e vswks cöwewa I bxwz wefvm evsjv `k e vsk cöavb Kvh vjq XvKv

|

|

|

- Donald Spencer

- 5 years ago

- Views:

Transcription

1 e vswks cöwewa I bxwz wefvm evsjv `k e vsk cöavb Kvh vjq XvKv website: 30 A ±vei 2018 weaviwcww mvky jvi bs-16 ZvwiL t KvwZ K 1425 e e vcbv cwipvjk/cöavb wbe vnx Kg KZ v evsjv ` k Kvh iz mkj Zdwmwj e vsk wcöq g nv`q, Guidelines on Internal Credit Risk Rating System for Banks cöm ½ Dch z³ wel q AÎ wefv Mi weaviwcww mvkz jvi bs 18, ZvwiLt 11 ww m ^i 2005 Gi cöwz ` wó AvKl Y Kiv hv Q 02 FY SzuwK mwvkfv e wpwýzkiy Ges h_vh_fv e e e vcbvi j D³ mvk zjv ii gva g µwwu wi MÖwWs g vbyqvj Rvwi Kiv nq D³ mvk zjv ii gva g RvwiK Z g vbyqvj I mswkøó wdb vwýqvj g Wj ch v jvpbvc~e K e vs Ki FY SzuwK e e vcbv AwaKZi Kvh Ki I mg qvc hvmx Kivi j G ch v q bzzb Avw½ K "Guidelines on Internal Credit Risk Rating System for Banks" Rvwi Kiv n jv 03 RvwiK Z MvBWjvBÝ I GZ`mshy³ g WjwUi h_vh_ e envi wbwðz Kiv n j Dchy³ e w³/cöwzôvb FYcÖvwßi hvm Zv Abyhvqx FY myweav MÖnY Ki Z cvi e GQvov, e vswks Lv Z Ljvwc F Yi cwigvy nªvmki YI g WjwU AwaKZi mnvqk f wgkv cvjb Ki e g WjwU Z 04 wu cöavb Lv Zi AvIZvq me gvu 20 wu Dc LvZ i q Q Ges cöwzwu Dc Lv Zi ˆewkó, SzuwK, Avw_ K m gzv I e e vcbvi ` Zv we epbvq wb q 20 wu ^Zš g Wj AšÍf z³ Kiv n q Q bzzb cöyxz MvBWjvBÝ I g WjwU FYMÖnxZvi µwwu wi iwus Kivi Î b~ bzg gvb`û wn m e we ewpz n e 04 weaviwcww mvk zjvi bs 18/2005 Gi gva g RvwiK Z µwwu wi MÖwWs g vbyqvj Gi cvkvcvwk "Guidelines on Internal Credit Risk Rating System for Banks" I GZ`&mshy³ g WjwU AvMvgx 30 Ryb 2019 ZvwiL ch ší hymcr Pvjy _vk e AvMvgx 01 RyjvB 2019 ZvwiL _ K bzzb cöyxz MvBWjvBÝ I g WjwUi ev Íevqb eva Zvg~jKfv e wbwðz Ki Z n e 05 GZ`msµvšÍ g W ji md&u-kwc Avcvbv `i B- gbj wvkvbvq cöiy Kiv n jv Avcbv `i wek Í, (Avey divn gvt bv Qi) gnve e vck dvb:

2 GUIDELINES ON INTERNAL CREDIT RISK RATING SYSTEM FOR BANKS BANGLADESH BANK

3 GUIDELINES ON INTERNAL CREDIT RISK RATING SYSTEM FOR BANKS Advisors Mr. S. M. Moniruzzaman Deputy Governor, Bangladesh Bank Mr. Ahmed Jamal Deputy Governor, Bangladesh Bank Chairman Mr. Md. Abdur Rahim Executive Director, Bangladesh Bank Coordinators Mr. Abu Farah Md. Nasser General Manager, Bangladesh Bank Mr. Md. Shah Naoaj, CFA Deputy Director, Bangladesh Bank Dr. Mahmood Osman Imam, FCMA Professor, University of Dhaka Members Ms. Husne Ara Shikha Deputy General Manager, Bangladesh Bank Dr. Prashanta Kumar Banerjee Professor, Bangladesh Institute of Bank Management Mr. Zakir Hossain DMD, Mercantile Bank Limited Mr. Shadab Hossain Head of Wholesale Credit & Market Risk, HSBC Mr. Md. Ala Uddin Deputy General Manager, Bangladesh Bank Ms. Dipti Rani Hazra Deputy General Manager, Bangladesh Bank Mr. Amitabh Chakraborty Joint Director, Bangladesh Bank

4 Foreword Credit risk is the risk of losses arising from borrowers' failure to repay the loans or meet contractual obligations. In order to establish a sound credit risk management, adopting a modern rating mechanism is important. Bangladesh Bank (BB) introduced the Lending Risk Analysis (LRA) framework in 1993, for all lending exposures of the banks in excess of Bangladesh Taka (BDT )10 million. The LRA framework, however, made no attempt to introduce a Risk Grading System (RGS) for unclassified loan accounts. As an advancement in this area, BB made the Core Risk Management Guidelines (CRMG) mandatory in 2003, introducing the requirement of grading unclassified accounts. In 2005, Bangladesh Bank, vide its BRPD Circular No.18, advised all scheduled banks to implement Credit Risk Grading (CRG) for their borrowing clients. It is to note that the CRG-2005 was applicable for all exposures (irrespective of amount) except consumer loans, small enterprises financing, short-term agri loans and micro-credit. During the last couple of years, industry characteristics have changed a lot. Besides, necessity has evolved to review different weights applied in the CRG framework. In order to deal with growing complexities in a more dynamic banking industry, Bangladesh Bank feels the necessity to update the Credit Risk Grading mechanism. Bangladesh Bank formed a ten-member review committee headed by the executive director responsible to oversee the affairs of BRPD and comprising the officials from Banking Regulation and Policy Department, Financial Stability Department, Department of Banking Inspection as well as officials from the banking industry and academicians from the University of Dhaka and Bangladesh Institute of Bank Management (BIBM). The purpose of the committee was to revamp the policy on the credit grading mechanism and to develop a modern and effective rating technique. This guideline is the outcome of the hard works and relentless efforts of the committee, which has cautiously considered the various aspects before developing this Internal Credit Risk Rating System. Internal Credit Risk Rating System comprises with 20 (twenty) different rating templates for 20 (twenty) industries/sectors instead of just one template for all the sectors like previous CRG model. Different yardsticks have been used for assessing the borrowers of corresponding sectors. The assessment criteria for each of these sectors are unique and the ideal assessment parameters for each criterion are defined based on the analysis of historical three-year data of 220 (two hundred and twenty) audited financial statements of the firms/companies/institutions collected from 22 (twenty-two) scheduled banks. Moreover, data from annual financial statements of 54 (fifty-four) companies listed on Dhaka Stock Exchange (DSE) have also been analyzed for the aforesaid purpose and a rigorous validation has been conducted with real-time analysis from 4 (four) scheduled banks. Importantly, comments /feedback on the draft input templates has been collected from 26 (twenty six) banks. We believe this guidelines and enclosed model will be a valuable addition to the credit risk management tools and help the banks in developing and maintaining a better-quality credit portfolio. This is an evolving matter, which will regularly be reviewed by Bangladesh Bank to capture the changing dynamics of the economy and business environment. Md. Abdur Rahim Executive Director Bangladesh Bank

5 Table of Contents 1.1 Introduction Definition of Internal Credit Risk Rating System and Internal Credit Risk Rating Use of Internal Credit Risk Rating (ICRR) Functions of Internal Credit Risk Rating System: General Instructions Frequency of Credit Risk Scoring: Selected Sectors Credit Risk Ratings Scores Definitions of Credit Risk Rating Management Action Triggers: Exceptions to Credit Risk Scoring Chapter 2: Credit Risk Rating Components Components of Credit Risk Rating Quantitative indicators and associated weights Qualitative indicators and associated weights Chapter 3: Credit Risk Rating Process Input primary information of borrower and select sector/industry of the borrower: Input data of balance sheet, profit and loss statement and cash flow statement Qualitative Analysis Generating Score:

6 1.1 Introduction The aim of credit risk management is to maximize a bank s risk-adjusted rate of return by maintaining credit risk exposure within acceptable levels. Banks need to manage the credit risk inherent in the entire portfolio as well as the risk in individual borrower transaction. The effective management of credit risk is a critical component of a comprehensive approach to risk management and essential to the long-term success of any banking organization. Since exposure to credit risk continues to be the leading source of problems in banks, banks should have a keen awareness of the need to identify, measure, monitor and control credit risk as well as to determine that they hold adequate capital against these risks and they are adequately compensated for risks incurred. The Internal Credit Risk Rating System describes the creditworthiness of the borrower of a particular sector based on the assessment criteria set for that sector. Since the leverage, liquidity, profitability, as well as other quantitative and qualitative indicators, vary significantly from sector to sector, the ICRRS is developed to calibrate such diversities into the rating system. Moreover, relevant and appropriate numbers of financial ratios are used in Internal Credit Risk Rating System for assessing the strengths of the borrowers. The set of the qualitative questioners used in the process are also more robust. This will effectively ensure that the borrowers from different sectors and industries are assessed based on the unique characteristics of those sectors. 1.2 Definition of Internal Credit Risk Rating System and Internal Credit Risk Rating Internal Credit Risk Rating System refers to the system to analyze a borrower's repayment ability based on information about a customer's financial condition including their liquidity, cash flow, profitability, debt profile, market indicators, industry and operational background, management capabilities, and other indicators The summary indicator derived from the system will be called Internal Credit Risk Rating (ICRR)- a key reference for credit risk assessment and decision making. 1.3 Use of Internal Credit Risk Rating (ICRR) Internal Credit Risk Rating System will be an integral part of credit risk management for the banks. The key uses of these guidelines are as follows: a) To provide a granular, objective, transparent, consistent framework for the measurement and assessment of borrowers credit risk. b) To facilitate the portfolio management activities c) to assess the quality of individual borrower to help the banks to determine the quality of the credit portfolio, line of business, the branch or the Bank as a whole. d) To be used for individual credit selection, credit pricing, and setting credit limit and terms and conditions

