Rental market green shoots?

|

|

|

- Marilynn Randall

- 5 years ago

- Views:

Transcription

1 THE PAYPROP ANNUAL REVIEW 2018 First quarterly growth uptick in 2 years Average rent hits higher bracket Free State growth spurt Rental market green shoots? PAYPROP RENTAL INDEX ANNUAL REVIEW

2

3 INDEX A fresh start Below-inflation rental growth Provincial statistics 2018 Eastern Cape Free State Gauteng KwaZulu-Natal 50 Lowest-risk renters 10 The national context Limpopo Mpumalanga North West Northern Cape Western Cape What does low-risk look like? Not all bad news PAYPROP RENTAL INDEX ANNUAL REVIEW

4 Introduction A FRESH START Whether you believe in resolutions or not, there s something to be said for a new year. It s an opportunity to start afresh, learn from past mistakes and transform yourself and your business. In short, a chance to keep the things that worked and change the ones that didn t! That being said, not all change is positive is an election year and we can expect fresh political uncertainty, which in turn could create continued economic uncertainty and volatility. Just how much that could affect rental prices we ll have to wait and see. But it s pointless talking about the unknowns of 2019 without reflecting on what happened in 2018: At PayProp, we relaunched the Tenant Assessment Report and introduced the PayProp Rental Risk Rating a unique score that more accurately predicts bad tenant behaviour than a credit score, because it combines credit data with rental data. And lastly, we travelled the country with the ever-popular PayProp Academy, raising awareness about the need to embrace business-enhancing technologies in the property sector an industry ripe for disruption. As you ll see from the PayProp Annual Review for 2018, the market continued its gradual slowdown last year, although some provinces have started to see improvements. Read more about that in this issue. Until our next quarterly issue in April! Johette Smuts Head of Data and Analytics PayProp South Africa johette.smuts@payprop.co.za linkedin.com/in/johettesmuts We also launched the PayProp Owner App, putting our clients another step ahead of their competitors with a great tool for landlords to view their rental portfolios. PAYPROP RENTAL INDEX ANNUAL REVIEW

5 As you ll see from the PayProp Annual Review for 2018, the market continued its gradual slowdown last year, although some provinces have started to see improvements. PAYPROP RENTAL INDEX ANNUAL REVIEW

6 National rent statistics BELOW-INFLATION RENTAL GROWTH Throughout 2018 we saw a continuation of the downward trend in national rental growth, trailing inflation for most of the year. In fact, the average monthly rental growth rate, measured year on year (YoY), halved, ending the period on 3.9%, compared to 6.4% in. The South African Reserve Bank forecasts that inflation will average around 5.5% in 2019, so it will likely continue to outstrip rental growth if current rental trends continue. However, judging from rental cycles in past years, we expect growth to recover somewhat during The average monthly rental growth rate, measured year on year, halved to 3.9%. PAYPROP RENTAL INDEX ANNUAL REVIEW

7 9% Rental growth (YoY) Inflation (YoY) 8% 7% 6% 5% 4% 5.1% 5.2% 4.5% 4.9% 4.6% 3% 2% 2.9% 3.0% 1% 2018 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sept Oct Nov Dec Weighted average national rental growth rate (YoY) vs. inflation and 2018 Source: PayProp PAYPROP RENTAL INDEX ANNUAL REVIEW

8 David Summerton Owner at Harcourts Summerton Processing with PayProp is far easier and less labour intensive than it was with our old system.

9 David got hours back every month with PayProp. And you can too. BOOK A FREE CONSULTATION TODAY

10 Provincial rent statistics PROVINCIAL STATISTICS 2018 In this section we compare provincial rent and credit metrics for Q to the same quarter in and the national average. First, let s have a look at the national picture: National statistics We ve noted increasing consumer and rental market pressure for some time, and it shows in the numbers. Nationally, rental growth slowed to 4.14% in the last quarter of 2018, vs. 5.39% over the same period in. Nevertheless, it was the first quarterly uptick in the rental growth rate in two years, and also the highest quarterly year-on-year growth for But whether or not it is the start of a slow recovery remains to be seen. Affordability ratio The affordability ratio is calculated by adding a tenant s monthly debt repayments to their monthly rent and expressing the total as a percentage of their net monthly income. The lower the affordability ratio, the higher the percentage of disposable income left to the tenant after costs. PAYPROP RENTAL INDEX ANNUAL REVIEW

11 Credit metrics Credit metrics are pulled from credit checks performed via the PayProp system. Note that we use net income figures provided to agents by tenants, and that this figure affects multiple ratios that we report on. At R7,610, the average national rent moved into a higher rental bracket in Q4, from the R5,000 R7,500 category to the R7,500 R10,000 category. The R5,000 R7,500 bracket is still the most populous in South Africa, comprising about a third of all rentals, and we don t expect this to change soon. Net income levels have stagnated, increasing by only 1.56% between Q4 and Q With rent and inflation increasing at higher rates, consumers are struggling to keep up. This only partly explains the YoY increase in tenants debt-to-income ratios in Q4, tenants paid R13,756 on their monthly debt repayments vs. R15,031 in Q The increase in debt-to-income ratios, in turn, affects affordability ratios. And as incomes have grown more slowly than rents, the slight increase in the rent-to-income ratio was to be expected. It was the first quarterly uptick in the rental growth rate in two years, and also the highest quarterly yearon-year growth for PAYPROP RENTAL INDEX ANNUAL REVIEW

12 Provincial rent statistics THE NATIONAL CONTEXT We ve noted increasing consumer and rental market pressure for some time, and it shows in the numbers. Average rent R7,610 R7,308 Rental growth 4.14% 5.39% Average income R33,037 R32,531 Average credit score PAYPROP RENTAL INDEX ANNUAL REVIEW

13 Debt-to-income ratio 45.5% 42.3% Rent-to-income ratio 28.9% 28.0% Affordability ratio 74.4% 70.2% Risky tenants 36.3% 35.3% 9% 8% 7% 6% 7.62% 6.86% 5.94% 5.39% 5% 4% 4.10% 3.92% 3.25% 4.14% 3% 2% 1% 2018 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Weighted average national rental growth rate and 2018 Source: PayProp PAYPROP RENTAL INDEX ANNUAL REVIEW

14 Provincial rent statistics EASTERN CAPE MIXED BLESSINGS Average income in this province is the lowest of all the provinces, but it is also the second cheapest province to rent in. PAYPROP RENTAL INDEX ANNUAL REVIEW

15 Rental growth 3.39% It is encouraging to see an increase in the Eastern Cape s rental growth rate from 2.54% in Q4 to 3.39% in the same quarter in 2018, but growth is still subdued in the province and below the national average of 4.14%. The Eastern Cape is one of two provinces where income fell year on year (YoY) (the other is North West). Average income in this province is the lowest of all the provinces, but as it is also the second cheapest province to rent in, the rent-to-income ratio has stayed below 30%, despite an increase from 28.7%. And while the debt-to-income ratio increased slightly, it is better than the national average. The fact that tenants in the Eastern Cape spend a smaller-thanaverage percentage of their net income on servicing debt has had a knock-on effect on its affordability ratio. At 73.1%, it is also better than the rest of the country (74.4%). PAYPROP RENTAL INDEX ANNUAL REVIEW

16 Provincial rent statistics EASTERN CAPE Tenants in the Eastern Cape spend a smaller-than-average percentage of their net income on servicing debt. Average rent R5,703 R5,516 Rental growth 3.39% 2.54% Worse than national average (R7,610) Worse than national average (4.14%) Average income R27,125 R28,330 Average credit score Worse than national average (R33,037) Worse than national average (634) PAYPROP RENTAL INDEX ANNUAL REVIEW

17 Debt-to-income ratio 43.7% 40.1% Rent-to-income ratio 29.5% 28.7% Better than national average (45.5%) Worse than national average (28.9%) Affordability ratio 73.1% 68.8% Risky tenants 45.4% 44.1% Better than national average (74.4%) Worse than national average (36.3%) PAYPROP RENTAL INDEX ANNUAL REVIEW

18 Provincial rent statistics FREE STATE GROWTH SPURT Free State tenants enjoy the second highest percentage of net income after paying their debt and rent. Rental growth 8.25% PAYPROP RENTAL INDEX ANNUAL REVIEW

19 The Free State has emerged as the growth story of Rental growth in the province increased significantly, from 2.35% year on year (YoY) in Q4 to 8.25% in Q the highest growth percentage out of all the provinces. Average net income also increased by 8.2% YoY from Q4 to the end of the period under review likewise the highest growth out of all the provinces. It is also one of only two provinces where the credit score improved during this time. There are other very encouraging statistics here as well the decrease in the debt-to-income ratio being the most noteworthy. With tenants spending a smaller percentage of their salaries on debt repayments, this has positively affected the affordability ratio in the province. That much is to be expected with a high percentage growth in income, but surprisingly, we also see a dip in the actual rand amount Free State tenants pay to service debt from R12,517 to R11,955 over the period. Compared to other provinces, the Free State has the second lowest rent-to-income ratio. Coupled with a lower-than-average debt-to-income ratio, this makes for an affordability ratio that is among South Africa s lowest (best). This means Free State tenants enjoy the second highest percentage of net income after paying their debt and rent. PAYPROP RENTAL INDEX ANNUAL REVIEW

