Sector Remarks at the Paris EUROPLACE Financial Forum in Tokyo Haruhiko Kuroda Governor of the Bank of Japan Introduction

The Rt Hon Philip Hammond MP Chancellor of the Exchequer HM Treasury 1 Horse Guards Road London SW1A2HQ 5 December 2018

Mark Carney Governor The Rt Hon Philip Hammond MP Chancellor of the Exchequer HM Treasury 1 Horse Guards Road London SW1A2HQ 5 December 2018 In my role as Chair of the Financial Policy Committee (FPC),

Mark Carney Governor The Rt Hon Philip Hammond MP Chancellor of the Exchequer HM Treasury 1 Horse Guards Road London SW1A2HQ 5 December 2018 In my role as Chair of the Financial Policy Committee (FPC),

DANMARKS NATIONALBANK

ANALYSIS DANMARKS NATIONALBANK 31 MAY 1 NO. 5 STRESS TEST The largest banks are close to buffer requirements in stress test The systemically important banks have capital to withstand a severe recession

ANALYSIS DANMARKS NATIONALBANK 31 MAY 1 NO. 5 STRESS TEST The largest banks are close to buffer requirements in stress test The systemically important banks have capital to withstand a severe recession

Svein Gjedrem: Monetary policy and the outlook for the Norwegian economy

Svein Gjedrem: Monetary policy and the outlook for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Mid-Norway Chamber of Commerce and Industry,

Svein Gjedrem: Monetary policy and the outlook for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Mid-Norway Chamber of Commerce and Industry,

The Federal Reserve in the 21st Century Financial Stability Policies

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are