Accounting systems OPERATION OF AN ACCOUNTING SYSTEM. Converting data to information. Chapter 7. 3 basic phases. Input. Processing.

|

|

|

- Scot Morton

- 5 years ago

- Views:

Transcription

1 Chapter 7 Accounting systems PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd OPERATION OF AN ACCOUNTING SYSTEM 3 basic phases Input Source documents entered into journals Processing Journals posted to general ledger Output Financial statements 2 Converting data to information Business Transactions Source documents Journals Ledgers Reports Interested Parties 3 1

2 DEVELOPMENT OF AN ACCOUNTING SYSTEM Systems analysis Understanding information requirements and sources of information Systems implementation and review Implementing systems, training staff, preparing accounting manual, test-runs, evaluation and review Systems design Determining personnel requirements, source documents, accounting records and procedures, reports and reports format 4 Important considerations in developing an accounting system Must give consideration to: Cost versus benefits Compatibility Flexibility and adaptability Internal control 5 INTERNAL CONTROL SYSTEMS Efficient use and protection of an entity s asset is a primary management function All procedures adopted by an entity to control its activities and protect its assets are described collectively as an internal control system 6 2

3 Principles of internal control systems Clearly established lines of responsibility Separation of record keeping and custodianship Division of responsibility for related transactions Mechanical and electronic devices Adequate insurance Internal auditing Programming controls Physical controls Other controls 7 Limitations of internal control systems Absolute assurance not possible Effectiveness influenced by size of entity s operations Good controls can break down due to tiredness, indifference or carelessness Heavy reliance on segregation of duties Difficulties in detecting computer fraud 8 MANUAL ACCOUNTING SYSTEMS SUBSIDIARY LEDGERS Control accounts and subsidiary ledgers Summary information Control account Detailed information Subsidiary ledger Accounts receivable Accounts payable Inventory 9 3

4 General Ledger Accounts Receivable Control Date Debit Credit Balance Nov Nov Nov Schedule of Accounts Receivable as at 30 November P. Able $1 800 R. Baker D. Cane 500 $4 700 Subsidiary Ledger P. Able Date Debit Credit Balance Nov Nov Nov Subsidiary Ledger R. Baker Date Debit Credit Balance Nov Nov Nov Subsidiary Ledger D. Cane Date Debit Credit Balance Nov Nov Nov MANUAL ACCOUNTING SYSTEMS SPECIAL JOURNALS General journal inefficient where there are many transactions Group like transactions and record in a special purpose journal credit sales sales journal credit purchases purchases journal cash receipts cash receipts journal cash payments cash payments journal 11 Sales journal Records only credit sales of inventory Total posted to general ledger monthly Detail (by debtor) posted to subsidiary ledger daily Advantages Each transaction recorded on a single line Entries do not require a narration Posting efficiency achieved 12 4

5 Sales journal continued Sales Journal Invoice Post GST A/C Date no. Account Ref. Sales Collections Receivable Jan R Abbot D Ball N Camp R Abbot A Evans J Ford A Evans N Camp Purchases journal Records only credit purchases Can be used for items other than inventory Total posted to general ledger monthly Detail (by debtor) posted to subsidiary ledger daily Advantages as for sales journal 14 Purchases journal continued Purchases Journal Date Date of Post GST A/Cs Record Invoice Account Terms Ref. Purchases Outlays Payable Jan 3 Jan 2 Kirby Ltd n/ Jan 4 Risk Ltd n/ Jan 8 Dunn Supply n/ Jan 12 Dunn Supply n/ Jan 18 CSR Ltd 2/10, n/ Jan 24 Cooper Ltd 2/10, n/ Jan 26 Risk Ltd 2/10, n/ Jan 29 CSR Ltd n/

6 Cash receipts journal Records all receipts of cash Records each receipt and total banked Totals posted to general ledger monthly Detail (debtors only) posted to subsidiary ledger daily Columns set up for common receipts 16 Cash payments journal Records all payments of cash Records each payment and cheque number Totals posted to general ledger monthly Detail (creditors only) posted to subsidiary ledger daily Columns set up for common payments 17 Use of the general journal Generally inefficient Used for Infrequent transactions Adjusting entries Closing entries Reversing entries Correcting entries 18 6

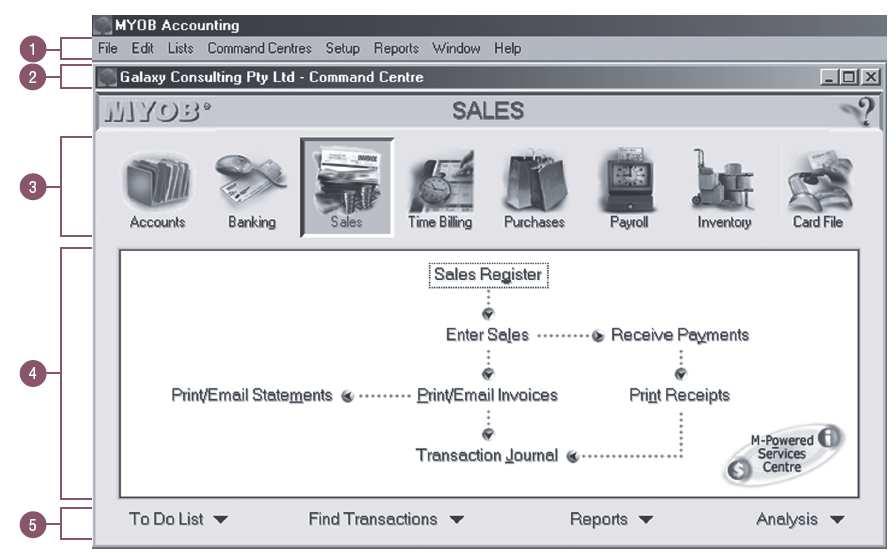

7 Other Issues Abnormal balances in subsidiary ledgers Credit balances in accounts receivable Debit balances in accounts payable Account set-offs Buying and selling from same customer/supplier Need legal right to set-off 19 Accounting Software Electronic spreadsheets Excel, Lotus 123 General ledger programs ACCPAC, Attache, MYOB, QuickBooks, Sybiz Data input obtained from source documents Output produced by the program 20 When advising a client on adopting a computerised accounting system, what criteria should be considered? 21 7

