Directive on D e D p e osit G u G ar a a r n a tee e e S c S hem m s e (DGS) 23/01/2015

|

|

|

- Margery Allen

- 5 years ago

- Views:

Transcription

1 Directive on Deposit Guarantee Schemes (DGS) 23/01/2015

2 Background: key steps July 2010 Commission legislative proposal September 2010 Start of negotiations in Council May/June 2011 ECON report / Council General Approach Sep-Dec 2011 Political & technical trilogues (no agreement) February 2012 EP Plenary vote (first reading) Mar Aug 2013 Negotiations blocked in Council Sep-Dec 2013 Political & technical trilogues (agreement) 16 April 2014 Adoption of the new Directive (2014/49/EU) 12 June 2014 Publication in Official Journal 2

3 Application of the Directive Directive shall apply to: Directive shall not apply 1 to: Statutory DGS Contractual DGS that are officially recognised as DGS Institutional Protection Schemes that are officially recognised as DGS Contractual schemes that are not officially recognised as DGS Institutional protection schemes that are not officially recognised as DGS Member banks of those schemes Except for some information requirements of the Directive (Art.14) 2 Each MS shall ensure that within its territory one or more DGS are introduced and officially recognised (Art.3) 3 No credit institution may take deposits unless it is a member of a scheme officially recognised in its home MS (Art.3) 3

4 Level of coverage Harmonised level of per depositor per bank applicable in all Member States and EEA countries Grandfathering: countries with higher coverage levels (e.g. Norway) may apply those levels until end-2018 afterwards, will apply No separate coverage per different brands of the same bank Temporary high deposit balances: Member States shall ensure coverage above for deposits arising from housing transactions (e.g. sale of residence) or from specific life events (e.g. marriage, divorce, inheritance) Covered in full or partially Covered from 3 up to 12 months 4

5 Scope of coverage Covered Not covered Depositors Individuals, all enterprises (small, medium, large) Financial institutions, public authorities* Products Deposits in non-eu currencies (USD, CHF, etc) Debt certificates, structured products, etc * Deposits of small local authorities (with annual budget up to ) may be covered by DGS 5

6 Covered deposits in the EU 6

7 Payout deadline (1) Original from months Past from March months Present from weeks Future from working days 7

8 Payout deadline (2) Payout deadline will be gradually reduced from the current 20 working days to 7 working days in three phases: 15 working days from working days from working days from 2024 During the transitional period (until end-2023), depositors in need may ask for so-called "social payout", i.e. limited amount to cover their costs of living to be paid within 5 working days 8

9 Factors facilitating faster payouts Banks Information obligation towards DGS, tagging eligible deposits, providing single customer views Involving DGS at an early stage by compulsorily informing them if a bank failure becomes likely Supervisors Early access to banks records, making payouts by DGS on their own initiative (no applications from depositors) DGS Payout to depositors 9

10 Payout modalities Payout currency (for Member States to decide): the currency of the MS where the DGS (or the account) is located the currency of the MS where the account holder is resident the currency of the account the euro Depositors at branches in other Member States: will be paid out by the DGS in that MS (host DGS), acting as a "single point of contact" on behalf of the home DGS the host DGS will make this payout if the home DGS provides it with the necessary funding in advance (and, after the payout, compensate the home DGS for the costs incurred) 10

11 Financing (1) Ex-ante funding (at least 0.8% of covered deposits) to be reached by Member States within 10 years Extraordinary (ex-post) contributions (up to 0.5% of covered deposits annually) Mutual borrowing facility on a voluntary basis (up to 0.5% of covered deposits of the borrowing scheme) Alternative funding arrangements (e.g. borrowing from governments or financial markets) 11

12 Financing (2) In principle, the target funding level for DGS is at least 0.8% of covered deposits to be reached in 10 years, but COM may approve a lower target level, but not lower than 0.5% of cov dep, e.g. in case of the banking sectors dominated by large banks if, during the build-up period, the DGS has made cumulative disbursements in excess of 0.8% of cov dep, MS may extend this period by max 4 years In principle, ex-ante funds of DGS should consist of cash, deposits, and low-risk liquid assets, but max 30% of the funding can be made up of payment commitments exceptionally, bank levies paid to the State budget may also count 12

Current DGS")

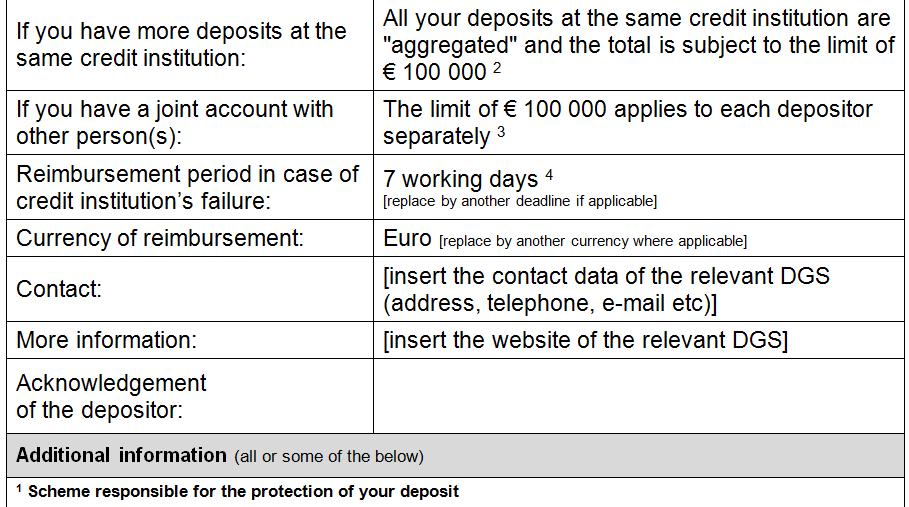

13 Financing (3) 0.8% of covered deposits DGS funds in 10 years ( billion) Current DGS funds vs. the target funding level (data as of end-2011) 13

14 Risk-based contributions Mandatory for all Member States: contributions to DGS will reflect individual risk profiles of member banks riskier banks will have to pay more EBA will elaborate guidelines on the technical aspects of risk-based contributions (calculation methods, risk indicators, risk classes, thresholds, percentages, etc) Some exceptions: option to apply lower contributions to some schemes (IPS) or low-risk sectors; option to use own risk-based methods by DGS 14

15 Use of DGS funds Payout DGS funds shall be primarily used to reimburse depositors after a bank failure Resolution DGS funds shall also be used to finance the resolution of credit institutions + + Early intervention DGS funds may be used for alternative measures in order to prevent a bank failure 15

16 Early intervention by DGS Only if several conditions are met, for example: the resolution authority has not taken any resolution action the DGS has appropriate systems and procedures the ability of the member banks to pay immediately the extraordinary contributions etc Member banks must immediately repay the DGS funds used for early intervention: if the DGS needs to make a payout and its funds amount to less than 2/3 of the target level always, if the DGS funds fall below 25% of the target level as a result of the early intervention 16

17 Role of DGS in bank resolution DGS shall contribute to the resolution of a failed bank as a preferred creditor: the DGS intervention would only take place in the last instance, i.e. after bailing-in all unsecured creditors and using the financial means of the Resolution Funds DGS's contribution would be limited: up to the amount they would have contributed in insolvency up to the amount equal to 50% of the DGS target funding level 17

18 Depositor preference Creditor hierarchy (in insolvency and resolution): eligible deposits of households and enterprises (micro, small and medium companies) shall be preferred covered deposits, i.e. those protected by DGS up to , shall be super-preferred Bail-in: covered deposits will not be affected, as exempted from bail-in and the DGS will step in their shoes eligible deposits of those mentioned above, unlikely to be affected as the resolution fund can step in their shoes provided 8% of liabilities of the failed bank have absorbed losses 18