7 1.4 Functions of Internal Credit Risk Rating System: a) Internal Credit Risk Rating System is a fully automated credit risk scoring system that calibrates the characteristics of different sectors and industries in one single model; b) To get the appropriate rating and score, the analyst shall select the appropriate sector or industry from the dropdown list given in the top page of the template; If the right sector or industry is not selected; the rating will not reflect the unique characteristics of the particular sector or industry. c) If the borrower is in multiple lines of business, the sector should be used assessing the line of business generating the highest portion of the revenue &/or profit. If there is no particular line of businesses can be singled out- the ICRRS should be conducted using "other industry- if manufacturing" or "other service-if service". 1.5 General Instructions a) Banks shall strictly follow this guidelines and rating system issued by Bangladesh Bank without making any change, extension, modification or deletion. b) The ICRR shall be applicable for all exposures (irrespective of amount) except consumer loans, small enterprises having total loans exposures less than BDT 50 (fifty) lac, short-term agri loans, micro-credit and lending to bank, NBFI and Insurance. c) The quantitative part of the ICRR exercise shall be conducted by a credit officer/ an analyst. The Relationship Manager/ Branch Manager shall complete the qualitative assessment part to generate the total scores. d) ICCR shall be an integral part of the credit approval process. e) The credit risk function of the bank is responsible for the accuracy and integrity of the rating as the second line of defense. f) The executive summary report of the ICRR of the borrower shall be approved and signed by the Chief Risk Officer (CRO) and for those loans that are approved below the CRO level e.g zonal office or branch office, the executive summary report of the ICRR shall be approved and signed by the final approval authority. g) Banks shall use the latest audited financial statements of the borrower for generating the quantitative rating under ICRR. h) All credit proposals whether new, renewal or enhancement shall be gone through the ICRR process and a set of the ICRR report shall be retained in the loan file. i) The Relationship Manager shall pass the approved ICRR report to the related department for updating their MIS/record. j) Banks shall conduct the routine internal audit to check whether the Internal Credit Risk Rating System is functioning as per the instructions laid down in the guidelines

8 1.6 Frequency of Credit Risk Scoring: 1.7 Selected Sectors ICRR shall be conducted for all credit proposals including new, renewal and enhancement of the existing proposal; For existing credit relationship, the ICRR shall be reviewed at least annually at the time of annual/regular credit review. To ensure the current system useful, the following sectors are selected considering the size of exposures of banks in these industries. A. Industry 1. Ready Made Garments (RMG) 2. Textile (including spinning, knitting, weaving) 3. Food and Allied Industries 4. Pharmaceutical 5. Chemical 6. Fertilizer 7. Cement 8. Ceramic 9. Ship building 10. Ship breaking 11. Jute Mills 12. Steel Engineering 13. Power and Gas 14. Other industry (only to be selected if the borrower falls under industry but does not fit with other 13 specific sub-categories) B. Trade and Commerce C. Agro Base and Agro Processing D. Service 1. Housing and Construction 2. Hospitals and Clinics 3. Telecommunication 4. Other service - 4 -

9 1.8 Credit Risk Ratings Scores The ICRR consists of 4-notched rating system covering the Quantitative and Qualitative parameters. The ratings and scores are mentioned below: Rating Scores Aggregate Excellent 80% Good 70% to <80% Marginal 60% to <70% Unacceptable <60% 1.9 Definitions of Credit Risk Rating The features of the different categories of Credit Risk Ratings are given below: a) Excellent Aggregate score of 80 or greater in ICRR. Strong repayment capacity of the borrower evident by the high liquidity, low leverage, strong earnings, and cash flow Borrower has well established strong market share. Very good management skill & expertise. b) Good Aggregate score of 70 or greater but less than 80 and the quantitative score of at least 30. These borrowers are not as strong as "Excellent "borrowers, but still demonstrate consistent earnings, cash flow and have a good track record. Borrower is well established and has strong market share. Very good management skill & expertise. c) Marginal Aggregate score of 60 or greater but less than 70 and the quantitative score of at least 30. This grade has potential weaknesses that deserve management s close attention. If left uncorrected, these weaknesses may result in a deterioration of the repayment prospects of the borrower. d) Unacceptable Aggregate score of less than

10 Financial condition is weak and no capacity or inclination to repay. Severe management problems exist. Facilities should be downgraded to this grade if sustained deterioration in financial condition is noted (consecutive losses, negative net worth, excessive leverage) Management Action Triggers: a) Banks are allowed lending to a borrower if the borrower's ICRR is "Excellent" or "Good". However, for the "Marginal "cases, the bank shall take cautionary measures in renewing the facilities or lending new money to the customers. While assessing credit proposals, banks must satisfy themselves on the future prospect of the business, additional collateral coverage etc. Banks shall take heightened measures for monitoring these accounts including but not limited to regular client visits, monitoring of the improvement plans, close monitoring of the repayment performances, timely review of the facilities, oversight on the improvement areas etc. b) No loan shall be sanctioned to borrowers whose ICRR is "Unacceptable" unless the loan is 100% cash covered or fully guaranteed by the Government or Multilateral Development Banks (MDBs) or the loan is for any state-owned organization or stateowned project. c) For the quantitative and qualitative risk analysis, if the ICRR falls under "Marginal" or "Unacceptable" for any risk criteria (among 16 quantitative and 18 qualitative); whatever the aggregate score is, the relationship manager shall evaluate what would be the impacts of such on loan repayment and justify how those risks are mitigated; and in loan proposal the approval authority should review that justifications thoroughly and make necessary evaluations on it and should be documented in the loan file. d) In deriving ICRR, whatever score a borrower gets in the qualitative analysis if the score in the quantitative part is less than 50%, the borrower s ICRR shall be "Unacceptable". e) Bank can make renewal and enhancement of existing loans for maximum 2 (two) times if the borrower's ICRR is "Unacceptable". f) In conducting qualitative analysis, justifications for all criteria are required to be documented. g) Bank must maintain portfolio level data base for the asset base with "Excellent", "Good" Marginal and Unacceptable category and maintains risk appetite/tolerance level for portfolio

11 1.11 Exceptions to Credit Risk Rating a) For a newly established company with no meaningful financial statements, the bank can apply a rating based on the projected financial statements and the rating of the borrower shall not be better than Marginal. However, the bank must run the rating module once the full year audited financial statements became available reflecting customer's full-fledged business operation. b) For the companies under large business conglomerate, rating substitution is allowed based on the rating of Corporate Guarantor of the performing concern of the same group or holding company. In case of rating substitution based on the corporate guarantor, the guarantee must be legally enforceable, irrevocable and unconditional. In this regard, a full-fledged ICRR shall be conducted on the guarantor to determine whether the guarantor has the ability to the support the borrower at the time of need. c) Rating generation is discouraged using outdated financial statements (i.e available audited financial statements are more than 18 months old). In exceptional cases where there is valid reason for delay in audited financial publication, out dated financial statements can be accepted only if up to date unaudited financial statement is submitted, but the rating shall not be better than Marginal. In this case, the conditioned mentioned in para 1.10(a) is to be followed. d) Rating shall be downgraded if there is any internal/external factors or information that have not been captured in the rating/financial statements (because they are post balance sheet events) having the material impact on the customer's business operation and loan repayment. A conservative and consistent approach should be used in employing judgments in the case of events like the death of key sponsor, prolonged factory shut down, deteriorating financial profile reported in interim financial statements, change in tax structure/duty, large expansions funded by debt, excessive leverage ratio, merger-acquisition etc. e) For the proprietorship & partnership concern where preparation of the audited financial statements are not mandatory, un audited financial statement can be used for rating generation but due diligence should be conducted on the accuracy of the financial statements with high-level checking of the bank statements recording the sales collection, stock/receivable position, peer analysis, bank liabilities etc. f) If the customer is in multiple lines of business, the most appropriate sector/industry shall be the line of business generating revenue more than 50% of total revenue. If there is no particular line of businesses can be singled out- the rating for "other industry" or "other services" should be used. g) This guideline and enclosed model will be the minimum standard of risk rating; and banks may adopt more sophisticated risk rating model in line with the size and complexity of their business

12 2.1 Components of Credit Risk Rating Chapter 2: Credit Risk Rating Components In the previous version of Credit Risk Grading Manual, 50 percent weights were assigned for quantitative indicators while 50 percent weights were for subjective judgment. In the ICRR, these weights have been revised; 60 percent weights are assigned for quantitative indicators while 40 percent are assigned for qualitative indicators. 2.2 Quantitative indicators and associated weights Quantitative indicators in ICRR fall into six broad categories; leverage, liquidity, profitability, coverage, operational efficiency, and earning quality. Details indicators under these categories and associated weights are furnished below: Quantitative Indicators Weight Definition a) Debt to Tangible Net Total Interest-bearing liabilities or 1.Leverage (10%) Worth (DTN) 7 Financial Debt/ Total Tangible Net Worth 1 2.Liquidity (10%) 3.Profitability (10%) 4.Coverage (15%) 5.Operational Efficiency (10%) b) Debt to Total Assets (DTA) a) Current Ratio (CR) b) Cash Ratio (Cash) 3 a) Net Profit Margin (NPM) b) Return on Assets (ROA) 3 c) Operating Profit to Operating Assets (OPOA) a) Interest Coverage (IC) 3 b) Debt Service Coverage Ratio (DSCR) 5 c) Financial Debt to Operating Cash Flow (FDOCF) d) Cash flow Coverage Ratio (CCR) a) Stock Turnover Days (STD) b) Trade Debtor Collection Days (TDCD) 1 Total Tangible Net Worth= Total Equity-Intangible Assets. 3 Total Interest-Bearing Liabilities or Financial Debt/ Average Total Assets 7 Current Assets/ Current Liabilities Cash and easily marketable securities/ Current Liabilities 5 Net profit after tax/ Net Sales 2 Net profit after tax/ Average Total Assets Operating Profit/ Average Operating Assets Earnings Before Interest and Tax/Interest Expense Earnings Before Interest Tax Depreciation Amortization/ Debts to be Serviced 4 Financial Debt / Operating Cash Flow 3 4 Cash flow from operation / Debts to be Serviced (Total Inventory/Cost of Goods Sold)*360 3 (Total Accounts Receivable/ - 8 -