20 Provincial rent statistics FREE STATE Coupled with a lower-than-average debt-to-income ratio, the Free State's low rent-to-income ratio makes for an affordability ratio that is among South Africa s lowest. Average rent R5,942 R5,490 Rental growth 8.25% 2.35% Worse than national average (R7,610) Better than national average (4.14%) Average income R31,796 R29,383 Average credit score Worse than national average (R33,037) Worse than national average (634) PAYPROP RENTAL INDEX ANNUAL REVIEW

21 Debt-to-income ratio 37.6% 42.6% Rent-to-income ratio 26.9% 24.8% Better than national average (45.5%) Better than national average (28.9%) Affordability ratio 64.5% 67.4% Risky tenants 37.7% 41.0% Better than national average (74.4%) Worse than national average (36.3%) PAYPROP RENTAL INDEX ANNUAL REVIEW

22 Rental growth 4.84% Provincial rent statistics GAUTENG SIGNS OF RECOVERY? The average Gauteng rent breached R8,000 for the first time in Q It was the province s first increase in quarterly growth in two years. PAYPROP RENTAL INDEX ANNUAL REVIEW

23 The average Gauteng rent breached R8,000 for the first time in Q This is 4.84% more than the year before and the third highest growth rate in the country for the quarter. While this rate was lower than the year before, it was the province s first increase in quarterly growth in two years, which might signal the beginning of a recovering rental market in the province. But before we get too excited about growth, let s balance the discussion out with a look at credit metrics. We saw a rise in the debt-to-income ratio in the province in addition to a slight decrease in the rent-to-income ratio. Both these scores are worse than the national average, which means the affordability ratio for Gauteng (75.9%) is also worse that the national average. Consequently, Gauteng tenants have less than a quarter of their net income left after paying debts and rent. Even so, the average credit score in the province is the same as the year before, at % 9.24% 9% 8% 7% 6% 5% 4% 3% 2% 1% 8.38% 7.85% 5.77% 3.80% 3.62% 3.58% % Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Year-on-year growth rates for Gauteng and 2018 Source: PayProp PAYPROP RENTAL INDEX ANNUAL REVIEW

24 Provincial rent statistics GAUTENG The affordability ratio for Gauteng (75.9%) is worse than the national average. Average rent R8,064 R7,692 Rental growth 4.84% 5.77% Better than national average (R7,610) Better than national average (4.14%) Average income R31,962 R30,327 Average credit score Worse than national average (R33,037) Worse than national average (634) PAYPROP RENTAL INDEX ANNUAL REVIEW

25 Debt-to-income ratio 46.3% 43.5% Rent-to-income ratio 29.6% 30.5% Worse than national average (45.5%) Worse than national average (28.9%) Affordability ratio 75.9% 74.0% Risky tenants 42.3% 41.0% Worse than national average (74.4%) Worse than national average (36.3%) PAYPROP RENTAL INDEX ANNUAL REVIEW

26 Provincial rent statistics KWAZULU-NATAL ON THE REBOUND Rentals grew faster than income in the province. PAYPROP RENTAL INDEX ANNUAL REVIEW

27 Rental growth 7.25% KwaZulu-Natal (KZN) achieved the second highest rental growth for Q4 2018, at 7.25%. This marks a good recovery from the low growth seen during. At current levels R8,129 rents in this province are the third highest in the country. While we see an increase in KZN tenants debt-to-income ratio (from 37.9% to 45.6% in Q4 2018), it s encouraging to see the percentage of risky tenants decreasing to 37.7% although it is still slightly higher than the national average of 36.3%. The average credit score stayed unchanged at 631 versus the year before, indicating that tenants are still managing their finances responsibly, even with higher levels of debt. We also saw a slight increase in the rent-to-income ratio to 30.4%, the highest in the country. This makes sense as rentals grew faster than income in the province. This increase, together with the increase in the debt-to-income ratio, means the affordability ratio increased (worsened) significantly to 76%, up from 65.8% a year before. PAYPROP RENTAL INDEX ANNUAL REVIEW

28 Provincial rent statistics KWAZULU-NATAL While we see an increase in KZN tenants debt-to-income ratio (from 37.9% to 45.6% in Q4 2018), it s encouraging to see the percentage of risky tenants decreasing to 37.7%. Average rent R8,129 R7,580 Rental growth 7.25% 5.29% Better than national average (R7,610) Better than national average (4.14%) Average income R33,954 R33,699 Average credit score Better than national average (R33,037) Worse than national average (634) PAYPROP RENTAL INDEX ANNUAL REVIEW

29 Debt-to-income ratio 45.6% 37.9% Rent-to-income ratio 30.4% 27.9% Worse than national average (45.5%) Worse than national average (28.9%) Affordability ratio 76.0% 65.8% Risky tenants 37.7% 38.4% Worse than national average (74.4%) Worse than national average (36.3%) 9% 8% 7% 7.31% 7.75% 6.47% 7.25% 6% 5% 5.29% 4% 3% 3.26% 2.87% 3.22% 2% 1% 2018 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Year-on-year growth rates for KwaZulu-Natal and 2018 Source: PayProp PAYPROP RENTAL INDEX ANNUAL REVIEW

30 Rental growth -4.01% Provincial rent statistics LIMPOPO NEGATIVE GROWTH The province suffered negative growth in all four quarters. PAYPROP RENTAL INDEX ANNUAL REVIEW

growth in all four quarters, causing its average rent to slip from R7,472 in Q4 to R7,173 a year later the worst rental performance of the provincial")

31 2018 came with the nearly unthinkable for Limpopo a reduction in rentals over the previous year. The province suffered negative year-on-year (YoY) growth in all four quarters, causing its average rent to slip from R7,472 in Q4 to R7,173 a year later the worst rental performance of the provincial markets. No, the graph is not upside down! 0% -1% -2% -3% -4% -5% -6% -7% % -5.24% -6.24% -4.01% Q1 Q2 Q3 Q4 Year-on-year growth rates for Limpopo in 2018 Source: PayProp But it s not all bad news. Lower rents in turn lowered the rentto-income ratio to 27.1%, resulting in a decrease (improvement) in tenants affordability ratio to 70.1% better than the national average. Limpopo tenants now have more of their income after paying their rent and monthly debt commitments, despite being the second lowest earners in the country. Notwithstanding this, the percentage of risky tenants in the province increased to 33.7% in Q4 2018, which is nonetheless still below the national average of 36.3%. PAYPROP RENTAL INDEX ANNUAL REVIEW

32 Provincial rent statistics LIMPOPO Lower rents lowered the rent-to-income ratio to 27.1%, resulting in a decrease in tenants affordability ratio to 70.1%. Average rent R7,173 R7,472 Rental growth -4.01% -2.12% Worse than national average (R7,610) Worse than national average (4.14%) Average income R28,457 R28,132 Average credit score Worse than national average (R33,037) Worse than national average (634) PAYPROP RENTAL INDEX ANNUAL REVIEW

33 Debt-to-income ratio 43.0% 44.0% Rent-to-income ratio 27.1% 33.2% Better than national average (45.5%) Better than national average (28.9%) Affordability ratio 70.1% 77.2% Risky tenants 33.7% 30.9% Better than national average (74.4%) Better than national average (36.3%) PAYPROP RENTAL INDEX ANNUAL REVIEW

34 Provincial rent statistics MPUMALANGA COMEBACK KID Income-wise, the province saw above-average growth. PAYPROP RENTAL INDEX ANNUAL REVIEW

35 Rental growth 4.74% 2018 was something of a comeback year for Mpumalanga. Between Q4 and Q4 2018, every measure but one improved. Income-wise, the province saw above-average growth. The average monthly salary in the province is now only about R1,000 less than the national average. The average credit score moreover improved by 5 points, but at 629 in Q4 2018, it is still below the national average (634). In addition, the increase in income measured in Q was largely responsible for an improvement in the debt-to-income ratio, but at 46.8% the ratio is still above the national average (and the highest in the country after North West). This, combined with a higher-than-average rent-to-income ratio, has affected the affordability ratio, which is currently at 76.5%. In a similar vein to the debt-to-income ratio, the affordability ratio is the second highest ratio seen in the country, after North West. Lastly, there has been a big improvement in the percentage of risky tenants, but at the current level of 42.4% it is still one of the highest in the country after the Northern and Eastern Cape. PAYPROP RENTAL INDEX ANNUAL REVIEW

36 Provincial rent statistics MPUMALANGA The average credit score improved by 5 points, but at 629 in Q4 2018, it is still below the national average (634). Average rent R7,248 R6,919 Rental growth 4.74% 1.62% Worse than national average (R7,610) Better than national average (4.14%) Average income R32,036 R29,724 Average credit score Worse than national average (R33,037) Worse than national average (634) PAYPROP RENTAL INDEX ANNUAL REVIEW

37 Debt-to-income ratio 46.8% 50.8% Rent-to-income ratio 29.7% 29.1% Worse than national average (45.5%) Worse than national average (28.9%) Affordability ratio 76.5% 79.9% Risky tenants 42.4% 48.2% Worse than national average (74.4%) Worse than national average (36.3%) PAYPROP RENTAL INDEX ANNUAL REVIEW