19 Bail-in: treatment of deposits/dgs 3. Alternative financing sources 2. 5% Resolution financing arrangement 1. 8% internal loss absorbtion Only after 5% of the financing arrangement's cap has been reached, and all unsecured and nonpreferred liabilities other than eligible deposits have been bail-in Resolution financing arrangement may provide loss absorption or capital injection of up to 5% of total liabilities 8% of total liabilities or 20% of RWAs to be absorbed by shareholders and creditors before the use of the resolution financing arrangement DGS (covered deposits) Households, micro, SMEs > 100,000 Senior debt & corporate deposits >100,000 Subordinated debt AT1 & T2 CET1 More bail-in or eventually alternative financing sources (private, public/esm) Resolution financing arrangement 5% of liabilities Internal absorbtion 8% of liabilities or 20% of RWAs (in order of hierarchy)* * Flexibility to depart from creditor hierarchy if not possible to bail-in the liability during the timeframe, would create contagion risks, lead to destruction in value, necessary to ensure continuity of critical functions. 19

20 Better information for depositors While depositing money at a bank, depositors will have to countersign a standardised information sheet containing all relevant information about deposit protection by the DGS The updated standardised information sheet will be sent by banks to their customers at least once a year Banks will be obliged to inform their depositors about DGS protection of their deposits on the statements of account Some restrictions on advertising on deposit products (only factual information, no referring to unlimited protection, etc) 20

21 Depositor information template 21

22 Next steps (1) Entry into force 2 July 2014 General transposition deadline for Member States 12 months after the entry into force (3 July 2015) Longer implementation period for some issues, e.g. social payout and risk-based contributions (May 2016) 3 years after the entry into force (by 3 July 2017) and at least every 5 years thereafter, EBA shall conduct a review of the guidelines on risk-based or alternative own-risk-based methods applied by DGS 22

23 Next steps (2) 5 years after the entry into force (by 3 July 2019), the Commission will submit to the European Parliament and to the Council: a report on the target fund level (assessing the appropriateness of the percentage set), the adequacy of the current coverage level, the impact of the early intervention measures on deposit protection, etc a report (+ legislative proposal, if appropriate) setting out how DGS may cooperate through a European Scheme to prevent risks arising from cross-border activities and protect deposits from such risks 23

24 Next steps (3) From 1 January 2024 onwards, the payout deadline will be shortened to 7 working days 10 years after the entry into force (by 3 July 2024), the available financial means of all DGS will reach a target level of at least 0.8% of covered deposits 24

The EU Framework for Deposit Guarantee Schemes

The EU Framework for Deposit Guarantee Schemes Raluca Painter European Commission Senior Policy Officer, Financial Stability Unit 21/09/2014 Background: key steps Directive 94/19/EC of 30 May 1994 on DGS

The EU Framework for Deposit Guarantee Schemes Raluca Painter European Commission Senior Policy Officer, Financial Stability Unit 21/09/2014 Background: key steps Directive 94/19/EC of 30 May 1994 on DGS

Deposit Guarantee Schemes Frequently Asked Questions

EUROPEAN COMMISSION MEMO Brussels, 15 April 2014 Deposit Guarantee Schemes Frequently Asked Questions Why was the revision of the Directive on Deposit Guarantee Schemes necessary? The original Directive

EUROPEAN COMMISSION MEMO Brussels, 15 April 2014 Deposit Guarantee Schemes Frequently Asked Questions Why was the revision of the Directive on Deposit Guarantee Schemes necessary? The original Directive

Public support and the use of the Resolution Fund under BRRD

Public support and the use of the Resolution Fund under BRRD Paolo Fucile Directorate General Financial Stability, Financial Markets and Capital Markets Union 05/12/2016 Key objectives of BRRD Maintain

Public support and the use of the Resolution Fund under BRRD Paolo Fucile Directorate General Financial Stability, Financial Markets and Capital Markets Union 05/12/2016 Key objectives of BRRD Maintain

BAIL IN and RESOLUTION FINANCING in BRRD

FGDR 28 March 2014 BAIL IN and RESOLUTION FINANCING in BRRD INTERVENTION INSTRUMENTS Resolution tools Sale of business tools The Resolution Authority (RA) can force the selling or transfer of shares, assets

FGDR 28 March 2014 BAIL IN and RESOLUTION FINANCING in BRRD INTERVENTION INSTRUMENTS Resolution tools Sale of business tools The Resolution Authority (RA) can force the selling or transfer of shares, assets

Europe: Progress in bank resolution and banking union

Europe: Progress in bank resolution and banking union Shaping the New Framework for Global Financial Regulation LACEA & LAMES 2013 Annual Meetings Mexico City, 31 October 2013 Santiago Fernández de Lis

Europe: Progress in bank resolution and banking union Shaping the New Framework for Global Financial Regulation LACEA & LAMES 2013 Annual Meetings Mexico City, 31 October 2013 Santiago Fernández de Lis

DIRECTIVES. DIRECTIVE 2014/49/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 16 April 2014 on deposit guarantee schemes.

12.6.2014 Official Journal of the European Union L 173/149 DIRECTIVES DIRECTIVE 2014/49/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 16 April 2014 on deposit guarantee schemes (recast) (Text with

12.6.2014 Official Journal of the European Union L 173/149 DIRECTIVES DIRECTIVE 2014/49/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 16 April 2014 on deposit guarantee schemes (recast) (Text with

European Commission Proposal for a Directive on Recovery and Resolution

European Commission Proposal for a Directive on Recovery and Resolution The 7th DICJ Round Table Andras Fekete-Gyor Managing Director March 5-8, 2013 Tokyo Presentation Outline Introduction and Overview

European Commission Proposal for a Directive on Recovery and Resolution The 7th DICJ Round Table Andras Fekete-Gyor Managing Director March 5-8, 2013 Tokyo Presentation Outline Introduction and Overview

Deposit Guarantee Schemes

To the European Commission via E-Mail: markt-dgs-consultation@ec.europa.eu Federal Division of Banking and Insurance Wiedner Hauptstrasse 63 PO Box 320 1045 Vienna T +43 (0)5 90 900-EXT F +43 (0)5 90 900-272

To the European Commission via E-Mail: markt-dgs-consultation@ec.europa.eu Federal Division of Banking and Insurance Wiedner Hauptstrasse 63 PO Box 320 1045 Vienna T +43 (0)5 90 900-EXT F +43 (0)5 90 900-272

COUNCIL OF THE EUROPEAN UNION. Brussels, 4 March 2014 (OR. en) 5199/1/14 REV 1. Interinstitutional File: 2010/0207 (COD)

5199/1/14 REV 1. Interinstitutional File: 2010/0207 (COD)") COUNCIL OF THE EUROPEAN UNION Brussels, 4 March 2014 (OR. en) Interinstitutional File: 2010/0207 (COD) 5199/1/14 REV 1 EF 7 ECOFIN 23 CODEC 50 PARLNAT 78 LEGISLATIVE ACTS AND OTHER INSTRUMTS Subject: Position

COUNCIL OF THE EUROPEAN UNION Brussels, 4 March 2014 (OR. en) Interinstitutional File: 2010/0207 (COD) 5199/1/14 REV 1 EF 7 ECOFIN 23 CODEC 50 PARLNAT 78 LEGISLATIVE ACTS AND OTHER INSTRUMTS Subject: Position

Annex IV List of Definitions and Examples

EUROPEAN COMMISSION DIRECTORATE GENERAL JRC JOINT RESEARCH CENTRE Annex IV List of Definitions and Examples European Commission, Joint Research Centre, Unit G09, Ispra (Italy) DGS Project, Final Report,

EUROPEAN COMMISSION DIRECTORATE GENERAL JRC JOINT RESEARCH CENTRE Annex IV List of Definitions and Examples European Commission, Joint Research Centre, Unit G09, Ispra (Italy) DGS Project, Final Report,

Cooperation between authorities Preserving the relevance of deposit guarantee in Europe

Cooperation between authorities Preserving the relevance of deposit guarantee in Europe EFDI International Conference, Dubrovnik, 3 September 2015 Charles Canonne European Banking Authority, Resolution