13 6.Earning Quality (5%) Sales)*360 c) Asset Turnover (AT) 3 Sales /Average Total Assets a) Operating Cash Flow to Sales (OCFS) 3 Operating Cash flow / Sales b) Cash flow based accrual ratio (CAR) 2 =NI-(CFO+CFI) /Average Net Operating Assets 2.3 Qualitative indicators and associated weights Qualitative indicators covers six broad aspects of the firms/institutions to be rated, namely business/industry risk, credit quality enhancement, performance behavior, management risk, relationship risk, and compliance risk. Noteworthy that aggregate weights against the qualitative indicators stand at 40 percent. Detail indicators and associated weights are appended below in details: Indicators Weights 1. Performance Behavior 10 Performance Behavior With Banks Borrowings 9 Performance Behavior With Suppliers/ Creditors 1 2. Business and Industry Risk 7 Sales Growth 2 Age Of Business 2 Industry Prospects 1 Long-Term External Credit Rating Of The Borrower 2 3. Management Risk 7 Experience Of The Management 2 Existence Of Succession Plan 2 Auditing Firms 2 Change In Auditors In Last 4 Years 1 4. Security Risk 11 Primary Security 2 Collateral 2 Collateral/ Security Coverage 5 Type Of Guarantee 2 5. Relationship Risk 3 Account Conduct 3 6. Compliance Risk 2 Compliance With Environmental Rules, Regulations And Covenants 1 Corporate Governance 1 Total

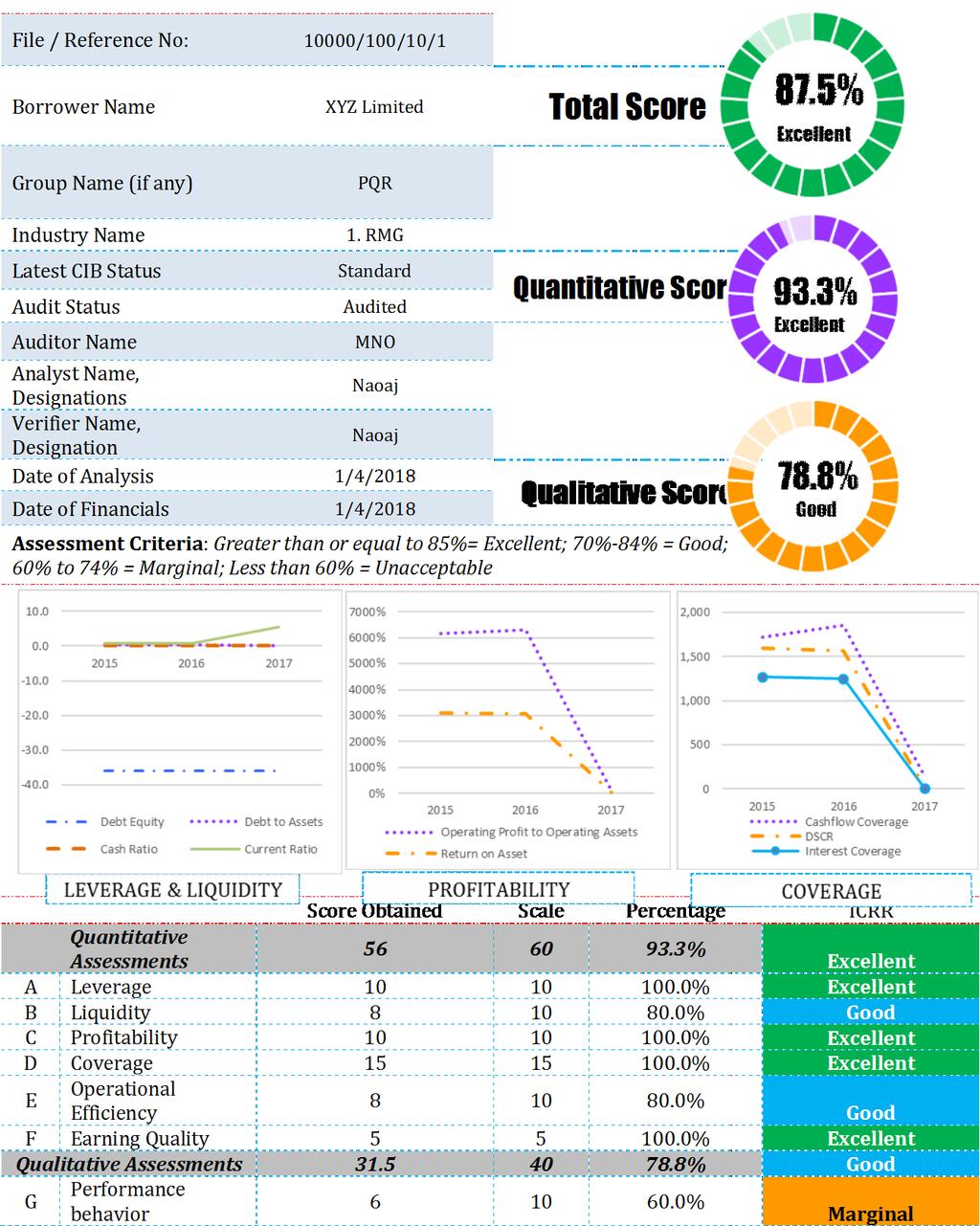

14 Chapter 3: Credit Risk Rating Process After the risk identification & weight assignment process (as mentioned in chapter 2), the next steps will be to input actual parameters in the score sheet to arrive at the scores corresponding to the actual parameters. These guidelines also provide a well programmed MS Excel-based credit risk scoring system to arrive at a total score on each borrower. The excel program requires inputting data accurately in particular cells for input and will automatically calculate the risk grade for a particular borrower based on the total score obtained. The following steps are to be followed while using the MS Excel program. a) Open the MS XL file named, ICRRS b) The entire XL model named, ICRRS is protected except the particular cells to input data. c) Some input cells contain DROP DOWN LIST for some criteria corresponding to the Key Parameters. Click to the input cell and select the appropriate parameters from the DROP DOWN LIST as shown below. e) All the cells provided for input must be filled in order to arrive at accurate risk grade. The following step-wise activities outline the detail process for arriving at Credit Risk Rating. 3.1 Input primary information of borrower and select sector/industry of the borrower: Bank's Name : ABC Bank Limited Branch Name : Gulshan File/ Reference No : 10000/100/10/1 Borrower Name : XYZ Limited Group Name, if any : PQR Type of Industry/ Sector : 1. RMG Industry Code : 101 Ownership Type : Sole Proprietorship Registration No/Trade License No : 123 CIB Status : Standard

15 Financials Audit Status: : Audited Name of Audit Farm : MNO Analyst Name, Designation : PQR Verifier Name, Designation : UBW Date of Financials Date of Analysis (DD-MM- YYYY) : Date of Verification (DD-MM- YYYY) : Input data of balance sheet, profit and loss statement and cash flow statement In the input sheet of the balance sheet, profit, and loss statement and cash flow statement, Input must be given to all cells that are marked with yellow colors. Moreover, while providing input to the balance sheet, profit and loss statement and cash flow statement following issues should be taken care of: a) Current Portion of Long-Term Borrowing/Loan Input must be given to this cell. This cell is crucial to calculate "debt service coverage ratio". If "Current Portion of Long-Term Borrowing/Loan" is not found in the balance sheet, the analyst shall communicate this to the borrower and determine the amount based on other material information including notes and communication with the borrower. If the amount is already added with the total loans in the balances sheet then "Current Portion of Long-Term Borrowing/Loan" must be deducted from the total loans and must insert the split figures in related cells. If the figure is still zero, it means the borrower has no existing long-term borrowings; which is unusual. If found so, the analyst should interview the borrower. If the analyst becomes certain that the borrower has no existing borrowings, then 0.01 shall be inserted in the corresponding cell. b) Other Current Liabilities: To make the balance sheet balance i.e as sets = liabilities + equity, deduct amount 0.01 in this cell, if the same is inserted in row 56: Current Portion of Long-Term borrowing/ Loan. c) Financial/Interest Expenses Input must be given to this cell. If not found in the P&L, the analyst shall look into the notes of financial statement and communicate with the borrower to determine the amount

16 If the figure is zero, it means the borrower has no existing borrowings; which is unusual. If the analyst becomes certain that the borrower has no existing borrowings, then figure 1 must be inserted in the corresponding cell. 3.3 Qualitative Analysis After providing input to the balance sheet, profit and loss statement and cash flow statement, the rigorous qualitative analysis shall be conducted. The qualitative analysis shall be conducted by the relationship manager. The details qualitative analysis are as follows: G Performance Behavior 10 G.1 Performance behavior with lending banks G.1.1 How many times the borrower was adversely classified in last 3 years [ Aversely classified means the 0 time 5 borrower's loans classified as per BB 1 time 4 loan classifications policy i.e SS, DF, 2 times 3 BL] 3 times 1 G1.2 G.2 How many times the borrower's loans was rescheduled/ restructured in last 3 years Performance behavior with suppliers/ Creditors Did The Borrower Pay Its Suppliers/ Creditors Regularly In Last 1 Year >3 times 0 0 time 4 1 time 3 2 times 2 3 times 1 >3 times 0 Yes 1 No 0 H Business and Industry Risk 7 H.1 Sales Growth * Sales growth means annual sales growth >10% 2 The formula for calculating sales growth is [(current year sales - previous year sales)/ previous year sales]*100 H.2 Age of Business 5%-10% 1 Less than 5%

17 The number of years the borrower >10 years 2 engaged in this line of business 7 to 10 years to 7 years 1 4 to 5 years 0.5 <4 years 0 H.3 Industry Prospects H.4 Critical assessment of 5 (five) years prospect of industry and borrower's sales volatility * Volatility denotes sales volatility Long-Term External Credit Rating of the Borrower Rating Grade should be assigned in line with BB Rating Mapping as per BRPD circular 18/2014 on Risk-Based Capital Adequacy in line with Basel III (see annex 2) Growing and Low Volatility 1 Stable 0.75 Growing but High Volatility 0.5 Declining &3 1.5 >3 0.5 Unrated 0 I Management Risk 7 I.1 Experience of the Management Quality of the management based on total number of years of experience of the senior management in the Industry. * Senior Management means MD and next two tiers I.2 Existence of Succession Plan I.3 Auditing Firms I.4 BSEC listed auditors are considered as recognized Change In External Auditors In Last 4 Years More than 10 years in the related line of business 5 10 years in the related line of business 1 Less than 5 years 0 Yes, with good capability of successor 2 Yes, but questionable capacity of successor 1 No successor 0 Recognized Auditors 2 Other Auditors 1 Un audited 0 Yes 1 No 0 J Security Risk