8 22 An Introduction to MYOB 23 An Introduction to QuickBooks 24 8

9 COMPUTERISED ACCOUNTING Advantages Reduction in processing costs Speed of processing Error reduction Automatic posting Automatic production of documents and reports Improved reporting and decision making Faster response time 25 COMPUTERISED ACCOUNTING continued Disadvantages Failed systems Power failure Viruses Hackers Fraud

2/10/2009. The accounting ACCOUNTING TRANSACTIONS AND EVENTS. Analysing transactions. Chapter 2

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

Receivables TYPES OF RECEIVABLES. Chapter 12. Accounts receivable Bills receivable Other receivables

Chapter 12 Receivables PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd TYPES OF RECEIVABLES Accounts receivable Bills receivable Other receivables

Chapter 12 Receivables PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd TYPES OF RECEIVABLES Accounts receivable Bills receivable Other receivables

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 4 Recording Transactions Chapter 3 - Recording Transactions Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this week s study,

ACC100 Introduction to Accounting Week 4 Recording Transactions Chapter 3 - Recording Transactions Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this week s study,

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

2/18/2009. Reporting and THE CORPORATE FORM OF ORGANISATION. Characteristics of a corporation. Chapter 10. A corporation:

Chapter 10 Reporting and analysing equity PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE CORPORATE FORM OF ORGANISATION A corporation: Is created

Chapter 10 Reporting and analysing equity PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE CORPORATE FORM OF ORGANISATION A corporation: Is created

ACCOUNTING. Written examination 1

Victorian Certificate of Education ACCOUNTING Written examination 1 Tuesday 10 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

Victorian Certificate of Education ACCOUNTING Written examination 1 Tuesday 10 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

Analysis and interpretation of financial statements

Chapter 19 Analysis and interpretation of financial statements PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd SOURCES OF FINANCIAL INFORMATION Financial

Chapter 19 Analysis and interpretation of financial statements PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd SOURCES OF FINANCIAL INFORMATION Financial

Grade XI Accountancy. (Important Concepts) #GrowWithGreen

#GrowWithGreen") Grade XI Accountancy (Important Concepts) #GrowWithGreen Financial Accounting [Part-I] Chapter 1 (Introduction to Accounting) 1. Difference between Book-Keeping, Accounting and Accountancy 2. Users of

Grade XI Accountancy (Important Concepts) #GrowWithGreen Financial Accounting [Part-I] Chapter 1 (Introduction to Accounting) 1. Difference between Book-Keeping, Accounting and Accountancy 2. Users of

Partnerships: formation, operation and reporting

Chapter 08 Partnerships: formation, operation and reporting PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd PARTNERSHIP DEFINED Partnership Act: The

Chapter 08 Partnerships: formation, operation and reporting PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd PARTNERSHIP DEFINED Partnership Act: The

Perriam & Partners Ltd Chartered Accountants & Business Advisors

Perriam & Partners Ltd Chartered Accountants & Business Advisors 2015 SUPPLEMENTARY TRUST QUESTIONNAIRE NAME: E-MAIL ADDRESS: CONTACT PERSON: HOME PHONE NUMBER: CELLPHONE NUMBER: ADDRESS: AUTHORITY AND

Perriam & Partners Ltd Chartered Accountants & Business Advisors 2015 SUPPLEMENTARY TRUST QUESTIONNAIRE NAME: E-MAIL ADDRESS: CONTACT PERSON: HOME PHONE NUMBER: CELLPHONE NUMBER: ADDRESS: AUTHORITY AND

Accounting Building Business Skills. Learning Objectives. Learning Objectives. Paul D. Kimmel. Chapter Seven: Internal Control, Cash and Receivables

Accounting Building Business Skills Paul D. Kimmel Chapter Seven: Internal Control, Cash and Receivables PowerPoint presentation by Christine Langridge Swinburne University of Technology, Lilydale 2003

Accounting Building Business Skills Paul D. Kimmel Chapter Seven: Internal Control, Cash and Receivables PowerPoint presentation by Christine Langridge Swinburne University of Technology, Lilydale 2003

Accounting with MYOB Accounting Plus v18. Chapter Four Accounts Payable

Accounting with MYOB Accounting Plus v18 Chapter Four Accounts Payable Recording a Purchase Important Points A Purchase is obtaining goods for re-sale. Purchases are obtained from Suppliers. Amounts owed

Accounting with MYOB Accounting Plus v18 Chapter Four Accounts Payable Recording a Purchase Important Points A Purchase is obtaining goods for re-sale. Purchases are obtained from Suppliers. Amounts owed

Class: XI Subject: ACCOUNTANCY. NO OF PERIOD Unit-1 (25 periods) LEARNING OUTCOMES

LEARNING OUTCOMES") Unit-1 (25 CH-1. Introduction to Accounting - Project on Accounting: objectives, advantages and International limitations, types of accounting information; Accounting users of accounting information and

Unit-1 (25 CH-1. Introduction to Accounting - Project on Accounting: objectives, advantages and International limitations, types of accounting information; Accounting users of accounting information and

2007 VCE VET Financial Services GA 2: Written examination

2007 VCE VET Financial Services GA 2: Written examination GENERAL COMMENTS Students were well prepared for the 2007 VCE VET Financial Services examination. They are reminded to attempt each question and

2007 VCE VET Financial Services GA 2: Written examination GENERAL COMMENTS Students were well prepared for the 2007 VCE VET Financial Services examination. They are reminded to attempt each question and