Cooperation between authorities Preserving the relevance of deposit guarantee in Europe EFDI International Conference, Dubrovnik, 3 September 2015 Charles Canonne European Banking Authority, Resolution

Review of the Regulatory Framework Risk Reduction Package

Review of the Regulatory Framework Risk Reduction Package Emiliano Tornese Deputy Head of Unit - crisis management and resolution, DG FISMA Ljubljana, February 2018 Agenda 1. Banking sector reform in the

Review of the Regulatory Framework Risk Reduction Package Emiliano Tornese Deputy Head of Unit - crisis management and resolution, DG FISMA Ljubljana, February 2018 Agenda 1. Banking sector reform in the

SRM and ARTICULATION with BRRD

SRM and ARTICULATION with BRRD FGDR 17 April 2014 - Selected provisions of SRM and intergovernmental agreement (IGA) - Institutional framework Participating member states of SRM ( = Contracting Parties

SRM and ARTICULATION with BRRD FGDR 17 April 2014 - Selected provisions of SRM and intergovernmental agreement (IGA) - Institutional framework Participating member states of SRM ( = Contracting Parties

A8-0302/ Ranking of unsecured debt instruments in insolvency hierarchy

22.11.2017 A8-0302/ 001-001 AMDMTS 001-001 by the Committee on Economic and Monetary Affairs Report Gunnar Hökmark Ranking of unsecured debt instruments in insolvency hierarchy A8-0302/2017 Proposal for

22.11.2017 A8-0302/ 001-001 AMDMTS 001-001 by the Committee on Economic and Monetary Affairs Report Gunnar Hökmark Ranking of unsecured debt instruments in insolvency hierarchy A8-0302/2017 Proposal for

How to ensure enough Loss Absorbing Capacity: From TLAC to MREL

How to ensure enough Loss Absorbing Capacity: From TLAC to MREL Nikoletta Kleftouri European Banking Authority 13 December 2016 FINSAC Workshop on bail-in and MREL Plan 1. Why do we need loss absorbing

How to ensure enough Loss Absorbing Capacity: From TLAC to MREL Nikoletta Kleftouri European Banking Authority 13 December 2016 FINSAC Workshop on bail-in and MREL Plan 1. Why do we need loss absorbing

Chapter 9: Financial Services

Chapter 9: Financial Services Serbian Deposit Insurance Scheme Republic of Serbia Deposit Insurance Scheme Legal Framework EU regulations: Directive 2014/49/EU of the European Parliament and of the Council

Chapter 9: Financial Services Serbian Deposit Insurance Scheme Republic of Serbia Deposit Insurance Scheme Legal Framework EU regulations: Directive 2014/49/EU of the European Parliament and of the Council

European Association of Co-operative Banks Groupement Européen des Banques Coopératives Europäische Vereinigung der Genossenschaftsbanken

To : Honourable MEP European Parliament Brussels, 8 October 2013 Ref : HG/VH/KKH/B19/13-098 E-MAIL Subject: Key concerns for Trialogue on Deposit Guarantee Schemes Directive DearSir/Madam, In view of the

To : Honourable MEP European Parliament Brussels, 8 October 2013 Ref : HG/VH/KKH/B19/13-098 E-MAIL Subject: Key concerns for Trialogue on Deposit Guarantee Schemes Directive DearSir/Madam, In view of the

Consultation Paper. Draft guidelines on cooperation agreements between deposit guarantee schemes under Directive 2014/49/EU EBA/CP/2015/13

EBA/CP/2015/13 29 July 2015 Consultation Paper Draft guidelines on cooperation agreements between deposit guarantee schemes under Directive 2014/49/EU Contents 1. Responding to this consultation 3 2. Executive

EBA/CP/2015/13 29 July 2015 Consultation Paper Draft guidelines on cooperation agreements between deposit guarantee schemes under Directive 2014/49/EU Contents 1. Responding to this consultation 3 2. Executive

Resolution Regimes: FSB s Key Attributes, TLAC & EU s MREL. Seminar on Crisis Management and Bank Resolution

Resolution Regimes: FSB s Key Attributes, TLAC & EU s MREL Seminar on Crisis Management and Bank Resolution Abuja, Nigeria 16-20 January 2017 Amarendra Mohan Independent Financial Sector Expert (formerly

Resolution Regimes: FSB s Key Attributes, TLAC & EU s MREL Seminar on Crisis Management and Bank Resolution Abuja, Nigeria 16-20 January 2017 Amarendra Mohan Independent Financial Sector Expert (formerly

COMMISSION CONSULTATION ON REVIEW OF DIRECTIVE 94/19/EC ON DEPOSIT GUARANTEE SCHEMES

European Commission Internal Market and Services DG Financial Institutions markt-dgs-consultation@ec.europa.eu Interest Representative ID 7328496842-09 COMMISSION CONSULTATION ON REVIEW OF DIRECTIVE 94/19/EC

European Commission Internal Market and Services DG Financial Institutions markt-dgs-consultation@ec.europa.eu Interest Representative ID 7328496842-09 COMMISSION CONSULTATION ON REVIEW OF DIRECTIVE 94/19/EC

EFFECTS ANALYSIS (EA) ON THE EUROPEAN DEPOSIT INSURANCE SCHEME (EDIS)

ON THE EUROPEAN DEPOSIT INSURANCE SCHEME (EDIS)") Disclaimer This non-paper from the Commission services is for information and discussion purposes only. It may not be interpreted as stating an official position of the European Commission. EFFECTS ANALYSIS

Disclaimer This non-paper from the Commission services is for information and discussion purposes only. It may not be interpreted as stating an official position of the European Commission. EFFECTS ANALYSIS

Resolution Industry Briefing. February 2018

Resolution Industry Briefing February 2018 EU resolution framework Bank and investment firm resolution BRRD implementation and designation as NRA EU Bank Recovery and Resolution Directive (BRRD) Resolution

Resolution Industry Briefing February 2018 EU resolution framework Bank and investment firm resolution BRRD implementation and designation as NRA EU Bank Recovery and Resolution Directive (BRRD) Resolution

The below new definitions are inserted into the TOB at Annex 1, Part 1, definitions:

NOTICE SUPPLEMENTING CITI'S TERMS OF BUSINESS FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES IN RELATION TO THE BANK RECOVERY AND RESOLUTION DIRECTIVE Dear Client, We refer to Citi s Terms of Business

NOTICE SUPPLEMENTING CITI'S TERMS OF BUSINESS FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES IN RELATION TO THE BANK RECOVERY AND RESOLUTION DIRECTIVE Dear Client, We refer to Citi s Terms of Business

EUROPEAN CENTRAL BANK

26.4.2017 EN Official Journal of the European Union C 132/1 III (Preparatory acts) EUROPEAN CENTRAL BANK OPINION OF THE EUROPEAN CENTRAL BANK of 8 March 2017 on a proposal for a directive of the European

26.4.2017 EN Official Journal of the European Union C 132/1 III (Preparatory acts) EUROPEAN CENTRAL BANK OPINION OF THE EUROPEAN CENTRAL BANK of 8 March 2017 on a proposal for a directive of the European

Having regard to the Treaty on the Functioning of the European Union, and in particular Article 114 thereof,

L 345/96 Official Journal of the European Union 27.12.2017 DIRECTIVE (EU) 2017/2399 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 12 December 2017 amending Directive 2014/59/EU as regards the ranking

L 345/96 Official Journal of the European Union 27.12.2017 DIRECTIVE (EU) 2017/2399 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 12 December 2017 amending Directive 2014/59/EU as regards the ranking

EUROPEAN CENTRAL BANK

31.3.2011 Official Journal of the European Union C 99/1 I (Resolutions, recommendations and opinions) OPINIONS EUROPEAN CENTRAL BANK OPINION OF THE EUROPEAN CENTRAL BANK of 16 February 2011 on a proposal

31.3.2011 Official Journal of the European Union C 99/1 I (Resolutions, recommendations and opinions) OPINIONS EUROPEAN CENTRAL BANK OPINION OF THE EUROPEAN CENTRAL BANK of 16 February 2011 on a proposal