18 J.1 Primary Security Fully Pledged Facilities 2 J.2 Collateral J.3 Eligible Collateral Coverage The formula of eligible collateral coverage is [eligible collateral / total loans] * Forced sale value should be determined as per BRPD circular no 14 issued on September 23, 2012 (Para 07: Eligible Collateral) (Annex 3) J.4 Type of Guarantee Strong Corporate Guarantee means the credit rating of the guarantor should be at least 1 or 2 as per BB rating mapping mentioned in BRPD circular 18/2014 on Risk Based Capital Adequacy in line with Basel III. (see annex 2) Registered Hypothecation (1 st Charge/1st Pari Passu Charge) 1.5 2nd Charge/Inferior Charge 1 No Security 0 Registered Mortgage On Municipal 2 Corporation/Prime Area Property Registered Mortgage On Pourashava/Semi-Urban/ Union 1.5 Parishad Area Property Equitable Mortgage Or No Property But Plant And Machinery As 1 Collateral No Collateral 0 >100% 5 80% to 100% 4 70% to 80% 3 50% to 70% 2 <50% 0 Government Guarantee and/or Bank Guarantee 2 Strong Corporate Guarantee 1.5 Personal Guarantees or Corporate Guarantee without Strong Financial Strength 1 No support/guarantee 0 K Relationship Risk 3 K.1 Account Conduct More than 3 years Accounts with Faultless Record 3 Less than 3 years Accounts with faultless record 2 Accounts having satisfactory dealings with some late payments. 1 Frequent Past dues & Irregular dealings in account 0 L Compliance Risk 2 L.1 Compliance with environmental rules,

19 regulations and covenants Yes 1 No 0 L.2 Corporate Governance Independence of Management Good Corporate Governance 1 Questionable Corporate Governance 0 Total Generating Score: After providing inputs to the balance sheet, profit and loss statement, cash flow statement and qualitative analysis, the detail management report and executive summary report will automatically be generated. In the detail management report and executive summary report, fourcolor coding are used. The detail of the color coding are as follows: Color Green Blue Yellow Red Rating Excellent Good Marginal Unacceptable The analyst should meticulously review all color coding and rating. For the quantitative and qualitative risk analysis, if the ICRR falls under "Marginal" or "Unacceptable" for any risk criteria (among 16 quantitative and 20 qualitative); whatever the aggregate score is, the relationship manager shall evaluate what would be the impacts of such on loan repayment and justify how those risks are mitigated; and in loan proposal the approval authority should review that justifications thoroughly and make necessary evaluations on it and should be documented in the loan file. In the executive summary report, the movement of the key quantitative indicators for last three years are also disclosed. The details of the executive summary are as follows:

20 - 16 -

21 Annexure Detail Management Report File / Reference No: 10000/100/10/1 Borrower Name Group Name (if any) Industry Name XYZ Limited PQR 1. RMG Latest CIB Status Standard Indicators Assessment Criteria: Greater than or equal to 80%= Excellent; 75%- 80% = Good; 60% to 70% = Marginal; Less than 60% = Unacceptable Score Obtained Audit Status Audited 56 Quantitative Auditor Name MNO 93.3% Analyst Name, Designations nbv 31.5 Qualitative 78.8% Verifier Name, Designation xyz 87.5 Aggregate Date of Analysis 1/4/ % Date of Financials 1/4/2018 Risk Rating Excellent Good Excellent Outcome Score Obtained Scale Percentage Risk Rating Quantitative Assessments % Excellent A Leverage % Excellent A.1 1. Financial Debt to Tangible Net Worth % Excellent (DTN) B.2 2. Financial Debt to Total Assets (DTA) % Excellent B Liquidity % Good B.1 1. Current Ratio (CR) % Excellent B.2 2. Cash Ratio (Cash) % Unacceptable C Profitability % Excellent C.1 1. Net Profit Margin (NPM) % Excellent C.2 2. Return on Assets (ROA) % Excellent C.3 3. Operating Profit to Operating Assets % Excellent (OPOA) 0.62 D Coverage % Excellent D.1 1. Interest Coverage (IC) % Excellent

22 D.2 2. Debt Service Coverage Ratio (DSCR) % Excellent D.3 3. Operating Cashflow to Debt Ratio (CDR) % Excellent D.4 4. Cashflow Coverage Ratio (CCR) % Excellent E Operational Efficiency % Good E.1 1. Stock Turnover Days (STD) % Excellent E.2 2. Trade Debtor Collection Days (TDCD) % Excellent E.3 3. Asset Turnover (AT) % Unacceptable F Earning Quality % Excellent F.1 1. Operating Cash Flow to Sales (CFS) % Excellent F.2 2. Cashflow based accrual ratio (CAR) % Excellent Qualitative Assessments % Good G Performance Behavior % Marginal G.1.1 G.1.2 G.2 How many times the borrower got adversely classified in last 5 years How many times the borrower's loans got rescheduled/ restructured in last 5 years Did the borrower pay its Suppliers/ Creditors regularly in last 1 year 0 time % Excellent >3 times % Unacceptable Yes % Excellent H Business and Industry Risk % Excellent H.1 Sales Growth >10% % Excellent H.2 Age of Business >10 years % Excellent H.3 Industry Prospects Growing but High Volatility % Unacceptable H.4 Long Term External Credit Rating of the % Excellent Borrower I Management Risk % Excellent I.1 Experience of the Management More than 10 years in the related line of business % Excellent

23 I.2 Existence of Succession Plan I.3 Auditing Firms I.4 Change in Auditors in last 3 years Yes, with good capability of successor Recognized Auditors % Excellent % Excellent Yes % Excellent J Security Risk % Good J.1 Primary Security Fully Pledged facilities % Excellent J.2 Collateral Registered Mortgage on Municipal corporation/prime Area property % Excellent J.3 Collateral Coverage >100% % Excellent J.4 Guarantee Personal Guarantees or Corporate Guarantee without FALSE 2 0.0% Unacceptable Strong Financial Strength K Relationship Risk % Unacceptable K.1 Account Conduct Accounts having satisfactory dealings with some late payments % Unacceptable L Compliance Risk % Excellent L.1 Compliance with environmental rules, regulations and covenants Yes % Excellent L.2 Corporate Governance Good Corporate and CSR activities Governance % Excellent

24 Annex 2: ECAI s Credit Rating Categories Mapped with BB s SME Rating Grade BB Rating Grade Equivalent Rating of S&P and Fitch Equivalent Rating of Moody Equivalent Rating of CRISL Equivalent Rating of CRAB Equivalent Rating of NCRL Equivalent Rating of ECRL Equivalent Rating of ACRSL Equivalent Rating of ACRL Equivalent Rating of WASO 1 AAA to AA Aaa to Aa AAA, AA+, AA, AA- AAA, AA1, AA2, AA3 AAA, AA+, AA, AA- AAA, AA+, AA, AA- AAA, AA+, AA, AA- AAA, AA+, AA, AA- AAA AA1, AA2, AA3 2 A A A+, A, A- A1, A2, A3 A+, A, A- A+, A, A- A+, A, A- A+, A, A- A1, A2, A3 3 BBB Baa BBB+, BBB, BBB- BBB1, BBB2, BBB3 BBB+, BBB, BBB- BBB+, BBB, BBB- BBB+, BBB, BBB- BBB+, BBB, BBB- BBB1, BBB2, BBB3 4 BB to B Ba to B BB+, BB, BB- BB1, BB2, BB3 BB+, BB, BB- BB+, BB, BB- BB+, BB, BB- BB+, BB, BB- BB1, BB2, BB3 5 Below B Below B B+, B, B-, CCC+, CCC, CCC-, CC+, CC, CC- B1, B2, B3, CCC1, CCC2, CCC3, CC B+, B, B- B+, B, B- B+, B, B-, CC+,CC,CC- B+, B, B-, CCC B1, B2, B3, CCC 6 C+, C, C-, D C, D C+, C, C-, D D C+, C, C-, D CC+,CC,CC-, C+, C, C-, D CC1, CC2, CC3, C+, C, C-, D Short-Term Rating Category Mapping S1 F1+ P1 ST-1 ST-1 N1 ECRL-1 ST-1 AR-1 P-1 S2 F1 P2 ST-2 ST-2 N2 ECRL-2 ST-2 AR-2 P-2 S3 F2 P3 ST-3 ST-3 N3 ECRL-3 ST-3 AR-3 P-3 S4 F3 ST-4 ST-4 N4 ECRL-4 ST-4 AR-4 P-4 S5,S6 B,C, D NP ST-5, ST-6 ST-5, ST-6 N5 D ST-5, ST-6 AR-5, AR-6 P-5, P-6 20

25 Annex 3: List of Eligible Collateral (as per BRPD circular no 14/2012 on Loan Classification and Provisioning): 100% of deposit under lien against the loan. 100% of the value of government bond/savings certificate under lien. 100% of the value of guarantee given by Government or Bangladesh Bank 100% of the market value of gold or gold ornaments pledged with the bank. 50% of the market value of easily marketable commodities kept under control of the bank. Maximum 50% of the market value of land and building mortgaged with the ban 50% of the average market value for last 06 months or 50% of the face value, whichever is less, of the shares traded in stock exchange. 21

26 Annex 4: Detail Quantitative Analysis Quantitative Analysis File / Reference No: 10000/100/10/1 Borrowe Name xyx Group Name (if any) ABC Industry Name 14. Other Industries Latest CIB Status Standard Audit Status Audited Auditor Name EFG Analyst Name, Designations Naoaj Verifier Name, Designation PQR Date of Analysis Date of Financials Quantitative Indicators (60) Criteria Parameter Scale Actual Parameter Score Obtained A. Leverage Financial Debt to Tangible Net Worth (DTN) Financial Debt to Total Assets (DTA) B. Liquidity Current Ratio (CR) Cash Ratio (Cash) C. Profitability Net Profit Margin (NPM) % Return on Assets (ROA) % Operating Profit to Operating Assets (OPOA) % 1.00 D. Coverage Interest Coverage (IC) Debt Service Coverage Ratio (DSCR)

27 3. Operating Cashflow to Debt Ratio (CDR) 4. Cashflow Coverage Ratio (CCR) E. Operational Efficiency Stock Turnover Days (STD) Trade Debtor Collection Days (TDCD) Asset Turnover (AT) 88.15% 2.00 F. Earning Quality Operating Cash Flow to Sales (CFS) % Cashflow based accrual ratio (CAR) Total Percentage 37% 23

evsjv `k e vsk cöavb Kvh vjq WvKev bs 325 XvKv

Website:www.bb.org.bd evsjv `k e vsk cöavb Kvh vjq WvKev bs 325 XvKv wwcvu g U Ae AdmvBU mycviwfkb 6 cšl, 1422 e½vã wwigm mvky jvi bs03 ZvwiLt 20 ww m ^i,2015 Lªxóvã cöavb wbe vnx evsjv ` k Kvh iz mkj