Part 5: GLOSSARY OF TERMS

Part 5: GLOSSARY OF TERMS ABN Withholding Tax Account Levels Accounts Accounting Equation Accounts List Accounts Payable Accounts Receivable Accounting Period The amount withheld from a supplier who provides

Part 5: GLOSSARY OF TERMS ABN Withholding Tax Account Levels Accounts Accounting Equation Accounts List Accounts Payable Accounts Receivable Accounting Period The amount withheld from a supplier who provides

Fundamentals of Accounting Resources

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Grade XI Accountancy. (Mock Test) #GrowWithGreen

#GrowWithGreen") Grade XI Accountancy (Mock Test) #GrowWithGreen Q.1 What is GST? [1 mark] Q.2 Write any one limitation of Single Entry System. [1 mark] Q.3 Which of the following alternatives is an example of profit for

Grade XI Accountancy (Mock Test) #GrowWithGreen Q.1 What is GST? [1 mark] Q.2 Write any one limitation of Single Entry System. [1 mark] Q.3 Which of the following alternatives is an example of profit for

Process Map. McIntosh and Son. Administration Module. Process Code: A310 Bank Statement Processing

Process Map McIntosh and Son Administration Module Process Code: A310 2 Contents High Level Process Definition... 3 Process Flowchart... 4... 4 Dishonoured Deposit Entry... 5 Cancelled Cheque Entry...

Process Map McIntosh and Son Administration Module Process Code: A310 2 Contents High Level Process Definition... 3 Process Flowchart... 4... 4 Dishonoured Deposit Entry... 5 Cancelled Cheque Entry...

HCSS Accounting. User Manual. Journals and Corrections

HCSS Accounting User Manual Journals and Corrections Contents 1 Journals... 3 a View Journals... 3 b Cash Book Journal (including Balance Sheet Codes)... 5 c VAT Reimbursement... 7 d VAT Payment... 8 e

HCSS Accounting User Manual Journals and Corrections Contents 1 Journals... 3 a View Journals... 3 b Cash Book Journal (including Balance Sheet Codes)... 5 c VAT Reimbursement... 7 d VAT Payment... 8 e

Activity 1: Transactions

Activity 1: Transactions Prepare the general journal entries to record the following transactions for the business for the month of May 2016 (ignore GST): May 1 Owner deposited $50,000 of his own money

Activity 1: Transactions Prepare the general journal entries to record the following transactions for the business for the month of May 2016 (ignore GST): May 1 Owner deposited $50,000 of his own money

SAMPLE COURSE OUTLINE ACCOUNTING AND FINANCE GENERAL YEAR 12

SAMPLE COURSE OUTLINE ACCOUNTING AND FINANCE GENERAL YEAR 12 Copyright School Curriculum and Standards Authority, 2018 This document apart from any third party copyright material contained in it may be

SAMPLE COURSE OUTLINE ACCOUNTING AND FINANCE GENERAL YEAR 12 Copyright School Curriculum and Standards Authority, 2018 This document apart from any third party copyright material contained in it may be

Adjusting The Accounts

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

Chapter 5. Control Accounts. Notes to teachers

Chapter 5 Control Accounts Notes to teachers 1 Start with Chapters 3 and 4 of Frank Wood s Introduction to Accounting and briefly explain to students the basic principles of recording in the books and

Chapter 5 Control Accounts Notes to teachers 1 Start with Chapters 3 and 4 of Frank Wood s Introduction to Accounting and briefly explain to students the basic principles of recording in the books and

How to Journalize using Data Entry

Steps Essential to Success 1. Print a copy of the Problem you intend to complete. To do so, go to the software log-in page and click on Download Student Manual button, click on the Problem to open it.

Steps Essential to Success 1. Print a copy of the Problem you intend to complete. To do so, go to the software log-in page and click on Download Student Manual button, click on the Problem to open it.

Grade XI. Accountancy. (Important Concepts) #GrowWithGreen

#GrowWithGreen") Grade XI Accountancy (Important Concepts) #GrowWithGreen Financial Accounting [Part-I] Chapter 1 (Introduction to Accounting) 1. Difference between Book-Keeping, Accounting and Accountancy 2. Users of

Grade XI Accountancy (Important Concepts) #GrowWithGreen Financial Accounting [Part-I] Chapter 1 (Introduction to Accounting) 1. Difference between Book-Keeping, Accounting and Accountancy 2. Users of

Mark Scheme (Results) June International GCSE Accounting (4AC0)

June International GCSE Accounting (4AC0)") Scheme (Results) June 2014 International GCSE Accounting (4AC0) Edexcel and BTEC Qualifications Edexcel and BTEC qualifications come from Pearson, the world s leading learning company. We provide a wide

Scheme (Results) June 2014 International GCSE Accounting (4AC0) Edexcel and BTEC Qualifications Edexcel and BTEC qualifications come from Pearson, the world s leading learning company. We provide a wide

Dawood Public School Course Outline Principles of Accounts Class IX

Dawood Public School Course Outline 2017-18 Principles of Accounts Class IX Cambridge O level Principles of Accounts Syllabus Code 7110 Course Books: 1. Wood, Frank, Business Accounting, FT Pitman Publishers

Dawood Public School Course Outline 2017-18 Principles of Accounts Class IX Cambridge O level Principles of Accounts Syllabus Code 7110 Course Books: 1. Wood, Frank, Business Accounting, FT Pitman Publishers

ACCOUNTING. Written examination 1. Tuesday 9 June 2009

Victorian Certificate of Education ACCOUNTING Written examination 1 Tuesday 9 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

Victorian Certificate of Education ACCOUNTING Written examination 1 Tuesday 9 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

2011 BUSINESS QUESTIONNAIRE

Business Name: Financial Year Ended: Contact Person: Fax Number: 2011 BUSINESS QUESTIONNAIRE 31 March 2011 Phone Number: Email Address: Please answer all questions below. If "yes" please complete the relevant