Introduction Post crisis Bank resolution principles with a focus on the BRRD in the EU

Introduction Post crisis Bank resolution principles with a focus on the BRRD in the EU Pamela Lintner Sr. Financial Sector Specialist Workshop on the role of the Judiciary in Bank resolution for Judges

Introduction Post crisis Bank resolution principles with a focus on the BRRD in the EU Pamela Lintner Sr. Financial Sector Specialist Workshop on the role of the Judiciary in Bank resolution for Judges

An EU Framework for Cross-Border Crisis Management in the Banking Sector

An EU Framework for Cross-Border Crisis Management in the Banking Sector Elisa Ferreira BUILDING A NEW FINANCIAL ARCHITECTURE Lisbon, 26-03-2010 Context Final total bill weighted too much on taxpayers,

An EU Framework for Cross-Border Crisis Management in the Banking Sector Elisa Ferreira BUILDING A NEW FINANCIAL ARCHITECTURE Lisbon, 26-03-2010 Context Final total bill weighted too much on taxpayers,

June 2018 The Bank of England s approach to setting a minimum requirement for own funds and eligible liabilities (MREL)

") June 2018 The Bank of England s approach to setting a minimum requirement for own funds and eligible liabilities (MREL) Statement of Policy (updating November 2016) June 2018 The Bank of England s approach

June 2018 The Bank of England s approach to setting a minimum requirement for own funds and eligible liabilities (MREL) Statement of Policy (updating November 2016) June 2018 The Bank of England s approach

DEPOSIT GUARANTEE SCHEMES Proposal for a Directive (recast)

") DEPOSIT GUARANTEE SCHEMES Proposal for a Directive (recast) BEUC position paper Contact: Financial Services Team financialservices@beuc.eu Ref.: X/083/2010-08/12/10 revised on 21/03/11 EC register for

DEPOSIT GUARANTEE SCHEMES Proposal for a Directive (recast) BEUC position paper Contact: Financial Services Team financialservices@beuc.eu Ref.: X/083/2010-08/12/10 revised on 21/03/11 EC register for

UK implementation of the EU Bank Recovery and Resolution Directive: What you need to know 1

UK implementation of the EU Bank Recovery and Resolution Directive: What you need to know 1 Briefing note January 2015 UK implementation of the EU Bank Recovery and Resolution Directive: What you need

UK implementation of the EU Bank Recovery and Resolution Directive: What you need to know 1 Briefing note January 2015 UK implementation of the EU Bank Recovery and Resolution Directive: What you need

ECB-PUBLIC OPINION OF THE EUROPEAN CENTRAL BANK. of 8 March 2017

EN ECB-PUBLIC OPINION OF THE EUROPEAN CENTRAL BANK of 8 March 2017 on a proposal for a directive of the European Parliament and of the Council on amending Directive 2014/59/EU as regards the ranking of

EN ECB-PUBLIC OPINION OF THE EUROPEAN CENTRAL BANK of 8 March 2017 on a proposal for a directive of the European Parliament and of the Council on amending Directive 2014/59/EU as regards the ranking of

Verso l Unione Bancaria Europea

Verso l Unione Bancaria Europea Ignazio Angeloni Conferenza in onore di Marco Onado Modena, 15 gennaio 2014 1 My idea of a bank before knowing Marco Onado 2 Twenty years later Narrow monetary union: one

Verso l Unione Bancaria Europea Ignazio Angeloni Conferenza in onore di Marco Onado Modena, 15 gennaio 2014 1 My idea of a bank before knowing Marco Onado 2 Twenty years later Narrow monetary union: one

DGG 1B EUROPEAN UNION. Brussels, 1 December 2017 (OR. en) 2016/0363 (COD) PE-CONS 57/17 EF 264 ECOFIN 907 DRS 64 CODEC 1744

2016/0363 (COD) PE-CONS 57/17 EF 264 ECOFIN 907 DRS 64 CODEC 1744") EUROPEAN UNION THE EUROPEAN PARLIAMT THE COUNCIL Brussels, 1 December 2017 (OR. en) 2016/0363 (COD) PE-CONS 57/17 EF 264 ECOFIN 907 DRS 64 CODEC 1744 LEGISLATIVE ACTS AND OTHER INSTRUMTS Subject: DIRECTIVE

EUROPEAN UNION THE EUROPEAN PARLIAMT THE COUNCIL Brussels, 1 December 2017 (OR. en) 2016/0363 (COD) PE-CONS 57/17 EF 264 ECOFIN 907 DRS 64 CODEC 1744 LEGISLATIVE ACTS AND OTHER INSTRUMTS Subject: DIRECTIVE

A EUROPEAN FRAMEWORK FOR A MORE RESILIENT BANKING SYSTEM

A EUROPEAN FRAMEWORK FOR A MORE RESILIENT BANKING SYSTEM 31 January 2013 Mario Nava European Commission Acting Director Financial institutionstions 14/11/2012 Disclaimer i The remarks in this presentation

A EUROPEAN FRAMEWORK FOR A MORE RESILIENT BANKING SYSTEM 31 January 2013 Mario Nava European Commission Acting Director Financial institutionstions 14/11/2012 Disclaimer i The remarks in this presentation

Bank resolution from a small host perspective

Bank resolution from a small host perspective The FinSAC experience in Emerging Europe Pamela Lintner World Bank FinSAC Workshop on Resolution Regimes in Europe Vienna, 19 April 2017 AGENDA Overview FinSAC

Bank resolution from a small host perspective The FinSAC experience in Emerging Europe Pamela Lintner World Bank FinSAC Workshop on Resolution Regimes in Europe Vienna, 19 April 2017 AGENDA Overview FinSAC

European Commission 27. July Estonian response to consultation document concerning deposit guarantee schemes

RAHANDUSMINISTEERIUM MINISTRY OF FINANCE OF ESTONIA European Commission markt-dgs-consultation@ec.europa.eu 27. July 2009 Estonian response to consultation document concerning deposit guarantee schemes

RAHANDUSMINISTEERIUM MINISTRY OF FINANCE OF ESTONIA European Commission markt-dgs-consultation@ec.europa.eu 27. July 2009 Estonian response to consultation document concerning deposit guarantee schemes

Strengthening the European banking system Overview of the CRDIV. World Bank CFRR IFRS Seminar for banking supervisors 18 April 2012, Zagreb

Strengthening the European banking system Overview of the CRDIV World Bank CFRR IFRS Seminar for banking supervisors 18 April 2012, Zagreb 1 Main Drivers Financial Stability and Sustainable Growth Unprecedented

Strengthening the European banking system Overview of the CRDIV World Bank CFRR IFRS Seminar for banking supervisors 18 April 2012, Zagreb 1 Main Drivers Financial Stability and Sustainable Growth Unprecedented

Delegations will find hereby the above mentioned Opinion of the European Central Bank.

Council of the European Union Brussels, 27 March 2017 (OR. en) Interinstitutional File: 2016/0363 (COD) 7735/17 COVER NOTE From: date of receipt: 27 March 2017 To: Subject: EF 63 ECOFIN 235 DRS 19 CODEC

Council of the European Union Brussels, 27 March 2017 (OR. en) Interinstitutional File: 2016/0363 (COD) 7735/17 COVER NOTE From: date of receipt: 27 March 2017 To: Subject: EF 63 ECOFIN 235 DRS 19 CODEC

SRB 2 nd Industry Dialogue January 12th, 2016

SRB 2 nd Industry Dialogue January 12th, 2016 SRB 2 nd Industry Dialogue SRB Approach to MREL in 2016 Dominique Laboureix, Member of the Board Key features of SRB's MREL policy in 2016 Banking groups require

SRB 2 nd Industry Dialogue January 12th, 2016 SRB 2 nd Industry Dialogue SRB Approach to MREL in 2016 Dominique Laboureix, Member of the Board Key features of SRB's MREL policy in 2016 Banking groups require

Guidelines on payment commitments under Directive 2014/49/EU on deposit guarantee schemes (EBA/GL/2015/09)

") Guidelines on payment commitments under Directive 2014/49/EU on deposit guarantee schemes (EBA/GL/2015/09) These guidelines are addressed to the deposit guarantee schemes and the bodies which administer

Guidelines on payment commitments under Directive 2014/49/EU on deposit guarantee schemes (EBA/GL/2015/09) These guidelines are addressed to the deposit guarantee schemes and the bodies which administer

Minimum Requirement for Own Funds and Eligible Liabilities (MREL) SRB Policy for 2017 and Next Steps. Published on 20 December 2017.