Website:www.bb.org.bd evsjv `k e vsk cöavb Kvh vjq WvKev bs 325 XvKv wwcvu g U Ae AdmvBU mycviwfkb 6 cšl, 1422 e½vã wwigm mvky jvi bs03 ZvwiLt 20 ww m ^i,2015 Lªxóvã cöavb wbe vnx evsjv ` k Kvh iz mkj

D wz Ò Master Circular: Loan Classification and Provisioning

cöavb Kvh vjq B nvi bs- 124 Fb Av`vq I kªbxweb vm wefvm B nvi bs- 05 mvbvjx e vsk wjwg UW cöavb Kvh vjq, XvKv wfwrj vý GÛ K Uªvj wwwfkb (K Uªvj wwcvu g U) 17 RyjvB, 2012 ZvwiL t ÐÐÐÐÐÐÐÐÐÐÐÐÐÐÐÐ mkj wrgg

cöavb Kvh vjq B nvi bs- 124 Fb Av`vq I kªbxweb vm wefvm B nvi bs- 05 mvbvjx e vsk wjwg UW cöavb Kvh vjq, XvKv wfwrj vý GÛ K Uªvj wwwfkb (K Uªvj wwcvu g U) 17 RyjvB, 2012 ZvwiL t ÐÐÐÐÐÐÐÐÐÐÐÐÐÐÐÐ mkj wrgg

Bank of China (Malaysia) Berhad Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 30 June 2014

Berhad Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 30 June 2014") Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 30 June 2014 CONTENTS 1. Introduction 2. Scope of Application 3. Capital 3.1 Capital Management 3.2 Capital Adequacy

Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 30 June 2014 CONTENTS 1. Introduction 2. Scope of Application 3. Capital 3.1 Capital Management 3.2 Capital Adequacy

Market Disclosure under Basel - II

Market Disclosure under Basel - II as on 31 st December, 2011 (Solo basis) a) Scope of application (a) The name of the top corporate International Finance Investment & Commerce Bank entity in the group

Market Disclosure under Basel - II as on 31 st December, 2011 (Solo basis) a) Scope of application (a) The name of the top corporate International Finance Investment & Commerce Bank entity in the group

Disclosures on Risk Based Capital (Basel II)

") Disclosures on Risk Based Capital (Basel II) As per the Bangladesh Bank BRPD Circular no. 24 dated August 03 of 2010 regarding the Guidelines on Risk Based Capital Adequacy of Banks under Basel II framework,

Disclosures on Risk Based Capital (Basel II) As per the Bangladesh Bank BRPD Circular no. 24 dated August 03 of 2010 regarding the Guidelines on Risk Based Capital Adequacy of Banks under Basel II framework,

Bank of China (Malaysia) Berhad Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 31 Dec 2014

Berhad Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 31 Dec 2014") Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 31 Dec 2014 CONTENTS 1. Introduction 2. Scope of Application 3. Capital 3.1 Capital Management 3.2 Capital Adequacy

Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 31 Dec 2014 CONTENTS 1. Introduction 2. Scope of Application 3. Capital 3.1 Capital Management 3.2 Capital Adequacy

Bank of China (Malaysia) Berhad Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 30 June 2015

Berhad Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 30 June 2015") Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 30 June 2015 CONTENTS 1. Introduction 2. Scope of Application 3. Capital 3.1 Capital Management 3.2 Capital Adequacy

Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 30 June 2015 CONTENTS 1. Introduction 2. Scope of Application 3. Capital 3.1 Capital Management 3.2 Capital Adequacy

Agrani Bank Limited. a) Minimum Capital Requirements to be maintained by a bank against credit, market and operational risks

Minimum Capital Requirements to be maintained by a bank against credit, market and operational risks") Agrani Bank Limited Disclosure Under Basel-II Qualitative and Quantitative Disclosures Under Pillar-III of Risk Based Capital Adequacy as of 31st December 2014 These disclosures have been made in accordance

Agrani Bank Limited Disclosure Under Basel-II Qualitative and Quantitative Disclosures Under Pillar-III of Risk Based Capital Adequacy as of 31st December 2014 These disclosures have been made in accordance

Qualitative and Quantitative disclosures Under Pillar- III of Risk Based Capital Adequacy (Basel-II) December 31, 2014

December 31, 2014") Qualitative and Quantitative disclosures Under Pillar- III of Risk Based Capital Adequacy (Basel-II) December 31, 2014 Market discipline has long been recognized as a key objective of the Risk Based Capital

Qualitative and Quantitative disclosures Under Pillar- III of Risk Based Capital Adequacy (Basel-II) December 31, 2014 Market discipline has long been recognized as a key objective of the Risk Based Capital

e `wkk gỳ ªv bxwz wefvm

e `wkk gỳ ªv bxwz wefvm evsjv `k e vsk cöavb Kvhv jq XvKv www.bb.org.bd 13 m Þ ^i, 2015 Lªxóvã GdBwcwW mvkz jvi bs- 11 ZvwiL t --------------------------- 29 fv`ö, 1422 e½vã cöavb wbe vnx/e e vcbv cwipvjk

e `wkk gỳ ªv bxwz wefvm evsjv `k e vsk cöavb Kvhv jq XvKv www.bb.org.bd 13 m Þ ^i, 2015 Lªxóvã GdBwcwW mvkz jvi bs- 11 ZvwiL t --------------------------- 29 fv`ö, 1422 e½vã cöavb wbe vnx/e e vcbv cwipvjk

PRUDENTIAL REGULATIONS FOR BANKS : SELECTED ISSUES. Bangladesh Bank

PRUDENTIAL REGULATIONS FOR BANKS : SELECTED ISSUES Bangladesh Bank January, 2014 PRUDENTIAL REGULATIONS FOR BANKS : SELECTED ISSUES [Updated till January, 2014] BANGLADESH BANK Table of Contents POLICY

PRUDENTIAL REGULATIONS FOR BANKS : SELECTED ISSUES Bangladesh Bank January, 2014 PRUDENTIAL REGULATIONS FOR BANKS : SELECTED ISSUES [Updated till January, 2014] BANGLADESH BANK Table of Contents POLICY

REGULATION ON BANK CAPITAL ADEQUACY. Article 1 Purpose and Scope

Pursuant to Article 23, paragraph 1, Article 35, paragraph 1, subparagraph 1.1 of the Law No. 03/L-209 on the Central Bank of the Republic of Kosovo (Official Gazette of the Republic of Kosovo, No. 77/16,

Pursuant to Article 23, paragraph 1, Article 35, paragraph 1, subparagraph 1.1 of the Law No. 03/L-209 on the Central Bank of the Republic of Kosovo (Official Gazette of the Republic of Kosovo, No. 77/16,

FUNDAMENTALS OF CREDIT ANALYSIS

FUNDAMENTALS OF CREDIT ANALYSIS 1 MV = Market Value NOI = Net Operating Income TV = Terminal Value RC = Replacement Cost DSCR = Debt Service Coverage Ratio 1. INTRODUCTION CR = Credit Risk Y.S = Yield

FUNDAMENTALS OF CREDIT ANALYSIS 1 MV = Market Value NOI = Net Operating Income TV = Terminal Value RC = Replacement Cost DSCR = Debt Service Coverage Ratio 1. INTRODUCTION CR = Credit Risk Y.S = Yield

e vswks cöwewa I bxwz wefvm evsjv `k e vsk cöavb Kvh vjq XvKv

website: www.bb.org.bd e vswks cöwewa I bxwz wefvm evsjv `k e vsk cöavb Kvh vjq XvKv 11 g, 2017 weaviwcww mvky jvi bs-07 ZvwiLt ------------------ 28 ˆekvL, 1424 e e vcbv cwipvjk/cöavb wbe vnx Kg KZ v

website: www.bb.org.bd e vswks cöwewa I bxwz wefvm evsjv `k e vsk cöavb Kvh vjq XvKv 11 g, 2017 weaviwcww mvky jvi bs-07 ZvwiLt ------------------ 28 ˆekvL, 1424 e e vcbv cwipvjk/cöavb wbe vnx Kg KZ v

In various tables, use of - indicates not meaningful or not applicable.

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

Supplementary Notes on the Financial Statements (continued)

") The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2014 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2014 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

Contents. Supplementary Notes on the Financial Statements (unaudited)

") The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2015 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2015 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

Basel II Pillar 3 Disclosure

Basel II Pillar 3 Disclosure 230 Overview 231 1.0 Scope of Application 231 2.0 Capital 2.1 Capital Adequacy Ratios 2.2 Capital Structure 2.3 Risk-Weighted Assets and Capital Requirements 238 3.0 Credit

Basel II Pillar 3 Disclosure 230 Overview 231 1.0 Scope of Application 231 2.0 Capital 2.1 Capital Adequacy Ratios 2.2 Capital Structure 2.3 Risk-Weighted Assets and Capital Requirements 238 3.0 Credit

THE INVESTOR FOR SECURITIES COMPANY. PILLAR III DISCLOSURE As of 31 December 2017

THE INVESTOR FOR SECURITIES COMPANY PILLAR III DISCLOSURE As of 31 December 2017 Table of Contents 1. Scope of Application... 3 1.1. Basis of Disclosure... 4 1.2. Frequency of Disclosures... 4 1.3. Material

THE INVESTOR FOR SECURITIES COMPANY PILLAR III DISCLOSURE As of 31 December 2017 Table of Contents 1. Scope of Application... 3 1.1. Basis of Disclosure... 4 1.2. Frequency of Disclosures... 4 1.3. Material

REGULATION ON BANK CAPITAL ADEQUACY. Article 1 Purpose and Scope

Pursuant to Article 35, paragraph1, to Article 35, paragraph 1, subparagraph 1.1 of the Law No. 03/L-209 of the Central Bank of the Republic of Kosovo (Official Gazette of the Republic of Kosovo, No. 77/16

Pursuant to Article 35, paragraph1, to Article 35, paragraph 1, subparagraph 1.1 of the Law No. 03/L-209 of the Central Bank of the Republic of Kosovo (Official Gazette of the Republic of Kosovo, No. 77/16

Supplementary Notes on the Financial Statements (continued)

") The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2013 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2013 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

Contents. Pillar 3 Disclosure. 02 Introduction. 03 Capital Adequacy. 10 Capital Structure. 11 Risk Management. 12 Credit Risk.