Business Name: Financial Year Ended: Contact Person: Fax Number: 2011 BUSINESS QUESTIONNAIRE 31 March 2011 Phone Number: Email Address: Please answer all questions below. If "yes" please complete the relevant

Accounting with MYOB v18. Chapter Three Cash Accounting

Accounting with MYOB v18 Chapter Three Cash Accounting Cash Accounting Activities 1. Receive and pay money using Banking. 2. Create and use Recurring Templates. 3. Combine receipts for banking. 4. Identify

Accounting with MYOB v18 Chapter Three Cash Accounting Cash Accounting Activities 1. Receive and pay money using Banking. 2. Create and use Recurring Templates. 3. Combine receipts for banking. 4. Identify

Accounting with MYOB v18. Chapter Five Accounts Receivable

Accounting with MYOB v18 Chapter Five Accounts Receivable Recording a Sale Important Points A Sale is the supply of goods or services to Customers in the normal course of business. Amounts owed by these

Accounting with MYOB v18 Chapter Five Accounts Receivable Recording a Sale Important Points A Sale is the supply of goods or services to Customers in the normal course of business. Amounts owed by these

Accountings Summary OUTLINE

Accountings Summary OUTLINE 1. Accounting and Business Environment 2. Recording Business Transaction 3. The Adjusting Process 4. Completing the Accounting Cycle 5. Merchandising Operations 6. Accounting

Accountings Summary OUTLINE 1. Accounting and Business Environment 2. Recording Business Transaction 3. The Adjusting Process 4. Completing the Accounting Cycle 5. Merchandising Operations 6. Accounting

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Topic notes 7: General Ledger

Topic notes 7: General Ledger Balance Day Adjustments 1. Accrued Expense 2. Prepaid Expense 3. Accrued Income 4. Income Received in Advance 5. Bad Debts & Doubtful Debts 6. Depreciation 7. Leave Entitlements

Topic notes 7: General Ledger Balance Day Adjustments 1. Accrued Expense 2. Prepaid Expense 3. Accrued Income 4. Income Received in Advance 5. Bad Debts & Doubtful Debts 6. Depreciation 7. Leave Entitlements

The General Journal and the General Ledger

chapter College Accounting The General Journal and the General Ledger 11 th Edition 3 1 Learning Objectives After you have completed this chapter, you will be able to do the following: 3 2 The General

chapter College Accounting The General Journal and the General Ledger 11 th Edition 3 1 Learning Objectives After you have completed this chapter, you will be able to do the following: 3 2 The General

2/2/2009. Financial statement EARNING POWER AND IRREGULAR ITEMS. EARNING POWER AND IRREGULAR ITEMS continued. Chapter 14

Chapter 14 Financial statement analysis PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd EARNING POWER AND IRREGULAR ITEMS Earning power refers to

Chapter 14 Financial statement analysis PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd EARNING POWER AND IRREGULAR ITEMS Earning power refers to

Week 4/5, Chap 4. The General Journal and the General Ledger. Instructor: Michael Booth

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

1 What Accounting Systems have you used during this financial year? - A complete computerised accounting package (e.g. MYOB)? 1A

? 1A") Perriam & Partners Ltd Chartered Accountants & Business Advisors 2018 BUSINESS QUESTIONNAIRE BUSINESS NAME: E-MAIL ADDRESS: CONTACT PERSON: HOME PHONE NO: MOBILE NO: ADDRESS: AUTHORITY AND TERMS OF ENGAGEMENT

Perriam & Partners Ltd Chartered Accountants & Business Advisors 2018 BUSINESS QUESTIONNAIRE BUSINESS NAME: E-MAIL ADDRESS: CONTACT PERSON: HOME PHONE NO: MOBILE NO: ADDRESS: AUTHORITY AND TERMS OF ENGAGEMENT

CHAPTER 23 Evaluating Firm Performance

Part 6 Understanding What the Numbers Mean CHAPTER 23 Evaluating Firm Performance Longenecker Moore Petty Palich 2008 Cengage Learning. All rights reserved. PowerPoint Presentation by Charlie Cook The

Part 6 Understanding What the Numbers Mean CHAPTER 23 Evaluating Firm Performance Longenecker Moore Petty Palich 2008 Cengage Learning. All rights reserved. PowerPoint Presentation by Charlie Cook The

Adjusting the Accounts

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

Trial Balance. Format of Trial Balance. The under mention points may be noted for preparing a trial balance.

Trial Balance All the businessmen after completion of posting from journal or subsidiary books to the ledger want to verify the accuracy of the posting. For this purpose, our statement is prepared wherein

Trial Balance All the businessmen after completion of posting from journal or subsidiary books to the ledger want to verify the accuracy of the posting. For this purpose, our statement is prepared wherein

IAB LEVEL 2 CERTIFICATE IN MANUAL AND COMPUTERISED BOOKKEEPING (QCF)

") CONTENTS IAB LEVEL 2 CERTIFICATE IN MANUAL AND COMPUTERISED BOOKKEEPING (QCF) Qualification Accreditation Number 601/3789/7 (Accreditation review date 31 st December 2016) QUALIFICATION SPECIFICATION Introduction

CONTENTS IAB LEVEL 2 CERTIFICATE IN MANUAL AND COMPUTERISED BOOKKEEPING (QCF) Qualification Accreditation Number 601/3789/7 (Accreditation review date 31 st December 2016) QUALIFICATION SPECIFICATION Introduction

Week 5, Chap 4 Part 1

Slide 1 Week 5, Chap 4 Part 1 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal and the General Ledger The General Journal Section Objectives 1. Record transactions

Slide 1 Week 5, Chap 4 Part 1 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal and the General Ledger The General Journal Section Objectives 1. Record transactions

IAB LEVEL 2 CERTIFICATE IN APPLIED BOOKKEEPING (QCF)

") IAB LEVEL 2 CERTIFICATE IN APPLIED BOOKKEEPING (QCF) Qualification Accreditation Number 500/9262/5 (Accreditation end date 31 st December 2012) CONTENTS QUALIFICATION SPECIFICATION 1. Introduction 2. Aims