SRB Policy for 2017 and Next Steps. Published on 20 December 2017.") Minimum Requirement for Own Funds and Eligible Liabilities (MREL) SRB Policy for 2017 and Next Steps Published on 20 December 2017 Page 1 MREL Policy for 2017 and Next Steps Keywords: MREL, TLAC, SRB,

Minimum Requirement for Own Funds and Eligible Liabilities (MREL) SRB Policy for 2017 and Next Steps Published on 20 December 2017 Page 1 MREL Policy for 2017 and Next Steps Keywords: MREL, TLAC, SRB,

Council of the European Union Brussels, 27 November 2017 (OR. en)

") Conseil UE Council of the European Union Brussels, 27 November 2017 (OR. en) Interinstitutional File: 2016/0362 (COD) 14894/17 LIMITE PUBLIC EF 305 ECOFIN 1032 CODEC 1911 DRS 77 NOTE From: To: Subject:

Conseil UE Council of the European Union Brussels, 27 November 2017 (OR. en) Interinstitutional File: 2016/0362 (COD) 14894/17 LIMITE PUBLIC EF 305 ECOFIN 1032 CODEC 1911 DRS 77 NOTE From: To: Subject:

1. Resolution of banks and investment firms

C. Recovery and resolution During the year under review, the Bank s work on recovery and resolution mainly concerned resolution in the banking sector. While the European institutional framework remained

C. Recovery and resolution During the year under review, the Bank s work on recovery and resolution mainly concerned resolution in the banking sector. While the European institutional framework remained

Appendix 5 Certificate of Experience. Deposit Guarantee Scheme. Annual Report 2016

Appendix 5 Certificate of Experience 2016 Deposit Guarantee Scheme Annual Report 2016 Contents Overview... iii DGS Eligibility... iv Key Features of the Deposit Guarantee Scheme...v Key Activities in 2016...

Appendix 5 Certificate of Experience 2016 Deposit Guarantee Scheme Annual Report 2016 Contents Overview... iii DGS Eligibility... iv Key Features of the Deposit Guarantee Scheme...v Key Activities in 2016...

of which : Shortfall in the equity capital of majority owned financial entities which have not been consolidated

Basel III common disclosure March 31, 2018 Pillar 3 Table DF11 Composition of Capital Common Equity Tier 1 capital : instruments and reserves 1 Directly issued qualifying common share capital plus related

Basel III common disclosure March 31, 2018 Pillar 3 Table DF11 Composition of Capital Common Equity Tier 1 capital : instruments and reserves 1 Directly issued qualifying common share capital plus related

Chapter E: The US versus EU resolution regime

Chapter E: The US versus EU resolution regime 1. Introduction Resolution frameworks should always seek two objectives. First, resolving banks should be a quick process and must avoid negative spill over

Chapter E: The US versus EU resolution regime 1. Introduction Resolution frameworks should always seek two objectives. First, resolving banks should be a quick process and must avoid negative spill over

GUERNSEY FINANCIAL SERVICES COMMISSION ISLE OF MAN FINANCIAL SUPERVISION COMMISSION JERSEY FINANCIAL SERVICES COMMISSION

GUERNSEY FINANCIAL SERVICES COMMISSION ISLE OF MAN FINANCIAL SUPERVISION COMMISSION JERSEY FINANCIAL SERVICES COMMISSION DISCUSSION PAPER ON: BASEL III: CAPITAL ADEQUACY Issued: 17 December 2013 Glossary

GUERNSEY FINANCIAL SERVICES COMMISSION ISLE OF MAN FINANCIAL SUPERVISION COMMISSION JERSEY FINANCIAL SERVICES COMMISSION DISCUSSION PAPER ON: BASEL III: CAPITAL ADEQUACY Issued: 17 December 2013 Glossary

Conference on Nordic-Baltic financial linkages and challenges (IMF, Eesti Pank, Sveriges Riksbank)

") Mauro Grande European Central Bank Conference on Nordic-Baltic financial linkages and challenges (IMF, Eesti Pank, Sveriges Riksbank) Tallinn, Estonia 13 December 2013 EU regulatory reforms: some implications

Mauro Grande European Central Bank Conference on Nordic-Baltic financial linkages and challenges (IMF, Eesti Pank, Sveriges Riksbank) Tallinn, Estonia 13 December 2013 EU regulatory reforms: some implications

WORKING PAPER SERIES No 2016/16

WORKING PAPER SERIES No 2016/16 MINIMUM REQUIREMENTS FOR OWN FUNDS AND ELIGIBLE LIABILITIES (MREL): A COMPREHENSIVE ANALYSIS OF THE NEW PRUDENTIAL REQUIREMENT FOR CREDIT INSTITUTIONS by Ph.D. Candidate

WORKING PAPER SERIES No 2016/16 MINIMUM REQUIREMENTS FOR OWN FUNDS AND ELIGIBLE LIABILITIES (MREL): A COMPREHENSIVE ANALYSIS OF THE NEW PRUDENTIAL REQUIREMENT FOR CREDIT INSTITUTIONS by Ph.D. Candidate

Annexure 2 Table 2a Reconciliation between published financial statements and regulatory capital adequacy workings

Basel III regulatory reporting: The Central Bank of Oman has issued final guidelines on the implementation of the new capital norms as well as the Liquidity norms along with the phase in arrangements and

Basel III regulatory reporting: The Central Bank of Oman has issued final guidelines on the implementation of the new capital norms as well as the Liquidity norms along with the phase in arrangements and

CONSULTATION. Draft regulations transposing Directive 2014/49/EU on deposit guarantee schemes, and other ancillary rules [MFSA REF: 06/2015]

![CONSULTATION. Draft regulations transposing Directive 2014/49/EU on deposit guarantee schemes, and other ancillary rules [MFSA REF: 06/2015]](/thumbs/80/81926851.jpg "CONSULTATION. Draft regulations transposing Directive 2014/49/EU on deposit guarantee schemes, and other ancillary rules [MFSA REF: 06/2015]") Draft regulations transposing Directive 2014/49/EU on deposit guarantee schemes, and other ancillary rules [MFSA REF: 06/2015] 19 August 2015 Closing Date: 30 September 2015 Table of Contents Introduction...

Draft regulations transposing Directive 2014/49/EU on deposit guarantee schemes, and other ancillary rules [MFSA REF: 06/2015] 19 August 2015 Closing Date: 30 September 2015 Table of Contents Introduction...

APPLICATION OF THE MINIMUM REQUIREMENT FOR OWN FUNDS AND ELIGIBLE LIABILITIES (MREL) Bank Resolution and Recovery Directive 2014/59/EU

Bank Resolution and Recovery Directive 2014/59/EU") MEMORANDUM 14.2.2018 This memorandum was last updated on 14 February 2018, and it reflects the outlines set in the memorandum on MREL called "SRB Policy for 2017 and Next Steps" issued by the SRB on 20

MEMORANDUM 14.2.2018 This memorandum was last updated on 14 February 2018, and it reflects the outlines set in the memorandum on MREL called "SRB Policy for 2017 and Next Steps" issued by the SRB on 20

Positioning in respect of the European Commission s proposal for a recast Directive on Deposit Guarantee Schemes EBF final position.

EBF Ref.: D1325H-2010 Brussels, 12 October 2010 Set up in 1960, the European Banking Federation is the voice of the European banking sector (European Union & European Free Trade Association countries).

