SPECIAL RULES FOR FORECLOSURES ON HOMES. Joseph M. Licare, Esq. Bryan Cave LLP New York, New York

|

|

|

- Austin Kelly

- 5 years ago

- Views:

Transcription

1 SPECIAL RULES FOR FORECLOSURES ON HOMES by Joseph M. Licare, Esq. Bryan Cave LLP New York, New York 81

2 82

3 Special Rules For Foreclosures On Homes A. 90-day Pre-Foreclosure Notice and Related Requirements 1. RPAPL 1304: 90-day notice a. Pre-foreclosure notice i. informs the borrower that: 1. he/she is at risk of losing his/her home 2. attached is a list of government approved housing counseling agencies in your area 3. loss mitigation programs may be available, including loan modification options ii. at least 90 days before a lender, an assignee, or a mortgage loan servicer commences legal action against the borrower, including mortgage foreclosure, such lender, assignee, or mortgage loan servicer shall give notice to the borrower 1. Additional notice requirements: this notice must be in at least 14- point type which shall include: YOU COULD LOSE YOUR HOME. PLEASE READ THE FOLLOWING NOTICE CAREFULLY. iii. states an amount that can be paid in order to cure the default iv. 12 months b. Additional Requirements i. Must be sent by registered or certified mail and also by first class mail to the last known address of the borrower 1. If the last known address of the borrower is not the property in foreclosure, then the notice must also be sent to the property subject of the mortgage ii. Must include a list of at least 5 local housing counseling agencies ( that serve in the region where the borrower resides ) 1. *There is currently no definition to the term region iii. iv. Must be mailed in a separate envelope from any other mailing or notice Must be a home loan 1. Definition of home loan a. (1) borrower is a natural person b. (2) debt incurred primarily for personal, family, or household purposes c. (3) loan secured by a mortgage on real estate of one to four family dwelling used or intended to be used as the borrower s primary dwelling d. (4) property located in New York c. Failure to send this notice requires dismissal of the action. Aurora Loan Servs. v. Weisblum, 85 A.D.3d 95, N.Y.S.2d 609, 616 (2d Dep t 2011); see also Deutsche Bank Nat l Trust Co. v. Spanos, 102 A.D.3d 909, 910, 961 N.Y.S.2d 200, 202 (2d Dep t 2013); Meyerson Capital X LLC v. Kats, 33 Misc.3d 1017, , 935 N.Y.S.2d 257, 259 (Sup. Ct. Kings Co. 2011). i. There are very few cases that address the circumstances in which a 90-day notice is excused for non-residency 83 1

4 1. NOT an excuse service elsewhere, even out of state. IndyMac Federal Bank, FSB v. Black, No. 2268/06, 2009 WL (Sup. Ct. Rensselaer Co. Jan. 23, 2009). 2. NOT enough proof that the mortgaged premises was not borrower s primary residence bank affidavit and affirmation of counsel in support of its position when the mortgage loan documents and loan application evidenced borrower s intention to occupy the premises as her primary residence. Credit Based Asset Servicing and Securitizations LLC v. Stokes, No. 4703/09, 2012 WL (N.Y. City Crim. Ct. Sept. 24, 2012). ii. Accredited Home Lenders, Inc. v. Hughes, 22 Misc.3d 323, , 866 N.Y.S.2d 860, 863 (Sup. Ct. Essex Co. 2008) concluded that residency is determined from the time the loan was entered into and noted that the goal of RPAPL 1304 regarding occupancy is to remove owners of investment properties or second homes from the ambit of the statute 1. Therefore, when evaluating residency, important documents that may support an argument for excusing the 90-day notice include: a. Original loan application b. Tax returns, W-2s, Bank Statements, Earnings Statements (compelling proof of borrower s alternative residence). Butler Capital Corp. v. Canasta, 26 Misc.3d 598, , 891 N.Y.S.2d 238, 243 (Sup. Ct. Suffolk Co. 2009) i. See also HSBC Bank USA, Nat l Ass n v. McKenna, 37 Misc.3d 885, , 952 N.Y.S.2d 746, (Sup. Ct. Kings Co. 2012) court still found the mortgaged property to be the borrower s residence, and thus, a 90-notice was necessary 2. RPAPL 1306: filing 90-day notice with Department of Financial Services a. A lender, assignee, or mortgage loan servicer must file the 90-day notice, and other certain information, with the Superintendent of the Department of Financial Services within 3 business days after (i) the mailing of the 90-day pre-foreclosure notice [or] (ii) the notice required by Section 9-611(f) of the New York Uniform Commercial Code (non-judicial foreclosure of a co-op share). b. Purpose: i. (1) monitor the extent of foreclosure filings ii. (2) monitor loan types that are the subject of pre-foreclosure notices iii. (3) provide available public and private foreclosure prevention and counseling services to borrowers at risk of foreclosure 3. Notice of Intent to Accelerate a. AKA: 30-day notice b. Notice informs the borrower(s) that: i. the Loan is in serious default because the required payments have not been made ii. the borrowers have a right to cure the default iii. if the default is not cured by a certain date, the Loan will be accelerated 84 2

5 4. National Mortgage Servicer Settlement May 2012 a. Product of extensive negotiations between federal and state regulators and the major banks b. Terms do NOT extend to mortgages serviced by FNMA and FHLMC c. In place for 3.5 years d. Banks involved: (1) Bank of America (2) Chase (3) Citibank (4) Wells Fargo (5) Ally Financial e. 14-day pre-foreclosure notice i. IN ALL STATES Servicer shall send borrowers a statement setting forth facts supporting Servicer s or holder s right to foreclose and containing the information in: 1. I.B.6 items available upon borrower request 2. I.B.10 account statement 3. I.C.2 and I.C.3 ownership statement 4. IV.B.13 loss mitigation statement f. Dual Tracking Prohibitions i. Similar rules from the CFPB ii. MEANS: moving forward with foreclosure while a loss mitigation request is pending iii. RULE: a borrower who completes an application by day 120 of delinquency, or within 30 days after a referral to foreclosure letter, is protected from any foreclosure referral or action until the application is decided iv. CAVEAT: the application MUST be complete B. Required Allegations In Foreclosure Complaint 1. Allegations / Notices with the Foreclosure Complaint a. RPAPL 1320: Special Summons Requirement in Private Residence Cases i. In an action to foreclose a mortgage on a residential property, the summons shall contain a notice in boldface in the following form: NOTICE YOU ARE IN DANGER OF LOSING YOUR HOME ii. Additional required language is specifically stated within RPAPL 1320 b. RPAPL 1302: Foreclosure of High-Cost Home Loans and Sub-prime Home Loans i. Any complaint served in a proceeding initiated pursuant to this article relating to a high-cost home loan or a subprime home loan, as such terms are defined in Sections 6-l & 6-m of the NYS Banking Law ii. Additional required language is specifically stated within RPAPL