Contents 02 Introduction 03 Capital Adequacy 10 Capital Structure 11 Risk Management 12 Credit Risk 39 Securitization 39 Market Risk 40 Operational Risk 41 Equity Exposures in the Banking Book 42 Interest

Contents 02 Introduction 03 Capital Adequacy 10 Capital Structure 11 Risk Management 12 Credit Risk 39 Securitization 39 Market Risk 40 Operational Risk 41 Equity Exposures in the Banking Book 42 Interest

Capital adequacy in accordance with BASEL II

Capital adequacy in accordance with BASEL II Basel accords are the international standards for creating regulations about how much capital is needed to put aside to guard against the types of financial

Capital adequacy in accordance with BASEL II Basel accords are the international standards for creating regulations about how much capital is needed to put aside to guard against the types of financial

disclosures on risk based capital (Basel II)

") disclosures on risk based capital (Basel II) ANNUAL REPORT 2012 79 disclosure on risk based capital (Basel II) Scope of Application a) The name of the top corporate entity in the group to which this guidelines

disclosures on risk based capital (Basel II) ANNUAL REPORT 2012 79 disclosure on risk based capital (Basel II) Scope of Application a) The name of the top corporate entity in the group to which this guidelines

CREDIT RISK GRADING MANUAL NBFI. Non Banking Financial Institution

CREDIT RISK GRADING MANUAL NBFI Non Banking Financial Institution JUNE, 2007 Credit Risk Grading Manual - NBFI 1 CREDIT RISK GRADING MANUAL - NBFI Bangladesh Bank vide its BRPD Circular No.18 dated December

CREDIT RISK GRADING MANUAL NBFI Non Banking Financial Institution JUNE, 2007 Credit Risk Grading Manual - NBFI 1 CREDIT RISK GRADING MANUAL - NBFI Bangladesh Bank vide its BRPD Circular No.18 dated December

Market Discipline Disclosures on Risk Based Capital (Basel II) as on

as on") Market Discipline Disclosures on Risk Based Capital (Basel II) as on 31.12.2013 The purpose of Market Discipline in Basel- II is to establish more transparent and more disciplined financial market so that

Market Discipline Disclosures on Risk Based Capital (Basel II) as on 31.12.2013 The purpose of Market Discipline in Basel- II is to establish more transparent and more disciplined financial market so that

Rating Methodology Banks and Financial Institutions

CREDIT RATING INFORMATION AND SERVICES LIMITED Rating Methodology Banks and Financial Institutions CREDIT RATING PHILOSOPHY CRISL follows structured rating methodologies for each sectors of the national

CREDIT RATING INFORMATION AND SERVICES LIMITED Rating Methodology Banks and Financial Institutions CREDIT RATING PHILOSOPHY CRISL follows structured rating methodologies for each sectors of the national

Bank of China (Malaysia) Berhad Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 31 December 2017

Berhad Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 31 December 2017") Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 31 December 2017 CONTENTS 1. Introduction 2. Scope of Application 3. Capital 3.1 Capital Management 3.2 Capital Adequacy

Risk Weighted Capital Adequacy Framework (Basel II) Disclosure Requirements (Pillar 3) 31 December 2017 CONTENTS 1. Introduction 2. Scope of Application 3. Capital 3.1 Capital Management 3.2 Capital Adequacy

Market Discloser under Pillar-III of BASEL-II: 2013

Market Discloser under Pillar-III of BASEL-II: 2013 A) Scope of Application Qualitative Discloser a) The name of the top corporate entity in the group to which this guidelines applies b) An outline of

Market Discloser under Pillar-III of BASEL-II: 2013 A) Scope of Application Qualitative Discloser a) The name of the top corporate entity in the group to which this guidelines applies b) An outline of

Statement of Guidance

Statement of Guidance Credit Risk Classification, Provisioning and Management Policy and Development Division Page 1 of 20 Table of Contents 1. Statement of Objectives... 3 2. Scope... 3 3. Terminology...

Statement of Guidance Credit Risk Classification, Provisioning and Management Policy and Development Division Page 1 of 20 Table of Contents 1. Statement of Objectives... 3 2. Scope... 3 3. Terminology...

CREDIT RISK GRADING MANUAL BANK

CREDIT RISK GRADING MANUAL BANK JUNE, 2007 Credit Risk Grading Manual - BANK 1 CREDIT RISK GRADING MANUAL - BANK Bangladesh Bank vide its BRPD Circular No.18 dated December 11, 2005 advised all Banks to

CREDIT RISK GRADING MANUAL BANK JUNE, 2007 Credit Risk Grading Manual - BANK 1 CREDIT RISK GRADING MANUAL - BANK Bangladesh Bank vide its BRPD Circular No.18 dated December 11, 2005 advised all Banks to

CREDIT RATING INFORMATION & SERVICES LIMITED

Rating Methodology SME CREDIT RATING INFORMATION & SERVICES LIMITED Nakshi Homes (4th & 5th Floor), 6/1A, Segunbagicha, Dhaka 1000, Bangladesh Tel: 717 3700 1, Fax: 956 5783 Email: crisl@bdonline.com Web:

Rating Methodology SME CREDIT RATING INFORMATION & SERVICES LIMITED Nakshi Homes (4th & 5th Floor), 6/1A, Segunbagicha, Dhaka 1000, Bangladesh Tel: 717 3700 1, Fax: 956 5783 Email: crisl@bdonline.com Web:

Basel II Pillar 3 disclosures

Basel II Pillar 3 disclosures 6M10 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG and its consolidated

Basel II Pillar 3 disclosures 6M10 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG and its consolidated

Disclosures on Risk Based Capital (BASEL II) For the year ended 31 December 2014

For the year ended 31 December 2014") Disclosures on Risk Based Capital (BASEL II) For the year ended 31 December 2014 Introduction In accordance to Pillar III of the revised Framework for International Convergence of Capital Measurement and

Disclosures on Risk Based Capital (BASEL II) For the year ended 31 December 2014 Introduction In accordance to Pillar III of the revised Framework for International Convergence of Capital Measurement and

C A Y M A N I S L A N D S MONETARY AUTHORITY

Statement of Guidance Credit Risk Classification, Provisioning and Management Policy and Development Division Page 1 of 22 Table of Contents 1 Statement of Objectives... 3 2 Scope... 3 3 Terminology...

Statement of Guidance Credit Risk Classification, Provisioning and Management Policy and Development Division Page 1 of 22 Table of Contents 1 Statement of Objectives... 3 2 Scope... 3 3 Terminology...

Disclosures on Risk Based Capital under Basel-II For the Year Ended December 31, 2016

Disclosures on Risk Based Capital under Basel-II For the Year Ended December 31, 2016 Disclosures under Pillar III- Market Discipline For the year ended 31 st December 2016 Overview The Basel-II disclosures

Disclosures on Risk Based Capital under Basel-II For the Year Ended December 31, 2016 Disclosures under Pillar III- Market Discipline For the year ended 31 st December 2016 Overview The Basel-II disclosures

CREDIT RATING INFORMATION & SERVICES LIMITED

Rating Methodology BANKS AND FINANCIAL INSTITUTIONS CREDIT RATING INFORMATION & SERVICES LIMITED Nakshi Homes (4th & 5th Floor), 6/1A, Segunbagicha, Dhaka 1000, Bangladesh Tel: 717 3700 1, Fax: 956 5783

Rating Methodology BANKS AND FINANCIAL INSTITUTIONS CREDIT RATING INFORMATION & SERVICES LIMITED Nakshi Homes (4th & 5th Floor), 6/1A, Segunbagicha, Dhaka 1000, Bangladesh Tel: 717 3700 1, Fax: 956 5783

Pubali Bank Limited Market Discipline-Pillar-III Disclosures under Basel-II As on 31 December 2010

Capital Adequacy under Basel-II Banks operating in Bangladesh are maintaining capital since 1996 on the basis of risk weighted assets in line with the Basel Committee on Banking Supervision (BCBS) capital

Capital Adequacy under Basel-II Banks operating in Bangladesh are maintaining capital since 1996 on the basis of risk weighted assets in line with the Basel Committee on Banking Supervision (BCBS) capital

PILLAR 3 DISCLOSURE As at 31 December 2017

PILLAR 3 DISCLOSURE As at 31 December 2017 Overview The Pillar 3 Disclosure is required under the Bank Negara Malaysia ("BNM")'s Capital Adequacy Framework for Islamic Banks ("CAFIB"), which is the equivalent

PILLAR 3 DISCLOSURE As at 31 December 2017 Overview The Pillar 3 Disclosure is required under the Bank Negara Malaysia ("BNM")'s Capital Adequacy Framework for Islamic Banks ("CAFIB"), which is the equivalent

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD ( D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II)

BERHAD ( D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II)") INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) Pillar 3 Disclosure for Financial Year Ended 31 December 2015 Table of Contents 1.0 OVERVIEW... 1 2.0 CAPITAL

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) Pillar 3 Disclosure for Financial Year Ended 31 December 2015 Table of Contents 1.0 OVERVIEW... 1 2.0 CAPITAL

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD ( D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II)

BERHAD ( D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II)") INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) Pillar 3 Disclosure for the Half-Year Ended 30 June 2016 Table of Contents 1.0 OVERVIEW... 1 2.0 CAPITAL

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) Pillar 3 Disclosure for the Half-Year Ended 30 June 2016 Table of Contents 1.0 OVERVIEW... 1 2.0 CAPITAL

Basel II Pillar 3 disclosures 6M 09

Basel II Pillar 3 disclosures 6M 09 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group

Basel II Pillar 3 disclosures 6M 09 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD ( D)

BERHAD ( D)") Company No. 911666-D INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (Incorporated in Malaysia) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) PILLAR 3 DISCLOSURE

Company No. 911666-D INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (Incorporated in Malaysia) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) PILLAR 3 DISCLOSURE

FINANCIAL DUE DILIGENCE OF CANDIDATE PARTICIPATING FINANCIAL INSTITUTIONS (PFIs)

") Second Small and Medium-Sized Enterprise Development Project (RRP BAN 36200) FINANCIAL DUE DILIGENCE OF CANDIDATE PARTICIPATING FINANCIAL INSTITUTIONS (PFIs) A. Bangladesh Bank Credit Rating of Selected

Second Small and Medium-Sized Enterprise Development Project (RRP BAN 36200) FINANCIAL DUE DILIGENCE OF CANDIDATE PARTICIPATING FINANCIAL INSTITUTIONS (PFIs) A. Bangladesh Bank Credit Rating of Selected

UNAUDITED SUPPLEMENTARY FINANCIAL INFORMATION

1. Capital charge for credit, market and operational risks The bases of regulatory capital calculation for credit risk, market risk and operational risk are described in Note 4.5 to the Financial Statements

1. Capital charge for credit, market and operational risks The bases of regulatory capital calculation for credit risk, market risk and operational risk are described in Note 4.5 to the Financial Statements

Banking Regulation & Policy Department Bangladesh Bank Head Office Dhaka

Banking Regulation & Policy Department Bangladesh Bank Head Office Dhaka Website: www.bb.org.bd September 23, 2012 BRPD Circular No. 15 Date: ------------------------------ Ashwin 08, 1419 Chief Executives

Banking Regulation & Policy Department Bangladesh Bank Head Office Dhaka Website: www.bb.org.bd September 23, 2012 BRPD Circular No. 15 Date: ------------------------------ Ashwin 08, 1419 Chief Executives

Disclosures on Capital Adequacy and Market Discipline - Pillar III Based on 31 December, 2017

Qualitative disclosures Disclosures on Capital Adequacy and Market Discipline - Pillar III Based on 31 December, 2017 This disclosure is given as per the requirement of Bangladesh Bank s Prudential Guideline

Qualitative disclosures Disclosures on Capital Adequacy and Market Discipline - Pillar III Based on 31 December, 2017 This disclosure is given as per the requirement of Bangladesh Bank s Prudential Guideline

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD ( D)

BERHAD ( D)") Company No. 911666 D INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (Incorporated in Malaysia) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) PILLAR 3 DISCLOSURE

Company No. 911666 D INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (Incorporated in Malaysia) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) PILLAR 3 DISCLOSURE

Basel II Pillar 3 Disclosure As at 31 December Overview. 1.0 Scope of Application

Basel II Pillar 3 Disclosure As at 31 December 2011 Overview The Group adopted the Standardised Approach in determining the capital requirements for credit risk and market risk and applied the Basic Indicator

Basel II Pillar 3 Disclosure As at 31 December 2011 Overview The Group adopted the Standardised Approach in determining the capital requirements for credit risk and market risk and applied the Basic Indicator

Collective Allowances - Sound Credit Risk Assessment and Valuation Practices for Financial Instruments at Amortized Cost

Guideline Subject: Collective Allowances - Sound Credit Risk Assessment and Valuation Practices for Category: Accounting No: C-5 Date: October 2001 Revised: July 2010 This guideline outlines the regulatory

Guideline Subject: Collective Allowances - Sound Credit Risk Assessment and Valuation Practices for Category: Accounting No: C-5 Date: October 2001 Revised: July 2010 This guideline outlines the regulatory

Citibank Berhad Pillar 3 Disclosure June 2018

Citibank Berhad Pillar 3 Disclosure June 2018 Contents Page No 1. Introduction 3 2. Capital Adequacy 4 3. Capital Structure 11 4. Credit Risk 12 5. Securitization 38 6. Equity in the Banking Book 38 7.

Citibank Berhad Pillar 3 Disclosure June 2018 Contents Page No 1. Introduction 3 2. Capital Adequacy 4 3. Capital Structure 11 4. Credit Risk 12 5. Securitization 38 6. Equity in the Banking Book 38 7.

PILLAR 3 DISCLOSURE As at 31 December 2018

PILLAR 3 DISCLOSURE As at 31 December 2018 Overview The Pillar 3 Disclosure is required under the Bank Negara Malaysia ("BNM")'s Capital Adequacy Framework for Islamic Banks ("CAFIB"), which is the equivalent

PILLAR 3 DISCLOSURE As at 31 December 2018 Overview The Pillar 3 Disclosure is required under the Bank Negara Malaysia ("BNM")'s Capital Adequacy Framework for Islamic Banks ("CAFIB"), which is the equivalent

HONG LEONG INVESTMENT BANK BERHAD Company no: P (Incorporated in Malaysia)

") BASEL II PILLAR 3 DISCLOSURES FOR THE FINANCIAL PERIOD ENDED 31 DECEMBER 2011 BASEL II PILLAR 3 DISCLOSURES FOR THE FINANCIAL PERIOD ENDED 31 DECEMBER 2011 Content Page INTRODUCTION 1 SCOPE OF APPLICATION

BASEL II PILLAR 3 DISCLOSURES FOR THE FINANCIAL PERIOD ENDED 31 DECEMBER 2011 BASEL II PILLAR 3 DISCLOSURES FOR THE FINANCIAL PERIOD ENDED 31 DECEMBER 2011 Content Page INTRODUCTION 1 SCOPE OF APPLICATION

RATING METHODOLOGY SME. Rating Methodology SME

Rating Methodology S M E CREDIT RATING INFORMATION & SERVICES LIMITED N ak s h i H om es ( 4 th & 5 th F l oor), 6/ 1A, S egu nbagi c h a, D h ak a 1 00 0, B an gl a d e sh Tel : 7 1 7 3 70 0 1, F a x:

Rating Methodology S M E CREDIT RATING INFORMATION & SERVICES LIMITED N ak s h i H om es ( 4 th & 5 th F l oor), 6/ 1A, S egu nbagi c h a, D h ak a 1 00 0, B an gl a d e sh Tel : 7 1 7 3 70 0 1, F a x:

BANGKOK BANK BERHAD (Company No W)

") BANGKOK BANK BERHAD (Company No. 299740-W) Risk Weighted Capital Adequacy Framework (BASEL II) - Pillar 3 Disclosures As at 30 June 2014 ATTESTATION BY CHIEF EXECUTIVE OFFICER PURSUANT TO RISK WEIGHTED

BANGKOK BANK BERHAD (Company No. 299740-W) Risk Weighted Capital Adequacy Framework (BASEL II) - Pillar 3 Disclosures As at 30 June 2014 ATTESTATION BY CHIEF EXECUTIVE OFFICER PURSUANT TO RISK WEIGHTED

ANNUAL DISCLOSURE UNDER PILLAR III OF BASEL II AS OF DECEMBER 31, 2010 RISK MANAGEMENT

ANNUAL DISCLOSURE UNDER PILLAR III OF BASEL II AS OF DECEMBER 31, 2010 RISK MANAGEMENT Bangladeshi Banking Industry already entered into the Basel II regime with effect from Jan 01, 2010, so as CBL. The

ANNUAL DISCLOSURE UNDER PILLAR III OF BASEL II AS OF DECEMBER 31, 2010 RISK MANAGEMENT Bangladeshi Banking Industry already entered into the Basel II regime with effect from Jan 01, 2010, so as CBL. The

BANGKOK BANK BERHAD (Company No W)

") BANGKOK BANK BERHAD (Company No. 299740-W) Risk Weighted Capital Adequacy Framework (BASEL II) - Pillar 3 Disclosures As at 31 December 2013 ATTESTATION BY CHIEF EXECUTIVE OFFICER PURSUANT TO RISK WEIGHTED

BANGKOK BANK BERHAD (Company No. 299740-W) Risk Weighted Capital Adequacy Framework (BASEL II) - Pillar 3 Disclosures As at 31 December 2013 ATTESTATION BY CHIEF EXECUTIVE OFFICER PURSUANT TO RISK WEIGHTED

MARKET DISCLOSURE FOR DEC 09 UNDER PILLAR-III OF BASEL II Risk Management Department The City Bank Limited

MARKET DISCLOSURE FOR DEC 09 UNDER PILLAR-III OF BASEL II Risk Management Department The City Bank Limited 1. Consequent upon globalization, Banks and other financial institutions all over the world are

MARKET DISCLOSURE FOR DEC 09 UNDER PILLAR-III OF BASEL II Risk Management Department The City Bank Limited 1. Consequent upon globalization, Banks and other financial institutions all over the world are

Basel II Pillar 3 Disclosures Year ended 31 December 2009

DBS Group Holdings Ltd and its subsidiaries (the Group) have adopted Basel II as set out in the revised Monetary Authority of Singapore Notice to Banks No. 637 (Notice on Risk Based Capital Adequacy Requirements

DBS Group Holdings Ltd and its subsidiaries (the Group) have adopted Basel II as set out in the revised Monetary Authority of Singapore Notice to Banks No. 637 (Notice on Risk Based Capital Adequacy Requirements

Pillar-3 Disclosure under Basel-III Norms December 31, 2017

Pillar-3 Disclosure under Basel-III Norms as on 31.12.2017 (i) Qualitative Disclosures: Table: DF-2: CAPITAL ADEQUACY Bank s approach to assess the adequacy of its capital to support its current and future

Pillar-3 Disclosure under Basel-III Norms as on 31.12.2017 (i) Qualitative Disclosures: Table: DF-2: CAPITAL ADEQUACY Bank s approach to assess the adequacy of its capital to support its current and future

J.P. MORGAN CHASE BANK BERHAD (Incorporated in Malaysia)

") FOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2012 0100B3/py FOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2012 1 OVERVIEW The Pillar 3 Disclosures is governed under the Bank Negara Malaysia ( BNM ) s revised Risk-

FOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2012 0100B3/py FOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2012 1 OVERVIEW The Pillar 3 Disclosures is governed under the Bank Negara Malaysia ( BNM ) s revised Risk-

SECTION I.1 - CREDIT RISK: STANDARDISED APPROACH General Principles

SECTION I.1 - CREDIT RISK: STANDARDISED APPROACH General Principles 1.0 Under the Standardised Approach, the exposure value of an asset shall be a) the balance-sheet value, and b) the resultant value of

SECTION I.1 - CREDIT RISK: STANDARDISED APPROACH General Principles 1.0 Under the Standardised Approach, the exposure value of an asset shall be a) the balance-sheet value, and b) the resultant value of

Disclosures under Pillar III- Market Discipline

Disclosures under Pillar III- Market Discipline A) Scope of application Qualitative Disclosures: a) The name of the Financial Institutions GSP Finance Company (Bangladesh) Limited b) An outline of differences

Disclosures under Pillar III- Market Discipline A) Scope of application Qualitative Disclosures: a) The name of the Financial Institutions GSP Finance Company (Bangladesh) Limited b) An outline of differences

Market Discipline-Pillar-III Disclosures under Basel-II

Market Discipline-Pillar-III Disclosures under Basel-II (Ref. Annual Report-2010) Page No. 62-71 Capital Adequacy under Basel-II Banks operating in Bangladesh are maintaining capital since 1996 on the

Market Discipline-Pillar-III Disclosures under Basel-II (Ref. Annual Report-2010) Page No. 62-71 Capital Adequacy under Basel-II Banks operating in Bangladesh are maintaining capital since 1996 on the

Pillar-3 Disclosure under Basel-III Norms

Pillar-3 Disclosure as on 31.12.2016 Table: DF-2: CAPITAL ADEQUACY (i) Qualitative Disclosures: Bank s approach to assess the adequacy of its capital to support its current and future activities. With

Pillar-3 Disclosure as on 31.12.2016 Table: DF-2: CAPITAL ADEQUACY (i) Qualitative Disclosures: Bank s approach to assess the adequacy of its capital to support its current and future activities. With

(i) Pillar 1 Outlines the minimum regulatory capital that banking institutions must hold against the credit, market and operational risks assumed.