EBF Ref.: D1325H-2010 Brussels, 12 October 2010 Set up in 1960, the European Banking Federation is the voice of the European banking sector (European Union & European Free Trade Association countries).

Draft Technical Standards on criteria for MREL. 19 January 2015

Draft Technical Standards on criteria for MREL 19 January 2015 Contents 1. Context 2. Main features of draft Technical Standards 3. MREL and TLAC 4. Next steps 5. Questions? 1. Context: BRRD requirements

Draft Technical Standards on criteria for MREL 19 January 2015 Contents 1. Context 2. Main features of draft Technical Standards 3. MREL and TLAC 4. Next steps 5. Questions? 1. Context: BRRD requirements

Setting of MREL for subsidiaries of foreign banks

Setting of MREL for subsidiaries of foreign banks Emil Vonvea, Director, Bank Resolution Department National Bank of Romania FINSAC WORKSHOP ON BAIL-IN AND MREL, Vienna 13 th December, 2016 The opinions

Setting of MREL for subsidiaries of foreign banks Emil Vonvea, Director, Bank Resolution Department National Bank of Romania FINSAC WORKSHOP ON BAIL-IN AND MREL, Vienna 13 th December, 2016 The opinions

Submission of The Hong Kong Association of Banks in response to. the Financial Stability Board s 10 November 2014 Consultation Document on

Submission of The Hong Kong Association of Banks in response to the Financial Stability Board s 10 November 2014 Consultation Document on Introduction Adequacy of loss-absorbing capital of global systemically

Submission of The Hong Kong Association of Banks in response to the Financial Stability Board s 10 November 2014 Consultation Document on Introduction Adequacy of loss-absorbing capital of global systemically

Final Guidelines. on the treatment of shareholders in bail-in or the write-down and conversion of capital instruments EBA/GL/2017/04 11/07/2017

GUIDELINES ON THE TREATMENT OF SHAREHOLDERS EBA/GL/2017/04 11/07/2017 Final Guidelines on the treatment of shareholders in bail-in or the write-down and conversion of capital instruments 1. Compliance

GUIDELINES ON THE TREATMENT OF SHAREHOLDERS EBA/GL/2017/04 11/07/2017 Final Guidelines on the treatment of shareholders in bail-in or the write-down and conversion of capital instruments 1. Compliance

Hearing with Mrs Elke König, Chair of the Single Resolution Board

IPOL EGOV DIRECTORATE-GENERAL FOR INTERNAL POLICIES ECONOMIC GOVERNANCE SUPPORT UNIT B R IE F IN G Hearing with Mrs Elke König, Chair of the Single Resolution Board ECON, 28 January 2016 The Single Resolution

IPOL EGOV DIRECTORATE-GENERAL FOR INTERNAL POLICIES ECONOMIC GOVERNANCE SUPPORT UNIT B R IE F IN G Hearing with Mrs Elke König, Chair of the Single Resolution Board ECON, 28 January 2016 The Single Resolution

New package of banking reforms

REGULATION New package of banking reforms Regulation & Public Policies The European Commission has presented today a new legislative package aimed at amending both the current banking prudential and resolution

REGULATION New package of banking reforms Regulation & Public Policies The European Commission has presented today a new legislative package aimed at amending both the current banking prudential and resolution

Disclosure of UniCredit Bank Austria AG as of 30 September 2018

Bank Austria Disclosure Report as of 30 September 2018 pursuant to Part 8 of the Capital Requirements Regulation (CRR) / Disclosure by Institutions (Pillar 3) Disclosure of UniCredit Bank Austria AG as

Bank Austria Disclosure Report as of 30 September 2018 pursuant to Part 8 of the Capital Requirements Regulation (CRR) / Disclosure by Institutions (Pillar 3) Disclosure of UniCredit Bank Austria AG as

Introduction. Regulatory environment in Legal Context

P. 15 Introduction Regulatory environment in 2017 Legal Context As a Spanish credit institution, BBVA is subject to Directive 2013/36/EU of the European Parliament and of the Council dated June 26, 2013,

P. 15 Introduction Regulatory environment in 2017 Legal Context As a Spanish credit institution, BBVA is subject to Directive 2013/36/EU of the European Parliament and of the Council dated June 26, 2013,

Pillar 3 Disclosures (OCBC Group As at 30 June 2018)

") Oversea-Chinese Banking Corporation Limited Pillar 3 Disclosures (OCBC Group As at 30 June 2018) Incorporated in Singapore Company Registration Number: 193200032W Table of Contents 1. Introduction... 3

Oversea-Chinese Banking Corporation Limited Pillar 3 Disclosures (OCBC Group As at 30 June 2018) Incorporated in Singapore Company Registration Number: 193200032W Table of Contents 1. Introduction... 3

***I REPORT. EN United in diversity EN. European Parliament A8-0216/

European Parliament 2014-2019 Plenary sitting A8-0216/2018 25.6.2018 ***I REPORT on the proposal for a regulation of the European Parliament and of the Council amending Regulation (EU) No 806/2014 as regards

European Parliament 2014-2019 Plenary sitting A8-0216/2018 25.6.2018 ***I REPORT on the proposal for a regulation of the European Parliament and of the Council amending Regulation (EU) No 806/2014 as regards

Sr. No. 1 Issuer Axis Bank Ltd. 2 Unique identifier ISIN: INE238A01026

XIII. MAIN FEATURES OF REGULATORY CAPITAL AS ON 8 th NOVEMBER 2018 The main features of equity capital are given below: Particulars Equity 1 Issuer Axis Bank Ltd. 2 Unique identifier ISIN: INE238A01026

XIII. MAIN FEATURES OF REGULATORY CAPITAL AS ON 8 th NOVEMBER 2018 The main features of equity capital are given below: Particulars Equity 1 Issuer Axis Bank Ltd. 2 Unique identifier ISIN: INE238A01026

The Special Resolution Regime. Mark Adams & Miles Bake Special Resolution Unit, Bank of England 30 June 2010

The Special Resolution Regime Mark Adams & Miles Bake Special Resolution Unit, Bank of England 3 June 21 1 Why a Special Resolution Regime? General insolvency law is inadequate for dealing with failing

The Special Resolution Regime Mark Adams & Miles Bake Special Resolution Unit, Bank of England 3 June 21 1 Why a Special Resolution Regime? General insolvency law is inadequate for dealing with failing

Table DF - 11 : Composition of Capital as of September 30, 2016

Table DF 11 : Composition of Capital as of September 30, 2016 Basel III common disclosure template to be used during the transition of regulatory adjustments Amounts Subject to PreBasel III Treatment (Rs.

Table DF 11 : Composition of Capital as of September 30, 2016 Basel III common disclosure template to be used during the transition of regulatory adjustments Amounts Subject to PreBasel III Treatment (Rs.

Treating the E.U. as a Single Jurisdiction for the Implementation of TLAC (EBA Report on MREL, December 2016)

") Treating the E.U. as a Single Jurisdiction for the Implementation of TLAC (EBA Report on MREL, December 2016) 2 nd Annual Bank Structuring and Resolvability London, 20-21/02/2017 David BLACHE Deputy Director

Treating the E.U. as a Single Jurisdiction for the Implementation of TLAC (EBA Report on MREL, December 2016) 2 nd Annual Bank Structuring and Resolvability London, 20-21/02/2017 David BLACHE Deputy Director

May Guidelines on LCR Calculation for the Interim Observation Period

May 2014 Guidelines on LCR Calculation for the Interim Observation Period Contents 1 Overview... 3 2 Context... 4 3 Liquidity Coverage Ratio... 7 4 Definition of High Quality Liquid Assets ( HQLA )...

May 2014 Guidelines on LCR Calculation for the Interim Observation Period Contents 1 Overview... 3 2 Context... 4 3 Liquidity Coverage Ratio... 7 4 Definition of High Quality Liquid Assets ( HQLA )...

EC Consultation Document Review of Directive 94/19/EC on Deposit-Guarantee Schemes (DGS)

") EC-consultation-review of Directive(2)-060709 (3)ENG.docx version 24/07/2009 EC Consultation Document Review of Directive 94/19/EC on Deposit-Guarantee Schemes (DGS) BHB 3 Executive summary In this preliminary

EC-consultation-review of Directive(2)-060709 (3)ENG.docx version 24/07/2009 EC Consultation Document Review of Directive 94/19/EC on Deposit-Guarantee Schemes (DGS) BHB 3 Executive summary In this preliminary

Definitions and guidance in the SRB 2016 Contributions Reporting Form reporting form prevail over the information in the slides

2016 ex-ante contributions to the SRF Additional guidance for the industry 30 November 2015 Definitions and guidance in the SRB 2016 Contributions Reporting Form reporting form prevail over the information

2016 ex-ante contributions to the SRF Additional guidance for the industry 30 November 2015 Definitions and guidance in the SRB 2016 Contributions Reporting Form reporting form prevail over the information

7 TH SRB BANKING INDUSTRY DIALOGUE MEETING SINGLE RESOLUTION FUND

7 TH SRB BANKING INDUSTRY DIALOGUE MEETING SINGLE RESOLUTION FUND Presenter: Timo Löyttyniemi Brussels, AGENDA 1. UPDATE ON EX-ANTE CONTRIBUTIONS TO THE SRF 2. UPDATE ON CONTRIBUTIONS TO THE ADMINISTRATIVE

7 TH SRB BANKING INDUSTRY DIALOGUE MEETING SINGLE RESOLUTION FUND Presenter: Timo Löyttyniemi Brussels, AGENDA 1. UPDATE ON EX-ANTE CONTRIBUTIONS TO THE SRF 2. UPDATE ON CONTRIBUTIONS TO THE ADMINISTRATIVE

Disclosure Report in accordance with the EU Capital Requirements Regulation (CRR)

") Disclosure Report in accordance with the EU Capital Requirements Regulation (CRR) as at 31 December 2014 2 Disclosure Report 2014 1 Preamble 3 2 Capital Structure and Adequacy 5 2.1 Capital Structure 6

Disclosure Report in accordance with the EU Capital Requirements Regulation (CRR) as at 31 December 2014 2 Disclosure Report 2014 1 Preamble 3 2 Capital Structure and Adequacy 5 2.1 Capital Structure 6

Policy Rules for the Deposit Guarantee Scheme

Policy Rules for the Deposit Guarantee Scheme July 2017 This translation is made available by DNB. No rights can be derived from this English version. The Dutch version that has been published in the Staatscourant

Policy Rules for the Deposit Guarantee Scheme July 2017 This translation is made available by DNB. No rights can be derived from this English version. The Dutch version that has been published in the Staatscourant

Official Journal of the European Union. (Non-legislative acts) REGULATIONS

REGULATIONS") 3.9.2016 L 237/1 II (Non-legislative acts) REGULATIONS COMMISSION DELEGATED REGULATION (EU) 2016/1450 of 23 May 2016 supplementing Directive 2014/59/EU of the European Parliament and of the Council with

3.9.2016 L 237/1 II (Non-legislative acts) REGULATIONS COMMISSION DELEGATED REGULATION (EU) 2016/1450 of 23 May 2016 supplementing Directive 2014/59/EU of the European Parliament and of the Council with

Consultation Paper. Draft Guidelines On the treatment of shareholders in bail-in or the write-down and conversion of capital instruments

11 November 2014 EBA/CP/2014/40 Consultation Paper Draft Guidelines On the treatment of shareholders in bail-in or the write-down and conversion of capital instruments Contents 1. Responding to this Consultation

11 November 2014 EBA/CP/2014/40 Consultation Paper Draft Guidelines On the treatment of shareholders in bail-in or the write-down and conversion of capital instruments Contents 1. Responding to this Consultation

11 July EBA Standardised templates for Additional Tier 1 instruments - DRAFT

11 July 2016 EBA Standardised templates for Additional Tier 1 instruments - DRAFT 1 Reasons for publication 1. Pursuant to Article 80 of Regulation (EU) No 575/2013 (Capital Requirements Regulation CRR)

11 July 2016 EBA Standardised templates for Additional Tier 1 instruments - DRAFT 1 Reasons for publication 1. Pursuant to Article 80 of Regulation (EU) No 575/2013 (Capital Requirements Regulation CRR)

In response to the current consultation, the NVB asks the Commission to take note of the following points:

European Commission Directorate-General Internal Market, Unit H1 Rue de Spa 2 B-1049 Brussels markt-dgs-consultation@ec.europa.eu Date: 27 July 2009 Reference: BR-970 Subject: NVB response to the Commission

European Commission Directorate-General Internal Market, Unit H1 Rue de Spa 2 B-1049 Brussels markt-dgs-consultation@ec.europa.eu Date: 27 July 2009 Reference: BR-970 Subject: NVB response to the Commission

Banking Resolution Spanish experience. Future implications of BRRD.

Banking Resolution Spanish experience. Future implications of BRRD. FinSAC workshop on Recovery and Resolution Planning 24 April Mario Delgado EY; Partner, Risk & Regulation Banking resolution Spanish

Banking Resolution Spanish experience. Future implications of BRRD. FinSAC workshop on Recovery and Resolution Planning 24 April Mario Delgado EY; Partner, Risk & Regulation Banking resolution Spanish

Pillar 3, Liquidity Coverage Ratio ("LCR") and Net Stable Funding Ratio ("NSFR") Disclosures

and Net Stable Funding Ratio (NSFR) Disclosures") Pillar 3, Liquidity Coverage Ratio ("LCR") and Net Stable Funding Ratio ("NSFR") Disclosures Second Quarter 2018 DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number:

Pillar 3, Liquidity Coverage Ratio ("LCR") and Net Stable Funding Ratio ("NSFR") Disclosures Second Quarter 2018 DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number:

Council of the European Union Brussels, 6 March 2018 (OR. en)

") Conseil UE Council of the European Union Brussels, 6 March 2018 (OR. en) Interinstitutional File: 2016/0362 (COD) 6616/18 LIMITE PUBLIC EF 57 ECOFIN 187 DRS 8 CODEC 273 NOTE From: To: Subject: Presidency

Conseil UE Council of the European Union Brussels, 6 March 2018 (OR. en) Interinstitutional File: 2016/0362 (COD) 6616/18 LIMITE PUBLIC EF 57 ECOFIN 187 DRS 8 CODEC 273 NOTE From: To: Subject: Presidency

Final Guidelines. on the treatment of shareholders in bail-in or the write-down and conversion of capital instruments. EBA/GL/2017/04 05 April 2017

GUIDELINES ON THE TREATMENT OF SHAREHOLDERS EBA/GL/2017/04 05 April 2017 Final Guidelines on the treatment of shareholders in bail-in or the write-down and conversion of capital instruments Contents 1.

GUIDELINES ON THE TREATMENT OF SHAREHOLDERS EBA/GL/2017/04 05 April 2017 Final Guidelines on the treatment of shareholders in bail-in or the write-down and conversion of capital instruments Contents 1.