38 Provincial rent statistics NORTH WEST THE EXCEPTION THAT PROVES THE RULE The North West has the country s lowest rents, but because of the high debt-toincome ratio, it also has the worst affordability ratio, at 89.9%. While rent levels in the North West came to a standstill between Q4 and Q4 2018, the same can t be said for other metrics. A year ago, the province had the second highest average income after the Western Cape. But after a decrease in average income, it slumped to 5th place on the income ladder. The fall in earnings only partly explains the increase in the debt-to-income ratio from 54.3% to 67.8%. In Q4, North West tenants spent R18,965 per month on debt. This number increased by almost R2,700 in Q4 2018, to R21,639. Lower income levels not only affected the debt-to-income ratio, but also the rent-to-income ratio, pushing it up to 22.1%. The North West has the country s lowest rents, but because of the high debt-to-income ratio, it also has the worst affordability ratio, at 89.9%. Accompanying lower income levels, we note a decrease in the average credit score from 645 to 640 which is nevertheless still the country's highest. Rental growth -0.09% PAYPROP RENTAL INDEX ANNUAL REVIEW

39 Student housing As we know from previous indices, the North West is a bit of an anomaly because of the large proportion of student housing, credit checks are done on parents for student-level rents. This has the effect of throwing various credit metrics out of kilter for that region, ranging from credit scores, income and average age to debtand rent-to-income ratios. PAYPROP RENTAL INDEX ANNUAL REVIEW

40 Provincial rent statistics NORTH WEST The fall in earnings only partly explains the increase in the debt-to-income ratio from 54.3% to 67.8%. Average rent R4,986 R4,990 Rental growth -0.09% 8.57% Worse than national average (R7,610) Worse than national average (4.14%) Average income R31,917 R34,927 Average credit score Worse than national average (R33,037) Better than national average (634) PAYPROP RENTAL INDEX ANNUAL REVIEW

41 Debt-to-income ratio 67.8% 54.3% Rent-to-income ratio 22.1% 19.0% Worse than national average (45.5%) Better than national average (28.9%) Affordability ratio 89.9% 73.4% Risky tenants 30.4% 24.0% Worse than national average (74.4%) Better than national average (36.3%) PAYPROP RENTAL INDEX ANNUAL REVIEW

42 PAYPROP RENTAL INDEX ANNUAL REVIEW

43 Provincial rent statistics Rental growth -0.70% NORTHERN CAPE MOVING INTO NEGATIVE TERRITORY The province's rent-toincome ratio is the lowest in the country, and the same can be said about its affordability ratio. Between Q4 and Q4 2018, the Northern Cape experienced slightly negative rental growth of 0.7%. Even so, the region still has the second highest rents after the Western Cape at R8,153. Lower rent and higher income levels explain a decrease in the rent-to-income ratio, but it is great to also see a decrease in the debt-to-income ratio. At 35%, this metric is the lowest in the country, and the same can be said about the province s affordability ratio (62.3%). Unfortunately, we also measured a decrease in the average credit score, coupled with an increase in the percentage of high-risk tenants in the province, indicating that tenants are not managing their finances well. Factors such as sporadic payments and shortterm loans can have a big impact on credit scores. PAYPROP RENTAL INDEX ANNUAL REVIEW

44 Provincial rent statistics NORTHERN CAPE We also measured a decrease in the average credit score, coupled with an increase in the percentage of high-risk tenants. Average rent R8,153 R8,211 Rental growth -0.70% 7.90% Better than national average (R7,610) Worse than national average (4.14%) Average income R31,509 R30,683 Average credit score Worse than national average (R33,037) Worse than national average (634) PAYPROP RENTAL INDEX ANNUAL REVIEW

45 Debt-to-income ratio 35.0% 40.4% Rent-to-income ratio 27.3% 29.2% Better than national average (45.5%) Better than national average (28.9%) Affordability ratio 62.3% 69.6% Risky tenants 48.4% 45.7% Better than national average (74.4%) Worse than national average (36.3%) PAYPROP RENTAL INDEX ANNUAL REVIEW

46 Rental growth 3.96% Provincial rent statistics WESTERN CAPE HOW THINGS CHANGE 2018 yielded the lowest growth figures for the province since the launch of the Rental Index in PAYPROP RENTAL INDEX ANNUAL REVIEW

47 In its current situation, it s hard to believe that the Western Cape experienced four consecutive quarters of 10% year-on-year (YoY) growth in. By comparison, 2018 yielded the lowest growth figures for the province since the launch of the Rental Index in At its lowest point of the year, growth in the Cape slowed to just 3.96% in Q (The YoY figure for December was only 0.4%!) Even so, the average Western Cape rent surpassed the R9,000 mark during the year, still making it the most expensive province to live in with an average price differential of nearly R1,000 compared to the second most expensive province. But don t be too concerned for Western Cape tenants, as they are better off than most enjoying the highest income levels, second highest credit scores and featuring the lowest percentage of risky tenants. Because of high rents, the average rent-to-income ratio in the province is slightly higher than the national average, but that is offset by better-than-average debtto-income and affordability ratios. The average Cape tenant has 30% of their net income left after paying rent and debt obligations, which is the third best level out of all the provinces. When looking at long-term rental cycles, rental growth in the Fairest Cape could possibly start to pick up again towards the latter half of The average Cape tenant has 30% of their net income left after paying rent and debt-obligations. 12% 10% 10.26% 10.95% 10.16% 10.79% 8.86% 8% 6.97% 6% 5.20% 4% 3.96% 2% 2018 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Year-on-year growth rates for the Western Cape and 2018 Source: PayProp PAYPROP RENTAL INDEX ANNUAL REVIEW

48 WESTERN CAPE The average Western Cape rent surpassed the R9,000 mark during the year, still making it the most expensive province to live in. Average rent R9,124 R8,777 Rental growth 3.96% 10.79% Better than national ave (R7,610) Worse than national ave (4.14%) Average income R35,815 R35,080 Average credit score Better than national ave (R33,037) Better than national ave (634) PAYPROP RENTAL INDEX ANNUAL REVIEW

49 Debt-to-income ratio 40.2% 37.2% Rent-to-income ratio 29.8% 29.2% Better than national ave (45.5%) Worse than national ave (28.9%) Affordability ratio 70.0% 66.4% Risky tenants 29.2% 29.6% Better than national ave (74.4%) Better than national ave (36.3%) PAYPROP RENTAL INDEX ANNUAL REVIEW

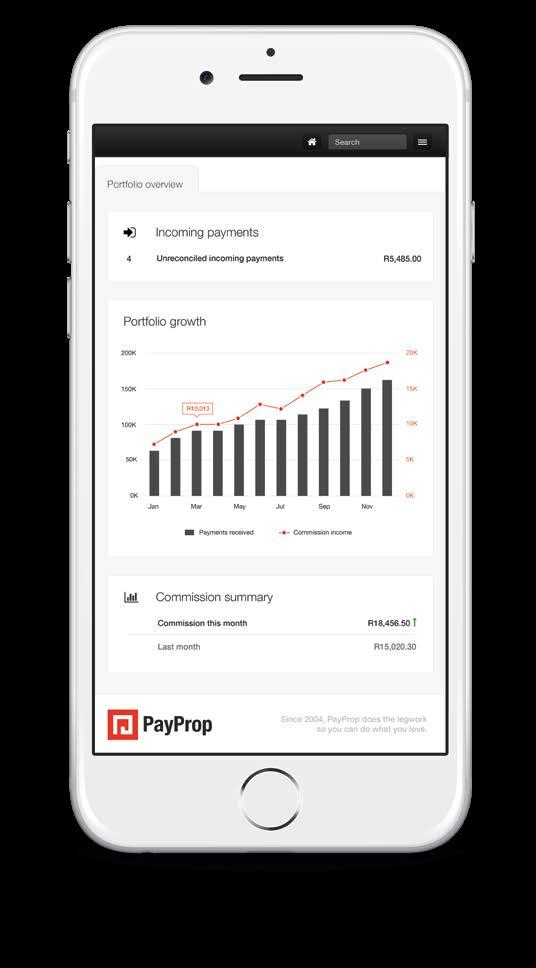

50 Automated payments and reconciliation AT YOUR FINGERTIPS

51

52 Risky business LOWEST-RISK RENTERS We see a correlation between a tenant s risk level (determined by their credit score) and the percentage of income they spend on rent. A widely accepted rule of thumb holds that a tenant shouldn t spend more than 30% of their net income on rent. Many tenants follow this rule to good effect, and many rental agents use it as a general measure of affordability. And while this figure was indeed just below 30% in the fourth quarter of 2018 (and had been, more or less, for two years), the true measure of appropriate rent-to-income levels is slightly more nuanced. In addition, we see a correlation between a tenant s risk level (determined by their credit score) and the percentage of income they spend on rent. PAYPROP RENTAL INDEX ANNUAL REVIEW

53 Generally speaking, financially savvy tenants, who have higher credit scores (and therefore lower risk ratings), spend less of their income on rent than high-risk and very high-risk tenants. The figure for lower-risk tenants is less than 30%, with the lowestrisk ones spending just 23% of their income on rent 20% less than the average tenant! On the other end of the spectrum, the riskiest tenants spend about 33% of their income on rent. Herein lies good advice for tenants looking to increase their credit scores rent a cheaper place and use the money you save to pay off your debts. In this way, you will reduce the portion of your income going on servicing your debts, and you ll lower your overall cost of living, making you less dependent on debt in the future. 32% 33% 28% 29% 29% 23% Minimum risk Low risk Average risk High risk Very high risk Average Rent-to-income ratios per risk category for the Western Cape and 2018 Source: PayProp PAYPROP RENTAL INDEX ANNUAL REVIEW