IAB LEVEL 2 CERTIFICATE IN APPLIED BOOKKEEPING (QCF) Qualification Accreditation Number 500/9262/5 (Accreditation end date 31 st December 2012) CONTENTS QUALIFICATION SPECIFICATION 1. Introduction 2. Aims

Process Map. McIntosh and Son. Administration Module. Process Code: A120 Creditors General Ledger Cheque Entry

Process Map McIntosh and Son Administration Module Process Code: A120 Creditors General Ledger Cheque Entry 2 Contents High Level Process Definition... 3 Process Flowchart... 4 Business Policies... 5 General

Process Map McIntosh and Son Administration Module Process Code: A120 Creditors General Ledger Cheque Entry 2 Contents High Level Process Definition... 3 Process Flowchart... 4 Business Policies... 5 General

LEDGER. MODULE - 1 Basic Accounting. Ledger. Notes

6 LEDGER You have learnt that business transactions are recorded in various special purpose books and journal proper. The accounting process does not stop here. The transactions are recorded in number

6 LEDGER You have learnt that business transactions are recorded in various special purpose books and journal proper. The accounting process does not stop here. The transactions are recorded in number

A Guide to Month-end & Year-end Accounting

A Guide to Month-end & Year-end Accounting Version 2015.2 Page 1 Contents Structure of Xebra Accounting After you have reconciled all your Bank Accounts: Reports - General Ledger Balance - Accrual Basis

A Guide to Month-end & Year-end Accounting Version 2015.2 Page 1 Contents Structure of Xebra Accounting After you have reconciled all your Bank Accounts: Reports - General Ledger Balance - Accrual Basis

Chapter 5. Solution 5.1. Donncha O Donoghue 1

Chapter 5 Solution 5.1 Distinguish between books of original entry and ledger accounts The books of original entry ( day books or journals ) are the books in which transactions are first recorded and are

Chapter 5 Solution 5.1 Distinguish between books of original entry and ledger accounts The books of original entry ( day books or journals ) are the books in which transactions are first recorded and are

Script Reference. Complete the monthly REC1 Description & Objectives

Title Complete the monthly REC1 Description & Objectives Script Reference FMS REC1 Schools are required to complete the monthly REC1 to reconcile bank statements and FMS. Script Name Date Comments Created

Title Complete the monthly REC1 Description & Objectives Script Reference FMS REC1 Schools are required to complete the monthly REC1 to reconcile bank statements and FMS. Script Name Date Comments Created

Index. Assets (continued) scrapping or disposal trading-in Auditing Profession Act 26 of

scrapping or disposal trading-in Auditing Profession Act 26 of") Index A Accounts balancing... 61 incomplete records... 369 Accounting balancing an account... 61 basic accounting equation... 27 cycle... 130 definition... 4, 13 developments... 5 domains... 14 function...

Index A Accounts balancing... 61 incomplete records... 369 Accounting balancing an account... 61 basic accounting equation... 27 cycle... 130 definition... 4, 13 developments... 5 domains... 14 function...

PANCHAKSHARI S PROFESSIONAL ACADEMY PVT LTD (Your Lifelong Knowledge Partner )

") 50 Questions 50 Marks 60 Minutes Rectification of Error Select the best choice to answer the following questions: 1. Which of the following statement is/are correct? (i) A separate suspense account should

50 Questions 50 Marks 60 Minutes Rectification of Error Select the best choice to answer the following questions: 1. Which of the following statement is/are correct? (i) A separate suspense account should

QuickBooks Pro Manual

QuickBooks Pro Manual for Development Organisations Fifth version prepared December 2009 for users of QuickBooks Pro 2006. For limited circulation within Mango and selected NGOs (further information from

QuickBooks Pro Manual for Development Organisations Fifth version prepared December 2009 for users of QuickBooks Pro 2006. For limited circulation within Mango and selected NGOs (further information from

Performing of Financial Accounting Controls

Advanced Financial Accounting [AA21] Supplementary for Chapter 01 Performing of Financial Accounting Controls The syllabus content from 1.6 to chapter 01 is changed and included in this supplementary.

Advanced Financial Accounting [AA21] Supplementary for Chapter 01 Performing of Financial Accounting Controls The syllabus content from 1.6 to chapter 01 is changed and included in this supplementary.

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

ANNUAL BUSINESS QUESTIONNAIRE

Business Information Questionnaire Nexia New Zealand ANNUAL BUSINESS QUESTIONNAIRE Taxpayer Name: Financial Year Ended: Contact Person: Email Address: Phone Number: Fax Number: It is a requirement of Inland

Business Information Questionnaire Nexia New Zealand ANNUAL BUSINESS QUESTIONNAIRE Taxpayer Name: Financial Year Ended: Contact Person: Email Address: Phone Number: Fax Number: It is a requirement of Inland

EOY: Financials and Accountant

Institute of Certified Bookkeepers Making you Count EOY: Financials and Accountant ICB Technical Webinar Series 28 th July 2015 Institute of Certified Bookkeepers Making you Count Your presenters Deborah

Institute of Certified Bookkeepers Making you Count EOY: Financials and Accountant ICB Technical Webinar Series 28 th July 2015 Institute of Certified Bookkeepers Making you Count Your presenters Deborah

Sage UBS Accounting Sample Report. Sage UBS Accounting. Sample Report 1.0. VIVID SOLUTIONS SDN BHD

Sage UBS Accounting Sample Report 1.0 www.vivid.com.my 1 Contents Chapter 1: Debtors... 6 1.1: Chart of Account... 6 1.2: Tax Code Maintenance... 6 1.3: Debtors Listing... 7 1.4: Print Labels... 7 1.5:

Sage UBS Accounting Sample Report 1.0 www.vivid.com.my 1 Contents Chapter 1: Debtors... 6 1.1: Chart of Account... 6 1.2: Tax Code Maintenance... 6 1.3: Debtors Listing... 7 1.4: Print Labels... 7 1.5:

CHAPTER 3 Selected Solutions. The Accounting Information System. Brief Topics Questions Exercises Exercises Problems

CHAPTER 3 Selected Solutions The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Brief Topics Questions Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5,

CHAPTER 3 Selected Solutions The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Brief Topics Questions Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5,

2018 VCE Accounting examination report

General comments The Accounting examination consisted of eight questions, with most containing several parts. One graph was presented for interpretation in. There was also one discuss question, where students

General comments The Accounting examination consisted of eight questions, with most containing several parts. One graph was presented for interpretation in. There was also one discuss question, where students

IPMA-HR Chapter &Region Accounting Manual

IPMA-HR Chapter &Region Accounting Manual Issued July 2014 1 P age Basic Financial Statements As Chapter/Region Treasurer you will be generally be concerned with two basic financial statements: balance

IPMA-HR Chapter &Region Accounting Manual Issued July 2014 1 P age Basic Financial Statements As Chapter/Region Treasurer you will be generally be concerned with two basic financial statements: balance

Adjusting the Accounts

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

Reconciling GST and Preparing your BAS. Webinar

Reconciling GST and Preparing your BAS Webinar INTRODUCTION INTRODUCTION Webinar manual Specific learning objectives Cover new concepts using PowerPoint and MYOB AccountRight demonstrations Questions are

Reconciling GST and Preparing your BAS Webinar INTRODUCTION INTRODUCTION Webinar manual Specific learning objectives Cover new concepts using PowerPoint and MYOB AccountRight demonstrations Questions are

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

Computerised Accounting

Preface Computerised Accounting using MYOB Accounting v18 This workbook has been written to cover Cash Book, General Ledger, Accounts Receivable and Accounts Payable information on how to use MYOB Accounting,

Preface Computerised Accounting using MYOB Accounting v18 This workbook has been written to cover Cash Book, General Ledger, Accounts Receivable and Accounts Payable information on how to use MYOB Accounting,

Cashflow Management & Forecasting Module

Cashflow Management & Forecasting Module Introduction The careful management of your cashflow is fundamental to managing your business, especially in these more difficult economic times. Depending on your

Cashflow Management & Forecasting Module Introduction The careful management of your cashflow is fundamental to managing your business, especially in these more difficult economic times. Depending on your

Award in Computerised Accounting Skills

Award in Computerised Accounting Skills ASE20055 Level 3 Time allowed: 3 hours Instructions You should read through the assignment carefully before you begin. You must attempt all tasks in the order given.

Award in Computerised Accounting Skills ASE20055 Level 3 Time allowed: 3 hours Instructions You should read through the assignment carefully before you begin. You must attempt all tasks in the order given.

ACCOUNTING. Written examination 2. Thursday 8 November 2007

Victorian CertiÞcate of Education 2007 ACCOUNTING Written examination 2 Thursday 8 November 2007 Reading time: 11.45 am to 12.00 noon (15 minutes) Writing time: 12.00 noon to 1.30 pm (1 hour 30 minutes)

Victorian CertiÞcate of Education 2007 ACCOUNTING Written examination 2 Thursday 8 November 2007 Reading time: 11.45 am to 12.00 noon (15 minutes) Writing time: 12.00 noon to 1.30 pm (1 hour 30 minutes)

Once the financial position of a business is determined in the form of a balance sheet, there is a need to record it in permanent form.

Opening Entries Once the financial position of a business is determined in the form of a balance sheet, there is a need to record it in permanent form. The journal is the book of original entry. The journal

Opening Entries Once the financial position of a business is determined in the form of a balance sheet, there is a need to record it in permanent form. The journal is the book of original entry. The journal

ACCOUNTING ACC1 Unit 1 Financial Accounting: The Accounting Information System You will need no other materials. Instructions all Information ACC1

Surname Other Names For Examiner s Use Centre Number Candidate Number Candidate Signature General Certifi cate of Education June 2008 Advanced Subsidiary Examination ACCOUNTING ACC1 Unit 1 Financial Accounting:

Surname Other Names For Examiner s Use Centre Number Candidate Number Candidate Signature General Certifi cate of Education June 2008 Advanced Subsidiary Examination ACCOUNTING ACC1 Unit 1 Financial Accounting:

Financial procedures manual

Contents Introduction... 2 Finance authorisation procedure... 2 Bank account procedure... 3 Petty cash procedure... 4 Use of business credit card procedure... 5 New supplier procedure... 6 New customer

Contents Introduction... 2 Finance authorisation procedure... 2 Bank account procedure... 3 Petty cash procedure... 4 Use of business credit card procedure... 5 New supplier procedure... 6 New customer

Institute of Certified Bookkeepers

Making you count Institute of Certified Bookkeepers Level II Certificate in Bookkeeping Syllabus from April 2014 1 Level II Certificate in Bookkeeping from April 2014 Course Code L2C Introduction Level

Making you count Institute of Certified Bookkeepers Level II Certificate in Bookkeeping Syllabus from April 2014 1 Level II Certificate in Bookkeeping from April 2014 Course Code L2C Introduction Level

INTERMEDIATE EXAMINATION GROUP - I (SYLLABUS 2016)

") INTERMEDIATE EXAMINATION GROUP - I (SYLLABUS 2016) SUGGESTED ANSWERS TO QUESTIONS JUNE - 2017 Paper - 5 : FINANCIAL ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right

INTERMEDIATE EXAMINATION GROUP - I (SYLLABUS 2016) SUGGESTED ANSWERS TO QUESTIONS JUNE - 2017 Paper - 5 : FINANCIAL ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right

CHAPTER3 Adjusting the Accounts

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

Chapter # 9. Correction of Errors. Principles of Accounting XI. Sameer Hussain.