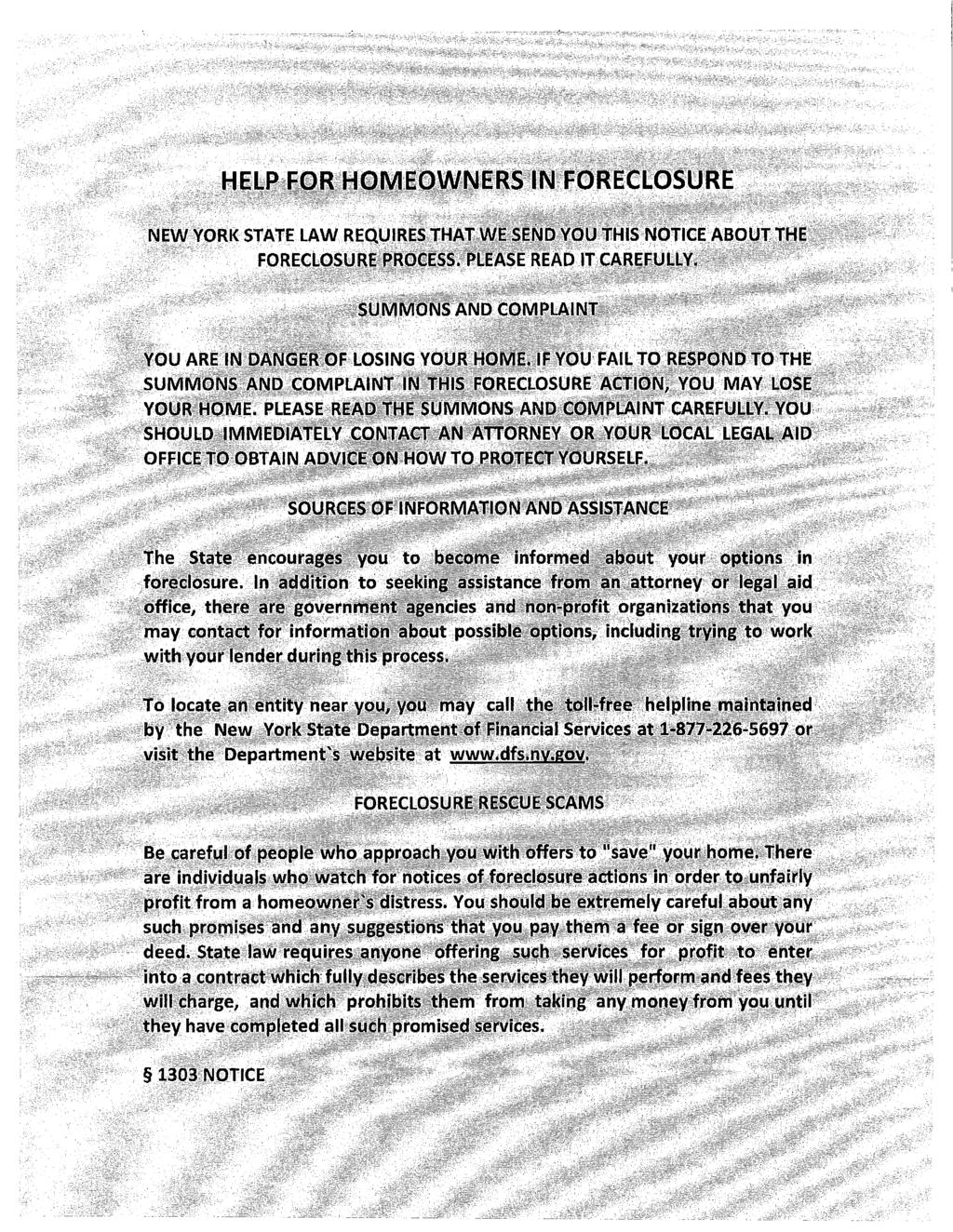

6 c. RPAPL 1303: Help for Homeowners in Foreclosure Notice i. Notice shall provide notice to the mortgagor with regard to information and assistance about the foreclosure process ii. Required language is specifically stated within RPAPL 1303 iii. Additional Requirements: this notice shall be: 1. delivered with the summons and complaint to commence the foreclosure action 2. in bold, 14-point type 3. printed on colored paper that is other than the color of the summons and complaint 4. title of notice shall be in bold, 20-point type 5. printed on its own page d. RPAPL 1306: A lender, assignee, or mortgage loan servicer must file the 90- day notice, and other certain information, with the Superintendent of the Department of Financial Services within 3 business days after the mailing of the 90-day pre-foreclosure notice C. Post-Complaint Filing Requirements 1. Request for Judicial Intervention (RJI), 22 N.Y.C.R.R a a. Applicable to residential mortgage foreclosure actions, involving a home loan secured by a mortgage on a one to four-family dwelling or condo in which the defendant is a resident of the property subject to foreclosure b. Must be filed at the time of proof of service of the summons and complaint is filed c. Shall contain the name, address, telephone number and address, if available, of the defendant in the action d. Shall request that a settlement conference be scheduled (3408 conference) e. The RJI is usually filed by the Plaintiff, but it can be filed by Plaintiff or Defendant 2. CPLR 3012-b: Certificate of Merit a. Replaced the Lippman Affirmation (OCA Rule AO/431/11) because the Lippman Affirmation only required the foreclosing plaintiff to state that the plaintiff had standing to foreclose b. Began August 30, 2013 the documents required to commence a foreclosure action now include a certificate of merit in addition to the summons and complaint c. Required in all foreclosure actions, affecting owner-occupied residential property d. Designed: to address the problem of the concerning shadow docket e. Goal: ensure that borrowers are able to reach the settlement conference quickly, thereby allowing them to meet with the lender and the court to explore options to avoid foreclosure, such as a loan modification f. Requirements: i. (1) Identify the representatives of the plaintiff with whom the attorney has consulted regarding the mortgage under foreclosure ii. (2) state that there is a reasonable basis for the commencement of the action and that the plaintiff is entitled to enforce the mortgage, security agreement and note 86 4

7 iii. (3) provide copies of the mortgage, security agreement and note, assignment(s) of mortgage, modification agreements, consolidation agreements, or other instruments of indebtedness g. IMPORTANT CAVEAT: failure to comply with this provision may be cause for dismissal of the complaint without prejudice 3. RPAPL 1307: Duty to Maintain Foreclosed Property a. Plaintiff maintenance obligation i. Until: 1. Ownership has been transferred, and 2. Deed is recorded b. Applies to residential real property where a plaintiff who obtains a judgment of foreclosure and sale, that is: i. (1) vacant, or ii. (2) becomes vacant after a judgment of foreclosure and sale, or iii. (3) abandoned by the mortgagor but still occupied by a tenant c. Intent: to help municipalities where foreclosures are high and blight is rampant, and to protect tenants who have been left high and dry by their landlords D. Notices to Tenants 1. RPAPL 1303: a. Requires: Plaintiff in an action to foreclose a mortgage on a one to four-family dwelling to serve the statutory Home for Homeowners in Foreclosure notice on tenants b. Requirements: i. Shall be delivered within 10 days of service of the summons and complaint ii. Shall be in bold, 14-point type iii. Shall be printed on colored paper that is other than the color of the summons and complaint iv. The title of the notice shall be in bold, 20-point type v. Shall be on its own page vi. Buildings with fewer than 5 dwelling units, the Notice: 1. (1) shall be delivered to the tenant, by certified mail, return receipt requested AND 2. (2) by first-class mail to the tenant s address at the property if the identity of the tenant is known to the plaintiff AND 3. (3) by first-class mail to occupant if the identity of the tenant is not known to the plaintiff vii. Buildings with 5 or more dwelling units, a legible copy of the Notice shall be posted on the outside of each entrance and exit of the building 2. RPAPL 1305: Rights of Tenants to Remain in Foreclosed Property a. Applies: a successor-in-interest: who acquires title to residential real estate as a result of a judgment of foreclosure and sale, or other disposition during a 87 5

8 foreclosure proceeding must send written notice to all tenants informing them of their rights, as well as the name and address of the new owner b. ONLY protects tenants who are still paying their rent (eviction can occur at any time if the tenant does not pay rent pursuant to the lease) c. Designed: i. gives tenants who reside in a foreclosed property the right to remain in occupancy on the same terms and conditions that were in effect at the time of entry of the judgment of foreclosure and sale for 90 days from the date they receive the 1305 notice from a successor-in-interest in the property [OR] until the end of the lease (whichever is greater) d. Exception for Single Unit: an exception exists that limits a tenant s right to occupancy to 90 days if the successor-in-interest who acquires title intends to occupy a single unit as his or her primary residence AND if the unit is not subject to a federal or state statutory system of subsidy or other federal or state statutory scheme e. Definition of tenant: anyone who pays market rent; the former homeowner is not a tenant f. Written or oral lease agreements g. This section does not supersede any other rights tenants have 4. RPAPL 1307: Duty to Maintain Foreclosed Property a. Plaintiff maintenance obligation i. Until: 1. Ownership has been transferred, and 2. Deed is recorded b. Applies to residential real property where a plaintiff who obtains a judgment of foreclosure and sale, that is: i. (1) vacant, or ii. (2) becomes vacant after a judgment of foreclosure and sale, or iii. (3) abandoned by the mortgagor but still occupied by a tenant c. Intent: to help municipalities where foreclosures are high and blight is rampant, and to protect tenants who have been left high and dry by their landlords E. Mandatory Settlement Conference for Foreclosure on Homes 1. CPLR 3408: Mandatory Settlement Conferences In Residential Foreclosure Action a. In any residential action involving a home loan as defined in RPAPL 1304, in which defendant is a resident of the property subject to foreclosure, the court shall hold a mandatory conference within 60 days after the date when proof of service upon such defendant is filed with the county clerk b. Designed: mandatory conferences are held for the purpose of holding settlement discussions pertaining to the relative rights and obligations of the parties under the mortgage loan documents, including, but not limited to, determining whether the parties can reach a mutually agreeable resolution to help the defendant avoid losing his or her home, and evaluating the potential for a resolution (loan modification if possible) 88 6

9 c. Both plaintiff and defendant shall negotiate in good faith to reach a mutually agreeable resolution, including a loan modification, if possible d. Exhibits: i. Court Worksheet ii. General Loan Modification Checklist iii. Court Foreclosure Conference Notice iv. Request for Judicial Intervention v. Court Orders 1. Dismissal Orders (CPLR 3215 & 3216) 2. Notice To Resume Prosecution of Action Mortgage Loan Workouts/Modifications of Homeowner Loans A. Overview Of Major Modification Programs i. Home Affordable Modification Program (HAMP) 1. Goal: to reach a monthly payment of principal, interest, taxes and insurance (PITI) that is 31% of the borrower s monthly gross income 2. Follows a waterfall analysis to get to the 31% target payment a. Reduce interest rate to as low as 2% b. Extend term of years to 40 years c. Forbear principal (to non-interest bearing balloon payment at maturity) 3. Modification is not required dependent on positive NPV test, meaning that a modification is more profitable to the mortgagee than continued foreclosure ii. HAMP Tier 2 1. Modification program for: a. Homeowners who did not qualify for or defaulted on a HAMP Tier 1 trial or permanent modification b. Investment properties (meaning: properties occupied by tenants or mortgagor s 2 nd home) c. Homeowners whose loan payments (PITI) are less than 31% of monthly gross income iii. FHA Loans 1. Most modification / forbearance programs are based on monthly net income 2. Programs a. Forbearance (Formal and Informal) b. FHA Loan Modification c. Partial Claim d. FHA HAMP 89 7