54 Better than the rest WHAT DOES LOW-RISK LOOK LIKE? The average age for minimum-risk tenants is 50, the highest average age for any risk category and more than 25% higher than the average age overall. PAYPROP RENTAL INDEX ANNUAL REVIEW

55 Minimum Low Average High Very high Average Average age per risk category Q Source: PayProp In the previous PayProp Rental Index, we saw that older tenants tend to have better credit scores and therefore pose lower risk to agents and landlords. The average age for minimum-risk tenants is 50, the highest average age for any risk category and more than 25% higher than the overall average age. This affirms the correlation between age and risk. But how big is the minimum-risk category? Our data shows that only 16% of tenants fall into this cohort. By contrast, 28% of tenants fall into the low-risk category, presenting a bigger opportunity to delve into what a low-risk tenant looks like and how they compare to tenants in other categories. While the ratios don t hold too many surprises, a few things are worth noting concerning rand values. Compared to the average tenant, low-risk tenants have higher incomes and average rent-to-income ratios but lower debt ratios which is seemingly the key. PAYPROP RENTAL INDEX ANNUAL REVIEW

56 36% 20% 16% 28% Percentage of tenants per risk category Source: PayProp Minimum risk Low risk Average risk High and very high risk Surprisingly, minimum-risk tenants have higher-thanaverage debt-to-income ratios. However, given the type of debt these older tenants usually have, the length of their payment history and their higher incomes, their credit ratings do not suffer as a result. When we convert these groups' debt ratios into rand amounts, we see a few interesting things: Minimumrisk tenants earn more than R10,000 per month more than low-risk tenants, but spend almost all of it on debt repayments. Low-risk tenants have the highest disposable income after debts and rent. Minimum-risk tenants have R11,445 left, while low-risk tenants are left with R11,763. Low-risk tenants spend the same amount of money on repaying debt as the average tenant (but slightly more on rent). The difference in disposable income is therefore mostly due to a difference in income. Again, we see that one of the easiest ways for tenants to improve their credit scores is to rent for cheaper and use the extra disposable income to repay debt. In the long run, cheaper rent lowers a tenant s cost of living and reliance on debt. Average tenant Low-risk tenant Minimum-risk tenant Age Credit score Rent-to-income ratio 29% 28% 23% Debt-to-income ratio 45.5% 40.6% 53.4% Affordability ratio 74.4% 68.2% 76.0% Net income R33, R37, R47, Rent in Rand R9, R10, R10, Debt in Rand R15, R15, R25, Disposable income R8, R11, R11, Average national credit metrics for selected risk categories 2018 Source: PayProp PAYPROP RENTAL INDEX ANNUAL REVIEW

57 In summary NOT ALL BAD NEWS 2018 was a tough economic year for businesses and consumers alike, and it shows in the numbers: We saw a continuation of the downward trend in rental growth, languishing below the inflation rate for most of the year. Q was the first quarter in two years to show an uptick in year-on-year growth, but whether that is the start of a recovery remains to be seen. Most provinces saw lower rental growth and a deterioration in the average tenant s financial situation from to Below-inflation income growth makes it harder to keep up with debt and other costs. We note a correlation between a tenant s risk level and the percentage of income they spend on rent a great tip for tenants who want to better their credit rating. We also saw that minimum-risk clients don t always have the lowest debt-to-income ratios, highlighting the importance of taking various credit metrics into account when vetting tenants. PAYPROP RENTAL INDEX ANNUAL REVIEW

58 PAYPROP RENTAL INDEX The PayProp Rental Index is a quarterly guide outlining trends in the South African residential rental market, and is compiled from transactional data collected by PayProp, the largest processor of residential letting transactions in South Africa. Contact details This publication was produced by PayProp South Africa. PayProp South Africa is operated under licence from Humanstate. PayProp and the PayProp logo are registered trademarks of Humanstate. For all business and media enquiries, please contact: Johette Smuts Head of Data and Analytics johette.smuts@payprop.co.za Tel: The PayProp Rental Index is available on the PayProp website at Join PayProp If you would like to know more about using PayProp to manage your rental portfolio, please visit: Disclaimer This document is intended as a basis for debate and discussion and should not be relied on as legal or professional advice. Whilst every reasonable effort has been made to ensure the accuracy of the contents, no warranty is made with regard to that content. PayProp accepts no responsibility for any errors or omissions. PayProp recommends you seek professional, legal or technical advice where necessary. PayProp cannot accept any liability for any loss or damage suffered by any person as a result of the editorial content, or by any person acting or refraining to act as a result of the material included. PAYPROP RENTAL INDEX ANNUAL REVIEW

59 PAYPROP RENTAL INDEX ANNUAL REVIEW

60 THE PAYPROP ROADSHOW PROTECT YOURSELF AGAINST CYBERCRIME MAY 2019 Durban Johannesburg Port Elizabeth Stellenbosch

IN REVIEW. Ups, downs and overdue change. You vs. your provincial average. Rental growth vs. the inflation rate

PAYPROP ACADEMY 2018 all about PropTech! ANNUAL REVIEW 2017 Ups, downs and overdue change You vs. your provincial average Rental growth vs. the inflation rate 2017 IN REVIEW Automated payments and reconciliation

PAYPROP ACADEMY 2018 all about PropTech! ANNUAL REVIEW 2017 Ups, downs and overdue change You vs. your provincial average Rental growth vs. the inflation rate 2017 IN REVIEW Automated payments and reconciliation

A comprehensive view of the state of the residential rental market in South Africa Q JAN - MAR

A comprehensive view of the state of the residential rental market in South Africa JAN - MAR PayProp Rental Index Quarterly The current downward trend in the South African economy appears to be taking

A comprehensive view of the state of the residential rental market in South Africa JAN - MAR PayProp Rental Index Quarterly The current downward trend in the South African economy appears to be taking

Western Cape rental market benefits from 'semigration'.

THE STATE OF THE RESIDENTIAL RENTAL MARKET IN SOUTH AFRICA THE HOLISTIC ISSUE MORE IS MORE! Q1 2017 JAN - MAR In this issue: Flat growth? Look again. The jury is out on tenant quality. Western Cape rental

THE STATE OF THE RESIDENTIAL RENTAL MARKET IN SOUTH AFRICA THE HOLISTIC ISSUE MORE IS MORE! Q1 2017 JAN - MAR In this issue: Flat growth? Look again. The jury is out on tenant quality. Western Cape rental

Knowledge is too important to leave in the hands of the bosses INFLATION MONITOR MARCH 2018

Knowledge is too important to leave in the hands of the bosses INFLATION MONITOR MARCH 2018 1 The Consumer Price Index (CPI) declined to 3.8% in March 2018 The term inflation means a sustained increase

Knowledge is too important to leave in the hands of the bosses INFLATION MONITOR MARCH 2018 1 The Consumer Price Index (CPI) declined to 3.8% in March 2018 The term inflation means a sustained increase

FNB PROPERTY MARKET ANALYTICS

1 June 21 FNB MAY HOUSE PRICE INDEX AND PROPERTY ECONOMIC REVIEW - Price growth acceleration continues, with expected peak believed to be nearing MARKET ANALYTICS JOHN LOOS: FNB HOME LOANS STRATEGIST 11-64912

1 June 21 FNB MAY HOUSE PRICE INDEX AND PROPERTY ECONOMIC REVIEW - Price growth acceleration continues, with expected peak believed to be nearing MARKET ANALYTICS JOHN LOOS: FNB HOME LOANS STRATEGIST 11-64912

LRS INFLATION MONITOR JANUARY 2015

LRS INFLATION MONITOR JANUARY 201 1 CPI SLOWED SLIGHTLY TO.% IN JANUARY 201 KEY FINDINGS Inflation measures how much more expensive a set of goods and services has become over a certain period, usually

LRS INFLATION MONITOR JANUARY 201 1 CPI SLOWED SLIGHTLY TO.% IN JANUARY 201 KEY FINDINGS Inflation measures how much more expensive a set of goods and services has become over a certain period, usually

1. Introduction 2. DOMESTIC ECONOMIC DEVELOPMENTS. 2.1 Economic performance in South Africa ISBN: SECOND QUARTER 2013

November 2013 ISBN: 978-1-920493-99-8 SECOND QUARTER 2013 1. Introduction The Quarterly Economic Update for the second quarter of 2013 (2Q2013) has been expanded and contains a range of new indicators.

November 2013 ISBN: 978-1-920493-99-8 SECOND QUARTER 2013 1. Introduction The Quarterly Economic Update for the second quarter of 2013 (2Q2013) has been expanded and contains a range of new indicators.

The status of performance management. Consolidated general report on the national and provincial audit outcomes

4 The status of performance management 57 4. Annual performance reports Figure 1 provides an overview of audit outcomes on the APRs, the APRs submitted with no material misstatements (red line) and the

4 The status of performance management 57 4. Annual performance reports Figure 1 provides an overview of audit outcomes on the APRs, the APRs submitted with no material misstatements (red line) and the

Public Opinion Monitor

The Public Opinion Monitor Reflecting the mood and attitudes of British people Growing economic confidence proves misplaced as Britain slips into double dip recession The TNS-BMRB Public Opinion Monitor

The Public Opinion Monitor Reflecting the mood and attitudes of British people Growing economic confidence proves misplaced as Britain slips into double dip recession The TNS-BMRB Public Opinion Monitor

Residential Property Indices. Date Published: March 2018

Residential Property Indices Date Published: March 2018 National Inflation Current annual inflation rate is 4.08% and monthly is 0.31% Market Review As at the end of February 2018 the national house price

Residential Property Indices Date Published: March 2018 National Inflation Current annual inflation rate is 4.08% and monthly is 0.31% Market Review As at the end of February 2018 the national house price

Foxtons Interim results presentation For the period ended June 2017

Foxtons Interim results presentation For the period ended June 2017 Important information This presentation includes statements that are, or may be deemed to be, forward-looking statements. These forward-looking

Foxtons Interim results presentation For the period ended June 2017 Important information This presentation includes statements that are, or may be deemed to be, forward-looking statements. These forward-looking

Residential Property Indices. Date Published: October 2018

Residential Property Indices Date Published: October 2018 National Inflation Current annual inflation rate is 3.77% and monthly is 0.25%. Market Review As at the end of September 2018 the national house

Residential Property Indices Date Published: October 2018 National Inflation Current annual inflation rate is 3.77% and monthly is 0.25%. Market Review As at the end of September 2018 the national house

Residential Property Indices. Date Published: July 2018

Residential Property Indices Date Published: July 2018 National Inflation Current annual inflation rate is 3.93% and monthly is 0.28% Market Review As at the end of June 2018 the national house price inflation

Residential Property Indices Date Published: July 2018 National Inflation Current annual inflation rate is 3.93% and monthly is 0.28% Market Review As at the end of June 2018 the national house price inflation

ECONOMIC GROWTH PROVINCIAL INTRODUCTION QUARTERLY DATA SERIES

ISSUE 7 OCTOBER 2016 PROVINCIAL QUARTERLY DATA SERIES ECONOMIC GROWTH INTRODUCTION The Quarterly Economic Review is a statistical release compiled by the Eastern Cape Socio Economic Consultative Council

ISSUE 7 OCTOBER 2016 PROVINCIAL QUARTERLY DATA SERIES ECONOMIC GROWTH INTRODUCTION The Quarterly Economic Review is a statistical release compiled by the Eastern Cape Socio Economic Consultative Council

Report for April 2017

Report for il 2017 Issued. 28, 2017 National Association of Credit Management Combined Sectors The big question circulating among those who try to read the economic tea leaves is whether reality or expectation

Report for il 2017 Issued. 28, 2017 National Association of Credit Management Combined Sectors The big question circulating among those who try to read the economic tea leaves is whether reality or expectation

Residential Property Indices. Date Published: February 2018

Residential Property Indices Date Published: February 2018 National Inflation Current annual inflation rate is 4.21% and monthly is 0.34% Market Review As at the end of January 2018 the national house

Residential Property Indices Date Published: February 2018 National Inflation Current annual inflation rate is 4.21% and monthly is 0.34% Market Review As at the end of January 2018 the national house

Residential Property Indices. Date Published: September 2018

Residential Property Indices Date Published: September 2018 National Inflation Current annual inflation rate is 3.85% and monthly is 0.27% Market Review As at the end of August 2018 the national house

Residential Property Indices Date Published: September 2018 National Inflation Current annual inflation rate is 3.85% and monthly is 0.27% Market Review As at the end of August 2018 the national house

1 February 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT. JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST

1 February 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST 087-328 0157

1 February 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST 087-328 0157

Biannual Economic and Capacity Survey. July December2017

Biannual Economic and Capacity Survey July December2017 1 Firm distribution based on Annual Turnover (based on responses received) July December 2017 Full survey Category by gross annual income % of firms

Biannual Economic and Capacity Survey July December2017 1 Firm distribution based on Annual Turnover (based on responses received) July December 2017 Full survey Category by gross annual income % of firms

South African SMME Business Confidence Index Report: 2nd Quarter 2014

ISSN 1811-5187 AFRICAGROWTH INSTITUTE Tel: (021) 914 6778 Fax: (021) 914 4438 www.africagrowth.com South African SMME Business Confidence Index Report: 2nd Quarter 2014 Compiled by: Africagrowth Institute

ISSN 1811-5187 AFRICAGROWTH INSTITUTE Tel: (021) 914 6778 Fax: (021) 914 4438 www.africagrowth.com South African SMME Business Confidence Index Report: 2nd Quarter 2014 Compiled by: Africagrowth Institute

South African SMME Business Confidence Index Report: 4th Quarter 2013

ISSN 1811-5187 AFRICAGROWTH INSTITUTE Tel: (021) 914 6778 Fax: (021) 914 4438 www.africagrowth.com South African SMME Business Confidence Index Report: 4th Quarter 13 Compiled by: Africagrowth Institute

ISSN 1811-5187 AFRICAGROWTH INSTITUTE Tel: (021) 914 6778 Fax: (021) 914 4438 www.africagrowth.com South African SMME Business Confidence Index Report: 4th Quarter 13 Compiled by: Africagrowth Institute

One in two Australians build savings amid concerns for the economy

ING DIRECT FINANCIAL WELLBEING INDEX Q2 2011 One in two Australians build savings amid concerns for the economy Households boost savings by an average of $313 each month. Australian households are tucking

ING DIRECT FINANCIAL WELLBEING INDEX Q2 2011 One in two Australians build savings amid concerns for the economy Households boost savings by an average of $313 each month. Australian households are tucking

Residential Property Indices. Date Published: August 2018

Residential Property Indices Date Published: August 2018 National Inflation Current annual inflation rate is 3.79% and monthly is 0.26% Market Review As at the end of July 2018 the national house price

Residential Property Indices Date Published: August 2018 National Inflation Current annual inflation rate is 3.79% and monthly is 0.26% Market Review As at the end of July 2018 the national house price

Report for November 2018

Report for ember 2018 Issued ember 30, 2018 National Association of Credit Management Combined Sectors It was not a big bounce back, but the good news is the data certainly didn t get any worse. This is

Report for ember 2018 Issued ember 30, 2018 National Association of Credit Management Combined Sectors It was not a big bounce back, but the good news is the data certainly didn t get any worse. This is

1 March 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT. JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST

1 March 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST 087-328 0157 tswanepoel@fnb.co.za

1 March 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST 087-328 0157 tswanepoel@fnb.co.za

KwaZulu-Natal Business Barometer

KwaZulu-Natal Business Barometer April 2014 Ex-Joshua Doore building 270 Jabu Ndlovu Street Pietermaritzburg Tel: +27 33 264 2500 Email: info@kznded.gov.za Web: www.kznded.gov.za Treasury House 145 Chief

KwaZulu-Natal Business Barometer April 2014 Ex-Joshua Doore building 270 Jabu Ndlovu Street Pietermaritzburg Tel: +27 33 264 2500 Email: info@kznded.gov.za Web: www.kznded.gov.za Treasury House 145 Chief

economic growth QUARTERLY DATA SERIES

ISSUE 8 December 2016 PROVINCIAL economic growth QUARTERLY DATA SERIES introduction The Quarterly Economic Review is a statistical release compiled by the Eastern Cape Socio Economic Consultative Council

ISSUE 8 December 2016 PROVINCIAL economic growth QUARTERLY DATA SERIES introduction The Quarterly Economic Review is a statistical release compiled by the Eastern Cape Socio Economic Consultative Council

Asda Income Tracker. Report: July 2016 Released: August Centre for Economics and Business Research ltd

Asda Income Tracker Report: July 2016 Released: August 2016 M a k i n g B u s i n e s s S e n s e Centre for Economics and Business Research ltd Unit 1, 4 Bath Street, London EC1V 9DX t 020 7324 2850 w

Asda Income Tracker Report: July 2016 Released: August 2016 M a k i n g B u s i n e s s S e n s e Centre for Economics and Business Research ltd Unit 1, 4 Bath Street, London EC1V 9DX t 020 7324 2850 w

First Quarter. January March 2016

First Quarter January March 2016 Highlights First quarter showed positive momentum for design industry. Design firms in March reported strong and accelerating business after a weak January and February.

First Quarter January March 2016 Highlights First quarter showed positive momentum for design industry. Design firms in March reported strong and accelerating business after a weak January and February.