Pillar 1 Outlines the minimum regulatory capital that banking institutions must hold against the credit, market and operational risks assumed.") Industrial and Commercial Bank of China (Malaysia) Berhad (Company No. 839839 M) (Incorporated in Malaysia) 1 Risk-Weighted Capital Adequacy Framework (Basel II) Pillar 3 Disclosure 1.0 Overview The Pillar

Industrial and Commercial Bank of China (Malaysia) Berhad (Company No. 839839 M) (Incorporated in Malaysia) 1 Risk-Weighted Capital Adequacy Framework (Basel II) Pillar 3 Disclosure 1.0 Overview The Pillar

UBS Saudi Arabia (A SAUDI JOINT STOCK COMPANY) Pillar III Disclosure As of 31 December 2014

Pillar III Disclosure As of 31 December 2014") UBS Saudi Arabia King Fahad Road Tatweer Towers Tower 4, 9 th Floor PO Box 75724 Riyadh 11588 Kingdom of Saudi Arabia Tel. +966 (0) 11 203 8000 www.ubs.com UBS Saudi Arabia (A SAUDI JOINT STOCK COMPANY)

UBS Saudi Arabia King Fahad Road Tatweer Towers Tower 4, 9 th Floor PO Box 75724 Riyadh 11588 Kingdom of Saudi Arabia Tel. +966 (0) 11 203 8000 www.ubs.com UBS Saudi Arabia (A SAUDI JOINT STOCK COMPANY)

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD ( D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II)

BERHAD ( D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II)") INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) Pillar 3 Disclosure for Financial Year Ended 31 December 2013 TABLE OF CONTENTS 1.0 Overview 1 2.0 Capital

INDIA INTERNATIONAL BANK (MALAYSIA) BERHAD (911666-D) RISK WEIGHTED CAPITAL ADEQUACY (BASEL II) Pillar 3 Disclosure for Financial Year Ended 31 December 2013 TABLE OF CONTENTS 1.0 Overview 1 2.0 Capital

UBS Saudi Arabia (A SAUDI JOINT STOCK COMPANY) Pillar III Disclosure As of 31 December 2017

Pillar III Disclosure As of 31 December 2017") UBS Saudi Arabia King Fahad Road Tatweer Towers Tower 4, 9 th Floor PO Box 75724 Riyadh 11588 Kingdom of Saudi Arabia Tel. +966 (0) 11 203 8000 www.ubs.com UBS Saudi Arabia (A SAUDI JOINT STOCK COMPANY)

UBS Saudi Arabia King Fahad Road Tatweer Towers Tower 4, 9 th Floor PO Box 75724 Riyadh 11588 Kingdom of Saudi Arabia Tel. +966 (0) 11 203 8000 www.ubs.com UBS Saudi Arabia (A SAUDI JOINT STOCK COMPANY)

Pillar-3 Disclosure under Basel-III Norms June 30, 2017

Pillar-3 Disclosure under Basel-III Norms as on 30.06.2017 (i) Qualitative Disclosures: Table: DF-2: CAPITAL ADEQUACY Bank s approach to assess the adequacy of its capital to support its current and future

Pillar-3 Disclosure under Basel-III Norms as on 30.06.2017 (i) Qualitative Disclosures: Table: DF-2: CAPITAL ADEQUACY Bank s approach to assess the adequacy of its capital to support its current and future

Pillar-3 Disclosure under Basel-III Norms

Pillar-3 Disclosure (As on 30.06.2015) Table: DF-2: CAPITAL ADEQUACY Qualitative Disclosures: Bank s approach to assess the adequacy of its capital to support its current and future activities. The Bank

Pillar-3 Disclosure (As on 30.06.2015) Table: DF-2: CAPITAL ADEQUACY Qualitative Disclosures: Bank s approach to assess the adequacy of its capital to support its current and future activities. The Bank

PILLAR 3 DISCLOSURE CITIBANK BERHAD

CITIBANK BERHAD PILLAR 3 DISCLOSURE CONTENTS Introduction Capital Adequacy Capital Structure Risk Management Credit Risk Securitization Market Risk Operational Risk Equities Interest Rate Risk/ Rate of

CITIBANK BERHAD PILLAR 3 DISCLOSURE CONTENTS Introduction Capital Adequacy Capital Structure Risk Management Credit Risk Securitization Market Risk Operational Risk Equities Interest Rate Risk/ Rate of

ASSET CLASSIFICATION, PROVISIONING AND SUSPENSION OF INTEREST

FINANCIAL INSTITUTIONS COMMISSION PRUDENTIAL REGULATION FIC-PR-02 ASSET CLASSIFICATION, PROVISIONING AND SUSPENSION OF INTEREST Arrangement of Paragraphs PARAGRAPH 1. Short Title 2. Authorization 3. Application

FINANCIAL INSTITUTIONS COMMISSION PRUDENTIAL REGULATION FIC-PR-02 ASSET CLASSIFICATION, PROVISIONING AND SUSPENSION OF INTEREST Arrangement of Paragraphs PARAGRAPH 1. Short Title 2. Authorization 3. Application

BANGKOK BANK BERHAD (Company No W)

") BANGKOK BANK BERHAD (Company No. 299740-W) Risk Weighted Capital Adequacy Framework (BASEL II) - Pillar 3 Disclosures As at 30 June 2012 ATTESTATION BY CHIEF EXECUTIVE OFFICER PURSUANT TO RISK WEIGHTED

BANGKOK BANK BERHAD (Company No. 299740-W) Risk Weighted Capital Adequacy Framework (BASEL II) - Pillar 3 Disclosures As at 30 June 2012 ATTESTATION BY CHIEF EXECUTIVE OFFICER PURSUANT TO RISK WEIGHTED

Basel II Pillar 3 Disclosure As at 31 December Overview. 1.0 Scope of Application

Basel II Pillar 3 Disclosure As at 31 December 2013 Overview The Royal Bank of Scotland Berhad and its subsidiaries (collectively the Group ) adopted the Standardised Approach in determining the capital

Basel II Pillar 3 Disclosure As at 31 December 2013 Overview The Royal Bank of Scotland Berhad and its subsidiaries (collectively the Group ) adopted the Standardised Approach in determining the capital

PILLAR 3 REPORT FOR THE FINANCIAL YEAR ENDED 31 MARCH 2017

PILLAR 3 REPORT FOR THE FINANCIAL YEAR ENDED 31 MARCH 2017 Overview Bank Negara Malaysia's ("BNM") guidelines on capital adequacy require Alliance Islamic Bank Berhad ("the Bank") to maintain an adequate

PILLAR 3 REPORT FOR THE FINANCIAL YEAR ENDED 31 MARCH 2017 Overview Bank Negara Malaysia's ("BNM") guidelines on capital adequacy require Alliance Islamic Bank Berhad ("the Bank") to maintain an adequate

ICB Islamic Bank Limited (ICBIBL) Head Office, Dhaka ANNUAL DISCLOSURE UNDER PILLAR III OF BASEL II AS OF DECEMBER 31, 2011

Head Office, Dhaka ANNUAL DISCLOSURE UNDER PILLAR III OF BASEL II AS OF DECEMBER 31, 2011") Scope and purpose ICB Islamic Bank Limited (ICBIBL) Head Office, Dhaka ANNUAL DISCLOSURE UNDER PILLAR III OF BASEL II AS OF DECEMBER 31, 2011 The purpose of disclosures in pursuance of the Market Discipline

Scope and purpose ICB Islamic Bank Limited (ICBIBL) Head Office, Dhaka ANNUAL DISCLOSURE UNDER PILLAR III OF BASEL II AS OF DECEMBER 31, 2011 The purpose of disclosures in pursuance of the Market Discipline

BANGKOK BANK BERHAD (Company No W)

") BANGKOK BANK BERHAD (Company No. 299740-W) Risk Weighted Capital Adequacy Framework (BASEL II) - Pillar 3 Disclosure As at 31 December 2011 CONTENTS Page 1. Introduction 1 2. Scope of Application 1 3.

BANGKOK BANK BERHAD (Company No. 299740-W) Risk Weighted Capital Adequacy Framework (BASEL II) - Pillar 3 Disclosure As at 31 December 2011 CONTENTS Page 1. Introduction 1 2. Scope of Application 1 3.

Default & Transition Study. July CARE s DEFAULT AND TRANSITION STUDY (For the period March 31, 2005 March 31, 2015) Summary

Summary") July 2015 Default & Transition Study CARE s DEFAULT AND TRANSITION STUDY 2015 (For the period March 31, 2005 March 31, 2015) Summary CARE commenced its rating activity in 1993, and has over the years acquired

July 2015 Default & Transition Study CARE s DEFAULT AND TRANSITION STUDY 2015 (For the period March 31, 2005 March 31, 2015) Summary CARE commenced its rating activity in 1993, and has over the years acquired

Pillar 3 Disclosure. Sumitomo Mitsui Trust Bank (Thai) Public Company Limited. March 31 st, Pillar 3 Disclosures 31 March 2018

Public Company Limited. March 31 st, Pillar 3 Disclosures 31 March 2018") Sumitomo Mitsui Trust Bank (Thai) Public Company Limited Pillar 3 Disclosure March 31 st, 2018 Sumitomo Mitsui Trust Bank (Thai) Public Company Limited 1 Contents 1. Scope of Application... 3 2. Capital...

Sumitomo Mitsui Trust Bank (Thai) Public Company Limited Pillar 3 Disclosure March 31 st, 2018 Sumitomo Mitsui Trust Bank (Thai) Public Company Limited 1 Contents 1. Scope of Application... 3 2. Capital...

PILLAR 3 DISCLOSURES (CONSOLIDATED) AS ON

AS ON") PILLAR 3 DISCLOSURES (CONSOLIDATED) AS ON 30.06.2017 Qualitative Disclosures DF-2: CAPITAL ADEQUACY (a) A summary discussion of the Bank s approach to assessing the adequacy of its capital to support current