10 iv. Department of Justice Program 1. Significant difference from many other programs: Principal Forgiveness / Reduction 2. Goal: to reach a monthly payment of principal, interest, taxes and insurance (PITI) that is 31% of the borrower s monthly gross income 3. Waterfall Analysis: a. (1) Capitalize delinquent interest and late fees b. (2) Forgive principal to achieve 25% DTI, not requiring LTV below 100% c. (3) After step #2, if DTI is greater than 31%, reduce interest down to 2% to achieve 31% DTI, calculating interest steps as in HAMP d. (4) After step #3, if DTI is greater than 31%, forbear principal to achieve 31% DTI e. (5) Limit forbearance and forgiveness to not result in less than 70% LTV f. (6) NPV must be positive i. Key factors to NPV: value of property and gross income of borrower v. 2MP (for 2 nd Liens) 1. Part of HAMP 2. Requires modification of 2 nd lien when 1 st lien is modified under HAMP and 2 nd lienholder participates in 2MP vi. Home Affordable Unemployment Program (UP) 1. Temporary forbearance program vii. Traditional Modification Programs 1. FNMA and FHLMC Standard Loan Modifications (prior to HAMP) 2. Lender / Servicer in-house modification programs B. Related Issues: i. Negotiations in Good Faith; Findings of Bad Faith 1. Interpretation of CPLR 3408 ii. Investor Guidelines (ex: Hudson City) iii. Private Investors iv. Trusts 1. FNMA 2. FHLMC 3. REMIC v. Courts / Investment Properties 1. Some Court s inclusion of investment properties into the 3408 conference process 90 8

11 91

12 92

13 93

14 94

15 95

16 96

17 97

18 98

19 99

20 100

21 101

22 102

23 103

24 104

25 105

26 106

27 107

28 108

29 109

30 110

31 111

32 112

33 113

34 114

35 115

36 116

37 117

38 118

39 119

40 120

41 121

42 122

NEW YORK S RESIDENTIAL MORTGAGE FORECLOSURE PROCESS. Western New York Law Center, Inc. Tanisha T. Bramwell, Esq.

NEW YORK S RESIDENTIAL MORTGAGE FORECLOSURE PROCESS Western New York Law Center, Inc. Tanisha T. Bramwell, Esq. Mortgage Foreclosure In a mortgage foreclosure, the holder of the mortgage files a lawsuit

NEW YORK S RESIDENTIAL MORTGAGE FORECLOSURE PROCESS Western New York Law Center, Inc. Tanisha T. Bramwell, Esq. Mortgage Foreclosure In a mortgage foreclosure, the holder of the mortgage files a lawsuit

RE: Servicer Compliance with Newly Enacted Statutory Changes to the New York State Mortgage Foreclosure Law / Chapter 507 of the Laws of 2009

By E mail March 2, 2010 RE: Servicer Compliance with Newly Enacted Statutory Changes to the New York State Mortgage Foreclosure Law / Chapter 507 of the Laws of 2009 Dear SONYMA Servicer: On December 15,

By E mail March 2, 2010 RE: Servicer Compliance with Newly Enacted Statutory Changes to the New York State Mortgage Foreclosure Law / Chapter 507 of the Laws of 2009 Dear SONYMA Servicer: On December 15,

2016 Foreclosure Law Amendments and Vacant and Abandoned Property Legislation. Two Major Prongs to Legislation

2016 Foreclosure Law Amendments and Vacant and Abandoned Property Legislation November 2016 Jacob Inwald Legal Services NYC Two Major Prongs to Legislation Addressing Zombie Properties: Vacant and Abandoned

2016 Foreclosure Law Amendments and Vacant and Abandoned Property Legislation November 2016 Jacob Inwald Legal Services NYC Two Major Prongs to Legislation Addressing Zombie Properties: Vacant and Abandoned

Flagstar Bank, FSB, Plaintiffs, against. Bevan Walker and Pamella M. Walker a/k/a Pamella Walker, et al, Defendants.

Page 1 of 7 [*1] Flagstar Bank, FSB v Walker 2012 NY Slip Op 22148 Decided on May 31, 2012 Supreme Court, Kings County Kramer, J. Published by New York State Law Reporting Bureau pursuant to Judiciary

Page 1 of 7 [*1] Flagstar Bank, FSB v Walker 2012 NY Slip Op 22148 Decided on May 31, 2012 Supreme Court, Kings County Kramer, J. Published by New York State Law Reporting Bureau pursuant to Judiciary

session of the legislature, significant changes to New York s judicial residential

2016 Amendments to New York Foreclosure Settlement Conference and Predicate Notice Laws Jacob Inwald Director of Foreclosure Prevention Legal Services NYC As part of a package of legislation enacted in

2016 Amendments to New York Foreclosure Settlement Conference and Predicate Notice Laws Jacob Inwald Director of Foreclosure Prevention Legal Services NYC As part of a package of legislation enacted in

INTRODUCTION TO ILLINOIS MORTGAGE FORECLOSURE PROCESS

INTRODUCTION TO ILLINOIS MORTGAGE FORECLOSURE PROCESS JAMES BRADY, SUPERVISORY ATTORNEY THE FORECLOSURE PROCESS Illinois is a judicial foreclosure state (one of about 22 states) Process is governed by

INTRODUCTION TO ILLINOIS MORTGAGE FORECLOSURE PROCESS JAMES BRADY, SUPERVISORY ATTORNEY THE FORECLOSURE PROCESS Illinois is a judicial foreclosure state (one of about 22 states) Process is governed by

The National Mortgage Settlement: Loan Modifications and Servicing Standards

The National Mortgage Settlement: Loan Modifications and Servicing Standards MHA Trusted Advisor Webinar July 24, 2013 Sarah Bolling Mancini Home Defense Program of the Atlanta Legal Aid Society, Inc.

The National Mortgage Settlement: Loan Modifications and Servicing Standards MHA Trusted Advisor Webinar July 24, 2013 Sarah Bolling Mancini Home Defense Program of the Atlanta Legal Aid Society, Inc.

Waushara County Circuit Court Rules

Waushara County Circuit Court Rules (Sixth Judicial District) Small Claims Rules Facsimile Transmission of Documents to the Court Civil Rule-Mortgage Foreclosure Small Claims Rules I. These rules are made

Waushara County Circuit Court Rules (Sixth Judicial District) Small Claims Rules Facsimile Transmission of Documents to the Court Civil Rule-Mortgage Foreclosure Small Claims Rules I. These rules are made

ASSEMBLY, No STATE OF NEW JERSEY. 217th LEGISLATURE INTRODUCED FEBRUARY 22, 2016

ASSEMBLY, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED FEBRUARY, 0 Sponsored by: Assemblyman PATRICK J. DIEGNAN, JR. District (Middlesex) Assemblyman JERRY GREEN District (Middlesex, Somerset and

ASSEMBLY, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED FEBRUARY, 0 Sponsored by: Assemblyman PATRICK J. DIEGNAN, JR. District (Middlesex) Assemblyman JERRY GREEN District (Middlesex, Somerset and

CHAPTER 244 FORECLOSURE AND REDEMPTION OF MORTGAGES*

CHAPTER 244 FORECLOSURE AND REDEMPTION OF MORTGAGES* *selected sections relating to foreclosures by sale Section 1 Foreclosure by entry or action; continued possession Section 1. A mortgagee may, after

CHAPTER 244 FORECLOSURE AND REDEMPTION OF MORTGAGES* *selected sections relating to foreclosures by sale Section 1 Foreclosure by entry or action; continued possession Section 1. A mortgagee may, after

FILLING OUT THE ANSWER

EMPIRE JUSTICE CENTER 31 FILLING OUT THE ANSWER Below is the form Answer provided in this guidebook. STEP 1: FILL OUT THE CAPTION OF THE ANSWER - As shown in the sample Answer below, fill in the top part

EMPIRE JUSTICE CENTER 31 FILLING OUT THE ANSWER Below is the form Answer provided in this guidebook. STEP 1: FILL OUT THE CAPTION OF THE ANSWER - As shown in the sample Answer below, fill in the top part

UNITED STATES DISTRICT COURT DISTRICT OF MASSACHUSETTS CIVIL ACTION NO GAO. VINIETA LAWRENCE, Plaintiff, BANK OF AMERICA, N.A., Defendant.

Lawrence v. Bank Of America Doc. 33 UNITED STATES DISTRICT COURT DISTRICT OF MASSACHUSETTS CIVIL ACTION NO. 15-11486-GAO VINIETA LAWRENCE, Plaintiff, v. BANK OF AMERICA, N.A., Defendant. OPINION AND ORDER

Lawrence v. Bank Of America Doc. 33 UNITED STATES DISTRICT COURT DISTRICT OF MASSACHUSETTS CIVIL ACTION NO. 15-11486-GAO VINIETA LAWRENCE, Plaintiff, v. BANK OF AMERICA, N.A., Defendant. OPINION AND ORDER

Making Home Affordable. The Second Lien Modification Program (2MP) for Servicers

for Servicers") Making Home Affordable The Second Lien Modification Program (2MP) for Servicers Agenda 1 2 3 4 5 6 7 8 9 10 11 12 13 Overview Eligibility Lien Matching Process Evaluation 2MP Modification Waterfall 2MP

Making Home Affordable The Second Lien Modification Program (2MP) for Servicers Agenda 1 2 3 4 5 6 7 8 9 10 11 12 13 Overview Eligibility Lien Matching Process Evaluation 2MP Modification Waterfall 2MP

2MP Servicer Training 1

Making Home Affordable The Second Lien Modification Program (2MP) for Servicers Agenda 1 2 3 4 5 6 7 8 9 10 11 12 13 Overview Eligibility Lien Matching Process Evaluation 2MP Modification Waterfall 2MPTrial

Making Home Affordable The Second Lien Modification Program (2MP) for Servicers Agenda 1 2 3 4 5 6 7 8 9 10 11 12 13 Overview Eligibility Lien Matching Process Evaluation 2MP Modification Waterfall 2MPTrial

SENATE, No STATE OF NEW JERSEY. 218th LEGISLATURE INTRODUCED JANUARY 25, 2018

SENATE, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED JANUARY, 0 Sponsored by: Senator RONALD L. RICE District (Essex) Senator TROY SINGLETON District (Burlington) SYNOPSIS Codifies the Judiciary's

SENATE, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED JANUARY, 0 Sponsored by: Senator RONALD L. RICE District (Essex) Senator TROY SINGLETON District (Burlington) SYNOPSIS Codifies the Judiciary's

[Second Reprint] ASSEMBLY, No STATE OF NEW JERSEY. 213th LEGISLATURE INTRODUCED JUNE 8, 2009

![[Second Reprint] ASSEMBLY, No STATE OF NEW JERSEY. 213th LEGISLATURE INTRODUCED JUNE 8, 2009](/thumbs/76/73127638.jpg "[Second Reprint] ASSEMBLY, No STATE OF NEW JERSEY. 213th LEGISLATURE INTRODUCED JUNE 8, 2009") [Second Reprint] ASSEMBLY, No. 0 STATE OF NEW JERSEY 1th LEGISLATURE INTRODUCED JUNE, 00 Sponsored by: Assemblywoman BONNIE WATSON COLEMAN District 1 (Mercer) Assemblywoman MILA M. JASEY District (Essex)

[Second Reprint] ASSEMBLY, No. 0 STATE OF NEW JERSEY 1th LEGISLATURE INTRODUCED JUNE, 00 Sponsored by: Assemblywoman BONNIE WATSON COLEMAN District 1 (Mercer) Assemblywoman MILA M. JASEY District (Essex)

Page 1 of 6 [*1] Citibank N.A. v McCray 2013 NY Slip Op 51931(U) Decided on November 22, 2013 Supreme Court, Bronx County González, J. Published by New York State Law Reporting Bureau pursuant to Judiciary

Page 1 of 6 [*1] Citibank N.A. v McCray 2013 NY Slip Op 51931(U) Decided on November 22, 2013 Supreme Court, Bronx County González, J. Published by New York State Law Reporting Bureau pursuant to Judiciary

Effective Foreclosure Timeline Management Reference Guide

Effective Foreclosure Timeline Management Reference Guide A foreclosure timeline is the number of days it takes to process a foreclosure, from the due date of the last paid installment (DDLPI) to the foreclosure

Effective Foreclosure Timeline Management Reference Guide A foreclosure timeline is the number of days it takes to process a foreclosure, from the due date of the last paid installment (DDLPI) to the foreclosure

Home Affordable Unemployment Program (UP)

") Home Affordable Unemployment Program (UP) Training for Servicers 1 Agenda 1 2 Phase 1 Phase 2 Phase 3 3 4 Overview UP Process Evaluation Phase Forbearance Period Transition Phase Reporting Requirements

Home Affordable Unemployment Program (UP) Training for Servicers 1 Agenda 1 2 Phase 1 Phase 2 Phase 3 3 4 Overview UP Process Evaluation Phase Forbearance Period Transition Phase Reporting Requirements

Servicing and Loss Mitigation. Jennifer Schultz, Esq. Community Legal Services, Inc W. Erie Ave. Philadelphia, PA

Servicing and Loss Mitigation Jennifer Schultz, Esq. Community Legal Services, Inc. 1410 W. Erie Ave. Philadelphia, PA 19140 jschultz@clsphila.org What kind of loan do you have? FHA GSE Origination-based

Servicing and Loss Mitigation Jennifer Schultz, Esq. Community Legal Services, Inc. 1410 W. Erie Ave. Philadelphia, PA 19140 jschultz@clsphila.org What kind of loan do you have? FHA GSE Origination-based

Pre- Foreclosure Step By Step Compliance Checklist & Order Form

GOLDEN WEST FORECLOSURE SERVICE, INC. 611 Veterans Blvd., Suite 217, Redwood City, CA 94063-1401 Ph. (888) 982-3888 Fax. (650) 369-2261 Website: www.goldenwestforeclosure.com Email: gwfs@earthlink.net

GOLDEN WEST FORECLOSURE SERVICE, INC. 611 Veterans Blvd., Suite 217, Redwood City, CA 94063-1401 Ph. (888) 982-3888 Fax. (650) 369-2261 Website: www.goldenwestforeclosure.com Email: gwfs@earthlink.net

SB 558 Oregon s New Mandatory Resolution Conference Law Helping Homeowners Facing Foreclosure (2013)

") SB 558 Oregon s New Mandatory Resolution Conference Law Helping Homeowners Facing Foreclosure (2013) By Phillip C. Querin, QUERIN LAW, LLC Website: www.q-law.com Introduction. After a false start in 2012,

SB 558 Oregon s New Mandatory Resolution Conference Law Helping Homeowners Facing Foreclosure (2013) By Phillip C. Querin, QUERIN LAW, LLC Website: www.q-law.com Introduction. After a false start in 2012,

Office of Massachusetts Attorney General Maura Healey. One Ashburton Place Boston, MA (617)

") Office of Massachusetts Attorney General Maura Healey One Ashburton Place Boston, MA 02108 (617) 727-2200 www.mass.gov/ago The Job of the Attorney General Attorney General Maura Healey is the chief lawyer

Office of Massachusetts Attorney General Maura Healey One Ashburton Place Boston, MA 02108 (617) 727-2200 www.mass.gov/ago The Job of the Attorney General Attorney General Maura Healey is the chief lawyer

MINNESOTA REAL ESTATE FORECLOSURES: 21 COMMON QUESTIONS & ANSWERS

MINNESOTA REAL ESTATE FORECLOSURES: 21 COMMON QUESTIONS & ANSWERS Our Creditors Remedies attorneys answer the most asked questions from their clients. Practice Area: CREDITORS REMEDIES, BANKRUPTCY & WORK-OUT

MINNESOTA REAL ESTATE FORECLOSURES: 21 COMMON QUESTIONS & ANSWERS Our Creditors Remedies attorneys answer the most asked questions from their clients. Practice Area: CREDITORS REMEDIES, BANKRUPTCY & WORK-OUT

Foreclosure Hodge Podge. Deanne R. Stodden Managing Partner Castle Meinhold & Stawiarski, LLC

Foreclosure Hodge Podge Deanne R. Stodden Managing Partner Castle Meinhold & Stawiarski, LLC Agenda Title insurance options HAMP and HAFA update The eviction process and PTAFA Amos v. Aspen Alps 123, LLC

Foreclosure Hodge Podge Deanne R. Stodden Managing Partner Castle Meinhold & Stawiarski, LLC Agenda Title insurance options HAMP and HAFA update The eviction process and PTAFA Amos v. Aspen Alps 123, LLC

Streamline HAMP Modification Process. Training for Servicers

Streamline HAMP Modification Process Training for Servicers Agenda 1 2 3 64 5 Overview Eligibility Criteria Streamline HAMP Policy and Streamline HAMP NPV Tool Streamline HAMP Process Resources 2 MHA Offers

Streamline HAMP Modification Process Training for Servicers Agenda 1 2 3 64 5 Overview Eligibility Criteria Streamline HAMP Policy and Streamline HAMP NPV Tool Streamline HAMP Process Resources 2 MHA Offers

Department of Legislative Services Maryland General Assembly 2010 Session

Department of Legislative Services Maryland General Assembly 2010 Session HB 472 FISCAL AND POLICY NOTE Revised House Bill 472 (Delegate Niemann and the Speaker, et al.) (By Request - Administration) Environmental

Department of Legislative Services Maryland General Assembly 2010 Session HB 472 FISCAL AND POLICY NOTE Revised House Bill 472 (Delegate Niemann and the Speaker, et al.) (By Request - Administration) Environmental

Servicemember Financial Protection

Servicemember Financial Protection Outlook Live Webinar September 10, 2012 An Interagency Discussion of Recent Servicemember Financial Protection Guidance and Compliance with the Servicemembers Civil Relief

Servicemember Financial Protection Outlook Live Webinar September 10, 2012 An Interagency Discussion of Recent Servicemember Financial Protection Guidance and Compliance with the Servicemembers Civil Relief

Home Affordable Modification Program (HAMP )

") Home Affordable Modification Program (HAMP ) Training for Trusted Advisors Objectives 1 2 3 4 5 6 Step 1 Step 2 Step 3 Step 4 Step 5 7 8 MHA Program Highlights HAMP Overview Eligibility Criteria Protections

Home Affordable Modification Program (HAMP ) Training for Trusted Advisors Objectives 1 2 3 4 5 6 Step 1 Step 2 Step 3 Step 4 Step 5 7 8 MHA Program Highlights HAMP Overview Eligibility Criteria Protections

HAMP Servicer Training 1

Home Affordable Modification Program (HAMP ) Training for Servicers Part 2 of 2 MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure Transition from Home Ownership

Home Affordable Modification Program (HAMP ) Training for Servicers Part 2 of 2 MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure Transition from Home Ownership

REFORMS Overview of Reforms to Mortgage and Foreclosure Processing Standards in the Settlement

Office of WV Attorney General Darrell McGraw MORTGAGE FORECLOSURE SETTLEMENT REFORMS Overview of Reforms to Mortgage and Foreclosure Processing Standards in the Settlement As negotiated nationally I. RETURN

Office of WV Attorney General Darrell McGraw MORTGAGE FORECLOSURE SETTLEMENT REFORMS Overview of Reforms to Mortgage and Foreclosure Processing Standards in the Settlement As negotiated nationally I. RETURN

HAMP Trusted Advisor 1

Home Affordable Modification Program ( ) Training for Trusted Advisors Making Home Affordable February February 2016 2016 Objectives 1 MHA Program Highlights 2 Overview 3 Eligibility Criteria 4 Protections

Home Affordable Modification Program ( ) Training for Trusted Advisors Making Home Affordable February February 2016 2016 Objectives 1 MHA Program Highlights 2 Overview 3 Eligibility Criteria 4 Protections

Navigating the Loan Modification Process Part III. Presented by: Empire Justice Center Kevin Purcell, Esq.

Navigating the Loan Modification Process Part III Presented by: Empire Justice Center Kevin Purcell, Esq. 1 Other MHA Programs HAMP Tier Two Principal Reduction Alternative Home Affordable Unemployment

Navigating the Loan Modification Process Part III Presented by: Empire Justice Center Kevin Purcell, Esq. 1 Other MHA Programs HAMP Tier Two Principal Reduction Alternative Home Affordable Unemployment

Home Affordable Modification Program (HAMP )

") Home Affordable Modification Program (HAMP ) Training for Servicers Part 2 of 2 MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure Transition from Home Ownership

Home Affordable Modification Program (HAMP ) Training for Servicers Part 2 of 2 MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure Transition from Home Ownership

STATE OF NEW JERSEY. ASSEMBLY, No th LEGISLATURE

ASSEMBLY, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED FEBRUARY, 0 Sponsored by: Assemblywoman CLEOPATRA G. TUCKER District (Essex) Assemblywoman BRITNEE N. TIMBERLAKE District (Essex and Passaic)

ASSEMBLY, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED FEBRUARY, 0 Sponsored by: Assemblywoman CLEOPATRA G. TUCKER District (Essex) Assemblywoman BRITNEE N. TIMBERLAKE District (Essex and Passaic)

U.S. Bank, N.A., as Trustee for Bear Stearns asset Backed Securities, AC1, Plaintiff, against. Jorge Luis Rodriguez, et al., Defendants.

Page 1 of 11 [*1] U.S. Bank, N.A. v Rodriguez 2013 NY Slip Op 23298 Decided on August 5, 2013 Supreme Court, Bronx County Torres, J. Published by New York State Law Reporting Bureau pursuant to Judiciary

Page 1 of 11 [*1] U.S. Bank, N.A. v Rodriguez 2013 NY Slip Op 23298 Decided on August 5, 2013 Supreme Court, Bronx County Torres, J. Published by New York State Law Reporting Bureau pursuant to Judiciary

Announcement SVC September 21, 2010

Announcement SVC-2010-15 September 21, 2010 Updates to Fannie Mae's Forbearance, Income Eligibility, and Home Affordable Modification Program Requirements. Introduction In this Announcement, Fannie Mae

Announcement SVC-2010-15 September 21, 2010 Updates to Fannie Mae's Forbearance, Income Eligibility, and Home Affordable Modification Program Requirements. Introduction In this Announcement, Fannie Mae

PLM Loan Management Services, Inc. 46 N. Second Street, Campbell, CA TEL (408) FAX (408)

FAX (408)") PLM Loan Management Services, Inc. 46 N. Second Street, Campbell, CA 95008 TEL (408) 370-4030 FAX (408) 370-5488 Today s Date FORECLOSURE INSTRUCTIONS AND AGREEMENT - California Instructions for Starting

PLM Loan Management Services, Inc. 46 N. Second Street, Campbell, CA 95008 TEL (408) 370-4030 FAX (408) 370-5488 Today s Date FORECLOSURE INSTRUCTIONS AND AGREEMENT - California Instructions for Starting

HAMP Home Affordable Modification Program UPDATE

HAMP Home Affordable Modification Program UPDATE The whole purpose of HAMP is to try and prevent foreclosures. Homeowners have to prove a hardship and go through a protocol that proves this is a good use

HAMP Home Affordable Modification Program UPDATE The whole purpose of HAMP is to try and prevent foreclosures. Homeowners have to prove a hardship and go through a protocol that proves this is a good use

2012 BASIC SKILLS IN VERMONT PRACTICE & PROCEDURE. Debtor-Creditor Law

Vermont Bar Association Seminar Materials 2012 BASIC SKILLS IN VERMONT PRACTICE & PROCEDURE Debtor-Creditor Law August 23 & 24, 2012 Windjammer Conference Center South Burlington, VT Faculty: Jennifer

Vermont Bar Association Seminar Materials 2012 BASIC SKILLS IN VERMONT PRACTICE & PROCEDURE Debtor-Creditor Law August 23 & 24, 2012 Windjammer Conference Center South Burlington, VT Faculty: Jennifer

Available at:

Available at: http://www.dfs.ny.gov/legal/regulations/emergency/banking/ar419tx.htm Regulations Adopted on an Emergency Basis Part 419. Servicing Mortgage Loans: Business Conduct Rules (Statutory Authority:

Available at: http://www.dfs.ny.gov/legal/regulations/emergency/banking/ar419tx.htm Regulations Adopted on an Emergency Basis Part 419. Servicing Mortgage Loans: Business Conduct Rules (Statutory Authority:

A G & R ABDULAZIZ, GROSSBART & RUDMAN

A G & R ABDULAZIZ, GROSSBART & RUDMAN PRIVATE WORKS MECHANIC S LIEN, STOP NOTICE AND BOND CHECKLIST I. WHAT IS A MECHANIC S LIEN?: A. A Mechanic s Lien is a lien on real estate that has been improved.

A G & R ABDULAZIZ, GROSSBART & RUDMAN PRIVATE WORKS MECHANIC S LIEN, STOP NOTICE AND BOND CHECKLIST I. WHAT IS A MECHANIC S LIEN?: A. A Mechanic s Lien is a lien on real estate that has been improved.

Servicing Guide. North Carolina Housing Finance Agency. Revised October 2017

North Carolina Housing Finance Agency Servicing Guide Revised October 2017 Page 1 Servicing Guide Table of Contents Note: The North Carolina Housing Finance Agency s Servicing Guide ( NCHFA s Servicing

North Carolina Housing Finance Agency Servicing Guide Revised October 2017 Page 1 Servicing Guide Table of Contents Note: The North Carolina Housing Finance Agency s Servicing Guide ( NCHFA s Servicing

FANNIE MAE AND FREDDIE MAC FLEX MODIFICATION NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION SEPTEMBER 26, 2017

FANNIE MAE AND FREDDIE MAC FLEX MODIFICATION NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION SEPTEMBER 26, 2017 1 Diane Cipollone, Esq. Consultant to National Fair Housing Alliance Former Director

FANNIE MAE AND FREDDIE MAC FLEX MODIFICATION NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION SEPTEMBER 26, 2017 1 Diane Cipollone, Esq. Consultant to National Fair Housing Alliance Former Director

Case 1:12-cv RMC Document 14 Filed 04/04/12 Page 1 of 92

Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 1 of 92 Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 2 of 92 Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 3 of 92 Case 1:12-cv-00361-RMC

Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 1 of 92 Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 2 of 92 Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 3 of 92 Case 1:12-cv-00361-RMC

Case 1:12-cv RMC Document 11 Filed 04/04/12 Page 1 of 86

Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 1 of 86 Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 2 of 86 Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 3 of 86 Case 1:12-cv-00361-RMC

Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 1 of 86 Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 2 of 86 Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 3 of 86 Case 1:12-cv-00361-RMC

Senate Bill No. 818 CHAPTER 404

Senate Bill No. 818 CHAPTER 404 An act to amend Section 2924 of, to amend and repeal Sections 2923.4, 2923.5, 2923.6, 2923.7, 2924.12, 2924.15, and 2924.17 of, to add Sections 2923.55, 2924.9, 2924.10,

Senate Bill No. 818 CHAPTER 404 An act to amend Section 2924 of, to amend and repeal Sections 2923.4, 2923.5, 2923.6, 2923.7, 2924.12, 2924.15, and 2924.17 of, to add Sections 2923.55, 2924.9, 2924.10,

Foreclosure Diversion Program Information Session. Understanding and Preparing for Mediation

Foreclosure Diversion Program Information Session Understanding and Preparing for Mediation *For more detailed information and additional resources, go to the Pine Tree Legal website at www.ptla.org/foreclosure-prevention-toolkit

Foreclosure Diversion Program Information Session Understanding and Preparing for Mediation *For more detailed information and additional resources, go to the Pine Tree Legal website at www.ptla.org/foreclosure-prevention-toolkit

Uniform Rules of Practice Circuit Court of Illinois Nineteenth Judicial Circuit

If a l ~ DEC 1 4 2015 Uniform Rules of Practice Circuit Court of Illinois Nineteenth Judicial Circuit ~~ CIRCUIT CLERK Amendment to Rule 19.00, LAKE COUNTY RESIDENTIAL REAL ESTATE MORTGAGE FORECLOSURE

If a l ~ DEC 1 4 2015 Uniform Rules of Practice Circuit Court of Illinois Nineteenth Judicial Circuit ~~ CIRCUIT CLERK Amendment to Rule 19.00, LAKE COUNTY RESIDENTIAL REAL ESTATE MORTGAGE FORECLOSURE

Specialized Loan Servicing LLC ( SLS ) Home Affordable Foreclosure Alternative (HAFA) Matrix

Home Affordable Foreclosure Alternative (HAFA) Matrix") Specialized Loan Servicing LLC ( SLS ) Home Affordable Foreclosure Alternative (HAFA) Matrix All servicers that have signed agreements with the U.S. Department of the Treasury (Treasury) to participate

Specialized Loan Servicing LLC ( SLS ) Home Affordable Foreclosure Alternative (HAFA) Matrix All servicers that have signed agreements with the U.S. Department of the Treasury (Treasury) to participate

Home Affordable Modification Program Policies and Procedures Manual

Home Affordable Modification Program Policies and Procedures Manual Policies and procedures herein apply generally to loans subserviced by Franklin Credit Management Corporation, and are integrated with

Home Affordable Modification Program Policies and Procedures Manual Policies and procedures herein apply generally to loans subserviced by Franklin Credit Management Corporation, and are integrated with

UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK In re: MARK RICHARD LIPPOLD, Debtor. 1 FOR PUBLICATION Chapter 7 Case No. 11-12300 (MG) MEMORANDUM OPINION AND ORDER DENYING MOTION FOR RELIEF

UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK In re: MARK RICHARD LIPPOLD, Debtor. 1 FOR PUBLICATION Chapter 7 Case No. 11-12300 (MG) MEMORANDUM OPINION AND ORDER DENYING MOTION FOR RELIEF

Supplemental Directive December 10, 2013

Supplemental Directive 13-12 December 10, 2013 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 13-12 December 10, 2013 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

State of N.Y. Mtge. Agency v Cliffcrest Hous. Dev. Fund Corp NY Slip Op 32575(U) December 4, 2016 Supreme Court, New York County Docket

December 4, 2016 Supreme Court, New York County Docket") State of N.Y. Mtge. Agency v 936-938 Cliffcrest Hous. Dev. Fund Corp. 2016 NY Slip Op 32575(U) December 4, 2016 Supreme Court, New York County Docket Number: 850011/13 Judge: Joan A. Madden Cases posted

State of N.Y. Mtge. Agency v 936-938 Cliffcrest Hous. Dev. Fund Corp. 2016 NY Slip Op 32575(U) December 4, 2016 Supreme Court, New York County Docket Number: 850011/13 Judge: Joan A. Madden Cases posted

Department of Legislative Services

Department of Legislative Services Maryland General Assembly 2008 Session SB 216 Senate Bill 216 Judicial Proceedings FISCAL AND POLICY NOTE Revised (Senator Pugh and the President, et al.) (By Request

Department of Legislative Services Maryland General Assembly 2008 Session SB 216 Senate Bill 216 Judicial Proceedings FISCAL AND POLICY NOTE Revised (Senator Pugh and the President, et al.) (By Request

Foreclosure Prevention Certification Exam Study Guide Sample Questions With Answers from Previous Exams

Foreclosure Prevention Certification Exam Study Guide Sample Questions With Answers from Previous Exams Exam structure and tips: Structure: the exam is composed of 20-25 questions divided into two parts

Foreclosure Prevention Certification Exam Study Guide Sample Questions With Answers from Previous Exams Exam structure and tips: Structure: the exam is composed of 20-25 questions divided into two parts

Government and Private Initiatives to Address the Foreclosure Crisis

Government and Private Initiatives to Address the Foreclosure Crisis David Moskowitz Deputy General Counsel Berkeley Business Law Journal Berkeley Center for Law, Business and the Economy 2012 Symposium

Government and Private Initiatives to Address the Foreclosure Crisis David Moskowitz Deputy General Counsel Berkeley Business Law Journal Berkeley Center for Law, Business and the Economy 2012 Symposium

Supplemental Directive November 30, 2012

Supplemental Directive 12-09 November 30, 2012 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

Supplemental Directive 12-09 November 30, 2012 Making Home Affordable Program Administrative Clarifications In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program

A Lender s Guide to Massachusetts Foreclosures

A Lender s Guide to Massachusetts Foreclosures By Francesco A. De Vito and Jonathan C. Hayden Table of Contents Introduction 3 What to Do After Default 4 Foreclosing on Residential Property 6 Prior to

A Lender s Guide to Massachusetts Foreclosures By Francesco A. De Vito and Jonathan C. Hayden Table of Contents Introduction 3 What to Do After Default 4 Foreclosing on Residential Property 6 Prior to

Matter of Lewis County 2012 NY Slip Op 33565(U) October 18, 2012 Supreme Court, Lewis County Docket Number: Judge: Charles C.

October 18, 2012 Supreme Court, Lewis County Docket Number: Judge: Charles C.") Matter of Lewis County 2012 NY Slip Op 33565(U) October 18, 2012 Supreme Court, Lewis County Docket Number: 2010-000556 Judge: Charles C. Merrell Cases posted with a "30000" identifier, i.e., 2013 NY Slip

Matter of Lewis County 2012 NY Slip Op 33565(U) October 18, 2012 Supreme Court, Lewis County Docket Number: 2010-000556 Judge: Charles C. Merrell Cases posted with a "30000" identifier, i.e., 2013 NY Slip

OHIO FORECLOSURE PROCESS AND TIMELINE

OHIO FORECLOSURE PROCESS AND TIMELINE Ohio utilizes the process of judicial foreclosure in connection with the enforcement of both commercial and residential mortgages and liens on real property. 1 In

OHIO FORECLOSURE PROCESS AND TIMELINE Ohio utilizes the process of judicial foreclosure in connection with the enforcement of both commercial and residential mortgages and liens on real property. 1 In

UNREPORTED IN THE COURT OF SPECIAL APPEALS OF MARYLAND. No September Term, 2016 CAROL G. SULLIVAN, ET VIR. MARK S. DEVAN, ET AL.

Circuit Court for Baltimore County Case No. 03-C-12-012422 FC UNREPORTED IN THE COURT OF SPECIAL APPEALS OF MARYLAND No. 821 September Term, 2016 CAROL G. SULLIVAN, ET VIR. v. MARK S. DEVAN, ET AL. Eyler,

Circuit Court for Baltimore County Case No. 03-C-12-012422 FC UNREPORTED IN THE COURT OF SPECIAL APPEALS OF MARYLAND No. 821 September Term, 2016 CAROL G. SULLIVAN, ET VIR. v. MARK S. DEVAN, ET AL. Eyler,

Sale of the Housing Unit

Policy 22: Sale of the Housing Unit Adoption date: October 2007 Revision date: January 2010 Revision date: July 2015 1.0 Purpose The purpose of this policy is to provide standards for setting the sale

Policy 22: Sale of the Housing Unit Adoption date: October 2007 Revision date: January 2010 Revision date: July 2015 1.0 Purpose The purpose of this policy is to provide standards for setting the sale

REQUEST TO PREPARE NOTICE OF DEFAULT AND DECLARATION OF DEFAULT

th 936-B 7 Street, #341, Novato, CA 94945 Phone/Fax (888) 536-6409 www.foreclosureservice.com REQUEST TO PREPARE NOTICE OF DEFAULT AND DECLARATION OF DEFAULT Date: To: Federated Trust Deed Services 936B

th 936-B 7 Street, #341, Novato, CA 94945 Phone/Fax (888) 536-6409 www.foreclosureservice.com REQUEST TO PREPARE NOTICE OF DEFAULT AND DECLARATION OF DEFAULT Date: To: Federated Trust Deed Services 936B

Case: Document: Filed: 07/03/2012 Page: 1. NOT RECOMMENDED FOR FULL-TEXT PUBLICATION File Name: 12a0709n.06. No.

Case: 11-1806 Document: 006111357179 Filed: 07/03/2012 Page: 1 NOT RECOMMENDED FOR FULL-TEXT PUBLICATION File Name: 12a0709n.06 UNITED STATES COURT OF APPEALS FOR THE SIXTH CIRCUIT MARY K. HARGROW; M.

Case: 11-1806 Document: 006111357179 Filed: 07/03/2012 Page: 1 NOT RECOMMENDED FOR FULL-TEXT PUBLICATION File Name: 12a0709n.06 UNITED STATES COURT OF APPEALS FOR THE SIXTH CIRCUIT MARY K. HARGROW; M.

Loan Modifications 101 Tara Twomey National Consumer Law Center

Loan ifications 101 Tara Twomey National Consumer Law Center By the time the foreclosure crisis reached its peak in 2008, the climate for loan modifications had changed dramatically from earlier options

Loan ifications 101 Tara Twomey National Consumer Law Center By the time the foreclosure crisis reached its peak in 2008, the climate for loan modifications had changed dramatically from earlier options

The National Mortgage Settlement: July 31, :00 4:00pm

U.S. Department of Housing and Urban Development The National Mortgage Settlement: What Does it Mean for NSP? July 31, 2012 2:00 4:00pm Webinar Objectives Today Provide an overview of the National Mortgage

U.S. Department of Housing and Urban Development The National Mortgage Settlement: What Does it Mean for NSP? July 31, 2012 2:00 4:00pm Webinar Objectives Today Provide an overview of the National Mortgage

Third District Court of Appeal State of Florida

Third District Court of Appeal State of Florida Opinion filed August 1, 2018. Not final until disposition of timely filed motion for rehearing. No. 3D17-1246 Lower Tribunal No. 13-20646 Eduardo Gonzalez

Third District Court of Appeal State of Florida Opinion filed August 1, 2018. Not final until disposition of timely filed motion for rehearing. No. 3D17-1246 Lower Tribunal No. 13-20646 Eduardo Gonzalez

Supplemental Directive November 3, Home Affordable Modification Program Borrower Notices

Supplemental Directive 09-08 November 3, 2009 Home Affordable Modification Program Borrower Notices Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility,

Supplemental Directive 09-08 November 3, 2009 Home Affordable Modification Program Borrower Notices Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility,

Mortgage Reinstatement Assistance Program

Mortgage Reinstatement 1. Overview The Mortgage Reinstatement ( MRAP ) is one of CalHFA MAC s federally-funded programs developed to provide temporary financial assistance to eligible homeowners who wish

Mortgage Reinstatement 1. Overview The Mortgage Reinstatement ( MRAP ) is one of CalHFA MAC s federally-funded programs developed to provide temporary financial assistance to eligible homeowners who wish

IN THE COURT OF SPECIAL APPEALS OF MARYLAND. September Term, No CAROL G. SULLIVAN, et vir., MARK S. DEVAN, et al.,

IN THE COURT OF SPECIAL APPEALS OF MARYLAND September Term, 2016 No. 00821 CAROL G. SULLIVAN, et vir., Appellants, v. MARK S. DEVAN, et al., Appellees. APPEAL FROM THE CIRCUIT COURT FOR BALTIMORE COUNTY

IN THE COURT OF SPECIAL APPEALS OF MARYLAND September Term, 2016 No. 00821 CAROL G. SULLIVAN, et vir., Appellants, v. MARK S. DEVAN, et al., Appellees. APPEAL FROM THE CIRCUIT COURT FOR BALTIMORE COUNTY

IN RE: MEDIATION MANDATORY MEDIATION CIRCUIT COURT BREVARD COUNTY OWNER OCCUPIED RESIDENTIAL MORTGAGE FORECLOSURE

IN THE CIRCUIT COURT OF THE EIGHTEENTH JUDICIAL CIRCUIT IN AND FOR BREVARD COUNTY, FLORIDA ADMINISTRATIVE ORDER NO: 09-14-B IN RE: MEDIATION MANDATORY MEDIATION CIRCUIT COURT BREVARD COUNTY OWNER OCCUPIED

IN THE CIRCUIT COURT OF THE EIGHTEENTH JUDICIAL CIRCUIT IN AND FOR BREVARD COUNTY, FLORIDA ADMINISTRATIVE ORDER NO: 09-14-B IN RE: MEDIATION MANDATORY MEDIATION CIRCUIT COURT BREVARD COUNTY OWNER OCCUPIED

ASSEMBLY STANDING COMMITTEE ON HOUSING Oversight of the State Fiscal Year State Budget for New York State Homes & Community Renewal

ASSEMBLY STANDING COMMITTEE ON HOUSING Oversight of the State Fiscal Year 2018-2019 State Budget for New York State Homes & Community Renewal Thursday, December 20, 2018 10:00 a.m. Hearing Room C Legislative

ASSEMBLY STANDING COMMITTEE ON HOUSING Oversight of the State Fiscal Year 2018-2019 State Budget for New York State Homes & Community Renewal Thursday, December 20, 2018 10:00 a.m. Hearing Room C Legislative

AMENDMENTS TO THE CFPB MORTGAGE SERVICING REGULATIONS EFFECTIVE OCTOBER 19, 2017 NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION OCTOBER 18, 2017

AMENDMENTS TO THE CFPB MORTGAGE SERVICING REGULATIONS EFFECTIVE OCTOBER 19, 2017 NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION OCTOBER 18, 2017 1 Diane Cipollone, Esq. Consultant to National Fair

AMENDMENTS TO THE CFPB MORTGAGE SERVICING REGULATIONS EFFECTIVE OCTOBER 19, 2017 NATIONAL FAIR HOUSING ALLIANCE WEBINAR PRESENTATION OCTOBER 18, 2017 1 Diane Cipollone, Esq. Consultant to National Fair

HAMP Resolution Matrix

Homeowner HAMP Eligibility Issues HAMP Resolution Matrix 1 (1) Verify whether the property is owner occupied (for HAMP Tier 2 rental properties, must have missed 2 or more payments). Homeowner is (2) Verify

Homeowner HAMP Eligibility Issues HAMP Resolution Matrix 1 (1) Verify whether the property is owner occupied (for HAMP Tier 2 rental properties, must have missed 2 or more payments). Homeowner is (2) Verify

New York State Legislature 2019 Joint Budget Hearing. Housing

119 Washington Ave. Albany, NY 12210 Phone 518.462.6831 Fax 518.462.6687 www.empirejustice.org New York State Legislature 2019 Joint Budget Hearing Housing February 4, 2019 Prepared by: Kirsten Keefe Senior

119 Washington Ave. Albany, NY 12210 Phone 518.462.6831 Fax 518.462.6687 www.empirejustice.org New York State Legislature 2019 Joint Budget Hearing Housing February 4, 2019 Prepared by: Kirsten Keefe Senior

Delinquency Management for Mortgages Secured by Primary Residences

Delinquency Management for Mortgages Secured by Primary Residences This reference guide highlights Freddie Mac s requirements for managing delinquent mortgages secured by a borrower s primary residence.

Delinquency Management for Mortgages Secured by Primary Residences This reference guide highlights Freddie Mac s requirements for managing delinquent mortgages secured by a borrower s primary residence.

UNITED STATES BANKRUPTCY COURT DISTRICT OF RHODE ISLAND FOURTH AMENDED LOSS MITIGATION PROGRAM AND PROCEDURES I. PURPOSE

APPENDIX IX (Rev. 2/14/11) UNITED STATES BANKRUPTCY COURT DISTRICT OF RHODE ISLAND FOURTH AMENDED LOSS MITIGATION PROGRAM AND PROCEDURES I. PURPOSE The Loss Mitigation Program (LMP) is designed to function

APPENDIX IX (Rev. 2/14/11) UNITED STATES BANKRUPTCY COURT DISTRICT OF RHODE ISLAND FOURTH AMENDED LOSS MITIGATION PROGRAM AND PROCEDURES I. PURPOSE The Loss Mitigation Program (LMP) is designed to function

P. O. BOX 19999, RALEIGH, NC / / FAX: 919/

P. O. BOX 19999, RALEIGH, NC 27619-9916 / 800-662-7044 / FAX: 919/881-9909 Legal Memorandum August 11, 2010 Vol. 42, No. 3 TO: RE: Legal Memorandum Mailing List Summary of Senate Bill 1216 Amendments to

P. O. BOX 19999, RALEIGH, NC 27619-9916 / 800-662-7044 / FAX: 919/881-9909 Legal Memorandum August 11, 2010 Vol. 42, No. 3 TO: RE: Legal Memorandum Mailing List Summary of Senate Bill 1216 Amendments to

Loan Workout Hierarchy for Fannie Mae Conventional Loans

Loan Workout Hierarchy for Fannie Mae Conventional Loans The following table identifies the Fannie Mae loss mitigation options that are available to assist borrowers experiencing financial hardship. Generally,

Loan Workout Hierarchy for Fannie Mae Conventional Loans The following table identifies the Fannie Mae loss mitigation options that are available to assist borrowers experiencing financial hardship. Generally,

Foreclosure Process in Minnesota

Foreclosure Process in Minnesota Foreclosure by Advertisement Missed payments 6 weeks before sale 4 weeks before sale Sheriff s Sale Missed payment notices Default / intent to foreclose notice Pre foreclosure

Foreclosure Process in Minnesota Foreclosure by Advertisement Missed payments 6 weeks before sale 4 weeks before sale Sheriff s Sale Missed payment notices Default / intent to foreclose notice Pre foreclosure

New Servicing Rules under RESPA Early Intervention, Continuous Contact and Loss Mitigation

New Servicing Rules under RESPA Early Intervention, Continuous Contact and Loss Mitigation FIS Regulatory Advisory Services Regulatory.Services@fisglobal.com New Servicing Rules Under RESPA Early Intervention,

New Servicing Rules under RESPA Early Intervention, Continuous Contact and Loss Mitigation FIS Regulatory Advisory Services Regulatory.Services@fisglobal.com New Servicing Rules Under RESPA Early Intervention,

TITLE 230 DEPARTMENT OF BUSINESS REGULATION

230-RICR-40-10-4 TITLE 230 DEPARTMENT OF BUSINESS REGULATION CHAPTER 40 BANKING SUBCHAPTER 10 LENDING PART 4 Mortgage Foreclosure Disclosure 4.1 Authority This Part is promulgated pursuant to R.I. Gen.