Leumi Economic Weekly November 30, 2016

Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Leumi Economic Weekly November 30, 2016 The composite

Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Leumi Economic Weekly November 30, 2016 The composite

October 2018 Data Release

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

January 2019 Data Release

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

TBCSA FNB Tourism Business Index

TBCSA FNB Tourism Business Index 4 th Quarter 2012 Results and Outlook for the year 2013 Compiled by Grant Thornton Page 2 TBCSA FNB Tourism Business Index Introduction The Tourism Business Index ( TBI

TBCSA FNB Tourism Business Index 4 th Quarter 2012 Results and Outlook for the year 2013 Compiled by Grant Thornton Page 2 TBCSA FNB Tourism Business Index Introduction The Tourism Business Index ( TBI

Asda Income Tracker. Report: September 2015 Released: October Centre for Economics and Business Research ltd

Asda Income Tracker Report: September 2015 Released: October 2015 M a k i n g B u s i n e s s S e n s e Centre for Economics and Business Research ltd Unit 1, 4 Bath Street, London EC1V 9DX t 020 7324

Asda Income Tracker Report: September 2015 Released: October 2015 M a k i n g B u s i n e s s S e n s e Centre for Economics and Business Research ltd Unit 1, 4 Bath Street, London EC1V 9DX t 020 7324

Release date: 14 August 2018

Release date: 14 August 218 UK Finance: Mortgage Trends Update June 218 House purchase activity slows in June but remortgaging activity remains high Key data highlights: There were 34,9 new first-time

Release date: 14 August 218 UK Finance: Mortgage Trends Update June 218 House purchase activity slows in June but remortgaging activity remains high Key data highlights: There were 34,9 new first-time

PROPERTY BAROMETER FNB HOME BUYING ESTATE AGENT SURVEY RAND AREA

22 September 2015 FNB HOME LOANS: MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 John.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST

22 September 2015 FNB HOME LOANS: MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 John.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST

Why Cape Peninsula house prices are losing out

155 Chapter 15: Why Cape Peninsula house prices are losing out House prices during the third quarter of 2005 were still almost 20% higher than they were a year earlier. However, growth continued to lose

155 Chapter 15: Why Cape Peninsula house prices are losing out House prices during the third quarter of 2005 were still almost 20% higher than they were a year earlier. However, growth continued to lose

SME Monitor Q aldermore.co.uk

SME Monitor Q1 2014 aldermore.co.uk aldermore.co.uk Contents Executive summary UK economic overview SME inflation index one year review SME cost inflation trends SME business confidence SME credit conditions

SME Monitor Q1 2014 aldermore.co.uk aldermore.co.uk Contents Executive summary UK economic overview SME inflation index one year review SME cost inflation trends SME business confidence SME credit conditions

Portugal: GDP growth forecasts for 2018 reviewed upwards to 1.7%

13 March 217 ECONOMIC ANALYSIS Portugal: GDP growth forecasts for 218 reviewed upwards to 1.7% Myriam Montañez Growth of the Portuguese economy in 4Q16 reached.6% QoQ 1, once again causing positive surprise

13 March 217 ECONOMIC ANALYSIS Portugal: GDP growth forecasts for 218 reviewed upwards to 1.7% Myriam Montañez Growth of the Portuguese economy in 4Q16 reached.6% QoQ 1, once again causing positive surprise

Focus on Household and Economic Statistics. Insights from Stats SA publications. Nthambeleni Mukwevho Stats SA

Focus on Household and Economic Statistics Insights from Stats SA publications Nthambeleni Mukwevho Stats SA South African Population Results from CS 2016 Source: CS 2016 EC Household Results from CS 2016

Focus on Household and Economic Statistics Insights from Stats SA publications Nthambeleni Mukwevho Stats SA South African Population Results from CS 2016 Source: CS 2016 EC Household Results from CS 2016

January 2018 Data Release

January 2018 Data Release The Home Purchase Sentiment Index (HPSI) is a composite index designed to track consumers housing-related attitudes, intentions, and perceptions, using six questions from the

January 2018 Data Release The Home Purchase Sentiment Index (HPSI) is a composite index designed to track consumers housing-related attitudes, intentions, and perceptions, using six questions from the

Report for December 2018

Report for ember 2018 Issued ember 31, 2018 National Association of Credit Management Combined Sectors It can be tempting to read too much into the monthly changes that take place in the Credit Managers

Report for ember 2018 Issued ember 31, 2018 National Association of Credit Management Combined Sectors It can be tempting to read too much into the monthly changes that take place in the Credit Managers

The Money Statistics. December.

The Money Statistics December 2018 Welcome to the December 2018 edition of The Money Statistics, The Money Charity s monthly roundup of statistics about how we use money in the UK. If you have any questions,

The Money Statistics December 2018 Welcome to the December 2018 edition of The Money Statistics, The Money Charity s monthly roundup of statistics about how we use money in the UK. If you have any questions,

Asda Income Tracker. Report: June 2012 Released: July Centre for Economics and Business Research ltd

Asda Income Tracker Report: June 2012 Released: July 2012 M a k i n g B u s i n e s s S e n s e Centre for Economics and Business Research ltd Unit 1, 4 Bath Street, London EC1V 9DX t 020 7324 2850 w www.cebr.com

Asda Income Tracker Report: June 2012 Released: July 2012 M a k i n g B u s i n e s s S e n s e Centre for Economics and Business Research ltd Unit 1, 4 Bath Street, London EC1V 9DX t 020 7324 2850 w www.cebr.com

CONSTRUCTION MONITOR Supply & Demand Q1 2018

CONSTRUCTION MONITOR Supply & Demand Q1 218 CIDB CONSTRUCTION MONITOR SUPPLY AND DEMAND; APRIL 218 Revision 1 Acknowledgements: The support of Industry Insight in providing details of contracts awarded

CONSTRUCTION MONITOR Supply & Demand Q1 218 CIDB CONSTRUCTION MONITOR SUPPLY AND DEMAND; APRIL 218 Revision 1 Acknowledgements: The support of Industry Insight in providing details of contracts awarded

Part 1 Academic Reading 1

Contents Introduction How to Use This Book v Part 1 Academic Reading 1 Unit 1 About the Academic Reading Test 1 Unit 2 The Skills You Need 7 Unit 3 Multiple-choice Questions 14 Unit 4 True/False/Not Given

Contents Introduction How to Use This Book v Part 1 Academic Reading 1 Unit 1 About the Academic Reading Test 1 Unit 2 The Skills You Need 7 Unit 3 Multiple-choice Questions 14 Unit 4 True/False/Not Given

Asda Income Tracker. Report: March 2013 Released: April Centre for Economics and Business Research ltd

Asda Income Tracker Report: March 2013 Released: April 2013 M a k i n g B u s i n e s s S e n s e Centre for Economics and Business Research ltd Unit 1, 4 Bath Street, London EC1V 9DX t 020 7324 2850 w

Asda Income Tracker Report: March 2013 Released: April 2013 M a k i n g B u s i n e s s S e n s e Centre for Economics and Business Research ltd Unit 1, 4 Bath Street, London EC1V 9DX t 020 7324 2850 w

ECONOMIC COMMENTARY. Vehicle Sales. Economics South Africa. Total sales growth continues to points towards a rebound off a low base.

ECONOMIC COMMENTARY Economics South Africa 01 November 2017 Vehicle Sales Total sales growth continues to points towards a rebound off a low base Total new vehicle sales increased to 51 037 units in October,

ECONOMIC COMMENTARY Economics South Africa 01 November 2017 Vehicle Sales Total sales growth continues to points towards a rebound off a low base Total new vehicle sales increased to 51 037 units in October,

Improved Macroeconomic Conditions Boost Consumer Sentiment to Its Highest Level in 3½-Year

ECONOMIC REPORT Business & Consumer Confidence 17 April 2018 Improved Macroeconomic Conditions Boost Consumer Sentiment to Its Highest Level in 3½-Year MIER s CSI rebounded to 3.5-year high. Underpin by

ECONOMIC REPORT Business & Consumer Confidence 17 April 2018 Improved Macroeconomic Conditions Boost Consumer Sentiment to Its Highest Level in 3½-Year MIER s CSI rebounded to 3.5-year high. Underpin by

June 2018 Data Release

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

Report for August 2017

Report for ust 2017 Issued ust 31, 2017 National Association of Credit Management Combined Sectors At least the ride seems to have come to an end, but nobody really knows for how long. The data this month

Report for ust 2017 Issued ust 31, 2017 National Association of Credit Management Combined Sectors At least the ride seems to have come to an end, but nobody really knows for how long. The data this month

Experian Consumer Credit Default Index October 2017

Experian Consumer Credit Default Index October 2017 Index Page 1 Default Index Overview What is measures? Default Index Overview Experian Composite Consumer Default Index Page 2 Default Index Overview

Experian Consumer Credit Default Index October 2017 Index Page 1 Default Index Overview What is measures? Default Index Overview Experian Composite Consumer Default Index Page 2 Default Index Overview

Equity Release Market Report

Setting the standard in equity release Equity Release Market Report Spring 2015 2 Introduction The third edition of the Equity Release Market Report comes at a time when the continued success of the sector

Setting the standard in equity release Equity Release Market Report Spring 2015 2 Introduction The third edition of the Equity Release Market Report comes at a time when the continued success of the sector

Experian Consumer Credit Default Index. Monthly Update - March 2018

Experian Consumer Credit Default Index Monthly Update - March 2018 Index Page 1 Experian Consumer Default Index () Overview What it measures? Page 2 Experian Consumer Default Index Composite & Product

Experian Consumer Credit Default Index Monthly Update - March 2018 Index Page 1 Experian Consumer Default Index () Overview What it measures? Page 2 Experian Consumer Default Index Composite & Product

Foxtons Interim results presentation For the period ended 30 June 2018

Foxtons Interim results presentation For the period ended 30 June 2018 Important information This presentation includes statements that are, or may be deemed to be, forward-looking statements. These forward-looking

Foxtons Interim results presentation For the period ended 30 June 2018 Important information This presentation includes statements that are, or may be deemed to be, forward-looking statements. These forward-looking

Mortgage Trends Update

Mortgage Trends Update UK Finance: Mortgage Trends Update December 218 of first-time reaches 12-year high in 218 Key data highlights: There were 37, new first-time buyer mortgages completed in 218, some

Mortgage Trends Update UK Finance: Mortgage Trends Update December 218 of first-time reaches 12-year high in 218 Key data highlights: There were 37, new first-time buyer mortgages completed in 218, some

BROLL RETAIL BAROMETER

BROLL RETAIL BAROMETER MAXIMISING PROPERTY POTENTIAL www.broll.co.za Review of Fourth Quarter 2011 RESEARCH Key facts Prime shopping centres Gross rentals Cap rates Vacancies Prime high street Gross rentals

BROLL RETAIL BAROMETER MAXIMISING PROPERTY POTENTIAL www.broll.co.za Review of Fourth Quarter 2011 RESEARCH Key facts Prime shopping centres Gross rentals Cap rates Vacancies Prime high street Gross rentals

Asda Income Tracker. Report: December 2015 Released: January Centre for Economics and Business Research ltd

Asda Income Tracker Report: December 2015 Released: January 2016 M a k i n g B u s i n e s s S e n s e Centre for Economics and Business Research ltd Unit 1, 4 Bath Street, London EC1V 9DX t 020 7324 2850

Asda Income Tracker Report: December 2015 Released: January 2016 M a k i n g B u s i n e s s S e n s e Centre for Economics and Business Research ltd Unit 1, 4 Bath Street, London EC1V 9DX t 020 7324 2850

Home Loans. Housing review Fourth quarter 2016

Home Loans Contents Economic overview 2 Household sector overview 2 Property sector overview House prices Building costs Land values 7 Affordability of housing 7 Outlook 7 Graphs 9 Statistics 11 Compiled

Home Loans Contents Economic overview 2 Household sector overview 2 Property sector overview House prices Building costs Land values 7 Affordability of housing 7 Outlook 7 Graphs 9 Statistics 11 Compiled

BDO MONTHLY BUSINESS TRENDS INDICES April Copyright BDO LLP. All rights reserved.

BDO MONTHLY BUSINESS TRENDS INDICES April 2017 Copyright BDO LLP. All rights reserved. INTRODUCTION The BDO Monthly Trends Indices are polls of polls that pull together the results of all the main UK business

BDO MONTHLY BUSINESS TRENDS INDICES April 2017 Copyright BDO LLP. All rights reserved. INTRODUCTION The BDO Monthly Trends Indices are polls of polls that pull together the results of all the main UK business

Underwriting, Metrics, and Credit Scoring That Reduce Losses

Underwriting, Metrics, and Credit Scoring That Reduce Losses Presentation to Innovate 2012 Monday, September 17, 2012 Part One Ken Shilson, CPA President, Subprime Analytics Booth # 132 2180 North Loop

Underwriting, Metrics, and Credit Scoring That Reduce Losses Presentation to Innovate 2012 Monday, September 17, 2012 Part One Ken Shilson, CPA President, Subprime Analytics Booth # 132 2180 North Loop

Release date: 16 May 2018

Release date: 16 May 218 UK Finance: Mortgage Trends Update March 218 Remortgaging market softens in March after busy start to year Key data highlights: There was 51bn of new lending to first-time in the

Release date: 16 May 218 UK Finance: Mortgage Trends Update March 218 Remortgaging market softens in March after busy start to year Key data highlights: There was 51bn of new lending to first-time in the

LETTER. economic COULD INTEREST RATES HEAD UP IN 2015? JANUARY Canada. United States. Interest rates. Oil price. Canadian dollar.

economic LETTER JANUARY 215 COULD INTEREST RATES HEAD UP IN 215? For six years now, that is, since the financial crisis that shook the world in 28, Canadian interest rates have stayed low. The key interest

economic LETTER JANUARY 215 COULD INTEREST RATES HEAD UP IN 215? For six years now, that is, since the financial crisis that shook the world in 28, Canadian interest rates have stayed low. The key interest

Premium Drivers. A quarterly motor insurance savings index by comparethemarket.com

Premium Drivers A quarterly motor insurance savings index by comparethemarket.com December 2015 Introduction Motor insurance headlines have made for fairly grim reading in the last few months. Premiums

Premium Drivers A quarterly motor insurance savings index by comparethemarket.com December 2015 Introduction Motor insurance headlines have made for fairly grim reading in the last few months. Premiums

New Hampshire Medicaid Program Enrollment Forecast SFY Update

New Hampshire Medicaid Program Enrollment Forecast SFY 2011-2013 Update University of New Hampshire Whittemore School of Business and Economics Ross Gittell, James R Carter Professor Matt Magnusson, M.B.A.

New Hampshire Medicaid Program Enrollment Forecast SFY 2011-2013 Update University of New Hampshire Whittemore School of Business and Economics Ross Gittell, James R Carter Professor Matt Magnusson, M.B.A.

Experian Consumer Credit Default Index. Monthly Update - April 2018

Experian Consumer Credit Default Index Monthly Update - April 2018 Index Page 1 Experian Consumer Default Index () Overview What it measures? Page 2 Experian Consumer Default Index Composite & Product

Experian Consumer Credit Default Index Monthly Update - April 2018 Index Page 1 Experian Consumer Default Index () Overview What it measures? Page 2 Experian Consumer Default Index Composite & Product

April 2018 Data Release

April 2018 Data Release The Home Purchase Sentiment Index (HPSI) is a composite index designed to track consumers housing-related attitudes, intentions, and perceptions, using six questions from the National

April 2018 Data Release The Home Purchase Sentiment Index (HPSI) is a composite index designed to track consumers housing-related attitudes, intentions, and perceptions, using six questions from the National

LETTER. economic. The price of oil and prices at the pump: why the difference? NOVEMBER bdc.ca

economic LETTER NOVEMBER 211 The price of oil and prices at the pump: why the difference? Since the end of April the price of crude oil based on the West Texas Intermediate (WTI) benchmark has dropped

economic LETTER NOVEMBER 211 The price of oil and prices at the pump: why the difference? Since the end of April the price of crude oil based on the West Texas Intermediate (WTI) benchmark has dropped

Home Loan Rates. RBNZ OCR cut triggers a mortgage rate drop. 22 June 2015

Home Loan Rates 22 June 201 RBNZ OCR cut triggers a mortgage rate drop The RBNZ cut the OCR by 2bp in June, and we expect another cut will soon follow. Influential global interest rates remain low, but

Home Loan Rates 22 June 201 RBNZ OCR cut triggers a mortgage rate drop The RBNZ cut the OCR by 2bp in June, and we expect another cut will soon follow. Influential global interest rates remain low, but

South African SMME Business Confidence Index Report: 1st Quarter 2016

ISSN 1811-5187 AFRICAGROWTH INSTITUTE Tel: (021) 914 6778 Fax: (021) 914 4438 www.africagrowth.com South African SMME Business Confidence Index Report: 1st Quarter 2016 Compiled by: Africagrowth Institute

ISSN 1811-5187 AFRICAGROWTH INSTITUTE Tel: (021) 914 6778 Fax: (021) 914 4438 www.africagrowth.com South African SMME Business Confidence Index Report: 1st Quarter 2016 Compiled by: Africagrowth Institute

MORTGAGE AND CONSUMER CREDIT TRENDS National Report Q2 2018

HOUSING INDICATORS AND ANALYTICS MORTGAGE AND CONSUMER CREDIT TRENDS National Report Q2 2018 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N December 2018 Executive summary The year-over-year

HOUSING INDICATORS AND ANALYTICS MORTGAGE AND CONSUMER CREDIT TRENDS National Report Q2 2018 C A N A D A M O R T G A G E A N D H O U S I N G C O R P O R A T I O N December 2018 Executive summary The year-over-year

Experian Consumer Credit Default Index. Monthly Update - January 2018

Experian Consumer Credit Default Index Monthly Update - January 2018 Index Page 1 Experian Consumer Default Index () Overview What is measures? Page 2 Experian Consumer Default Index Composite & Product

Experian Consumer Credit Default Index Monthly Update - January 2018 Index Page 1 Experian Consumer Default Index () Overview What is measures? Page 2 Experian Consumer Default Index Composite & Product

Australian Business Expectations Survey

Australian Business Expectations Survey Dun & Bradstreet Q4 2017 PRELIMINARY RESULTS RELEASED 1 AUGUST 2017 Index UPLIFT IN BUSINESS SENTIMENT Australian businesses are looking ahead to the final quarter

Australian Business Expectations Survey Dun & Bradstreet Q4 2017 PRELIMINARY RESULTS RELEASED 1 AUGUST 2017 Index UPLIFT IN BUSINESS SENTIMENT Australian businesses are looking ahead to the final quarter

HKU announces 2014 Q4 HK Macroeconomic Forecast

Press Release October 8, 2014 HKU announces 2014 Q4 HK Macroeconomic Forecast Hong Kong Economic Outlook The APEC Studies Programme of the Hong Kong Institute of Economics and Business Strategy at the

Press Release October 8, 2014 HKU announces 2014 Q4 HK Macroeconomic Forecast Hong Kong Economic Outlook The APEC Studies Programme of the Hong Kong Institute of Economics and Business Strategy at the

GDP Forecast Revised Due to Weak Global Outlook

5 July 2016 MONTHLY ECONOMIC REVIEW Jun 2016 GDP Forecast Revised Due to Weak Global Outlook Exports were down by 0.9%yoy in May, while trade balance moderated to RM3.2 billion. This was largely due to

5 July 2016 MONTHLY ECONOMIC REVIEW Jun 2016 GDP Forecast Revised Due to Weak Global Outlook Exports were down by 0.9%yoy in May, while trade balance moderated to RM3.2 billion. This was largely due to

Report for November 2017

Report for ember 2017 Issued ember 30, 2017 National Association of Credit Management Combined Sectors That old familiar pattern has returned after a couple of months where we seemed to be heading for

Report for ember 2017 Issued ember 30, 2017 National Association of Credit Management Combined Sectors That old familiar pattern has returned after a couple of months where we seemed to be heading for

Who cares about regional data?

Who cares about regional data? Development happens somewhere - in a spatial locality. Aggregations hide [important] variety in the data Within South Africa: KwaZulu-Natal is not like the Western Cape Within

Who cares about regional data? Development happens somewhere - in a spatial locality. Aggregations hide [important] variety in the data Within South Africa: KwaZulu-Natal is not like the Western Cape Within

RESIDENTIAL MARKET COMMENTARY

A Cushman & Wakefield Insight Publication RESIDENTIAL MARKET COMMENTARY September 2017 Economic Overview ECONOMIC OVERVIEW September s MPC meeting witnessed a clear shift in sentiment amongst members regarding

A Cushman & Wakefield Insight Publication RESIDENTIAL MARKET COMMENTARY September 2017 Economic Overview ECONOMIC OVERVIEW September s MPC meeting witnessed a clear shift in sentiment amongst members regarding

Survey of Residential Landlords

Survey of Residential Landlords Fourth Quarter 2014 REPORT O M Carey Jones 5 Henshaw Lane, Yeadon, Leeds, LS19 7RW Telephone: 0113 250 6411 CONTENTS Page 1. INTRODUCTION & BACKGROUND 4 2. METHODOLOGY 5

Survey of Residential Landlords Fourth Quarter 2014 REPORT O M Carey Jones 5 Henshaw Lane, Yeadon, Leeds, LS19 7RW Telephone: 0113 250 6411 CONTENTS Page 1. INTRODUCTION & BACKGROUND 4 2. METHODOLOGY 5

Choosing a Cell Phone Plan-Verizon Investigating Linear Equations

Choosing a Cell Phone Plan-Verizon Investigating Linear Equations I n 2008, Verizon offered the following cell phone plans to consumers. (Source: www.verizon.com) Verizon: Nationwide Basic Monthly Anytime

Choosing a Cell Phone Plan-Verizon Investigating Linear Equations I n 2008, Verizon offered the following cell phone plans to consumers. (Source: www.verizon.com) Verizon: Nationwide Basic Monthly Anytime

ECFIN/C-1 Fourth quarter 2000

ECFIN/C-1 Fourth quarter 2000 ECFIN/44/4/00-EN This document exists in English only. European Communities, 2001. MAIN FEATURES During the fourth quarter of 2000, the euro appreciated against the US dollar,

ECFIN/C-1 Fourth quarter 2000 ECFIN/44/4/00-EN This document exists in English only. European Communities, 2001. MAIN FEATURES During the fourth quarter of 2000, the euro appreciated against the US dollar,

Eurozone. Economic Watch FEBRUARY 2017

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Presentation to the Select Committee on Appropriations COMMUNITY LIBRARY SERVICES GRANT. 25 May 2011

Presentation to the Select Committee on Appropriations COMMUNITY LIBRARY SERVICES GRANT 25 May 2011 Community Library Services Grant 31 December 2010 Table: Community Library Services Grant expenditure

Presentation to the Select Committee on Appropriations COMMUNITY LIBRARY SERVICES GRANT 25 May 2011 Community Library Services Grant 31 December 2010 Table: Community Library Services Grant expenditure

Statistical release P0141

Statistical release Consumer Price Index September 2010 Embargoed until: 27 October 2010 11:30 Enquiries: Forthcoming issue: Expected release date User information services October 2010 24 November 2010

Statistical release Consumer Price Index September 2010 Embargoed until: 27 October 2010 11:30 Enquiries: Forthcoming issue: Expected release date User information services October 2010 24 November 2010

Economic activity gathers pace

Produced by the Economic Research Unit October 2014 A quarterly analysis of trends in the Irish economy Economic activity gathers pace Positive data flow Recovery broadening out GDP growth revised up to

Produced by the Economic Research Unit October 2014 A quarterly analysis of trends in the Irish economy Economic activity gathers pace Positive data flow Recovery broadening out GDP growth revised up to

MLS Sales vs. Listings (seasonaly adjusted)

") QUARTER 4: Canada Guaranty Housing Market Review OCTOBER - DECEMBER 21 The Canadian economy posted positive indicators of growth in early 21; however, the optimistic sentiment deteriorated in the latter

QUARTER 4: Canada Guaranty Housing Market Review OCTOBER - DECEMBER 21 The Canadian economy posted positive indicators of growth in early 21; however, the optimistic sentiment deteriorated in the latter

Public Opinion Monitor

The Public Opinion Monitor Reflecting the mood and attitudes of British people Signs of growing optimism over personal income as unemployment falls. The TNS-BMRB Public Opinion Monitor tracks public attitudes

The Public Opinion Monitor Reflecting the mood and attitudes of British people Signs of growing optimism over personal income as unemployment falls. The TNS-BMRB Public Opinion Monitor tracks public attitudes

October 2016 Data Release

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

Home Loans. Housing review First quarter 2016

Home Loans Contents Economic overview Household sector overview Property sector overview House prices Building costs Land values Affordability of housing Outlook 7 Graphs 9 Statistics 11 Compiled by Jacques

Home Loans Contents Economic overview Household sector overview Property sector overview House prices Building costs Land values Affordability of housing Outlook 7 Graphs 9 Statistics 11 Compiled by Jacques

ARLA Survey of Residential Investment Landlords

Prepared for The Association of Residential Letting Agents ARLA Survey of Residential Investment Landlords June 2012 Prepared by O M Carey Jones 5 Henshaw Lane, Yeadon, Leeds, LS19 7RW June 2012 CONTENTS

Prepared for The Association of Residential Letting Agents ARLA Survey of Residential Investment Landlords June 2012 Prepared by O M Carey Jones 5 Henshaw Lane, Yeadon, Leeds, LS19 7RW June 2012 CONTENTS

Commercial Banking Performance 1st Quarter 2017

Commercial Banking Performance 1st Quarter 2017 Lackluster results with continued weak loan and deposit growth as well as a small decline in ROA Overall 1Q17 Results: Commercial earnings rose by 1. versus

Commercial Banking Performance 1st Quarter 2017 Lackluster results with continued weak loan and deposit growth as well as a small decline in ROA Overall 1Q17 Results: Commercial earnings rose by 1. versus

ARLA Survey of Residential Investment Landlords

Prepared for The Association of Residential Letting Agents ARLA Survey of Residential Investment Landlords March 2013 Prepared by O M Carey Jones 5 Henshaw Lane, Yeadon, Leeds, LS19 7RW March 2013 CONTENTS

Prepared for The Association of Residential Letting Agents ARLA Survey of Residential Investment Landlords March 2013 Prepared by O M Carey Jones 5 Henshaw Lane, Yeadon, Leeds, LS19 7RW March 2013 CONTENTS

Weekly Market Commentary

LPL FINANCIAL RESEARCH Weekly Market Commentary November 18, 2014 Emerging Markets Opportunity Still Emerging Burt White Chief Investment Officer LPL Financial Jeffrey Buchbinder, CFA Market Strategist

LPL FINANCIAL RESEARCH Weekly Market Commentary November 18, 2014 Emerging Markets Opportunity Still Emerging Burt White Chief Investment Officer LPL Financial Jeffrey Buchbinder, CFA Market Strategist

BANKING SECTOR. Rationale for report: Banking statistics for January 2017

BANKING SECTOR Sector Report 2 March 2017 Kelvin Ong,CFA kelvin-ong@ambankgroup.com 03-20362294 Higher deposit growth with stronger CASA momentum Rationale for report: Banking statistics for January 2017

BANKING SECTOR Sector Report 2 March 2017 Kelvin Ong,CFA kelvin-ong@ambankgroup.com 03-20362294 Higher deposit growth with stronger CASA momentum Rationale for report: Banking statistics for January 2017

DEVELOPMENTS IN THE COST COMPETITIVENESS OF THE EUROPEAN UNION, THE UNITED STATES AND JAPAN MAIN FEATURES

DEVELOPMENTS IN THE COST COMPETITIVENESS OF THE EUROPEAN UNION, THE UNITED STATES AND JAPAN MAIN FEATURES The euro against major international currencies: During the second quarter of 2000, the US dollar,

DEVELOPMENTS IN THE COST COMPETITIVENESS OF THE EUROPEAN UNION, THE UNITED STATES AND JAPAN MAIN FEATURES The euro against major international currencies: During the second quarter of 2000, the US dollar,

LABOUR MARKET PROVINCIAL 54.3 % 45.7 % Unemployed Discouraged work-seekers % 71.4 % QUARTERLY DATA SERIES

QUARTERLY DATA SERIES ISSUE 6 October 2016 PROVINCIAL LABOUR MARKET introduction introduction The Eastern Cape Quarterly Review of Labour Markets is a statistical release compiled by the Eastern Cape Socio