Correction of Errors Principles of Accounting XI Chapter contents Correction of errors. Errors where trial balance still balances: o Error of omission. o Error of commission. o Error of principle. o Compensating

Correction of Errors Principles of Accounting XI Chapter contents Correction of errors. Errors where trial balance still balances: o Error of omission. o Error of commission. o Error of principle. o Compensating

Leisa Donlan FSAE FINANCIAL MANAGEMENT FOR MOWS

Leisa Donlan FSAE FINANCIAL MANAGEMENT FOR MOWS 3 Basics Of Finances Financial Monitoring Reporting Auditing Taxation Reporting Financial Performance Increasing Income Decreasing Expenses Financial Planning

Leisa Donlan FSAE FINANCIAL MANAGEMENT FOR MOWS 3 Basics Of Finances Financial Monitoring Reporting Auditing Taxation Reporting Financial Performance Increasing Income Decreasing Expenses Financial Planning

ACCOUNTING. Written examination. Tuesday 6 June Reading time: am to am (15 minutes) Writing time: am to 12.

Writing time: am to 12.") Victorian Certificate of Education ACCOUNTING Written examination Tuesday 6 June Reading time: 10.00 am to 10.15 am (15 minutes) Writing time: 10.15 am to 12.15 pm (2 hours) QUESTION BOOK Number of questions

Victorian Certificate of Education ACCOUNTING Written examination Tuesday 6 June Reading time: 10.00 am to 10.15 am (15 minutes) Writing time: 10.15 am to 12.15 pm (2 hours) QUESTION BOOK Number of questions

VisionVPM General Ledger Module User Guide

VisionVPM General Ledger Module User Guide Version 1.0 VisionVPM user documentation is continually being developed. For the most up-to-date documentation please visit the VisionVPM website at www.visionvpm.com

VisionVPM General Ledger Module User Guide Version 1.0 VisionVPM user documentation is continually being developed. For the most up-to-date documentation please visit the VisionVPM website at www.visionvpm.com

GST Report User Guide

GST Report User Guide Created in version 2009.4.0.117 1/9 Table of Contents GST Processing... 2 GST Reports... 4 Balance the GST... 6 Combined Cash GST/Accrual Accounting... 6 Debtors Invoice Report...

GST Report User Guide Created in version 2009.4.0.117 1/9 Table of Contents GST Processing... 2 GST Reports... 4 Balance the GST... 6 Combined Cash GST/Accrual Accounting... 6 Debtors Invoice Report...

ACCOUNTING. Written examination 1. Tuesday 12 June 2007

Victorian CertiÞcate of Education ACCOUNTING Written examination 1 Tuesday 12 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

Victorian CertiÞcate of Education ACCOUNTING Written examination 1 Tuesday 12 June Reading time: 2.45 pm to 3.00 pm (15 minutes) Writing time: 3.00 pm to 4.30 pm (1 hour 30 minutes) QUESTION BOOK Number

How to Enter Opening Balances - Standard VAT

How to Enter Opening Balances - Standard VAT Opening balances represent the financial position of your organisation on the day you start using Sage Accounts. Whatever date you choose, you are likely to

How to Enter Opening Balances - Standard VAT Opening balances represent the financial position of your organisation on the day you start using Sage Accounts. Whatever date you choose, you are likely to

Institute of Certified Bookkeepers

Making you count Institute of Certified Bookkeepers Level II Certificate in Bookkeeping Syllabus from April 2014 1 Level II Certificate in Bookkeeping Level II Certificate in Bookkeeping (Skills and Underpinning

Making you count Institute of Certified Bookkeepers Level II Certificate in Bookkeeping Syllabus from April 2014 1 Level II Certificate in Bookkeeping Level II Certificate in Bookkeeping (Skills and Underpinning

The Uniting Church in Australia Northern Synod

TREASURERS HANDBOOK The Uniting Church in Australia Northern Synod Prepared by Synod Financial Services CONTENTS Page No. 1.0 Introduction 1.1 Overview 3 1.2 Summary of the Work Flow for Congregations

TREASURERS HANDBOOK The Uniting Church in Australia Northern Synod Prepared by Synod Financial Services CONTENTS Page No. 1.0 Introduction 1.1 Overview 3 1.2 Summary of the Work Flow for Congregations

MYOB Bookkeeping Practice Assessment B: Computerised (MYOB) Bookkeeping

Bookkeeping") 1B MYOB Bookkeeping Assessment About the practice assessment MYOB Bookkeeping Practice Assessment B: Computerised (MYOB) Bookkeeping About the practice assessment What you will need Current version of

1B MYOB Bookkeeping Assessment About the practice assessment MYOB Bookkeeping Practice Assessment B: Computerised (MYOB) Bookkeeping About the practice assessment What you will need Current version of

ACCOUNTING PRINCIPLES

ACCOUNTING PRINCIPLES ENTITY The business must be a separate accounting entity from its owner and from other entities. This includes multiple businesses as they are each a separate accounting entity in

ACCOUNTING PRINCIPLES ENTITY The business must be a separate accounting entity from its owner and from other entities. This includes multiple businesses as they are each a separate accounting entity in

Accounting To Trial Balance 10th Edition

ACCOUNTING TO TRIAL BALANCE 10TH EDITION PDF - Are you looking for accounting to trial balance 10th edition Books? Now, you will be happy that at this time accounting to trial balance 10th edition PDF

ACCOUNTING TO TRIAL BALANCE 10TH EDITION PDF - Are you looking for accounting to trial balance 10th edition Books? Now, you will be happy that at this time accounting to trial balance 10th edition PDF

Purchasing. MYOB Advanced Quick Guide Australian Tax and BAS Reporting. 20 Purchasing Overview. D120 Hands on Course

MYOB Advanced Quick Guide Australian Tax and BAS Reporting Purchasing D120 Hands on Course 20 Purchasing Overview D120 - Hands-on Purchasing Overview Page 1 of 18 Page 2 Table of Contents Table of Contents...