BRFkredit a/s ANNEX I Balance Sheet Reconciliation Methodology Disclosure according to article 437 of the Capital Requirements Regulation

BRFkredit a/s ANNEX I Balance Sheet Reconciliation Methodology Disclosure according to article 437 of the Capital Requirements Regulation Capital base 31.12.2015 DKKm Shareholders' equity according to

BRFkredit a/s ANNEX I Balance Sheet Reconciliation Methodology Disclosure according to article 437 of the Capital Requirements Regulation Capital base 31.12.2015 DKKm Shareholders' equity according to

Overview of the post-consultation revisions to the TLAC Principles and Term Sheet

9 November 2015 Overview of the post-consultation revisions to the TLAC Principles and Term Sheet On 10 November 2014, the FSB published a consultative document with policy proposals developed at the request

9 November 2015 Overview of the post-consultation revisions to the TLAC Principles and Term Sheet On 10 November 2014, the FSB published a consultative document with policy proposals developed at the request

***I DRAFT REPORT. EN United in diversity EN. European Parliament 2016/0363(COD)

") European Parliament 2014-2019 Committee on Economic and Monetary Affairs 2016/0363(COD) 4.7.2017 ***I DRAFT REPORT on the proposal for a directive of the European Parliament and of the Council on amending

European Parliament 2014-2019 Committee on Economic and Monetary Affairs 2016/0363(COD) 4.7.2017 ***I DRAFT REPORT on the proposal for a directive of the European Parliament and of the Council on amending

The Bank of England s approach to setting a minimum requirement for own funds and eligible liabilities (MREL)

") November 2016 The Bank of England s approach to setting a minimum requirement for own funds and eligible liabilities (MREL) Responses to Consultation and Statement of Policy November 2016 The Bank of

November 2016 The Bank of England s approach to setting a minimum requirement for own funds and eligible liabilities (MREL) Responses to Consultation and Statement of Policy November 2016 The Bank of

EUROPEAN COMMISSION. Brussels, COM(2010) 579 final

579 final") EN EN EN EUROPEAN COMMISSION Brussels, 20.10.2010 COM(2010) 579 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE, THE COMMITTEE

EN EN EN EUROPEAN COMMISSION Brussels, 20.10.2010 COM(2010) 579 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE, THE COMMITTEE

Consultation Paper CP41/16 Deposit protection limit

Consultation Paper CP41/16 Deposit protection limit November 2016 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority, registered office: 8 Lothbury, London EC2R

Consultation Paper CP41/16 Deposit protection limit November 2016 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority, registered office: 8 Lothbury, London EC2R

Delegations will find below a revised Presidency compromise text on the abovementioned proposal.

Council of the European Union Brussels, 29 November 2017 (OR. en) Interinstitutional File: 2016/0361 (COD) 14895/1/17 REV 1 EF 306 ECOFIN 1033 CODEC 1912 NOTE From: To: Subject: Presidency Delegations

Council of the European Union Brussels, 29 November 2017 (OR. en) Interinstitutional File: 2016/0361 (COD) 14895/1/17 REV 1 EF 306 ECOFIN 1033 CODEC 1912 NOTE From: To: Subject: Presidency Delegations

Standard Chartered Bank (Singapore) Limited Registration Number: C. Pillar 3 Disclosures as at 31 December 2017

Limited Registration Number: C. Pillar 3 Disclosures as at 31 December 2017") Standard Chartered Bank (Singapore) Limited Registration Number: 201224747C Pillar 3 Disclosures as at 31 December 2017 1 Contents 1. Capital Adequacy and Leverage Ratio... 2 2. Overview of RWA... 3 3.

Standard Chartered Bank (Singapore) Limited Registration Number: 201224747C Pillar 3 Disclosures as at 31 December 2017 1 Contents 1. Capital Adequacy and Leverage Ratio... 2 2. Overview of RWA... 3 3.

After the global financial crisis: challenges for the EU Banking System

After the global financial crisis: challenges for the EU Banking System Conference on «The Changing Environment and Deposit Insurers» Session 1 Tokyo, 16 February 2017 Giuseppe Boccuzzi Agenda 1 2 3 4

After the global financial crisis: challenges for the EU Banking System Conference on «The Changing Environment and Deposit Insurers» Session 1 Tokyo, 16 February 2017 Giuseppe Boccuzzi Agenda 1 2 3 4

Ahli United Bank B.S.C. Pillar III Disclosures - Basel III. 30 June 2018

] Six month ended (Unaudited) Table 1 Capital structure. 2 Table 2 Gross credit risk exposures.. 3 Table 3 Risk weighted exposures. 4 Table 4 Geographic distribution of gross credit exposures 5 Table 5

] Six month ended (Unaudited) Table 1 Capital structure. 2 Table 2 Gross credit risk exposures.. 3 Table 3 Risk weighted exposures. 4 Table 4 Geographic distribution of gross credit exposures 5 Table 5

THE SINGLE RESOLUTION FUND

THE SINGLE RESOLUTION FUND THE SINGLE RESOLUTION FUND (SRF) : ensures uniform practice in the financing of resolutions within the Single Resolution Mechanism (SRM); pools contributions raised at national

THE SINGLE RESOLUTION FUND THE SINGLE RESOLUTION FUND (SRF) : ensures uniform practice in the financing of resolutions within the Single Resolution Mechanism (SRM); pools contributions raised at national

PRA RULEBOOK: CRR FIRMS, NON CRR FIRMS AND NON AUTHORISED PERSONS: DEPOSITOR PROTECTION (AMENDMENT No. 3) INSTRUMENT 2015

INSTRUMENT 2015") PRA RULEBOOK: CRR FIRMS, NON CRR FIRMS AND NON AUTHORISED PERSONS: DEPOSITOR PROTECTION (AMENDMENT No. 3) INSTRUMENT 2015 Powers exercised A. The Prudential Regulation Authority ( PRA ) makes this instrument

PRA RULEBOOK: CRR FIRMS, NON CRR FIRMS AND NON AUTHORISED PERSONS: DEPOSITOR PROTECTION (AMENDMENT No. 3) INSTRUMENT 2015 Powers exercised A. The Prudential Regulation Authority ( PRA ) makes this instrument

2 Retained earnings 13,598 b+c+d+e 3 Accumulated other comprehensive income (and other reserves) -

-") DF 11 Composition of Capital as at March 31, 2015 Common Equity Tier 1 capital: instruments and reserves 1 Directly issued qualifying common share capital plus related stock surplus (share premium) Amounts

DF 11 Composition of Capital as at March 31, 2015 Common Equity Tier 1 capital: instruments and reserves 1 Directly issued qualifying common share capital plus related stock surplus (share premium) Amounts

Deutsche Bank. Pillar 3 Report as of March 31, 2018

Pillar 3 Report as of March 31, 2018 Content 3 Regulatory Framework 3 Introduction 3 Basel 3 and CRR/ CRD 4 6 Capital requirements 6 Article 438 (c-f) CRR Overview of capital requirements 7 Credit risk

Pillar 3 Report as of March 31, 2018 Content 3 Regulatory Framework 3 Introduction 3 Basel 3 and CRR/ CRD 4 6 Capital requirements 6 Article 438 (c-f) CRR Overview of capital requirements 7 Credit risk

ANNEX I. REPORTING ON FUNDING PLANS Table of Contents

ANNEX I REPORTING ON FUNDING PLANS Table of Contents PART I: GENERAL INSTRUCTIONS... 3 1. Structure and conventions... 3 1.1. Structure... 3 1.2. Numbering convention... 3 1.3. Sign convention... 3 PART

ANNEX I REPORTING ON FUNDING PLANS Table of Contents PART I: GENERAL INSTRUCTIONS... 3 1. Structure and conventions... 3 1.1. Structure... 3 1.2. Numbering convention... 3 1.3. Sign convention... 3 PART

The FSA's Approach to Introduce the TLAC Framework

(Provisional Translation) First version published: April 15, 2016 Second version published: April 13, 2018 Financial Services Agency The FSA's Approach to Introduce the TLAC Framework Based on the experience

(Provisional Translation) First version published: April 15, 2016 Second version published: April 13, 2018 Financial Services Agency The FSA's Approach to Introduce the TLAC Framework Based on the experience

Financial instruments - Commission guidance notes. Commission guidance Lisbon, 18 January 2016

Financial instruments - Commission guidance notes Commission guidance Lisbon, 18 January 2016 Guidance notes complementary to short guidance covering all issues relevant to MA/fund managers developed systematically

Financial instruments - Commission guidance notes Commission guidance Lisbon, 18 January 2016 Guidance notes complementary to short guidance covering all issues relevant to MA/fund managers developed systematically

Feedback statement July 2016

Feedback statement Response to the public consultation on the approach for the recognition of institutional protection schemes (IPS) for prudential purposes July 2016 Contents This document is divided

Feedback statement Response to the public consultation on the approach for the recognition of institutional protection schemes (IPS) for prudential purposes July 2016 Contents This document is divided