230-RICR-40-10-4 TITLE 230 DEPARTMENT OF BUSINESS REGULATION CHAPTER 40 BANKING SUBCHAPTER 10 LENDING PART 4 Mortgage Foreclosure Disclosure 4.1 Authority This Part is promulgated pursuant to R.I. Gen.

FIFTH JUDICIAL DISTRICT

FIFTH JUDICIAL DISTRICT COUNTY OF CLACKAMAS COUNTY COURTHOUSE, OREGON CITY, OREGON 97045 Elizabeth Lemoine Luby Law Firm Christopher Kayser Larkins Vacura, LLP Lisa McMahon-Myhran Robinson Tait, PS Elizabeth@lubylaw.org

FIFTH JUDICIAL DISTRICT COUNTY OF CLACKAMAS COUNTY COURTHOUSE, OREGON CITY, OREGON 97045 Elizabeth Lemoine Luby Law Firm Christopher Kayser Larkins Vacura, LLP Lisa McMahon-Myhran Robinson Tait, PS Elizabeth@lubylaw.org

Home Mortgage Foreclosures in Maine

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

CFPB National Servicing Standards, Are Servicers Ready?

CFPB National Servicing Standards, Are Servicers Ready? On January 13 th of this year the US Consumer Financial Protection Bureau (CFPB) published comprehensive rules establishing national servicing standards

CFPB National Servicing Standards, Are Servicers Ready? On January 13 th of this year the US Consumer Financial Protection Bureau (CFPB) published comprehensive rules establishing national servicing standards

SECTION 8 DOWNPAYMENT ASSISTANCE PROGRAM

SECTION 8 DOWNPAYMENT ASSISTANCE PROGRAM 8.1 Qualification of Participating Lenders 8.2 Funds Availability 8.3 Eligibility 8.4 Computation of DAP Loan Amounts 8.5 Application Processing 8.6 Loan Preparation

SECTION 8 DOWNPAYMENT ASSISTANCE PROGRAM 8.1 Qualification of Participating Lenders 8.2 Funds Availability 8.3 Eligibility 8.4 Computation of DAP Loan Amounts 8.5 Application Processing 8.6 Loan Preparation

National Mortgage Settlement & California Commitment

National Mortgage Settlement & California Commitment Help for Homeowners Community Pre Event Webinar Noah Zinner, Visiting Clinical Professor, UC Irvine Law School California Monitor, A Program of the

National Mortgage Settlement & California Commitment Help for Homeowners Community Pre Event Webinar Noah Zinner, Visiting Clinical Professor, UC Irvine Law School California Monitor, A Program of the

Impact: Federal and State Chartered Credit Unions Relevant Department: Lending and Collections / CEO Priority Level: Medium

Comment Call (15-1) CFPB: Amendments to 2013 Mortgage Servicing Rules under Real Estate Settlement Procedures Act (Regulation X) and Truth in Lending Act (Regulation Z) Impact: Federal and State Chartered

Comment Call (15-1) CFPB: Amendments to 2013 Mortgage Servicing Rules under Real Estate Settlement Procedures Act (Regulation X) and Truth in Lending Act (Regulation Z) Impact: Federal and State Chartered

Making Home Affordable Program Performance Report Third Quarter 2015

Making Home Affordable PROGRAM PERFORMANCE REPORT THROUGH THE THIRD QUARTER OF 2015 MHA AT-A-GLANCE Approximately 2.5 Million Homeowner Assistance Actions have taken place under Making Home Affordable

Making Home Affordable PROGRAM PERFORMANCE REPORT THROUGH THE THIRD QUARTER OF 2015 MHA AT-A-GLANCE Approximately 2.5 Million Homeowner Assistance Actions have taken place under Making Home Affordable

Standard and Alternative Waterfalls 1

Standard and Alternative Modification Waterfalls Training Presentation for Servicers Agenda 1 2 3 4 5 6 7 8 Overview of Eligibility Tier 1 Standard Modification Waterfall Tier 1 Alternative Modification

Standard and Alternative Modification Waterfalls Training Presentation for Servicers Agenda 1 2 3 4 5 6 7 8 Overview of Eligibility Tier 1 Standard Modification Waterfall Tier 1 Alternative Modification

Principal Reduction Program

1. Overview The Principal Reduction ( PRP ) is one of CalHFA MAC s federallyfunded programs developed with a goal to provide capital to homeowners who have suffered an eligible hardship in order to reduce

1. Overview The Principal Reduction ( PRP ) is one of CalHFA MAC s federallyfunded programs developed with a goal to provide capital to homeowners who have suffered an eligible hardship in order to reduce

Certified Distressed Property Expert

Certified Distressed Property Expert If we all did the things we are capable of doing we would literally astound ourselves. -Thomas Edison National Delinquency Numbers Mortgage Bankers Association 4.38%

Certified Distressed Property Expert If we all did the things we are capable of doing we would literally astound ourselves. -Thomas Edison National Delinquency Numbers Mortgage Bankers Association 4.38%

Default Management Servicing Guide

Homeowner Assistance Program I Mortgage Insurance Default Management Servicing Guide January 10, 2014 7566293.0114 Genworth Mortgage Insurance Homeowner Assistance Program Default Management Servicing

Homeowner Assistance Program I Mortgage Insurance Default Management Servicing Guide January 10, 2014 7566293.0114 Genworth Mortgage Insurance Homeowner Assistance Program Default Management Servicing

PRINCIPAL REDUCTION ASSISTANCE PROGRAM ( PRP ) Operational Term Sheet

Operational Term Sheet") PRINCIPAL REDUCTION ASSISTANCE PROGRAM ( PRP ) Operational Term Sheet All homeowner intake, counseling, eligibility and benefit determination, and KYHC program benefit processing will be performed by the

PRINCIPAL REDUCTION ASSISTANCE PROGRAM ( PRP ) Operational Term Sheet All homeowner intake, counseling, eligibility and benefit determination, and KYHC program benefit processing will be performed by the

STATE OF NEW JERSEY. SENATE, No th LEGISLATURE

SENATE, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED FEBRUARY, 0 Sponsored by: Senator RONALD L. RICE District (Essex) Senator BRIAN P. STACK District (Hudson) SYNOPSIS Provides foreclosure forbearance

SENATE, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED FEBRUARY, 0 Sponsored by: Senator RONALD L. RICE District (Essex) Senator BRIAN P. STACK District (Hudson) SYNOPSIS Provides foreclosure forbearance

FILED: NEW YORK COUNTY CLERK 08/16/ :46 PM INDEX NO /2014 NYSCEF DOC. NO. 12 RECEIVED NYSCEF: 08/16/2016

FILED: NEW YORK COUNTY CLERK 08/16/2016 08:46 PM INDEX NO. 850312/2014 NYSCEF DOC. NO. 12 RECEIVED NYSCEF: 08/16/2016 SUPREME COURT OF THE STATE OF NEW YORK COUNTY OF NEW YORK WELLS FARGO BANK, N.A, as

FILED: NEW YORK COUNTY CLERK 08/16/2016 08:46 PM INDEX NO. 850312/2014 NYSCEF DOC. NO. 12 RECEIVED NYSCEF: 08/16/2016 SUPREME COURT OF THE STATE OF NEW YORK COUNTY OF NEW YORK WELLS FARGO BANK, N.A, as

Executive Summary of the 2016 Mortgage Servicing Rule

1700 G Street NW, Washington, DC 20552 October 18, 2017 Executive Summary of the 2016 Mortgage Servicing Rule On August 4, 2016, the Consumer Financial Protection Bureau (Bureau) issued a final rule (2016

1700 G Street NW, Washington, DC 20552 October 18, 2017 Executive Summary of the 2016 Mortgage Servicing Rule On August 4, 2016, the Consumer Financial Protection Bureau (Bureau) issued a final rule (2016

TOPIC CFPB HBOR NMS. January 10, January 1, April 4, Servicers and sub-servicers; not trustees acting under a DOT (a).

.") TOPIC CFPB HBOR NMS Effective date January 10, 2014. January 1, 2013. April 4, 2012. Entities regulated Property protected All servicers of federally related mortgage loans (nearly all servicers). 1024.2.*

TOPIC CFPB HBOR NMS Effective date January 10, 2014. January 1, 2013. April 4, 2012. Entities regulated Property protected All servicers of federally related mortgage loans (nearly all servicers). 1024.2.*

City of Cranston Foreclosure Conciliation & Recording Requirements Duties of Participants Applying the Ordinance Model Certifications

City of Cranston Foreclosure Conciliation & Recording Requirements Duties of Participants Applying the Ordinance Model Certifications Ordinance Implementation Requirements It is the responsibility of the

City of Cranston Foreclosure Conciliation & Recording Requirements Duties of Participants Applying the Ordinance Model Certifications Ordinance Implementation Requirements It is the responsibility of the