MYOB Advanced Quick Guide Australian Tax and BAS Reporting Purchasing D120 Hands on Course 20 Purchasing Overview D120 - Hands-on Purchasing Overview Page 1 of 18 Page 2 Table of Contents Table of Contents...

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Assessment Schedule 2009 Accounting: Prepare financial statements and related accounting entries for sole proprietors (90224)

") NCEA Level 2 Accounting (90224) 2009 Page 1 of 8 Assessment Schedule 2009 Accounting: Prepare financial statements and related accounting entries for sole proprietors (90224) Evidence Statement ONE (a)

NCEA Level 2 Accounting (90224) 2009 Page 1 of 8 Assessment Schedule 2009 Accounting: Prepare financial statements and related accounting entries for sole proprietors (90224) Evidence Statement ONE (a)

Chapter 3: The Ledger and Double-Entry Accounting System. 3. How to record in Assets, Liabilities & Owner s Equity account:

1 Chapter 3: The Ledger and Double-Entry Accounting System Topic Outline: 1. Ledger 2. Ledger Account the T-account 3. How to record in Assets, Liabilities & Owner s Equity account: - the increases - the

1 Chapter 3: The Ledger and Double-Entry Accounting System Topic Outline: 1. Ledger 2. Ledger Account the T-account 3. How to record in Assets, Liabilities & Owner s Equity account: - the increases - the

ACCOUNTING NOVEMBER 2017 MEMORANDUM

NATIONAL GRADE 11 SENIOR CERTIFICATE ACCOUNTING NOVEMBER 017 MEMORANDUM MARKS: 300 MARIKING PRINCIPLES: 1. Penalties for foreign items are applied. No foreign item penalty for misplaced item. No double

NATIONAL GRADE 11 SENIOR CERTIFICATE ACCOUNTING NOVEMBER 017 MEMORANDUM MARKS: 300 MARIKING PRINCIPLES: 1. Penalties for foreign items are applied. No foreign item penalty for misplaced item. No double

Livestock Office Native Accounting

Livestock Office Native Accounting 12/04/2017 Contents Native Accounting... 2 General Ledger... 3 G/L Codes... 3 G/L Code Budgets... 4 G/L Tree... 5 G/L Journals... 6 Bank Accounts... 7 Bank Statements...

Livestock Office Native Accounting 12/04/2017 Contents Native Accounting... 2 General Ledger... 3 G/L Codes... 3 G/L Code Budgets... 4 G/L Tree... 5 G/L Journals... 6 Bank Accounts... 7 Bank Statements...

MTP_Intermediate_Syllabus 2016_June2019_Set1 Paper 5- Financial Accounting

Paper 5- Financial Accounting Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 5- Financial Accounting Full Marks : 100 Time allowed: 3 hours Section

Paper 5- Financial Accounting Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 5- Financial Accounting Full Marks : 100 Time allowed: 3 hours Section

ACCOUNTING. Written examination. Friday 9 November Reading time: 3.00 pm to 3.15 pm (15 minutes) Writing time: 3.15 pm to 5.

Writing time: 3.15 pm to 5.") Victorian Certificate of Education ACCOUNTING Written examination Friday 9 November Reading time: 3.00 pm to 3.15 pm (15 minutes) Writing time: 3.15 pm to 5.15 pm (2 hours) QUESTION BOOK Number of questions

Victorian Certificate of Education ACCOUNTING Written examination Friday 9 November Reading time: 3.00 pm to 3.15 pm (15 minutes) Writing time: 3.15 pm to 5.15 pm (2 hours) QUESTION BOOK Number of questions

Paper Reference. Paper Reference(s) 4305/01 London Examinations IGCSE. Friday 3 November 2006 Afternoon Time: 2 hours 30 minutes

4305/01 London Examinations IGCSE. Friday 3 November 2006 Afternoon Time: 2 hours 30 minutes") Centre No. Candidate No. Paper Reference(s) 4305/01 London Examinations IGCSE Accounting Paper 1 Friday 3 November 2006 Afternoon Time: 2 hours 30 minutes Materials required for examination Nil Paper Reference

Centre No. Candidate No. Paper Reference(s) 4305/01 London Examinations IGCSE Accounting Paper 1 Friday 3 November 2006 Afternoon Time: 2 hours 30 minutes Materials required for examination Nil Paper Reference

Creditor Payments User Guide

Creditor Payments User Guide Table of Contents Payment Execution... 2 Invoice Details... 2 Execute Payments... 3 Reverse or Clear Transactions... 4 Printing Cheques and Remittance Advices... 5 Sample Reports...

Creditor Payments User Guide Table of Contents Payment Execution... 2 Invoice Details... 2 Execute Payments... 3 Reverse or Clear Transactions... 4 Printing Cheques and Remittance Advices... 5 Sample Reports...

ACCOUNTING. Written examination 2. Thursday 7 November 2002

ACCNT EXAM 2A Victorian Certificate of Education ACCOUNTING Written examination 2 Thursday 7 November 2002 Reading time: 11.45 am to 12.00 noon (15 minutes) Writing time: 12.00 noon to 1.30 pm (1 hour

ACCNT EXAM 2A Victorian Certificate of Education ACCOUNTING Written examination 2 Thursday 7 November 2002 Reading time: 11.45 am to 12.00 noon (15 minutes) Writing time: 12.00 noon to 1.30 pm (1 hour

VCE VET FINANCIAL SERVICES

Victorian Certificate of Education 2012 SUPERVISOR TO ATTACH PROCESSING LABEL HERE STUDENT NUMBER Letter Figures Words VCE VET FINANCIAL SERVICES Written examination Thursday 22 November 2012 Reading time:

Victorian Certificate of Education 2012 SUPERVISOR TO ATTACH PROCESSING LABEL HERE STUDENT NUMBER Letter Figures Words VCE VET FINANCIAL SERVICES Written examination Thursday 22 November 2012 Reading time: